Interactive Investor: Detailed Management Accounting Report Analysis

VerifiedAdded on 2021/02/21

|27

|5607

|326

Report

AI Summary

This report delves into the significance of management accounting within the context of Interactive Investor, an online business platform. It explores the essential requirements of a management accounting system, contrasting it with financial accounting and highlighting its evolution. The report examines various management accounting methods, including job costing, inventory management, and price optimization, illustrating their practical applications. It provides insights into cost calculation, the preparation of income statements, and the application of planning tools for budgeting and forecasting. Furthermore, the report addresses the identification of financial problems, financial governance, and the use of management accounting skills to develop effective strategies and systems. The analysis showcases how Interactive Investor utilizes these tools and techniques to enhance decision-making, improve efficiency, and achieve its organizational goals. The report covers topics like costing methods (absorption and marginal), fixed/variable costs, and pricing strategies, ultimately aiming to provide a comprehensive understanding of management accounting's role in business development.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................4

P1 Essential requirement of management accounting system................................................4

Management accounting.........................................................................................................4

Management accounting system.............................................................................................5

Evolution of management accounting....................................................................................5

Difference between the financial and management accounting.............................................5

P2 various method used for management accounting report..................................................6

Characteristics of good management accounting system.......................................................7

Need of the understandability of the management accounting report....................................8

Various management accounting reports...............................................................................9

LO 2.................................................................................................................................................9

P 3 Calculation of cost and preparation of income statements...............................................9

Definition of cost and cost analysis........................................................................................9

Explanation of cost- Volume Profit, flexible budgeting and cost variances........................10

Calculation of Absorption costing and Marginal Costing....................................................10

Fixed and Variable costs, Cost allocation............................................................................14

Normal and Standard Costing, activity- based costing and the role of costing in setting Price

..............................................................................................................................................14

LO3................................................................................................................................................15

P4 Use of Planning tools used in management accounting .................................................15

Application of planning tools in forecasting of budgets......................................................16

Pricing...................................................................................................................................18

LO 4...............................................................................................................................................19

P5 Identification of financial problems................................................................................19

Financial Governance...........................................................................................................21

Management accounting skills.............................................................................................21

Effective strategies and systems...........................................................................................22

CONCLUSION..............................................................................................................................22

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................4

P1 Essential requirement of management accounting system................................................4

Management accounting.........................................................................................................4

Management accounting system.............................................................................................5

Evolution of management accounting....................................................................................5

Difference between the financial and management accounting.............................................5

P2 various method used for management accounting report..................................................6

Characteristics of good management accounting system.......................................................7

Need of the understandability of the management accounting report....................................8

Various management accounting reports...............................................................................9

LO 2.................................................................................................................................................9

P 3 Calculation of cost and preparation of income statements...............................................9

Definition of cost and cost analysis........................................................................................9

Explanation of cost- Volume Profit, flexible budgeting and cost variances........................10

Calculation of Absorption costing and Marginal Costing....................................................10

Fixed and Variable costs, Cost allocation............................................................................14

Normal and Standard Costing, activity- based costing and the role of costing in setting Price

..............................................................................................................................................14

LO3................................................................................................................................................15

P4 Use of Planning tools used in management accounting .................................................15

Application of planning tools in forecasting of budgets......................................................16

Pricing...................................................................................................................................18

LO 4...............................................................................................................................................19

P5 Identification of financial problems................................................................................19

Financial Governance...........................................................................................................21

Management accounting skills.............................................................................................21

Effective strategies and systems...........................................................................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of using the various data to generate information

for further use of different management levels like top management, middle management and

lower level management to improve the performance of the organization by taking the effective

decisions. Interactive investor is a medium size company which operates their business via

online. They provide platform to the retail companies to operate their business from their

websites and portal and get the financial information and investment option on their portal. The

report highlights the importance of management accounting systems within the organization with

different management functions and evolution of management accounting. This report

demonstrates the difference between the management accounting and financial accounting. The

report explains the different types of management accounting systems like job costing, inventory

management and cost accounting. It also explains the functioning of accounting tools in the

organization and the various uses of accounting tools. Management accounting techniques help

to provide the information by using the different costing method like absorption and marginal

cost to make decisions for the company and provide a suitable method to minimize the cost of

the production.

