ACCM4600 - Accounting Theory: Integrated Reporting Analysis

VerifiedAdded on 2022/08/18

|17

|3526

|9

Report

AI Summary

This report provides a comprehensive analysis of integrated reporting, beginning with its background and evolution from corporate reporting. It delves into the arguments for and against its adoption, highlighting advantages such as increased stakeholder understanding and value creation, while also addressing disadvantages like implementation costs and transparency concerns. The report further examines the skills required for successful implementation, including training programs and competency matrices, along with internal adoption strategies to maximize benefits. It explores the benefits at both management and reporting levels, emphasizing the importance of communication, risk reduction, and improved decision-making. The report concludes by emphasizing the importance of integrated reporting in enhancing business value and stakeholder relations.

Running head: ACCOUNTING THEORY AND CONTEMPORARY ISSUES

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Name of Student

Name of University

Author’s Note

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Name of Student

Name of University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

EXECUTIVE SUMMARY:

This report discusses about the integrated reporting method. The detailed analysis of the

integrated reporting method has been provided in this report. The report also provides advantages

and disadvantages of the integrated reporting. This report also provides complete insight about

the methods that are required to train the employees about the integrated reporting. The process

of adoption of the integrated reporting method in the business are also been discussed in this

report. To solidify the advantages of the integrated reporting different articles and journals are

being reviewed.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

EXECUTIVE SUMMARY:

This report discusses about the integrated reporting method. The detailed analysis of the

integrated reporting method has been provided in this report. The report also provides advantages

and disadvantages of the integrated reporting. This report also provides complete insight about

the methods that are required to train the employees about the integrated reporting. The process

of adoption of the integrated reporting method in the business are also been discussed in this

report. To solidify the advantages of the integrated reporting different articles and journals are

being reviewed.

2

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

BACKGROUND OF INTEGRATED REPORTING

Founded in the year 2009 by the Prince of Wales along with the investors companies and

accounting bodies, the integrated reporting is based on International Integrated Reporting

Framework which helps to adopt the use of integrated reporting across the world. Integrated

reporting is used in most of the countries across the organisation around the world. It is an

evolution from corporate reporting which was a narrow concept in the financial statements.

Certain information’s cannot be found from the corporate report therefore the integrated report

came into practice. It is a process which helps to increase the value of the business over time.

Integrated report is a concise and detailed report which helps the organisation to understand the

strategy of the organisation as well as successfully perform in the market. To understand the

allocation of capital which is delivered to the investors, integrated reporting is very important as

it provides the necessary data about capital as well as helps the organisation to properly allocate

their capital in the business. It delivers not only financial but also non- financial performance in a

report which also provides non-financial data as social and environmental parameters. Integrated

reporting also helps the investors and stakeholders to analyse the company’s ability to create

market value in the long run (Steyn 2014). It is a sustainable report which helps the organisation

to create the value of their firm over a period of short, medium and long time. This is a broader

concept of non-financial data as well as the financial reports of the company. Integrated report

should follow the six elements to make integrated reporting successful in the organisation.

Integrated reporting should also strategically focus the goals of the organisation. It also helps the

directors with different kinds of information from the report. The stakeholders and investors also

find useful information which helps them to understand the position of the business in the

market.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

BACKGROUND OF INTEGRATED REPORTING

Founded in the year 2009 by the Prince of Wales along with the investors companies and

accounting bodies, the integrated reporting is based on International Integrated Reporting

Framework which helps to adopt the use of integrated reporting across the world. Integrated

reporting is used in most of the countries across the organisation around the world. It is an

evolution from corporate reporting which was a narrow concept in the financial statements.

Certain information’s cannot be found from the corporate report therefore the integrated report

came into practice. It is a process which helps to increase the value of the business over time.

Integrated report is a concise and detailed report which helps the organisation to understand the

strategy of the organisation as well as successfully perform in the market. To understand the

allocation of capital which is delivered to the investors, integrated reporting is very important as

it provides the necessary data about capital as well as helps the organisation to properly allocate

their capital in the business. It delivers not only financial but also non- financial performance in a

report which also provides non-financial data as social and environmental parameters. Integrated

reporting also helps the investors and stakeholders to analyse the company’s ability to create

market value in the long run (Steyn 2014). It is a sustainable report which helps the organisation

to create the value of their firm over a period of short, medium and long time. This is a broader

concept of non-financial data as well as the financial reports of the company. Integrated report

should follow the six elements to make integrated reporting successful in the organisation.

