Comprehensive Analysis of Integrated Reporting in Business Development

VerifiedAdded on 2020/04/13

|13

|4125

|29

Essay

AI Summary

This essay provides a comprehensive analysis of integrated reporting in the context of modern business practices. It explores the concept of integrated reporting as a crucial communication process for organizations, focusing on its benefits and challenges. The essay examines the value of integrated reporting, its role in financial and non-financial communication, and its impact on stakeholder value. It delves into the integration of various reporting standards, the role of the International Integrated Reporting Council (IIRC), and the six capitals framework. Furthermore, the essay discusses the relationship between integrated reporting and financial analysis, sustainability management, and quality management. The analysis highlights the importance of integrated reporting in enhancing organizational development and improving the overall reporting system of business organizations, emphasizing both qualitative and quantitative information disclosure.

Running head: PARTICIPATION IN STANDARD SETTING

Participation in Standard Setting

Name of the Student

Name of the University

Author’s Note

Participation in Standard Setting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PARTICIPATION IN STANDARD SETTING

Introduction

In today’s business world all over the world, Integrated Reporting is considered as one of

the major aspect for the companies. Integrated Reporting refers to an effective communication

process of the organization’s strategy related to governance, performance and the process of

value creation (integratedreporting.org 2017). In the recent years, it has been seen that the

business and various investors have recognized a broader approach for organizational value

creation. For this reason, business organizations are being forced for the critical re-evaluation of

the communication strategies of financial information to the stakeholders. Due to this, Integrated

Reporting is considered as the combination of measurement of the company’s financial and non-

financial performance (Flower 2015). For this reason, most of the companies all over the world

are adopting integrated reporting for communicating financial and non-financial performance

related information (de Villiers, Rinaldi and Unerman 2014). While there has been an increased

demand in the communication of financial and non-financial information from the companies, it

is not clear for the stakeholders how they can add value by using this information. In the recent

years, it can be seen that incentives are provided to the short-term behavior of the business

organizations; and in this process, the capital market are becoming weaker. The people of society

are becoming poorer and the environment is suffering a lot from different business activities of

the companies. In this process, integrated reporting plays an integral part. The framework of

integrated reporting helps the companies in long-term value creation with various purposes. In

the current business world of various financial crises, it is required for the business organizations

to link financial stability and sustainable development with investment decisions, corporate

behavior and reporting. In other words, today’s businesses need a massive evolution in the

system of performance reporting, facilitating and organizational communication in order to

reduce the communication gap between the companies and their shareholders. In the process of

reducing this gap, various approaches of integrated reporting play a crucial part. Thus, the main

aim of this essay is to analyze and evaluate various aspect of integrated reporting so that they can

be beneficial for overall organizational development.

The University of Greenwich

Introduction

In today’s business world all over the world, Integrated Reporting is considered as one of

the major aspect for the companies. Integrated Reporting refers to an effective communication

process of the organization’s strategy related to governance, performance and the process of

value creation (integratedreporting.org 2017). In the recent years, it has been seen that the

business and various investors have recognized a broader approach for organizational value

creation. For this reason, business organizations are being forced for the critical re-evaluation of

the communication strategies of financial information to the stakeholders. Due to this, Integrated

Reporting is considered as the combination of measurement of the company’s financial and non-

financial performance (Flower 2015). For this reason, most of the companies all over the world

are adopting integrated reporting for communicating financial and non-financial performance

related information (de Villiers, Rinaldi and Unerman 2014). While there has been an increased

demand in the communication of financial and non-financial information from the companies, it

is not clear for the stakeholders how they can add value by using this information. In the recent

years, it can be seen that incentives are provided to the short-term behavior of the business

organizations; and in this process, the capital market are becoming weaker. The people of society

are becoming poorer and the environment is suffering a lot from different business activities of

the companies. In this process, integrated reporting plays an integral part. The framework of

integrated reporting helps the companies in long-term value creation with various purposes. In

the current business world of various financial crises, it is required for the business organizations

to link financial stability and sustainable development with investment decisions, corporate

behavior and reporting. In other words, today’s businesses need a massive evolution in the

system of performance reporting, facilitating and organizational communication in order to

reduce the communication gap between the companies and their shareholders. In the process of

reducing this gap, various approaches of integrated reporting play a crucial part. Thus, the main

aim of this essay is to analyze and evaluate various aspect of integrated reporting so that they can

be beneficial for overall organizational development.

The University of Greenwich

2PARTICIPATION IN STANDARD SETTING

Benefits and Challenges of Integrated Reporting

Integrated Reporting and Financial Communication

In the recent years, it has been seen that the corporate reporting practice of the companies

are going through some of the major changes as the stakeholders of the companies are

considering that they are not getting enough information regarding the financial and non-

financial performance. For this reason, the companies are forced to re-evaluate their process of

the communication of financial and non-financial information in order to bring transparency.

