Financial Accounting Report: AASB 138/IAS 38 and Intangible Assets

VerifiedAdded on 2022/09/05

|9

|3117

|19

Report

AI Summary

This report delves into the intricacies of financial accounting for intangible assets, with a specific focus on the impacts of AASB 138/IAS 38 (and IAS 38) on internally generated intangible assets. The report examines changes and improvements in accounting practices brought about by these standards, particularly in Australia. It contrasts the accounting treatments for internally generated versus acquired intangible assets, highlighting differences in recognition and measurement criteria. Furthermore, the report explores the reasons why companies might be reluctant to fully embrace changes in accounting practices for these assets. The report includes a discussion of goodwill calculation and concludes with recommendations for improved financial reporting, aiming to provide investors and other stakeholders with a clearer understanding of intangible asset valuation.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Executive Summary

Accounting for intangible assets has attracted key attention in the recent time because the

companies are facing challenges in correctly account for the internally generated intangible

assets. The adoption of wrong accounting treatment either internationally or unintentionally is

contributing towards the major differences in the accounting numbers in the financial

statements of the companies. AASB 138 Intangible Assets/IAS 38 Intangible Assets (AASB

138/IAS 38) provides the required standards and regulations for the accounting of intangible

assets.

Executive Summary

Accounting for intangible assets has attracted key attention in the recent time because the

companies are facing challenges in correctly account for the internally generated intangible

assets. The adoption of wrong accounting treatment either internationally or unintentionally is

contributing towards the major differences in the accounting numbers in the financial

statements of the companies. AASB 138 Intangible Assets/IAS 38 Intangible Assets (AASB

138/IAS 38) provides the required standards and regulations for the accounting of intangible

assets.

2FINANCIAL ACCOUNTING

Table of Contents

1. Introduction............................................................................................................................3

2. Impacts of AASB 138/IAS 38 for Internally Generated Intangible Assets...........................3

2.1 Change in the Accounting for Internally Generated Intangible Assets............................3

2.2 Improvement in the Accounting for Internally Generated Intangible Assets...................3

3. Dissimilarities between Internal Intangible Assets and Acquired Intangible Assets.............4

3.1 Recognition Criteria.........................................................................................................4

3.2 Measurement Criteria.......................................................................................................5

4. Reasons for the Companies to be Reluctant...........................................................................6

5. Conclusion and Recommendation..........................................................................................6

6. References..............................................................................................................................8

Table of Contents

1. Introduction............................................................................................................................3

2. Impacts of AASB 138/IAS 38 for Internally Generated Intangible Assets...........................3

2.1 Change in the Accounting for Internally Generated Intangible Assets............................3

2.2 Improvement in the Accounting for Internally Generated Intangible Assets...................3

3. Dissimilarities between Internal Intangible Assets and Acquired Intangible Assets.............4

3.1 Recognition Criteria.........................................................................................................4

3.2 Measurement Criteria.......................................................................................................5

4. Reasons for the Companies to be Reluctant...........................................................................6

5. Conclusion and Recommendation..........................................................................................6

6. References..............................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

1. Introduction

Accounting for intangible assets is considered as a major part of the financial

reporting related operations of the companies and the managements are required to take into

consideration all the required factors while accounting for intangible assets (Vetoshkina and

Tukhvatullin, 2014). One crucial factor is to correctly account for the intangible assets that

are generated internally and the intangible assets that are acquired. It is the responsibility of

the managements of the companies to correctly account for these two types of intangible

assets by complying with the required rules and standards (Yallwe and Buscemi, 2014).

However, the presence of a tendency can be seen among the senior managements of the firms

to account for the intangible asset differently for certain personal benefits. This report aims at

discussing the impacts of AASB 138/IAS 38 on the internally generated intangible assets.

After that, this report discusses about the dissimilarities amid the accounting treatments for

two types of intangible assets. Lastly, it sheds light on the unwillingness of the companies to

press for change in the accounting for intangible assets. On the basis of the whole discussion,

the report contains a conclusion part at the end.

2. Impacts of AASB 138/IAS 38 for Internally Generated Intangible Assets

2.1 Change in the Accounting for Internally Generated Intangible Assets

In Australia, the accounting board has announced the inception of AASB 138/IAS 38

so that the accounts of the Australian business organizations can get the necessary accounting

standards for intangible assets accounting. Two variance of intangible assets are acquired

intangible assets and internally generated intangible assets. This has created certain

differences in the accounting processes for internally generated intangible assets as the

accountants are not require to follow accounting policies that contribute to more appropriate

bookkeeping of internally generated intangible assets (Ji and Lu, 2014). The accounting for

internally generated intangible assets is largely influenced due to the introduction of new

processes for recognizing and measuring the variances of intangible assets. Therefore, the

accounting methods adopted by the Australian companies are positively influence in a key

manner. One of the major changes in the accounting processes for the internally generated

intangible assets due to the inception of 138/IAS 38 is the recognition as well as

measurement of this types of asset only when the definition of intangible assets is satisfied by

these assets. It implies that the managements of the companies are restricted from the

recognition and measurement of internally generated intangible assets when these criteria are

not satisfied. All these have positively impacted the accounting for internally generated

intangible assets (Jaafar and Halim, 2013).

