FPC004 - Strategic Management Accounting: Insurance Advice Assignment

VerifiedAdded on 2022/08/12

|14

|3574

|29

Homework Assignment

AI Summary

This assignment solution for FPC004, Strategic Management Accounting, delves into the nuances of insurance advice within the Australian context. Section A addresses pure and speculative risks, diversifiable and non-diversifiable risks, and the most significant laws governing the Australian insurance industry, including the Insurance Act 1973 and the Corporations Act 2001. It also examines the role of underwriters and the impact of premium increases on policyholders and the company's risk concentration. Section B provides a detailed analysis of Courtney's financial situation, calculating her life cover needs and recommending suitable premium strategies like hybrid premiums. It also explores additional personal insurance options such as trauma insurance, building insurance, and personal sickness and accident insurance. The solution outlines the client engagement process, including exploring client needs, recommending suitable insurance products, and determining premiums. The assignment further analyzes the tax implications of life insurance premiums, including deductibility for employers and employees. Finally, it explains trauma insurance, its benefits, exclusions, and available policy structures. This comprehensive solution provides a practical understanding of insurance advice, financial planning, and risk management.

Running head: FINANCE

FPC004 AS2 v6A1

Name of the Student

Name of the University

Author Note

FPC004 AS2 v6A1

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1STRATEGIC MANAGEMENT ACCOUNTING

Table of Contents

Section A......................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Section B......................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................7

Question 3....................................................................................................................................8

Question 4..................................................................................................................................10

References..................................................................................................................................13

Table of Contents

Section A......................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Section B......................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................7

Question 3....................................................................................................................................8

Question 4..................................................................................................................................10

References..................................................................................................................................13

2STRATEGIC MANAGEMENT ACCOUNTING

Section A

Question 1

a) A pure risk is a situation in which there is only the possibility of a loss or no loss being

incurred by the person undertaking the risk. Speculative risk is one where there is a

possibility of the taxpayer either earning a profit or a loss based on circumstances.

b) A diversifiable risk is one which can be avoided by changing the investments in the

portfolio of the investor. However, a non-diversifiable risk is inherent and cannot be

avoided by changing the portfolio.

c) Disability is a personal risk whereas investment in shares is a speculative risk. A

technological change is a diversifiable risk whereas inflation is a non-diversifiable risk.

Question 2

The most significant laws in the Australian insurance industry are the Insurance Act

1973, Insurance Contracts Act 1984, Insurance Contracts Amendment Act 2013 and

Corporations Act 2001. Insurance Act 1973 is a key act which sets the suitability guidelines for

the companies operating in the industry. If the customers feel that the company may be suffering

from an unsatisfactory management or an unsatisfactory financial position, this law may be

immediately called upon by them to protect their interests. Similarly, if a company winds up, it is

ensured that the interests of the policy holders are protected. The Insurance Contracts Act 1984

ensures that the correct information is provided by the insurance companies to the insured. If

there is any hidden information which is not properly communicated, the insured may call upon

this act. The Insurance Contracts Amendment Act 2013 states that the insured should avoid

misrepresenting themselves under any circumstances. Otherwise, it would result in the

cancellation of their contract and hence should be avoided in all circumstances. The Corporations

Section A

Question 1

a) A pure risk is a situation in which there is only the possibility of a loss or no loss being

incurred by the person undertaking the risk. Speculative risk is one where there is a

possibility of the taxpayer either earning a profit or a loss based on circumstances.

b) A diversifiable risk is one which can be avoided by changing the investments in the

portfolio of the investor. However, a non-diversifiable risk is inherent and cannot be

avoided by changing the portfolio.

c) Disability is a personal risk whereas investment in shares is a speculative risk. A

technological change is a diversifiable risk whereas inflation is a non-diversifiable risk.

Question 2

The most significant laws in the Australian insurance industry are the Insurance Act

1973, Insurance Contracts Act 1984, Insurance Contracts Amendment Act 2013 and

Corporations Act 2001. Insurance Act 1973 is a key act which sets the suitability guidelines for

the companies operating in the industry. If the customers feel that the company may be suffering

from an unsatisfactory management or an unsatisfactory financial position, this law may be

immediately called upon by them to protect their interests. Similarly, if a company winds up, it is

ensured that the interests of the policy holders are protected. The Insurance Contracts Act 1984

ensures that the correct information is provided by the insurance companies to the insured. If

there is any hidden information which is not properly communicated, the insured may call upon

this act. The Insurance Contracts Amendment Act 2013 states that the insured should avoid

misrepresenting themselves under any circumstances. Otherwise, it would result in the

cancellation of their contract and hence should be avoided in all circumstances. The Corporations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3STRATEGIC MANAGEMENT ACCOUNTING

Act 2001 states that the insurer should take utmost care about the situation of the insured and the

policy which is being formulated should not contain any form of deception in the insurance

contracts or the conduct of the company (Wood 2017).

