Kaplan DFP2: Insurance and Risk Protection Written Assignment

VerifiedAdded on 2021/09/16

|39

|11019

|91

Homework Assignment

AI Summary

This document presents a complete written assignment solution for the Insurance and Risk Protection (DFP2_AS_v4) course. It includes a detailed case study involving a young couple, John and Elsbeth Smyth, and their need for insurance and financial planning. The assignment tasks require the completion of a fact finder template, analysis of the Smyths' financial situation, and responses to case study questions related to insurance needs, risk assessment, and product recommendations. The case study provides comprehensive information on the Smyths' income, expenses, assets, liabilities, and existing insurance coverage. The assignment aims to assess the student's ability to apply financial planning principles, evaluate risk, and recommend appropriate insurance solutions to meet the clients' needs. The assignment also references the oral assessment component, highlighting the integrated approach to evaluating the student's understanding of the subject matter. The provided solution demonstrates the application of financial planning knowledge and skills in a real-world scenario.

Written Assignment

Insurance and Risk Protection (DFP2_AS_v4)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written assignment result (assessor to complete)

Result — first submission (details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Fact finder Section 2 Not yet demonstrated Not yet demonstrated

Case study

assignment

questions

Section 3 Not yet demonstrated Not yet demonstrated

Section 4 Not yet demonstrated Not yet demonstrated

Section 5 Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

DFP2_AS_v4

Insurance and Risk Protection (DFP2_AS_v4)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written assignment result (assessor to complete)

Result — first submission (details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Fact finder Section 2 Not yet demonstrated Not yet demonstrated

Case study

assignment

questions

Section 3 Not yet demonstrated Not yet demonstrated

Section 4 Not yet demonstrated Not yet demonstrated

Section 5 Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

DFP2_AS_v4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Before you begin

Read everything in this document before you start your written assignment for Insurance and Risk

Protection (DFP2_AS_v4).

About this document

This document is the written assignment — half of the overall Written and Oral Assignment.

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Case study

• Insurance and Risk Protection assessment:

– Fact finder and risk profile template

– Case study questions

– Cash flow

– Assumptions.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Insurance and Risk

Protection (DFP2_AS_v4) subject room.

Instructions for completing and submitting this written

assignment

Completing the written assignment

You are required to complete the following tasks in this assignment document:

• complete the fact finder template for your clients (the risk profile template is included in this document

for you to view, but you are not required to complete the risk profile template for this assignment)

• answer the assignment questions as they relate to sections 3, 4 and 5 of the case study.

The information and data you need to do this work is presented as a case study. Some data will have to be

externally sourced; the templates clearly indicate where this will be necessary.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Page 2 of 39

Read everything in this document before you start your written assignment for Insurance and Risk

Protection (DFP2_AS_v4).

About this document

This document is the written assignment — half of the overall Written and Oral Assignment.

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Case study

• Insurance and Risk Protection assessment:

– Fact finder and risk profile template

– Case study questions

– Cash flow

– Assumptions.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Insurance and Risk

Protection (DFP2_AS_v4) subject room.

Instructions for completing and submitting this written

assignment

Completing the written assignment

You are required to complete the following tasks in this assignment document:

• complete the fact finder template for your clients (the risk profile template is included in this document

for you to view, but you are not required to complete the risk profile template for this assignment)

• answer the assignment questions as they relate to sections 3, 4 and 5 of the case study.

The information and data you need to do this work is presented as a case study. Some data will have to be

externally sourced; the templates clearly indicate where this will be necessary.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Page 2 of 39

Additional research

You will be required to source additional information from other organisations in the financial services

industry to find the right product/s to meet the Smyths’ requirements, and to calculate your service fees.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DFP2_AS_v4_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB. Once you submit your written assignment for marking, you will be unable

to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions in the Assessment section of

KapLearn for details on how to submit your written and Oral assignment.

Your Written Assignment and Oral Assignment must be submitted together, including; Written

assignment template (Word doc), Oral assignment template (Word doc) and Oral assignment audio

recording (M4A/MP3 file), on or before your due date. Please check KapLearn for the due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your written and oral assignment and return it to you in the Insurance and Risk

Protection (DFP2_AS_v4) subject room in KapLearn under the ‘Assessment’ tab.

Page 3 of 39

You will be required to source additional information from other organisations in the financial services

industry to find the right product/s to meet the Smyths’ requirements, and to calculate your service fees.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DFP2_AS_v4_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB. Once you submit your written assignment for marking, you will be unable

to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions in the Assessment section of

KapLearn for details on how to submit your written and Oral assignment.

