Auditing Report: Analysis of IAG's Financial Performance

VerifiedAdded on 2020/02/24

|26

|5520

|47

Report

AI Summary

This report provides a comprehensive auditing analysis of Insurance Australia Group (IAG), a multinational insurance company. It begins with an overview of IAG's business operations, investment activities, and financing activities, followed by an examination of the insurance industry, including its size, growth, supply chain, major players, and critical success factors. The report then delves into the legal and external environmental factors affecting IAG, utilizing PEST, Porter's Five Forces, and SWOT analyses to assess the company's position. Further sections cover IAG's objectives, strategies, and business risk assessment, alongside an analysis of analytical procedures used to evaluate the entity's performance and management and governance. The report concludes with a summary of key findings and recommendations based on the audit analysis.

Running head: AUDITING

Auditing

Name of the University

Name of the Student

Authors Note

Course ID

Auditing

Name of the University

Name of the Student

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Introduction:...............................................................................................................................2

Part 1: Understanding the Nature of the Entity:.........................................................................2

Business Operations:..................................................................................................................2

Investment and investment activities:........................................................................................2

Financing and Financing Activities:..........................................................................................3

Financial reporting practices:.....................................................................................................3

Part 2: Understanding the industry:............................................................................................3

Industry size:..............................................................................................................................3

Industry Growth:........................................................................................................................4

Supply chain:..............................................................................................................................4

Major Players:............................................................................................................................4

Market Share of Industry Players:..............................................................................................5

Critical success factors:..............................................................................................................6

Major threats:.............................................................................................................................6

Part 3: Understanding the Legal Environment...........................................................................6

Part 4: Understanding the external environment factors:...........................................................7

PEST Analysis...........................................................................................................................7

Porters Five Forces Analysis:.....................................................................................................9

SWOT Analysis:......................................................................................................................11

Part 5: Understanding objectives, strategies and Assessing Business Risk:............................12

Table of Contents

Introduction:...............................................................................................................................2

Part 1: Understanding the Nature of the Entity:.........................................................................2

Business Operations:..................................................................................................................2

Investment and investment activities:........................................................................................2

Financing and Financing Activities:..........................................................................................3

Financial reporting practices:.....................................................................................................3

Part 2: Understanding the industry:............................................................................................3

Industry size:..............................................................................................................................3

Industry Growth:........................................................................................................................4

Supply chain:..............................................................................................................................4

Major Players:............................................................................................................................4

Market Share of Industry Players:..............................................................................................5

Critical success factors:..............................................................................................................6

Major threats:.............................................................................................................................6

Part 3: Understanding the Legal Environment...........................................................................6

Part 4: Understanding the external environment factors:...........................................................7

PEST Analysis...........................................................................................................................7

Porters Five Forces Analysis:.....................................................................................................9

SWOT Analysis:......................................................................................................................11

Part 5: Understanding objectives, strategies and Assessing Business Risk:............................12

2AUDITING

Industry Development:.............................................................................................................12

New products and services:......................................................................................................12

Expansion of business:.............................................................................................................12

New accounting requirements:.................................................................................................13

Regulatory Requirements:........................................................................................................13

Current and prospective financing requirements:....................................................................13

USE of IT.................................................................................................................................13

Part 6: Performing Analytical Procedures to Understand Entity’s Performance.....................14

Part 7: Understand Management and Governance...................................................................18

Conclusion:..............................................................................................................................19

Reference List:.........................................................................................................................20

Appendix:.................................................................................................................................23

Computations of Profitability Ratio:........................................................................................23

Computations of Current Ratios:.............................................................................................23

Computations of Stability Ratios:............................................................................................23

Industry Development:.............................................................................................................12

New products and services:......................................................................................................12

Expansion of business:.............................................................................................................12

New accounting requirements:.................................................................................................13

Regulatory Requirements:........................................................................................................13

Current and prospective financing requirements:....................................................................13

USE of IT.................................................................................................................................13

Part 6: Performing Analytical Procedures to Understand Entity’s Performance.....................14

Part 7: Understand Management and Governance...................................................................18

Conclusion:..............................................................................................................................19

Reference List:.........................................................................................................................20

Appendix:.................................................................................................................................23

Computations of Profitability Ratio:........................................................................................23

Computations of Current Ratios:.............................................................................................23

Computations of Stability Ratios:............................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Introduction:

Insurance Australia Group Limited which is informally known as IAG is a

multinational insurance company having it’s headquarter in Sydney, Australia. The company

was formed by the demutualisation of the NRMA insurance business in the year 2000 with a

return of shares to the members of NRMA. As per the information stated from the website of

the company NRMA insurance group ltd changed its name to Insurance Australia Group Ltd

in the year 2000 (Iag.com.au, 2017). IAG is formally known as the listed company it is

generally not a consumer facing brand, nevertheless it presents the Umbrella organization

that holds several well established insurance brands.