2.2 Improvement in the Accounting for Internally Generated Intangible Assets

According to AASB 138/IAS 38, the business entities should follow all the provided

criteria to account for the internally generated intangible assets. In order to examine whether

an internally generated intangible asset satisfies the standards of recognition, the generation

of assets is classified into two particular phases; they are a research phase and a development

phase (Ratiu and Tudor, 2013). However, the companies cannot recognize all of these assets

as there is obligation put by AASB 138/IAS 38 which restricts the companies from the

recognition of goodwill, brands, publishing titles, mastheads, customer lists and others under

internally generated intangible assets. Most importantly, there are six conditions that need to

be demonstrated for the recognition of intangible assets from development stage; they are the

technical feasibility to complete the intangible asset for making it available to use or sale, the

intention of completing the intangible asset so that it can be used or sold, the ability for

selling or using the intangible asset, the procedures to generated probable future economic

benefit by the intangible asset, the accessibility of sufficient financial, technical and other

1. Introduction

Accounting for intangible assets is considered as a major part of the financial

reporting related operations of the companies and the managements are required to take into

consideration all the required factors while accounting for intangible assets (Vetoshkina and

Tukhvatullin, 2014). One crucial factor is to correctly account for the intangible assets that

are generated internally and the intangible assets that are acquired. It is the responsibility of

the managements of the companies to correctly account for these two types of intangible

assets by complying with the required rules and standards (Yallwe and Buscemi, 2014).

However, the presence of a tendency can be seen among the senior managements of the firms

to account for the intangible asset differently for certain personal benefits. This report aims at

discussing the impacts of AASB 138/IAS 38 on the internally generated intangible assets.

After that, this report discusses about the dissimilarities amid the accounting treatments for

two types of intangible assets. Lastly, it sheds light on the unwillingness of the companies to

press for change in the accounting for intangible assets. On the basis of the whole discussion,

the report contains a conclusion part at the end.

2. Impacts of AASB 138/IAS 38 for Internally Generated Intangible Assets

2.1 Change in the Accounting for Internally Generated Intangible Assets

In Australia, the accounting board has announced the inception of AASB 138/IAS 38

so that the accounts of the Australian business organizations can get the necessary accounting

standards for intangible assets accounting. Two variance of intangible assets are acquired

intangible assets and internally generated intangible assets. This has created certain

differences in the accounting processes for internally generated intangible assets as the

accountants are not require to follow accounting policies that contribute to more appropriate

bookkeeping of internally generated intangible assets (Ji and Lu, 2014). The accounting for

internally generated intangible assets is largely influenced due to the introduction of new

processes for recognizing and measuring the variances of intangible assets. Therefore, the

accounting methods adopted by the Australian companies are positively influence in a key

manner. One of the major changes in the accounting processes for the internally generated

intangible assets due to the inception of 138/IAS 38 is the recognition as well as

measurement of this types of asset only when the definition of intangible assets is satisfied by

these assets. It implies that the managements of the companies are restricted from the

recognition and measurement of internally generated intangible assets when these criteria are

not satisfied. All these have positively impacted the accounting for internally generated

intangible assets (Jaafar and Halim, 2013).

2.2 Improvement in the Accounting for Internally Generated Intangible Assets

According to AASB 138/IAS 38, the business entities should follow all the provided

criteria to account for the internally generated intangible assets. In order to examine whether

an internally generated intangible asset satisfies the standards of recognition, the generation

of assets is classified into two particular phases; they are a research phase and a development

phase (Ratiu and Tudor, 2013). However, the companies cannot recognize all of these assets

as there is obligation put by AASB 138/IAS 38 which restricts the companies from the

recognition of goodwill, brands, publishing titles, mastheads, customer lists and others under

internally generated intangible assets. Most importantly, there are six conditions that need to

be demonstrated for the recognition of intangible assets from development stage; they are the

technical feasibility to complete the intangible asset for making it available to use or sale, the

intention of completing the intangible asset so that it can be used or sold, the ability for

selling or using the intangible asset, the procedures to generated probable future economic

benefit by the intangible asset, the accessibility of sufficient financial, technical and other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

resources for completing the development of the intangible asset so that it can be used or

sold, and the ability of reliably measuring the expenditures incurred for the development of

the intangible asset (Radu and Isai, 2014). Apart from these, AASB 138/IAS 38 prescribes

the required measurement criteria at recognition of the internal intangible assets and this

makes the financial accounting of these assets more dependable due to the presence of

acceptable recognition criteria and measurement method. A company is required to undertake

the measurement of an internally generated intangible asset at cost with cost determined as

the sum of incurred expenditures from the date of first meeting the recognition criteria

(Cosmulese, Grosu and Hlaciuc, 2017).