The report explains the different planning tools and their importance in the company to

set the budget and calculating the variances to improve the performance of the different

department by analysing their functioning. It also explains the different pricing strategies to set

the price to maximize their profit by capturing the greater market share and increasing the profit

margin like penetration pricing, skimming pricing etc. The report highlights the various financial

problem like increasing the production cost, management cost etc. and adopt various method to

resolve the financial problems. They use controlling tools to evaluate the variances in the

expected and actual budget like key performance indicators, budgetary control, Benchmarking

etc.

LO 1

P1 Essential requirement of management accounting system

Management accounting

Management accounting : Management accounting is the process to gather, sort,

analyse and process financial information in order to prepare reports to help the organisation to

4

Management accounting is the process of using the various data to generate information

for further use of different management levels like top management, middle management and

lower level management to improve the performance of the organization by taking the effective

decisions. Interactive investor is a medium size company which operates their business via

online. They provide platform to the retail companies to operate their business from their

websites and portal and get the financial information and investment option on their portal. The

report highlights the importance of management accounting systems within the organization with

different management functions and evolution of management accounting. This report

demonstrates the difference between the management accounting and financial accounting. The

report explains the different types of management accounting systems like job costing, inventory

management and cost accounting. It also explains the functioning of accounting tools in the

organization and the various uses of accounting tools. Management accounting techniques help

to provide the information by using the different costing method like absorption and marginal

cost to make decisions for the company and provide a suitable method to minimize the cost of

the production.

The report explains the different planning tools and their importance in the company to

set the budget and calculating the variances to improve the performance of the different

department by analysing their functioning. It also explains the different pricing strategies to set

the price to maximize their profit by capturing the greater market share and increasing the profit

margin like penetration pricing, skimming pricing etc. The report highlights the various financial

problem like increasing the production cost, management cost etc. and adopt various method to

resolve the financial problems. They use controlling tools to evaluate the variances in the

expected and actual budget like key performance indicators, budgetary control, Benchmarking

etc.

LO 1

P1 Essential requirement of management accounting system

Management accounting

Management accounting : Management accounting is the process to gather, sort,

analyse and process financial information in order to prepare reports to help the organisation to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

take the effective decision about the usage of resources and funds to get the better result. It also

helps to accomplish the organisational goal. Management accounting support the decisions of top

management and provide them various data and information to explore their knowledge and

understand the financial position of the business (Otley, 2016). It is used to prepare the

accounting information to help managers for making policy, procedure and plan for achieving

the organization objective.

Management accounting system

Management accounting system: It is the process of using the internal financial

information and prepare reports presenting the data in useful manner to take the effective

decisions for the growth and development of the company. It provides the direction to run the

company more efficiently by analysing the various alternatives and variances.

Evolution of management accounting

The evolution of management accounting is improved due to the changes in technology,

government interference and the different policies. Before 1950 the focus of the accounting is

financial accounting and cost accounting to provide the financial data and maintain the profit of

the organization but after 1950 the emergence of management accounting is start. The role of

management accounting is increasing nowadays. People are more concern about the management

accounting to use the data for taking decisions and also improving non-financial performance.

Now the role of management accounting is to communicate the information within the

organization to connect the employees toward the common organization goal and improve their

performance to get the goal and objective.