Part 1: Understanding the Nature of the Entity:

Business Operations:

IAG has business division in Australia that represents 26 per cent of the group GWP.

The business operations of IAG produces fee income by acting in the form of agent under

both the segment of New South Wales and Victorian workers compensation scheme, which is

underwritten by respective governments of the state (Iag.com.au, 2017). Another secondary

source of business operations represents a fee income from the interest from the authorised

representative brokers. The business operations of New Zealand represents 19% of the group

GWP. Its New Zealand operations continued its better performance by registering a robust

underlying margin of 16.9%.

Investment and investment activities:

Investment activities forms the important part of the insurance business. The funds

that is received by IAG from the collection of premiums are invested in the form of key

source of return for the company in a comprehensive investment values. IAG starts investing

the insurance premium almost immediately when they are collected and continues to produce

Introduction:

Insurance Australia Group Limited which is informally known as IAG is a

multinational insurance company having it’s headquarter in Sydney, Australia. The company

was formed by the demutualisation of the NRMA insurance business in the year 2000 with a

return of shares to the members of NRMA. As per the information stated from the website of

the company NRMA insurance group ltd changed its name to Insurance Australia Group Ltd

in the year 2000 (Iag.com.au, 2017). IAG is formally known as the listed company it is

generally not a consumer facing brand, nevertheless it presents the Umbrella organization

that holds several well established insurance brands.

Part 1: Understanding the Nature of the Entity:

Business Operations:

IAG has business division in Australia that represents 26 per cent of the group GWP.

The business operations of IAG produces fee income by acting in the form of agent under

both the segment of New South Wales and Victorian workers compensation scheme, which is

underwritten by respective governments of the state (Iag.com.au, 2017). Another secondary

source of business operations represents a fee income from the interest from the authorised

representative brokers. The business operations of New Zealand represents 19% of the group

GWP. Its New Zealand operations continued its better performance by registering a robust

underlying margin of 16.9%.

Investment and investment activities:

Investment activities forms the important part of the insurance business. The funds

that is received by IAG from the collection of premiums are invested in the form of key

source of return for the company in a comprehensive investment values. IAG starts investing

the insurance premium almost immediately when they are collected and continues to produce

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

returns until the claims and other expenditure are paid out. The outcomes from the

underwriting evaluates the profits or loss that is produced from the activities of underwriting

for a certain period (Iag.com.au, 2017). The Insurance outcomes that is the vital performance

metrics, adds the amount of net investment return to the outcome of underwriting in order to

derive the overall pre-tax profit or loss from the operations of insurance.

Financing and Financing Activities:

The financing activities are comprises of the proceeds from the issue of shares along

with the outlays for the purchase of treasury shares. The financing activities of IAG consists

of the proceeds from borrowing of $326 million with repayment of borrowings of 131 million

(Iag.com.au, 2017). The financing activities includes dividends that were paid to the

shareholders of 948 million and dividends to the non-controlling interest of 56 million.

Financial reporting practices:

The financial reporting practices of IAG insurances complies with the IFRS that is

issued by the IASB. The company complies with the Corporation Act 2001, AASB adopted

by the AASB (Iag.com.au, 2017). The financial statements of IASB is prepared in accordance

with historical cost principles as reformed by certain exceptions that is noted in the financial

report.

Part 2: Understanding the industry:

Industry size:

There are 115 licensed general insurers with as much as 18 of these companies in the

industry are in run-off. At the present date with 103 licensed insurers have accounted

approximately 90% of the industry’s $114.4 billion in overall assets (Geneva, 2014). The

acquisition of Insurance Australia Groups of Wesfarmers insurance business occurred in the

year 2014 that ultimately strengthened the market share that was held by the large insurance

returns until the claims and other expenditure are paid out. The outcomes from the

underwriting evaluates the profits or loss that is produced from the activities of underwriting

for a certain period (Iag.com.au, 2017). The Insurance outcomes that is the vital performance

metrics, adds the amount of net investment return to the outcome of underwriting in order to

derive the overall pre-tax profit or loss from the operations of insurance.

