Comprehensive Financial Statement and Investment Analysis of ING Bank

VerifiedAdded on 2023/05/31

|10

|2208

|254

Report

AI Summary

This report provides a comprehensive financial analysis of ING Bank, examining its core business activities, including retail, commercial, and investment banking, as well as asset management and insurance services. The report highlights major changes in the company's financial performance, such as increased net profits, a high return on equity, and a strong CET 1 ratio. It also discusses the company's strategic initiatives, including investments in financial technology start-ups and the implementation of online wealth management services. The report includes a detailed ratio analysis of the company for 2016 and 2017, covering liquidity, debt management, and profitability ratios. Furthermore, it presents the consolidated statement of financial position and profit or loss, providing an overview of the company's financial performance. The analysis concludes with an overall assessment of ING Bank's financial health and future prospects, including its plans for expansion and investment in new markets and technologies.

Financial Statement

and Investment

Analysis Assignment

and Investment

Analysis Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Background and Abstract............................................................................................................................3

Introduction: Core business and different segments...................................................................................3

Discussion and Analysis...............................................................................................................................3

Major changes in the financial performance...........................................................................................3

Ratio Analysis of the company.................................................................................................................4

Conclusion...................................................................................................................................................5

Financial Analysis and overall assessment...............................................................................................5

References...................................................................................................................................................9

2 | P a g e

Contents

Background and Abstract............................................................................................................................3

Introduction: Core business and different segments...................................................................................3

Discussion and Analysis...............................................................................................................................3

Major changes in the financial performance...........................................................................................3

Ratio Analysis of the company.................................................................................................................4

Conclusion...................................................................................................................................................5

Financial Analysis and overall assessment...............................................................................................5

References...................................................................................................................................................9

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Background and Abstract

A report has been prepared on the one of the banks called ING Bank. The report highlights the core

business activity of the company and the different segments in which the company is involved. It also

mentions the major changes that have took place in the company over the past years as shown in the

chairman’s message and the review by the managing director. Key financial ratios have also been

computed for the last 2 years, 2017 and 2016 and finally the overall assessment of the company and the

prospects in future have also been highlighted.

Introduction: Core business and different segments

The ING group is a Dutch multinational banking financial services offering company based out of

Amsterdam. It is one of the pioneer companies in banking industry and has its stretch over a number of

countries all around the word. The core business activities of the company includes direct and retail

banking, commercial banking and investment banking as well. It also deals in asset management

activities and insurance services as well (Belton, 2017). The company has served more than 37.4 million

customers in over 40 nations over the world and is a part of Euro Stoxx 50 stock market index. The

primary purpose of the company is empower people to be step ahead in both lives as well as business.

The company has been operating in some of the major economies like those of United States, India,

China, United Kingdom, Spain, Brazil, Hungary, Malaysia, Luxembourg, Monaco, Netherlands, Columbia,

etc. The company has the largest market share in the retail banking which scales up to 40%, followed by

direct banking and commercial banking (Trieu, 2017).

Discussion and Analysis

Major changes in the financial performance

The company has been focusing on the international expansion and capital injection for the last couple

of years through mergers and acquisition. As per the message of the Chairman of the company and the

managing director, the group’s net profits have increased by more than 5% over the past year, the

group’s return on equity was 10.2% which is much higher than the normal industry trend. The Fully

loaded CET 1 ratio ING Group was 14.7% which is one of the major achievements in the history of the

company as it shows minimal risk for the company (Mubako & O'Donnell, 2018). Amongst the major

financial changes, the company came up with innovation techniques to compete with giants like Google

and Amazon. The company also announced venturing and investing in the start-ups as well. For the

same, 300 Million Euro was being planned to invest in the financial technology based start-ups. In the

Global Bank Awards 2017, it was awarded the best bank in the world. The company also started with the

online wealth management services in Germany where the customer would not have to be concerned

regarding the asset allocation and the product selection (Sithole, Chandler, Abeysekera, & Paas, 2017).

Amongst the non-financial measures, the company started with the Think Forward Leadership

Experience to train 5000+ managers. All these measures have fuelled up growth for the company and

has increased the performance of the company over the past years. Many such measures are still there

in the pipeline (Choy, 2018).