Integrated reporting should also strategically focus the goals of the organisation. It also helps the

directors with different kinds of information from the report. The stakeholders and investors also

find useful information which helps them to understand the position of the business in the

market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Integrated reporting helps the organisation in value creation. The value creation process

concepts discusses about how a company should use their resources in expanding their report.

Integrated reporting also connects the information’s of managements to identify and manage the

issues regarding to material and value creation over time which further helps to focus the

organisation to meet their short term and long term goals. This also helps in solve the issues

regarding social and environmental problems. Capital is the most important aspect in any

business. Integrated reporting helps to understand the capital of the business as well as the

sustainability of the financial functions and it helps to link between the capitals which helps to

improve the decision making of the firm. Integrated reporting helps to merge both financial and

sustainable report into one and therefore helps the company to decide and change their business

strategy as well as identify the areas of non- financial environment. Integrated report should be

concise, reliable and there should be sufficient information relating to the materiality as well as

the value creation which is needed to be evaluated in the report. Futher, integrated reporting

follows integrated reporting framework which is necessarily improve the capital position of the

business.

ARGUMENTS FOR AND AGAINST INTEGRATED REPORTING

Integrated reporting is one of the most debated matter in the reporting community. There

are various arguments relating to the usefulness of integrated reporting that needs to be

discussed. Some experts think that integrated reporting should be used in every organisation

where other stated that integrated reporting has severe issues. There are certain benefits of

integrated reporting over corporate reporting as well as some drawbacks of the same that is

needed to be argued. The advantages and disadvantages of integrated reporting are discussed

below:

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Integrated reporting helps the organisation in value creation. The value creation process

concepts discusses about how a company should use their resources in expanding their report.

Integrated reporting also connects the information’s of managements to identify and manage the

issues regarding to material and value creation over time which further helps to focus the

organisation to meet their short term and long term goals. This also helps in solve the issues

regarding social and environmental problems. Capital is the most important aspect in any

business. Integrated reporting helps to understand the capital of the business as well as the

sustainability of the financial functions and it helps to link between the capitals which helps to

improve the decision making of the firm. Integrated reporting helps to merge both financial and

sustainable report into one and therefore helps the company to decide and change their business

strategy as well as identify the areas of non- financial environment. Integrated report should be

concise, reliable and there should be sufficient information relating to the materiality as well as

the value creation which is needed to be evaluated in the report. Futher, integrated reporting

follows integrated reporting framework which is necessarily improve the capital position of the

business.

ARGUMENTS FOR AND AGAINST INTEGRATED REPORTING

Integrated reporting is one of the most debated matter in the reporting community. There

are various arguments relating to the usefulness of integrated reporting that needs to be

discussed. Some experts think that integrated reporting should be used in every organisation

where other stated that integrated reporting has severe issues. There are certain benefits of

integrated reporting over corporate reporting as well as some drawbacks of the same that is

needed to be argued. The advantages and disadvantages of integrated reporting are discussed

below:

5

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Advantages:

Integrated reporting allows the stakeholders as well as the directors to understand the

business of the organisation. It also helps to increase the funds of the organisation by reducing

the risk factors included in the business. Integrated reporting also helps the organisation in value

creation of the organisation as well as focuses on the financial approach of the business. Using

integrated reporting helps to gain competitive advantage and optimises the performance of the

organisation. Integrated reporting also helps the organisation with decision making of the boards

and management. Integrated reporting helps the firm to connect the internal management with

shareholders. The report is useful to focus on the objectives of the firm strategically. In also

describes the future orientation on the report. Integrated reporting also provides the organisation

with opportunities that will help them to enhance, establish, analyse the process of value

creation. Integrated reporting also contributes efficiently in the market by providing the liquidity

position, value of the company. It also helps to understand the value of the organisation whether

long term or short term. It also helps the organisation to gain people’s trust and therefore

increasing its reputation in the market. The increased reputation helps the company to have better

relation with the investors, employees and other stakeholders. The transparency of the integrated

reporting is one of the major factors that makes it acceptable among the companies.

