IAG Financial Performance: Ratio Analysis and Trend Evaluation

VerifiedAdded on 2021/04/17

|11

|2730

|54

Report

AI Summary

This report provides a comprehensive financial analysis of Insurance Australia Group Limited (IAG). It begins with an abstract summarizing the company's history and current position in the Australian insurance market. The introduction emphasizes the importance of financial statement analysis for assessing a company's health. The report calculates and analyzes key financial ratios for 2016 and 2017, including profitability (net profit margin, return on assets, return on equity, gross profit margin, and earnings per share) and liquidity ratios (current, quick, operating cash flow, asset efficiency, current liability coverage, long-term debt coverage, and cash generating power). The analysis reveals positive trends in profitability and asset utilization, with improvements in net profit margin, return on assets, and return on equity. The report also examines the company's competitors, including Westpac Banking Corporation, Commonwealth Bank Limited, and Suncorp, and analyzes IAG's corporate governance practices, highlighting compliance with the ASX Corporate Governance Council principles. The conclusion summarizes the findings and overall financial performance of IAG.

INSURANCE AUSTRALIA GROUP LIMITED

Student Name :

Student ID :

9/5/2018

Student Name :

Student ID :

9/5/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

ABSTRACT....................................................................................................................................................2

INTRODUCTION...........................................................................................................................................3

CALCULATION OF FINANCIAL RATIOS..........................................................................................................3

ANALYSIS OF RATIOS AND ITS RELATED TRENDS.........................................................................................6

COMPANY AND ITS COMPETITORS..............................................................................................................8

ANALYSIS OF THE CORPORATE GOVERNANCE.............................................................................................9

Board’s Role.............................................................................................................................................9

Ethical and Responsible decision making..............................................................................................10

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................10

ABSTRACT

The company that has been provided is Insurance Australia Group Limited and it belongs to the

group of financing industry. The company has its roots beginning from the year of nineteen

hundred and twenty five when it was working in the form of association under the trade name of

National Roads and Motorists Association. Through this association the company was providing

the facilities related to insurance only to its member and in the year of nineteen hundred and

eighty one it has been regarded as largest insurance service provider and in the year of 1995, the

company has started its expansion outside the operating state and opened their offices in Victoria

and moves to Queensland. In the year of 2000, the association status has been waived and the

new company – NRMA Insurance Group Limited has been formed and later in the year of 2002

the name has been changed to Insurance Australia Group Limited and in the today’s world, the

company is leading the business in the Insurance sector in Australia. It is working across

Australia, Asia and New Zealand. The company is constantly working for providing better

insurance facilities to the customers and giving maximum returns to their stakeholders.

2

ABSTRACT....................................................................................................................................................2

INTRODUCTION...........................................................................................................................................3

CALCULATION OF FINANCIAL RATIOS..........................................................................................................3

ANALYSIS OF RATIOS AND ITS RELATED TRENDS.........................................................................................6

COMPANY AND ITS COMPETITORS..............................................................................................................8

ANALYSIS OF THE CORPORATE GOVERNANCE.............................................................................................9

Board’s Role.............................................................................................................................................9

Ethical and Responsible decision making..............................................................................................10

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................10

ABSTRACT

The company that has been provided is Insurance Australia Group Limited and it belongs to the

group of financing industry. The company has its roots beginning from the year of nineteen

hundred and twenty five when it was working in the form of association under the trade name of

National Roads and Motorists Association. Through this association the company was providing

the facilities related to insurance only to its member and in the year of nineteen hundred and

eighty one it has been regarded as largest insurance service provider and in the year of 1995, the

company has started its expansion outside the operating state and opened their offices in Victoria

and moves to Queensland. In the year of 2000, the association status has been waived and the

new company – NRMA Insurance Group Limited has been formed and later in the year of 2002

the name has been changed to Insurance Australia Group Limited and in the today’s world, the

company is leading the business in the Insurance sector in Australia. It is working across

Australia, Asia and New Zealand. The company is constantly working for providing better

insurance facilities to the customers and giving maximum returns to their stakeholders.

2

INTRODUCTION

Analysis of the financial statements is the very important part of the financing function. The

analysis shall be done by each and every company operating in the countries irrespective of the

form of the industry to which the company belongs. It may be of financing industry or from real

estate. It is because only through the analysis of the financial statements, the company came to

know about the financial health and performance of the company. Through this report the

financial statements of the company – Insurance Australia Group Limited has been done with the

help of the accounting ratios and that too for the consecutive period of two years so as to provide

the trend analysis also. Secondly the analysis of the corporate governance of the company has

been made with respect to the necessary disclosures made by the company in the statement of the

corporate governance. Corporate governance provides an insight about the proper functioning of

the management of the company. The competitors of the companies have also been considered in

the analysis which has equipped the users of the financial statements and the stakeholders about

the strategies adopted by the company to grow the company in the future. The report has then

ended up with the conclusion stating the fact and the results that has been gathered in the whole

of the report.

