Inherent Risk Assessment Template for Woodside Petroleum: Task 2(b)

VerifiedAdded on 2022/09/14

|7

|1878

|23

Homework Assignment

AI Summary

This document presents an inherent risk assessment for Woodside Petroleum, focusing on the susceptibility of material misstatement before considering any internal controls. The assessment analyzes various factors, including the nature of the client's business in the oil and gas industry, results of previous audits, the quantity of non-routine transactions, required estimates and judgments, and potential fraud risk factors. The analysis considers factors like the company's exploration plans, changes in the IT environment, and accounting procedures. The conclusion summarizes the overall inherent risk level as a combination of low, moderate, and high risks based on the evaluation of these factors. The document also includes references to relevant annual reports and auditing standards (ASA).

Assessment Task 2(b) Template – Overall inherent risk assessment.

You will find the template on the next page of this document (adapted from Exhibit 3-

8 in the Lakeside Company Case Study).

PLEASE read and follow these instructions carefully for filling in the template

AND inserting it in your Discussion Forum (DF) post.

You only need to complete (fill-in) the relevant blank columns of the Template –

there is no need to change ANY formatting, just fill-in the requested information.

There is no need to add your name anywhere because you will copy the template

into the DF post that automatically adds your name.

If you need more lines, the text you enter in the right hand column of the template

will automatically wrap … again, there is NO NEED to adjust any formatting!

MAKE SURE you pay attention to and follow the instructions (and additional

guidance) provided in the Assessment (Assignment) Task 2(b) folder in the

Once you have added the requested information to this Template:

1. SAVE a copy for your records;

2. Locate and open the DF post on which you nominated your chosen entity;

3. Choose to REPLY to your original post, select the completed TABLE on the

template and COPY the TABLE into the message.

You will find the template on the next page of this document (adapted from Exhibit 3-

8 in the Lakeside Company Case Study).

PLEASE read and follow these instructions carefully for filling in the template

AND inserting it in your Discussion Forum (DF) post.

You only need to complete (fill-in) the relevant blank columns of the Template –

there is no need to change ANY formatting, just fill-in the requested information.

There is no need to add your name anywhere because you will copy the template

into the DF post that automatically adds your name.

If you need more lines, the text you enter in the right hand column of the template

will automatically wrap … again, there is NO NEED to adjust any formatting!

MAKE SURE you pay attention to and follow the instructions (and additional

guidance) provided in the Assessment (Assignment) Task 2(b) folder in the

Once you have added the requested information to this Template:

1. SAVE a copy for your records;

2. Locate and open the DF post on which you nominated your chosen entity;

3. Choose to REPLY to your original post, select the completed TABLE on the

template and COPY the TABLE into the message.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

