Why Companies Disclose Intellectual Capital in Corporate Reports

VerifiedAdded on 2022/12/06

|10

|2290

|270

Report

AI Summary

This report provides a comprehensive analysis of intellectual capital (IC) disclosure in corporate annual reports. It explores the components of IC, including human, structural, and relational capital, and examines why companies choose to disclose this information. The report highlights the shift from tangible to intangible assets, the role of IC in a knowledge economy, and the importance of managing "artistic" properties to increase shareholder equity. It discusses the challenges in measuring and reporting IC, including information asymmetry and the lack of standardized accounting practices. The report also examines the impact of IC disclosure on market value, company ratings, and investor confidence. It concludes that enhanced IC disclosure is associated with a lower cost of capital and better market participation, emphasizing the importance of IC for policymakers and regulators. The report draws on various journal articles and research to support its findings.

Intellectual

capital

capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Why would companies choose to disclose Intellectual Capital information in the narrative

sections of corporate annual reports?..............................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Why would companies choose to disclose Intellectual Capital information in the narrative

sections of corporate annual reports?..............................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

journal articles

Why would companies choose to disclose Intellectual Capital information in

the narrative sections of corporate annual reports? Buenechea-Elberdin,

2017

Why would companies choose to disclose Intellectual Capital information in

the narrative sections of corporate annual reports? Buenechea-Elberdin,

2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Intellectual capital

Intellectual capital - Intellectual capital is considered as the most important capital element

which is present in a business to facilitate its operations. The intangible and tangible

intellectual capital which is present in a business is helpful in achievement of various

objectives and goals of an organisation. The human, structure and relational capital are one

of the most important source of capital which is required to run as well as to develop a

business in a precise manner.

Keywords: word; intellectual property, economics, business

Subject classification codes: Economics Hickman, L.E., 2020. Information

asymmetry in CSR reporting: publicly-traded versus privately-held firms.

Sustainability Accounting, Management and Policy Journal.

Jamil, A., Ghazali, N.A.M. and Nelson, S.P., 2020. The influence of corporate

governance structure on sustainability reporting in Malaysia. Social Responsibility

Journal.

Manes‐Rossi, F., Nicolò, G. and Argento, D., 2020. Non-financial reporting formats in

public sector organizations: a structured literature review. Journal of Public Budgeting,

Accounting & Financial Management.

Introduction

As stated by (Buenechea-Elberdin, 2017), human, structural and relational capitals are

considered to be one of the major parts of intangible capital. With the rapid increase in

information markets, the planet is rapidly transitioning from a "economic" to a "knowledge"

economy, and the country's economy has drawn the interest of the entire world. The role of

information management, intellectual capital, and creativity in economic growth is bolstered by

the emergence of the digital economy. Learning and command of IC have become "primary"

Intellectual capital - Intellectual capital is considered as the most important capital element

which is present in a business to facilitate its operations. The intangible and tangible

intellectual capital which is present in a business is helpful in achievement of various

objectives and goals of an organisation. The human, structure and relational capital are one

of the most important source of capital which is required to run as well as to develop a

business in a precise manner.

Keywords: word; intellectual property, economics, business

Subject classification codes: Economics Hickman, L.E., 2020. Information

asymmetry in CSR reporting: publicly-traded versus privately-held firms.

Sustainability Accounting, Management and Policy Journal.

Jamil, A., Ghazali, N.A.M. and Nelson, S.P., 2020. The influence of corporate

governance structure on sustainability reporting in Malaysia. Social Responsibility

Journal.

Manes‐Rossi, F., Nicolò, G. and Argento, D., 2020. Non-financial reporting formats in

public sector organizations: a structured literature review. Journal of Public Budgeting,

Accounting & Financial Management.

Introduction

As stated by (Buenechea-Elberdin, 2017), human, structural and relational capitals are

considered to be one of the major parts of intangible capital. With the rapid increase in

information markets, the planet is rapidly transitioning from a "economic" to a "knowledge"

economy, and the country's economy has drawn the interest of the entire world. The role of

information management, intellectual capital, and creativity in economic growth is bolstered by

the emergence of the digital economy. Learning and command of IC have become "primary"

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

success drivers in international competitiveness in today's innovation-driven environment.