Financing and Financing Activities:

The financing activities are comprises of the proceeds from the issue of shares along

with the outlays for the purchase of treasury shares. The financing activities of IAG consists

of the proceeds from borrowing of $326 million with repayment of borrowings of 131 million

(Iag.com.au, 2017). The financing activities includes dividends that were paid to the

shareholders of 948 million and dividends to the non-controlling interest of 56 million.

Financial reporting practices:

The financial reporting practices of IAG insurances complies with the IFRS that is

issued by the IASB. The company complies with the Corporation Act 2001, AASB adopted

by the AASB (Iag.com.au, 2017). The financial statements of IASB is prepared in accordance

with historical cost principles as reformed by certain exceptions that is noted in the financial

report.

Part 2: Understanding the industry:

Industry size:

There are 115 licensed general insurers with as much as 18 of these companies in the

industry are in run-off. At the present date with 103 licensed insurers have accounted

approximately 90% of the industry’s $114.4 billion in overall assets (Geneva, 2014). The

acquisition of Insurance Australia Groups of Wesfarmers insurance business occurred in the

year 2014 that ultimately strengthened the market share that was held by the large insurance

5AUDITING

groups in the personal and commercial industry lines. In spite of the expanding concentration

in both industries, there is healthy competition among the wide number insurance groups.

Industry Growth:

The industry reported a strong operating outcome for the year ended 30 June 2016

with net profit after tax of $4.9 billion that was largely driven by the underwriting results of

the insurers. The growth in the gross earned premium for the year ended 30 June 2016 was

primarily recorded in the personal lines classes of business householders and domestic motor

along a high growth in premium that was reported in the compulsory third party

(Khachaturian & Oliver, 2016). Property insures have continued to experience gain from the

benign weather conditions leading to low claim costs. In contrast with the current strong

claims performance in the short tail property classes of business the experience in the long

tail classes namely, professional indemnity and public product liability have presented a

mixed result.

Supply chain:

The competitiveness of the insurance industry can be improved or reserved depending

upon the nature of the competition along the supply chain within which the insurance

industry is nested. Some parts of the supply chain in the industry are highly concentrated

while some are fragmented that can create an impact on the nature and efficiency of the

operations along the supply chain (Bodie, 2013). As evident from the variation in the

insurance industry whether the supply chain is competitive or not balanced and ineffective

can be an important perspective. To some extent it can stated that industry determines the

degree of competition along the supply chain and produces counter balances so that it can

equalize the market forces.

groups in the personal and commercial industry lines. In spite of the expanding concentration

in both industries, there is healthy competition among the wide number insurance groups.

Industry Growth:

The industry reported a strong operating outcome for the year ended 30 June 2016

with net profit after tax of $4.9 billion that was largely driven by the underwriting results of

the insurers. The growth in the gross earned premium for the year ended 30 June 2016 was

primarily recorded in the personal lines classes of business householders and domestic motor

along a high growth in premium that was reported in the compulsory third party

(Khachaturian & Oliver, 2016). Property insures have continued to experience gain from the

benign weather conditions leading to low claim costs. In contrast with the current strong

claims performance in the short tail property classes of business the experience in the long

tail classes namely, professional indemnity and public product liability have presented a

mixed result.

Supply chain:

The competitiveness of the insurance industry can be improved or reserved depending

upon the nature of the competition along the supply chain within which the insurance

industry is nested. Some parts of the supply chain in the industry are highly concentrated

while some are fragmented that can create an impact on the nature and efficiency of the

operations along the supply chain (Bodie, 2013). As evident from the variation in the

insurance industry whether the supply chain is competitive or not balanced and ineffective

can be an important perspective. To some extent it can stated that industry determines the

degree of competition along the supply chain and produces counter balances so that it can

equalize the market forces.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

Major Players:

Australian insurance industry has a large, moneymaking and well established

insurance market. Statistics represents that private insurance industry produces a gross

premium of $34.9 billion yearly with total assets of $113.9 billion (Rollins et al., 2014). In

the year 2014, the Australian insurance industry earned a $42.1 billion in terms of revenue

with a profit of $5.6 billion. Suncorp, IAG, QBE insurance and Allianz Australia Ltd are

regarded as the major players in this industry.