3 | P a g e

Background and Abstract

A report has been prepared on the one of the banks called ING Bank. The report highlights the core

business activity of the company and the different segments in which the company is involved. It also

mentions the major changes that have took place in the company over the past years as shown in the

chairman’s message and the review by the managing director. Key financial ratios have also been

computed for the last 2 years, 2017 and 2016 and finally the overall assessment of the company and the

prospects in future have also been highlighted.

Introduction: Core business and different segments

The ING group is a Dutch multinational banking financial services offering company based out of

Amsterdam. It is one of the pioneer companies in banking industry and has its stretch over a number of

countries all around the word. The core business activities of the company includes direct and retail

banking, commercial banking and investment banking as well. It also deals in asset management

activities and insurance services as well (Belton, 2017). The company has served more than 37.4 million

customers in over 40 nations over the world and is a part of Euro Stoxx 50 stock market index. The

primary purpose of the company is empower people to be step ahead in both lives as well as business.

The company has been operating in some of the major economies like those of United States, India,

China, United Kingdom, Spain, Brazil, Hungary, Malaysia, Luxembourg, Monaco, Netherlands, Columbia,

etc. The company has the largest market share in the retail banking which scales up to 40%, followed by

direct banking and commercial banking (Trieu, 2017).

Discussion and Analysis

Major changes in the financial performance

The company has been focusing on the international expansion and capital injection for the last couple

of years through mergers and acquisition. As per the message of the Chairman of the company and the

managing director, the group’s net profits have increased by more than 5% over the past year, the

group’s return on equity was 10.2% which is much higher than the normal industry trend. The Fully

loaded CET 1 ratio ING Group was 14.7% which is one of the major achievements in the history of the

company as it shows minimal risk for the company (Mubako & O'Donnell, 2018). Amongst the major

financial changes, the company came up with innovation techniques to compete with giants like Google

and Amazon. The company also announced venturing and investing in the start-ups as well. For the

same, 300 Million Euro was being planned to invest in the financial technology based start-ups. In the

Global Bank Awards 2017, it was awarded the best bank in the world. The company also started with the

online wealth management services in Germany where the customer would not have to be concerned

regarding the asset allocation and the product selection (Sithole, Chandler, Abeysekera, & Paas, 2017).

Amongst the non-financial measures, the company started with the Think Forward Leadership

Experience to train 5000+ managers. All these measures have fuelled up growth for the company and

has increased the performance of the company over the past years. Many such measures are still there

in the pipeline (Choy, 2018).

