University ACCT3003: Intangible Asset Valuation Client Briefing Report

VerifiedAdded on 2022/11/29

|7

|627

|234

Report

AI Summary

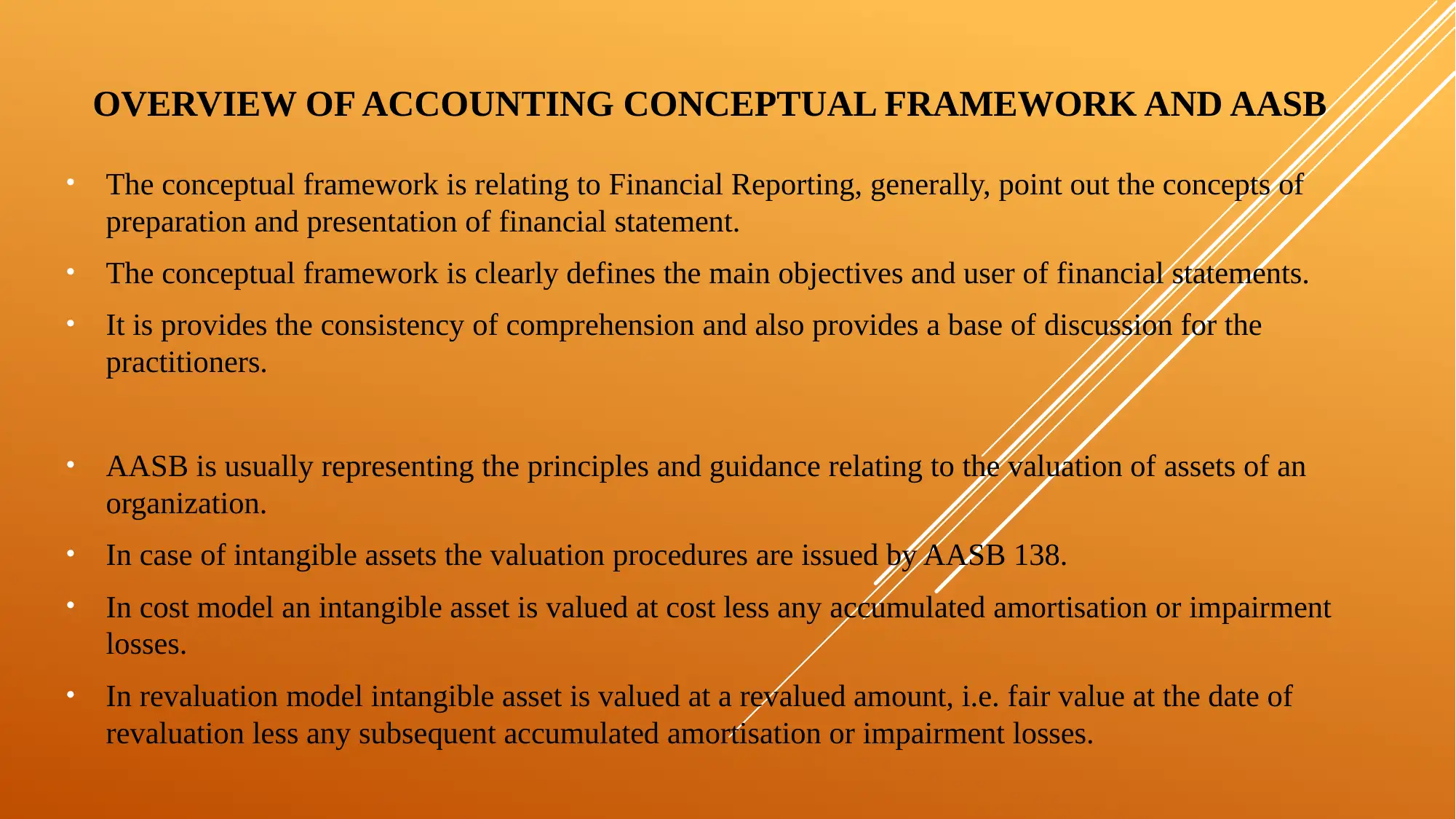

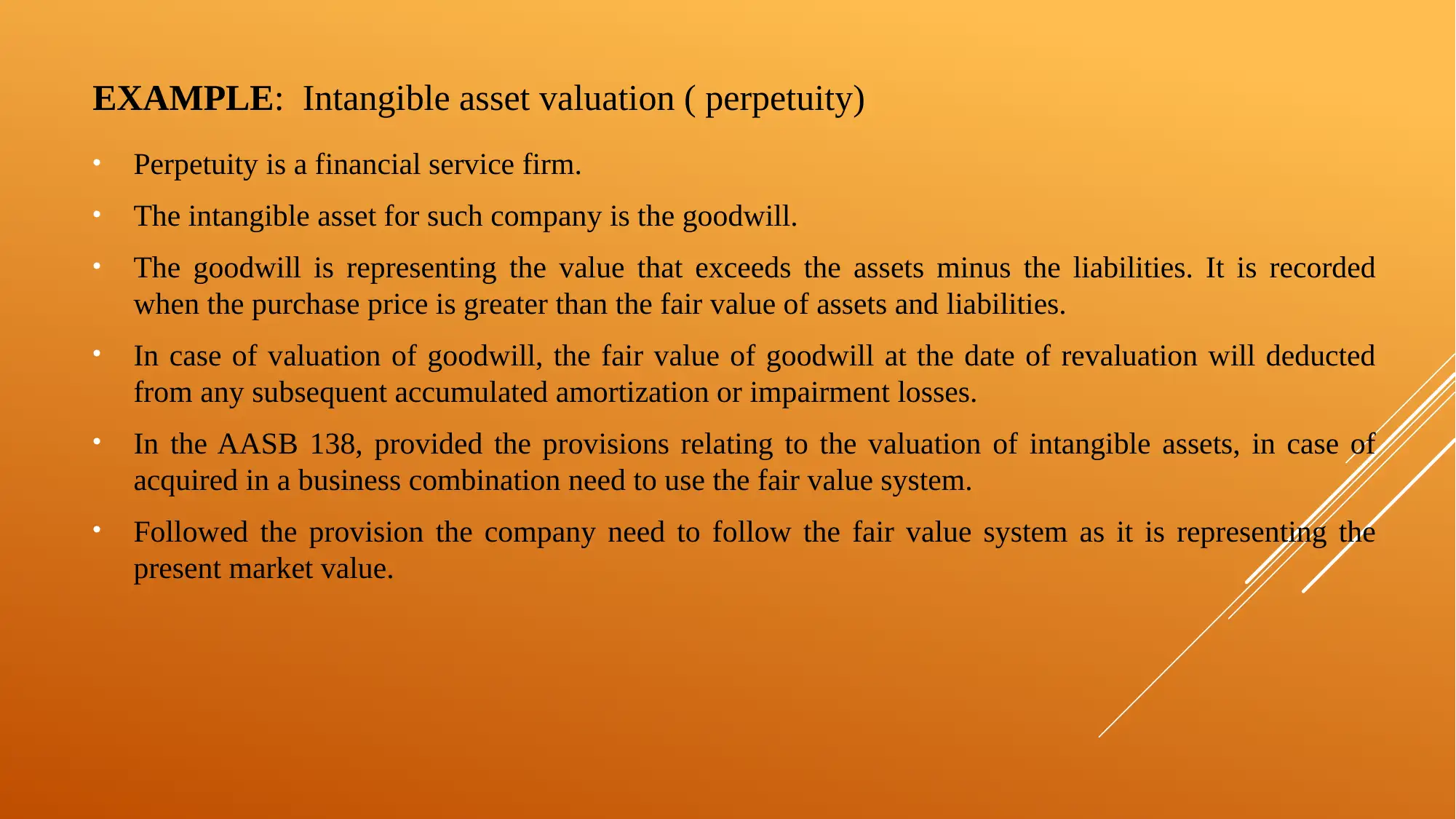

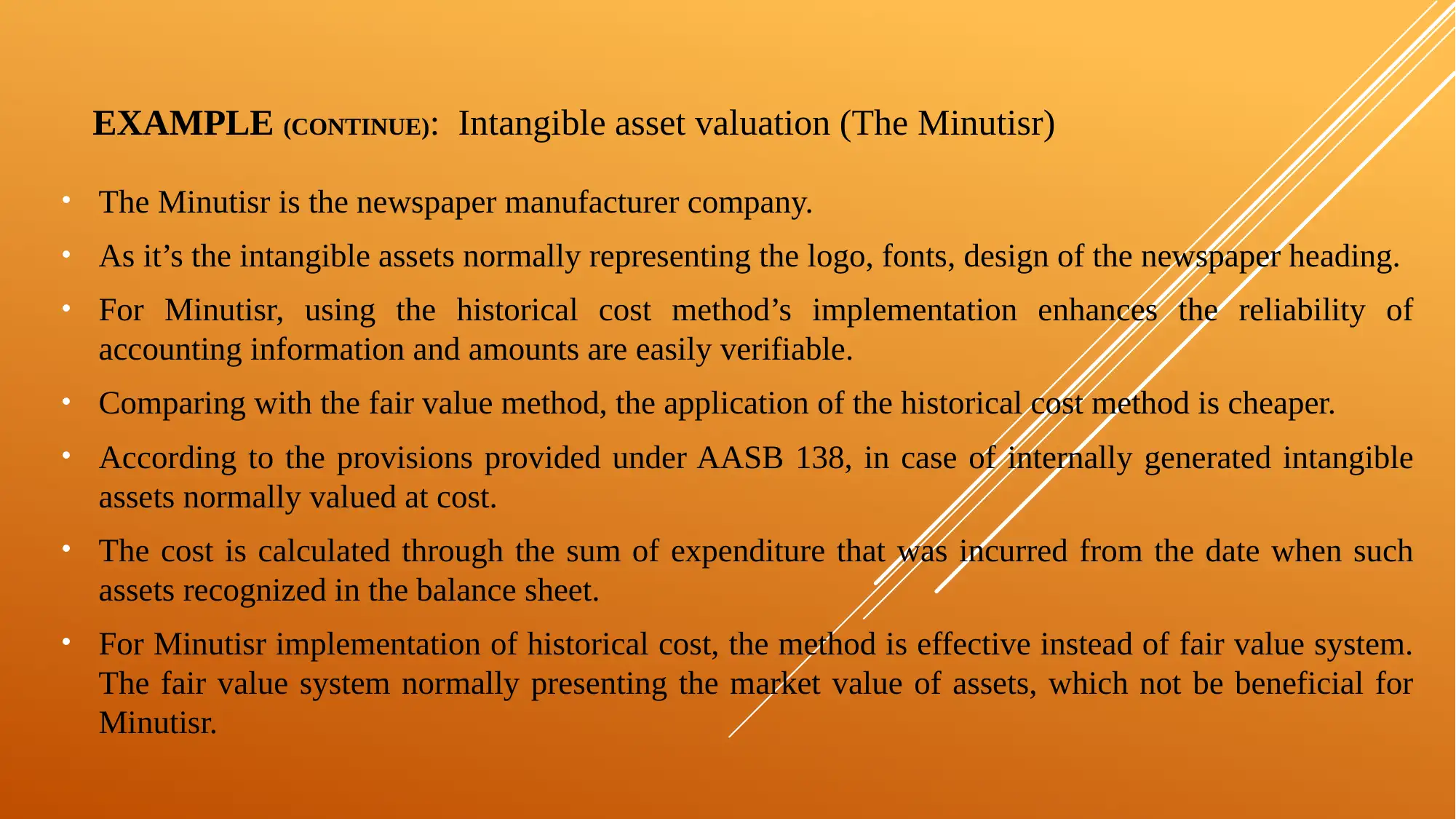

This report provides a client briefing on contemporary issues in accounting, focusing on the valuation of intangible assets. It begins with an overview of the accounting conceptual framework and AASB, specifically AASB 138, which provides guidance on intangible asset valuation. The report discusses the cost model and revaluation model, using examples of perpetuity (goodwill) and The Minutisr (logos, fonts, etc.) to illustrate the application of historical cost versus fair value methods. The analysis highlights the considerations for choosing between these valuation methods, emphasizing the reliability and verifiability of accounting information. The report concludes by referencing relevant IASB publications and research on accounting principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.