Management Accounting: Performance Evaluation of ITS (UK) Ltd

VerifiedAdded on 2020/02/05

|15

|4338

|97

Report

AI Summary

This report provides a comprehensive analysis of the performance of Integrated Technology Services (ITS), a UK-based technology solutions provider. It begins with an introduction to management accounting and performance evaluation, emphasizing the role of balance scorecards (BSC) in assessing both financial and non-financial aspects of the business. Task 1 explains the use of BSC for performance evaluation within ITS, highlighting its benefits in measuring key performance indicators across four perspectives: learning and growth, business processes, customers, and finances. Task 2 focuses on creating a balanced scorecard tailored for ITS, outlining the strategic objectives and performance measures for each perspective. Task 3 provides recommendations to the ITS board regarding the recruitment of an additional accountant, considering the benefits and costs associated with the decision. The report concludes by summarizing the findings and emphasizing the importance of strategic planning and performance management for ITS's future success.

MANAGEMENT

ACCOUNTING

PERFORMANCE

EVALUATION

ACCOUNTING

PERFORMANCE

EVALUATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 1 .....................................................................................................................................1

Explaining the use of balance scorecards for performance evaluation in ITS......................1

TASK 2......................................................................................................................................5

Creating Balanced Scorecard for Integrated Technology Services (UK)..............................5

TASK 3......................................................................................................................................7

TASK 4......................................................................................................................................9

TASK 5......................................................................................................................................9

Review of the use of Integrated Technological Service share scheme whether it helps to . .9

motivate employees to work towards achieving the goals or not..........................................9

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

Index of Tables

Table 1: Balanced Scorecards of Integrated Technology Services Ltd......................................9

INTRODUCTION......................................................................................................................1

TASK 1 .....................................................................................................................................1

Explaining the use of balance scorecards for performance evaluation in ITS......................1

TASK 2......................................................................................................................................5

Creating Balanced Scorecard for Integrated Technology Services (UK)..............................5

TASK 3......................................................................................................................................7

TASK 4......................................................................................................................................9

TASK 5......................................................................................................................................9

Review of the use of Integrated Technological Service share scheme whether it helps to . .9

motivate employees to work towards achieving the goals or not..........................................9

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

Index of Tables

Table 1: Balanced Scorecards of Integrated Technology Services Ltd......................................9

INTRODUCTION

In the present age, management plays an crucial role in the company's success as they

make business planning, controlling, coordinating the functions and take strategic decisions

in order to perform better in future. Present market is highly competitive in which every

business organization need to use advanced technology to compete effectively in the market.

Integrated Technology Services (ITS) is a UK based organization who is responsible to

provide best quality of information technological products and services to large number of

consumers. It was established in the year 1995 and highly dedicated to fulfil customer needs

through serving them qualitative products. Present project report will discuss the range of

financial as well as non-financial performance measurement tools that can be use by ITS for

performance evaluation. Balance scorecards is one of the significant tools that can be use by

ITS's management to evaluate and examine and examine their performance so that managing

director can take efficient quality of decision. It will lead to improve future performance of

the company to a great extent.

TASK 1

Explaining the use of balance scorecards for performance evaluation in ITS

ITS (UK) Ltd, is a providing wide range of communication services that includes

telephone services, Local Area Network (LAN)/Wide Area Network (WAN) , Video

conferencing, Video Surveillance, Access Control, Networking Services and other data

security services to large number of users. The aim of ITS is to serve customers with

exceptional services and at cost effective prices. ITS uses six selection criteria to achieve this

objective that are quality, reliability, ease of use, cost effectiveness, continuous evolution and

market commitment. All these factors lead to fulfil customer demand effectively.

In the present age, management plays an crucial role in the company's success as they

make business planning, controlling, coordinating the functions and take strategic decisions

in order to perform better in future. Present market is highly competitive in which every

business organization need to use advanced technology to compete effectively in the market.

Integrated Technology Services (ITS) is a UK based organization who is responsible to

provide best quality of information technological products and services to large number of

consumers. It was established in the year 1995 and highly dedicated to fulfil customer needs

through serving them qualitative products. Present project report will discuss the range of

financial as well as non-financial performance measurement tools that can be use by ITS for

performance evaluation. Balance scorecards is one of the significant tools that can be use by

ITS's management to evaluate and examine and examine their performance so that managing

director can take efficient quality of decision. It will lead to improve future performance of

the company to a great extent.

TASK 1

Explaining the use of balance scorecards for performance evaluation in ITS

ITS (UK) Ltd, is a providing wide range of communication services that includes

telephone services, Local Area Network (LAN)/Wide Area Network (WAN) , Video

conferencing, Video Surveillance, Access Control, Networking Services and other data

security services to large number of users. The aim of ITS is to serve customers with

exceptional services and at cost effective prices. ITS uses six selection criteria to achieve this

objective that are quality, reliability, ease of use, cost effectiveness, continuous evolution and

market commitment. All these factors lead to fulfil customer demand effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the scenario, Group Managing Director of ITS faced a declined in net profit by

6%. It indicates that ITS's financial performance in terms of profitability has been reduced.