Disadvantages:

Integrated reporting also includes certain disadvantages which needed to be discussed for

successfully evaluating the integrated reporting. The primary disadvantages in using integrated

reporting that it is very costly in the implementation. The requirements of resources of integrated

reporting is very high and there are complex present in integrated reporting for adopting it to

small businesses. The integrated reporting process is very time consuming and it takes great

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Advantages:

Integrated reporting allows the stakeholders as well as the directors to understand the

business of the organisation. It also helps to increase the funds of the organisation by reducing

the risk factors included in the business. Integrated reporting also helps the organisation in value

creation of the organisation as well as focuses on the financial approach of the business. Using

integrated reporting helps to gain competitive advantage and optimises the performance of the

organisation. Integrated reporting also helps the organisation with decision making of the boards

and management. Integrated reporting helps the firm to connect the internal management with

shareholders. The report is useful to focus on the objectives of the firm strategically. In also

describes the future orientation on the report. Integrated reporting also provides the organisation

with opportunities that will help them to enhance, establish, analyse the process of value

creation. Integrated reporting also contributes efficiently in the market by providing the liquidity

position, value of the company. It also helps to understand the value of the organisation whether

long term or short term. It also helps the organisation to gain people’s trust and therefore

increasing its reputation in the market. The increased reputation helps the company to have better

relation with the investors, employees and other stakeholders. The transparency of the integrated

reporting is one of the major factors that makes it acceptable among the companies.

Disadvantages:

Integrated reporting also includes certain disadvantages which needed to be discussed for

successfully evaluating the integrated reporting. The primary disadvantages in using integrated

reporting that it is very costly in the implementation. The requirements of resources of integrated

reporting is very high and there are complex present in integrated reporting for adopting it to

small businesses. The integrated reporting process is very time consuming and it takes great

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

effort in the area of operation to complete the report properly. In some areas, the connectivity

between the data’s is absent which can create massive disruption in the financial statement. Most

of the companies observed that the integrated reports are not concise and it is impossible for the

companies to evaluate the report if it is huge and massive. Before implementation if integrated

reporting, the report should be reliable and complete so that the company should implement it.

Another drawback of integrated reporting is it is very transparent and it leads to the creation of

risk for the company. The accounting process which is involved in the integrated reporting is

also very insufficient to be produced in the report, creating miss confusion around the

organisation. Another problem that is associated with the integrated reporting method is that it

does not entertain any innovation in disclosure method. Thus, the company needs to follow the

stipulated rules and regulations that are mentioned under the guidebook of integrated reporting.

SKILLS REQUIRED FOR IMPLEMENTATION OF INTEGRATED REPORTING

Before implementation of integrated reporting, certain training and skills are required to

be provided to the employees in the organisation.

IIRC has released a new matrix of competence which will help to implement integrated

reporting globally therefore easily implementing the training. This matrix helps the employees to

implement the reporting framework and also helps to understand the behaviour and skills needed

to work in the integrated reporting environment. This matrix uses principles based approach

which helps to learn the outcome of the business as well as building professional skills needed

for implementation of integrated reporting (Thomson 2015). The training is focused on different

companies and organisation which will help the employees to understand integrated reporting

better. Further, this process will also increase the skill of the employees before implementation

of IR. It will also help the employees to know the benefits of implementation of integrated

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

effort in the area of operation to complete the report properly. In some areas, the connectivity

between the data’s is absent which can create massive disruption in the financial statement. Most

of the companies observed that the integrated reports are not concise and it is impossible for the

companies to evaluate the report if it is huge and massive. Before implementation if integrated

reporting, the report should be reliable and complete so that the company should implement it.

Another drawback of integrated reporting is it is very transparent and it leads to the creation of

risk for the company. The accounting process which is involved in the integrated reporting is

also very insufficient to be produced in the report, creating miss confusion around the

organisation. Another problem that is associated with the integrated reporting method is that it

does not entertain any innovation in disclosure method. Thus, the company needs to follow the

stipulated rules and regulations that are mentioned under the guidebook of integrated reporting.

SKILLS REQUIRED FOR IMPLEMENTATION OF INTEGRATED REPORTING

Before implementation of integrated reporting, certain training and skills are required to

be provided to the employees in the organisation.

IIRC has released a new matrix of competence which will help to implement integrated

reporting globally therefore easily implementing the training. This matrix helps the employees to

implement the reporting framework and also helps to understand the behaviour and skills needed

to work in the integrated reporting environment. This matrix uses principles based approach

which helps to learn the outcome of the business as well as building professional skills needed

for implementation of integrated reporting (Thomson 2015). The training is focused on different

companies and organisation which will help the employees to understand integrated reporting

better. Further, this process will also increase the skill of the employees before implementation

of IR. It will also help the employees to know the benefits of implementation of integrated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

reporting. The competence matrix has four areas which includes integrated reporting, integrated

thinking, the integrated report and implementation of integrated reporting. The competence

matrix involves two competences introductory and practitioner. Introductory level trains the

employees about the integrated thinking as well as discusses about the integrated reporting. It

also helps the employees to understand the concepts of capital, value creation and the process of

value creation. The factors which will help in successful implementation of integrated report will

be also discussed in this level. On the other hand, practitioner levels demonstrate the employees

about the learning outcomes of integrated report. Also it applies the value creation, capital and

the processes of value creation to the organisation. It also advices the requirements of integrated

reporting framework in the organisation as well as helps the organisation to participate

effectively in the team planning and the implementation of the integrated reporting.