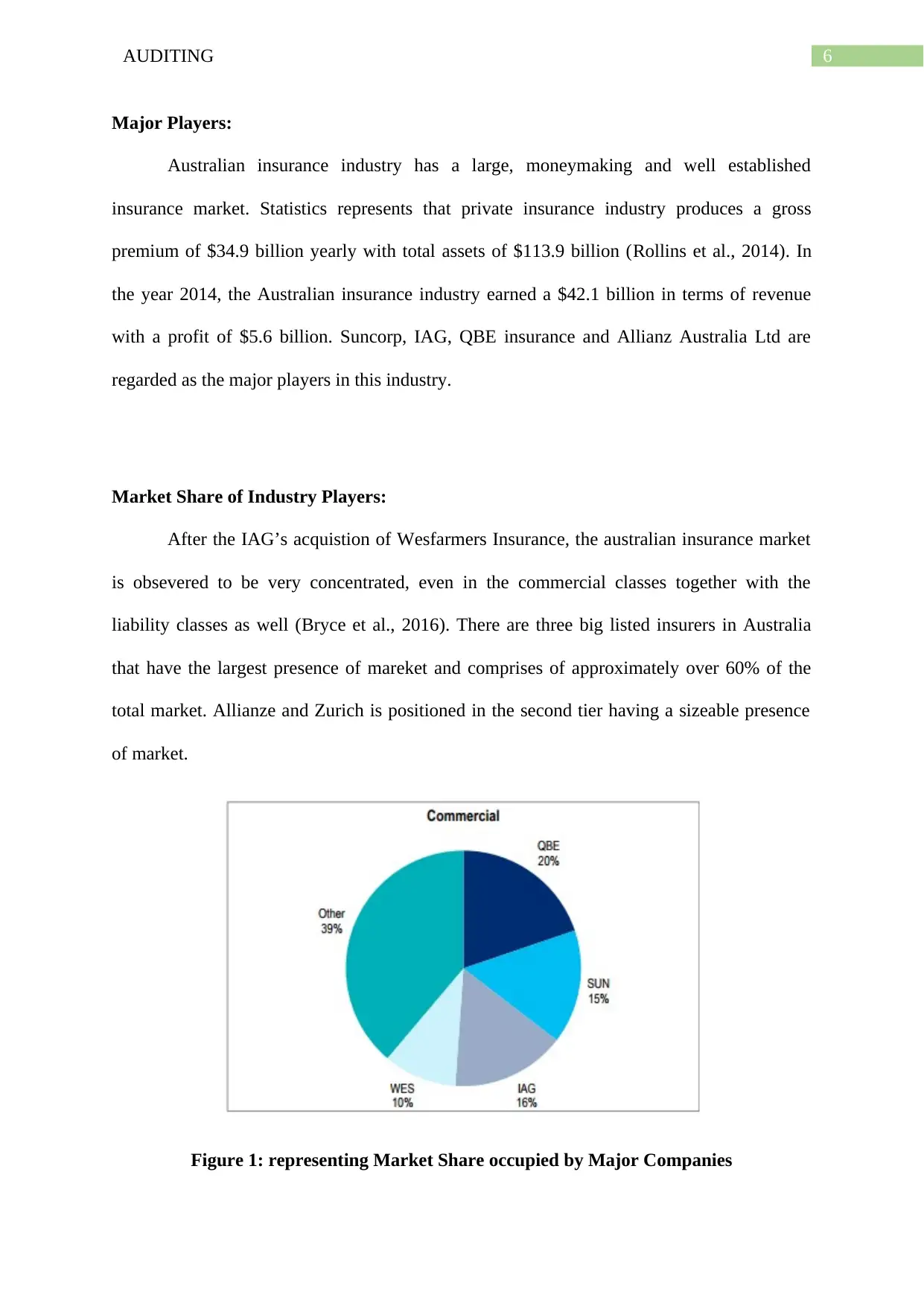

Market Share of Industry Players:

After the IAG’s acquistion of Wesfarmers Insurance, the australian insurance market

is obsevered to be very concentrated, even in the commercial classes together with the

liability classes as well (Bryce et al., 2016). There are three big listed insurers in Australia

that have the largest presence of mareket and comprises of approximately over 60% of the

total market. Allianze and Zurich is positioned in the second tier having a sizeable presence

of market.