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

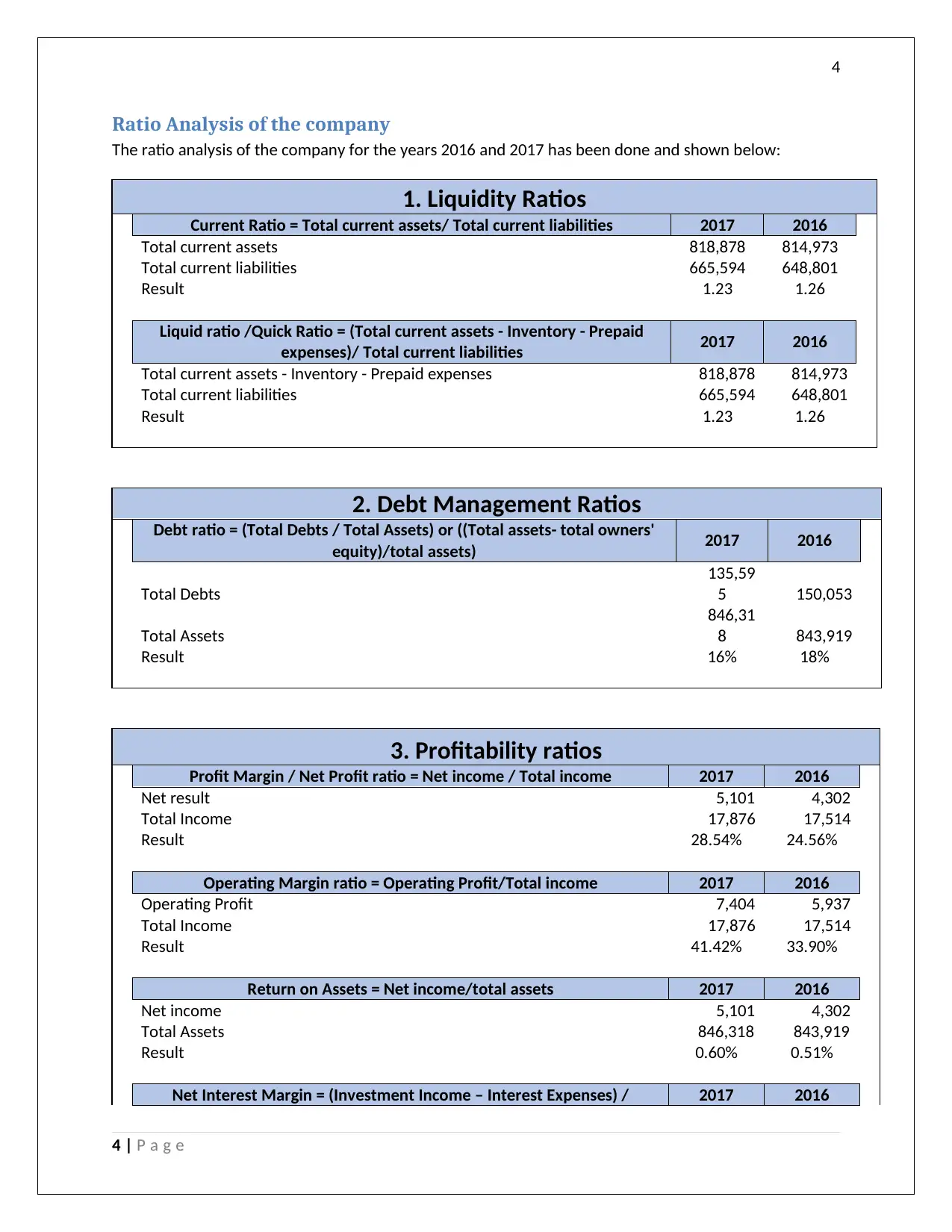

Ratio Analysis of the company

The ratio analysis of the company for the years 2016 and 2017 has been done and shown below:

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2017 2016

Total current assets 818,878 814,973

Total current liabilities 665,594 648,801

Result 1.23 1.26

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities 2017 2016

Total current assets - Inventory - Prepaid expenses 818,878 814,973

Total current liabilities 665,594 648,801

Result 1.23 1.26

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets) 2017 2016

Total Debts

135,59

5 150,053

Total Assets

846,31

8 843,919

Result 16% 18%

3. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Total income 2017 2016

Net result 5,101 4,302

Total Income 17,876 17,514

Result 28.54% 24.56%

Operating Margin ratio = Operating Profit/Total income 2017 2016

Operating Profit 7,404 5,937

Total Income 17,876 17,514

Result 41.42% 33.90%

Return on Assets = Net income/total assets 2017 2016

Net income 5,101 4,302

Total Assets 846,318 843,919

Result 0.60% 0.51%

Net Interest Margin = (Investment Income – Interest Expenses) / 2017 2016

4 | P a g e

Ratio Analysis of the company

The ratio analysis of the company for the years 2016 and 2017 has been done and shown below:

