IS Strategy, Management, and Acquisition Report - Standard Chartered

VerifiedAdded on 2019/11/26

|12

|4084

|226

Report

AI Summary

This report provides a comprehensive analysis of Information System (IS) strategy, management, and acquisition within Standard Chartered Bank. It begins with an introduction highlighting the use of information systems to gain a competitive advantage in the banking industry, focusing on the bank's value chain structure. The report then delves into IS strategy and IT management structures, emphasizing the importance of aligning business approaches with information systems to achieve strategic objectives. It examines the nature of Standard Chartered Bank's business, detailing its various financial services, customer interactions, and operational processes. The governance structures, including the Board of Directors and its committees, are explored, along with the business processes and policies that guide the bank's operations. The report also addresses regulatory requirements, risk mitigation strategies, and potential areas for improvement within the bank's IS framework. The conclusion summarizes the key findings and implications of the analysis, offering a holistic view of the bank's IS strategy.

Running head: IS Strategy, Management and Acquisition 1

IS Strategy, Management and Acquisition

Name

Institution affiliation

IS Strategy, Management and Acquisition

Name

Institution affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: IS Strategy, Management and Acquisition 2

Table of Contents

Introduction......................................................................................................................................3

IS Strategy and IT Management Structures.....................................................................................3

Nature of the Business.....................................................................................................................3

Governance Structures, Processes, and Policies..............................................................................4

Governance Structure......................................................................................................................4

Business Processes...........................................................................................................................6

Policies.............................................................................................................................................7

Regulatory Requirements................................................................................................................8

Mitigating Risk................................................................................................................................8

Possible Improvements....................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

IS Strategy and IT Management Structures.....................................................................................3

Nature of the Business.....................................................................................................................3

Governance Structures, Processes, and Policies..............................................................................4

Governance Structure......................................................................................................................4

Business Processes...........................................................................................................................6

Policies.............................................................................................................................................7

Regulatory Requirements................................................................................................................8

Mitigating Risk................................................................................................................................8

Possible Improvements....................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Running head: IS Strategy, Management and Acquisition 3

Introduction

Information systems can be utilized to gain competitive advantage at the industry level by

engaging with other companies to make standards for sharing business transactions electronically

or sharing of information which will market actors to implement same standards.

I identified Standard chartered bank as my case study and realized that the company uses a value

chain structure in determining areas where information systems can be used to improve banking

processes.

IS Strategy and IT Management Structures

The data needed to support business approach and the establishment of data systems appropriate

to supplying such information requires to be planned and implemented with each other. This

positioning of business approach with information system yields information systems strategy. It

is a constant process that enhance the information system support design to progressively remain

significant for any business strategic aims and objectives. (Deutch & Milo, 2012).

Standard chartered bank has a cogent approach for information system, that deliver information

that is of high strategic value. All the systems and technology in the organization are conformed

to a larger strategic vision therefore enhancing performance in a synchronized manner.

Compatibility is the rule rather than the exclusion. As such business objectives and goals are

largely impacted by such information system strategies. Opportunities are grasped. The bank

possesses an information system that has a calculated focus. It is closely lined up with business

approach and is driven by business requirements rather than technological prospects. It is joined

with the organizational approach to hand over information that assist the management to outrival

competition and thereby using information system as a device for competitive benefits.

Information system therefore, delivers anticipated awareness into business issues. (Draheim,

2010).

Nature of the Business

Standard chartered bank is a system that offers cash management assistance for clients, recording

the execution of their accounts and portfolios of the day, exchange goods and services with

financial and bank's financial equipment, provide change of currency and distribute distinct type

of capital. It provides various expertness and opportunities to their clients. It offers security of

money and commodities and offer credit, loans, and payment aid, like inquiring on money

orders, accounts, and cashier's checks. It also provides insurance and investment goods. The

following are some of the activities that standard chartered bank undertakes;

Receiving deposits and granting loans as financial equipment – apart from receiving deposits and

giving loans, the bank offers transaction accounts. Accounts are normally opened for small and

medium customers, the retail clients, and for the enterprise clients. Funds deposited by the

deponents in the bank is used for distribution and generation of financial instruments and other

loan. This institution offers and possess liquidity supportable flow for financial and non-financial

organizations.

Introduction

Information systems can be utilized to gain competitive advantage at the industry level by

engaging with other companies to make standards for sharing business transactions electronically

or sharing of information which will market actors to implement same standards.

I identified Standard chartered bank as my case study and realized that the company uses a value

chain structure in determining areas where information systems can be used to improve banking

processes.

IS Strategy and IT Management Structures

The data needed to support business approach and the establishment of data systems appropriate

to supplying such information requires to be planned and implemented with each other. This

positioning of business approach with information system yields information systems strategy. It

is a constant process that enhance the information system support design to progressively remain

significant for any business strategic aims and objectives. (Deutch & Milo, 2012).

Standard chartered bank has a cogent approach for information system, that deliver information

that is of high strategic value. All the systems and technology in the organization are conformed

to a larger strategic vision therefore enhancing performance in a synchronized manner.

Compatibility is the rule rather than the exclusion. As such business objectives and goals are

largely impacted by such information system strategies. Opportunities are grasped. The bank

possesses an information system that has a calculated focus. It is closely lined up with business

approach and is driven by business requirements rather than technological prospects. It is joined

with the organizational approach to hand over information that assist the management to outrival

competition and thereby using information system as a device for competitive benefits.