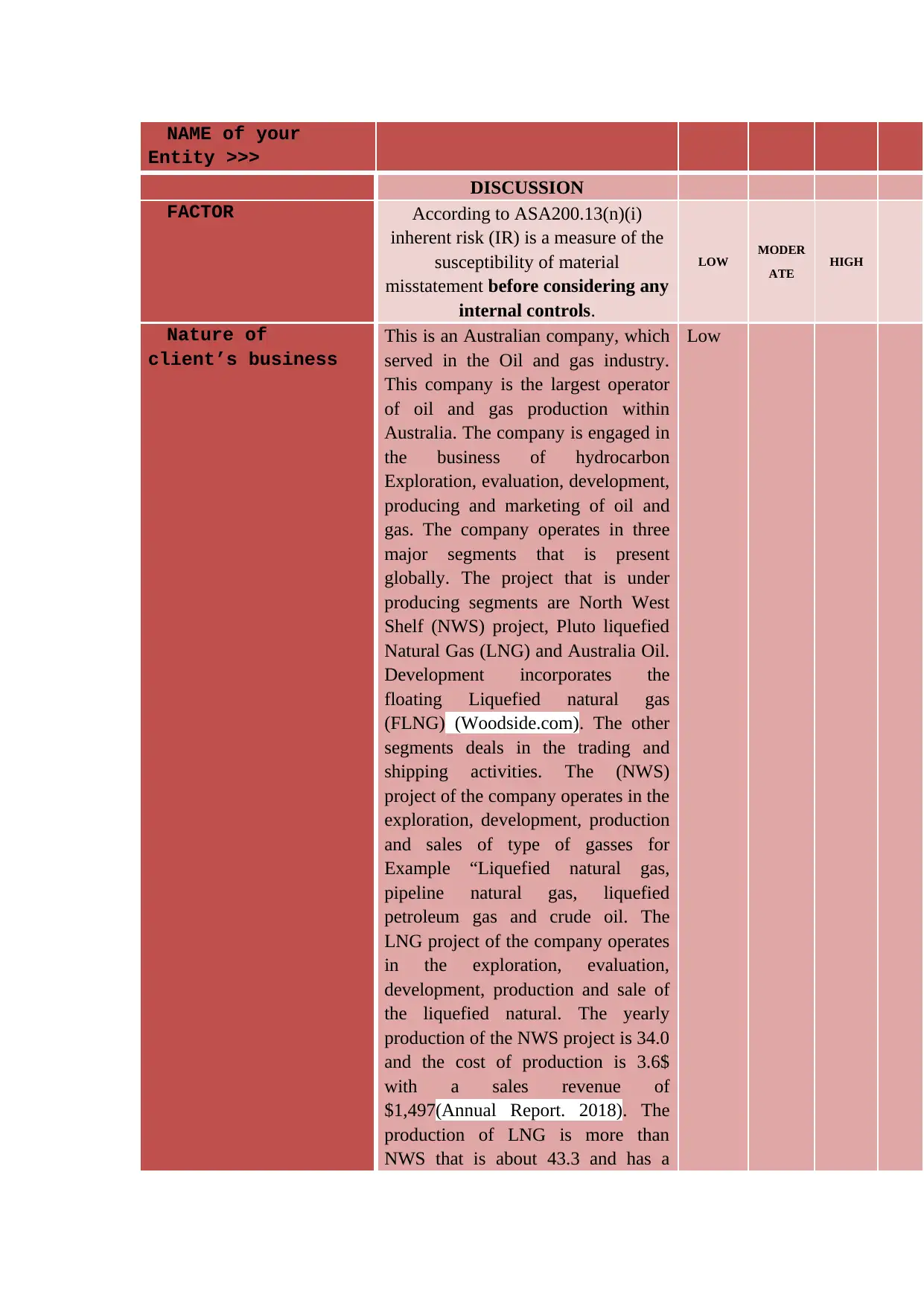

NAME of your

Entity >>>

DISCUSSION

FACTOR According to ASA200.13(n)(i)

inherent risk (IR) is a measure of the

susceptibility of material

misstatement before considering any

internal controls.

LOW MODER

ATE HIGH

Nature of

client’s business

This is an Australian company, which

served in the Oil and gas industry.

This company is the largest operator

of oil and gas production within

Australia. The company is engaged in

the business of hydrocarbon

Exploration, evaluation, development,

producing and marketing of oil and

gas. The company operates in three

major segments that is present

globally. The project that is under

producing segments are North West

Shelf (NWS) project, Pluto liquefied

Natural Gas (LNG) and Australia Oil.

Development incorporates the

floating Liquefied natural gas

(FLNG) (Woodside.com). The other

segments deals in the trading and

shipping activities. The (NWS)

project of the company operates in the

exploration, development, production

and sales of type of gasses for

Example “Liquefied natural gas,

pipeline natural gas, liquefied

petroleum gas and crude oil. The

LNG project of the company operates

in the exploration, evaluation,

development, production and sale of

the liquefied natural. The yearly

production of the NWS project is 34.0

and the cost of production is 3.6$

with a sales revenue of

$1,497(Annual Report. 2018). The

production of LNG is more than

NWS that is about 43.3 and has a

Low

Entity >>>

DISCUSSION

FACTOR According to ASA200.13(n)(i)

inherent risk (IR) is a measure of the

susceptibility of material

misstatement before considering any

internal controls.

LOW MODER

ATE HIGH

Nature of

client’s business

This is an Australian company, which

served in the Oil and gas industry.

This company is the largest operator

of oil and gas production within

Australia. The company is engaged in

the business of hydrocarbon

Exploration, evaluation, development,

producing and marketing of oil and

gas. The company operates in three

major segments that is present

globally. The project that is under

producing segments are North West

Shelf (NWS) project, Pluto liquefied

Natural Gas (LNG) and Australia Oil.