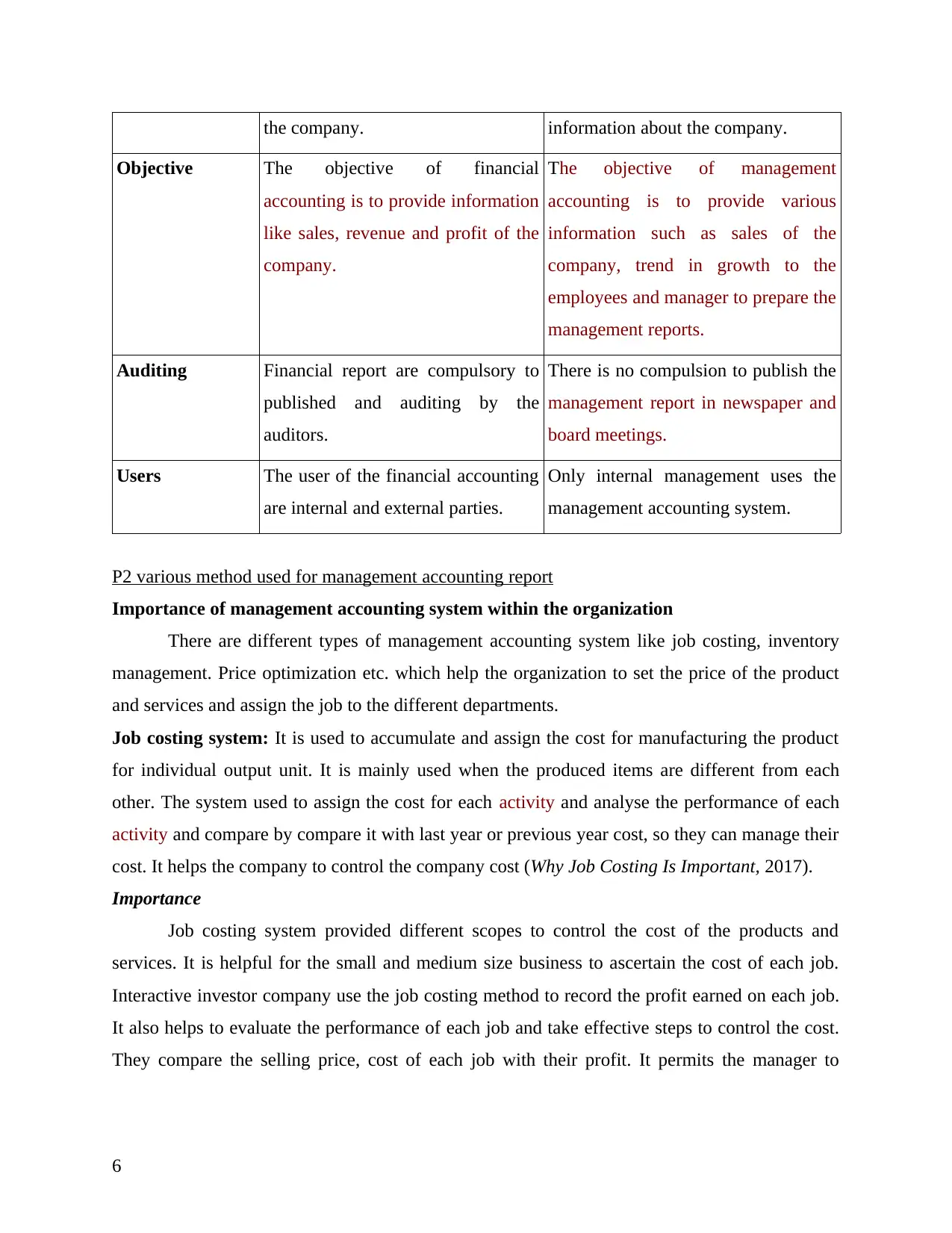

Difference between the financial and management accounting

Basis Financial accounting Management Accounting

Meaning The aim of financial accounting is to

concentrates on the financial

statement of the organization like

balance sheet, income statement and

cash flow statement.

Management accounting help the

managers to take the effective

decisions for the organization to

improve organization performance by

using these financial data.

Information Financial accounting only provides

the monetary information regarding

Management accounting provide the

monetary and non monetary

5

helps to accomplish the organisational goal. Management accounting support the decisions of top

management and provide them various data and information to explore their knowledge and

understand the financial position of the business (Otley, 2016). It is used to prepare the

accounting information to help managers for making policy, procedure and plan for achieving

the organization objective.

Management accounting system

Management accounting system: It is the process of using the internal financial

information and prepare reports presenting the data in useful manner to take the effective

decisions for the growth and development of the company. It provides the direction to run the

company more efficiently by analysing the various alternatives and variances.

Evolution of management accounting

The evolution of management accounting is improved due to the changes in technology,

government interference and the different policies. Before 1950 the focus of the accounting is

financial accounting and cost accounting to provide the financial data and maintain the profit of

the organization but after 1950 the emergence of management accounting is start. The role of

management accounting is increasing nowadays. People are more concern about the management

accounting to use the data for taking decisions and also improving non-financial performance.

Now the role of management accounting is to communicate the information within the

organization to connect the employees toward the common organization goal and improve their

performance to get the goal and objective.