Information system therefore, delivers anticipated awareness into business issues. (Draheim,

2010).

Nature of the Business

Standard chartered bank is a system that offers cash management assistance for clients, recording

the execution of their accounts and portfolios of the day, exchange goods and services with

financial and bank's financial equipment, provide change of currency and distribute distinct type

of capital. It provides various expertness and opportunities to their clients. It offers security of

money and commodities and offer credit, loans, and payment aid, like inquiring on money

orders, accounts, and cashier's checks. It also provides insurance and investment goods. The

following are some of the activities that standard chartered bank undertakes;

Receiving deposits and granting loans as financial equipment – apart from receiving deposits and

giving loans, the bank offers transaction accounts. Accounts are normally opened for small and

medium customers, the retail clients, and for the enterprise clients. Funds deposited by the

deponents in the bank is used for distribution and generation of financial instruments and other

loan. This institution offers and possess liquidity supportable flow for financial and non-financial

organizations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: IS Strategy, Management and Acquisition 4

The banks are dealing with humans- the major participants in the standard chartered bank

include: non-financial organizations, retail divisions, other banks, small and medium firms,

conglomerate companies, big companies, insurance firms, multinational companies, security,

international companies, among others. The upholder of each mentioned organization is a

person. Human beings are the connection to all financial projects.

Different types of clients, manners and behaviors- the bank handles different customer behavior,

personality, cultures and manners. This is because clients possess different tastes, opportunities,

social traits, financial might, egos, among others. As such the bank differentiate its’ client and

position them accordance to the requirements and interest. The bank therefore provides its’

goods and services in accordance to the position given. (Weske, 2007).

Different culture and religion- Clients view their world based on their cultural belief. Believes,

culture, values and religion aim act as highway to particular behavior direction and culture. As

such the bank grants freedom to its client for the choice of the preferred good and services that

will meet their needs.

Unlimited wants with limited resources by its customer- resources become scarce due to

individuals’ ability and competence to make money and have enough for the particular

limitation. Inadequacy guide client on use of funds wisely to meet their needs and forego their

wants.

Generation of profit through client operations and provision of different services- standard

chartered bank act as intermediary in receiving deposits and channeling those deposits into

lending operations, either through loans or capital markets. It links clients with capital shortage

with those with surplus capital. It acts as disbursement agents by analyzing present accounts for

clients, handing over checks withdrawn by clients on the bank, and gathering checks lend to

clients' present accounts. It also enhances client payments through other payment ways like the

automated clearing house, EFTPOS, telegraphic transfer, and automated teller machine. The

bank take money for temporary use through issuance of debt securities like bonds, acceptance of

deposited funds on present accounts, term deposit. However, it lends money through production

of advances to clients on present accounts, and installment. Some of the channel the bank uses

for allocation are: internet banking, Automated Teller Machines, offices, video banking, call

center, telephone banking, mail, relationship managers, mobile banking, agents, sales forces,

among others. (Brotby, 2008).