Now, directors are wishing to identify the reasons behind this adverse business performance.

Balance scorecards (BSC) is an effective tool available for this purpose. It is a strategic

planning and performance management tool that is highly using in the present market. It

helps to measure ITS's financial as well as non-financial performance to a great extent

(Grigoroudis, Orfanoudaki and Zopounidis, 2012). It is a tool that assist managing directors

to keep track of execution of all the operating activities by the staff within their control and

monitor these functions on a regular basis. Some of the most important characteristics of BSC

is given below:

It highlight the strategy of the company through focusing on cause and effect

relationship among different elements. In context to Integrated Technology Services,

it can use BSC which pinpoint about its objectives and strategic goals. In other words,

BSC will help to focus on the strategic agenda of ITS (Giannopoulos and et.al., 2013).

It helps to communicate formulated business strategy to all the members of Integrated

Technology Services. This in turn, all the associated members will do their work

accordingly to it and take decisions that will contribute to accomplish ITS's targets in

a great manner.

In ITS, BSC system will help to give strong emphasis on its financial as well as non-

financial objectives. Under the financial performance, it helps to analyse revenues,

6%. It indicates that ITS's financial performance in terms of profitability has been reduced.

Now, directors are wishing to identify the reasons behind this adverse business performance.

Balance scorecards (BSC) is an effective tool available for this purpose. It is a strategic

planning and performance management tool that is highly using in the present market. It

helps to measure ITS's financial as well as non-financial performance to a great extent

(Grigoroudis, Orfanoudaki and Zopounidis, 2012). It is a tool that assist managing directors

to keep track of execution of all the operating activities by the staff within their control and

monitor these functions on a regular basis. Some of the most important characteristics of BSC

is given below:

It highlight the strategy of the company through focusing on cause and effect

relationship among different elements. In context to Integrated Technology Services,

it can use BSC which pinpoint about its objectives and strategic goals. In other words,

BSC will help to focus on the strategic agenda of ITS (Giannopoulos and et.al., 2013).

It helps to communicate formulated business strategy to all the members of Integrated

Technology Services. This in turn, all the associated members will do their work

accordingly to it and take decisions that will contribute to accomplish ITS's targets in

a great manner.

In ITS, BSC system will help to give strong emphasis on its financial as well as non-

financial objectives. Under the financial performance, it helps to analyse revenues,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost and business profitability of ITS (Machado, 2013). While, other non-financial

performance indicators includes learning and growth, customer satisfaction and

business process perspective.

It focuses management attention to the key factors while formulating the business

strategy. So that, each and every elements that can contribute to achieve success can

be covered in managerial planning of Integrated Technology Services.