Most of the analysts all over the world is considering that integrated reporting will have major

positive impact on the value creation of the organizations (repository.up.ac.za 2017). At the

initial stage of inception, the major aim of integrated reporting was to communicate the

company’s financial and non-financial performance information to various stakeholders of the

company. However, in the current years, another major objective of integrated reporting is

related with the investors of the businesses. For this reason, integrated reports of today’s world

are developed for a board range of stakeholders and investors of the companies. In the article

named “Is Integrated Reporting the silver bullet of financial communication? A stakeholder

perspective from South Africa”, it can be seen that in today’s business world, it is the duty of the

companies to release information related to financial and non-financial performance to the

stakeholders and investors (repository.up.ac.za 2017). According to the findings of this particular

article, it can be seen that the business organizations are facing major problems in the

communication of valuable non-financial and financial investment information to the

stakeholders and investors with incurring large amount of costs. The article states that it is the

responsibility of the financial officers of the companies to communicate performance related

information to the broad stakeholders in more effective manner (repository.up.ac.za 2017). For

this reason, integrated reporting is considered as one of the major tools for the communication of

financial and non-financial information to the stakeholders. Hence, integrated reporting can be

considered as the silver bullet of financial communication as it has become crucial for the

companies all over the globe.

Value of Integrated Reporting

In the recent years, it has been seen that most of the renowned corporations all over the

world have adopted integrated reporting as a part of their financial and non-financial reporting.

The University of Greenwich

Benefits and Challenges of Integrated Reporting

Integrated Reporting and Financial Communication

In the recent years, it has been seen that the corporate reporting practice of the companies

are going through some of the major changes as the stakeholders of the companies are

considering that they are not getting enough information regarding the financial and non-

financial performance. For this reason, the companies are forced to re-evaluate their process of

the communication of financial and non-financial information in order to bring transparency.

Most of the analysts all over the world is considering that integrated reporting will have major

positive impact on the value creation of the organizations (repository.up.ac.za 2017). At the

initial stage of inception, the major aim of integrated reporting was to communicate the

company’s financial and non-financial performance information to various stakeholders of the

company. However, in the current years, another major objective of integrated reporting is

related with the investors of the businesses. For this reason, integrated reports of today’s world

are developed for a board range of stakeholders and investors of the companies. In the article

named “Is Integrated Reporting the silver bullet of financial communication? A stakeholder

perspective from South Africa”, it can be seen that in today’s business world, it is the duty of the

companies to release information related to financial and non-financial performance to the

stakeholders and investors (repository.up.ac.za 2017). According to the findings of this particular

article, it can be seen that the business organizations are facing major problems in the

communication of valuable non-financial and financial investment information to the

stakeholders and investors with incurring large amount of costs. The article states that it is the

responsibility of the financial officers of the companies to communicate performance related

information to the broad stakeholders in more effective manner (repository.up.ac.za 2017). For

this reason, integrated reporting is considered as one of the major tools for the communication of

financial and non-financial information to the stakeholders. Hence, integrated reporting can be

considered as the silver bullet of financial communication as it has become crucial for the

companies all over the globe.

Value of Integrated Reporting

In the recent years, it has been seen that most of the renowned corporations all over the

world have adopted integrated reporting as a part of their financial and non-financial reporting.

The University of Greenwich

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PARTICIPATION IN STANDARD SETTING

According to the article named “How valuable is Integrated Reporting?”, some specific factors

are required to be considered while implementing integrated reporting in the companies

(static1.squarespace.com 2017). As per this article, the primary executives of the companies like

CEO and others are the main initiator of the implementation of integrated reporting

(static1.squarespace.com 2017). In addition, the management of the companies is required to

have sufficient awareness for the use and implementation of integrated reporting. According to

this article, companies have to face some major pros and cons for the implementation of

integrated reporting. According to the pros, the implementation of integrated reporting provides

the organizations better understanding regarding creation of value and a more holistic view of the

whole organizations. Integrated reporting helps to improve organizational risk management

strategies and procedures. However, increased cost in the implementation of integrated reporting

is a major limitation as it helps in the occurrence of additional risk factor of businesses. As a

result of these challenges, the organizational managers are required to consider certain factors.

Before implementation of integrated reporting, it is required to secure the support of all related

parties. After that, the implementation process is required to be done by complying with all the

principles and regulations of the implementation framework (static1.squarespace.com 2017).

After that, it is required for the companies to arrange proper training and development

workshops so that all the organizational people can acquire the information related to Integrated

Reporting. Thus, the above discussion shows that integrated reporting helps the business

organizations in various ways for creating organizational values. However, the implementation

of integrated reporting needs to be done by considering the major challenges of it.