Therefore, it can be seen from the above analysis that rules and regulations of AASB

138/IAS 38 ensures the accounting of internally generated intangible assets in the most

appropriate and systematic manner. These standards also reduce the scope to do manipulation

in the accounting of internally generated intangible assets by the managements of the

companies (Ratiu and Tudor, 2013). All these create major impact on the assets and all these

impacts are required to be considered as the positive impact on the whole accounting

procedures of intangible assets in the accounting books. This helps the investors and other

users of the financial reports to assess the treatment of internal intangible assets in the

financial reports.

3. Dissimilarities between Internal Intangible Assets and Acquired Intangible Assets

AASB 138/IAS 38 prescribe the required accounting methods that need to be

monitored by the firms in the accounting of intangible assets that include both the intangible

assets. Now, it needs to be mentioned that there are certain dissimilarities between the

accounting treatment for internally generated intangible assets and acquired intangible assets

as mentioned in AASB 138/IAS 38. This difference can be seen in the recognition of these

two types of intangible assets.

3.1 Recognition Criteria

AASB 138/IAS 38 prescribe different recognition procedures for recognizing

internally generated intangible assets and acquired intangible assets. As per AASB 138,

Paragraph 21, a company needs to recognize an intangible asset in case a) there is a

likelihood of inflow of future economic benefit allied with the asset to the company; and b)

the company can dependably measure the cost of the asset. Since intangible assets are

acquired separately and generated internally, difference in the above-mentioned recognition

criteria can be seen. As per Paragraph 25 of AASB 138, the price paid by a company for

separately acquiring an intangible asset will reflect expectation about the probability that

there will be inflow economic benefit to the company (aasb.gov.au, 2019). For this reason,

the recognition criteria under Paragraph 21 (a) of AASB 138 needs to be considered as

appropriate. This same concept is also applicable in case of the intangible assets acquired as a

part of business combination since the asset is acquired at fair value that will reflect the

expectation of the probability to receive future economic benefit associated with the asset.

However, the recognition criteria for internally generated intangible assets are

different from the same of acquired intangible assets in accordance with AASB 138/IAS 38

(Pucci, et al., 2014). According to Paragraph 48 of AASB 138, a company is restricted from

recognizing any internally generated goodwill. This is because a company incur expenditures

for generating future economic benefit, but there is not any creation of intangible asset for

meeting the recognition criteria. As per Paragraph 51 of AASB 138, there is sometimes

difficulty in assessing whether an internal intangible asset is qualified to be recognizes in the

presence of two problems in identifying whether and when an identifiable asset is there for

resources for completing the development of the intangible asset so that it can be used or

sold, and the ability of reliably measuring the expenditures incurred for the development of

the intangible asset (Radu and Isai, 2014). Apart from these, AASB 138/IAS 38 prescribes

the required measurement criteria at recognition of the internal intangible assets and this

makes the financial accounting of these assets more dependable due to the presence of

acceptable recognition criteria and measurement method. A company is required to undertake

the measurement of an internally generated intangible asset at cost with cost determined as

the sum of incurred expenditures from the date of first meeting the recognition criteria

(Cosmulese, Grosu and Hlaciuc, 2017).

Therefore, it can be seen from the above analysis that rules and regulations of AASB

138/IAS 38 ensures the accounting of internally generated intangible assets in the most

appropriate and systematic manner. These standards also reduce the scope to do manipulation

in the accounting of internally generated intangible assets by the managements of the

companies (Ratiu and Tudor, 2013). All these create major impact on the assets and all these

impacts are required to be considered as the positive impact on the whole accounting

procedures of intangible assets in the accounting books. This helps the investors and other

users of the financial reports to assess the treatment of internal intangible assets in the

financial reports.

3. Dissimilarities between Internal Intangible Assets and Acquired Intangible Assets

AASB 138/IAS 38 prescribe the required accounting methods that need to be

monitored by the firms in the accounting of intangible assets that include both the intangible

assets. Now, it needs to be mentioned that there are certain dissimilarities between the

accounting treatment for internally generated intangible assets and acquired intangible assets

as mentioned in AASB 138/IAS 38. This difference can be seen in the recognition of these

two types of intangible assets.