Question 3

a) The main purpose of an underwriter is to provide the most appropriate policy for a

customer with the right amount of premium which does not make losses for the company.

If the family health history is not very healthy, then the risk of the patient suffering from

a disease is higher. Similarly, people involved in risky jobs like car racing have higher

risk of meeting with an accident. Drug abuse and health history also have a long term

impact on individuals. Hence, these are considered as determinants in the health of an

individual and need to be considered in the risk assessment procedures (Cornell et al.

2016).

b) The constant increase in premiums results in the policies becoming unfavourable to the

policy holders and they may opt out of the policy due to the higher costs. This will force

the company to lower its premiums to retain the customers for a long period of time.

However, reducing the premiums results in an increase in the risk concentration of the

company. Due to an increase in risk concentration, the claim costs, earnings volatility and

the profitability of the business all tend to go down. Hence, constantly increasing

premiums is not a profitable sign for the business (French, Vital and Minot 2015).

Act 2001 states that the insurer should take utmost care about the situation of the insured and the

policy which is being formulated should not contain any form of deception in the insurance

contracts or the conduct of the company (Wood 2017).

Question 3

a) The main purpose of an underwriter is to provide the most appropriate policy for a

customer with the right amount of premium which does not make losses for the company.

If the family health history is not very healthy, then the risk of the patient suffering from

a disease is higher. Similarly, people involved in risky jobs like car racing have higher

risk of meeting with an accident. Drug abuse and health history also have a long term

impact on individuals. Hence, these are considered as determinants in the health of an

individual and need to be considered in the risk assessment procedures (Cornell et al.

2016).

b) The constant increase in premiums results in the policies becoming unfavourable to the

policy holders and they may opt out of the policy due to the higher costs. This will force

the company to lower its premiums to retain the customers for a long period of time.

However, reducing the premiums results in an increase in the risk concentration of the

company. Due to an increase in risk concentration, the claim costs, earnings volatility and

the profitability of the business all tend to go down. Hence, constantly increasing

premiums is not a profitable sign for the business (French, Vital and Minot 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4STRATEGIC MANAGEMENT ACCOUNTING

Section B

Question 1

a)

