Comprehensive Insurance Assignment for FNSR2101 Course

VerifiedAdded on 2022/10/10

|9

|1907

|10

Homework Assignment

AI Summary

This assignment solution for an Introduction to Insurance course comprehensively addresses key concepts within the field. It begins by differentiating between insurable and non-insurable risks, providing examples such as property damage, genetic defects, and gambling losses. The solution then explores the societal benefits of insurance, including wealth protection, social harmony, and enhanced living standards. It delves into physical hazards, reinsurance benefits, and contract formation, analyzing scenarios involving advertising, vehicle ownership, and burglary insurance. The assignment further examines legal positions of insurers, mortgage clauses, policy cancellation, and the application of coinsurance formulas to determine loss payments, providing a thorough understanding of insurance principles and practices. References to relevant literature support the analysis.

Running Head: INSURANCE 1

INSURANCE

INSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSURANCE

Table of Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................4

Protects the wealth of society..................................................................................................................4

Eliminates the social evil.........................................................................................................................4

Helps in enhancing the standard of living................................................................................................4

The benefits also accounts for the social security benefits.......................................................................5

Equitable distribution of loss...................................................................................................................5

Question 3...............................................................................................................................................5

Question 4...............................................................................................................................................5

PART II.......................................................................................................................................................6

Question 5...............................................................................................................................................6

Question 6...............................................................................................................................................6

Question 7...............................................................................................................................................6

Question 8...............................................................................................................................................7

Part III.........................................................................................................................................................7

Question 9...............................................................................................................................................7

Question 10.............................................................................................................................................7

Question 11.................................................................................................................................................8

References...................................................................................................................................................9

Table of Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................4

Protects the wealth of society..................................................................................................................4

Eliminates the social evil.........................................................................................................................4

Helps in enhancing the standard of living................................................................................................4

The benefits also accounts for the social security benefits.......................................................................5

Equitable distribution of loss...................................................................................................................5

Question 3...............................................................................................................................................5

Question 4...............................................................................................................................................5

PART II.......................................................................................................................................................6

Question 5...............................................................................................................................................6

Question 6...............................................................................................................................................6

Question 7...............................................................................................................................................6

Question 8...............................................................................................................................................7

Part III.........................................................................................................................................................7

Question 9...............................................................................................................................................7

Question 10.............................................................................................................................................7

Question 11.................................................................................................................................................8

References...................................................................................................................................................9

Running Head: INSURANCE

Question 1

A

Rusting of an unprotected structure can be considered as the insurable risk as the damage

to the property can be insured and it also falls down in the parameters of the insurance company.

The property can be insured up to the amount of the loss (Zuo & Hang, 2018).

B

A genetic defect affects 9 of 10 new born males in a family can be cured and cannot be

cured. The insurance companies generally take the decisions on the basis of the level of the risk

associated with the disease can be cured or not. Hence, some considers it as a insurable risk, only

to the extent of the preliminary stage (Andrews, 2015).

C

Developing a cancer can be insured but only to a particular stage. It has been observed in

many policies that the organs are covered by the insurance policy, even the payment of the

dialysis can be made, however the payment for the cancer will be made only when the tumor

reflects the uncontrolled growth. The future premiums are not waived. Hence, it is considered as

non-insurable risk (Soni, Sabik, Simon & Sommers, 2018).

D

Eventual obsolescence of a personal computer can be insured under the Oriental

Insurance company limited. The electronic equipment is insured and protects the Owner, Lessor

Question 1

A

Rusting of an unprotected structure can be considered as the insurable risk as the damage

to the property can be insured and it also falls down in the parameters of the insurance company.

The property can be insured up to the amount of the loss (Zuo & Hang, 2018).

B

A genetic defect affects 9 of 10 new born males in a family can be cured and cannot be

cured. The insurance companies generally take the decisions on the basis of the level of the risk

associated with the disease can be cured or not. Hence, some considers it as a insurable risk, only

to the extent of the preliminary stage (Andrews, 2015).

C

Developing a cancer can be insured but only to a particular stage. It has been observed in

many policies that the organs are covered by the insurance policy, even the payment of the

dialysis can be made, however the payment for the cancer will be made only when the tumor

reflects the uncontrolled growth. The future premiums are not waived. Hence, it is considered as

non-insurable risk (Soni, Sabik, Simon & Sommers, 2018).

D

Eventual obsolescence of a personal computer can be insured under the Oriental

Insurance company limited. The electronic equipment is insured and protects the Owner, Lessor

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: INSURANCE

and hirer. The computer and the allied peripherals and the other auxiliary equipment are also

insured.