Governance Structures, Processes, and Policies

Governance Structure

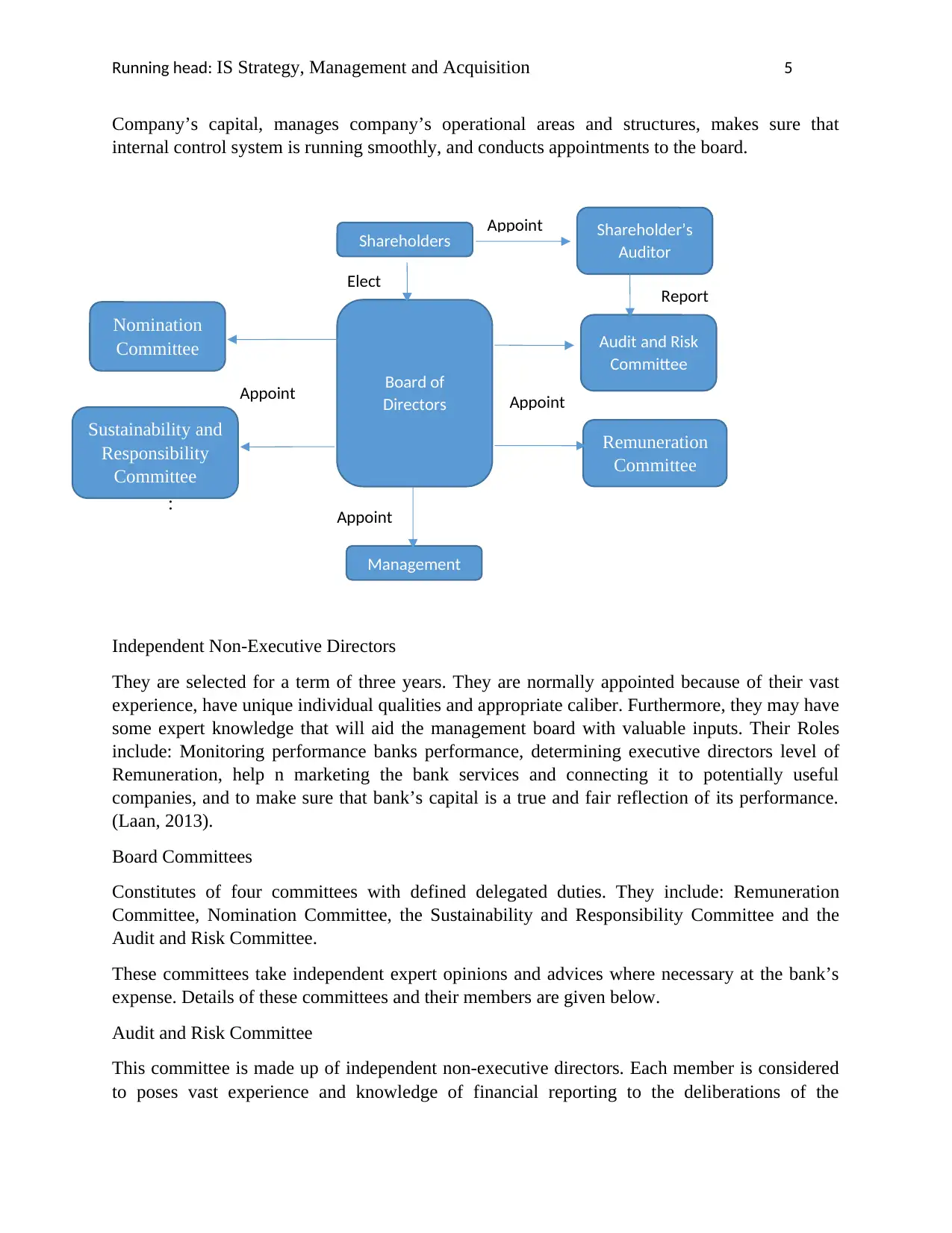

The Board of Directors

It is composed of the chairman, four executive directors, and ten independent non-executive

directors whose role is to see the flourishment of the company. Shareholder has to conduct and

election to appoint their directors. Their roles and responsibilities include; It’s the mandate of the

board to review and determine the strategy of the company, overseeing the compliance of the

Group with regulatory and statutory commitment, handling of concerns pertaining to the

The banks are dealing with humans- the major participants in the standard chartered bank

include: non-financial organizations, retail divisions, other banks, small and medium firms,

conglomerate companies, big companies, insurance firms, multinational companies, security,

international companies, among others. The upholder of each mentioned organization is a

person. Human beings are the connection to all financial projects.

Different types of clients, manners and behaviors- the bank handles different customer behavior,

personality, cultures and manners. This is because clients possess different tastes, opportunities,

social traits, financial might, egos, among others. As such the bank differentiate its’ client and

position them accordance to the requirements and interest. The bank therefore provides its’

goods and services in accordance to the position given. (Weske, 2007).

Different culture and religion- Clients view their world based on their cultural belief. Believes,

culture, values and religion aim act as highway to particular behavior direction and culture. As

such the bank grants freedom to its client for the choice of the preferred good and services that

will meet their needs.

Unlimited wants with limited resources by its customer- resources become scarce due to

individuals’ ability and competence to make money and have enough for the particular

limitation. Inadequacy guide client on use of funds wisely to meet their needs and forego their

wants.

Generation of profit through client operations and provision of different services- standard

chartered bank act as intermediary in receiving deposits and channeling those deposits into

lending operations, either through loans or capital markets. It links clients with capital shortage

with those with surplus capital. It acts as disbursement agents by analyzing present accounts for

clients, handing over checks withdrawn by clients on the bank, and gathering checks lend to

clients' present accounts. It also enhances client payments through other payment ways like the

automated clearing house, EFTPOS, telegraphic transfer, and automated teller machine. The

bank take money for temporary use through issuance of debt securities like bonds, acceptance of

deposited funds on present accounts, term deposit. However, it lends money through production

of advances to clients on present accounts, and installment. Some of the channel the bank uses

for allocation are: internet banking, Automated Teller Machines, offices, video banking, call

center, telephone banking, mail, relationship managers, mobile banking, agents, sales forces,

among others. (Brotby, 2008).

Governance Structures, Processes, and Policies

Governance Structure

The Board of Directors

It is composed of the chairman, four executive directors, and ten independent non-executive

directors whose role is to see the flourishment of the company. Shareholder has to conduct and

election to appoint their directors. Their roles and responsibilities include; It’s the mandate of the

board to review and determine the strategy of the company, overseeing the compliance of the

Group with regulatory and statutory commitment, handling of concerns pertaining to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: IS Strategy, Management and Acquisition 5

Company’s capital, manages company’s operational areas and structures, makes sure that

internal control system is running smoothly, and conducts appointments to the board.

:

Independent Non-Executive Directors

They are selected for a term of three years. They are normally appointed because of their vast

experience, have unique individual qualities and appropriate caliber. Furthermore, they may have

some expert knowledge that will aid the management board with valuable inputs. Their Roles

include: Monitoring performance banks performance, determining executive directors level of

Remuneration, help n marketing the bank services and connecting it to potentially useful

companies, and to make sure that bank’s capital is a true and fair reflection of its performance.

(Laan, 2013).

Board Committees

Constitutes of four committees with defined delegated duties. They include: Remuneration

Committee, Nomination Committee, the Sustainability and Responsibility Committee and the

Audit and Risk Committee.

These committees take independent expert opinions and advices where necessary at the bank’s

expense. Details of these committees and their members are given below.