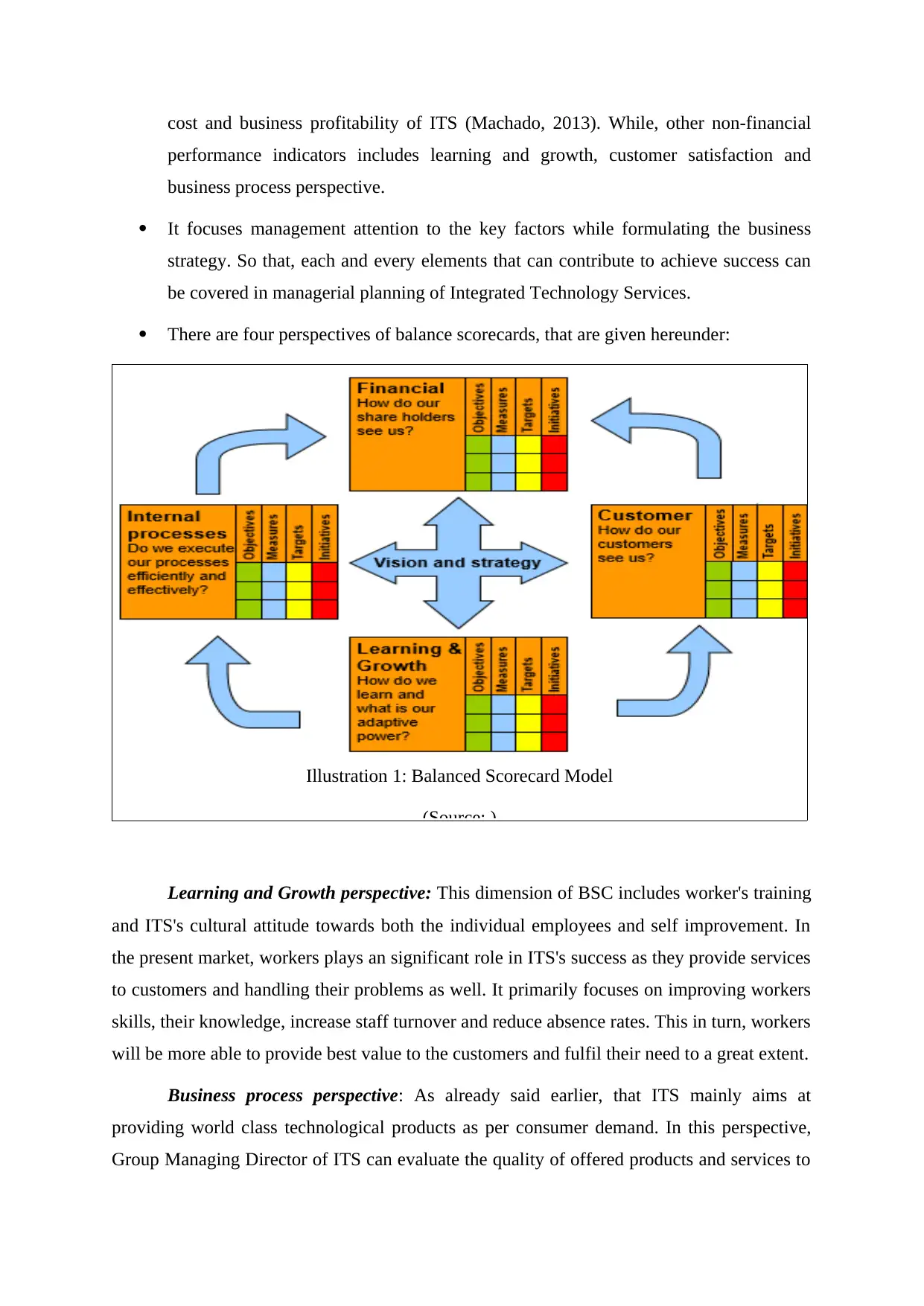

There are four perspectives of balance scorecards, that are given hereunder:

Illustration 1: Balanced Scorecard Model

(Source: )

Learning and Growth perspective: This dimension of BSC includes worker's training

and ITS's cultural attitude towards both the individual employees and self improvement. In

the present market, workers plays an significant role in ITS's success as they provide services

to customers and handling their problems as well. It primarily focuses on improving workers

skills, their knowledge, increase staff turnover and reduce absence rates. This in turn, workers

will be more able to provide best value to the customers and fulfil their need to a great extent.

Business process perspective: As already said earlier, that ITS mainly aims at

providing world class technological products as per consumer demand. In this perspective,

Group Managing Director of ITS can evaluate the quality of offered products and services to

performance indicators includes learning and growth, customer satisfaction and

business process perspective.

It focuses management attention to the key factors while formulating the business

strategy. So that, each and every elements that can contribute to achieve success can

be covered in managerial planning of Integrated Technology Services.

There are four perspectives of balance scorecards, that are given hereunder:

Illustration 1: Balanced Scorecard Model

(Source: )

Learning and Growth perspective: This dimension of BSC includes worker's training

and ITS's cultural attitude towards both the individual employees and self improvement. In

the present market, workers plays an significant role in ITS's success as they provide services

to customers and handling their problems as well. It primarily focuses on improving workers

skills, their knowledge, increase staff turnover and reduce absence rates. This in turn, workers

will be more able to provide best value to the customers and fulfil their need to a great extent.

Business process perspective: As already said earlier, that ITS mainly aims at

providing world class technological products as per consumer demand. In this perspective,

Group Managing Director of ITS can evaluate the quality of offered products and services to

analyse its non-financial performance. In the current climate of rapid technological change,

ITS is fulfilling customer need through providing innovated and advanced products (Larsson,

Säfsten and Syberfeldt, 2015). Henceforth, quality is the most significant factor that can

contribute to the business success or failure as well. In context to ITS, company is regularly

trying to offer value added and qualitative products which satisfy large consumers demand.

Customer perspective: In the present competitive age, all the organizations are

competing with each other to increase their customer base so as to attain high growth and

success. This dimension says that ITS cannot achieve this mission without satisfying their

customers. Therefore, this perspective helps to assess the level of consumer satisfaction

through using ITS's products and services. Moreover, it includes the analysis of ITS's market

share, consumer retention, delivery of consumer orders and their complaints. This in turn,

Group Managing Director can evaluate their non-financial performance in the market.

Financial perspective: Along with all above mentioned non-financial performance

indicators, it is also important for ITS to analyse their financial performance. As per financial

perspective, Integrated Technology Services Ltd, need to determine its revenues, growth in

revenues, change in costs and profitability to identify its financial performance (Chee and

et.al., 2006). Rising trend of revenues and profitability is a good sign of ITS's financial

performance and vice versa.

It is a organization's strategic map that assist businesses to accomplish their target

goals and mission. It helps to fulfil short-term as well as long-term business

objectives. Moreover, implementation of formulated strategic planning effectively

helps to improve potential performance and enjoy high growth and success

(Humphreys, Gary and Trotman, 2015).

On the basis of above benefits, it has became clear that ITS can make use of BSC to

carry out an in-depth evaluation of business performance. Group Managing Directors of ITS

can construct an BSC through considering all the four perspective. BSC must demonstrates

ITS's primary and secondary objectives to drive high success in future period. MD has to

group a set of different performance measurements indicators in each perspective to make

detailed evaluation of ITS performance.