E

Losing money at Casino comes under the activity of the gambling. Gambling process is

purely based on the luck factor and the calculative instincts. The company cannot insure an

individual just on the basis of the loss incurred while gambling and speculation. Hence, it is not

an insurable risk.

Question 2

The five benefits of the insurance to the society are discussed in detail to have an in-depth

understanding.

Protects the wealth of society

The major benefit of the insurance is that it provides the safety and the security to the

individuals and the members of the society. For example the life insurance that offers the

protection against the wealth.

Eliminates the social evil

There are different forms of the insurance, and the major focus is on the elimination of

the evils. When the social evil is solved there will be more harmony and peace. The social

aspects play vital roles in the overall development of the society and hence, it is also considered

as one of the major benefits.

and hirer. The computer and the allied peripherals and the other auxiliary equipment are also

insured.

E

Losing money at Casino comes under the activity of the gambling. Gambling process is

purely based on the luck factor and the calculative instincts. The company cannot insure an

individual just on the basis of the loss incurred while gambling and speculation. Hence, it is not

an insurable risk.

Question 2

The five benefits of the insurance to the society are discussed in detail to have an in-depth

understanding.

Protects the wealth of society

The major benefit of the insurance is that it provides the safety and the security to the

individuals and the members of the society. For example the life insurance that offers the

protection against the wealth.

Eliminates the social evil

There are different forms of the insurance, and the major focus is on the elimination of

the evils. When the social evil is solved there will be more harmony and peace. The social

aspects play vital roles in the overall development of the society and hence, it is also considered

as one of the major benefits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSURANCE

Helps in enhancing the standard of living

The insurance helps in the enhancement of the standard of the living. The high returns

are available to the insurers that lower the ideals of the communities.

The benefits also accounts for the social security benefits

Insurance plays a vital role in the fulfilling the certain needs for which the state might

have to provide. The social benefits for the old age, sickness and disability are the general gains

that are being accounted (Casaburi & Willis, 2018).

Equitable distribution of loss

Insurance also helps in the distribution of the costs in the parallel manner. In the absence

of the insurance it becomes difficult in the haphazard manner. The basic problem occurs when

the amount is included in the higher rent than others (ELECTRONIC EQUIPMENT

INSURANCE (EEI), 2018).

Question 3

The physical hazard is an agent, which can cause with or without harm. They can be

classified as the type of occasional hazard or the environmental hazard (Alberta Health, 2018).

The examples of the physical hazard are lighting conditions, working with high voltage

equipment, working at heights, overhead hazards, fast moving equipment, temperature extremes,

blocked walkaways and exposure to the electromagnetic fields (Dixon, Christensen & Duncan,

2018).

Question 4

The two major benefits that are listed in this assignment are to increase the capacity to write the

business whereas to maintain a reserve of liability balance.

Helps in enhancing the standard of living

The insurance helps in the enhancement of the standard of the living. The high returns

are available to the insurers that lower the ideals of the communities.

The benefits also accounts for the social security benefits

Insurance plays a vital role in the fulfilling the certain needs for which the state might

have to provide. The social benefits for the old age, sickness and disability are the general gains

that are being accounted (Casaburi & Willis, 2018).

Equitable distribution of loss

Insurance also helps in the distribution of the costs in the parallel manner. In the absence

of the insurance it becomes difficult in the haphazard manner. The basic problem occurs when

the amount is included in the higher rent than others (ELECTRONIC EQUIPMENT

INSURANCE (EEI), 2018).

Question 3

The physical hazard is an agent, which can cause with or without harm. They can be

classified as the type of occasional hazard or the environmental hazard (Alberta Health, 2018).

The examples of the physical hazard are lighting conditions, working with high voltage

equipment, working at heights, overhead hazards, fast moving equipment, temperature extremes,

blocked walkaways and exposure to the electromagnetic fields (Dixon, Christensen & Duncan,

2018).

Question 4

The two major benefits that are listed in this assignment are to increase the capacity to write the

business whereas to maintain a reserve of liability balance.

Running Head: INSURANCE

Since reinsurance expands the guaranteeing limit of an essential guarantor, the essential back up

plan can sell approaches that typically it would not acknowledge in light of the fact that as far as

possible is over the safety net provider's maintenance limit it increases the capacity of the

insurer. In the second situation when the policy is being sold by the insurer as stipulated by the

unearned part of the premium is transferred to the reserve or the liability account and the same

cannot be used for paying the expenses.

