Accounting Homework: NZ-IAS 38 Intangible Assets Analysis

VerifiedAdded on 2021/04/24

|6

|1002

|30

Homework Assignment

AI Summary

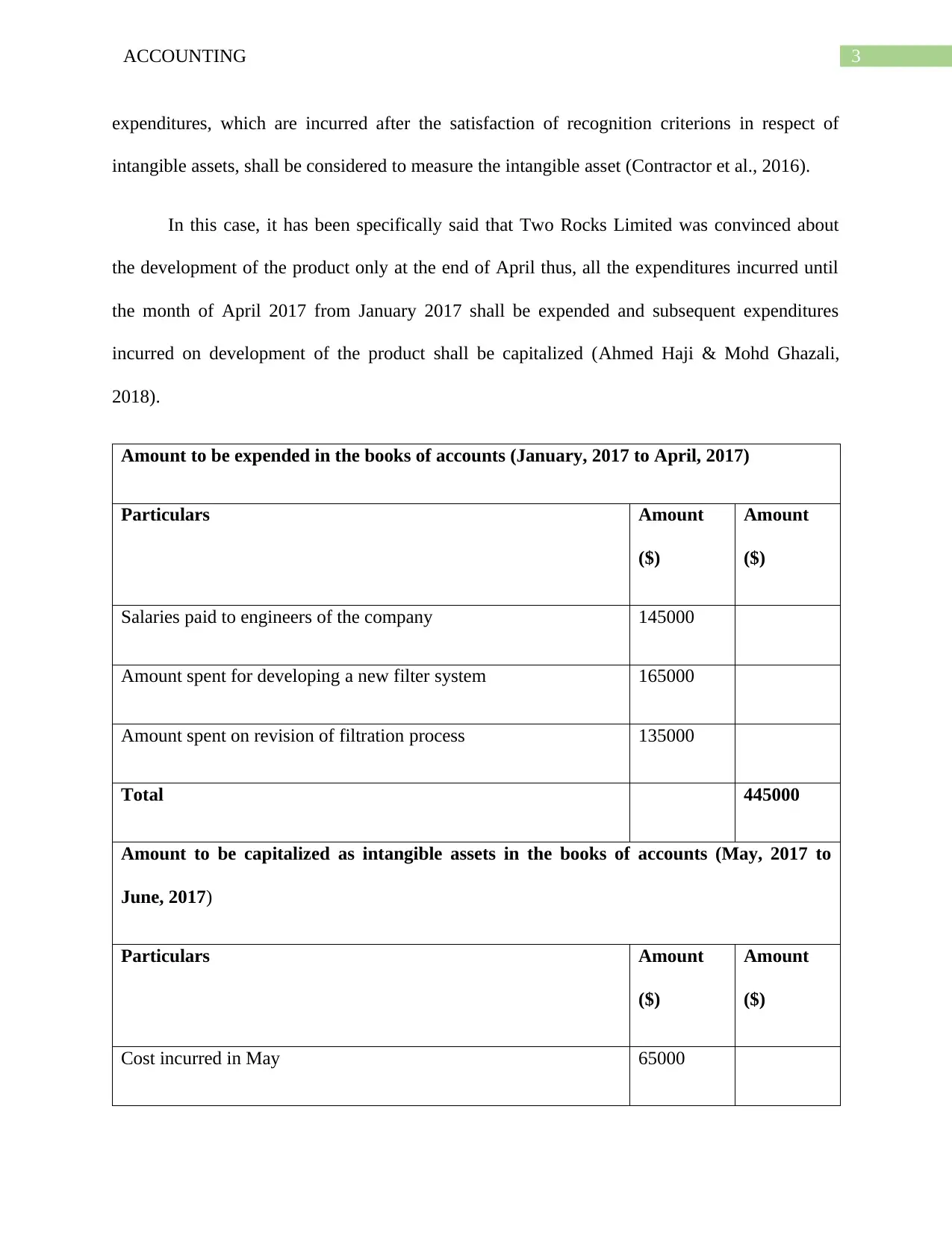

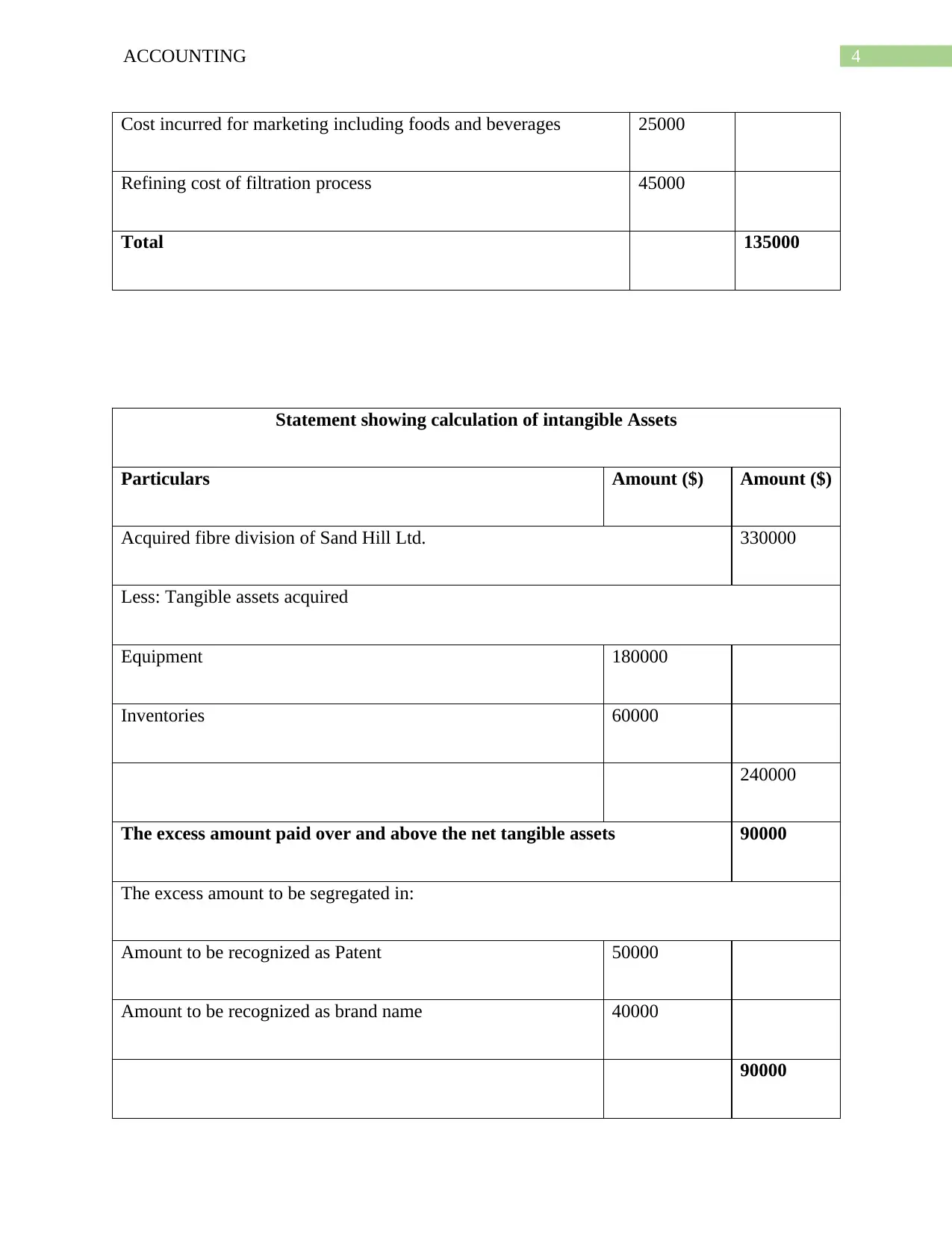

This accounting assignment focuses on the principles of NZ-IAS 38, specifically addressing the recognition and measurement of intangible assets. The assignment solution begins by defining intangible assets and outlining the criteria for their initial measurement, including the requirement of probable future economic benefits and reliable cost measurement. It differentiates between the measurement of assets acquired separately, in a business combination, and those generated internally. The solution then applies these principles to a case study involving Two Rocks Limited, determining which expenditures should be expensed versus capitalized, and providing calculations to determine the value of intangible assets. The assignment also includes a calculation of the intangible assets acquired in a business combination, separating the value of the tangible assets from the intangible assets like patents and brand names. References to relevant academic literature are provided.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.