Audit and Risk Committee

This committee is made up of independent non-executive directors. Each member is considered

to poses vast experience and knowledge of financial reporting to the deliberations of the

Nomination

Committee

Sustainability and

Responsibility

Committee

Management

Board of

Directors

Shareholders

Remuneration

Committee

Audit and Risk

Committee

Shareholder’s

Auditor

Elect

Appoint

Appoint

Report

Appoint

Appoint

Company’s capital, manages company’s operational areas and structures, makes sure that

internal control system is running smoothly, and conducts appointments to the board.

:

Independent Non-Executive Directors

They are selected for a term of three years. They are normally appointed because of their vast

experience, have unique individual qualities and appropriate caliber. Furthermore, they may have

some expert knowledge that will aid the management board with valuable inputs. Their Roles

include: Monitoring performance banks performance, determining executive directors level of

Remuneration, help n marketing the bank services and connecting it to potentially useful

companies, and to make sure that bank’s capital is a true and fair reflection of its performance.

(Laan, 2013).

Board Committees

Constitutes of four committees with defined delegated duties. They include: Remuneration

Committee, Nomination Committee, the Sustainability and Responsibility Committee and the

Audit and Risk Committee.

These committees take independent expert opinions and advices where necessary at the bank’s

expense. Details of these committees and their members are given below.

Audit and Risk Committee

This committee is made up of independent non-executive directors. Each member is considered

to poses vast experience and knowledge of financial reporting to the deliberations of the

Nomination

Committee

Sustainability and

Responsibility

Committee

Management

Board of

Directors

Shareholders

Remuneration

Committee

Audit and Risk

Committee

Shareholder’s

Auditor

Elect

Appoint

Appoint

Report

Appoint

Appoint

Running head: IS Strategy, Management and Acquisition 6

committee. The Committee’s responsibilities with regards to internal audit functions include:

assessing and monitoring efficiency of the internal audit functions, considering the selection,

termination or discharge of the Internal Audit head, making and considering suggestions and

recommendations to the Board on the selection, re-selection, discharge of the external auditor;

applauding the terms of contract, scope and nature of the audit;

Board Nomination Committee

The responsibilities of this committee include: in case Board vacancies come up, the assess the

knowledge, skill and experience needed to fill the position available, maintaining directors and

other senior executive succession plans under review to make sure the firm go on to compete in

the market place effectively and coming up with substantial suggestions to the Board.

Board Remuneration Committee

This committee decides the salary and favors of the bank’s chairperson, chief executive officer

and other directors. It also reassesses and accept the remuneration of other specific senior

management employees.

Sustainability and Responsibility Committee

This Committee acknowledges issues to do with how Standard Chartered can build a feasible

business through deliberation of economic development, social investment, environmental

protection, and other sustainability factors responsible for the firm’s long-term shareholder

value. The Committee's roles include: making sure that the banks business activities are in order,

reciprocating to external arising issues in regulation, stakeholder guidance, reporting and

legislation. Assessing new banks policies to make sure that adjustments are in order with

sustainability conventions and echo emerging trends and advancement. (Greuning & Brajovic,

2009).

Business Processes

A process is a designed set of operations that yield outcome. Repetition of processes ca be done

severally and are often structured carefully and optimized to influence efficiency and

productivity. Some of the processes that the standard chartered bank undertakes include;

Administration- This is the process of onboarding fresh employees with guidelines like provision

of an employee identity card.

Banking- After a stock exchange a bank's settlement operation delivers securities.

Operations- this are activities that involves acceptance of an order, service deliverance and

billing the client.

Procurement- this involves the guidelines needed to ensure security of parts and materials like,

accounts payable ,receiving, purchasing and invoice reconciliation.

Sales & Operations Planning- this process involves the procedure needed to scheme inventory

levels on the basis of factors like client demand and production dimensions.

committee. The Committee’s responsibilities with regards to internal audit functions include:

assessing and monitoring efficiency of the internal audit functions, considering the selection,

termination or discharge of the Internal Audit head, making and considering suggestions and

recommendations to the Board on the selection, re-selection, discharge of the external auditor;

applauding the terms of contract, scope and nature of the audit;

Board Nomination Committee

The responsibilities of this committee include: in case Board vacancies come up, the assess the

knowledge, skill and experience needed to fill the position available, maintaining directors and

other senior executive succession plans under review to make sure the firm go on to compete in

the market place effectively and coming up with substantial suggestions to the Board.

Board Remuneration Committee

This committee decides the salary and favors of the bank’s chairperson, chief executive officer

and other directors. It also reassesses and accept the remuneration of other specific senior

management employees.

Sustainability and Responsibility Committee

This Committee acknowledges issues to do with how Standard Chartered can build a feasible

business through deliberation of economic development, social investment, environmental

protection, and other sustainability factors responsible for the firm’s long-term shareholder

value. The Committee's roles include: making sure that the banks business activities are in order,

reciprocating to external arising issues in regulation, stakeholder guidance, reporting and

legislation. Assessing new banks policies to make sure that adjustments are in order with

sustainability conventions and echo emerging trends and advancement. (Greuning & Brajovic,

2009).

Business Processes

A process is a designed set of operations that yield outcome. Repetition of processes ca be done

severally and are often structured carefully and optimized to influence efficiency and

productivity. Some of the processes that the standard chartered bank undertakes include;

Administration- This is the process of onboarding fresh employees with guidelines like provision

of an employee identity card.

Banking- After a stock exchange a bank's settlement operation delivers securities.

Operations- this are activities that involves acceptance of an order, service deliverance and

billing the client.

Procurement- this involves the guidelines needed to ensure security of parts and materials like,

accounts payable ,receiving, purchasing and invoice reconciliation.

