Financial Reporting: Analysis of M&S and Kitchen Financials

VerifiedAdded on 2020/07/23

|8

|1629

|49

Report

AI Summary

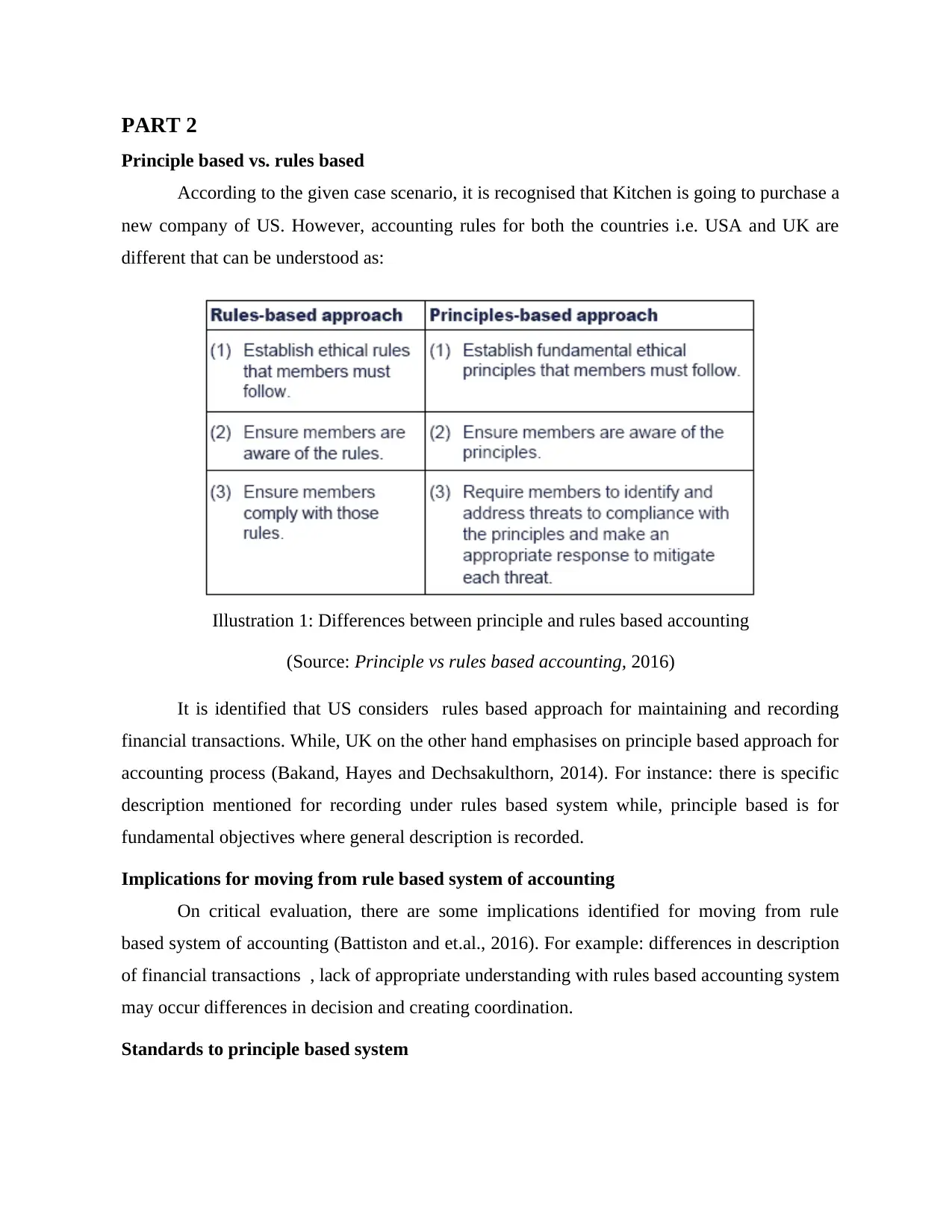

This report delves into the realm of financial reporting, examining its crucial role in conveying a company's financial performance and informing business decisions. It explores the significance of the integrated reporting framework, particularly concerning M&S, and the pivotal role stakeholders play in the decision-making process. Furthermore, the report provides a comparative analysis of principle-based and rule-based accounting standards, using Kitchen as a case study. It discusses the implications of moving from a rule-based to a principle-based system, including the importance of ethical considerations and the convergence of accounting principles. The analysis covers cash flow, predictive value, and the benefits of integrated reporting, offering critical evaluations of immaterial disclosures and the integrated reporting system itself. Decision-making tools for strategic planning, particularly in the context of purchasing a US company, are also introduced.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.