Before implementing the internal reporting training the company needs to conduct a

meeting where the management of the company needs to analyse the feasible method that can be

implemented to train the employees of the company. The meeting will also provide clear idea

about the time that the company will require to train their employees about the integrated

reporting. The training of the integrated reporting is considered to be less costly in comparison to

the training of other reporting standard. The review process will also assist the company to draw

a clear idea about the time and costs involve in the implementation of the integrated reporting.

Thus, the integrated reporting system will be much more feasible in comparison to other

reporting standard.

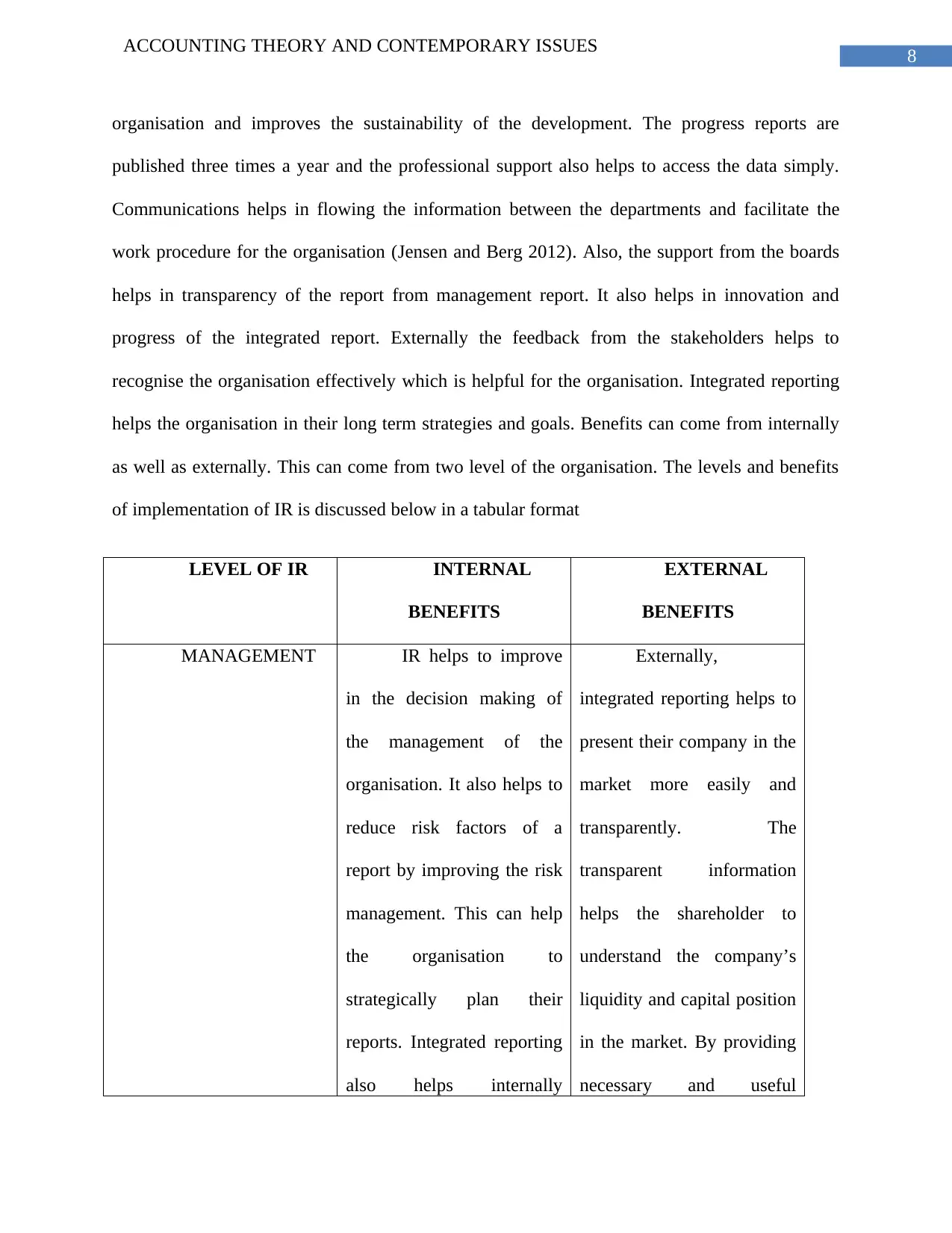

INTERNALLY ADOPTION OF INTEGRATED REPORTING:

Integrated reporting should be adopted internally as well as externally so that the

maximum benefit can be achieved by the organisation. It helps to improve the structure of the

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

reporting. The competence matrix has four areas which includes integrated reporting, integrated

thinking, the integrated report and implementation of integrated reporting. The competence

matrix involves two competences introductory and practitioner. Introductory level trains the

employees about the integrated thinking as well as discusses about the integrated reporting. It

also helps the employees to understand the concepts of capital, value creation and the process of

value creation. The factors which will help in successful implementation of integrated report will

be also discussed in this level. On the other hand, practitioner levels demonstrate the employees

about the learning outcomes of integrated report. Also it applies the value creation, capital and

the processes of value creation to the organisation. It also advices the requirements of integrated

reporting framework in the organisation as well as helps the organisation to participate

effectively in the team planning and the implementation of the integrated reporting.

Before implementing the internal reporting training the company needs to conduct a

meeting where the management of the company needs to analyse the feasible method that can be

implemented to train the employees of the company. The meeting will also provide clear idea

about the time that the company will require to train their employees about the integrated

reporting. The training of the integrated reporting is considered to be less costly in comparison to

the training of other reporting standard. The review process will also assist the company to draw

a clear idea about the time and costs involve in the implementation of the integrated reporting.

Thus, the integrated reporting system will be much more feasible in comparison to other

reporting standard.

INTERNALLY ADOPTION OF INTEGRATED REPORTING:

Integrated reporting should be adopted internally as well as externally so that the

maximum benefit can be achieved by the organisation. It helps to improve the structure of the

8

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

organisation and improves the sustainability of the development. The progress reports are

published three times a year and the professional support also helps to access the data simply.

Communications helps in flowing the information between the departments and facilitate the

work procedure for the organisation (Jensen and Berg 2012). Also, the support from the boards

helps in transparency of the report from management report. It also helps in innovation and

progress of the integrated report. Externally the feedback from the stakeholders helps to

recognise the organisation effectively which is helpful for the organisation. Integrated reporting

helps the organisation in their long term strategies and goals. Benefits can come from internally

as well as externally. This can come from two level of the organisation. The levels and benefits