Overall Summary of Integrated Reporting

It is required to be mentioned that the main reason behind the implementation of

integrated reporting is to enhance and consolidate the existing reporting practices. There are

many reasons for which it is required for the companies to implement the strategies of integrated

reporting (integratedreporting.org 2017). Integrated reporting helps the business organizations in

bringing together the important material information regarding the company’s strategy,

governance, performance and processes. On an overall basis, it can be said that integrated

reporting assists the organizations in the demonstration of stewardship in organizational value

creation. In the development of integrated reporting, International Integrated Reporting Council

(IIRC) plays an integral part. IIRC refers to the global alliance of various regulators, investors,

The University of Greenwich

According to the article named “How valuable is Integrated Reporting?”, some specific factors

are required to be considered while implementing integrated reporting in the companies

(static1.squarespace.com 2017). As per this article, the primary executives of the companies like

CEO and others are the main initiator of the implementation of integrated reporting

(static1.squarespace.com 2017). In addition, the management of the companies is required to

have sufficient awareness for the use and implementation of integrated reporting. According to

this article, companies have to face some major pros and cons for the implementation of

integrated reporting. According to the pros, the implementation of integrated reporting provides

the organizations better understanding regarding creation of value and a more holistic view of the

whole organizations. Integrated reporting helps to improve organizational risk management

strategies and procedures. However, increased cost in the implementation of integrated reporting

is a major limitation as it helps in the occurrence of additional risk factor of businesses. As a

result of these challenges, the organizational managers are required to consider certain factors.

Before implementation of integrated reporting, it is required to secure the support of all related

parties. After that, the implementation process is required to be done by complying with all the

principles and regulations of the implementation framework (static1.squarespace.com 2017).

After that, it is required for the companies to arrange proper training and development

workshops so that all the organizational people can acquire the information related to Integrated

Reporting. Thus, the above discussion shows that integrated reporting helps the business

organizations in various ways for creating organizational values. However, the implementation

of integrated reporting needs to be done by considering the major challenges of it.

Overall Summary of Integrated Reporting

It is required to be mentioned that the main reason behind the implementation of

integrated reporting is to enhance and consolidate the existing reporting practices. There are

many reasons for which it is required for the companies to implement the strategies of integrated

reporting (integratedreporting.org 2017). Integrated reporting helps the business organizations in

bringing together the important material information regarding the company’s strategy,

governance, performance and processes. On an overall basis, it can be said that integrated

reporting assists the organizations in the demonstration of stewardship in organizational value

creation. In the development of integrated reporting, International Integrated Reporting Council

(IIRC) plays an integral part. IIRC refers to the global alliance of various regulators, investors,

The University of Greenwich

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PARTICIPATION IN STANDARD SETTING

standard setters, companies and others in order to make promotion of value creation with the

help of effective corporate reporting. The mission of IIRC is to establish integrated reporting

within the mainstream business organizations. The vision of IIRC is to make alignment between

capital allocation and corporate behavior in order to get financial stability along with

sustainability management (integratedreporting.org 2017). According to the principles of IIRC,

the main objective of integrated reporting is to provide guidance to the organizations in the

communication of required information to their stakeholders and investors for creating long-term

value. It can be seen that there are five major principles of integrated reporting; they are Strategic

Focus, Connectivity of Information, Future Orientation, Responsiveness and stakeholders

inclusiveness; and Conciseness, reliability and materiality (integratedreporting.org 2017).

Integrated reporting makes the combination of different standards of reporting like financial,

management, governance, remuneration and others and develop a single coherent report that

helps in the creation of organization’s long term value. Thus, it can be observed that the major

output of integrated reporting is an Integrated Report that is considered as the primary report of

the organizations. One of the major advantages of integrated reporting is that it helps the

companies in the reduction of reporting burden while improving understanding about the

information need of various stakeholders (integratedreporting.org 2017). Thus, based on the

above discussion, it can be observed that integrated reporting helps in the overall development of

reporting system of the business organizations.

The primary focus of integrated reports is to explain the financial capital providers about

the process of value creation in the organizations. This can be done with the help of both

qualitative and quantitative information. In this situation, six capitals have their importance. The