Your Written Assignment and Oral Assignment must be submitted together, including; Written

assignment template (Word doc), Oral assignment template (Word doc) and Oral assignment audio

recording (M4A/MP3 file), on or before your due date. Please check KapLearn for the due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your written and oral assignment and return it to you in the Insurance and Risk

Protection (DFP2_AS_v4) subject room in KapLearn under the ‘Assessment’ tab.

Page 3 of 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the following process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written and oral assignment.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

Make changes to, but do not delete any part of your original submission. Use a different text colour for

your resubmission. Your assessor will be in a better position to gauge the quality and nature of your

changes. Ensure you leave your first assessor’s comments in your assignment, so your second assessor can

see the instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against this unit:

FNSASICX503 Provide advice in life insurance

Note that the Written and Oral Assignment is one of two assessments required to meet the requirements

of the units of competency.

Page 4 of 39

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the following process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written and oral assignment.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

Make changes to, but do not delete any part of your original submission. Use a different text colour for

your resubmission. Your assessor will be in a better position to gauge the quality and nature of your

changes. Ensure you leave your first assessor’s comments in your assignment, so your second assessor can

see the instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against this unit:

FNSASICX503 Provide advice in life insurance

Note that the Written and Oral Assignment is one of two assessments required to meet the requirements

of the units of competency.

Page 4 of 39

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

We are here to help

If you have any questions about this written assignment, you can post them at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 5 of 39

If you have any questions about this written assignment, you can post them at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 5 of 39

The case study

Section 1 — Meeting your client

The first phone call

John and Elsbeth Smyth are a young married couple with one child. Recently Chris, a business associate

of Elsbeth, who also has a young family, was seriously injured in a vehicle accident that has resulted in

uncertainty about his ability to return to work. John and Elsbeth have also learned that, due to inadequate

insurance cover, the family of the injured work colleague is now under financial stress. They do have some

insurance cover themselves, but are now unsure if it is adequate or suitable for their needs. Recalling a

positive experience, she had with you a few years ago on another financial matter, John and Elsbeth call to

see if you if you can help them with their insurance needs.

Over the phone you explain to John and Elsbeth the financial planning process and why you will need to ask

the couple for certain types of financial information. You stress that any information they give you will be

treated confidentially and will only be used to help you recommend an appropriate course of action that

the Smyths should consider to ultimately meet their needs. You give them information concerning privacy,

and you and your firm’s capability, and mention that other disclosure issues are in the firm’s financial

services guide (FSG) that you will send to them.

You go on to explain that part of the information gathering will include the need to complete a financial

profile. This means that they will need to tell you what they own, what they owe, what they earn and their

living expenses. All this information will be recorded in a fact finder form which you will compile.

You arrange a date and time for them to come to your office. You ask them to bring along as much financial

information as they can to the meeting, including income details, expenses, insurance details,

superannuation and investments. You also ask them to think about what specific financial goals they want

to achieve and any issues they wish to discuss at the meeting.

When you have concluded the call, you make a file note about the conversation including the date,

the potential clients’ names, and any other items that were discussed. This is the start of your paper trail.

You also complete some of the initial details in the data collection form as shown in Table 1.

Finally, you write to Elsbeth and John, as promised during your initial conversation, and include the FSG and

a checklist of the information they need to bring to the meeting.

Page 6 of 39

Section 1 — Meeting your client

The first phone call

John and Elsbeth Smyth are a young married couple with one child. Recently Chris, a business associate

of Elsbeth, who also has a young family, was seriously injured in a vehicle accident that has resulted in

uncertainty about his ability to return to work. John and Elsbeth have also learned that, due to inadequate

insurance cover, the family of the injured work colleague is now under financial stress. They do have some

insurance cover themselves, but are now unsure if it is adequate or suitable for their needs. Recalling a

positive experience, she had with you a few years ago on another financial matter, John and Elsbeth call to

see if you if you can help them with their insurance needs.

Over the phone you explain to John and Elsbeth the financial planning process and why you will need to ask

the couple for certain types of financial information. You stress that any information they give you will be

treated confidentially and will only be used to help you recommend an appropriate course of action that

the Smyths should consider to ultimately meet their needs. You give them information concerning privacy,

and you and your firm’s capability, and mention that other disclosure issues are in the firm’s financial

services guide (FSG) that you will send to them.