3.1 Recognition Criteria

AASB 138/IAS 38 prescribe different recognition procedures for recognizing

internally generated intangible assets and acquired intangible assets. As per AASB 138,

Paragraph 21, a company needs to recognize an intangible asset in case a) there is a

likelihood of inflow of future economic benefit allied with the asset to the company; and b)

the company can dependably measure the cost of the asset. Since intangible assets are

acquired separately and generated internally, difference in the above-mentioned recognition

criteria can be seen. As per Paragraph 25 of AASB 138, the price paid by a company for

separately acquiring an intangible asset will reflect expectation about the probability that

there will be inflow economic benefit to the company (aasb.gov.au, 2019). For this reason,

the recognition criteria under Paragraph 21 (a) of AASB 138 needs to be considered as

appropriate. This same concept is also applicable in case of the intangible assets acquired as a

part of business combination since the asset is acquired at fair value that will reflect the

expectation of the probability to receive future economic benefit associated with the asset.

However, the recognition criteria for internally generated intangible assets are

different from the same of acquired intangible assets in accordance with AASB 138/IAS 38

(Pucci, et al., 2014). According to Paragraph 48 of AASB 138, a company is restricted from

recognizing any internally generated goodwill. This is because a company incur expenditures

for generating future economic benefit, but there is not any creation of intangible asset for

meeting the recognition criteria. As per Paragraph 51 of AASB 138, there is sometimes

difficulty in assessing whether an internal intangible asset is qualified to be recognizes in the

presence of two problems in identifying whether and when an identifiable asset is there for

5FINANCIAL ACCOUNTING

generating expected future benefits and reliably ascertaining the cost of the asset. This

requires to be considered as a major difference between the recognition criteria of acquired

intangible asset and internally generated intangible assets. According to Paragraph 52 of

AASB 138, the generation of intangible assets is categorized in the research phase and

development phase with the intention to examine whether the recognition and measurement

criteria are met by the entity (aasb.gov.au, 2019). According to Paragraph 54 of AASB 138, a

company is not required to recognize any intangible asset raising from research; and the

company needs to recognize the research expenditures as an expense when the company

incurs it. Paragraph 57 of AASB 138 states that a company needs to recognize an intangible

asset raising from development stage when all the earlier-mentioned conditions are

demonstrated (Russell, 2017).

3.2 Measurement Criteria

Moreover, difference can be seen in case of measuring of acquired and internal

intangible assets. Separately acquired intangible assets are measured at cost that comprises

the purchase price; and fair value is used for measuring the intangible assets acquired in

business combination and acquired in free of charge respectively. However, the measurement

of internally generated intangible assets are done at cost with cost determined as the total

incurred expenditure at the acquisition date (cpaaustralia.com.au, 2019). The above whole

discussion demonstrates towards certain key differences in the measurement and recognition

of two types of intangible assets in the books of accounting. These differences are significant

and these are required to be taken into consideration by the companies, investors and other

users of the financial statements.