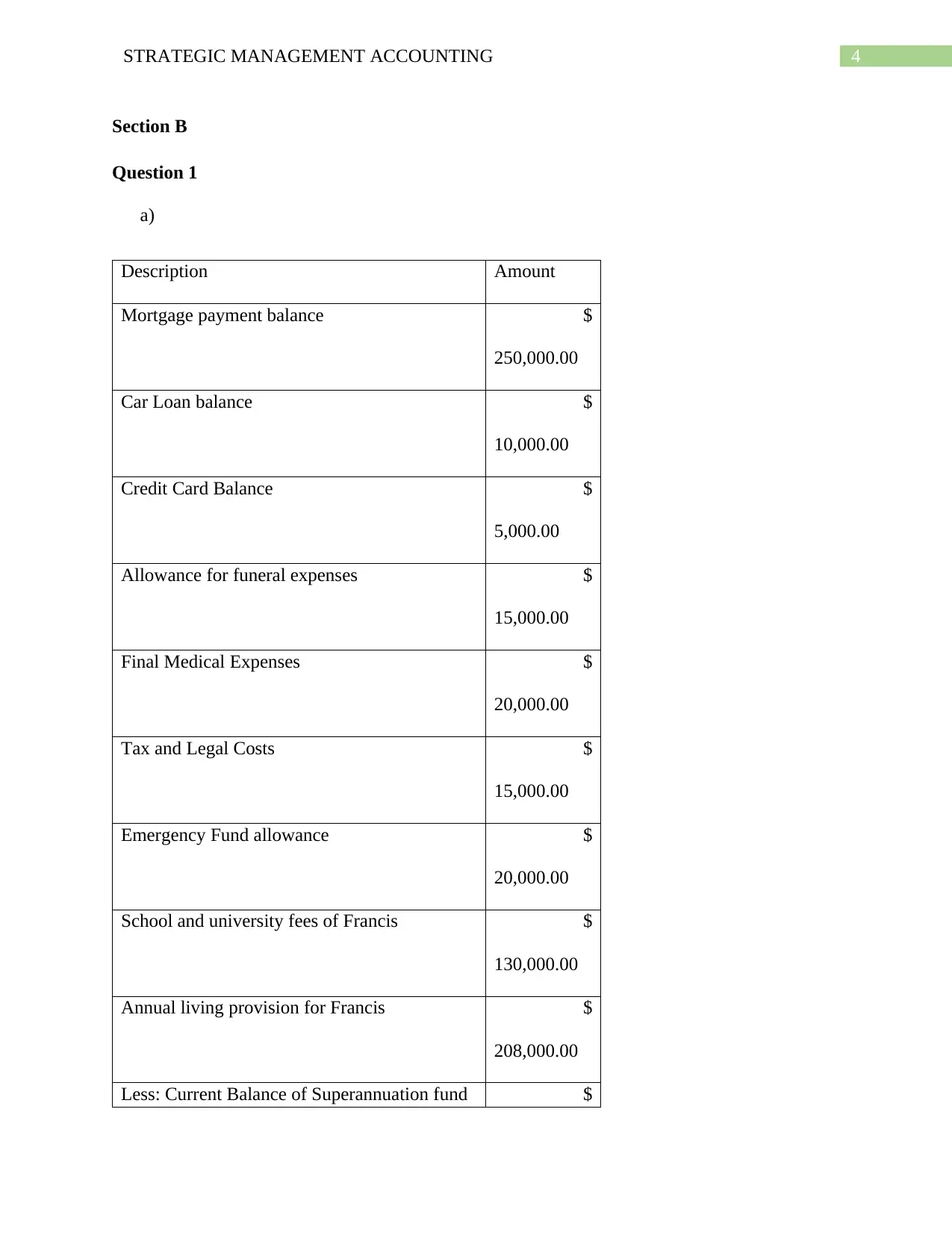

Description Amount

Mortgage payment balance $

250,000.00

Car Loan balance $

10,000.00

Credit Card Balance $

5,000.00

Allowance for funeral expenses $

15,000.00

Final Medical Expenses $

20,000.00

Tax and Legal Costs $

15,000.00

Emergency Fund allowance $

20,000.00

School and university fees of Francis $

130,000.00

Annual living provision for Francis $

208,000.00

Less: Current Balance of Superannuation fund $

Section B

Question 1

a)