You go on to explain that part of the information gathering will include the need to complete a financial

profile. This means that they will need to tell you what they own, what they owe, what they earn and their

living expenses. All this information will be recorded in a fact finder form which you will compile.

You arrange a date and time for them to come to your office. You ask them to bring along as much financial

information as they can to the meeting, including income details, expenses, insurance details,

superannuation and investments. You also ask them to think about what specific financial goals they want

to achieve and any issues they wish to discuss at the meeting.

When you have concluded the call, you make a file note about the conversation including the date,

the potential clients’ names, and any other items that were discussed. This is the start of your paper trail.

You also complete some of the initial details in the data collection form as shown in Table 1.

Finally, you write to Elsbeth and John, as promised during your initial conversation, and include the FSG and

a checklist of the information they need to bring to the meeting.

Page 6 of 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

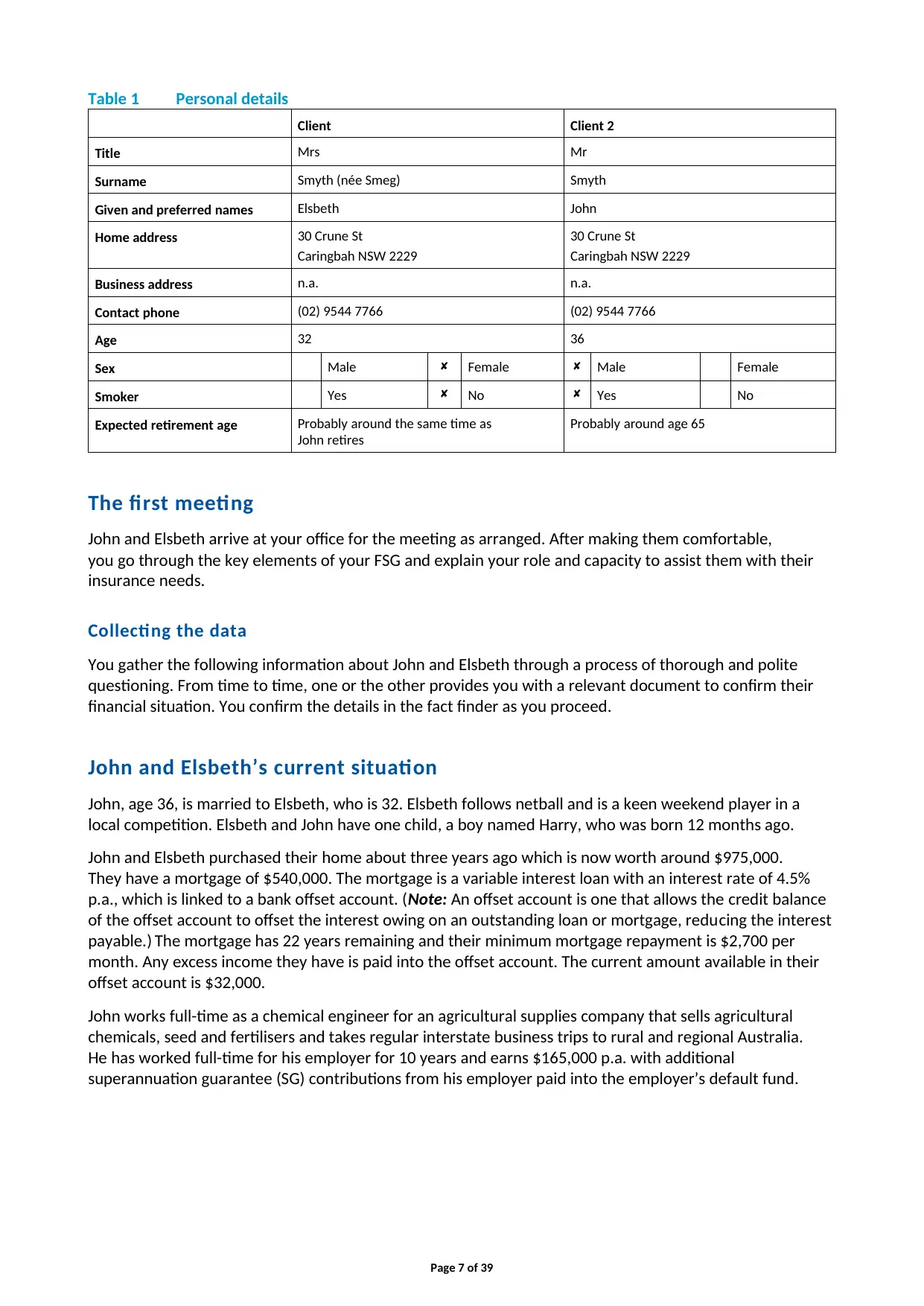

Table 1 Personal details

Client Client 2

Title Mrs Mr

Surname Smyth (née Smeg) Smyth

Given and preferred names Elsbeth John

Home address 30 Crune St

Caringbah NSW 2229

30 Crune St

Caringbah NSW 2229

Business address n.a. n.a.