PART II

Question 5

The contract has not been formed with the Brown’s acceptance as the essentials of the

valid contract are mot formed by Brown. The ad has been running for ten days yet the acceptance

has not been received from the John Smith. Generally the, advertisements are treated as the

invitation to treat. Hence, the contract is not a valid contract (Smits, 2017).

Question 6

According to the rule of the ownership and the operation of the vehicle it’s mandatory for

the operating and the owner of the vehicle. The right fact and the information of were not

delivered by the client and at the same time the broker also violated the concept of the due

diligence. Hence, the liability is on the part of both the owners and the clients as well. Hence,

these are the issues that have been accounted for (Hoffman & Eigen, 2017).

Question 7

In case of the Burglary insurance the protection is provided against damage caused by the

burglary. In the current scenario Mr. White’s store must have been covered by the alarm from the

Since reinsurance expands the guaranteeing limit of an essential guarantor, the essential back up

plan can sell approaches that typically it would not acknowledge in light of the fact that as far as

possible is over the safety net provider's maintenance limit it increases the capacity of the

insurer. In the second situation when the policy is being sold by the insurer as stipulated by the

unearned part of the premium is transferred to the reserve or the liability account and the same

cannot be used for paying the expenses.

PART II

Question 5

The contract has not been formed with the Brown’s acceptance as the essentials of the

valid contract are mot formed by Brown. The ad has been running for ten days yet the acceptance

has not been received from the John Smith. Generally the, advertisements are treated as the

invitation to treat. Hence, the contract is not a valid contract (Smits, 2017).

Question 6

According to the rule of the ownership and the operation of the vehicle it’s mandatory for

the operating and the owner of the vehicle. The right fact and the information of were not

delivered by the client and at the same time the broker also violated the concept of the due

diligence. Hence, the liability is on the part of both the owners and the clients as well. Hence,

these are the issues that have been accounted for (Hoffman & Eigen, 2017).

Question 7

In case of the Burglary insurance the protection is provided against damage caused by the

burglary. In the current scenario Mr. White’s store must have been covered by the alarm from the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: INSURANCE

protection and ABV will not honor the claim as it was the main requirement. Protection is the

necessity, more than the requirement hence, coverage is not available.

Question 8

The legal position of the insurer is to advice the client about the conditions that are covered

within the purchase of the vehicle. The staff adjuster must have informed before the repairs have

been done on the vehicle. The policy shall be properly read by the client and is the loss could not

have been covered it should have been mentioned clearly. Hence the insurer must distribute the

liability legally between the staff adjuster and the owner of the vehicle (Smits, 2017).

Part III

Question 9

Mortgagee is the lender in the process of the mortgage. This could be the bank, building

society, savings and association of the loan. The provision and the conditions included in the

clause of the mortgage is the transfer of the interest in a specific immovable property, for

securing the funds in the advance through the way of loan. The sections governing the Mortgage

are 54 to 104 of the Transfer of the property Act, 1882. The different types of the mortgage are

also provided in the sections which are simple mortgage, mortgage by conditional sale,

usufructuary mortgage, and equitable mortgage. There is no provision in the mortgage that can

be used to prevent or cease the redemption (Gay, ET AL 2015).

Question 10

The first named insured has the right to cancel the policy at any time via mail or

delivering the written notice to the insurer. The condition is such that the notice must be

provided "in advance." This means that if the owner wishes to make the cancellation on a

protection and ABV will not honor the claim as it was the main requirement. Protection is the

necessity, more than the requirement hence, coverage is not available.

Question 8

The legal position of the insurer is to advice the client about the conditions that are covered

within the purchase of the vehicle. The staff adjuster must have informed before the repairs have

been done on the vehicle. The policy shall be properly read by the client and is the loss could not

have been covered it should have been mentioned clearly. Hence the insurer must distribute the

liability legally between the staff adjuster and the owner of the vehicle (Smits, 2017).

Part III

Question 9

Mortgagee is the lender in the process of the mortgage. This could be the bank, building

society, savings and association of the loan. The provision and the conditions included in the

clause of the mortgage is the transfer of the interest in a specific immovable property, for

securing the funds in the advance through the way of loan. The sections governing the Mortgage

are 54 to 104 of the Transfer of the property Act, 1882. The different types of the mortgage are

also provided in the sections which are simple mortgage, mortgage by conditional sale,

usufructuary mortgage, and equitable mortgage. There is no provision in the mortgage that can

be used to prevent or cease the redemption (Gay, ET AL 2015).