Description Amount

Mortgage payment balance $

250,000.00

Car Loan balance $

10,000.00

Credit Card Balance $

5,000.00

Allowance for funeral expenses $

15,000.00

Final Medical Expenses $

20,000.00

Tax and Legal Costs $

15,000.00

Emergency Fund allowance $

20,000.00

School and university fees of Francis $

130,000.00

Annual living provision for Francis $

208,000.00

Less: Current Balance of Superannuation fund $

5STRATEGIC MANAGEMENT ACCOUNTING

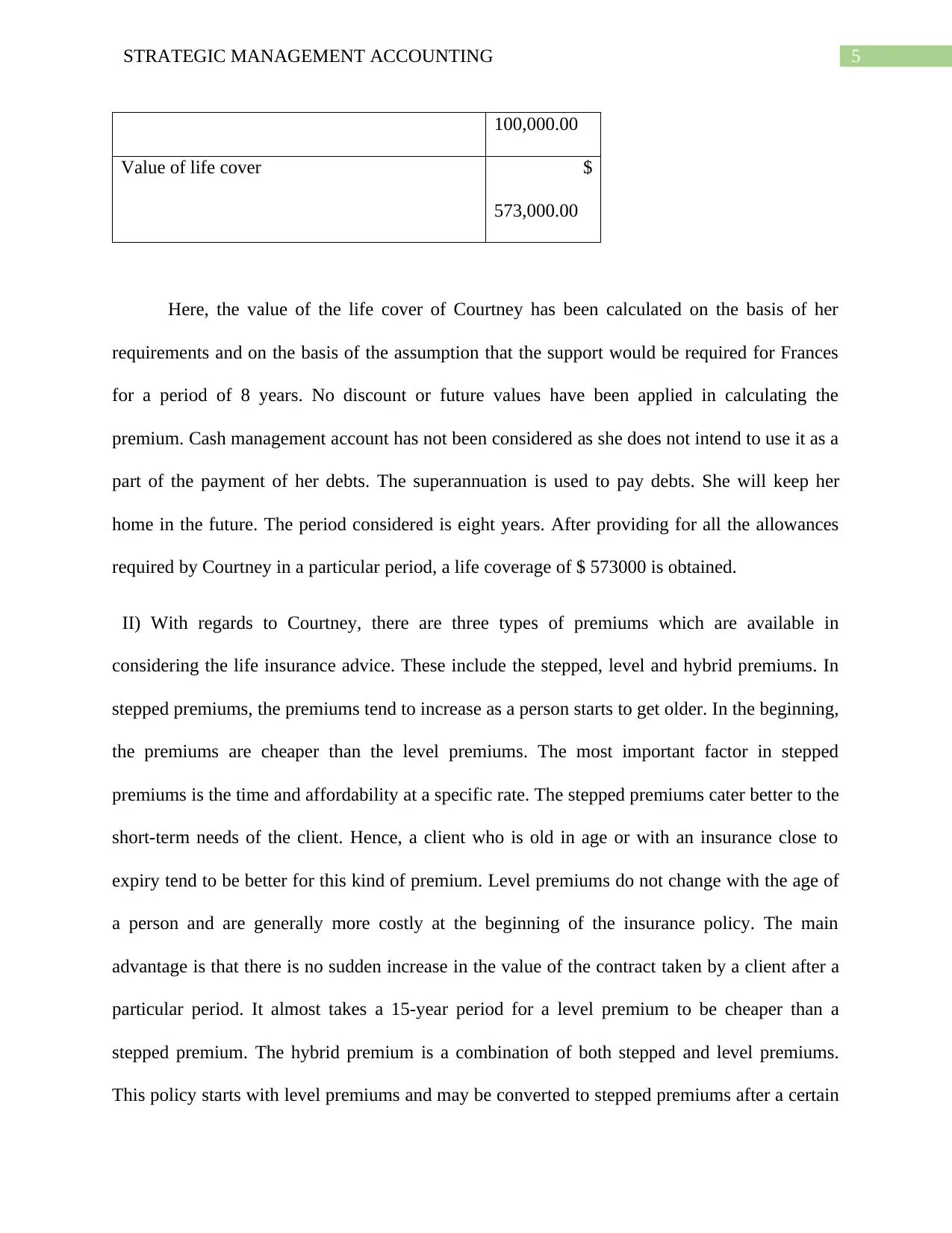

100,000.00

Value of life cover $

573,000.00

Here, the value of the life cover of Courtney has been calculated on the basis of her

requirements and on the basis of the assumption that the support would be required for Frances

for a period of 8 years. No discount or future values have been applied in calculating the

premium. Cash management account has not been considered as she does not intend to use it as a

part of the payment of her debts. The superannuation is used to pay debts. She will keep her

home in the future. The period considered is eight years. After providing for all the allowances

required by Courtney in a particular period, a life coverage of $ 573000 is obtained.

II) With regards to Courtney, there are three types of premiums which are available in

considering the life insurance advice. These include the stepped, level and hybrid premiums. In

stepped premiums, the premiums tend to increase as a person starts to get older. In the beginning,

the premiums are cheaper than the level premiums. The most important factor in stepped

premiums is the time and affordability at a specific rate. The stepped premiums cater better to the

short-term needs of the client. Hence, a client who is old in age or with an insurance close to

expiry tend to be better for this kind of premium. Level premiums do not change with the age of

a person and are generally more costly at the beginning of the insurance policy. The main

advantage is that there is no sudden increase in the value of the contract taken by a client after a

particular period. It almost takes a 15-year period for a level premium to be cheaper than a

stepped premium. The hybrid premium is a combination of both stepped and level premiums.

This policy starts with level premiums and may be converted to stepped premiums after a certain

100,000.00

Value of life cover $

573,000.00

Here, the value of the life cover of Courtney has been calculated on the basis of her

requirements and on the basis of the assumption that the support would be required for Frances

for a period of 8 years. No discount or future values have been applied in calculating the

premium. Cash management account has not been considered as she does not intend to use it as a

part of the payment of her debts. The superannuation is used to pay debts. She will keep her

home in the future. The period considered is eight years. After providing for all the allowances

required by Courtney in a particular period, a life coverage of $ 573000 is obtained.