With these considerations, the report has prepared and presented for the stakeholders of the

company.

CALCULATION OF FINANCIAL RATIOS

For the purpose of the calculation of the financial ratios, the annual report of the company for the

last two years ending 2017 and 2016 have been considered (Insurance Australia Official

Website, 2017). The liquidity ratios and the profitability ratios have been calculated as under:

FINANCIAL RATIOS FOR ANALYSIS - INSURANCE AUSTRALIA GROUP

LIMITED

S.

NO. Particulars 2017 2016

3

Analysis of the financial statements is the very important part of the financing function. The

analysis shall be done by each and every company operating in the countries irrespective of the

form of the industry to which the company belongs. It may be of financing industry or from real

estate. It is because only through the analysis of the financial statements, the company came to

know about the financial health and performance of the company. Through this report the

financial statements of the company – Insurance Australia Group Limited has been done with the

help of the accounting ratios and that too for the consecutive period of two years so as to provide

the trend analysis also. Secondly the analysis of the corporate governance of the company has

been made with respect to the necessary disclosures made by the company in the statement of the

corporate governance. Corporate governance provides an insight about the proper functioning of

the management of the company. The competitors of the companies have also been considered in

the analysis which has equipped the users of the financial statements and the stakeholders about

the strategies adopted by the company to grow the company in the future. The report has then

ended up with the conclusion stating the fact and the results that has been gathered in the whole

of the report.

With these considerations, the report has prepared and presented for the stakeholders of the

company.

CALCULATION OF FINANCIAL RATIOS

For the purpose of the calculation of the financial ratios, the annual report of the company for the

last two years ending 2017 and 2016 have been considered (Insurance Australia Official

Website, 2017). The liquidity ratios and the profitability ratios have been calculated as under:

FINANCIAL RATIOS FOR ANALYSIS - INSURANCE AUSTRALIA GROUP

LIMITED

S.