Intellectual Capital (IC) components are rapidly determining and driving business conditions in

the twenty-first century. According to (Cerbone, and Maroun, 2020)“ In the era of information

and intelligence, successful use of IC is the most important element that decides the performance

of a business,” Survilaite3 recently said. Companies have moved their emphasis from

investments in real assets to acquisitions in intangible assets, as the conventional viewpoint has

changed. Human capital, institutional capital, and consumer capital are all called components of

IC.” Intangible properties (or IC) must be measured and recorded in a systematic and reliable

manner. Human capital plays an important role in a business by maximising production quality

and satisfying customers.

According to the views of (Ginesti, 2018), structural and relational capital are very relevant

because they have a direct and substantial impact on the stock valuation of the company.6 As a

result, accounting standards should be concerned with this immediately. The use of IC data in

corporate financial statements will “result in an accounting records that more objectively

represents the industry's worth, and shows all related assets from which the company plans to

derive profits in the coming few years,” according to the authors. According to various figures,

“abstract” properties actually account for 60-75 percent of value proposition on aggregate. For

this reason, For example, Lev8 analyzed the investment patterns of 1929 and 1995 and found

that "in 1929, nearly 70% of U.S. firms' investment went into tangible assets (TA) and 30percent

of the total went into intangible resources." In 1995, however, the pattern was corrected. As per

the views of (Gangi, Daniele, and Varrone, 2020), it was discovered that a large portion of

investment goes into intangibles like design and technology, IT tech, schooling and key

competencies, and the internet.” Intangible assets (or IC) are “company accomplices and

Intellectual Capital (IC) components are rapidly determining and driving business conditions in

the twenty-first century. According to (Cerbone, and Maroun, 2020)“ In the era of information

and intelligence, successful use of IC is the most important element that decides the performance

of a business,” Survilaite3 recently said. Companies have moved their emphasis from

investments in real assets to acquisitions in intangible assets, as the conventional viewpoint has

changed. Human capital, institutional capital, and consumer capital are all called components of

IC.” Intangible properties (or IC) must be measured and recorded in a systematic and reliable

manner. Human capital plays an important role in a business by maximising production quality

and satisfying customers.

According to the views of (Ginesti, 2018), structural and relational capital are very relevant

because they have a direct and substantial impact on the stock valuation of the company.6 As a

result, accounting standards should be concerned with this immediately. The use of IC data in

corporate financial statements will “result in an accounting records that more objectively

represents the industry's worth, and shows all related assets from which the company plans to

derive profits in the coming few years,” according to the authors. According to various figures,

“abstract” properties actually account for 60-75 percent of value proposition on aggregate. For

this reason, For example, Lev8 analyzed the investment patterns of 1929 and 1995 and found

that "in 1929, nearly 70% of U.S. firms' investment went into tangible assets (TA) and 30percent

of the total went into intangible resources." In 1995, however, the pattern was corrected. As per

the views of (Gangi, Daniele, and Varrone, 2020), it was discovered that a large portion of

investment goes into intangibles like design and technology, IT tech, schooling and key

competencies, and the internet.” Intangible assets (or IC) are “company accomplices and

suppliers of value, as they convert capital into value.” output of added value.” As a result,

corporations are devoting a lot of time and money to managing their "artistic" properties in order

to increase shareholder equity. Despite the awareness and competition for IC data, prior literature

shows that there is a pervasive and substantial inconsistency in the ‘quantity' and ‘quality' of

statistics provided by businesses on this critical resource. Present economic and market indices

are tracking a decreasing proportion of the global economy, resulting in a deficit and

inefficiency. The growing knowledge "asymmetry" between "educated" and "uninformed"

investors is due to inconsistency in the reporting of IC-related data. This creates an ideal

environment for knowledgeable buyers to extract higher abnormal returns. 11 As a result, IC is

gradually being recognised as playing a larger role in achieving and retaining "competitive"

advantage and shareholder "benefit." This obviously necessitates a re-evaluation of corporate

standards, data reporting, and decision-making processes.