II) With regards to Courtney, there are three types of premiums which are available in

considering the life insurance advice. These include the stepped, level and hybrid premiums. In

stepped premiums, the premiums tend to increase as a person starts to get older. In the beginning,

the premiums are cheaper than the level premiums. The most important factor in stepped

premiums is the time and affordability at a specific rate. The stepped premiums cater better to the

short-term needs of the client. Hence, a client who is old in age or with an insurance close to

expiry tend to be better for this kind of premium. Level premiums do not change with the age of

a person and are generally more costly at the beginning of the insurance policy. The main

advantage is that there is no sudden increase in the value of the contract taken by a client after a

particular period. It almost takes a 15-year period for a level premium to be cheaper than a

stepped premium. The hybrid premium is a combination of both stepped and level premiums.

This policy starts with level premiums and may be converted to stepped premiums after a certain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6STRATEGIC MANAGEMENT ACCOUNTING

point of time. This takes both the time period of the policy and the amount of premium which

needs to be paid into consideration. The best premium strategy for Courtney would be the hybrid

premium strategy.

III) The other personal insurance advice that would be provided to Courtney would include the

variety of policies which are available to her and should be undertaken by her to protect herself

better. The primary policy which can be undertaken by her is the trauma insurance. This would

protect her from unforeseen circumstances which result in her not being able to work for an

extended period of time. In order to compensate herself for the loss of the income, the trauma

insurance becomes a useful tool for protecting herself. The other policies which can be taken by

her include the Building Insurance which protects her home from any unforeseen circumstances

adversely impacting it. These include the indemnity and the replacement policy. The indemnity

policy tends to put an individual in a similar position which they were in prior to the occurrence

of the loss. The replacement policy substitutes an old house with a new house. As Courtney

intends to protect her house for her son’s usage, it becomes necessary that she safeguards the

existence of the house by taking a suitable insurance policy. The other policy which is relevant in

her case includes the Personal sickness and accident insurance. It is a policy which is beneficial

in the short run and is offered on account of a personal accident only. This policy is a good cover

for any sudden which limit the ability of the insured to work and earn income in the short run.

b) The first step of the process of advising the client is the client engagement. In this case,

the aim will be to establish a rapport with the client by making them comfortable during

the interaction. This will be done by giving them full attention and providing full

attention to what they are saying. After which, the focus will be shifted towards exploring

the needs of the client. Here, the particular needs of the individual client will be

point of time. This takes both the time period of the policy and the amount of premium which

needs to be paid into consideration. The best premium strategy for Courtney would be the hybrid

premium strategy.

III) The other personal insurance advice that would be provided to Courtney would include the

variety of policies which are available to her and should be undertaken by her to protect herself

better. The primary policy which can be undertaken by her is the trauma insurance. This would

protect her from unforeseen circumstances which result in her not being able to work for an

extended period of time. In order to compensate herself for the loss of the income, the trauma

insurance becomes a useful tool for protecting herself. The other policies which can be taken by

her include the Building Insurance which protects her home from any unforeseen circumstances

adversely impacting it. These include the indemnity and the replacement policy. The indemnity

policy tends to put an individual in a similar position which they were in prior to the occurrence

of the loss. The replacement policy substitutes an old house with a new house. As Courtney

intends to protect her house for her son’s usage, it becomes necessary that she safeguards the

existence of the house by taking a suitable insurance policy. The other policy which is relevant in

her case includes the Personal sickness and accident insurance. It is a policy which is beneficial

in the short run and is offered on account of a personal accident only. This policy is a good cover

for any sudden which limit the ability of the insured to work and earn income in the short run.

b) The first step of the process of advising the client is the client engagement. In this case,

the aim will be to establish a rapport with the client by making them comfortable during

the interaction. This will be done by giving them full attention and providing full

attention to what they are saying. After which, the focus will be shifted towards exploring

the needs of the client. Here, the particular needs of the individual client will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STRATEGIC MANAGEMENT ACCOUNTING

thoroughly understood. After which, the needs which have been found out will be

discussed with the client. This will be done to ensure that the needs which have been

identified are in line with the needs of the client and there are no significant differences in

the thought process. The insurance products which are suitable for a client will be

determined on the basis of the requirements of the client. In this case, they will include

the life cover, trauma insurance, personal sickness and accident cover and the building

insurance. In providing the advice about the products available, all the necessary

information will be shared with the client without hiding anything from them. Similarly,

the client’s agreement will be obtained by keeping their preferences in mind. No conflict

of interest would be entertained during the client interaction procedure. After this, the

premium for the policies would be determined by keeping the past medical history, nature

of the job and the lifestyle habits of the client in mind. The next step would be to

implement the decision of the client after arriving at the required amount of premium.