NO. Particulars 2017 2016

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

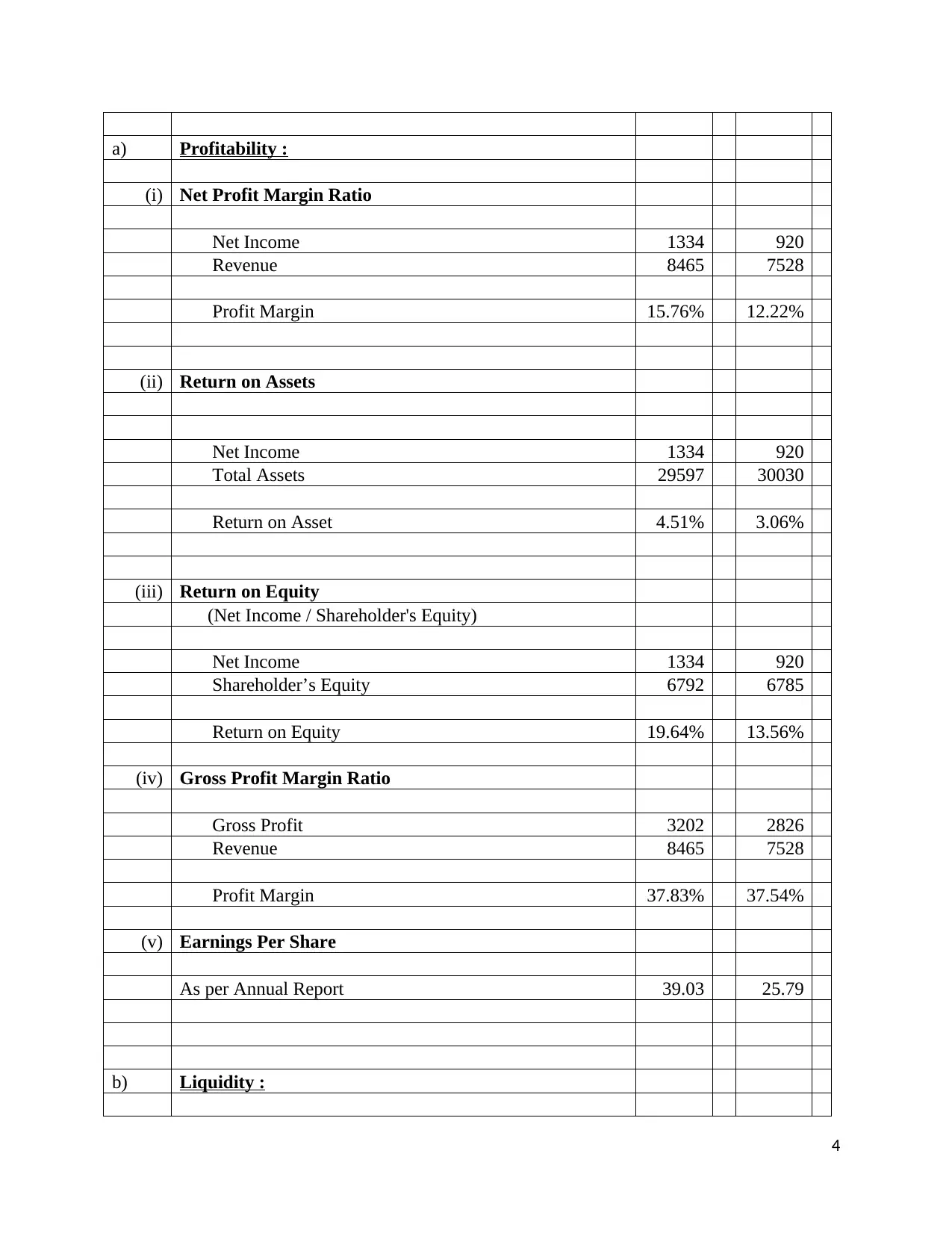

a) Profitability :

(i) Net Profit Margin Ratio

Net Income 1334 920

Revenue 8465 7528

Profit Margin 15.76% 12.22%

(ii) Return on Assets

Net Income 1334 920

Total Assets 29597 30030

Return on Asset 4.51% 3.06%

(iii) Return on Equity

(Net Income / Shareholder's Equity)

Net Income 1334 920

Shareholder’s Equity 6792 6785

Return on Equity 19.64% 13.56%

(iv) Gross Profit Margin Ratio

Gross Profit 3202 2826

Revenue 8465 7528

Profit Margin 37.83% 37.54%

(v) Earnings Per Share

As per Annual Report 39.03 25.79

b) Liquidity :

4

(i) Net Profit Margin Ratio

Net Income 1334 920

Revenue 8465 7528

Profit Margin 15.76% 12.22%

(ii) Return on Assets

Net Income 1334 920

Total Assets 29597 30030

Return on Asset 4.51% 3.06%

(iii) Return on Equity

(Net Income / Shareholder's Equity)

Net Income 1334 920

Shareholder’s Equity 6792 6785

Return on Equity 19.64% 13.56%

(iv) Gross Profit Margin Ratio

Gross Profit 3202 2826

Revenue 8465 7528

Profit Margin 37.83% 37.54%

(v) Earnings Per Share

As per Annual Report 39.03 25.79

b) Liquidity :