Logical analysis

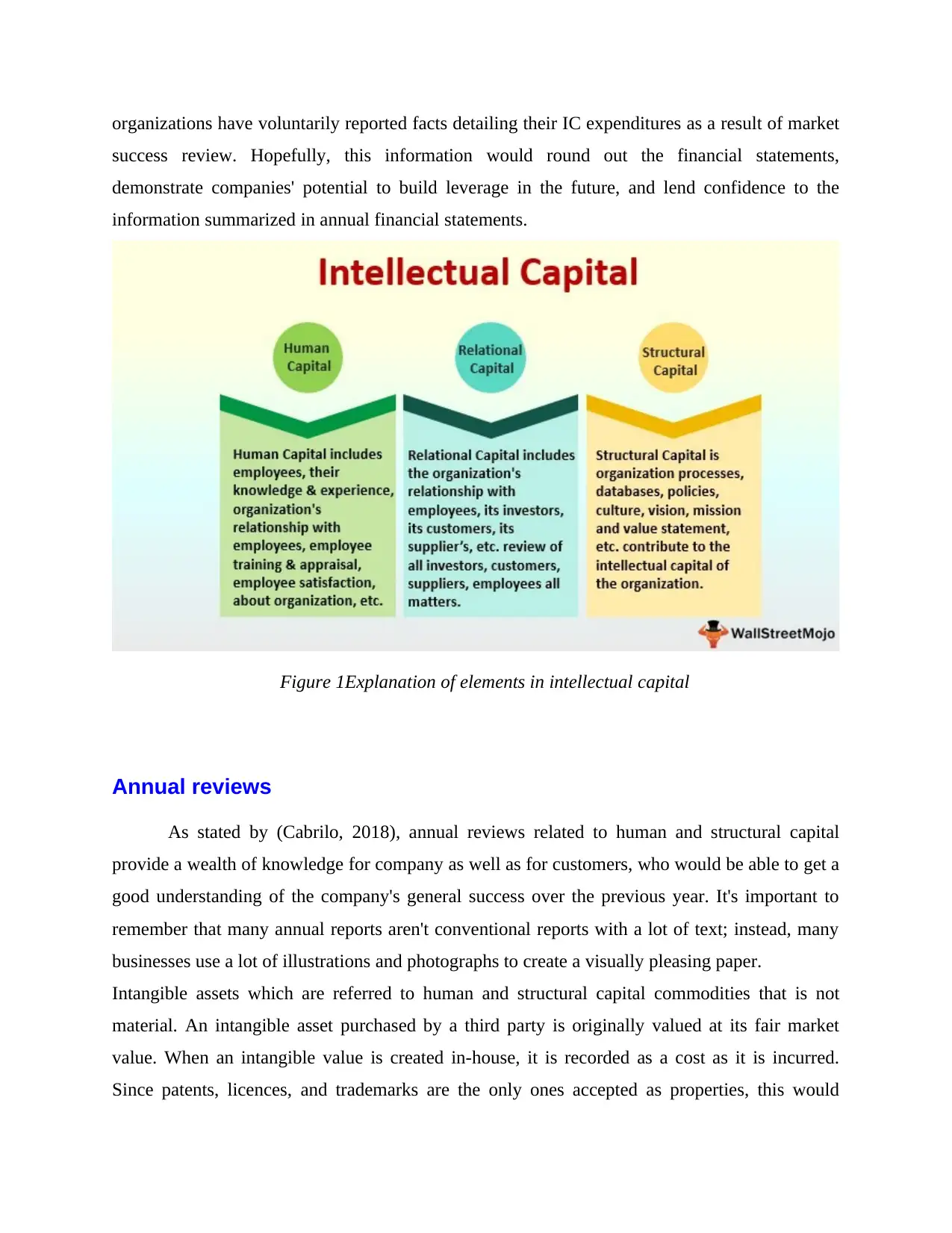

According to (Hickman, 2020), Monitoring and monitoring are also in its infancy. Human capital

such as accountants, company executives, and policymakers are all grappling with the

problem. Concepts and implementation in depth are the one would imagine, there are several

different definitions of IC. “It has become common to conclude that a company's IC is the

amount of its human capital (talent), institutional capital (intellectual property, methodologies,

applications, records, and other information artifacts), and consumer capital. In reality, Sveiby14

was the first to classify IC into three categories of intangibles: human resources, structural

capital, and strategic capital. Capital and Customer capital—a classification that was later

updated and expanded to include relational capital in place of customer capital. In Box-1, you'll

find some IC cases. The diagram is just a general representation of the components of IC, since

the elements mix and communicate with one another, as well as conventional capital elements