Development incorporates the

floating Liquefied natural gas

(FLNG) (Woodside.com). The other

segments deals in the trading and

shipping activities. The (NWS)

project of the company operates in the

exploration, development, production

and sales of type of gasses for

Example “Liquefied natural gas,

pipeline natural gas, liquefied

petroleum gas and crude oil. The

LNG project of the company operates

in the exploration, evaluation,

development, production and sale of

the liquefied natural. The yearly

production of the NWS project is 34.0

and the cost of production is 3.6$

with a sales revenue of

$1,497(Annual Report. 2018). The

production of LNG is more than

NWS that is about 43.3 and has a

Low

production cost of $3.6 with a sales

revenue of $2510. The capacity of the

project has also increased from 4.3 to

4.9 mtpa. The company produces 70

LNG cargoes out which all of them

are sols 9 cargoes on spot, and rest in

contracts. The company is focusing to

improve their NWS project as their

LNG project is operating well in the

market. The company also needs to

show a concern on their Natural gas

production and sales. The production

percentage is 86% and the sales

percentage is 80% which means the

company is not utilizing the full

production.

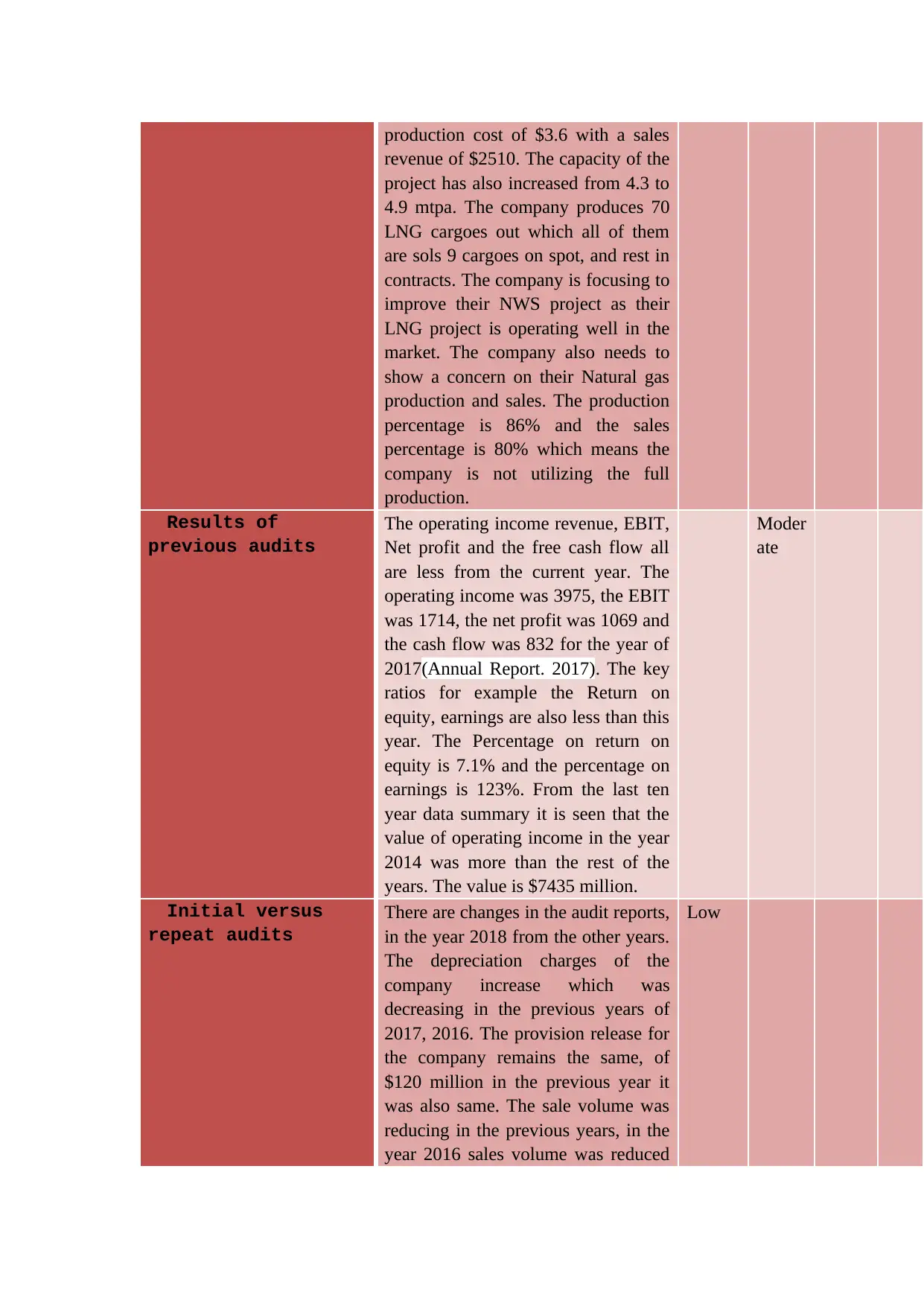

Results of

previous audits

The operating income revenue, EBIT,

Net profit and the free cash flow all

are less from the current year. The

operating income was 3975, the EBIT

was 1714, the net profit was 1069 and

the cash flow was 832 for the year of

2017(Annual Report. 2017). The key

ratios for example the Return on

equity, earnings are also less than this

year. The Percentage on return on

equity is 7.1% and the percentage on

earnings is 123%. From the last ten

year data summary it is seen that the

value of operating income in the year

2014 was more than the rest of the

years. The value is $7435 million.

Moder

ate

Initial versus

repeat audits

There are changes in the audit reports,

in the year 2018 from the other years.

The depreciation charges of the

company increase which was

decreasing in the previous years of

2017, 2016. The provision release for

the company remains the same, of

$120 million in the previous year it

was also same. The sale volume was

reducing in the previous years, in the

year 2016 sales volume was reduced

Low

revenue of $2510. The capacity of the

project has also increased from 4.3 to

4.9 mtpa. The company produces 70

LNG cargoes out which all of them

are sols 9 cargoes on spot, and rest in

contracts. The company is focusing to

improve their NWS project as their

LNG project is operating well in the

market. The company also needs to

show a concern on their Natural gas

production and sales. The production

percentage is 86% and the sales

percentage is 80% which means the

company is not utilizing the full

production.

Results of

previous audits