ITS is fulfilling customer need through providing innovated and advanced products (Larsson,

Säfsten and Syberfeldt, 2015). Henceforth, quality is the most significant factor that can

contribute to the business success or failure as well. In context to ITS, company is regularly

trying to offer value added and qualitative products which satisfy large consumers demand.

Customer perspective: In the present competitive age, all the organizations are

competing with each other to increase their customer base so as to attain high growth and

success. This dimension says that ITS cannot achieve this mission without satisfying their

customers. Therefore, this perspective helps to assess the level of consumer satisfaction

through using ITS's products and services. Moreover, it includes the analysis of ITS's market

share, consumer retention, delivery of consumer orders and their complaints. This in turn,

Group Managing Director can evaluate their non-financial performance in the market.

Financial perspective: Along with all above mentioned non-financial performance

indicators, it is also important for ITS to analyse their financial performance. As per financial

perspective, Integrated Technology Services Ltd, need to determine its revenues, growth in

revenues, change in costs and profitability to identify its financial performance (Chee and

et.al., 2006). Rising trend of revenues and profitability is a good sign of ITS's financial

performance and vice versa.

It is a organization's strategic map that assist businesses to accomplish their target

goals and mission. It helps to fulfil short-term as well as long-term business

objectives. Moreover, implementation of formulated strategic planning effectively

helps to improve potential performance and enjoy high growth and success

(Humphreys, Gary and Trotman, 2015).

On the basis of above benefits, it has became clear that ITS can make use of BSC to

carry out an in-depth evaluation of business performance. Group Managing Directors of ITS

can construct an BSC through considering all the four perspective. BSC must demonstrates

ITS's primary and secondary objectives to drive high success in future period. MD has to

group a set of different performance measurements indicators in each perspective to make

detailed evaluation of ITS performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

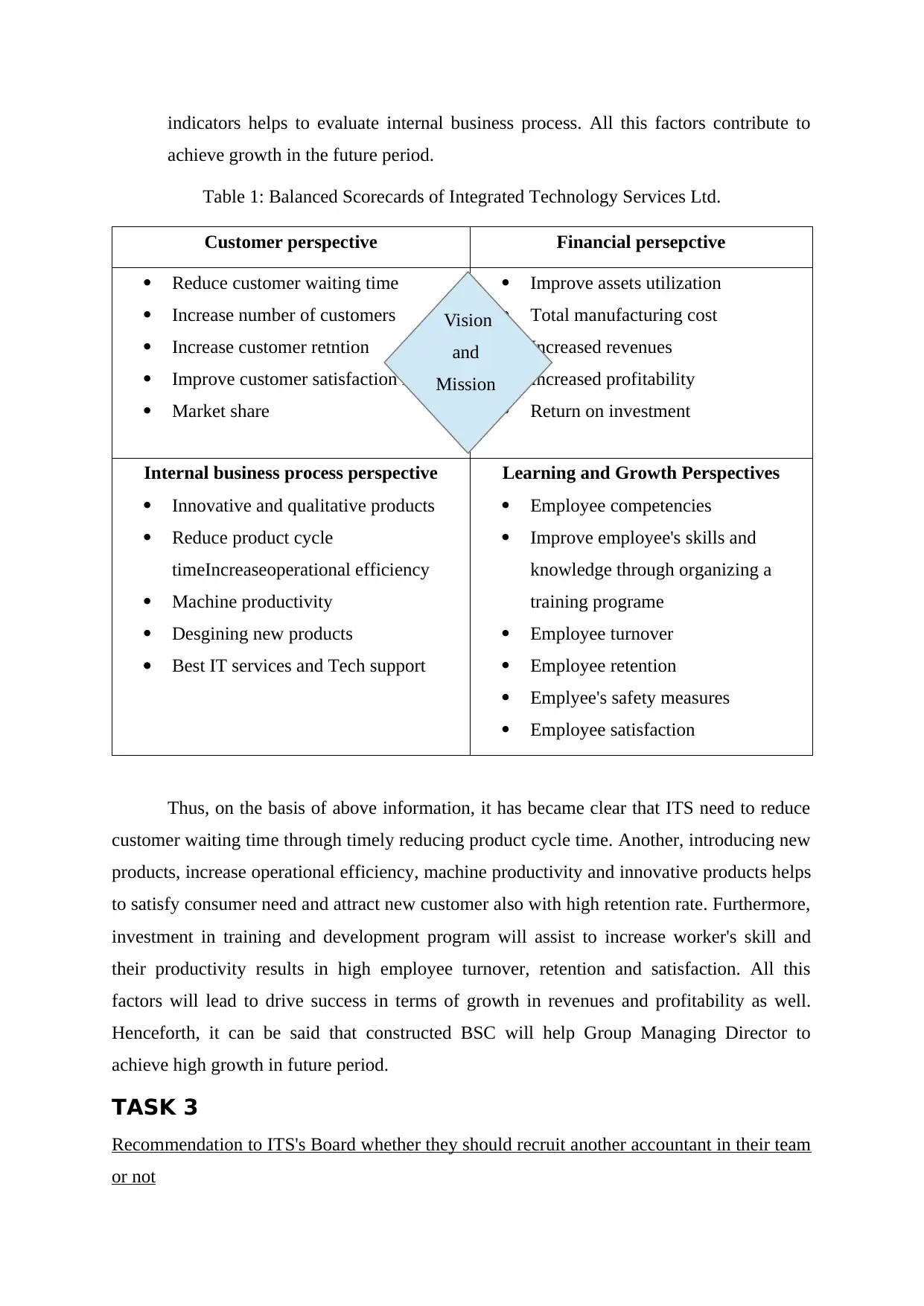

TASK 2

Creating Balanced Scorecard for Integrated Technology Services (UK)