Figure 1: representing Market Share occupied by Major Companies

Major Players:

Australian insurance industry has a large, moneymaking and well established

insurance market. Statistics represents that private insurance industry produces a gross

premium of $34.9 billion yearly with total assets of $113.9 billion (Rollins et al., 2014). In

the year 2014, the Australian insurance industry earned a $42.1 billion in terms of revenue

with a profit of $5.6 billion. Suncorp, IAG, QBE insurance and Allianz Australia Ltd are

regarded as the major players in this industry.

Market Share of Industry Players:

After the IAG’s acquistion of Wesfarmers Insurance, the australian insurance market

is obsevered to be very concentrated, even in the commercial classes together with the

liability classes as well (Bryce et al., 2016). There are three big listed insurers in Australia

that have the largest presence of mareket and comprises of approximately over 60% of the

total market. Allianze and Zurich is positioned in the second tier having a sizeable presence

of market.

Figure 1: representing Market Share occupied by Major Companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

(Source: Bryce et al., 2016)

Critical success factors:

Understanding and management of risk forms the critical success factors for the

insurance companies and the financial service organizations are currently experiencing an

improved degree of oversight from their respective boards instead of any other industry

(Chandel & Kumar, 2016). The companies in the insurance industry are required to maintain

its importance as the most valued partner by gaining an in depth understanding of the

industry concerns and offering appropriate solutions. Revolution of data is another key

success factor for the insurance companies as these firms can locate success by comparing,

pooling and underwriting large amount of risk data.

Major threats:

According to Kuo et al., (2017), a recent evaluation based on the Michael Porter’s

five forces found that the competition in Australian insurance market is considered to be

moderate. However, the threat of a new market entrant may limit some profits of some of the

well-known companies. The threat of new entrants introduces the threats of substitute

products could help in influencing the choice of the consumers. In addition to this, shift in the

economic situations is regarded as the major threats for the companies operating in this

industry. With the entry of new firms might substantially create an impact on the revenue and

profit making structures of the firms. More significantly, numerous government regulations

and legislations from the government can act as the major threat.

Part 3: Understanding the Legal Environment

Insurers are required to comply with the general contract law and statutes that are

concerned with the insurance contracts. IAG adheres to the legal, regulatory and prudential

requirements in all the nations wherever IAG conducts its operations (Iag.com.au, 2017). The

(Source: Bryce et al., 2016)

Critical success factors:

Understanding and management of risk forms the critical success factors for the

insurance companies and the financial service organizations are currently experiencing an

improved degree of oversight from their respective boards instead of any other industry

(Chandel & Kumar, 2016). The companies in the insurance industry are required to maintain

its importance as the most valued partner by gaining an in depth understanding of the

industry concerns and offering appropriate solutions. Revolution of data is another key

success factor for the insurance companies as these firms can locate success by comparing,

pooling and underwriting large amount of risk data.

Major threats:

According to Kuo et al., (2017), a recent evaluation based on the Michael Porter’s

five forces found that the competition in Australian insurance market is considered to be

moderate. However, the threat of a new market entrant may limit some profits of some of the

well-known companies. The threat of new entrants introduces the threats of substitute

products could help in influencing the choice of the consumers. In addition to this, shift in the

economic situations is regarded as the major threats for the companies operating in this

industry. With the entry of new firms might substantially create an impact on the revenue and

profit making structures of the firms. More significantly, numerous government regulations

and legislations from the government can act as the major threat.

Part 3: Understanding the Legal Environment

Insurers are required to comply with the general contract law and statutes that are

concerned with the insurance contracts. IAG adheres to the legal, regulatory and prudential

requirements in all the nations wherever IAG conducts its operations (Iag.com.au, 2017). The

8AUDITING

disaster reinsurance cover purchased affects the ICRC under the Australian Prudential

Regulatory Authority capital computations. Any form of new and amended risk exposure

should be approved in compliance with the IAG approval authority framework.