Question 10

The first named insured has the right to cancel the policy at any time via mail or

delivering the written notice to the insurer. The condition is such that the notice must be

provided "in advance." This means that if the owner wishes to make the cancellation on a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSURANCE

specified date, the notification shall be provided to the insurer before the date. The termination is

invalid as the cancellation has been done whereas the mail has been sent later on (Arena, Myers

& Kaminsky, 2016).

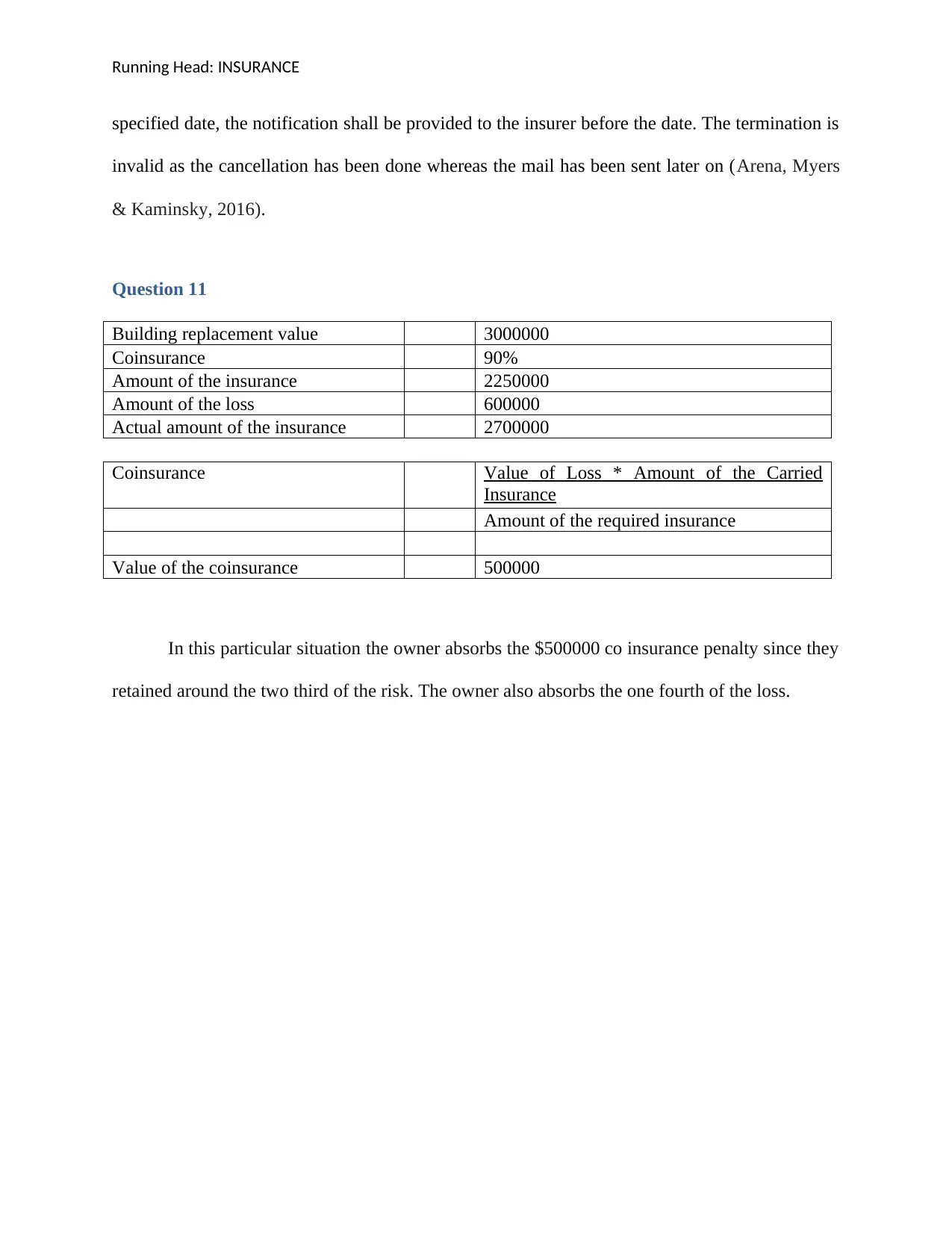

Question 11

Building replacement value 3000000

Coinsurance 90%

Amount of the insurance 2250000

Amount of the loss 600000

Actual amount of the insurance 2700000

Coinsurance Value of Loss * Amount of the Carried

Insurance

Amount of the required insurance

Value of the coinsurance 500000

In this particular situation the owner absorbs the $500000 co insurance penalty since they

retained around the two third of the risk. The owner also absorbs the one fourth of the loss.

specified date, the notification shall be provided to the insurer before the date. The termination is

invalid as the cancellation has been done whereas the mail has been sent later on (Arena, Myers

& Kaminsky, 2016).