BSC has been constructed here for ITS through which Group Managing Director will

be highly able to evaluate their performance. The scorecards will give assistance to ITS to

make strategic planning and communicate this plan to all the users such as managers,

employees and analysts.

BSC requires an in-depth planning in which each and every element that can cntribute

towards ITS success must be covered. There are some requisites that must be keep in mind

while making BSC, described below: Focus on primary objective: Integrated Technological Services Ltd is a profit seeking

organization henceforth, it primary objective is to get maximum revenues and

profitability as well. Therefore, it becomes necessary that BSC focuses on business

goals for which ITS has been established. In context to ITS, increase shareholders

wealth and profitability are its objectives. Relationship between business process and its contribution to achieve target: There

after, ITS need to be develop a relationship between business operations and its

contribution to achieve target goals. For instance, ITS's business process that is

concerned about offering qualitative and technological products and services helps to

drive large revenues and profits (Allan, n.d).

Developing secondary business objectives: This is the most challenging step in

construction of BSC for ITS. This task relates to the investment in various functions

to achieve desired outcomes. For instance, this task will answer that how much funds

will need to be invest in ITS's training and development programme, quality

improvement and customer satisfaction so that business performance can be

improved.

Develop different measurement to monitor performance: It is the conventional

concept in which ITS need to set different measurement for performance analysis. For

instance, under the customer perspective. ITS need to set some measurement to

analyse the level of consumer satisfaction (Dudin, 2015). However, under the learning

and growth perspective, ITS need to set out some elements that evaluate employees

motivation, skills and their knowledge. On contrary to it, quality measurement

Creating Balanced Scorecard for Integrated Technology Services (UK)

BSC has been constructed here for ITS through which Group Managing Director will

be highly able to evaluate their performance. The scorecards will give assistance to ITS to

make strategic planning and communicate this plan to all the users such as managers,

employees and analysts.

BSC requires an in-depth planning in which each and every element that can cntribute

towards ITS success must be covered. There are some requisites that must be keep in mind

while making BSC, described below: Focus on primary objective: Integrated Technological Services Ltd is a profit seeking

organization henceforth, it primary objective is to get maximum revenues and

profitability as well. Therefore, it becomes necessary that BSC focuses on business

goals for which ITS has been established. In context to ITS, increase shareholders

wealth and profitability are its objectives. Relationship between business process and its contribution to achieve target: There

after, ITS need to be develop a relationship between business operations and its

contribution to achieve target goals. For instance, ITS's business process that is

concerned about offering qualitative and technological products and services helps to

drive large revenues and profits (Allan, n.d).

Developing secondary business objectives: This is the most challenging step in

construction of BSC for ITS. This task relates to the investment in various functions

to achieve desired outcomes. For instance, this task will answer that how much funds

will need to be invest in ITS's training and development programme, quality

improvement and customer satisfaction so that business performance can be

improved.

Develop different measurement to monitor performance: It is the conventional

concept in which ITS need to set different measurement for performance analysis. For

instance, under the customer perspective. ITS need to set some measurement to

analyse the level of consumer satisfaction (Dudin, 2015). However, under the learning

and growth perspective, ITS need to set out some elements that evaluate employees

motivation, skills and their knowledge. On contrary to it, quality measurement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indicators helps to evaluate internal business process. All this factors contribute to

achieve growth in the future period.

Table 1: Balanced Scorecards of Integrated Technology Services Ltd.

Customer perspective Financial persepctive

Reduce customer waiting time

Increase number of customers

Increase customer retntion

Improve customer satisfaction level

Market share

Improve assets utilization

Total manufacturing cost

Increased revenues

Increased profitability

Return on investment

Internal business process perspective

Innovative and qualitative products

Reduce product cycle

timeIncreaseoperational efficiency

Machine productivity

Desgining new products

Best IT services and Tech support

Learning and Growth Perspectives

Employee competencies

Improve employee's skills and

knowledge through organizing a

training programe

Employee turnover

Employee retention

Emplyee's safety measures

Employee satisfaction

Thus, on the basis of above information, it has became clear that ITS need to reduce

customer waiting time through timely reducing product cycle time. Another, introducing new

products, increase operational efficiency, machine productivity and innovative products helps

to satisfy consumer need and attract new customer also with high retention rate. Furthermore,

investment in training and development program will assist to increase worker's skill and

their productivity results in high employee turnover, retention and satisfaction. All this

factors will lead to drive success in terms of growth in revenues and profitability as well.