The company maintains a sufficient amount of diverse credit risk exposure in order to

avoid the concentration charge that is added to the regulatory capital requirement. All the

insurers within the IAG group that executes the business insurance business in Australia are

required to obtain registration with the ARPA and are subjected to the ARPA Prudential

Standards. It is the policy of IAG to make sure that each of the licenced insurers maintains

the regulatory capital (Iag.com.au, 2017). IAG makes the use of Standardised Framework laid

down in the relevant prudential standards to compute the regulatory capital.

The financial statements of IAG are prepared in compliance with the Australian

Accounting Standard Board 101 for the presentation of financial statements and ascertains

that the financial statements of the group complies with the International Financial Reporting

Standards (Iag.com.au, 2017). The financial statements of IAG are prepared based on the

principles of historical cost and the balance sheet are prepared with respect to assets and

liabilities that are broadly classified in the order of liquidity in conformity the ASIC

corporation instrument 2016/191.

Part 4: Understanding the external environment factors:

External environmental factors possess large amount of effects on the business

operations of the companies operating in the insurance industry. There are some major tools

to analyse the effects of the external environmental factors of the companies, they are PEST

Analysis, Porter’s Five Forces Analysis and SWOT Analysis. These external factors are

explained below;

disaster reinsurance cover purchased affects the ICRC under the Australian Prudential

Regulatory Authority capital computations. Any form of new and amended risk exposure

should be approved in compliance with the IAG approval authority framework.

The company maintains a sufficient amount of diverse credit risk exposure in order to

avoid the concentration charge that is added to the regulatory capital requirement. All the

insurers within the IAG group that executes the business insurance business in Australia are

required to obtain registration with the ARPA and are subjected to the ARPA Prudential

Standards. It is the policy of IAG to make sure that each of the licenced insurers maintains

the regulatory capital (Iag.com.au, 2017). IAG makes the use of Standardised Framework laid

down in the relevant prudential standards to compute the regulatory capital.

The financial statements of IAG are prepared in compliance with the Australian

Accounting Standard Board 101 for the presentation of financial statements and ascertains

that the financial statements of the group complies with the International Financial Reporting

Standards (Iag.com.au, 2017). The financial statements of IAG are prepared based on the

principles of historical cost and the balance sheet are prepared with respect to assets and

liabilities that are broadly classified in the order of liquidity in conformity the ASIC

corporation instrument 2016/191.

Part 4: Understanding the external environment factors:

External environmental factors possess large amount of effects on the business

operations of the companies operating in the insurance industry. There are some major tools

to analyse the effects of the external environmental factors of the companies, they are PEST

Analysis, Porter’s Five Forces Analysis and SWOT Analysis. These external factors are

explained below;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

PEST Analysis

The main PEST analysis factors are stated below:

Figure 2: Figure illustrating PEST Analysis

(Source: As Created by Author)

Political Factors: Political conditions of Australia is stable as it assist the growth of the

business in country (Shabanova et al., 2015). The government of Australia promotes stable

business environment in order to harmonize the insurance industry of Australia. Some of the

major results from the stable political conditions includes stable business environment,

skilled employees etc.

Economic factor: The Australian government has undertaken several steps with the

objective of increasing the expenditure in the areas of general insurance in Australia (Diacon,

2016). Due to the international economic downturn, there has been a slight decline in the per

PEST

Analysis

Political

Economic

Social

Technological

PEST Analysis

The main PEST analysis factors are stated below:

Figure 2: Figure illustrating PEST Analysis

(Source: As Created by Author)

Political Factors: Political conditions of Australia is stable as it assist the growth of the

business in country (Shabanova et al., 2015). The government of Australia promotes stable

business environment in order to harmonize the insurance industry of Australia. Some of the

major results from the stable political conditions includes stable business environment,

skilled employees etc.

Economic factor: The Australian government has undertaken several steps with the

objective of increasing the expenditure in the areas of general insurance in Australia (Diacon,

2016). Due to the international economic downturn, there has been a slight decline in the per

PEST

Analysis

Political

Economic

Social

Technological

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

capita income of the individuals. As result of these insurance companies are forced to reduce

their prices, that ultimate effects the profitability of the company.

Social factors: Social factors comprises of the ageing populations of the Australian citizens

that creates the business opportunities of the insurance industry. Therefore, companies like

IAG is required to capitalize on these business opportunities (Ho, 2014). The consumer

expectations and demand have been found to be increasing and this could be viewed as the

business opportunities for companies like IAG operating in the insurance industry of

Australia.