Contact phone (02) 9544 7766 (02) 9544 7766

Age 32 36

Sex Male Female Male Female

Smoker Yes No Yes No

Expected retirement age Probably around the same time as

John retires

Probably around age 65

The first meeting

John and Elsbeth arrive at your office for the meeting as arranged. After making them comfortable,

you go through the key elements of your FSG and explain your role and capacity to assist them with their

insurance needs.

Collecting the data

You gather the following information about John and Elsbeth through a process of thorough and polite

questioning. From time to time, one or the other provides you with a relevant document to confirm their

financial situation. You confirm the details in the fact finder as you proceed.

John and Elsbeth’s current situation

John, age 36, is married to Elsbeth, who is 32. Elsbeth follows netball and is a keen weekend player in a

local competition. Elsbeth and John have one child, a boy named Harry, who was born 12 months ago.

John and Elsbeth purchased their home about three years ago which is now worth around $975,000.

They have a mortgage of $540,000. The mortgage is a variable interest loan with an interest rate of 4.5%

p.a., which is linked to a bank offset account. (Note: An offset account is one that allows the credit balance

of the offset account to offset the interest owing on an outstanding loan or mortgage, reducing the interest

payable.) The mortgage has 22 years remaining and their minimum mortgage repayment is $2,700 per

month. Any excess income they have is paid into the offset account. The current amount available in their

offset account is $32,000.

John works full-time as a chemical engineer for an agricultural supplies company that sells agricultural

chemicals, seed and fertilisers and takes regular interstate business trips to rural and regional Australia.

He has worked full-time for his employer for 10 years and earns $165,000 p.a. with additional

superannuation guarantee (SG) contributions from his employer paid into the employer’s default fund.

Page 7 of 39

Client Client 2

Title Mrs Mr

Surname Smyth (née Smeg) Smyth

Given and preferred names Elsbeth John

Home address 30 Crune St

Caringbah NSW 2229

30 Crune St

Caringbah NSW 2229

Business address n.a. n.a.

Contact phone (02) 9544 7766 (02) 9544 7766

Age 32 36

Sex Male Female Male Female

Smoker Yes No Yes No

Expected retirement age Probably around the same time as

John retires

Probably around age 65

The first meeting

John and Elsbeth arrive at your office for the meeting as arranged. After making them comfortable,

you go through the key elements of your FSG and explain your role and capacity to assist them with their

insurance needs.

Collecting the data

You gather the following information about John and Elsbeth through a process of thorough and polite

questioning. From time to time, one or the other provides you with a relevant document to confirm their

financial situation. You confirm the details in the fact finder as you proceed.

John and Elsbeth’s current situation

John, age 36, is married to Elsbeth, who is 32. Elsbeth follows netball and is a keen weekend player in a

local competition. Elsbeth and John have one child, a boy named Harry, who was born 12 months ago.

John and Elsbeth purchased their home about three years ago which is now worth around $975,000.

They have a mortgage of $540,000. The mortgage is a variable interest loan with an interest rate of 4.5%

p.a., which is linked to a bank offset account. (Note: An offset account is one that allows the credit balance

of the offset account to offset the interest owing on an outstanding loan or mortgage, reducing the interest

payable.) The mortgage has 22 years remaining and their minimum mortgage repayment is $2,700 per

month. Any excess income they have is paid into the offset account. The current amount available in their

offset account is $32,000.

John works full-time as a chemical engineer for an agricultural supplies company that sells agricultural

chemicals, seed and fertilisers and takes regular interstate business trips to rural and regional Australia.

He has worked full-time for his employer for 10 years and earns $165,000 p.a. with additional

superannuation guarantee (SG) contributions from his employer paid into the employer’s default fund.

Page 7 of 39

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Elsbeth has recently returned to work on a part-time basis (3 days a week) following maternity leave.