Sales & Operations Planning- this process involves the procedure needed to scheme inventory

levels on the basis of factors like client demand and production dimensions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: IS Strategy, Management and Acquisition 7

Information Technology-A different process of management accredits business group to comply

with requests of change for systems. Every change is prioritized, reviewed, evaluated,

implemented, and developed,

Information Security- this analyzes the state of exposure in systems for instance, access control

lists such as unused permissions.

Customer Service-this process investigates client discontent and decides if clients deserves a

compensation. The process also influences improvement to the company as setbacks may be

recorded as challenges and mended.

Infrastructure- this process carries out engineering evaluation of all bridges in a land annually

recognizes risks .

Asset Management- A data center carries out product inventory process annually that justifies

all devices in the store.

Performance Management- The process facilitates performance goal setup at the beginning of the

year and performance evaluation at the end of the year

Marketing- this process involves utilizing everything needed to establish and open new product

to market.

Sales-it includes guidelines needed to purchase to a customer, such as billing, orders, proposals,

quotes and delivery.

Policies

The following are some of the policies that guides standard chartered bank;

Position descriptions of the employee – this includes; definition of the role and responsibility of

an employee, amount of power possessed for making decision, overall objectives and particular

duties and creation of methods for accessing performance and building workers through training.

Personnel Policies – this includes; clear outlined business hours, retirement, condition of

employment, sick leave, salary, insurance and health advantages, and paid versus unpaid holiday

days.

Organizational Structure –this includes; creation of charts outlining each person’s identity, that

is, name and title showing everyone’s fitness in the organization structure.

Disciplinary action – this include; approaches on issues of safety, honesty, misconduct, and

performance and measures and disciplines taken upon violation of organization policy and rules.

Retaliation – retaliation policy should be avoided to safeguard employees and the organization.

Safety – this includes; Usage of best industry practices, and federal, local and state laws as steps

for creation of rules entailing best behavior mechanism at work, usage of safe equipment, and

ways of reporting safety hazards.

Information Technology-A different process of management accredits business group to comply

with requests of change for systems. Every change is prioritized, reviewed, evaluated,

implemented, and developed,

Information Security- this analyzes the state of exposure in systems for instance, access control

lists such as unused permissions.

Customer Service-this process investigates client discontent and decides if clients deserves a

compensation. The process also influences improvement to the company as setbacks may be

recorded as challenges and mended.

Infrastructure- this process carries out engineering evaluation of all bridges in a land annually

recognizes risks .

Asset Management- A data center carries out product inventory process annually that justifies

all devices in the store.

Performance Management- The process facilitates performance goal setup at the beginning of the

year and performance evaluation at the end of the year

Marketing- this process involves utilizing everything needed to establish and open new product

to market.

Sales-it includes guidelines needed to purchase to a customer, such as billing, orders, proposals,

quotes and delivery.

Policies

The following are some of the policies that guides standard chartered bank;

Position descriptions of the employee – this includes; definition of the role and responsibility of

an employee, amount of power possessed for making decision, overall objectives and particular

duties and creation of methods for accessing performance and building workers through training.

Personnel Policies – this includes; clear outlined business hours, retirement, condition of

employment, sick leave, salary, insurance and health advantages, and paid versus unpaid holiday

days.

Organizational Structure –this includes; creation of charts outlining each person’s identity, that

is, name and title showing everyone’s fitness in the organization structure.

Disciplinary action – this include; approaches on issues of safety, honesty, misconduct, and

performance and measures and disciplines taken upon violation of organization policy and rules.

Retaliation – retaliation policy should be avoided to safeguard employees and the organization.

Safety – this includes; Usage of best industry practices, and federal, local and state laws as steps

for creation of rules entailing best behavior mechanism at work, usage of safe equipment, and

ways of reporting safety hazards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: IS Strategy, Management and Acquisition 8

Technology – this include; establishment of legal and illegal usage of social media, internet and

email for personal reasons at work.

Policies for clients working with the organization include;

Privacy – this involves; protection of employees, the organization and clients through

establishment of a policy that promotes trust and transparency with the clients.

Credit – this include; decision on the terms of account opening and development of good credit

with the organization, settlement on the allowed amount of time for payment, establishment on

effects of late or overdue payments.

Confidentiality – this entails; protection of sensitive information, and of relationships using

clients, suppliers and vendors.

Regulatory Requirements

The above governance structure and policies of standard chartered bank meet the following

regulatory requirements; duty clarity, prevention of undue influence and trust maintenance,

decision establishment and governance of body design for independent regulators, transparency

and accountability, engagement, funding and evaluation on performance

Mitigating Risk

Risk identification- risks may appear from several channels like servicing, sales, mortgage,

product structure, debt collection, and client service. The bank identifies risks and documents

them, then evaluation methodologies are defined to assess these risks in a guarded manner. It

aligns these uncertainties with crucial decision-making guideline that assist in ensuring that all

organization decisions are established for the well-being of customers while meeting the needed

regulations.

There is a flexible structure to describe the company’s appetite with developed key metrics like

key risk, key performance, and key control indicators for conduct risks. To ensure transparency,

the bank factors the conduct risks into the organization strategy, and key metrics as well as risk

appetites are aligned with the decision-making processes and equivalent risks and controls. Some

of the key metrics include; tracking transparency, client satisfaction score, post-sales servicing,

and issue resolution. (Salem, 2013).