Difference between the financial and management accounting

Basis Financial accounting Management Accounting

Meaning The aim of financial accounting is to

concentrates on the financial

statement of the organization like

balance sheet, income statement and

cash flow statement.

Management accounting help the

managers to take the effective

decisions for the organization to

improve organization performance by

using these financial data.

Information Financial accounting only provides

the monetary information regarding

Management accounting provide the

monetary and non monetary

5

the company. information about the company.

Objective The objective of financial

accounting is to provide information

like sales, revenue and profit of the

company.

The objective of management

accounting is to provide various

information such as sales of the

company, trend in growth to the

employees and manager to prepare the

management reports.

Auditing Financial report are compulsory to

published and auditing by the

auditors.

There is no compulsion to publish the

management report in newspaper and

board meetings.

Users The user of the financial accounting

are internal and external parties.

Only internal management uses the

management accounting system.

P2 various method used for management accounting report

Importance of management accounting system within the organization

There are different types of management accounting system like job costing, inventory

management. Price optimization etc. which help the organization to set the price of the product

and services and assign the job to the different departments.

Job costing system: It is used to accumulate and assign the cost for manufacturing the product

for individual output unit. It is mainly used when the produced items are different from each

other. The system used to assign the cost for each activity and analyse the performance of each

activity and compare by compare it with last year or previous year cost, so they can manage their

cost. It helps the company to control the company cost (Why Job Costing Is Important, 2017).

Importance

Job costing system provided different scopes to control the cost of the products and

services. It is helpful for the small and medium size business to ascertain the cost of each job.

Interactive investor company use the job costing method to record the profit earned on each job.

It also helps to evaluate the performance of each job and take effective steps to control the cost.

They compare the selling price, cost of each job with their profit. It permits the manager to

6

Objective The objective of financial

accounting is to provide information

like sales, revenue and profit of the

company.

The objective of management

accounting is to provide various

information such as sales of the

company, trend in growth to the

employees and manager to prepare the

management reports.

Auditing Financial report are compulsory to

published and auditing by the

auditors.

There is no compulsion to publish the

management report in newspaper and

board meetings.

Users The user of the financial accounting

are internal and external parties.

Only internal management uses the

management accounting system.

P2 various method used for management accounting report

Importance of management accounting system within the organization

There are different types of management accounting system like job costing, inventory

management. Price optimization etc. which help the organization to set the price of the product

and services and assign the job to the different departments.

Job costing system: It is used to accumulate and assign the cost for manufacturing the product

for individual output unit. It is mainly used when the produced items are different from each

other. The system used to assign the cost for each activity and analyse the performance of each

activity and compare by compare it with last year or previous year cost, so they can manage their

cost. It helps the company to control the company cost (Why Job Costing Is Important, 2017).

Importance

Job costing system provided different scopes to control the cost of the products and

services. It is helpful for the small and medium size business to ascertain the cost of each job.

Interactive investor company use the job costing method to record the profit earned on each job.

It also helps to evaluate the performance of each job and take effective steps to control the cost.

They compare the selling price, cost of each job with their profit. It permits the manager to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

calculate each job cost and profit and understand the performance and take decisions whether the

job is desirables for the future use or not.

Price optimization system: It helps the organization to determine behaviour of the customer

regarding the different amount and value of money offer to them for the different product and

services. They analyse the inventory level, cost of the product, operating cost and historical

prices for the estimating the price which best suited their product and help them to increase the

operating profit (Ferreira, Lee, and Simchi-Levi, 2015). By price optimization system a company

can evaluate their performance by analysing the buying behaviour of the customer.

Importance

Interactive investor use the price optimization system to influence the buying behaviour

of the customer by evaluating their buying pattern and taste and preferences. It influence the

organization to concentrates on the areas like profit margin. Sales conversions number etc. It also

supports the organization to generate the revenue of the company. It helps the interactive

investor company to reduce the manpower by automating the entire process. Interactive investor

mainly done their business via online so price optimization system add value in their functioning.

Through this method company can easily take the decisions regarding setting the price of t eh

product.

Inventory management system : It is a management software which was used by the

organization to check the inventory level, order quantity, sales and delivery of the goods. It helps

to reduce the maintenance cost of the inventory in the warehouses by regulating the inventory

level timely and make the order when they needed. It also helps them to fulfilling the demand of

the customer.