She is a marketing manager for a local engineering company and has also been with the same firm for

10 years. She earns $63,000 p.a. with additional SG contributions from her employer paid into the

employer’s default fund. Elsbeth advises during the meeting that she feels she would like to change her

current employment, and is considering starting up her own consulting business from home. This would

enable her to spend more time with their son.

They currently use a child care centre, as well as Elsbeth’s mother, to look after Harry when Elsbeth is at

work. The child care fees are $88 per day (not including the Child Care Rebate), which Elsbeth utilises

two days per week for 48 weeks per year. These expenses are not included in their day-to-day living

expenses. Elsbeth’s mother minds Harry for one day a week at no cost. Once Harry starts school,

Elsbeth and John hope to send him to the local independent school at a total cost of $65,000 for his whole

school life.

Other than their cash in the bank, superannuation holdings and house contents, the only other assets

they have are their motor vehicles. Elsbeth drives a recent model Ford Focus, currently valued at $11,000,

and John drives a late model Holden HSV performance vehicle, currently valued at $33,000. Both cars are

fully paid off and are comprehensively insured. All motor vehicle expenses (except insurance) are included

in the clients’ living expenses.

Superannuation

John has $260,000 in his employer’s default superannuation fund, the ASSF Super Fund, and is invested in a

balanced portfolio. He joined the fund on 1 February 2004.

Elsbeth has $114,000 in her employer’s default superannuation fund, the CISF Super Fund and is invested in

a balanced portfolio. Elsbeth joined the fund on 19 January 2004.

Neither Elsbeth nor John makes any additional contributions to their superannuation funds.

Insurance

John’s default superannuation fund provides a death and total and permanent disability (TPD) benefit

which is currently equal to his annual income (excluding SG contributions). The premium for this cover is

$1.25 p.a. for each $1,000 of cover or part thereof, and is deducted from his superannuation contributions.

The ASSF Super Fund will allow a member to increase their benefit to twice the member’s annual salary at

this premium rate. The fund will allow a further increase in cover to a maximum of $750,000. However,

the premium will increase to $1.50 per $1,000 for any amount of cover that is over twice the member’s

annual salary. John’s superannuation fund can provide income protection cover with a 30 to 90-day waiting

period, and a two-year to age 65 benefit period. He has not taken out this cover.

Elsbeth’s default superannuation fund also provides a death and TPD benefit and she currently has cover of

$126,000 for each of life and TPD. The premium for this level of cover is $143 p.a. deducted from her

superannuation contributions. The CISF Super Fund allows for members to further increase their cover to a

maximum of $2 million and on the following premium scale:

• ≤$500,000 — $1.19 p.a. per $1,000 of cover

• $500,001 to $1 million — $1.45 p.a. per $1,000 of cover

• $1 million to $2 million — $1.65 p.a. per $1,000 of cover.

Elsbeth and John have no other personal insurance cover (except health insurance as per below).

They have full comprehensive insurance on their vehicles with a total annual premium of $2,800 p.a.

Page 8 of 39

She is a marketing manager for a local engineering company and has also been with the same firm for

10 years. She earns $63,000 p.a. with additional SG contributions from her employer paid into the

employer’s default fund. Elsbeth advises during the meeting that she feels she would like to change her

current employment, and is considering starting up her own consulting business from home. This would

enable her to spend more time with their son.

They currently use a child care centre, as well as Elsbeth’s mother, to look after Harry when Elsbeth is at

work. The child care fees are $88 per day (not including the Child Care Rebate), which Elsbeth utilises

two days per week for 48 weeks per year. These expenses are not included in their day-to-day living

expenses. Elsbeth’s mother minds Harry for one day a week at no cost. Once Harry starts school,

Elsbeth and John hope to send him to the local independent school at a total cost of $65,000 for his whole

school life.

Other than their cash in the bank, superannuation holdings and house contents, the only other assets

they have are their motor vehicles. Elsbeth drives a recent model Ford Focus, currently valued at $11,000,

and John drives a late model Holden HSV performance vehicle, currently valued at $33,000. Both cars are

fully paid off and are comprehensively insured. All motor vehicle expenses (except insurance) are included

in the clients’ living expenses.

Superannuation

John has $260,000 in his employer’s default superannuation fund, the ASSF Super Fund, and is invested in a

balanced portfolio. He joined the fund on 1 February 2004.

Elsbeth has $114,000 in her employer’s default superannuation fund, the CISF Super Fund and is invested in

a balanced portfolio. Elsbeth joined the fund on 19 January 2004.

Neither Elsbeth nor John makes any additional contributions to their superannuation funds.