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2017 2016

Total current assets 818,878 814,973

Total current liabilities 665,594 648,801

Result 1.23 1.26

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities 2017 2016

Total current assets - Inventory - Prepaid expenses 818,878 814,973

Total current liabilities 665,594 648,801

Result 1.23 1.26

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets) 2017 2016

Total Debts

135,59

5 150,053

Total Assets

846,31

8 843,919

Result 16% 18%

3. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Total income 2017 2016

Net result 5,101 4,302

Total Income 17,876 17,514

Result 28.54% 24.56%

Operating Margin ratio = Operating Profit/Total income 2017 2016

Operating Profit 7,404 5,937

Total Income 17,876 17,514

Result 41.42% 33.90%

Return on Assets = Net income/total assets 2017 2016

Net income 5,101 4,302

Total Assets 846,318 843,919

Result 0.60% 0.51%

Net Interest Margin = (Investment Income – Interest Expenses) / 2017 2016

4 | P a g e

5

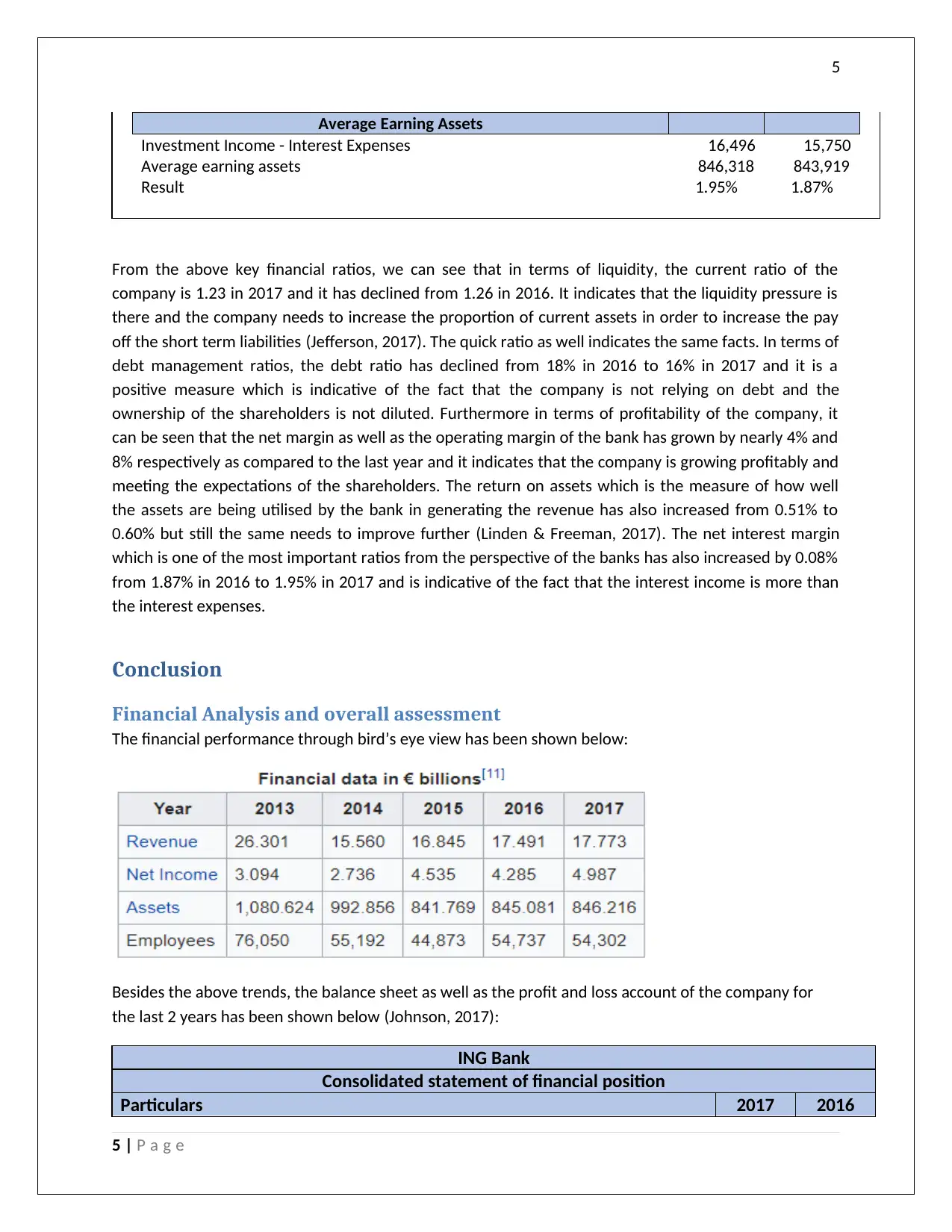

Average Earning Assets

Investment Income - Interest Expenses 16,496 15,750

Average earning assets 846,318 843,919

Result 1.95% 1.87%

From the above key financial ratios, we can see that in terms of liquidity, the current ratio of the

company is 1.23 in 2017 and it has declined from 1.26 in 2016. It indicates that the liquidity pressure is

there and the company needs to increase the proportion of current assets in order to increase the pay

off the short term liabilities (Jefferson, 2017). The quick ratio as well indicates the same facts. In terms of

debt management ratios, the debt ratio has declined from 18% in 2016 to 16% in 2017 and it is a

positive measure which is indicative of the fact that the company is not relying on debt and the

ownership of the shareholders is not diluted. Furthermore in terms of profitability of the company, it

can be seen that the net margin as well as the operating margin of the bank has grown by nearly 4% and

8% respectively as compared to the last year and it indicates that the company is growing profitably and

meeting the expectations of the shareholders. The return on assets which is the measure of how well

the assets are being utilised by the bank in generating the revenue has also increased from 0.51% to

0.60% but still the same needs to improve further (Linden & Freeman, 2017). The net interest margin

which is one of the most important ratios from the perspective of the banks has also increased by 0.08%

from 1.87% in 2016 to 1.95% in 2017 and is indicative of the fact that the interest income is more than

the interest expenses.