Henceforth, it can be said that constructed BSC will help Group Managing Director to

achieve high growth in future period.

TASK 3

Recommendation to ITS's Board whether they should recruit another accountant in their team

or not

Vision

and

Mission

achieve growth in the future period.

Table 1: Balanced Scorecards of Integrated Technology Services Ltd.

Customer perspective Financial persepctive

Reduce customer waiting time

Increase number of customers

Increase customer retntion

Improve customer satisfaction level

Market share

Improve assets utilization

Total manufacturing cost

Increased revenues

Increased profitability

Return on investment

Internal business process perspective

Innovative and qualitative products

Reduce product cycle

timeIncreaseoperational efficiency

Machine productivity

Desgining new products

Best IT services and Tech support

Learning and Growth Perspectives

Employee competencies

Improve employee's skills and

knowledge through organizing a

training programe

Employee turnover

Employee retention

Emplyee's safety measures

Employee satisfaction

Thus, on the basis of above information, it has became clear that ITS need to reduce

customer waiting time through timely reducing product cycle time. Another, introducing new

products, increase operational efficiency, machine productivity and innovative products helps

to satisfy consumer need and attract new customer also with high retention rate. Furthermore,

investment in training and development program will assist to increase worker's skill and

their productivity results in high employee turnover, retention and satisfaction. All this

factors will lead to drive success in terms of growth in revenues and profitability as well.

Henceforth, it can be said that constructed BSC will help Group Managing Director to

achieve high growth in future period.

TASK 3

Recommendation to ITS's Board whether they should recruit another accountant in their team

or not

Vision

and

Mission

Accounting is the major part of all the business functions and Accountant plays an

significant role in it. With reference to Integrated Technology Services (UK) Ltd, there are

following benefits to recruit additional accountant in company, listed below:

ITS need to maintain proper records of all the financial and operational affairs in an

appropriate way. Accountant is the person who has duty to keep detailed records of

each and every accounting transaction (Keršulienė and Turskis, 2014). If, it does not

happen that outsourcing may impose more cost than hiring a new accountant. In

relation to ITS, if present accountant does not fulfilling his duty efficiently and does

not maintaining adequate records of all the business affairs than it must be

recommended that ITS should recruit another accountant in the business.

If ITS hire another accountant with the existed ones than the business is freely to set

the tasks which he need to be perform. However, in case of finding any mistakes in

the accounting statements, than ITS has to take outsourcing services which may

impose greater cost with a high package. However, it might be possible that ITS can

not bear this cost henceforth, it will be more suitable to appoint new accountant in

ITS.

An outside accountants will have other clients also with ITS. This in turn, ITS's

sensitive information can be shared with the others and create adverse impact on the

business. Therefore, through hiring a new accountant, ITS does not need to get

external accountant services and ensure confidentiality of the information.

Through recruiting other accountant, ITS can choose the way that how work will be

done in the business. However, in case of appointing external accountants, his

working practices may be unfit for ITS (Mosher and Rudebeck, 2015). Thus, it is also

the benefits of hiring new accountant with the existed ones.

Appointing another accountant helps to get correct and authentic results of business

performance. It is because accountant will prepare all the financial statement in an

appropriate manner through combining all the operational functions. This in turn,

performance can be determined correctly.

Proper accounting of all the transactions will lead to reduce loss of embezzlement. It

is because in most of the organization, workers use business property and cash for

their own purpose and contribute to increase business cost (Barbera and Hasso, 2013).

significant role in it. With reference to Integrated Technology Services (UK) Ltd, there are

following benefits to recruit additional accountant in company, listed below:

ITS need to maintain proper records of all the financial and operational affairs in an

appropriate way. Accountant is the person who has duty to keep detailed records of

each and every accounting transaction (Keršulienė and Turskis, 2014). If, it does not

happen that outsourcing may impose more cost than hiring a new accountant. In

relation to ITS, if present accountant does not fulfilling his duty efficiently and does

not maintaining adequate records of all the business affairs than it must be

recommended that ITS should recruit another accountant in the business.

If ITS hire another accountant with the existed ones than the business is freely to set

the tasks which he need to be perform. However, in case of finding any mistakes in

the accounting statements, than ITS has to take outsourcing services which may

impose greater cost with a high package. However, it might be possible that ITS can

not bear this cost henceforth, it will be more suitable to appoint new accountant in

ITS.

An outside accountants will have other clients also with ITS. This in turn, ITS's

sensitive information can be shared with the others and create adverse impact on the

business. Therefore, through hiring a new accountant, ITS does not need to get

external accountant services and ensure confidentiality of the information.

Through recruiting other accountant, ITS can choose the way that how work will be

done in the business. However, in case of appointing external accountants, his

working practices may be unfit for ITS (Mosher and Rudebeck, 2015). Thus, it is also

the benefits of hiring new accountant with the existed ones.

Appointing another accountant helps to get correct and authentic results of business

performance. It is because accountant will prepare all the financial statement in an

appropriate manner through combining all the operational functions. This in turn,

performance can be determined correctly.