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

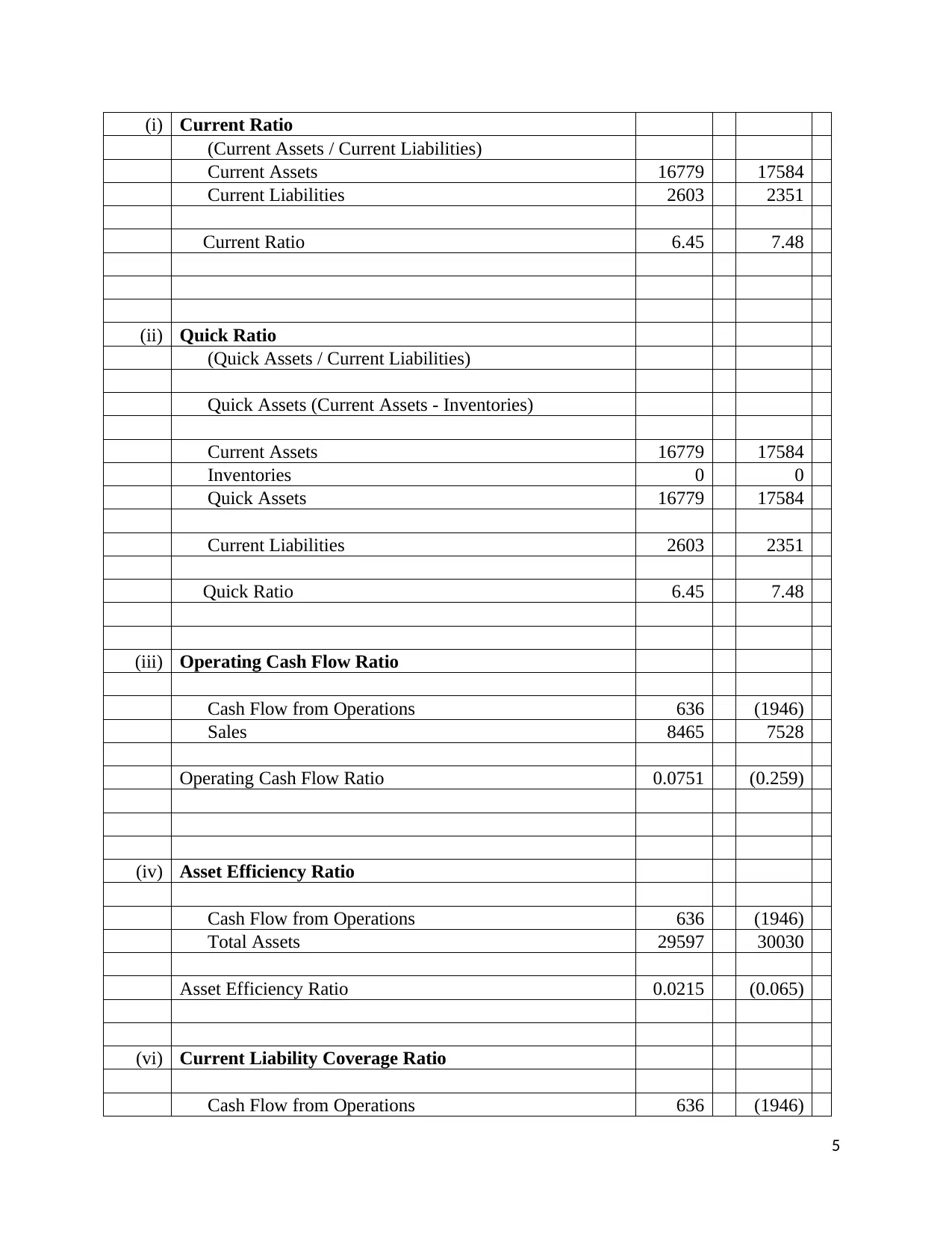

(i) Current Ratio

(Current Assets / Current Liabilities)

Current Assets 16779 17584

Current Liabilities 2603 2351

Current Ratio 6.45 7.48

(ii) Quick Ratio

(Quick Assets / Current Liabilities)

Quick Assets (Current Assets - Inventories)

Current Assets 16779 17584

Inventories 0 0

Quick Assets 16779 17584

Current Liabilities 2603 2351

Quick Ratio 6.45 7.48

(iii) Operating Cash Flow Ratio

Cash Flow from Operations 636 (1946)

Sales 8465 7528

Operating Cash Flow Ratio 0.0751 (0.259)

(iv) Asset Efficiency Ratio

Cash Flow from Operations 636 (1946)

Total Assets 29597 30030

Asset Efficiency Ratio 0.0215 (0.065)

(vi) Current Liability Coverage Ratio

Cash Flow from Operations 636 (1946)

5

(Current Assets / Current Liabilities)

Current Assets 16779 17584

Current Liabilities 2603 2351

Current Ratio 6.45 7.48

(ii) Quick Ratio

(Quick Assets / Current Liabilities)

Quick Assets (Current Assets - Inventories)

Current Assets 16779 17584

Inventories 0 0

Quick Assets 16779 17584

Current Liabilities 2603 2351

Quick Ratio 6.45 7.48

(iii) Operating Cash Flow Ratio

Cash Flow from Operations 636 (1946)

Sales 8465 7528

Operating Cash Flow Ratio 0.0751 (0.259)

(iv) Asset Efficiency Ratio

Cash Flow from Operations 636 (1946)

Total Assets 29597 30030

Asset Efficiency Ratio 0.0215 (0.065)

(vi) Current Liability Coverage Ratio

Cash Flow from Operations 636 (1946)