Conclusion

Financial Analysis and overall assessment

The financial performance through bird’s eye view has been shown below:

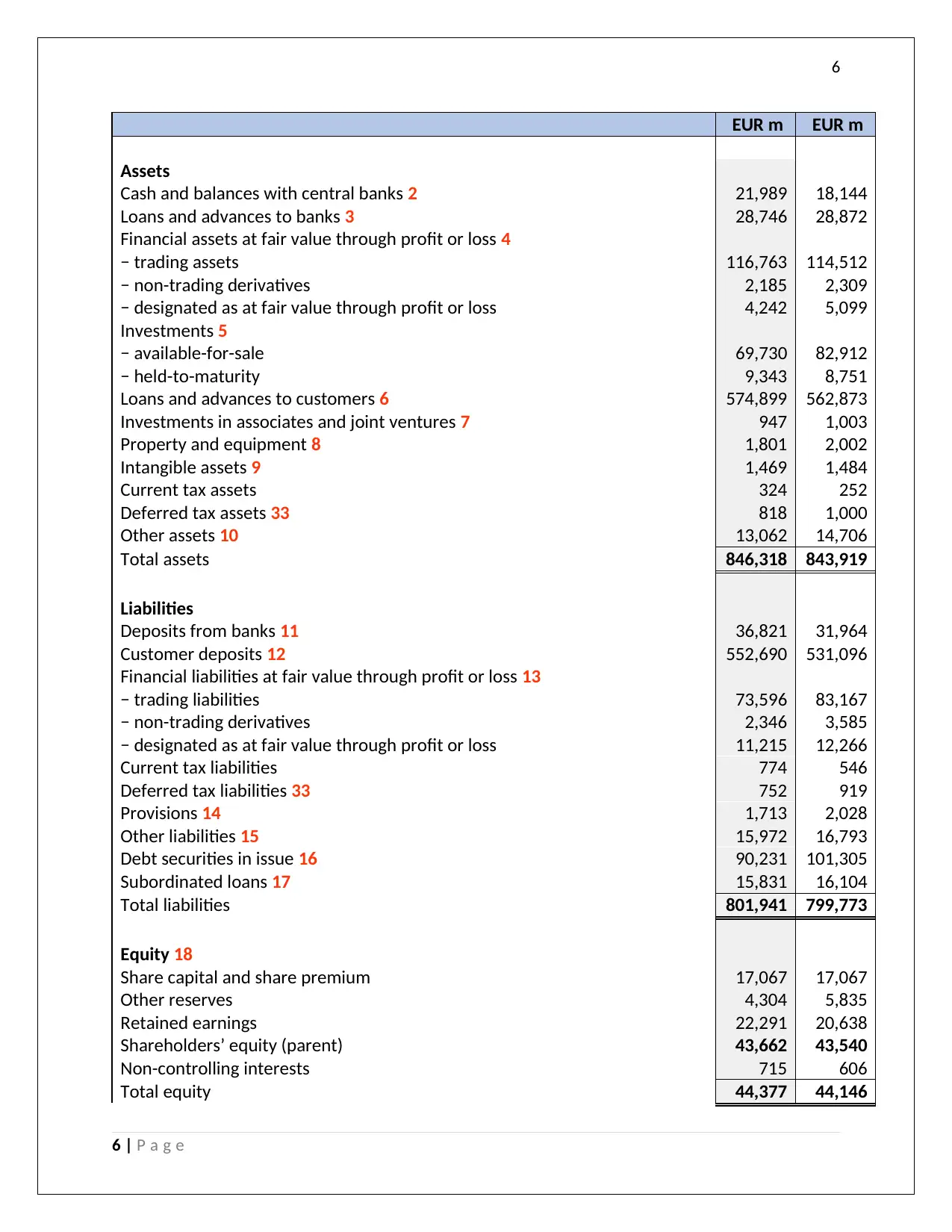

Besides the above trends, the balance sheet as well as the profit and loss account of the company for

the last 2 years has been shown below (Johnson, 2017):