of implementation of IR is discussed below in a tabular format

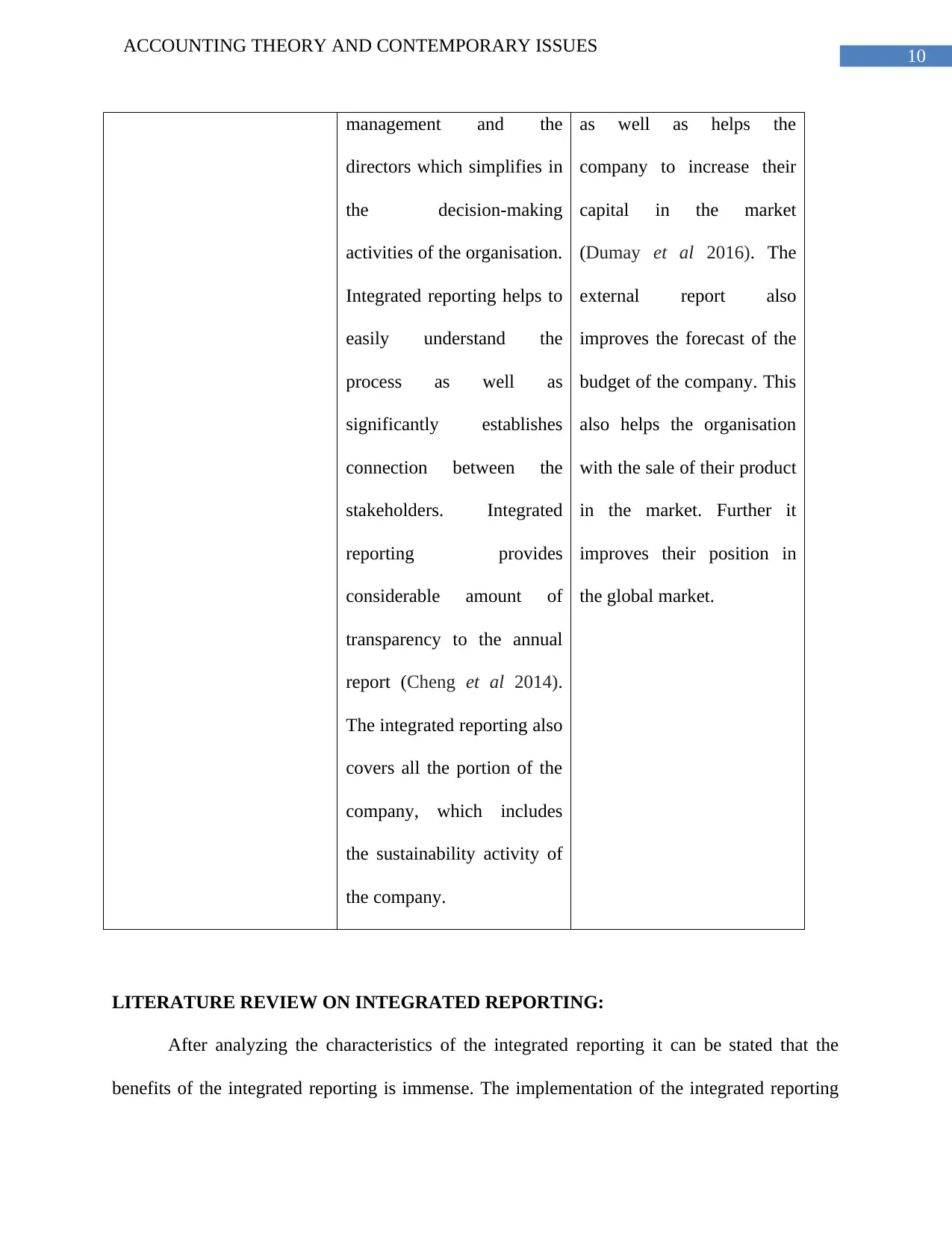

LEVEL OF IR INTERNAL

BENEFITS

EXTERNAL

BENEFITS

MANAGEMENT IR helps to improve

in the decision making of

the management of the

organisation. It also helps to

reduce risk factors of a

report by improving the risk

management. This can help

the organisation to

strategically plan their

reports. Integrated reporting

also helps internally

Externally,

integrated reporting helps to

present their company in the

market more easily and

transparently. The

transparent information

helps the shareholder to

understand the company’s

liquidity and capital position

in the market. By providing

necessary and useful

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

organisation and improves the sustainability of the development. The progress reports are

published three times a year and the professional support also helps to access the data simply.

Communications helps in flowing the information between the departments and facilitate the

work procedure for the organisation (Jensen and Berg 2012). Also, the support from the boards

helps in transparency of the report from management report. It also helps in innovation and

progress of the integrated report. Externally the feedback from the stakeholders helps to

recognise the organisation effectively which is helpful for the organisation. Integrated reporting

helps the organisation in their long term strategies and goals. Benefits can come from internally

as well as externally. This can come from two level of the organisation. The levels and benefits

of implementation of IR is discussed below in a tabular format

LEVEL OF IR INTERNAL

BENEFITS

EXTERNAL

BENEFITS

MANAGEMENT IR helps to improve

in the decision making of

the management of the

organisation. It also helps to

reduce risk factors of a

report by improving the risk

management. This can help

the organisation to

strategically plan their

reports. Integrated reporting

also helps internally

Externally,

integrated reporting helps to

present their company in the

market more easily and

transparently. The

transparent information

helps the shareholder to

understand the company’s

liquidity and capital position

in the market. By providing

necessary and useful

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

understanding in the value

creation and different

concepts of materiality and

value creation

implementation. This helps

the board of directors to

understand the management

of the organisation from the

report helping to remove any

gap in communication.

information in the report, it

helps to gain certain

advantages from their

competitors. The

shareholders are also helful

by this integrated reporting.

Integrated reporting helps to

improve the relation

between the shareholders by

communicating more

efficiently.