Importance

Inventory management system provides the better techniques to calculate the inventory

level via computerized system which reduces the role of manpower and help the organization to

regulate the inventory level and make order according the stock to manage the cost of

maintenance. Inventory system also help the organization to manage the sales and deliver the

product and services on time. Interactive investor company can manage the inventory level and

improve their performance by improving the delivery system.

7

job is desirables for the future use or not.

Price optimization system: It helps the organization to determine behaviour of the customer

regarding the different amount and value of money offer to them for the different product and

services. They analyse the inventory level, cost of the product, operating cost and historical

prices for the estimating the price which best suited their product and help them to increase the

operating profit (Ferreira, Lee, and Simchi-Levi, 2015). By price optimization system a company

can evaluate their performance by analysing the buying behaviour of the customer.

Importance

Interactive investor use the price optimization system to influence the buying behaviour

of the customer by evaluating their buying pattern and taste and preferences. It influence the

organization to concentrates on the areas like profit margin. Sales conversions number etc. It also

supports the organization to generate the revenue of the company. It helps the interactive

investor company to reduce the manpower by automating the entire process. Interactive investor

mainly done their business via online so price optimization system add value in their functioning.

Through this method company can easily take the decisions regarding setting the price of t eh

product.

Inventory management system : It is a management software which was used by the

organization to check the inventory level, order quantity, sales and delivery of the goods. It helps

to reduce the maintenance cost of the inventory in the warehouses by regulating the inventory

level timely and make the order when they needed. It also helps them to fulfilling the demand of

the customer.

Importance

Inventory management system provides the better techniques to calculate the inventory

level via computerized system which reduces the role of manpower and help the organization to

regulate the inventory level and make order according the stock to manage the cost of

maintenance. Inventory system also help the organization to manage the sales and deliver the

product and services on time. Interactive investor company can manage the inventory level and

improve their performance by improving the delivery system.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Characteristics of good management accounting system

Accuracy : It provides the accurate data regarding the performance of the organization

such as its total sales, revenue, cost, expenses etc. It provides accurate data to the Interactive

investor to measure its position in the market and take efficient measures to improve their

performance. The accuracy of the data shows the reliability of the organization.

Decision making : management accounting support the decisions of the organization by

presenting the data in different report such as balance sheet, cash flow etc. and help the manager

to evaluate the sale and profit of the interactive investor company. It also helps them to compare

the last year performance with the current year performance.

Improving efficiency: The role of management accounting is to contribute to make a

better use of resources the performance and efficiency of the firm by optimum utilization of

resource. They fix the target and goals for the different departments to accomplish the objective

of the organisation. The favourable variances are appreciated but in the case of adverse variance

they try to manage them by using the various tools like training and development program etc.

Techniques and concept : management accounting use the various techniques such ad

standard costing, budgetary control, cash flow, balance sheet, ratio analysis etc. to make t eh

information and accounting more useful (Zahller, 2017). Each technique used by the interactive

investor is for the special purpose like to present the data. Managing the organization or to take

the decisions.

Cause and effect relation: the role of financial accounting is to present the data in profit

and loss account of balance sheet but the role of management accounting is to present the cause

and effect relation of the data and their decisions. If the company suffer from the losses than the

role of management accounting is to find the reason behind the losses. The profit of the

organization is also analysed to check the accuracy of the process and data.

Forecasting : the role of management accounting is to take the decisions for the future

events on the current performance of the company. Interactive investor company forecast their

company sales and revenue by the past year performance and prepare budget according to it

forecast the expenses.

Need of the understandability of the management accounting report

The report of the management accounting should be in proper format so that it is easily

comprehensible, and functional to make decisions in better way and get the result quickly. The

8

Accuracy : It provides the accurate data regarding the performance of the organization

such as its total sales, revenue, cost, expenses etc. It provides accurate data to the Interactive

investor to measure its position in the market and take efficient measures to improve their

performance. The accuracy of the data shows the reliability of the organization.

Decision making : management accounting support the decisions of the organization by

presenting the data in different report such as balance sheet, cash flow etc. and help the manager

to evaluate the sale and profit of the interactive investor company. It also helps them to compare

the last year performance with the current year performance.