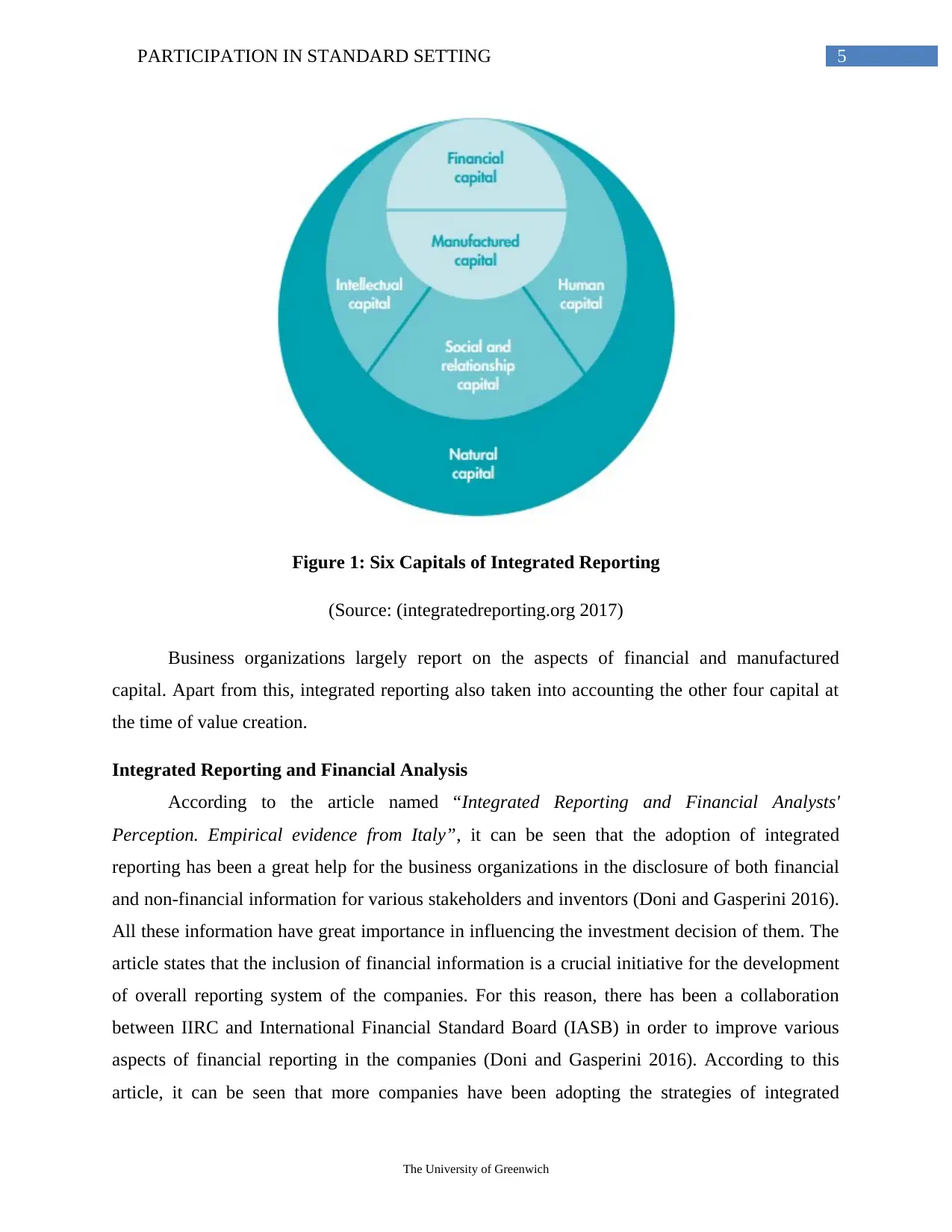

six capitals are Financial, Manufactured, Intellectual, Human, Social and Relationship, and

Natural capital.

The University of Greenwich

standard setters, companies and others in order to make promotion of value creation with the

help of effective corporate reporting. The mission of IIRC is to establish integrated reporting

within the mainstream business organizations. The vision of IIRC is to make alignment between

capital allocation and corporate behavior in order to get financial stability along with

sustainability management (integratedreporting.org 2017). According to the principles of IIRC,

the main objective of integrated reporting is to provide guidance to the organizations in the

communication of required information to their stakeholders and investors for creating long-term

value. It can be seen that there are five major principles of integrated reporting; they are Strategic

Focus, Connectivity of Information, Future Orientation, Responsiveness and stakeholders

inclusiveness; and Conciseness, reliability and materiality (integratedreporting.org 2017).

Integrated reporting makes the combination of different standards of reporting like financial,

management, governance, remuneration and others and develop a single coherent report that

helps in the creation of organization’s long term value. Thus, it can be observed that the major

output of integrated reporting is an Integrated Report that is considered as the primary report of

the organizations. One of the major advantages of integrated reporting is that it helps the

companies in the reduction of reporting burden while improving understanding about the

information need of various stakeholders (integratedreporting.org 2017). Thus, based on the

above discussion, it can be observed that integrated reporting helps in the overall development of

reporting system of the business organizations.

The primary focus of integrated reports is to explain the financial capital providers about

the process of value creation in the organizations. This can be done with the help of both

qualitative and quantitative information. In this situation, six capitals have their importance. The

six capitals are Financial, Manufactured, Intellectual, Human, Social and Relationship, and

Natural capital.

The University of Greenwich

5PARTICIPATION IN STANDARD SETTING

Figure 1: Six Capitals of Integrated Reporting

(Source: (integratedreporting.org 2017)

Business organizations largely report on the aspects of financial and manufactured

capital. Apart from this, integrated reporting also taken into accounting the other four capital at

the time of value creation.

Integrated Reporting and Financial Analysis

According to the article named “Integrated Reporting and Financial Analysts'

Perception. Empirical evidence from Italy”, it can be seen that the adoption of integrated

reporting has been a great help for the business organizations in the disclosure of both financial

and non-financial information for various stakeholders and inventors (Doni and Gasperini 2016).

All these information have great importance in influencing the investment decision of them. The

article states that the inclusion of financial information is a crucial initiative for the development

of overall reporting system of the companies. For this reason, there has been a collaboration

between IIRC and International Financial Standard Board (IASB) in order to improve various

aspects of financial reporting in the companies (Doni and Gasperini 2016). According to this

article, it can be seen that more companies have been adopting the strategies of integrated

The University of Greenwich

Figure 1: Six Capitals of Integrated Reporting

(Source: (integratedreporting.org 2017)

Business organizations largely report on the aspects of financial and manufactured

capital. Apart from this, integrated reporting also taken into accounting the other four capital at

the time of value creation.