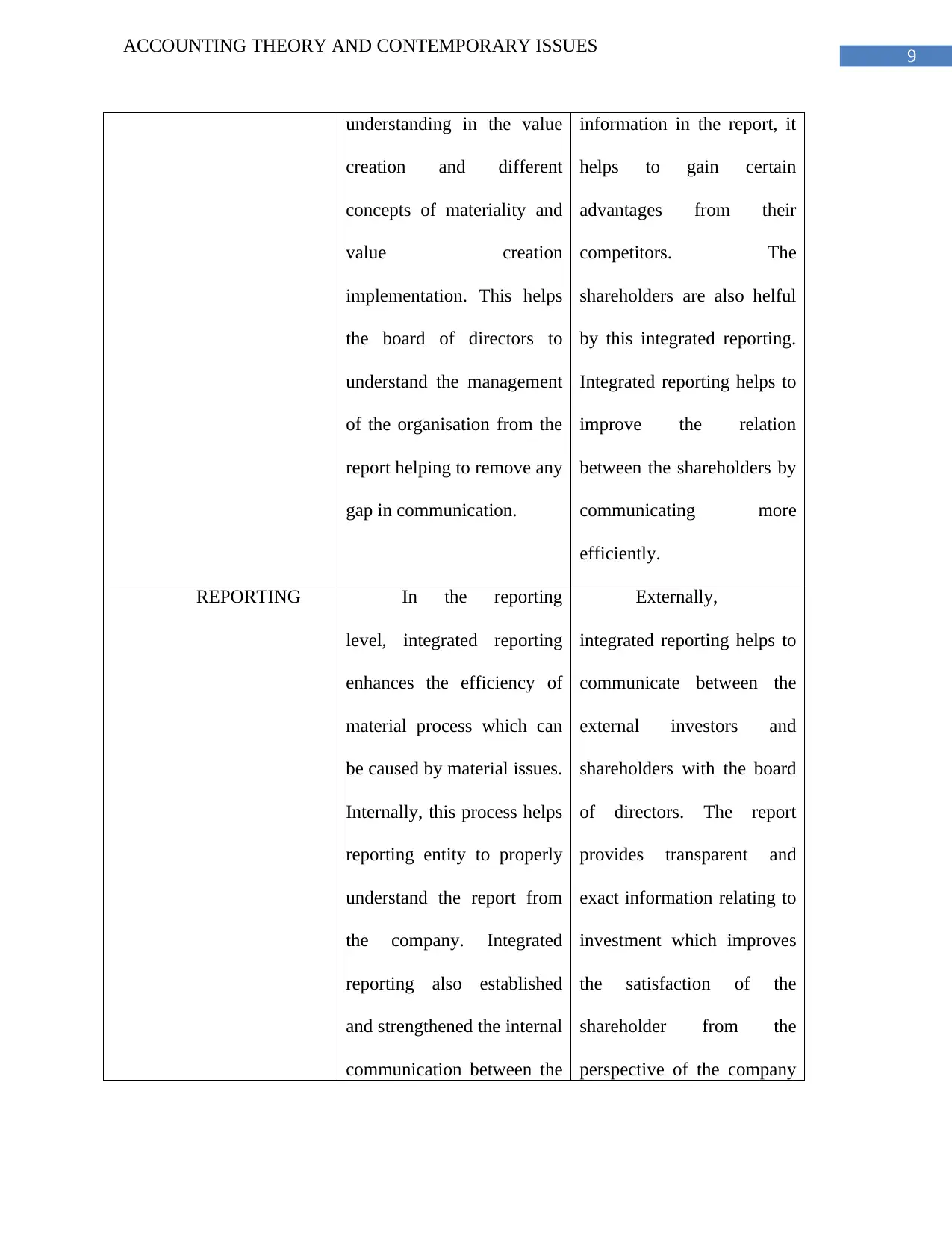

REPORTING In the reporting

level, integrated reporting

enhances the efficiency of

material process which can

be caused by material issues.

Internally, this process helps

reporting entity to properly

understand the report from

the company. Integrated

reporting also established

and strengthened the internal

communication between the

Externally,

integrated reporting helps to

communicate between the

external investors and

shareholders with the board

of directors. The report

provides transparent and

exact information relating to

investment which improves

the satisfaction of the

shareholder from the

perspective of the company

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

understanding in the value

creation and different

concepts of materiality and

value creation

implementation. This helps

the board of directors to

understand the management

of the organisation from the

report helping to remove any

gap in communication.

information in the report, it

helps to gain certain

advantages from their

competitors. The

shareholders are also helful

by this integrated reporting.

Integrated reporting helps to

improve the relation

between the shareholders by

communicating more

efficiently.

REPORTING In the reporting

level, integrated reporting

enhances the efficiency of

material process which can

be caused by material issues.

Internally, this process helps

reporting entity to properly

understand the report from

the company. Integrated

reporting also established

and strengthened the internal

communication between the

Externally,

integrated reporting helps to

communicate between the

external investors and

shareholders with the board

of directors. The report

provides transparent and

exact information relating to

investment which improves

the satisfaction of the

shareholder from the

perspective of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

management and the

directors which simplifies in

the decision-making

activities of the organisation.