Improving efficiency: The role of management accounting is to contribute to make a

better use of resources the performance and efficiency of the firm by optimum utilization of

resource. They fix the target and goals for the different departments to accomplish the objective

of the organisation. The favourable variances are appreciated but in the case of adverse variance

they try to manage them by using the various tools like training and development program etc.

Techniques and concept : management accounting use the various techniques such ad

standard costing, budgetary control, cash flow, balance sheet, ratio analysis etc. to make t eh

information and accounting more useful (Zahller, 2017). Each technique used by the interactive

investor is for the special purpose like to present the data. Managing the organization or to take

the decisions.

Cause and effect relation: the role of financial accounting is to present the data in profit

and loss account of balance sheet but the role of management accounting is to present the cause

and effect relation of the data and their decisions. If the company suffer from the losses than the

role of management accounting is to find the reason behind the losses. The profit of the

organization is also analysed to check the accuracy of the process and data.

Forecasting : the role of management accounting is to take the decisions for the future

events on the current performance of the company. Interactive investor company forecast their

company sales and revenue by the past year performance and prepare budget according to it

forecast the expenses.

Need of the understandability of the management accounting report

The report of the management accounting should be in proper format so that it is easily

comprehensible, and functional to make decisions in better way and get the result quickly. The

8

decisions of the top management and employee are base on these report (Hada, Todoran, and

Avram, 2016). By evaluating the records of the report like the sale, profit, employee

performance, productivity of the organization, overall expenses, cash inflow and outflow etc. on

the basis of this transaction they make the decisions. For example : If the profit of the Interactive

investor is high then they take the decision to invest them in more productive activity or

distribute the profit as dividend. But if the report are not present in the understandable manner

than there is high chances of taking wrong decision which may affect the business.

Various management accounting reports

The company uses various kind of management accounting report to present their data in

more systematic manner and calculate the variances on the basis of reports. The management

reports are as follows :

Performance report : It provides an overview about the performance of the organization

and its employees and help the company to get the knowledge about the organization activity in

particular period. It helps to get the growth and success journey of t eh company in accounting

year and compare the performance to different organisation to prepare a better strategy to

accomplish the goal and objectives. The performance report also helps to analyse the weak area

of the company to focus on the particular segment.

Budget report : Budget report help the company to estimate the expenses and sources of

income in particular period. It also provides a comparison to analyse the company performance

that how efficiently a company is able to achieve the target on time. It is based on historical data

and performance. It helps to allocate the financial resources to the different activities to complete

the task within the given budget.

Cash flow : It is used to present the total cash inflow and outflow of the organization in

particular accounting period. It was used by the organization to maintain the cash level to meet

the day to day requirement of the company. It helps Interactive investor company to manage the

cash inflow and outflow from the various retail business to provide their services and product.

LO 2

P 3 Calculation of cost and preparation of income statements

Micro economic techniques:

9

Avram, 2016). By evaluating the records of the report like the sale, profit, employee

performance, productivity of the organization, overall expenses, cash inflow and outflow etc. on

the basis of this transaction they make the decisions. For example : If the profit of the Interactive

investor is high then they take the decision to invest them in more productive activity or

distribute the profit as dividend. But if the report are not present in the understandable manner

than there is high chances of taking wrong decision which may affect the business.

Various management accounting reports

The company uses various kind of management accounting report to present their data in

more systematic manner and calculate the variances on the basis of reports. The management

reports are as follows :

Performance report : It provides an overview about the performance of the organization

and its employees and help the company to get the knowledge about the organization activity in

particular period. It helps to get the growth and success journey of t eh company in accounting

year and compare the performance to different organisation to prepare a better strategy to

accomplish the goal and objectives. The performance report also helps to analyse the weak area

of the company to focus on the particular segment.

Budget report : Budget report help the company to estimate the expenses and sources of

income in particular period. It also provides a comparison to analyse the company performance

that how efficiently a company is able to achieve the target on time. It is based on historical data

and performance. It helps to allocate the financial resources to the different activities to complete

the task within the given budget.

Cash flow : It is used to present the total cash inflow and outflow of the organization in

particular accounting period. It was used by the organization to maintain the cash level to meet

the day to day requirement of the company. It helps Interactive investor company to manage the

cash inflow and outflow from the various retail business to provide their services and product.