Integrated Reporting and Financial Analysis

According to the article named “Integrated Reporting and Financial Analysts'

Perception. Empirical evidence from Italy”, it can be seen that the adoption of integrated

reporting has been a great help for the business organizations in the disclosure of both financial

and non-financial information for various stakeholders and inventors (Doni and Gasperini 2016).

All these information have great importance in influencing the investment decision of them. The

article states that the inclusion of financial information is a crucial initiative for the development

of overall reporting system of the companies. For this reason, there has been a collaboration

between IIRC and International Financial Standard Board (IASB) in order to improve various

aspects of financial reporting in the companies (Doni and Gasperini 2016). According to this

article, it can be seen that more companies have been adopting the strategies of integrated

The University of Greenwich

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PARTICIPATION IN STANDARD SETTING

reporting due to its large advantages. This large adoption of integrated reporting by listed

companies all over the world is providing IIRC the chance to develop various aspects of

integrated reporting. The improvement of integrated reporting can improve the disclosure of non-

financial information contributing towards bringing reliability, accessibility and comparability of

them. This is a crucial aspect for the overall improvements of integrated reporting (Doni and

Gasperini 2016).

Integrated Reporting and Sustainability Management

According to the article named “Sustainability management and reporting: the role of

integrated reporting for communicating corporate sustainability management”, IIRC states that

integrated reports of the companies must include about the indicators of sustainability

management (Stacchezzini, Melloni and Lai 2016). This aspect has major impact on the process

of sustainability decisions-making process of the companies. However, this report also states that

there are many arguments saying that integrated reporting do not have any contribution towards

the aspect of sustainability management in the companies (Stacchezzini, Melloni and Lai 2016).

From the result of the research, it can be seen that the management of the companies are vastly

responsible for this misconception about integrated reporting. It has been seen that the

management of the companies use to make various manipulations in the disclosures of integrated

reporting. According to the manual content analysis report of IIRC, most of the companies

disclose biased integrated reports. As a result of this, business organizations provide limited

qualitative disclosure of their different sustainability management activities; in addition, the do

not publish their integrated reports when they fail to perform well in the field of sustainability

(Stacchezzini, Melloni and Lai 2016). For all these reason, most of the people all over the world

consider that integrated reporting do not have any contribution towards the sustainability

management of the companies.

Integrated Reporting and Quality Management

From the article named “Integrated Reporting, Quality of Management, and Financial

Performance”, it can be see that integrated reporting has major part to play in the quality

management of the companies (sustainablefinancialmarkets.net 2017). According to the research,

integrated reporting helps in solving different kinds of organizations issues in order to increase

the overall performance of the companies. The report states that the number of companies using

The University of Greenwich

reporting due to its large advantages. This large adoption of integrated reporting by listed

companies all over the world is providing IIRC the chance to develop various aspects of

integrated reporting. The improvement of integrated reporting can improve the disclosure of non-

financial information contributing towards bringing reliability, accessibility and comparability of

them. This is a crucial aspect for the overall improvements of integrated reporting (Doni and

Gasperini 2016).

Integrated Reporting and Sustainability Management

According to the article named “Sustainability management and reporting: the role of

integrated reporting for communicating corporate sustainability management”, IIRC states that

integrated reports of the companies must include about the indicators of sustainability

management (Stacchezzini, Melloni and Lai 2016). This aspect has major impact on the process

of sustainability decisions-making process of the companies. However, this report also states that

there are many arguments saying that integrated reporting do not have any contribution towards

the aspect of sustainability management in the companies (Stacchezzini, Melloni and Lai 2016).

From the result of the research, it can be seen that the management of the companies are vastly

responsible for this misconception about integrated reporting. It has been seen that the

management of the companies use to make various manipulations in the disclosures of integrated

reporting. According to the manual content analysis report of IIRC, most of the companies

disclose biased integrated reports. As a result of this, business organizations provide limited

qualitative disclosure of their different sustainability management activities; in addition, the do

not publish their integrated reports when they fail to perform well in the field of sustainability

(Stacchezzini, Melloni and Lai 2016). For all these reason, most of the people all over the world

consider that integrated reporting do not have any contribution towards the sustainability

management of the companies.

Integrated Reporting and Quality Management

From the article named “Integrated Reporting, Quality of Management, and Financial

Performance”, it can be see that integrated reporting has major part to play in the quality

management of the companies (sustainablefinancialmarkets.net 2017). According to the research,

integrated reporting helps in solving different kinds of organizations issues in order to increase

the overall performance of the companies. The report states that the number of companies using

The University of Greenwich

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PARTICIPATION IN STANDARD SETTING

the strategies of integrated reporting for managing quality is increasing in a fast pace. In

addition, effective quality management process of the companies helps in increasing the long-

term value of the firms (sustainablefinancialmarkets.net 2017). The report also states that

investors in today’s world do not limit their decision base only financial performance of the

organizations, they have started considering some additional facts about the firms like quality

management, non-financial performance, sustainability management and others. For this reason,

it is important for the business organizations to adopt the principles of integrated reporting for

managing the overall quality of their organizations. Now a days, most of the companies all over

the world are considering integrated reporting as one of the major ways to provide a reliable base

for the identification of high quality business. On the other hand, it needs to be mentioned that

the implementation of integrated reporting also helpful for the companies to bring improvements

in the aspect of quality management of the organizations. Most importantly, effective quality

management in the organizations leads to the improvements in overall financial performance of

the companies (sustainablefinancialmarkets.net 2017). Thus, it can be said that integrated

reporting in an important aspect for quality management.