5

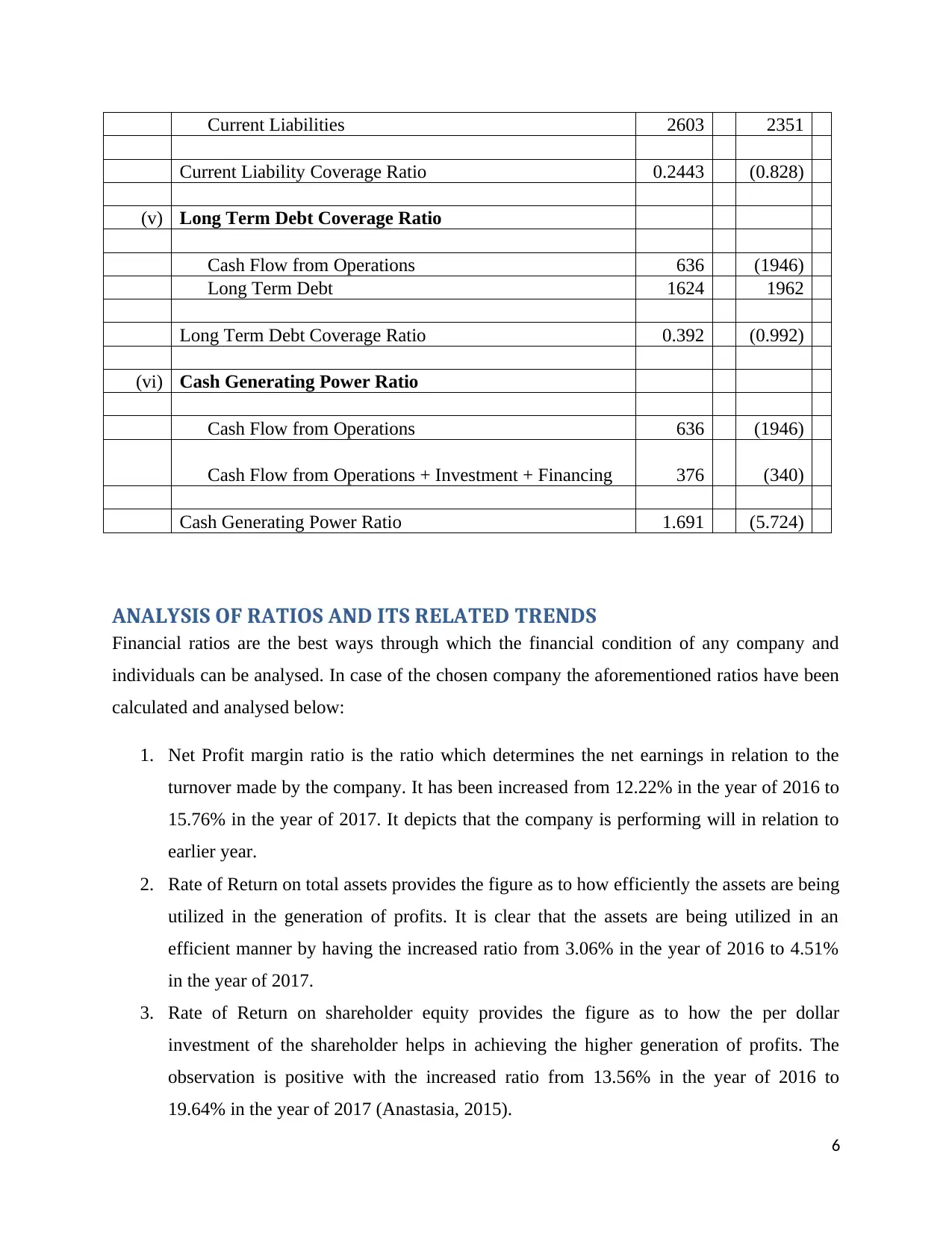

Current Liabilities 2603 2351

Current Liability Coverage Ratio 0.2443 (0.828)

(v) Long Term Debt Coverage Ratio

Cash Flow from Operations 636 (1946)

Long Term Debt 1624 1962

Long Term Debt Coverage Ratio 0.392 (0.992)

(vi) Cash Generating Power Ratio

Cash Flow from Operations 636 (1946)

Cash Flow from Operations + Investment + Financing 376 (340)

Cash Generating Power Ratio 1.691 (5.724)

ANALYSIS OF RATIOS AND ITS RELATED TRENDS

Financial ratios are the best ways through which the financial condition of any company and

individuals can be analysed. In case of the chosen company the aforementioned ratios have been

calculated and analysed below:

1. Net Profit margin ratio is the ratio which determines the net earnings in relation to the

turnover made by the company. It has been increased from 12.22% in the year of 2016 to

15.76% in the year of 2017. It depicts that the company is performing will in relation to

earlier year.

2. Rate of Return on total assets provides the figure as to how efficiently the assets are being

utilized in the generation of profits. It is clear that the assets are being utilized in an

efficient manner by having the increased ratio from 3.06% in the year of 2016 to 4.51%

in the year of 2017.

3. Rate of Return on shareholder equity provides the figure as to how the per dollar

investment of the shareholder helps in achieving the higher generation of profits. The

observation is positive with the increased ratio from 13.56% in the year of 2016 to

19.64% in the year of 2017 (Anastasia, 2015).

6

Current Liability Coverage Ratio 0.2443 (0.828)

(v) Long Term Debt Coverage Ratio

Cash Flow from Operations 636 (1946)

Long Term Debt 1624 1962

Long Term Debt Coverage Ratio 0.392 (0.992)

(vi) Cash Generating Power Ratio

Cash Flow from Operations 636 (1946)

Cash Flow from Operations + Investment + Financing 376 (340)

Cash Generating Power Ratio 1.691 (5.724)

ANALYSIS OF RATIOS AND ITS RELATED TRENDS

Financial ratios are the best ways through which the financial condition of any company and

individuals can be analysed. In case of the chosen company the aforementioned ratios have been

calculated and analysed below:

1. Net Profit margin ratio is the ratio which determines the net earnings in relation to the

turnover made by the company. It has been increased from 12.22% in the year of 2016 to

15.76% in the year of 2017. It depicts that the company is performing will in relation to

earlier year.