ING Bank

Consolidated statement of financial position

Particulars 2017 2016

5 | P a g e

Average Earning Assets

Investment Income - Interest Expenses 16,496 15,750

Average earning assets 846,318 843,919

Result 1.95% 1.87%

From the above key financial ratios, we can see that in terms of liquidity, the current ratio of the

company is 1.23 in 2017 and it has declined from 1.26 in 2016. It indicates that the liquidity pressure is

there and the company needs to increase the proportion of current assets in order to increase the pay

off the short term liabilities (Jefferson, 2017). The quick ratio as well indicates the same facts. In terms of

debt management ratios, the debt ratio has declined from 18% in 2016 to 16% in 2017 and it is a

positive measure which is indicative of the fact that the company is not relying on debt and the

ownership of the shareholders is not diluted. Furthermore in terms of profitability of the company, it

can be seen that the net margin as well as the operating margin of the bank has grown by nearly 4% and

8% respectively as compared to the last year and it indicates that the company is growing profitably and

meeting the expectations of the shareholders. The return on assets which is the measure of how well

the assets are being utilised by the bank in generating the revenue has also increased from 0.51% to

0.60% but still the same needs to improve further (Linden & Freeman, 2017). The net interest margin

which is one of the most important ratios from the perspective of the banks has also increased by 0.08%

from 1.87% in 2016 to 1.95% in 2017 and is indicative of the fact that the interest income is more than

the interest expenses.

Conclusion

Financial Analysis and overall assessment

The financial performance through bird’s eye view has been shown below:

Besides the above trends, the balance sheet as well as the profit and loss account of the company for

the last 2 years has been shown below (Johnson, 2017):