Control and mitigation management: once conduct risks are evaluated, the bank defines and

assess suitable control requirements in at the right time to enhance their effectiveness. The

organization describes aggressively as well as measuring controls

Remediation and issue management: issues should be unlimited to control inadequacy and

should be stated from any sector like product structure, client complaint, sale of a financial

goods, among others. The bank records and route the issues through an orderly investigation and

remediation method along with automatic alerts for following issues and action designs all

through their lifecycle.

Technology – this include; establishment of legal and illegal usage of social media, internet and

email for personal reasons at work.

Policies for clients working with the organization include;

Privacy – this involves; protection of employees, the organization and clients through

establishment of a policy that promotes trust and transparency with the clients.

Credit – this include; decision on the terms of account opening and development of good credit

with the organization, settlement on the allowed amount of time for payment, establishment on

effects of late or overdue payments.

Confidentiality – this entails; protection of sensitive information, and of relationships using

clients, suppliers and vendors.

Regulatory Requirements

The above governance structure and policies of standard chartered bank meet the following

regulatory requirements; duty clarity, prevention of undue influence and trust maintenance,

decision establishment and governance of body design for independent regulators, transparency

and accountability, engagement, funding and evaluation on performance

Mitigating Risk

Risk identification- risks may appear from several channels like servicing, sales, mortgage,

product structure, debt collection, and client service. The bank identifies risks and documents

them, then evaluation methodologies are defined to assess these risks in a guarded manner. It

aligns these uncertainties with crucial decision-making guideline that assist in ensuring that all

organization decisions are established for the well-being of customers while meeting the needed

regulations.

There is a flexible structure to describe the company’s appetite with developed key metrics like

key risk, key performance, and key control indicators for conduct risks. To ensure transparency,

the bank factors the conduct risks into the organization strategy, and key metrics as well as risk

appetites are aligned with the decision-making processes and equivalent risks and controls. Some

of the key metrics include; tracking transparency, client satisfaction score, post-sales servicing,

and issue resolution. (Salem, 2013).

Control and mitigation management: once conduct risks are evaluated, the bank defines and

assess suitable control requirements in at the right time to enhance their effectiveness. The

organization describes aggressively as well as measuring controls

Remediation and issue management: issues should be unlimited to control inadequacy and

should be stated from any sector like product structure, client complaint, sale of a financial

goods, among others. The bank records and route the issues through an orderly investigation and

remediation method along with automatic alerts for following issues and action designs all

through their lifecycle.

Running head: IS Strategy, Management and Acquisition 9

Complaints Management: the bank possesses an open and modernized approach to investigate,

record and remediate clients and internal discontent about an employees and company’s conduct.

Complaints are recorded either through risk evaluation surveys, emails or via mobile calls, or

online portals, and handled equivalently as an issue.

Survey Management: the bank uses questionnaires and surveys to evaluate staff behavior with

clients and recognize any fundamental issues and abide with the regulations.

Possible Improvements

The following are some of the possible improvements that the organization should focus on;

Business realignment- The basic argument of business realignment is to move out business areas

that costly and that have small margins and progress into areas that are more economical and

profitable. The bank should identify a robust way to necessary planning, evaluating the minimum

usage of assets required to compete in a specific area of business and recognize opportunities to

make a distinction of themselves from competitors. This means moving into nontraditional

businesses, like payment processing and specialty financing as long as their evaluations shows

that they can contest efficiently and effectively. (Berghahn, 2013).

Channel optimization- the aim of channel optimization is to evaluate the several ways client

communicates with a bank to enhance creation of an economical combination that is suitable to

each bank’s particular client base. This process encourages some fairly bold buying and selling

of branches as banks adapt to their geographic occupancy. The bank should reconfigure roles and

accountabilities within the branches and adopt fresh metrics for evaluating branch value and

performance and value. Other approach include improving the functioning hours and technical

abilities of call centers to see through client varying expectations.

The no one-size-fits-all approach-Some banks aggressively advocate opening of electronic

account, deposit capture that are out of the way through smart devices, and accounts that are

structured to be basically paperless. Other banks however, usually those with large commercial

clients follow a basically different way, aiming on individual service with a relationship

administrator and support group appointed to each certified account. The evaluation of such

organizations has acknowledged that the high-worth business developed by this way can more

than offset the added expenses. (Andersen, 2007).

Process costs- the chance to enhance process costs often is under acknowledged in financial

firms. The objective is to minimize the unit expense-to-value ratio of each operations or

transaction, for instance the expense of opening an account, generating a loan document bundle,

or managing a particular type of transaction. development in this line include constant

performance management and often arise as a result of analyzing, benchmarking, eventually

rethinking and mapping back-office processes.

Staff productivity- besides reducing process expense, automation tools can assist in improving

employee productivity, allowing banks to address more activities and greater capacity of

transactions with the same number of individuals. Work rate improvement does not rely on

technology alone. Some of the most important opportunities include using developed

Complaints Management: the bank possesses an open and modernized approach to investigate,

record and remediate clients and internal discontent about an employees and company’s conduct.

Complaints are recorded either through risk evaluation surveys, emails or via mobile calls, or

online portals, and handled equivalently as an issue.

Survey Management: the bank uses questionnaires and surveys to evaluate staff behavior with

clients and recognize any fundamental issues and abide with the regulations.