(physical objects and monetary elements), in forms that are particular to each company to

generate value. Investors and emerging global economies are putting a lot of emphasis on the

quality of knowledge and data. As stated by, (Jamil, Ghazali, and Nelson, 2020), Any

corporations are devoting a lot of time and money to managing their "artistic" properties in order

to increase shareholder equity. Despite the awareness and competition for IC data, prior literature

shows that there is a pervasive and substantial inconsistency in the ‘quantity' and ‘quality' of

statistics provided by businesses on this critical resource. Present economic and market indices

are tracking a decreasing proportion of the global economy, resulting in a deficit and

inefficiency. The growing knowledge "asymmetry" between "educated" and "uninformed"

investors is due to inconsistency in the reporting of IC-related data. This creates an ideal

environment for knowledgeable buyers to extract higher abnormal returns. 11 As a result, IC is

gradually being recognised as playing a larger role in achieving and retaining "competitive"

advantage and shareholder "benefit." This obviously necessitates a re-evaluation of corporate

standards, data reporting, and decision-making processes.

Logical analysis

According to (Hickman, 2020), Monitoring and monitoring are also in its infancy. Human capital

such as accountants, company executives, and policymakers are all grappling with the

problem. Concepts and implementation in depth are the one would imagine, there are several

different definitions of IC. “It has become common to conclude that a company's IC is the

amount of its human capital (talent), institutional capital (intellectual property, methodologies,

applications, records, and other information artifacts), and consumer capital. In reality, Sveiby14

was the first to classify IC into three categories of intangibles: human resources, structural

capital, and strategic capital. Capital and Customer capital—a classification that was later

updated and expanded to include relational capital in place of customer capital. In Box-1, you'll

find some IC cases. The diagram is just a general representation of the components of IC, since

the elements mix and communicate with one another, as well as conventional capital elements

(physical objects and monetary elements), in forms that are particular to each company to

generate value. Investors and emerging global economies are putting a lot of emphasis on the

quality of knowledge and data. As stated by, (Jamil, Ghazali, and Nelson, 2020), Any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organizations have voluntarily reported facts detailing their IC expenditures as a result of market

success review. Hopefully, this information would round out the financial statements,

demonstrate companies' potential to build leverage in the future, and lend confidence to the

information summarized in annual financial statements.

Figure 1Explanation of elements in intellectual capital

Annual reviews

As stated by (Cabrilo, 2018), annual reviews related to human and structural capital

provide a wealth of knowledge for company as well as for customers, who would be able to get a

good understanding of the company's general success over the previous year. It's important to

remember that many annual reports aren't conventional reports with a lot of text; instead, many

businesses use a lot of illustrations and photographs to create a visually pleasing paper.

Intangible assets which are referred to human and structural capital commodities that is not

material. An intangible asset purchased by a third party is originally valued at its fair market

value. When an intangible value is created in-house, it is recorded as a cost as it is incurred.

Since patents, licences, and trademarks are the only ones accepted as properties, this would

success review. Hopefully, this information would round out the financial statements,

demonstrate companies' potential to build leverage in the future, and lend confidence to the

information summarized in annual financial statements.

Figure 1Explanation of elements in intellectual capital

Annual reviews

As stated by (Cabrilo, 2018), annual reviews related to human and structural capital

provide a wealth of knowledge for company as well as for customers, who would be able to get a

good understanding of the company's general success over the previous year. It's important to

remember that many annual reports aren't conventional reports with a lot of text; instead, many

businesses use a lot of illustrations and photographs to create a visually pleasing paper.

Intangible assets which are referred to human and structural capital commodities that is not

material. An intangible asset purchased by a third party is originally valued at its fair market

value. When an intangible value is created in-house, it is recorded as a cost as it is incurred.