ING Bank

Consolidated statement of financial position

Particulars 2017 2016

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

EUR m EUR m

Assets

Cash and balances with central banks 2 21,989 18,144

Loans and advances to banks 3 28,746 28,872

Financial assets at fair value through profit or loss 4

− trading assets 116,763 114,512

− non-trading derivatives 2,185 2,309

− designated as at fair value through profit or loss 4,242 5,099

Investments 5

− available-for-sale 69,730 82,912

− held-to-maturity 9,343 8,751

Loans and advances to customers 6 574,899 562,873

Investments in associates and joint ventures 7 947 1,003

Property and equipment 8 1,801 2,002

Intangible assets 9 1,469 1,484

Current tax assets 324 252

Deferred tax assets 33 818 1,000

Other assets 10 13,062 14,706

Total assets 846,318 843,919

Liabilities

Deposits from banks 11 36,821 31,964

Customer deposits 12 552,690 531,096

Financial liabilities at fair value through profit or loss 13

− trading liabilities 73,596 83,167

− non-trading derivatives 2,346 3,585

− designated as at fair value through profit or loss 11,215 12,266

Current tax liabilities 774 546

Deferred tax liabilities 33 752 919

Provisions 14 1,713 2,028

Other liabilities 15 15,972 16,793

Debt securities in issue 16 90,231 101,305

Subordinated loans 17 15,831 16,104

Total liabilities 801,941 799,773

Equity 18

Share capital and share premium 17,067 17,067

Other reserves 4,304 5,835

Retained earnings 22,291 20,638

Shareholders’ equity (parent) 43,662 43,540

Non-controlling interests 715 606

Total equity 44,377 44,146

6 | P a g e

EUR m EUR m

Assets

Cash and balances with central banks 2 21,989 18,144

Loans and advances to banks 3 28,746 28,872

Financial assets at fair value through profit or loss 4

− trading assets 116,763 114,512

− non-trading derivatives 2,185 2,309

− designated as at fair value through profit or loss 4,242 5,099

Investments 5

− available-for-sale 69,730 82,912

− held-to-maturity 9,343 8,751

Loans and advances to customers 6 574,899 562,873

Investments in associates and joint ventures 7 947 1,003

Property and equipment 8 1,801 2,002

Intangible assets 9 1,469 1,484

Current tax assets 324 252

Deferred tax assets 33 818 1,000

Other assets 10 13,062 14,706

Total assets 846,318 843,919

Liabilities

Deposits from banks 11 36,821 31,964

Customer deposits 12 552,690 531,096

Financial liabilities at fair value through profit or loss 13

− trading liabilities 73,596 83,167

− non-trading derivatives 2,346 3,585

− designated as at fair value through profit or loss 11,215 12,266

Current tax liabilities 774 546

Deferred tax liabilities 33 752 919

Provisions 14 1,713 2,028

Other liabilities 15 15,972 16,793

Debt securities in issue 16 90,231 101,305

Subordinated loans 17 15,831 16,104

Total liabilities 801,941 799,773

Equity 18

Share capital and share premium 17,067 17,067

Other reserves 4,304 5,835

Retained earnings 22,291 20,638

Shareholders’ equity (parent) 43,662 43,540

Non-controlling interests 715 606

Total equity 44,377 44,146

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

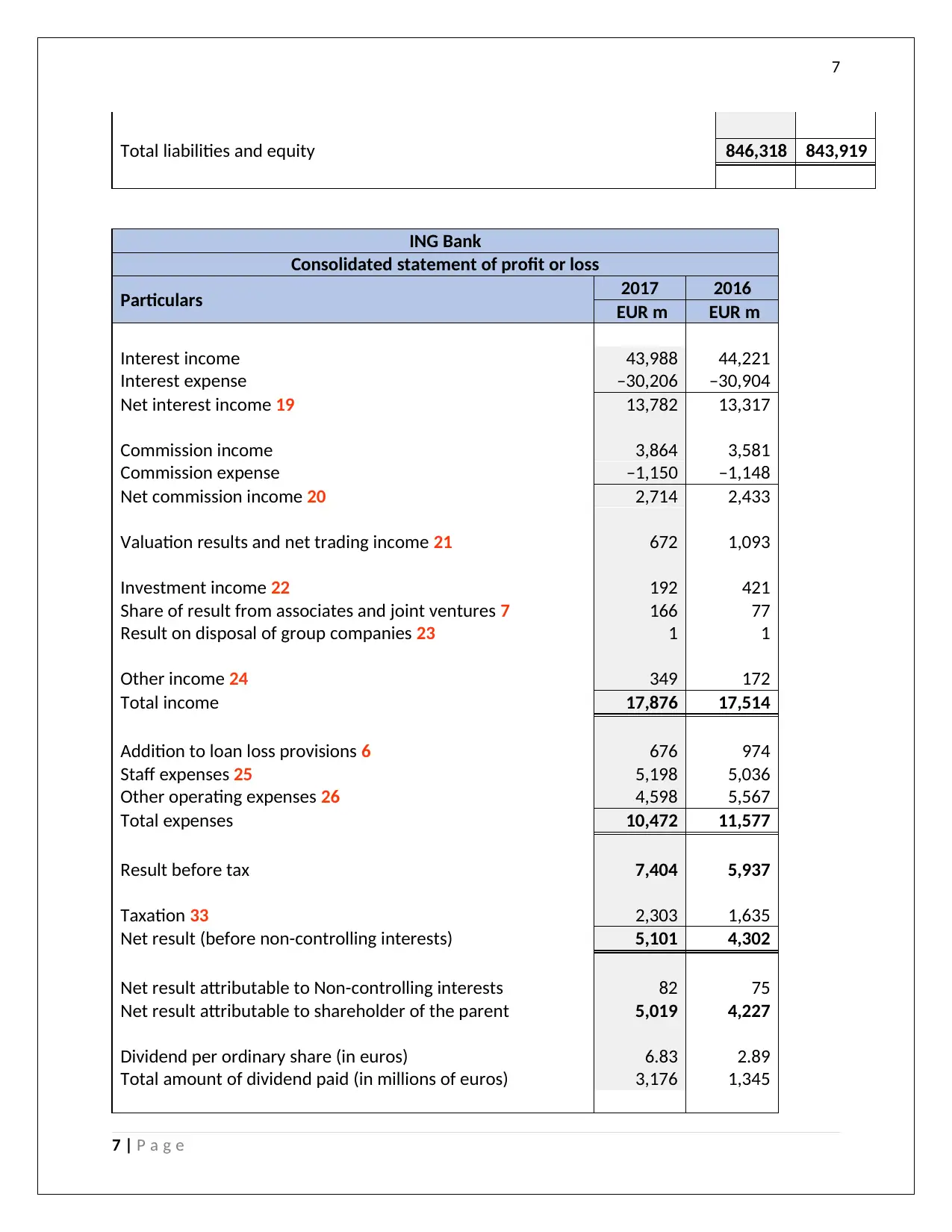

Total liabilities and equity 846,318 843,919

ING Bank

Consolidated statement of profit or loss

Particulars 2017 2016

EUR m EUR m

Interest income 43,988 44,221

Interest expense –30,206 –30,904

Net interest income 19 13,782 13,317

Commission income 3,864 3,581

Commission expense –1,150 –1,148

Net commission income 20 2,714 2,433

Valuation results and net trading income 21 672 1,093

Investment income 22 192 421

Share of result from associates and joint ventures 7 166 77

Result on disposal of group companies 23 1 1

Other income 24 349 172

Total income 17,876 17,514

Addition to loan loss provisions 6 676 974

Staff expenses 25 5,198 5,036

Other operating expenses 26 4,598 5,567

Total expenses 10,472 11,577

Result before tax 7,404 5,937

Taxation 33 2,303 1,635

Net result (before non-controlling interests) 5,101 4,302

Net result attributable to Non-controlling interests 82 75