2. Rate of Return on total assets provides the figure as to how efficiently the assets are being

utilized in the generation of profits. It is clear that the assets are being utilized in an

efficient manner by having the increased ratio from 3.06% in the year of 2016 to 4.51%

in the year of 2017.

3. Rate of Return on shareholder equity provides the figure as to how the per dollar

investment of the shareholder helps in achieving the higher generation of profits. The

observation is positive with the increased ratio from 13.56% in the year of 2016 to

19.64% in the year of 2017 (Anastasia, 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Gross Profit margin has been increased by 0.29% only irrespective of the 8.03% increase

in the figure of the revenue. It entails that the trading pattern of the company has been

changed due to which the company’s gross profit has been improved by small amount.

5. Earnings per share provide the amount that is attributable to the shareholders and the

amount they will earn on the amount they have invested per share. The earnings per share

have been tremendously increased from 25.79 in the year of 2016 to 39.03 in the year of

2017 (Lusardi, 2017).

6. Current ratio helps in analyzing the short term liquidity of the company and the same has

been decreased from 7.48 in the year of 2017 to 6.45 in the year of 2016, it depicts that

the company is not managing their working in an efficient manner.

7. Quick ratio is equivalent to the current ratio because of non presence of prepaid expenses

and inventories.

8. Cash flow ratios have also been calculated and each of the five cash flow ratios there is

separate significance. First ratio is operating cash flow ratio which describes the amount

of cash required to generate every dollar amount of the revenue. In the year ending 2016,

the cash flows has been negative 1946 dollars and in 2017 it has been positive 636 dollars

which shows that the company has been able to improve its cash management procedures

and the cash flow conditions (Edwards, 2015). Second ratio is the asset efficiency ratio

which ascertains the effective utilization of the assets to generate the cash flows. The

analysis has been same because the operating cash flow is the numerator in the equation.

Similar analysis has been made in the current liability and long term debt coverage ratio

which helps in understanding as to whether the company would be able to pay the current

liability and long term debt in time. The last ratio which is very important is the cash

generating power ratio which helps in ascertaining the ability of the company to generate

the operating cash flows as compared to the total cash flows. Again the analysis is the

same and in the current year, there has been tremendous change from negative 5.7 to

positive 1.6.

With the help of the ratios and the figures, the trend analysis has also been made in the following

major items:

7

in the figure of the revenue. It entails that the trading pattern of the company has been

changed due to which the company’s gross profit has been improved by small amount.

5. Earnings per share provide the amount that is attributable to the shareholders and the

amount they will earn on the amount they have invested per share. The earnings per share

have been tremendously increased from 25.79 in the year of 2016 to 39.03 in the year of

2017 (Lusardi, 2017).

6. Current ratio helps in analyzing the short term liquidity of the company and the same has

been decreased from 7.48 in the year of 2017 to 6.45 in the year of 2016, it depicts that

the company is not managing their working in an efficient manner.

7. Quick ratio is equivalent to the current ratio because of non presence of prepaid expenses

and inventories.

8. Cash flow ratios have also been calculated and each of the five cash flow ratios there is

separate significance. First ratio is operating cash flow ratio which describes the amount

of cash required to generate every dollar amount of the revenue. In the year ending 2016,

the cash flows has been negative 1946 dollars and in 2017 it has been positive 636 dollars

which shows that the company has been able to improve its cash management procedures

and the cash flow conditions (Edwards, 2015). Second ratio is the asset efficiency ratio

which ascertains the effective utilization of the assets to generate the cash flows. The

analysis has been same because the operating cash flow is the numerator in the equation.

Similar analysis has been made in the current liability and long term debt coverage ratio

which helps in understanding as to whether the company would be able to pay the current

liability and long term debt in time. The last ratio which is very important is the cash

generating power ratio which helps in ascertaining the ability of the company to generate

the operating cash flows as compared to the total cash flows. Again the analysis is the

same and in the current year, there has been tremendous change from negative 5.7 to

positive 1.6.

With the help of the ratios and the figures, the trend analysis has also been made in the following

major items:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Increase in Net Profit in relation to Revenue – The revenue of the company has been

increased by 8% approximately in 2017 as compared to the year of 2016. But the net

profit has been increased by 3.54% only which exhibits that the expenses have also been

increased as compared to the earlier year.

2. Decrease in Current Assets – The value of the current assets has been decreased in

relation to the increase in revenue. It exhibits that the cash flows of the company has been

increased and the same is very clear from the cash flow statement read with the cash flow

ratios.

3. Decrease in Long Term Debt – There has been decrease in the long term debt which

ensures that the company has paid the debt from the cash flows generated during the year

and hence it is the positive indication for the growth of the company.