The operating income revenue, EBIT,

Net profit and the free cash flow all

are less from the current year. The

operating income was 3975, the EBIT

was 1714, the net profit was 1069 and

the cash flow was 832 for the year of

2017(Annual Report. 2017). The key

ratios for example the Return on

equity, earnings are also less than this

year. The Percentage on return on

equity is 7.1% and the percentage on

earnings is 123%. From the last ten

year data summary it is seen that the

value of operating income in the year

2014 was more than the rest of the

years. The value is $7435 million.

Moder

ate

Initial versus

repeat audits

There are changes in the audit reports,

in the year 2018 from the other years.

The depreciation charges of the

company increase which was

decreasing in the previous years of

2017, 2016. The provision release for

the company remains the same, of

$120 million in the previous year it

was also same. The sale volume was

reducing in the previous years, in the

year 2016 sales volume was reduced

Low

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by $831 million and the in the year

2017 by $392 million (Annual

Report. 2016). This year the sales

volume have increased. This shows

the company is repeating audits the

company is trying or focusing to the

increase the numbers which was

reducing and decreasing.

Quantity of non-

routine

transactions

The transaction that involves

accession and destruction of an asset

or business unit, accepting or

rejecting an effective business plan,

closing or opening of a plant all these

transaction comes under routine

transaction. The transactions like

Exploration and evaluation of assets,

differed tax rate, Interest bearing

liabilities, impairment loss,

Exploration and Evaluation written

off. PRRT received, Payments for the

restoration these are all the Non

routine transactions that have been

found from the financial statement of

2018 audit report of the Woodside

petroleum.

Moder

ate

Quantity of

estimates and

judgement required

for accounts

There are some accounts which

require accounting estimates and

judgements. The income tax that is

$2062 million in the year 2018

requires judgement and estimation as

due to the changes in the tax laws and

rates, affect the business (Coetzee and

Lube. 2014). The value of the

inventory may change daily as due to

the fluctuation in the market. The

accountants then estimate the value

by using Fifo and Lifo method and

they also keep a judgement in writing

down the value if the inventory

becomes outdated. The Depreciation

also require some financial estimation

requirements.

Moder

ate

Potential for The risk factors according to ASA high

2017 by $392 million (Annual

Report. 2016). This year the sales

volume have increased. This shows

the company is repeating audits the

company is trying or focusing to the

increase the numbers which was

reducing and decreasing.