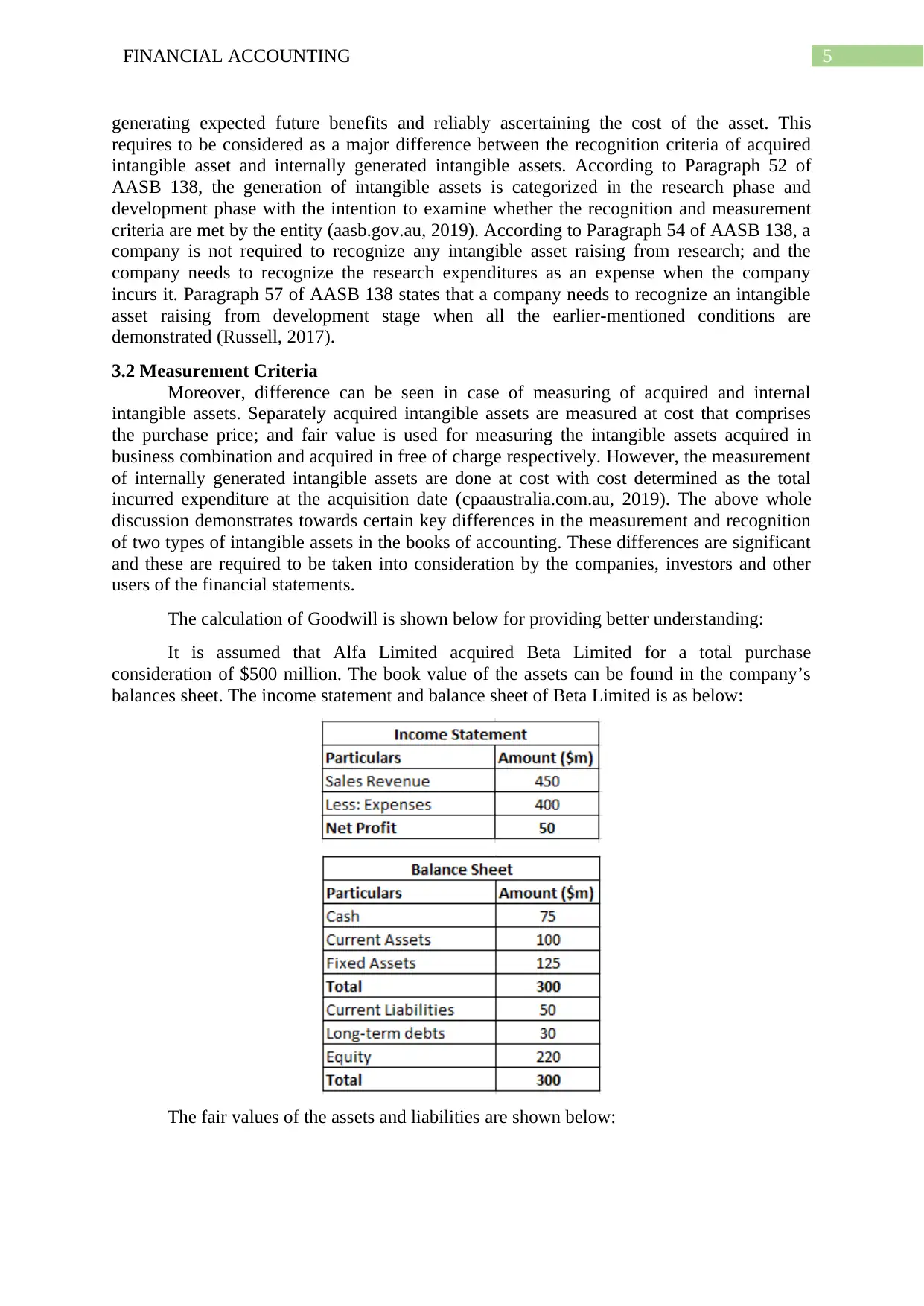

The calculation of Goodwill is shown below for providing better understanding:

It is assumed that Alfa Limited acquired Beta Limited for a total purchase

consideration of $500 million. The book value of the assets can be found in the company’s

balances sheet. The income statement and balance sheet of Beta Limited is as below:

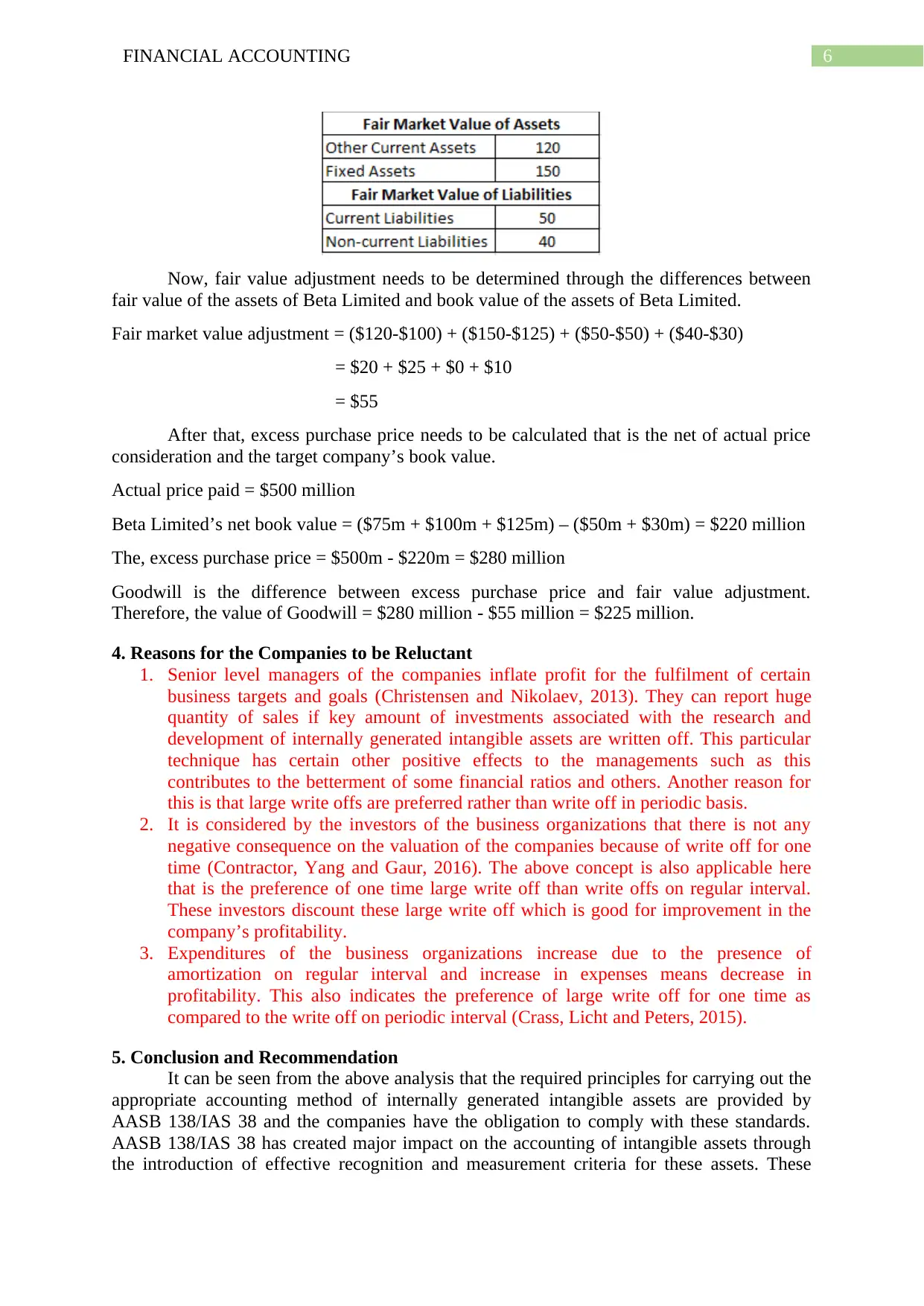

The fair values of the assets and liabilities are shown below:

generating expected future benefits and reliably ascertaining the cost of the asset. This

requires to be considered as a major difference between the recognition criteria of acquired

intangible asset and internally generated intangible assets. According to Paragraph 52 of

AASB 138, the generation of intangible assets is categorized in the research phase and

development phase with the intention to examine whether the recognition and measurement

criteria are met by the entity (aasb.gov.au, 2019). According to Paragraph 54 of AASB 138, a

company is not required to recognize any intangible asset raising from research; and the

company needs to recognize the research expenditures as an expense when the company

incurs it. Paragraph 57 of AASB 138 states that a company needs to recognize an intangible

asset raising from development stage when all the earlier-mentioned conditions are

demonstrated (Russell, 2017).

3.2 Measurement Criteria

Moreover, difference can be seen in case of measuring of acquired and internal

intangible assets. Separately acquired intangible assets are measured at cost that comprises

the purchase price; and fair value is used for measuring the intangible assets acquired in

business combination and acquired in free of charge respectively. However, the measurement

of internally generated intangible assets are done at cost with cost determined as the total

incurred expenditure at the acquisition date (cpaaustralia.com.au, 2019). The above whole

discussion demonstrates towards certain key differences in the measurement and recognition

of two types of intangible assets in the books of accounting. These differences are significant

and these are required to be taken into consideration by the companies, investors and other

users of the financial statements.

The calculation of Goodwill is shown below for providing better understanding:

It is assumed that Alfa Limited acquired Beta Limited for a total purchase

consideration of $500 million. The book value of the assets can be found in the company’s

balances sheet. The income statement and balance sheet of Beta Limited is as below:

The fair values of the assets and liabilities are shown below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Now, fair value adjustment needs to be determined through the differences between

fair value of the assets of Beta Limited and book value of the assets of Beta Limited.

Fair market value adjustment = ($120-$100) + ($150-$125) + ($50-$50) + ($40-$30)

= $20 + $25 + $0 + $10

= $55

After that, excess purchase price needs to be calculated that is the net of actual price

consideration and the target company’s book value.

Actual price paid = $500 million

Beta Limited’s net book value = ($75m + $100m + $125m) – ($50m + $30m) = $220 million

The, excess purchase price = $500m - $220m = $280 million

Goodwill is the difference between excess purchase price and fair value adjustment.

Therefore, the value of Goodwill = $280 million - $55 million = $225 million.

4. Reasons for the Companies to be Reluctant

1. Senior level managers of the companies inflate profit for the fulfilment of certain

business targets and goals (Christensen and Nikolaev, 2013). They can report huge

quantity of sales if key amount of investments associated with the research and

development of internally generated intangible assets are written off. This particular

technique has certain other positive effects to the managements such as this

contributes to the betterment of some financial ratios and others. Another reason for

this is that large write offs are preferred rather than write off in periodic basis.