With this the analysis of the ratios and the trends have been made and have been found positive

about the future certainty of the company keeping in consideration of the financial crisis that has

happened in the last decades.

COMPANY AND ITS COMPETITORS

The chosen company is Insurance Australia Group Limited and is into the financing sector of

Insurance and is registered in Sydney, Australia and is in existence for 90 plus years. The

company is providing not only the insurance of businesses but also for the individuals and also

includes the motor vehicle and compensation to workers insurance. The company operates its

functions through online mode under the brand name of Buzz (Insurance Australia Official

Website, 2017). There are three chief competitors of the company. One is Westpac Banking

Corporation, second is Commonwealth Bank Limited and the third one is Suncorp – Metway

Limited. Each of these companies has different strategies of operations and are working edge to

edge basis for each other.

Westpac Company is founded in the year of eighteen hundred and seventeen and has been found

as one of the top rival of the company and as on that the company is employing 20000 more

employees than the chosen company. The company has celebrated its 200th century in the year of

2017 and serving more than 12 million customers. But recently the company has been fined for

having the ineffective and bad mortgage system. Common Wealth bank is also founded in

8

increased by 8% approximately in 2017 as compared to the year of 2016. But the net

profit has been increased by 3.54% only which exhibits that the expenses have also been

increased as compared to the earlier year.

2. Decrease in Current Assets – The value of the current assets has been decreased in

relation to the increase in revenue. It exhibits that the cash flows of the company has been

increased and the same is very clear from the cash flow statement read with the cash flow

ratios.

3. Decrease in Long Term Debt – There has been decrease in the long term debt which

ensures that the company has paid the debt from the cash flows generated during the year

and hence it is the positive indication for the growth of the company.

With this the analysis of the ratios and the trends have been made and have been found positive

about the future certainty of the company keeping in consideration of the financial crisis that has

happened in the last decades.

COMPANY AND ITS COMPETITORS

The chosen company is Insurance Australia Group Limited and is into the financing sector of

Insurance and is registered in Sydney, Australia and is in existence for 90 plus years. The

company is providing not only the insurance of businesses but also for the individuals and also

includes the motor vehicle and compensation to workers insurance. The company operates its

functions through online mode under the brand name of Buzz (Insurance Australia Official

Website, 2017). There are three chief competitors of the company. One is Westpac Banking

Corporation, second is Commonwealth Bank Limited and the third one is Suncorp – Metway

Limited. Each of these companies has different strategies of operations and are working edge to

edge basis for each other.

Westpac Company is founded in the year of eighteen hundred and seventeen and has been found

as one of the top rival of the company and as on that the company is employing 20000 more

employees than the chosen company. The company has celebrated its 200th century in the year of

2017 and serving more than 12 million customers. But recently the company has been fined for

having the ineffective and bad mortgage system. Common Wealth bank is also founded in

8

Australia in the year of 1911 and has 38000 more employees than the chosen company and

accordingly the company has the roots in the banking industry with the larger effect. Suncorp

Company has been founded in Queensland having employees nearer to the chosen company but

has been able to generate the revenues equal to the approximately 6.42% of the revenue of the

chosen company. Thus, in this manner each of the competitors has its own significance with

regard to the chosen company.

ANALYSIS OF THE CORPORATE GOVERNANCE

Corporate Governance is the code of conduct along with the policies, procedures and rules and

regulations which are required to be ensure that the interest of the stakeholders and the

shareholders of the company have been considered with completeness (Dandino, 2014).

As per the statement of corporate governance as hosted on the website of the company, it has

been observed that the necessary compliance has been made with the third edition of Principles

and Recommendation of Australia Securities Exchange Corporate Governance Council. Also, the

board of director has the full responsibility to ensure the compliance with the corporate

governance framework which is accordance with the provisions of the Corporations Act 2001.

Following are the facts observed from the statement of corporate governance and is worth

mentioning as it shows the negative as well as positive side of the effective management of the

company.

Board’s Role

As per the first principle of the laying foundations for management and oversight, the

responsibility has been given totally to the board of director for protecting the various interests of

the shareholders as well as the stakeholders and for the effective running of the functions of the

company. Following are the areas where there attention is required:

- Strategies of the group towards the organizational objectives.

- Maintaining the integrity and faithfulness of the financial information and reporting

system of the company

9

accordingly the company has the roots in the banking industry with the larger effect. Suncorp

Company has been founded in Queensland having employees nearer to the chosen company but

has been able to generate the revenues equal to the approximately 6.42% of the revenue of the

chosen company. Thus, in this manner each of the competitors has its own significance with

regard to the chosen company.