Finally, the interaction with the client would be closed after agreeing to their

requirements. The policies would be reviewed on a timely basis to understand the

changing requirements of the client and act upon them accordingly.

Question 2

a) I) The premium paid on the life insurance policy owned and purchased by the insured is

tax deductible for the employer. The FBT is assessable on the premium paid by the

employer on a life insurance policy.

II) The Income protection fund paid for by the employer will be deductible in the hands

of the employer. However, no tax benefits will be provided on the FBT paid on premium.

thoroughly understood. After which, the needs which have been found out will be

discussed with the client. This will be done to ensure that the needs which have been

identified are in line with the needs of the client and there are no significant differences in

the thought process. The insurance products which are suitable for a client will be

determined on the basis of the requirements of the client. In this case, they will include

the life cover, trauma insurance, personal sickness and accident cover and the building

insurance. In providing the advice about the products available, all the necessary

information will be shared with the client without hiding anything from them. Similarly,

the client’s agreement will be obtained by keeping their preferences in mind. No conflict

of interest would be entertained during the client interaction procedure. After this, the

premium for the policies would be determined by keeping the past medical history, nature

of the job and the lifestyle habits of the client in mind. The next step would be to

implement the decision of the client after arriving at the required amount of premium.

Finally, the interaction with the client would be closed after agreeing to their

requirements. The policies would be reviewed on a timely basis to understand the

changing requirements of the client and act upon them accordingly.

Question 2

a) I) The premium paid on the life insurance policy owned and purchased by the insured is

tax deductible for the employer. The FBT is assessable on the premium paid by the

employer on a life insurance policy.

II) The Income protection fund paid for by the employer will be deductible in the hands

of the employer. However, no tax benefits will be provided on the FBT paid on premium.

8STRATEGIC MANAGEMENT ACCOUNTING

III) The TPD and trauma policy premium owned and paid by an individual is not allowed

as a deduction in the hands of the taxpayer. Similarly, there are no deductions available

on the FBT paid on the premium of these products.

b) The premiums paid on life insurance policies are not tax deductible in two situations. One

of them is when the life insurance policy is owned by the individual and the premium for

it is paid by them. For example, if an individual owns an insurance policy for which they

make their own payments, no deductions are allowed for tax benefits. Similarly, there are

no tax deductions available for the TPD and Trauma insurance premiums owned by and

paid for by individuals.

Question 3

I. A trauma insurance provides the benefit of insurance when the insured suffers from life-

threatening conditions like heart attack, cancer, organ transplant and other similar

dangerous conditions. Some other terms used to describe this insurance include Critical

Illness Insurance, Living Insurance Illness or Major Illness Insurance. The Trauma

insurance pays a lump sum benefit to those suffering from an illness or an accident

meeting the criteria of the definition of the term trauma. Numerous events such as the

ones mentioned above and paralysis along with head bypass surgery are all covered under

the definition of the term trauma. The lump sum amount is paid to the insured on the

occurrence of any of the above mentioned events. It may be either fully or in partial.

However, there are a few exclusions from the Trauma Insurance policy. The claims are

not paid for deliberate, self-inflected acts or infections. For events such as cancer, heart

attack and a stroke, no cover is provided for the first 90 days of the occurrence.

III) The TPD and trauma policy premium owned and paid by an individual is not allowed

as a deduction in the hands of the taxpayer. Similarly, there are no deductions available

on the FBT paid on the premium of these products.

b) The premiums paid on life insurance policies are not tax deductible in two situations. One

of them is when the life insurance policy is owned by the individual and the premium for

it is paid by them. For example, if an individual owns an insurance policy for which they

make their own payments, no deductions are allowed for tax benefits. Similarly, there are

no tax deductions available for the TPD and Trauma insurance premiums owned by and

paid for by individuals.

Question 3

I. A trauma insurance provides the benefit of insurance when the insured suffers from life-

threatening conditions like heart attack, cancer, organ transplant and other similar

dangerous conditions. Some other terms used to describe this insurance include Critical

Illness Insurance, Living Insurance Illness or Major Illness Insurance. The Trauma

insurance pays a lump sum benefit to those suffering from an illness or an accident

meeting the criteria of the definition of the term trauma. Numerous events such as the

ones mentioned above and paralysis along with head bypass surgery are all covered under

the definition of the term trauma. The lump sum amount is paid to the insured on the

occurrence of any of the above mentioned events. It may be either fully or in partial.