Insurance

John’s default superannuation fund provides a death and total and permanent disability (TPD) benefit

which is currently equal to his annual income (excluding SG contributions). The premium for this cover is

$1.25 p.a. for each $1,000 of cover or part thereof, and is deducted from his superannuation contributions.

The ASSF Super Fund will allow a member to increase their benefit to twice the member’s annual salary at

this premium rate. The fund will allow a further increase in cover to a maximum of $750,000. However,

the premium will increase to $1.50 per $1,000 for any amount of cover that is over twice the member’s

annual salary. John’s superannuation fund can provide income protection cover with a 30 to 90-day waiting

period, and a two-year to age 65 benefit period. He has not taken out this cover.

Elsbeth’s default superannuation fund also provides a death and TPD benefit and she currently has cover of

$126,000 for each of life and TPD. The premium for this level of cover is $143 p.a. deducted from her

superannuation contributions. The CISF Super Fund allows for members to further increase their cover to a

maximum of $2 million and on the following premium scale:

• ≤$500,000 — $1.19 p.a. per $1,000 of cover

• $500,001 to $1 million — $1.45 p.a. per $1,000 of cover

• $1 million to $2 million — $1.65 p.a. per $1,000 of cover.

Elsbeth and John have no other personal insurance cover (except health insurance as per below).

They have full comprehensive insurance on their vehicles with a total annual premium of $2,800 p.a.

Page 8 of 39

Elsbeth and John also have combined home building and contents insurance cover of:

• $100,000 home contents

• $750,000 home building.

Their home was built under an earlier version of the local building code. Additionally, the home was

purchased in a much lower market than the current one and is estimated to cost much more than

the $675,000 purchase price to replace. The policy has a contents excess of $500 and a building excess

of $1,100. The policy also includes legal liability cover of up to $20 million. Elsbeth and John pay

$145 per month for this insurance.

The Smyths have adequate private health insurance cover; this is the family cover option and includes

hospital cover with a $500 excess. They pay a premium of $270 per month for this cover. This premium

includes the private health insurance rebate. The above vehicle, home and contents and health insurance

payments are not included in their general living expenses.

Other information

John and Elsbeth have a credit card with a limit of $15,000 that they use for all their general expenses and

entertainment. However, they never spend up to their limit and always repay within the interest-free

period. They estimate their average monthly living expenses are $6,900 per month.

John and Elsbeth used to go on regular annual holidays and spent over $10,000 per trip. However, since the

start of their mortgage and the birth of Harry they now plan to take a holiday every two years spending

about $5,000, in addition to their general living expenses.

John advises he is quite healthy and has accumulated 78 days sick leave. However, he advises that he was

diagnosed with asthma symptoms in the past for which he was prescribed medication. He has not

experienced a return of these symptoms during the past couple of years. Elsbeth took all her accumulated

annual and long service leave as part of her maternity leave.

Other expenses include a donation by Elsbeth to the National Breast Cancer Foundation of $50 per month

and John makes a tax-deductible donation to Plan B of $50 per month. They each make tax-deductible

‘bucket’ donations of $50 p.a. to disaster relief funds, and accountants’ expenses come to $150 p.a. each.

These expenses are also in addition to their general living expenses.

Needs and objectives

During your conversation with John and Elsbeth, it becomes apparent that their main objective is to protect

their home and to provide for their son Harry.

Elsbeth commented that she is very concerned that they may not be able to maintain their lifestyle if either

of them died or suffered a prolonged illness. She would like to make sure that if anything were to happen

to them, Harry would be well taken care of.

At this time, they are not yet concerned with superannuation and retirement planning, believing that it is

still a long way off and that they will have time to address this part of their financial plan in the future.

Elsbeth and John have a full and comprehensive estate plan that John insisted on when they were married,

and which was updated when they purchased their house and on the birth of Harry. Also, Elsbeth’s mother

has agreed to increase her care of Harry to three days per week if anything were to happen to

Elsbeth (i.e. death or total and permanent disablement).

Page 9 of 39

• $100,000 home contents

• $750,000 home building.

Their home was built under an earlier version of the local building code. Additionally, the home was

purchased in a much lower market than the current one and is estimated to cost much more than

the $675,000 purchase price to replace. The policy has a contents excess of $500 and a building excess

of $1,100. The policy also includes legal liability cover of up to $20 million. Elsbeth and John pay

$145 per month for this insurance.