2. It is considered by the investors of the business organizations that there is not any

negative consequence on the valuation of the companies because of write off for one

time (Contractor, Yang and Gaur, 2016). The above concept is also applicable here

that is the preference of one time large write off than write offs on regular interval.

These investors discount these large write off which is good for improvement in the

company’s profitability.

3. Expenditures of the business organizations increase due to the presence of

amortization on regular interval and increase in expenses means decrease in

profitability. This also indicates the preference of large write off for one time as

compared to the write off on periodic interval (Crass, Licht and Peters, 2015).

5. Conclusion and Recommendation

It can be seen from the above analysis that the required principles for carrying out the

appropriate accounting method of internally generated intangible assets are provided by

AASB 138/IAS 38 and the companies have the obligation to comply with these standards.

AASB 138/IAS 38 has created major impact on the accounting of intangible assets through

the introduction of effective recognition and measurement criteria for these assets. These

Now, fair value adjustment needs to be determined through the differences between

fair value of the assets of Beta Limited and book value of the assets of Beta Limited.

Fair market value adjustment = ($120-$100) + ($150-$125) + ($50-$50) + ($40-$30)

= $20 + $25 + $0 + $10

= $55

After that, excess purchase price needs to be calculated that is the net of actual price

consideration and the target company’s book value.

Actual price paid = $500 million

Beta Limited’s net book value = ($75m + $100m + $125m) – ($50m + $30m) = $220 million

The, excess purchase price = $500m - $220m = $280 million

Goodwill is the difference between excess purchase price and fair value adjustment.

Therefore, the value of Goodwill = $280 million - $55 million = $225 million.

4. Reasons for the Companies to be Reluctant

1. Senior level managers of the companies inflate profit for the fulfilment of certain

business targets and goals (Christensen and Nikolaev, 2013). They can report huge

quantity of sales if key amount of investments associated with the research and

development of internally generated intangible assets are written off. This particular

technique has certain other positive effects to the managements such as this

contributes to the betterment of some financial ratios and others. Another reason for

this is that large write offs are preferred rather than write off in periodic basis.

2. It is considered by the investors of the business organizations that there is not any

negative consequence on the valuation of the companies because of write off for one

time (Contractor, Yang and Gaur, 2016). The above concept is also applicable here

that is the preference of one time large write off than write offs on regular interval.

These investors discount these large write off which is good for improvement in the

company’s profitability.

3. Expenditures of the business organizations increase due to the presence of

amortization on regular interval and increase in expenses means decrease in

profitability. This also indicates the preference of large write off for one time as

compared to the write off on periodic interval (Crass, Licht and Peters, 2015).

5. Conclusion and Recommendation

It can be seen from the above analysis that the required principles for carrying out the

appropriate accounting method of internally generated intangible assets are provided by

AASB 138/IAS 38 and the companies have the obligation to comply with these standards.

AASB 138/IAS 38 has created major impact on the accounting of intangible assets through

the introduction of effective recognition and measurement criteria for these assets. These

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

contribute to the effective accounting treatment of internally generated intangible assets by

the companies. The analysis also shows that there are certain differences between the

recognition and measurement criteria of acquired intangible assets and internally generated

intangible assets as prescribed in AASB 138/IAS 38. For example, the companies are

required to recognize the intangible assets that have been acquired, but the internally

generated goodwill and other assets in research phase should not be recognized as per AASB

138/IAS 38. It can also be observed from the above discussion that certain reasons for the

companies not to press are the tendency to inflate future profit by the management,

preference of one time large write off by the investors rather than amortization and others.

Based on the above whole discussion, it is recommended to the companies that they

need to comply with the principles and provisions of AASB 138 for correctly carrying out the

accounting treatments of acquired intangible assets and internally generated intangible assets.

Following the rules of AASB 138 will lead to the reduction of differences in the accounting

numbers in intangible assets accounting.

contribute to the effective accounting treatment of internally generated intangible assets by

the companies. The analysis also shows that there are certain differences between the

recognition and measurement criteria of acquired intangible assets and internally generated

intangible assets as prescribed in AASB 138/IAS 38. For example, the companies are

required to recognize the intangible assets that have been acquired, but the internally

generated goodwill and other assets in research phase should not be recognized as per AASB

138/IAS 38. It can also be observed from the above discussion that certain reasons for the

companies not to press are the tendency to inflate future profit by the management,

preference of one time large write off by the investors rather than amortization and others.

Based on the above whole discussion, it is recommended to the companies that they

need to comply with the principles and provisions of AASB 138 for correctly carrying out the

accounting treatments of acquired intangible assets and internally generated intangible assets.

Following the rules of AASB 138 will lead to the reduction of differences in the accounting

numbers in intangible assets accounting.