Possible Improvements

The following are some of the possible improvements that the organization should focus on;

Business realignment- The basic argument of business realignment is to move out business areas

that costly and that have small margins and progress into areas that are more economical and

profitable. The bank should identify a robust way to necessary planning, evaluating the minimum

usage of assets required to compete in a specific area of business and recognize opportunities to

make a distinction of themselves from competitors. This means moving into nontraditional

businesses, like payment processing and specialty financing as long as their evaluations shows

that they can contest efficiently and effectively. (Berghahn, 2013).

Channel optimization- the aim of channel optimization is to evaluate the several ways client

communicates with a bank to enhance creation of an economical combination that is suitable to

each bank’s particular client base. This process encourages some fairly bold buying and selling

of branches as banks adapt to their geographic occupancy. The bank should reconfigure roles and

accountabilities within the branches and adopt fresh metrics for evaluating branch value and

performance and value. Other approach include improving the functioning hours and technical

abilities of call centers to see through client varying expectations.

The no one-size-fits-all approach-Some banks aggressively advocate opening of electronic

account, deposit capture that are out of the way through smart devices, and accounts that are

structured to be basically paperless. Other banks however, usually those with large commercial

clients follow a basically different way, aiming on individual service with a relationship

administrator and support group appointed to each certified account. The evaluation of such

organizations has acknowledged that the high-worth business developed by this way can more

than offset the added expenses. (Andersen, 2007).

Process costs- the chance to enhance process costs often is under acknowledged in financial

firms. The objective is to minimize the unit expense-to-value ratio of each operations or

transaction, for instance the expense of opening an account, generating a loan document bundle,

or managing a particular type of transaction. development in this line include constant

performance management and often arise as a result of analyzing, benchmarking, eventually

rethinking and mapping back-office processes.

Staff productivity- besides reducing process expense, automation tools can assist in improving

employee productivity, allowing banks to address more activities and greater capacity of

transactions with the same number of individuals. Work rate improvement does not rely on

technology alone. Some of the most important opportunities include using developed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: IS Strategy, Management and Acquisition 10

performance management method, like well described expectations and scorecards, enhanced

rewards and motivation systems, and good supervision and training. (Lane, 2010).

Other useful accessory involves visible metrics and output charts together with some line-of-

intuitiveness incentives like bonuses that are given according individual performance and

training, not just organization work rate. Many organizations also discover achievement in

redefining work duties, testing with more bendable job structures, and outsourcing more specific

functions.

Technology and automation- the utilization of technology and automation also benefits

individual concentration as part of the general effectiveness improvement effort. The overarching

objective is bi-fold: first is to utilize technology to minimize the time spent in discovering data

and secondly is to utilize automated business guidelines to progress work around the

organization faster and effectively. (Tricker, 2015).

Vendor relationships- upgraded vendor management does not necessarily mean putting pressure

vendors to minimize their prices. Rather, it is structured to define the greatest possible worth

from a vendor relationship. Significant tools involve utilizing service-level alliance and vendor

scorecards to manager accomplishment issues, like availability of system, response times, and

direct consumption. Such gadgets assist in provision of a more complete design of the vendor

relationship.

Other fundamental expense-cutting method involves measuring expenses and consolidating

vendors against similar services in the market.

Conclusion

Information systems can bear impacts of infusion and diffusion in a company. Data systems will

be employed only in silos for information processing if infusion and diffusion are low.in cases

where infusion is low and diffusion is high there will be an information system that is

decentralized. In addition, if diffusion is low and infusion is high, there will be an information

system that is crucial to activities only. Nevertheless, if both infusion and diffusion are high, the

organizations’ information system will contribute to a calculated and competitive benefits.

performance management method, like well described expectations and scorecards, enhanced

rewards and motivation systems, and good supervision and training. (Lane, 2010).

Other useful accessory involves visible metrics and output charts together with some line-of-

intuitiveness incentives like bonuses that are given according individual performance and

training, not just organization work rate. Many organizations also discover achievement in

redefining work duties, testing with more bendable job structures, and outsourcing more specific

functions.

Technology and automation- the utilization of technology and automation also benefits

individual concentration as part of the general effectiveness improvement effort. The overarching

objective is bi-fold: first is to utilize technology to minimize the time spent in discovering data

and secondly is to utilize automated business guidelines to progress work around the

organization faster and effectively. (Tricker, 2015).

Vendor relationships- upgraded vendor management does not necessarily mean putting pressure

vendors to minimize their prices. Rather, it is structured to define the greatest possible worth

from a vendor relationship. Significant tools involve utilizing service-level alliance and vendor

scorecards to manager accomplishment issues, like availability of system, response times, and

direct consumption. Such gadgets assist in provision of a more complete design of the vendor

relationship.

Other fundamental expense-cutting method involves measuring expenses and consolidating

vendors against similar services in the market.

Conclusion

Information systems can bear impacts of infusion and diffusion in a company. Data systems will

be employed only in silos for information processing if infusion and diffusion are low.in cases

where infusion is low and diffusion is high there will be an information system that is

decentralized. In addition, if diffusion is low and infusion is high, there will be an information

system that is crucial to activities only. Nevertheless, if both infusion and diffusion are high, the

organizations’ information system will contribute to a calculated and competitive benefits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: IS Strategy, Management and Acquisition 11

References

Grant, K., Hackney, R., & Edgar, D. (2009). Strategic information systems management.

Andover: Cengage Learning.