ANALYSIS OF THE CORPORATE GOVERNANCE

Corporate Governance is the code of conduct along with the policies, procedures and rules and

regulations which are required to be ensure that the interest of the stakeholders and the

shareholders of the company have been considered with completeness (Dandino, 2014).

As per the statement of corporate governance as hosted on the website of the company, it has

been observed that the necessary compliance has been made with the third edition of Principles

and Recommendation of Australia Securities Exchange Corporate Governance Council. Also, the

board of director has the full responsibility to ensure the compliance with the corporate

governance framework which is accordance with the provisions of the Corporations Act 2001.

Following are the facts observed from the statement of corporate governance and is worth

mentioning as it shows the negative as well as positive side of the effective management of the

company.

Board’s Role

As per the first principle of the laying foundations for management and oversight, the

responsibility has been given totally to the board of director for protecting the various interests of

the shareholders as well as the stakeholders and for the effective running of the functions of the

company. Following are the areas where there attention is required:

- Strategies of the group towards the organizational objectives.

- Maintaining the integrity and faithfulness of the financial information and reporting

system of the company

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The statement has laid down the responsibilities for Chief Executive Officer also (Insurance

Australia Official Website, 2017). As per the provisions of Corporations Act 2001, he shall make

all the endeavors to manage the routine affairs of the company and if any regularity comes under

observation then the same shall be brought by him to the notice of the management of the

company in order to have the correction there from (Cameron, 2014).

Ethical and Responsible decision making

The third principle makes the company to mention all the ethical requirements that every

employee and officers shall follow. The same has been done and to mention it better the

company has bring on its roll the well known ethicist - Dr Simon Longstaff (Insurance Australia

Official Website, 2017) .

CONCLUSION

The report has been prepared with the objective of providing the detailed information about the

company and its working. The working has been analysed not only in the form of the financial

but also through the performance of the competitors and more important through the

effectiveness of the corporate governance. Each of the analysis is very important for

understanding the function of the company and the same has been depicted from and exhibited in

the report. The report has taught that the financial ratios have the important role in getting the

detailed degree of the performance of the company as each of the ratios have its own significance

and each of them has different linkage to different concepts. Second lesson that has been

concluded from the report is that the competitor’s analysis is required before taking any

necessary step.

REFERENCES

10

Australia Official Website, 2017). As per the provisions of Corporations Act 2001, he shall make

all the endeavors to manage the routine affairs of the company and if any regularity comes under

observation then the same shall be brought by him to the notice of the management of the

company in order to have the correction there from (Cameron, 2014).

Ethical and Responsible decision making

The third principle makes the company to mention all the ethical requirements that every

employee and officers shall follow. The same has been done and to mention it better the

company has bring on its roll the well known ethicist - Dr Simon Longstaff (Insurance Australia

Official Website, 2017) .

CONCLUSION

The report has been prepared with the objective of providing the detailed information about the

company and its working. The working has been analysed not only in the form of the financial

but also through the performance of the competitors and more important through the

effectiveness of the corporate governance. Each of the analysis is very important for

understanding the function of the company and the same has been depicted from and exhibited in

the report. The report has taught that the financial ratios have the important role in getting the

detailed degree of the performance of the company as each of the ratios have its own significance

and each of them has different linkage to different concepts. Second lesson that has been

concluded from the report is that the competitor’s analysis is required before taking any

necessary step.

REFERENCES

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 05/09/2018

Cameron A, (2014), “Corporate Governance Principles and Recommendations” available on

http://www.asx.com.au/documents/asx-compliance/cgc-principles-and-recommendations-3rd-

edn.pdf accessed on 05/09/2018.

Dandino P. (2014), “Corporate Governance : Something for everyone”, Franchising World,

pages 40-41.

Edwards, A., (2015), “Financial constraints and cash tax savings”. The Accounting

Review, 91(3), pp.859-881.

Insurance Australia Official Website, “Annual Report 2017” available on

http://www.iag.com.au/investors/reports accessed on 05/09/2018

Lusardi, A., (2017), “Optimal financial knowledge and wealth inequality”. Journal of Political

Economy, 125(2), pp.431-477.

11

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 05/09/2018

Cameron A, (2014), “Corporate Governance Principles and Recommendations” available on

http://www.asx.com.au/documents/asx-compliance/cgc-principles-and-recommendations-3rd-

edn.pdf accessed on 05/09/2018.

Dandino P. (2014), “Corporate Governance : Something for everyone”, Franchising World,

pages 40-41.

Edwards, A., (2015), “Financial constraints and cash tax savings”. The Accounting

Review, 91(3), pp.859-881.

Insurance Australia Official Website, “Annual Report 2017” available on

http://www.iag.com.au/investors/reports accessed on 05/09/2018

Lusardi, A., (2017), “Optimal financial knowledge and wealth inequality”. Journal of Political

Economy, 125(2), pp.431-477.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.