However, there are a few exclusions from the Trauma Insurance policy. The claims are

not paid for deliberate, self-inflected acts or infections. For events such as cancer, heart

attack and a stroke, no cover is provided for the first 90 days of the occurrence.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9STRATEGIC MANAGEMENT ACCOUNTING

II. There are four policy structures available in relation to the trauma insurance policies. One

of them is an optional rider benefit along with an endowment or a whole-of-life policy. If

there is a payment for a trauma benefit, then the payment would be considered as an

advancement of the payment of the policy benefits and the policy ends there. It is also

available as an optional rider benefit with that of a term life insurance policy. In this

situation as well, the payment of the trauma benefit is considered as an advancement of

the payment of the policy benefits. However, if the amount of payment is lower than the

benefit amount, then the policy continues with the remaining cover as the policy amount.

Some policies also have the term benefits separate from the death benefit. In these cases,

the payment made for the trauma does not impact the death benefit payment in any

manner. The option of ‘buyback’ is also available to the insured where the amount

reduced in the death benefit can be reinstated by the payment of a predetermined set of

amounts. There is also the option of standalone insurance payments where the policy

ends with the payment of the insurance sums.

III. The policy benefits available in a trauma insurance are the sum benefits paid to the

insured suffering from an illness or an accident meeting with the criteria of trauma

defined in the policy. Some of the circumstances under which the policy benefits are paid

to the insured individual include a heart attack, stroke, cancer, heart bypass surgery,

paralysis or a major head trauma. However, the full amount of payment is not made

under all circumstances. These include less serious events such as carcinoma in situ as

well as partial blindness. Only partial payments are made in this regard. The other

significant payments include the advance payments. These payments are made when

there is a diagnosis of specific chronic and progressive events such as multiple sclerosis

II. There are four policy structures available in relation to the trauma insurance policies. One

of them is an optional rider benefit along with an endowment or a whole-of-life policy. If

there is a payment for a trauma benefit, then the payment would be considered as an

advancement of the payment of the policy benefits and the policy ends there. It is also

available as an optional rider benefit with that of a term life insurance policy. In this

situation as well, the payment of the trauma benefit is considered as an advancement of

the payment of the policy benefits. However, if the amount of payment is lower than the

benefit amount, then the policy continues with the remaining cover as the policy amount.

Some policies also have the term benefits separate from the death benefit. In these cases,

the payment made for the trauma does not impact the death benefit payment in any

manner. The option of ‘buyback’ is also available to the insured where the amount

reduced in the death benefit can be reinstated by the payment of a predetermined set of

amounts. There is also the option of standalone insurance payments where the policy

ends with the payment of the insurance sums.

III. The policy benefits available in a trauma insurance are the sum benefits paid to the

insured suffering from an illness or an accident meeting with the criteria of trauma

defined in the policy. Some of the circumstances under which the policy benefits are paid

to the insured individual include a heart attack, stroke, cancer, heart bypass surgery,

paralysis or a major head trauma. However, the full amount of payment is not made

under all circumstances. These include less serious events such as carcinoma in situ as

well as partial blindness. Only partial payments are made in this regard. The other

significant payments include the advance payments. These payments are made when

there is a diagnosis of specific chronic and progressive events such as multiple sclerosis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10STRATEGIC MANAGEMENT ACCOUNTING

and cardiomyopathy. In order to ensure that the benefits paid to a consumer meet their

requirements, the policy amount is annually adjusted for inflation and by keeping the CPI

in consideration.

Question 4

a) The main difference between personal sickness and accident (PS&A) insurance and life

insurance products is the people authorised with issuing them. The PS&A products are

issued by general insurers while life insurance products like income protection and

trauma insurance policies are offered by the life insurance companies. Due to the PS&A

products being indemnity-styled, the benefits from the PS&A products will be subject to

the change in the income of the insured individual. However, life insurance products like

income protection insurance can be taken on a predetermined basis. This means that the

level of policy benefits received by the insured will remain the same as the ones which

were agreed upon at the time of agreeing the policy. The life insurance products usually

pay out all the money to the beneficiaries in case of the death of the insured. However,

some PS&A policies tend to pay the lump sum amount of the policy only if the death of

an individual happens as the result of an accident. Trauma cover tends to pay out a lump

sum benefit on the diagnosis of an event classified as trauma such as cancer, paralysis or

a heart condition, regardless of whether the person is able to return to the work due to the

trauma or not. PS&A products, however, make the required payments only if there is a

loss of income on a weekly or monthly basis as a result of the trauma. PS&A products

usually provide cover for 100% of the weekly income, whereas income protection

products tend to cover only up to 75% of the income lost by the individual. The timing

for which the benefits are received by the individuals also differ amongst the products.

and cardiomyopathy. In order to ensure that the benefits paid to a consumer meet their

requirements, the policy amount is annually adjusted for inflation and by keeping the CPI

in consideration.