Proper accounting of all the transactions will lead to reduce loss of embezzlement. It

is because in most of the organization, workers use business property and cash for

their own purpose and contribute to increase business cost (Barbera and Hasso, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, good financial reporting will assure that business assets and resources are

using for business purpose only resulted in lower cost and high profitability.

It is a way of in-house accounting services rather than taking services of external

accountants. Therefore, it will lead to reduce need of hiring outsider accountant for

many purpose such as for the preparation of tax return.

In case, when all the transactions are recorded appropriately, than bank reconciliation

statement can be prepared easily. Otherwise, it is very difficult task to determine the

difference between the cash book and bank's pass book. Moreover, incorrect financial

statement will lead to analyse performance incorrectly and take harmful decisions

(Cooper and Dart, 2013). However. If financial statements are prepared accurately

than managers can analyse performance correctly and take qualitative decisions as

well.

Hence, it became clear that ITS should recruit new accountant in the organization.

TASK 4

Utilising target costing at ITS UK and review how 20% gross margin is not enough to

achieve the 6% rate of required net margin

Target costing: It is a pricing method and cost management technique used by

companies to manage their products cost. Target costing is a system in which ITS can pre-

plan for the product cost so as to achieve desired profit margin (Omar and et.al., 2015).

ITS can use this costing method in their business to manage cost of their products and

services. At the primary stage, designing team will conduct research to identify the features

that are demanding by the consumers. There after, they will forecast the product cost which

will be incur in future period. After that, engineering and procurement team will design the

product to meet set target so that ITS will be highly able to earn desired profit percentage

(Baumöl and et.al., 2015). It will provide huge assistance to ITS to maintain its competitive

strength. It is because in the fierce level of competition, only the organization who are

producing their products at lower cost can survive effectively. Reduction in product cost will

contribute to get high profitability and vice versa. Thus, it can be said that ITS can use target

costing to reduce overall product cost over its entire production cycle such as production,

engineering and research and design.

Reasons why 20% Gross margin is not enough to get 6% Net margin

using for business purpose only resulted in lower cost and high profitability.

It is a way of in-house accounting services rather than taking services of external

accountants. Therefore, it will lead to reduce need of hiring outsider accountant for

many purpose such as for the preparation of tax return.

In case, when all the transactions are recorded appropriately, than bank reconciliation

statement can be prepared easily. Otherwise, it is very difficult task to determine the

difference between the cash book and bank's pass book. Moreover, incorrect financial

statement will lead to analyse performance incorrectly and take harmful decisions

(Cooper and Dart, 2013). However. If financial statements are prepared accurately

than managers can analyse performance correctly and take qualitative decisions as

well.

Hence, it became clear that ITS should recruit new accountant in the organization.

TASK 4

Utilising target costing at ITS UK and review how 20% gross margin is not enough to

achieve the 6% rate of required net margin

Target costing: It is a pricing method and cost management technique used by

companies to manage their products cost. Target costing is a system in which ITS can pre-

plan for the product cost so as to achieve desired profit margin (Omar and et.al., 2015).

ITS can use this costing method in their business to manage cost of their products and

services. At the primary stage, designing team will conduct research to identify the features

that are demanding by the consumers. There after, they will forecast the product cost which

will be incur in future period. After that, engineering and procurement team will design the

product to meet set target so that ITS will be highly able to earn desired profit percentage

(Baumöl and et.al., 2015). It will provide huge assistance to ITS to maintain its competitive

strength. It is because in the fierce level of competition, only the organization who are

producing their products at lower cost can survive effectively. Reduction in product cost will

contribute to get high profitability and vice versa. Thus, it can be said that ITS can use target

costing to reduce overall product cost over its entire production cycle such as production,

engineering and research and design.

Reasons why 20% Gross margin is not enough to get 6% Net margin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

High administration expenditures such as worker's salary, high number of workers,

postage, office rent, building insurance, printing and stationery and so on.

High selling and distribution expenses also will lead to increase operational

expenditures and lowering the net margin as well.

Excessive uses of debt funds also will lead to impose greater financial cost in terms of

regular interest charges results in declining net profitability (Avenir, n.d).

High rate of income tax is also the another reason for lowering net margin. It is

because increasing tax rate will impose high tax obligations resulte4d in lower profits

and vice versa.

TASK 5

Review of the use of Integrated Technological Service share scheme whether it helps to

motivate employees to work towards achieving the goals or not

Employee stock option scheme (ESOS) is the option that ITS granted to its employees

as part of their remuneration package. It is a benefit plan in which some proportion of

business stock is transferred to their employees. In other words, it makes employees owners

of stock in ITS. ITS using this option plan in their share scheme to reward and retain their

workforce in the business (Chang and et.al., 2015). This plan is highly suitable in IT

companies in which workers are the essential part of the organization. As already said earlier,

ITS is a IT based company henceforth, manpower is the main assets in the business. It is

extensively used scheme to rewarding the employees so that efficient and able workforce can

not be retained in the business. Thus, the tool is greatly helps to motivate ITS staff to put their

best efforts in their work (Barth, Hodder and Stubben, 2013). This in turn, ITS can enjoy

success of high employee turnover through retaining its highly talented employees who will

provide best services to the customers. It is because by having some ownership in the

business, employee will think that company is giving in return for their efforts so that they

will be highly motivated and perform better (Long and Musibau, 2013). It will ultimately lead

to enhance employee satisfaction and ITS performance as well.