Integrated Reporting and Users’ Information Needs

According to the article named “Meeting users’ information needs: The use and

usefulness of Integrated Reporting”, the implementation of integrated reporting in the business

organizations have been able to fulfill the information need of the users of the companies

(accaglobal.com 2017). At the time of taking investment decisions, the investors required

different kinds if information related to capital market, equity market and many others.

Integrated reports are considered as a major source of information for the stakeholders and

inventors (accaglobal.com 2017). However, in order to get different types of crucial information,

the stakeholders and investors are required to be familiar with various aspects of integrated

reporting (accaglobal.com 2017). This article shows that the knowledge of investors and

stakeholders of the companies regarding various aspects of integrated reporting is low and thus,

most of the times they are not able to extract the required financial as well as non-financial

information for investment decision-making (accaglobal.com 2017). For this reason, it is

required for the investors and stakeholders of the companies to acquire effective knowledge

about various aspects of integrated reports of the companies.

The University of Greenwich

the strategies of integrated reporting for managing quality is increasing in a fast pace. In

addition, effective quality management process of the companies helps in increasing the long-

term value of the firms (sustainablefinancialmarkets.net 2017). The report also states that

investors in today’s world do not limit their decision base only financial performance of the

organizations, they have started considering some additional facts about the firms like quality

management, non-financial performance, sustainability management and others. For this reason,

it is important for the business organizations to adopt the principles of integrated reporting for

managing the overall quality of their organizations. Now a days, most of the companies all over

the world are considering integrated reporting as one of the major ways to provide a reliable base

for the identification of high quality business. On the other hand, it needs to be mentioned that

the implementation of integrated reporting also helpful for the companies to bring improvements

in the aspect of quality management of the organizations. Most importantly, effective quality

management in the organizations leads to the improvements in overall financial performance of

the companies (sustainablefinancialmarkets.net 2017). Thus, it can be said that integrated

reporting in an important aspect for quality management.

Integrated Reporting and Users’ Information Needs

According to the article named “Meeting users’ information needs: The use and

usefulness of Integrated Reporting”, the implementation of integrated reporting in the business

organizations have been able to fulfill the information need of the users of the companies

(accaglobal.com 2017). At the time of taking investment decisions, the investors required

different kinds if information related to capital market, equity market and many others.

Integrated reports are considered as a major source of information for the stakeholders and

inventors (accaglobal.com 2017). However, in order to get different types of crucial information,

the stakeholders and investors are required to be familiar with various aspects of integrated

reporting (accaglobal.com 2017). This article shows that the knowledge of investors and

stakeholders of the companies regarding various aspects of integrated reporting is low and thus,

most of the times they are not able to extract the required financial as well as non-financial

information for investment decision-making (accaglobal.com 2017). For this reason, it is

required for the investors and stakeholders of the companies to acquire effective knowledge

about various aspects of integrated reports of the companies.

The University of Greenwich

8PARTICIPATION IN STANDARD SETTING

Reasons for Companies to Adopt Integrated Reporting

The above discussion shows that integrated reporting has its importance for the business

organizations from different aspects. It can be said that the companies have many reasons for the

implementation of integrated reporting in their businesses. The article named “Why Company

Should Adopt Integrated Reporting?” has mentioned many crucial reasons for the adoption of

integrated reporting by the business organizations (Hoque 2017). According to this article, in

order to overcome the deficiencies of traditional reporting system, it is required for the business

organizations to adopt the strategies of integrated reporting. In the business organizations,

integrated reporting helps the companies in the publication of one single report by combining all

necessary reports of the companies. After that, this article also states that integrated reporting

helps the business organizations in the management of sustainability aspects of them.

Sustainability reporting is considered as one of the major fundamental principles of integrated

reporting (Hoque 2017). With the help of integrated reporting, companies can well manage

sustainability reporting too. Apart from this, according to this article, Corporate Social

Responsibility (CSR) reporting is an integral part of integrated reporting. It implies that the

adoption of integrated reporting ensures that the organizations are socially as well as

environmentally responsible (Hoque 2017). It has been seen that the implementation of

integrated reporting helps in the generation of integrated thinking among the members of the

companies. IT implies that integrated reporting helps to change the corporate behavior of the

employees and upper level management. Most importantly, with the help of integrated reporting,

the organizations become able to implement corporate governance strategies in the business

organizations. Integrated reporting ensures that the stakeholders get all the necessary information

and this aspect increases stakeholder’s engagements. Thus, on the overall basis, it can be said

that integrated reporting helps in enhancing corporate reputation of the companies (Hoque 2017).

For all the above reasons, it is required for the companies to adopt the strategies of integrated

reporting.