The Smyths have adequate private health insurance cover; this is the family cover option and includes

hospital cover with a $500 excess. They pay a premium of $270 per month for this cover. This premium

includes the private health insurance rebate. The above vehicle, home and contents and health insurance

payments are not included in their general living expenses.

Other information

John and Elsbeth have a credit card with a limit of $15,000 that they use for all their general expenses and

entertainment. However, they never spend up to their limit and always repay within the interest-free

period. They estimate their average monthly living expenses are $6,900 per month.

John and Elsbeth used to go on regular annual holidays and spent over $10,000 per trip. However, since the

start of their mortgage and the birth of Harry they now plan to take a holiday every two years spending

about $5,000, in addition to their general living expenses.

John advises he is quite healthy and has accumulated 78 days sick leave. However, he advises that he was

diagnosed with asthma symptoms in the past for which he was prescribed medication. He has not

experienced a return of these symptoms during the past couple of years. Elsbeth took all her accumulated

annual and long service leave as part of her maternity leave.

Other expenses include a donation by Elsbeth to the National Breast Cancer Foundation of $50 per month

and John makes a tax-deductible donation to Plan B of $50 per month. They each make tax-deductible

‘bucket’ donations of $50 p.a. to disaster relief funds, and accountants’ expenses come to $150 p.a. each.

These expenses are also in addition to their general living expenses.

Needs and objectives

During your conversation with John and Elsbeth, it becomes apparent that their main objective is to protect

their home and to provide for their son Harry.

Elsbeth commented that she is very concerned that they may not be able to maintain their lifestyle if either

of them died or suffered a prolonged illness. She would like to make sure that if anything were to happen

to them, Harry would be well taken care of.

At this time, they are not yet concerned with superannuation and retirement planning, believing that it is

still a long way off and that they will have time to address this part of their financial plan in the future.

Elsbeth and John have a full and comprehensive estate plan that John insisted on when they were married,

and which was updated when they purchased their house and on the birth of Harry. Also, Elsbeth’s mother

has agreed to increase her care of Harry to three days per week if anything were to happen to

Elsbeth (i.e. death or total and permanent disablement).

Page 9 of 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Closing the interview

Prior to closing the interview, you review the information provided by Elsbeth and John to check whether it

is complete. You answer some additional questions they have about what happens next and what your

likely costs will be, and explain that with their agreement you will now prepare a written financial plan,

called a statement of advice (SOA), based on the information collected and their stated objectives.

The SOA will describe possible risk management strategies and insurances they should consider, and the

reasons behind your recommendations.

John and Elsbeth agree to proceed to the next stage of the financial planning process, and you make an

appointment to present the SOA in a fortnight.

Note: You are not required to complete a full and comprehensive SOA in this assignment.

Section 2 — The fact finder

The first step is to complete the fact finder for John and Elsbeth. Refer to section 2 of your Insurance and

Risk assignment.

Note to completing the fact finder: As this is a ‘risk’ assignment, you must complete the ‘Risk needs’ section.

However, where information has not been provided in the case study background, you may leave these

sections blank.

Page 10 of 39

Prior to closing the interview, you review the information provided by Elsbeth and John to check whether it

is complete. You answer some additional questions they have about what happens next and what your

likely costs will be, and explain that with their agreement you will now prepare a written financial plan,

called a statement of advice (SOA), based on the information collected and their stated objectives.

The SOA will describe possible risk management strategies and insurances they should consider, and the

reasons behind your recommendations.

John and Elsbeth agree to proceed to the next stage of the financial planning process, and you make an

appointment to present the SOA in a fortnight.

Note: You are not required to complete a full and comprehensive SOA in this assignment.

Section 2 — The fact finder

The first step is to complete the fact finder for John and Elsbeth. Refer to section 2 of your Insurance and

Risk assignment.

Note to completing the fact finder: As this is a ‘risk’ assignment, you must complete the ‘Risk needs’ section.

However, where information has not been provided in the case study background, you may leave these

sections blank.

Page 10 of 39

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 3 — Analysing the data

The next step in the financial planning process is to analyse the collected data. You do this so that you

can fully understand your clients’ needs and therefore design a financial plan that addresses their goals

and objectives.

By analysing the data provided under the following headings, you can start preparing a financial planning

strategy that will meet your clients’ needs:

• Review the fact-finding stage

• Current position

• Debt management

• Risk/protection

• Savings

• Present and future taxation issues.

Note: There are a series of questions relating to section 3 in the assignment that you must answer.

Use your answers for section 3 to help you decide on your recommendations for John and Elsbeth.