Question 4

a) The main difference between personal sickness and accident (PS&A) insurance and life

insurance products is the people authorised with issuing them. The PS&A products are

issued by general insurers while life insurance products like income protection and

trauma insurance policies are offered by the life insurance companies. Due to the PS&A

products being indemnity-styled, the benefits from the PS&A products will be subject to

the change in the income of the insured individual. However, life insurance products like

income protection insurance can be taken on a predetermined basis. This means that the

level of policy benefits received by the insured will remain the same as the ones which

were agreed upon at the time of agreeing the policy. The life insurance products usually

pay out all the money to the beneficiaries in case of the death of the insured. However,

some PS&A policies tend to pay the lump sum amount of the policy only if the death of

an individual happens as the result of an accident. Trauma cover tends to pay out a lump

sum benefit on the diagnosis of an event classified as trauma such as cancer, paralysis or

a heart condition, regardless of whether the person is able to return to the work due to the

trauma or not. PS&A products, however, make the required payments only if there is a

loss of income on a weekly or monthly basis as a result of the trauma. PS&A products

usually provide cover for 100% of the weekly income, whereas income protection

products tend to cover only up to 75% of the income lost by the individual. The timing

for which the benefits are received by the individuals also differ amongst the products.

11STRATEGIC MANAGEMENT ACCOUNTING

Under PS&A products, the claims can be made only for short periods whereas the

life insurance products provide the cover for longer periods, i.e. up to the retirement of

the individual. The PS&A policies can be cancelled by the insurer but the life insurance

products can only be cancelled by the insured. In case of situations like the change in the

occupation of the insured and the increase in the risk in the new occupation, the insurer

may opt to cancel the insurance of the individual. However, in case of life insurance

products, there is a guarantee of renewal if there is a timely payment of the premiums of

the policies. PS&A policies are more suitable for the short term whereas the life

insurance products are suitable for the long run. The nature of PS&A policies is generally

simple and hence there is no requirement of medical underwriting. The premiums in these

policies are low and make it viable for people who had their claims rejected in the past.

The underwriting process in Income protection insurance is extremely detailed and hence

the cost of the premium also goes up. This results in the rejection of some life insurance

policies at the time of screening.

b) The three distinct group of people who generally benefit from the PS&A insurance cover

are the employees, contract workers and the people who do not qualify for insurance

under the Income Protection scheme (McCrossan 2017). Employees tend to depend on

the salaries received by them during the course of employment to make a living.

However, there may occur short term accidents which restrict their ability to work in the

short run. In these cases, it becomes essential for the employees to not lose their income

for the period for which they are unable to work. In cases like these, the short term

insurance helps them recover their complete pay for a period without losing any of it.

Under PS&A products, the claims can be made only for short periods whereas the

life insurance products provide the cover for longer periods, i.e. up to the retirement of

the individual. The PS&A policies can be cancelled by the insurer but the life insurance

products can only be cancelled by the insured. In case of situations like the change in the

occupation of the insured and the increase in the risk in the new occupation, the insurer

may opt to cancel the insurance of the individual. However, in case of life insurance

products, there is a guarantee of renewal if there is a timely payment of the premiums of

the policies. PS&A policies are more suitable for the short term whereas the life

insurance products are suitable for the long run. The nature of PS&A policies is generally

simple and hence there is no requirement of medical underwriting. The premiums in these

policies are low and make it viable for people who had their claims rejected in the past.

The underwriting process in Income protection insurance is extremely detailed and hence

the cost of the premium also goes up. This results in the rejection of some life insurance

policies at the time of screening.

b) The three distinct group of people who generally benefit from the PS&A insurance cover

are the employees, contract workers and the people who do not qualify for insurance

under the Income Protection scheme (McCrossan 2017). Employees tend to depend on

the salaries received by them during the course of employment to make a living.

However, there may occur short term accidents which restrict their ability to work in the

short run. In these cases, it becomes essential for the employees to not lose their income

for the period for which they are unable to work. In cases like these, the short term

insurance helps them recover their complete pay for a period without losing any of it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.