Integrated reporting helps to

easily understand the

process as well as

significantly establishes

connection between the

stakeholders. Integrated

reporting provides

considerable amount of

transparency to the annual

report (Cheng et al 2014).

The integrated reporting also

covers all the portion of the

company, which includes

the sustainability activity of

the company.

as well as helps the

company to increase their

capital in the market

(Dumay et al 2016). The

external report also

improves the forecast of the

budget of the company. This

also helps the organisation

with the sale of their product

in the market. Further it

improves their position in

the global market.

LITERATURE REVIEW ON INTEGRATED REPORTING:

After analyzing the characteristics of the integrated reporting it can be stated that the

benefits of the integrated reporting is immense. The implementation of the integrated reporting

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

management and the

directors which simplifies in

the decision-making

activities of the organisation.

Integrated reporting helps to

easily understand the

process as well as

significantly establishes

connection between the

stakeholders. Integrated

reporting provides

considerable amount of

transparency to the annual

report (Cheng et al 2014).

The integrated reporting also

covers all the portion of the

company, which includes

the sustainability activity of

the company.

as well as helps the

company to increase their

capital in the market

(Dumay et al 2016). The

external report also

improves the forecast of the

budget of the company. This

also helps the organisation

with the sale of their product

in the market. Further it

improves their position in

the global market.

LITERATURE REVIEW ON INTEGRATED REPORTING:

After analyzing the characteristics of the integrated reporting it can be stated that the

benefits of the integrated reporting is immense. The implementation of the integrated reporting

11

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

requires several steps but the cost associated with the implementation of the reporting is much

less in comparison to the other process of reporting. The adoption of the integrated reporting is

also very feasible, as it assists the company to implement it within a short period of time. To

solidify the statement this report uses several articles.

As stated by Robert and Daniela in their journal “Achieving Sustainability through

Integrated Reporting” about the benefits of implementing the integrated reporting in the financial

system of any organization. The authors also discussed about the emergence of the integrated

reporting in the business world. The authors substantiate their point by showing the example of

implementation of integrated reporting in a company. The journal used Royal Philips Electronics

as an example. As per the authors, the Amsterdam based giant first adopts the integrated

reporting system in 2008 in their annual report. The company from then continued to use the

integrated reporting in their annual report because the company finds sustainability as a driver

for growth, which is also happens to be an integral part of integrated reporting (Eccles and

Saltzman 2011). The integrated reporting was one of the forces that assist the company to

increase their efficiency and also reduced cost. The authors also stated that integrated reporting

assists the company to improve their communication. The authors also related the role of civil

society with integrated reporting. As per the author integrated reporting considers the climate

change and other environmental issues in their report. The author also mentioned that integrated

reporting assists the company to showcase their transparency in the annual report.

It is often seen that traditional sustainability reporting is much better in comparison to the

integrated reporting system. The same was showcased by Julia and Nicola Berg in its article

where determinants of traditional sustainability reporting versus integrated reporting are being

explained. In this article the author used institutional theory to compare both the theories of

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

requires several steps but the cost associated with the implementation of the reporting is much

less in comparison to the other process of reporting. The adoption of the integrated reporting is

also very feasible, as it assists the company to implement it within a short period of time. To

solidify the statement this report uses several articles.

As stated by Robert and Daniela in their journal “Achieving Sustainability through

Integrated Reporting” about the benefits of implementing the integrated reporting in the financial

system of any organization. The authors also discussed about the emergence of the integrated

reporting in the business world. The authors substantiate their point by showing the example of

implementation of integrated reporting in a company. The journal used Royal Philips Electronics

as an example. As per the authors, the Amsterdam based giant first adopts the integrated

reporting system in 2008 in their annual report. The company from then continued to use the

integrated reporting in their annual report because the company finds sustainability as a driver

for growth, which is also happens to be an integral part of integrated reporting (Eccles and

Saltzman 2011). The integrated reporting was one of the forces that assist the company to

increase their efficiency and also reduced cost. The authors also stated that integrated reporting

assists the company to improve their communication. The authors also related the role of civil

society with integrated reporting. As per the author integrated reporting considers the climate

change and other environmental issues in their report. The author also mentioned that integrated

reporting assists the company to showcase their transparency in the annual report.

It is often seen that traditional sustainability reporting is much better in comparison to the

integrated reporting system. The same was showcased by Julia and Nicola Berg in its article

where determinants of traditional sustainability reporting versus integrated reporting are being

explained. In this article the author used institutional theory to compare both the theories of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.