8FINANCIAL ACCOUNTING

6. References

Aasb.gov.au. 2019. AASB 138 Intangible Assets. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPjul17_01-20.pdf

[Accessed 30 Dec. 2019].

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-financial

assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-775.

Contractor, F., Yang, Y. and Gaur, A.S., 2016. Firm-specific intangible assets and subsidiary

profitability: The moderating role of distance, ownership strategy and subsidiary

experience. Journal of World Business, 51(6), pp.950-964.

Cosmulese, C.G.L., Grosu, V. and HLACIUC, E., 2017. Intangible assets with a high degree

of difficulty in estimating their value. Ecoforum Journal, 6(3).

Cpaaustralia.com.au. 2019. IAS 38 INTANGIBLE ASSETS. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-

resources/reporting/reporting-ifrsfactsheet-intangible-assets.pdf?

la=en&rev=2713a8f0b1ad43b69e52db9b5f3b0819 [Accessed 30 Dec. 2019].

Crass, D., Licht, G. and Peters, B., 2015. Intangible assets and investments at the sector level:

Empirical evidence for Germany. In Intangibles, Market Failure and Innovation

Performance (pp. 57-111). Springer, Cham.

Jaafar, H. and Halim, H.A., 2013. Firm life cycle and the value relevance of intangible assets:

the impact of FRS 138 adoption. International Journal of Trade, Economics and

Finance, 4(5), p.252.

Ji, X.D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting, 22(3), pp.182-

216.

Pucci, S., Cenci, M., Tutino, M. and Luly, R., 2014. Intangible assets: Current requirements,

social statements, integrated reporting, and new models. In Value Creation, Reporting, and

Signaling for Human Capital and Human Assets (pp. 179-211). Palgrave Macmillan, New

York.

Radu, R.I. and Isai, V., 2014. Accountancy Modeling on Intangible Fixed Assets in Terms of

the Main Provisions of International Accounting Standards.

Ratiu, R.V. and Tudor, A.T., 2013. The Classification of Goodwill-An essential accounting

analysis. Review of Economic Studies and Research Virgil Madgearu, 6(2), p.137.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Vetoshkina, E.Y. and Tukhvatullin, R.S., 2014. The problem of accounting for the costs

incurred after the initial recognition of an intangible asset. Mediterranean Journal of Social

Sciences, 5(24), p.52.

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

6. References

Aasb.gov.au. 2019. AASB 138 Intangible Assets. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPjul17_01-20.pdf

[Accessed 30 Dec. 2019].

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-financial

assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-775.

Contractor, F., Yang, Y. and Gaur, A.S., 2016. Firm-specific intangible assets and subsidiary

profitability: The moderating role of distance, ownership strategy and subsidiary

experience. Journal of World Business, 51(6), pp.950-964.

Cosmulese, C.G.L., Grosu, V. and HLACIUC, E., 2017. Intangible assets with a high degree

of difficulty in estimating their value. Ecoforum Journal, 6(3).

Cpaaustralia.com.au. 2019. IAS 38 INTANGIBLE ASSETS. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-

resources/reporting/reporting-ifrsfactsheet-intangible-assets.pdf?

la=en&rev=2713a8f0b1ad43b69e52db9b5f3b0819 [Accessed 30 Dec. 2019].

Crass, D., Licht, G. and Peters, B., 2015. Intangible assets and investments at the sector level:

Empirical evidence for Germany. In Intangibles, Market Failure and Innovation

Performance (pp. 57-111). Springer, Cham.

Jaafar, H. and Halim, H.A., 2013. Firm life cycle and the value relevance of intangible assets:

the impact of FRS 138 adoption. International Journal of Trade, Economics and

Finance, 4(5), p.252.

Ji, X.D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting, 22(3), pp.182-

216.

Pucci, S., Cenci, M., Tutino, M. and Luly, R., 2014. Intangible assets: Current requirements,

social statements, integrated reporting, and new models. In Value Creation, Reporting, and

Signaling for Human Capital and Human Assets (pp. 179-211). Palgrave Macmillan, New

York.

Radu, R.I. and Isai, V., 2014. Accountancy Modeling on Intangible Fixed Assets in Terms of

the Main Provisions of International Accounting Standards.

Ratiu, R.V. and Tudor, A.T., 2013. The Classification of Goodwill-An essential accounting

analysis. Review of Economic Studies and Research Virgil Madgearu, 6(2), p.137.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Vetoshkina, E.Y. and Tukhvatullin, R.S., 2014. The problem of accounting for the costs

incurred after the initial recognition of an intangible asset. Mediterranean Journal of Social

Sciences, 5(24), p.52.

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.