Selling vs Transferring Shares: Analysis for AP Spencer's Estate

VerifiedAdded on 2023/06/12

|6

|1445

|428

Report

AI Summary

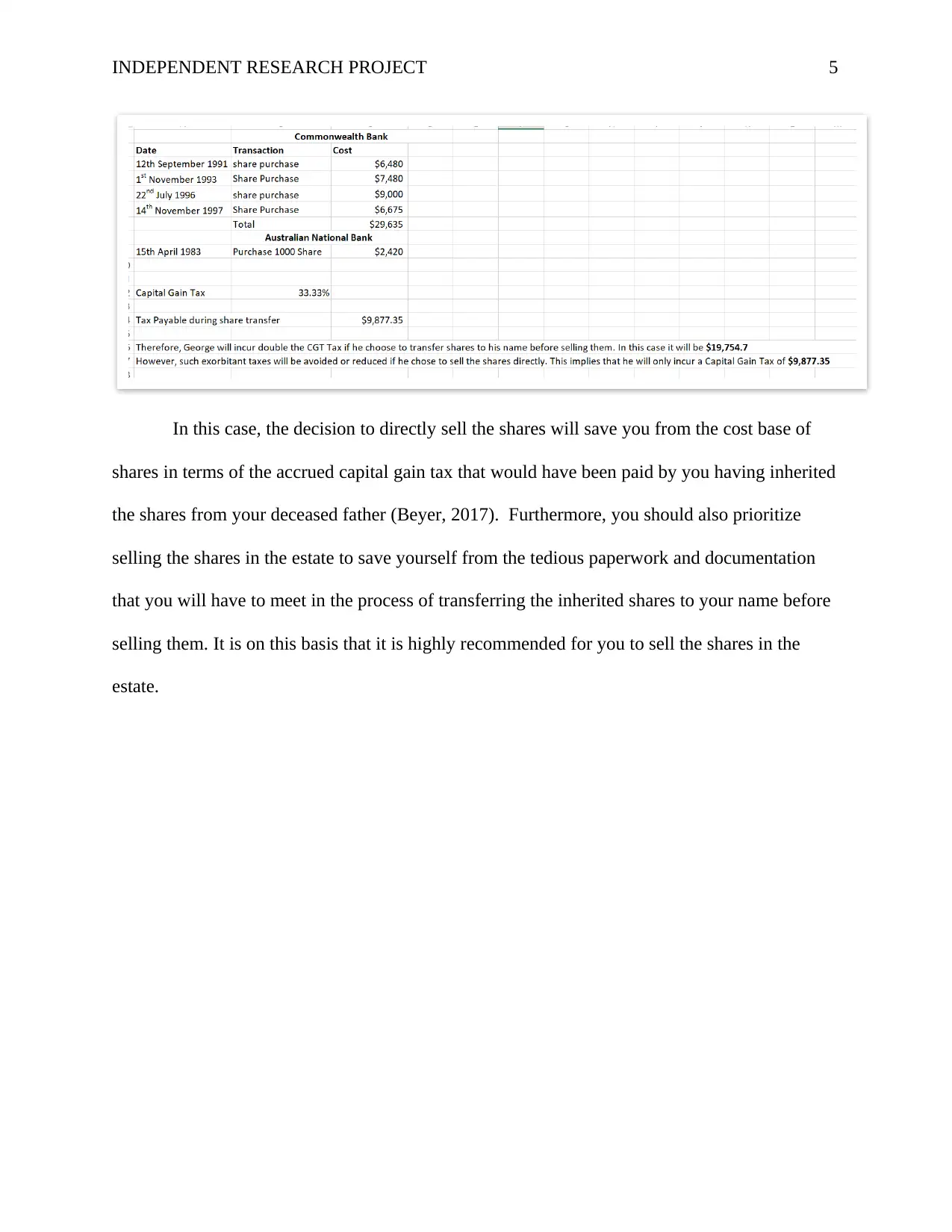

This report advises George Spencer, the sole executor and beneficiary of the AP Spencer Dec’d estate, on whether to sell inherited shares directly or transfer them to himself before selling. It highlights the tax implications, particularly capital gains tax (CGT), associated with both options. The report explains that shares purchased after September 20, 1985, are subject to CGT, and transferring shares before selling could lead to double taxation. It also notes the potential for inheriting the deceased's cost base. The analysis suggests that directly selling the shares would likely be more cost-effective and less burdensome in terms of paperwork, considering brokerage fees and other transaction costs. The recommendation is to sell the shares directly to minimize tax liabilities and streamline the process.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.