Jawadekar, W. S. (2010). Management information systems: Text and cases : a digital-firm

perspective. New Delhi: Tata Mcgraw-Hill.

Bharati, P., Lee, I., & Chaudhury, A. (2010). Global perspectives on small and medium

enterprises and strategic information systems: International approaches. Hershey, PA: Business

Science Reference.

United Arab Emirates., & United Arab Emirates. (2014). IT infrastructure.

Laan, S. (2013). It infrastructure architecture - infrastructure building blocks and concepts.

Place of publication not identified: Lulu Com.

Harvard Business Review Press. (2010). Improving business processes: Expert solutions to

everyday challenges. Boston, Mass: Harvard Business Review Press.

Deutch, D., & Milo, T. (2012). Business processes: A database perspective. San Rafael, Calif.:

Morgan & Claypool.

Draheim, D. (2010). Business process technology: A unified view on business processes,

workflows and enterprise applications. Heidelberg: Springer.

Weske, M. (2007). Business process management: Concepts, languages, architectures. Berlin:

Springer.

Brotby, W. K., & IT Governance Institute. (2008). Information security governance: Guidance

for information security managers. Rolling Meadows, Ill: IT Governance Institute.

Greuning, H. ., & Brajovic, B. S. (2009). Analyzing banking risk: A framework for assessing

corporate governance and risk management. Washington, D.C: World Bank.

Salem, R. A. (2013). Risk management for Islamic banks. Edinburgh: Edinburgh University

Press.

Wahyudi, I., Rosmanita, F., Prasetyo, M. B., & Surya, P. N. I. (2014). Risk management for

Islamic banks: Recent developments from Asia and the Middle East.

Berghahn, T. (2013). Managing diversity program of the deutsche bank. Place of publication not

identified: Grin Verlag.

Bologna, P., Prasad, A., & International Monetary Fund. (2009). Oman: Banking sector

resilience. Washington, D.C.: International Monetary Fund.

Italian Association for Information Systems., D'Atri, A., & Saccà, D. (2010). Information

systems: People, organizations, institutions, and technologies. Heidelberg: Physica-Verlag.

References

Grant, K., Hackney, R., & Edgar, D. (2009). Strategic information systems management.

Andover: Cengage Learning.

Jawadekar, W. S. (2010). Management information systems: Text and cases : a digital-firm

perspective. New Delhi: Tata Mcgraw-Hill.

Bharati, P., Lee, I., & Chaudhury, A. (2010). Global perspectives on small and medium

enterprises and strategic information systems: International approaches. Hershey, PA: Business

Science Reference.

United Arab Emirates., & United Arab Emirates. (2014). IT infrastructure.

Laan, S. (2013). It infrastructure architecture - infrastructure building blocks and concepts.

Place of publication not identified: Lulu Com.

Harvard Business Review Press. (2010). Improving business processes: Expert solutions to

everyday challenges. Boston, Mass: Harvard Business Review Press.

Deutch, D., & Milo, T. (2012). Business processes: A database perspective. San Rafael, Calif.:

Morgan & Claypool.

Draheim, D. (2010). Business process technology: A unified view on business processes,

workflows and enterprise applications. Heidelberg: Springer.

Weske, M. (2007). Business process management: Concepts, languages, architectures. Berlin:

Springer.

Brotby, W. K., & IT Governance Institute. (2008). Information security governance: Guidance

for information security managers. Rolling Meadows, Ill: IT Governance Institute.

Greuning, H. ., & Brajovic, B. S. (2009). Analyzing banking risk: A framework for assessing

corporate governance and risk management. Washington, D.C: World Bank.

Salem, R. A. (2013). Risk management for Islamic banks. Edinburgh: Edinburgh University

Press.

Wahyudi, I., Rosmanita, F., Prasetyo, M. B., & Surya, P. N. I. (2014). Risk management for

Islamic banks: Recent developments from Asia and the Middle East.

Berghahn, T. (2013). Managing diversity program of the deutsche bank. Place of publication not

identified: Grin Verlag.

Bologna, P., Prasad, A., & International Monetary Fund. (2009). Oman: Banking sector

resilience. Washington, D.C.: International Monetary Fund.

Italian Association for Information Systems., D'Atri, A., & Saccà, D. (2010). Information

systems: People, organizations, institutions, and technologies. Heidelberg: Physica-Verlag.

Running head: IS Strategy, Management and Acquisition 12

Andersen, B. (2007). Business process improvement toolbox. Milwaukee, Wis: ASQ Quality

Press.

Lane, M. J. (2010). Representing corporate officers, directors, managers, and trustees.

Frederick, MD: Aspen Publishers, Wolters Kluwer Law & Business.

Tricker, R. I. (2015). Corporate governance: Principles, policies, and practices.

Baxt, R., & Australian Institute of Company Directors. (2009). Duties and responsibilities of

directors and officers. Sydney: Australian Institute of Company Directors.

Andersen, B. (2007). Business process improvement toolbox. Milwaukee, Wis: ASQ Quality

Press.

Lane, M. J. (2010). Representing corporate officers, directors, managers, and trustees.

Frederick, MD: Aspen Publishers, Wolters Kluwer Law & Business.

Tricker, R. I. (2015). Corporate governance: Principles, policies, and practices.

Baxt, R., & Australian Institute of Company Directors. (2009). Duties and responsibilities of

directors and officers. Sydney: Australian Institute of Company Directors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.