Another share scheme plan is bonus shares scheme in which ITS will allot its share

free of cost. In this plan, at the time when ITS have large amount of profits than it can

distribute some of the profits as bonus shares rather than cash dividends. In context to ITS,

when company will issue bonus shares to its employees that having ownership in business

equity than employee will be highly motivated. It is because employees does not need to

postage, office rent, building insurance, printing and stationery and so on.

High selling and distribution expenses also will lead to increase operational

expenditures and lowering the net margin as well.

Excessive uses of debt funds also will lead to impose greater financial cost in terms of

regular interest charges results in declining net profitability (Avenir, n.d).

High rate of income tax is also the another reason for lowering net margin. It is

because increasing tax rate will impose high tax obligations resulte4d in lower profits

and vice versa.

TASK 5

Review of the use of Integrated Technological Service share scheme whether it helps to

motivate employees to work towards achieving the goals or not

Employee stock option scheme (ESOS) is the option that ITS granted to its employees

as part of their remuneration package. It is a benefit plan in which some proportion of

business stock is transferred to their employees. In other words, it makes employees owners

of stock in ITS. ITS using this option plan in their share scheme to reward and retain their

workforce in the business (Chang and et.al., 2015). This plan is highly suitable in IT

companies in which workers are the essential part of the organization. As already said earlier,

ITS is a IT based company henceforth, manpower is the main assets in the business. It is

extensively used scheme to rewarding the employees so that efficient and able workforce can

not be retained in the business. Thus, the tool is greatly helps to motivate ITS staff to put their

best efforts in their work (Barth, Hodder and Stubben, 2013). This in turn, ITS can enjoy

success of high employee turnover through retaining its highly talented employees who will

provide best services to the customers. It is because by having some ownership in the

business, employee will think that company is giving in return for their efforts so that they

will be highly motivated and perform better (Long and Musibau, 2013). It will ultimately lead

to enhance employee satisfaction and ITS performance as well.

Another share scheme plan is bonus shares scheme in which ITS will allot its share

free of cost. In this plan, at the time when ITS have large amount of profits than it can

distribute some of the profits as bonus shares rather than cash dividends. In context to ITS,

when company will issue bonus shares to its employees that having ownership in business

equity than employee will be highly motivated. It is because employees does not need to

make any payment for the receipts of bonus shares (Venkataraman and Kumar, 2015).

Moreover, they will receive dividend and earnings on their bonus shares. It will lead to

enhance their profits in turn, employee will believe that their performance are appreciating by

ITS. This in turn, workers will be highly motivated and motivated staff perform much better

than unmotivated worker. Henceforth, ITS can get services of efficient., able and skilled

workforce and attain high success in future period.

CONCLUSION

On the basis of above information, it can be concluded that BSC is a strategic tool that

can be use by ITS to analyse its financial and non-financial performance. Under the NFPI,

designed BSC will assist ITS to evaluate customer satisfaction, employee satisfaction, their

skills, workers turnover, customer retention, market share, production cycle time, new

product development and so on. On the other hand, its financial perspective will provide

assistance to evaluate ITS's revenues, cost and business profits. Thus, the overall performance

evaluation will help ITS management to take some strategic decision to improve future

performance. Along with this, the report advised that ITS should recruit new accountant in

the business due to huge benefits. Further, target costing is an effective method that can be

used by ITS to reduce overall product cost and get high profits. In addition to it, ESOS and

bonus plan are share schemes that motivate ITS's workforce so that company can retain their

talented pool and achieve greater success.

Moreover, they will receive dividend and earnings on their bonus shares. It will lead to

enhance their profits in turn, employee will believe that their performance are appreciating by

ITS. This in turn, workers will be highly motivated and motivated staff perform much better

than unmotivated worker. Henceforth, ITS can get services of efficient., able and skilled

workforce and attain high success in future period.

CONCLUSION

On the basis of above information, it can be concluded that BSC is a strategic tool that

can be use by ITS to analyse its financial and non-financial performance. Under the NFPI,

designed BSC will assist ITS to evaluate customer satisfaction, employee satisfaction, their

skills, workers turnover, customer retention, market share, production cycle time, new

product development and so on. On the other hand, its financial perspective will provide

assistance to evaluate ITS's revenues, cost and business profits. Thus, the overall performance

evaluation will help ITS management to take some strategic decision to improve future

performance. Along with this, the report advised that ITS should recruit new accountant in

the business due to huge benefits. Further, target costing is an effective method that can be

used by ITS to reduce overall product cost and get high profits. In addition to it, ESOS and

bonus plan are share schemes that motivate ITS's workforce so that company can retain their

talented pool and achieve greater success.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.