Since patents, licences, and trademarks are the only ones accepted as properties, this would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

restrict the acknowledgment of most IC to what is bought from outside the company. Human

capital and most of the structural capital, such as internally developed software, trademarks, and

brazenness, are not valued according to generally agreed accounting standards. The valuation of

intellectual resources, as well as much of the systemic importance, is not recognized by generally

agreed accounting standards. Internally produced software, trademarks, and labels are examples

of money. The FASB used the four identification requirements contained in FASB Concept

Statement No. 5.22 to create the Statement. These conditions are: (1) the item satisfies the

description of an asset, (2) the item can be measured with adequate accuracy, (3) the information

can influence actions, and (4) the information represents what it appears to represent, is

verifiable, and impartial.

According to (Allameh, 2018), the International Accounting Standards Committee and its

national counterparts face a difficult task in establishing accounting standards. Reporting

requirements for IC 42. So far, the measuring references have become so firm-specific, and no

series of metrics might expect to be broad enough to cover the needs of a wide range of

international and business contexts. At this stage, auditing any of the various systems will be

futile. According to (Paternostro, 2020), when ranking firms, the use of IC should be given due

consideration for optimum utilisation of resources. Since IC reporting has an impact on share

pricing, it can result in a rise in company ratings as a result of increased market capitalization. In

the short term, voluntary monitoring is the only option. In the short term, voluntary monitoring is

the only option. It would be up to the demands of the financial markets in the long run. As told

by (Polizzi, and Scannella, 2020), whether investors and experts agree, Companies would have

no choice but to please their audience until they believe that IC reporting is useful in describing

market success. Meanwhile, a company should encourage the role of human and structural

capital in formation of several organisational objectives.

CONCLUSION

As per the above discussion, it is analysed that enhanced evidence capita information

disclosure is related to cost of capital. It suggests that investors have to find information which is

useful for providing value for firms. That is why improved intellectual capital disclosure is

beneficial for market participation. It enables in context of having relevant information present

for the firm. It provides help for minimising the cost available for private information. This type

of information is very important for policy makers. The reason behind this is it provides the

capital and most of the structural capital, such as internally developed software, trademarks, and

brazenness, are not valued according to generally agreed accounting standards. The valuation of

intellectual resources, as well as much of the systemic importance, is not recognized by generally

agreed accounting standards. Internally produced software, trademarks, and labels are examples

of money. The FASB used the four identification requirements contained in FASB Concept

Statement No. 5.22 to create the Statement. These conditions are: (1) the item satisfies the

description of an asset, (2) the item can be measured with adequate accuracy, (3) the information

can influence actions, and (4) the information represents what it appears to represent, is

verifiable, and impartial.

According to (Allameh, 2018), the International Accounting Standards Committee and its

national counterparts face a difficult task in establishing accounting standards. Reporting

requirements for IC 42. So far, the measuring references have become so firm-specific, and no

series of metrics might expect to be broad enough to cover the needs of a wide range of

international and business contexts. At this stage, auditing any of the various systems will be

futile. According to (Paternostro, 2020), when ranking firms, the use of IC should be given due

consideration for optimum utilisation of resources. Since IC reporting has an impact on share

pricing, it can result in a rise in company ratings as a result of increased market capitalization. In

the short term, voluntary monitoring is the only option. In the short term, voluntary monitoring is

the only option. It would be up to the demands of the financial markets in the long run. As told

by (Polizzi, and Scannella, 2020), whether investors and experts agree, Companies would have

no choice but to please their audience until they believe that IC reporting is useful in describing

market success. Meanwhile, a company should encourage the role of human and structural

capital in formation of several organisational objectives.

CONCLUSION

As per the above discussion, it is analysed that enhanced evidence capita information

disclosure is related to cost of capital. It suggests that investors have to find information which is

useful for providing value for firms. That is why improved intellectual capital disclosure is

beneficial for market participation. It enables in context of having relevant information present

for the firm. It provides help for minimising the cost available for private information. This type

of information is very important for policy makers. The reason behind this is it provides the

development of base for regulators. This provides evaluation of cost and benefit of potential

regulation associated with intellectual capital information. There are firms which uses cost of

capital in their capital investment decisions. The finance director perceived disclosure for

influencing cost of capital. As per the findings from above report, it is analysed that managers

can have insight for enhancing disclosure of intellectual capital information about their firms.

regulation associated with intellectual capital information. There are firms which uses cost of

capital in their capital investment decisions. The finance director perceived disclosure for

influencing cost of capital. As per the findings from above report, it is analysed that managers

can have insight for enhancing disclosure of intellectual capital information about their firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Cerbone, D. and Maroun, W., 2020. Materiality in an integrated reporting setting: Insights using

an institutional logics framework. The British Accounting Review, 52(3), p.100876.