Question 11

Building replacement value 3000000

Coinsurance 90%

Amount of the insurance 2250000

Amount of the loss 600000

Actual amount of the insurance 2700000

Coinsurance Value of Loss * Amount of the Carried

Insurance

Amount of the required insurance

Value of the coinsurance 500000

In this particular situation the owner absorbs the $500000 co insurance penalty since they

retained around the two third of the risk. The owner also absorbs the one fourth of the loss.

Running Head: INSURANCE

References

Alberta Health, (2018). Examples of Common Workplace Hazards. Retrieved from

https://work.alberta.ca/elearning/healthcare/pdf/ExamplesCommonWorkplaceHazardsAH

S.pdf

Andrews, N. (2015). Contract law. Cambridge University Press. California.

Arena, R., Myers, J., & Kaminsky, L. A. (2016). Revisiting age-predicted maximal heart rate:

Can it be used as a valid measure of effort?. American heart journal, 173, 49-56.

Casaburi, L., & Willis, J. (2018). Time versus state in insurance: Experimental evidence from

contract farming in Kenya. American Economic Review, 108(12), 3778-3813.

Dixon, W., Christensen, S., & Duncan, W. (2018). Mortgagee sales, disclaimer and escheat: A

suggested statuory solution. Insolvency Law Journal, 26(Pt 2), 61-72.

ELECTRONIC EQUIPMENT INSURANCE (EEI), (2018). THE ORIENTAL INSURANCE

COMPANY LIMITED. Retrieved from https://orientalinsurance.org.in/electronic-

equipment-insuarance-policy

Gay, C. E., Christensen, S. T., Hayward, G., Cielocha, S., & Binion, T. (2015). U.S. Patent No.

9,105,066. Washington, DC: U.S. Patent and Trademark Office.

Hoffman, D. A., & Eigen, Z. J. (2017). Contract Consideration and Behavior. Geo. Wash. L.

Rev., 85, 351.

Smits, J. M. (Ed.). (2017). Contract law: a comparative introduction. Edward Elgar Publishing.

Soni, A., Sabik, L. M., Simon, K., & Sommers, B. D. (2018). Changes in insurance coverage

among cancer patients under the Affordable Care Act. JAMA oncology, 4(1), 122-124.

Zuo, Z., & Hang, Y. (2018). The Research on the Insurable of Catastrophe Risk based on the

Theory of Insurable Risk. Foreign Economic Relations & Trade, (4), 29.

References

Alberta Health, (2018). Examples of Common Workplace Hazards. Retrieved from

https://work.alberta.ca/elearning/healthcare/pdf/ExamplesCommonWorkplaceHazardsAH

S.pdf

Andrews, N. (2015). Contract law. Cambridge University Press. California.

Arena, R., Myers, J., & Kaminsky, L. A. (2016). Revisiting age-predicted maximal heart rate:

Can it be used as a valid measure of effort?. American heart journal, 173, 49-56.

Casaburi, L., & Willis, J. (2018). Time versus state in insurance: Experimental evidence from

contract farming in Kenya. American Economic Review, 108(12), 3778-3813.

Dixon, W., Christensen, S., & Duncan, W. (2018). Mortgagee sales, disclaimer and escheat: A

suggested statuory solution. Insolvency Law Journal, 26(Pt 2), 61-72.

ELECTRONIC EQUIPMENT INSURANCE (EEI), (2018). THE ORIENTAL INSURANCE

COMPANY LIMITED. Retrieved from https://orientalinsurance.org.in/electronic-

equipment-insuarance-policy

Gay, C. E., Christensen, S. T., Hayward, G., Cielocha, S., & Binion, T. (2015). U.S. Patent No.

9,105,066. Washington, DC: U.S. Patent and Trademark Office.

Hoffman, D. A., & Eigen, Z. J. (2017). Contract Consideration and Behavior. Geo. Wash. L.

Rev., 85, 351.

Smits, J. M. (Ed.). (2017). Contract law: a comparative introduction. Edward Elgar Publishing.

Soni, A., Sabik, L. M., Simon, K., & Sommers, B. D. (2018). Changes in insurance coverage

among cancer patients under the Affordable Care Act. JAMA oncology, 4(1), 122-124.

Zuo, Z., & Hang, Y. (2018). The Research on the Insurable of Catastrophe Risk based on the

Theory of Insurable Risk. Foreign Economic Relations & Trade, (4), 29.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.