Quantity of non-

routine

transactions

The transaction that involves

accession and destruction of an asset

or business unit, accepting or

rejecting an effective business plan,

closing or opening of a plant all these

transaction comes under routine

transaction. The transactions like

Exploration and evaluation of assets,

differed tax rate, Interest bearing

liabilities, impairment loss,

Exploration and Evaluation written

off. PRRT received, Payments for the

restoration these are all the Non

routine transactions that have been

found from the financial statement of

2018 audit report of the Woodside

petroleum.

Moder

ate

Quantity of

estimates and

judgement required

for accounts

There are some accounts which

require accounting estimates and

judgements. The income tax that is

$2062 million in the year 2018

requires judgement and estimation as

due to the changes in the tax laws and

rates, affect the business (Coetzee and

Lube. 2014). The value of the

inventory may change daily as due to

the fluctuation in the market. The

accountants then estimate the value

by using Fifo and Lifo method and

they also keep a judgement in writing

down the value if the inventory

becomes outdated. The Depreciation

also require some financial estimation

requirements.

Moder

ate

Potential for The risk factors according to ASA high

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fraudulent

financial reporting

& misappropriation

of assets (fraud

risk factors, see

ASA 240)

240 arising from the dishonest

financial reporting

(Legislation.gov.com). The economy,

industry or the operation of the entity

often threatens the company’s

financial position and stability. These

may occur dur to incapability of

generating cash flows from the

operation, facing difficulty in

adopting the new changes. Excessive

pressure on the management to meet

the goals of the organisation

(Johnstone, Grambling and

Rotenberg. 2013). Deficit in the

internal control components as the

high turnover rates and the internal

audit is not so effective. The risk

factors due to misappropriation of

Assets such as the Insufficient use of

keeping the records, insufficient in

safety of cash and inventory.

Deficiency in timely and completely

reconciliation of assets.

List any other

factors (can you

see any

illustrations in

your client’s

annual report of

the examples in ASA

315, Appendix 2 and

ASA 570.A2?)

The other factors that indicate risk

they are

Exploration plan in the business, as

the Woodside petroleum is having a

plan in exploration of their business

in Myanmar, Sengal, Gabon and Peru.

However if the business does not

operate well then the company will

have to incur a huge loss.

The relevant changes in the It

environment (Johansen and Peterson.

2013). The company planning to

some changes in the It department so

that can keep better control over the

business.

Lack of using appropriate methods of

accounting and analysing reporting

skills. The company is not using

appropriate methods for the

transaction. The complexity in the

Low

financial reporting

& misappropriation

of assets (fraud

risk factors, see

ASA 240)

240 arising from the dishonest

financial reporting

(Legislation.gov.com). The economy,

industry or the operation of the entity

often threatens the company’s

financial position and stability. These

may occur dur to incapability of

generating cash flows from the

operation, facing difficulty in

adopting the new changes. Excessive

pressure on the management to meet

the goals of the organisation

(Johnstone, Grambling and

Rotenberg. 2013). Deficit in the

internal control components as the

high turnover rates and the internal

audit is not so effective. The risk

factors due to misappropriation of

Assets such as the Insufficient use of

keeping the records, insufficient in

safety of cash and inventory.

Deficiency in timely and completely

reconciliation of assets.

List any other

factors (can you

see any

illustrations in

your client’s

annual report of

the examples in ASA

315, Appendix 2 and

ASA 570.A2?)

The other factors that indicate risk

they are

Exploration plan in the business, as

the Woodside petroleum is having a

plan in exploration of their business

in Myanmar, Sengal, Gabon and Peru.

However if the business does not

operate well then the company will

have to incur a huge loss.

The relevant changes in the It

environment (Johansen and Peterson.

2013). The company planning to

some changes in the It department so

that can keep better control over the

business.

Lack of using appropriate methods of

accounting and analysing reporting

skills. The company is not using

appropriate methods for the

transaction. The complexity in the

Low

accounting procedure they also make

the accounting wrong for the

company.

Conclusion:

Overall inherent

risk level

The above discussion come to a

conclusion with three low and three

moderate and one high risk level. The

nature of clients business, list of the

other factors and the initial versus low

report has a low risk. The reason

behind these is that the nature of

clients business is operating well the

audit reports shows the improvement

and the initial versus the previous

audit reports show that the initial

report improves a lot. The result of

the previous audit, the quantity of the

Non routine transaction, the quantity

of required estimates and judgement

inherits a moderate risk, the reason

behind this is that the quantity in non-

routine and the required estimation of

accounts of the entity has been

founded a lot which inherits a

moderate level of risk. The potential

for fraudulent risk factors is also there

for the company and the quantity for

these is more, so this why the level of

risk inherit is high.