Gangi, F., Daniele, L.M. and Varrone, N., 2020. How do corporate environmental policy and

corporate reputation affect risk‐adjusted financial performance?. Business Strategy and

the Environment, 29(5), pp.1975-1991.

Hickman, L.E., 2020. Information asymmetry in CSR reporting: publicly-traded versus

privately-held firms. Sustainability Accounting, Management and Policy Journal.

Jamil, A., Ghazali, N.A.M. and Nelson, S.P., 2020. The influence of corporate governance

structure on sustainability reporting in Malaysia. Social Responsibility Journal.

Manes‐Rossi, F., Nicolò, G. and Argento, D., 2020. Non-financial reporting formats in public

sector organizations: a structured literature review. Journal of Public Budgeting,

Accounting & Financial Management.

Paternostro, S., 2020. Integrated Reporting and Social Disclosure: True Love or Forced

Marriage? A Multidimensional Analysis of a Contested Concept. In Non-Financial

Disclosure and Integrated Reporting: Practices and Critical Issues. Emerald Publishing

Limited.

Polizzi, S. and Scannella, E., 2020. An empirical investigation into market risk disclosure: is

there room to improve for Italian banks?. Journal of Financial Regulation and

Compliance.

Allameh, S.M., 2018. Antecedents and consequences of intellectual capital. Journal of

Intellectual Capital.

Ginesti, G., Caldarelli, A. and Zampella, A., 2018. Exploring the impact of intellectual capital on

company reputation and performance. Journal of Intellectual Capital.

Cabrilo, S. and Dahms, S., 2018. How strategic knowledge management drives intellectual

capital to superior innovation and market performance. Journal of knowledge

management.

Buenechea-Elberdin, M., 2017. Structured literature review about intellectual capital and

innovation. Journal of Intellectual capital.

Books and Journals

Cerbone, D. and Maroun, W., 2020. Materiality in an integrated reporting setting: Insights using

an institutional logics framework. The British Accounting Review, 52(3), p.100876.

Gangi, F., Daniele, L.M. and Varrone, N., 2020. How do corporate environmental policy and

corporate reputation affect risk‐adjusted financial performance?. Business Strategy and

the Environment, 29(5), pp.1975-1991.

Hickman, L.E., 2020. Information asymmetry in CSR reporting: publicly-traded versus

privately-held firms. Sustainability Accounting, Management and Policy Journal.

Jamil, A., Ghazali, N.A.M. and Nelson, S.P., 2020. The influence of corporate governance

structure on sustainability reporting in Malaysia. Social Responsibility Journal.

Manes‐Rossi, F., Nicolò, G. and Argento, D., 2020. Non-financial reporting formats in public

sector organizations: a structured literature review. Journal of Public Budgeting,

Accounting & Financial Management.

Paternostro, S., 2020. Integrated Reporting and Social Disclosure: True Love or Forced

Marriage? A Multidimensional Analysis of a Contested Concept. In Non-Financial

Disclosure and Integrated Reporting: Practices and Critical Issues. Emerald Publishing

Limited.

Polizzi, S. and Scannella, E., 2020. An empirical investigation into market risk disclosure: is

there room to improve for Italian banks?. Journal of Financial Regulation and

Compliance.

Allameh, S.M., 2018. Antecedents and consequences of intellectual capital. Journal of

Intellectual Capital.

Ginesti, G., Caldarelli, A. and Zampella, A., 2018. Exploring the impact of intellectual capital on

company reputation and performance. Journal of Intellectual Capital.

Cabrilo, S. and Dahms, S., 2018. How strategic knowledge management drives intellectual

capital to superior innovation and market performance. Journal of knowledge

management.

Buenechea-Elberdin, M., 2017. Structured literature review about intellectual capital and

innovation. Journal of Intellectual capital.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.