Progress of Integrated Reporting

The article named “A lot of icing but little cake? Taking integrated reporting forward”

states about various ways to bring improvements in the aspect of integrated reporting (Perego,

Kennedy and Whiteman 2016). The first initiative to bring improvements in integrated reporting

is to gain knowledge about it. It is required for every member of the companies to have sufficient

The University of Greenwich

Reasons for Companies to Adopt Integrated Reporting

The above discussion shows that integrated reporting has its importance for the business

organizations from different aspects. It can be said that the companies have many reasons for the

implementation of integrated reporting in their businesses. The article named “Why Company

Should Adopt Integrated Reporting?” has mentioned many crucial reasons for the adoption of

integrated reporting by the business organizations (Hoque 2017). According to this article, in

order to overcome the deficiencies of traditional reporting system, it is required for the business

organizations to adopt the strategies of integrated reporting. In the business organizations,

integrated reporting helps the companies in the publication of one single report by combining all

necessary reports of the companies. After that, this article also states that integrated reporting

helps the business organizations in the management of sustainability aspects of them.

Sustainability reporting is considered as one of the major fundamental principles of integrated

reporting (Hoque 2017). With the help of integrated reporting, companies can well manage

sustainability reporting too. Apart from this, according to this article, Corporate Social

Responsibility (CSR) reporting is an integral part of integrated reporting. It implies that the

adoption of integrated reporting ensures that the organizations are socially as well as

environmentally responsible (Hoque 2017). It has been seen that the implementation of

integrated reporting helps in the generation of integrated thinking among the members of the

companies. IT implies that integrated reporting helps to change the corporate behavior of the

employees and upper level management. Most importantly, with the help of integrated reporting,

the organizations become able to implement corporate governance strategies in the business

organizations. Integrated reporting ensures that the stakeholders get all the necessary information

and this aspect increases stakeholder’s engagements. Thus, on the overall basis, it can be said

that integrated reporting helps in enhancing corporate reputation of the companies (Hoque 2017).

For all the above reasons, it is required for the companies to adopt the strategies of integrated

reporting.

Progress of Integrated Reporting

The article named “A lot of icing but little cake? Taking integrated reporting forward”

states about various ways to bring improvements in the aspect of integrated reporting (Perego,

Kennedy and Whiteman 2016). The first initiative to bring improvements in integrated reporting

is to gain knowledge about it. It is required for every member of the companies to have sufficient

The University of Greenwich

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PARTICIPATION IN STANDARD SETTING

knowledge about the process of integrated reporting. After that, it is required for the business

organizations to know the use of integrated reporting for their companies. In this context, it

needs to be mentioned that the adoption of integrated reporting is not enough for the companies

unless they are effectively installed (Perego, Kennedy and Whiteman 2016). Thus, the upper

level management of the companies is required to know the proper use of integrated reporting.

The article states that most of the companies do not have effective knowledge about the adoption

and use of integrated reporting for their businesses. Thus, based on the above discussion, it can

be seen that by obtaining effective knowledge about integrated reporting, business organizations

become able to bring improvements in their techniques for integrated reporting (Perego,

Kennedy and Whiteman 2016).

Conclusion

The above discussion makes a comparison among some of the major articles on the

challenges and benefits of Integrated Reporting. It can be seen that that all the selected articles

have stated something different about integrated reporting. The first article states that integrated

reporting can be used as a major tool for communicating financial information with the major

stakeholders and investors. In addition, it plays a crucial role in communicating the non-financial

information also. The contents of the second articles have well supported the contents of the first

article by stating the usefulness of integrated reporting in value creation in the organization.

However, high cost of integrated reporting implementation is a major challenge that the

organizational managers are required to consider while implementing it. The third article states

the role of IIRC in integrated reporting implementation. As per this article, the five major

principles of IIRC helps in the effective implementation of integrated reporting in the companies.

In this case, the six capital of integrated reporting are important parts of it. The collaboration of

IIRC and IASB is stated in the fourth article that is an important move to use integrated reporting

in financial analysis. However, the fifth article has raised a different benefit of integrated

reporting that is the role of integrated reporting in sustainability management. With the help of

integrated reporting, companies are able to publish details about their sustainability activities in a

more proper way. The sixth article shows that integrated reporting is a helpful tool for quality

management of the businesses that leads to better financial performance of the companies. The

seventh article summarizes the fact that integrated reporting provides the users with necessary

The University of Greenwich

knowledge about the process of integrated reporting. After that, it is required for the business

organizations to know the use of integrated reporting for their companies. In this context, it

needs to be mentioned that the adoption of integrated reporting is not enough for the companies

unless they are effectively installed (Perego, Kennedy and Whiteman 2016). Thus, the upper

level management of the companies is required to know the proper use of integrated reporting.

The article states that most of the companies do not have effective knowledge about the adoption

and use of integrated reporting for their businesses. Thus, based on the above discussion, it can

be seen that by obtaining effective knowledge about integrated reporting, business organizations

become able to bring improvements in their techniques for integrated reporting (Perego,

Kennedy and Whiteman 2016).