Net result attributable to shareholder of the parent 5,019 4,227

Dividend per ordinary share (in euros) 6.83 2.89

Total amount of dividend paid (in millions of euros) 3,176 1,345

7 | P a g e

Total liabilities and equity 846,318 843,919

ING Bank

Consolidated statement of profit or loss

Particulars 2017 2016

EUR m EUR m

Interest income 43,988 44,221

Interest expense –30,206 –30,904

Net interest income 19 13,782 13,317

Commission income 3,864 3,581

Commission expense –1,150 –1,148

Net commission income 20 2,714 2,433

Valuation results and net trading income 21 672 1,093

Investment income 22 192 421

Share of result from associates and joint ventures 7 166 77

Result on disposal of group companies 23 1 1

Other income 24 349 172

Total income 17,876 17,514

Addition to loan loss provisions 6 676 974

Staff expenses 25 5,198 5,036

Other operating expenses 26 4,598 5,567

Total expenses 10,472 11,577

Result before tax 7,404 5,937

Taxation 33 2,303 1,635

Net result (before non-controlling interests) 5,101 4,302

Net result attributable to Non-controlling interests 82 75

Net result attributable to shareholder of the parent 5,019 4,227

Dividend per ordinary share (in euros) 6.83 2.89

Total amount of dividend paid (in millions of euros) 3,176 1,345

7 | P a g e

8

From the above discussion and analysis, it can be mentioned that the company has been a growing one

and has also been earning profit over the period of time (Dichev, 2017). As far as the future prospects of

the company is concerned, it plans to expand further and venture into new markets and start several

online asset management services (Meroño-Cerdán, Lopez-Nicolas, & Molina-Castillo, 2017).

Furthermore, as has been mentioned above, the company also has planned investment in the

technology based start-ups which is aimed at increasing both the top line as well as bottom-line of the

company and improve the customer experience and services. Besides this, the company has met all the

sustainability reporting measures and is continuously working in the area of corporate governance and

hence all in all, the company has good future prospects (Marques, 2018).

8 | P a g e

From the above discussion and analysis, it can be mentioned that the company has been a growing one

and has also been earning profit over the period of time (Dichev, 2017). As far as the future prospects of

the company is concerned, it plans to expand further and venture into new markets and start several

online asset management services (Meroño-Cerdán, Lopez-Nicolas, & Molina-Castillo, 2017).

Furthermore, as has been mentioned above, the company also has planned investment in the

technology based start-ups which is aimed at increasing both the top line as well as bottom-line of the

company and improve the customer experience and services. Besides this, the company has met all the

sustainability reporting measures and is continuously working in the area of corporate governance and

hence all in all, the company has good future prospects (Marques, 2018).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

References

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance (Vol. 2). London:

Macat International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Johnson, R. (2017). The Best Strategies for Investing. In the News, 21-31.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Meroño-Cerdán, A., Lopez-Nicolas, C., & Molina-Castillo, F. (2017). Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, 1-15.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), 111-124.

9 | P a g e

References

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance (Vol. 2). London:

Macat International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Johnson, R. (2017). The Best Strategies for Investing. In the News, 21-31.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Meroño-Cerdán, A., Lopez-Nicolas, C., & Molina-Castillo, F. (2017). Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, 1-15.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), 111-124.

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.