References:

Annual Report 2017. (2017). Major Reports and Publications. [online] Woodside,

p.152. Available at:

https://files.woodside/docs/default-source/investor-documents/major-reports-(static-

pdfs)/14-02-2018-annual-report-2017.pdf?sfvrsn=a0f9590_14 [Accessed 31 Dec.

2017].

the accounting wrong for the

company.

Conclusion:

Overall inherent

risk level

The above discussion come to a

conclusion with three low and three

moderate and one high risk level. The

nature of clients business, list of the

other factors and the initial versus low

report has a low risk. The reason

behind these is that the nature of

clients business is operating well the

audit reports shows the improvement

and the initial versus the previous

audit reports show that the initial

report improves a lot. The result of

the previous audit, the quantity of the

Non routine transaction, the quantity

of required estimates and judgement

inherits a moderate risk, the reason

behind this is that the quantity in non-

routine and the required estimation of

accounts of the entity has been

founded a lot which inherits a

moderate level of risk. The potential

for fraudulent risk factors is also there

for the company and the quantity for

these is more, so this why the level of

risk inherit is high.

References:

Annual Report 2017. (2017). Major Reports and Publications. [online] Woodside,

p.152. Available at:

https://files.woodside/docs/default-source/investor-documents/major-reports-(static-

pdfs)/14-02-2018-annual-report-2017.pdf?sfvrsn=a0f9590_14 [Accessed 31 Dec.

2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Annual report. (2016). Major Reports and Publications. [online] Woodside, p.144.

Available at: https://files.woodside/docs/default-source/investor-documents/major-

reports-(static-pdfs)/01-03-2017-annual-report-2016.pdf?sfvrsn=39861556_8

[Accessed 31 Dec. 2016].

Annual Report. (2018). Major Reports and Publications. [online] Woodside, p.156.

Available at: https://files.woodside/docs/default-source/investor-documents/major-

reports-(static-pdfs)/annual-report-2018.pdf?sfvrsn=c9a46145_10 [Accessed 31 Dec.

2018].

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐

based internal audit engagements. International Journal of Auditing, 18(2), pp.115-

125.

Johansen, T.R. and Pettersson, K., 2013. The impact of board interlocks on auditor

choice and audit fees. Corporate Governance: An International Review, 21(3),

pp.287-310.

Johnstone, K., Gramling, A. and Rittenberg, L.E., 2013. Auditing: a risk-based

approach to conducting a quality audit. Cengage learning.

woodside.com (2019). Home. [online] Woodside. Available at:

https://www.woodside.com.au/ [Accessed 28 Aug. 2019].

www.legislation.gov (2006). Auditing Standard ASA 240 The Auditor's Responsibility

to Consider Fraud in an Audit of a Financial Report. [online] www.legislation.gov.

Available at: https://www.legislation.gov.au/Details/F2006L01368 [Accessed 28 Aug.

2019].

Available at: https://files.woodside/docs/default-source/investor-documents/major-

reports-(static-pdfs)/01-03-2017-annual-report-2016.pdf?sfvrsn=39861556_8

[Accessed 31 Dec. 2016].

Annual Report. (2018). Major Reports and Publications. [online] Woodside, p.156.

Available at: https://files.woodside/docs/default-source/investor-documents/major-

reports-(static-pdfs)/annual-report-2018.pdf?sfvrsn=c9a46145_10 [Accessed 31 Dec.

2018].

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐

based internal audit engagements. International Journal of Auditing, 18(2), pp.115-

125.

Johansen, T.R. and Pettersson, K., 2013. The impact of board interlocks on auditor

choice and audit fees. Corporate Governance: An International Review, 21(3),

pp.287-310.

Johnstone, K., Gramling, A. and Rittenberg, L.E., 2013. Auditing: a risk-based

approach to conducting a quality audit. Cengage learning.

woodside.com (2019). Home. [online] Woodside. Available at:

https://www.woodside.com.au/ [Accessed 28 Aug. 2019].

www.legislation.gov (2006). Auditing Standard ASA 240 The Auditor's Responsibility

to Consider Fraud in an Audit of a Financial Report. [online] www.legislation.gov.

Available at: https://www.legislation.gov.au/Details/F2006L01368 [Accessed 28 Aug.

2019].

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.