Technological factors: Australia is technologically well equipped in order to meet the rising

demands of the consumers (Gupta, 2013). Insurance companies generally keep record of the

consumers through the help of large database and this has resulted in positive impact on the

business performance of the IAG.

Porters Five Forces Analysis:

Porter’s five forces are regarded as the vital tool in determining the competitive

environment of a particular industry. The porter’s five forces of the model is discussed

below;

Existing Rivalry among companies: In the insurance industry of Australia, there are large

number of companies that provides direct competitions to IAG such as, QBE, Allianz and I-

Med Radiology etc. It can be ascertained that the above stated competition firms are identical

in size and industry (Cummins & Weiss, 2013). Therefore, it can be said that there is a

moderate to high threat from these firms.

Threat of New Entrants: A large sum of capital is required to enter in the insurance industry.

This is because new companies entering in the market are required to spend high amount of

capita income of the individuals. As result of these insurance companies are forced to reduce

their prices, that ultimate effects the profitability of the company.

Social factors: Social factors comprises of the ageing populations of the Australian citizens

that creates the business opportunities of the insurance industry. Therefore, companies like

IAG is required to capitalize on these business opportunities (Ho, 2014). The consumer

expectations and demand have been found to be increasing and this could be viewed as the

business opportunities for companies like IAG operating in the insurance industry of

Australia.

Technological factors: Australia is technologically well equipped in order to meet the rising

demands of the consumers (Gupta, 2013). Insurance companies generally keep record of the

consumers through the help of large database and this has resulted in positive impact on the

business performance of the IAG.

Porters Five Forces Analysis:

Porter’s five forces are regarded as the vital tool in determining the competitive

environment of a particular industry. The porter’s five forces of the model is discussed

below;

Existing Rivalry among companies: In the insurance industry of Australia, there are large

number of companies that provides direct competitions to IAG such as, QBE, Allianz and I-

Med Radiology etc. It can be ascertained that the above stated competition firms are identical

in size and industry (Cummins & Weiss, 2013). Therefore, it can be said that there is a

moderate to high threat from these firms.

Threat of New Entrants: A large sum of capital is required to enter in the insurance industry.

This is because new companies entering in the market are required to spend high amount of

11AUDITING

money in the areas of research and development (Bikker, 2016). With strong supplier base

companies generally faces low threat of new entertains in this industry.

Bargaining Power of the Buyers: Bargaining power of the consumers is relatively low with

limited number of companies with recognized operate in Australia and the buyers have very

little to choose from the firms providing service in this industry (Geneva, 2014).

Bargaining Power of Suppliers: There are ample of suppliers in the general insurance

industry. The facilities provided by the insurance companies such as large number of

suppliers generally provides medical coverage and lower premium service. Therefore, it can

be said that suppliers have higher power in this industry.

Threat of substitute: Threat of substitute products are generally low and the reason behind

this is that almost each products have identical facilities to offer. With base of suppliers it can

be said that the threat of substitute products are relatively lower.

Figure 3: Porter’s Five Forces Analysis

(Source: As created by author)

Existing Rivalry

Threat of New Entrants

Bargaining Power of Buyers

Bargainig Power of Suppliers

Threat of Substitute

money in the areas of research and development (Bikker, 2016). With strong supplier base

companies generally faces low threat of new entertains in this industry.

Bargaining Power of the Buyers: Bargaining power of the consumers is relatively low with

limited number of companies with recognized operate in Australia and the buyers have very

little to choose from the firms providing service in this industry (Geneva, 2014).

Bargaining Power of Suppliers: There are ample of suppliers in the general insurance

industry. The facilities provided by the insurance companies such as large number of

suppliers generally provides medical coverage and lower premium service. Therefore, it can

be said that suppliers have higher power in this industry.

Threat of substitute: Threat of substitute products are generally low and the reason behind

this is that almost each products have identical facilities to offer. With base of suppliers it can

be said that the threat of substitute products are relatively lower.

Figure 3: Porter’s Five Forces Analysis

(Source: As created by author)

Existing Rivalry

Threat of New Entrants

Bargaining Power of Buyers

Bargainig Power of Suppliers

Threat of Substitute

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.