Conclusion

The above discussion makes a comparison among some of the major articles on the

challenges and benefits of Integrated Reporting. It can be seen that that all the selected articles

have stated something different about integrated reporting. The first article states that integrated

reporting can be used as a major tool for communicating financial information with the major

stakeholders and investors. In addition, it plays a crucial role in communicating the non-financial

information also. The contents of the second articles have well supported the contents of the first

article by stating the usefulness of integrated reporting in value creation in the organization.

However, high cost of integrated reporting implementation is a major challenge that the

organizational managers are required to consider while implementing it. The third article states

the role of IIRC in integrated reporting implementation. As per this article, the five major

principles of IIRC helps in the effective implementation of integrated reporting in the companies.

In this case, the six capital of integrated reporting are important parts of it. The collaboration of

IIRC and IASB is stated in the fourth article that is an important move to use integrated reporting

in financial analysis. However, the fifth article has raised a different benefit of integrated

reporting that is the role of integrated reporting in sustainability management. With the help of

integrated reporting, companies are able to publish details about their sustainability activities in a

more proper way. The sixth article shows that integrated reporting is a helpful tool for quality

management of the businesses that leads to better financial performance of the companies. The

seventh article summarizes the fact that integrated reporting provides the users with necessary

The University of Greenwich

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PARTICIPATION IN STANDARD SETTING

financial as well as non-financial information of the companies. The next article has well

supported the above-mentioned articles by stating the major reasons for the companies to adopt

integrated reporting. The last article provides some ways to improve the process of integrated

reporting in the organizations. Thus, based on the above discussion, it can be concluded that all

the articles have complemented each other in a certain way.

The University of Greenwich

financial as well as non-financial information of the companies. The next article has well

supported the above-mentioned articles by stating the major reasons for the companies to adopt

integrated reporting. The last article provides some ways to improve the process of integrated

reporting in the organizations. Thus, based on the above discussion, it can be concluded that all

the articles have complemented each other in a certain way.

The University of Greenwich

11PARTICIPATION IN STANDARD SETTING

References

Accaglobal.com. (2017). Meeting users’ information needs: The use and usefulness of Integrated

Reporting. [online] Available at:

http://www.accaglobal.com/content/dam/ACCA_Global/Technical/integrate/pi-use-usefulness-

ir.pdf [Accessed 19 Nov. 2017].

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

Doni, F. and Gasperini, A., 2016. Integrated Reporting and Financial Analysts' Perception.

Empirical evidence from Italy. In INTERDISCIPLINARY WORKSHOP ON INTANGIBLES,

INTELLECTUAL CAPITAL AND FINANCIAL INFORMATION(pp. 1-35). European Institute on

Advanced Studies on Management EIASM.

Flower, J., 2015. The international integrated reporting council: a story of failure. Critical

Perspectives on Accounting, 27, pp.1-17.

Hoque, M.E., 2017. Why Company Should Adopt Integrated Reporting?. International Journal

of Economics and Financial Issues, 7(1).

Integratedreporting.org. (2017). Integrated Reporting. [online] Available at:

https://integratedreporting.org/ [Accessed 23 Nov. 2017].

Integratedreporting.org. (2017). TOWARDS INTEGRATED REPORTING Communicating Value

in the 21st Century. [online] Available at:

http://integratedreporting.org/wp-content/uploads/2011/09/IR-Discussion-Paper-

2011_spreads.pdf [Accessed 19 Nov. 2017].

Perego, P., Kennedy, S. and Whiteman, G., 2016. A lot of icing but little cake? Taking integrated

reporting forward. Journal of Cleaner Production, 136, pp.53-64.

The University of Greenwich

References

Accaglobal.com. (2017). Meeting users’ information needs: The use and usefulness of Integrated

Reporting. [online] Available at:

http://www.accaglobal.com/content/dam/ACCA_Global/Technical/integrate/pi-use-usefulness-

ir.pdf [Accessed 19 Nov. 2017].

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

Doni, F. and Gasperini, A., 2016. Integrated Reporting and Financial Analysts' Perception.

Empirical evidence from Italy. In INTERDISCIPLINARY WORKSHOP ON INTANGIBLES,

INTELLECTUAL CAPITAL AND FINANCIAL INFORMATION(pp. 1-35). European Institute on

Advanced Studies on Management EIASM.

Flower, J., 2015. The international integrated reporting council: a story of failure. Critical

Perspectives on Accounting, 27, pp.1-17.

Hoque, M.E., 2017. Why Company Should Adopt Integrated Reporting?. International Journal

of Economics and Financial Issues, 7(1).

Integratedreporting.org. (2017). Integrated Reporting. [online] Available at:

https://integratedreporting.org/ [Accessed 23 Nov. 2017].

Integratedreporting.org. (2017). TOWARDS INTEGRATED REPORTING Communicating Value

in the 21st Century. [online] Available at:

http://integratedreporting.org/wp-content/uploads/2011/09/IR-Discussion-Paper-

2011_spreads.pdf [Accessed 19 Nov. 2017].

Perego, P., Kennedy, S. and Whiteman, G., 2016. A lot of icing but little cake? Taking integrated

reporting forward. Journal of Cleaner Production, 136, pp.53-64.

The University of Greenwich

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.