Your answers to these questions are your opportunity to demonstrate your ability to analyse the clients’

needs in preparation for developing a strategy that aligns with their requirements.

Section 4 — The strategy

Now that you have analysed the data, you are in a position to think about appropriate strategy options and

start drafting appropriate strategies for them. This should include levels of cover and researching possible

products that can support the implementation of those strategies. You will use all of this information in

your SOA for the couple.

Note: There are a series of questions relating to section 4 in the assignment that you must answer.

You will use your answers for section 4 to help you decide on your recommendations for John and Elsbeth.

Your answers to these questions are your opportunity to demonstrate your ability to analyse your clients’

needs and develop a strategy that aligns with their requirements.

Section 5 — Presenting the SOA

You meet with John and Elsbeth as arranged to present the SOA. You take the time to reiterate their

financial situation and stated objectives and to explain the proposed strategies and recommendations,

confirming regularly that both John and Elsbeth understand each component of the plan and how it meets

their needs.

Even though satisfied with your explanation of the SOA and responses to each of their questions,

they have a key concern about one of the products you have selected with regards to the cost of premiums.

Before they agree to your recommendations you have to negotiate this part of the plan with your clients.

Note: There is a series of questions relating to section 5 in the assignment that you must answer.

Your answers to these questions are your opportunity to demonstrate your ability to continue to engage

your clients.

Page 11 of 39

The next step in the financial planning process is to analyse the collected data. You do this so that you

can fully understand your clients’ needs and therefore design a financial plan that addresses their goals

and objectives.

By analysing the data provided under the following headings, you can start preparing a financial planning

strategy that will meet your clients’ needs:

• Review the fact-finding stage

• Current position

• Debt management

• Risk/protection

• Savings

• Present and future taxation issues.

Note: There are a series of questions relating to section 3 in the assignment that you must answer.

Use your answers for section 3 to help you decide on your recommendations for John and Elsbeth.

Your answers to these questions are your opportunity to demonstrate your ability to analyse the clients’

needs in preparation for developing a strategy that aligns with their requirements.

Section 4 — The strategy

Now that you have analysed the data, you are in a position to think about appropriate strategy options and

start drafting appropriate strategies for them. This should include levels of cover and researching possible

products that can support the implementation of those strategies. You will use all of this information in

your SOA for the couple.

Note: There are a series of questions relating to section 4 in the assignment that you must answer.

You will use your answers for section 4 to help you decide on your recommendations for John and Elsbeth.

Your answers to these questions are your opportunity to demonstrate your ability to analyse your clients’

needs and develop a strategy that aligns with their requirements.

Section 5 — Presenting the SOA

You meet with John and Elsbeth as arranged to present the SOA. You take the time to reiterate their

financial situation and stated objectives and to explain the proposed strategies and recommendations,

confirming regularly that both John and Elsbeth understand each component of the plan and how it meets

their needs.

Even though satisfied with your explanation of the SOA and responses to each of their questions,

they have a key concern about one of the products you have selected with regards to the cost of premiums.

Before they agree to your recommendations you have to negotiate this part of the plan with your clients.

Note: There is a series of questions relating to section 5 in the assignment that you must answer.

Your answers to these questions are your opportunity to demonstrate your ability to continue to engage

your clients.

Page 11 of 39

Assignment

Fact finder — John and Elsbeth Smyth

Use the data collected in the interviews to complete the fact finder template on the following pages.

Note: As investment strategies are not required for this assignment, it is not necessary to complete the risk

profile section of the fact finder.

Important notice to clients

Your adviser must have reasonable grounds for making investment or insurance recommendations.

Before making a recommendation, the adviser must ask you about your investment objectives,

financial situation and your particular needs.

The information requested in this form will be used strictly for that purpose.

Warning

The adviser could make inappropriate recommendations or give inappropriate advice if you fail to fully and

accurately complete this form.

Page 12 of 39

Fact finder — John and Elsbeth Smyth

Use the data collected in the interviews to complete the fact finder template on the following pages.

Note: As investment strategies are not required for this assignment, it is not necessary to complete the risk

profile section of the fact finder.

Important notice to clients

Your adviser must have reasonable grounds for making investment or insurance recommendations.

Before making a recommendation, the adviser must ask you about your investment objectives,

financial situation and your particular needs.

The information requested in this form will be used strictly for that purpose.

Warning

The adviser could make inappropriate recommendations or give inappropriate advice if you fail to fully and

accurately complete this form.

Page 12 of 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.