LO 2

P 3 Calculation of cost and preparation of income statements

Micro economic techniques:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

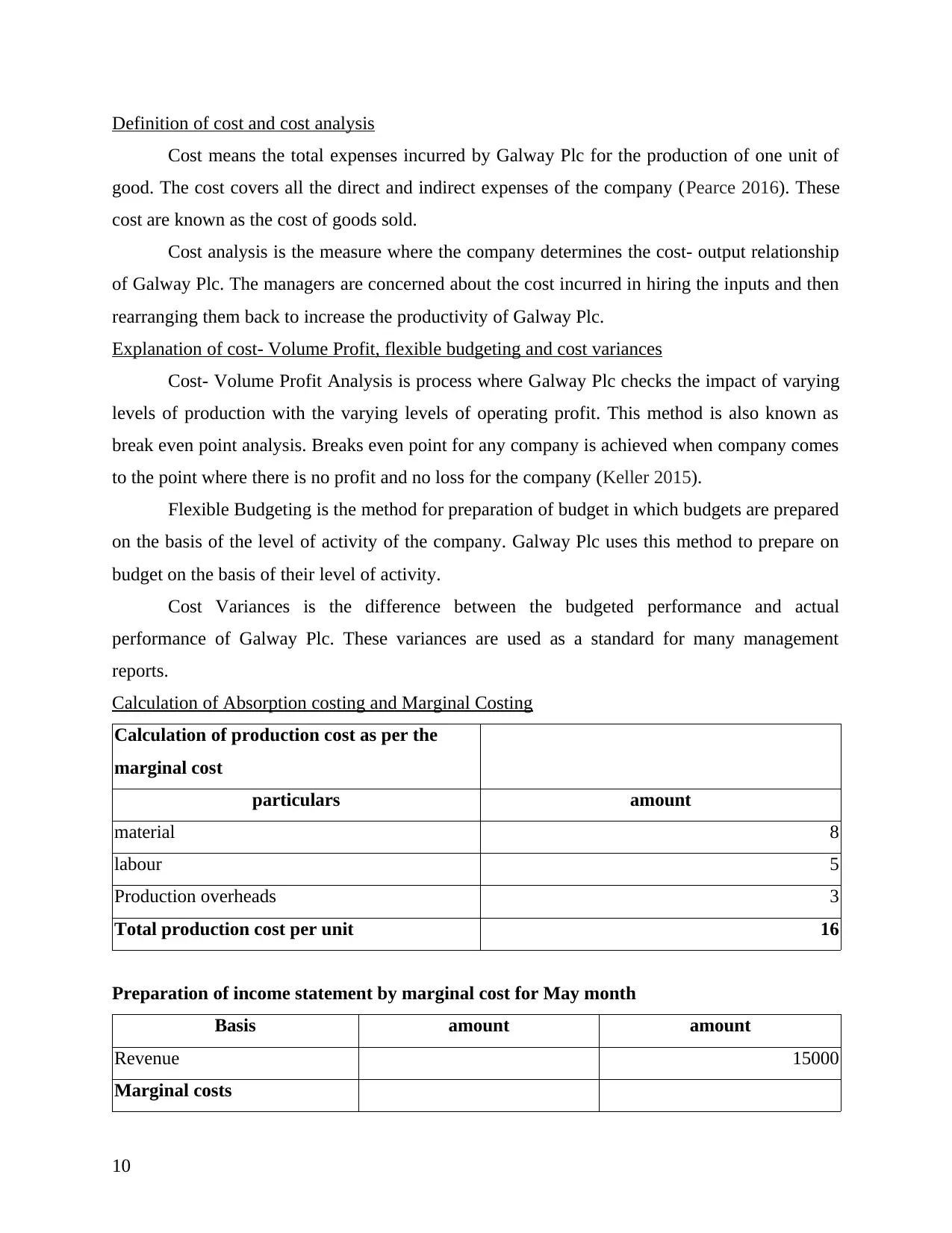

Definition of cost and cost analysis

Cost means the total expenses incurred by Galway Plc for the production of one unit of

good. The cost covers all the direct and indirect expenses of the company (Pearce 2016). These

cost are known as the cost of goods sold.

Cost analysis is the measure where the company determines the cost- output relationship

of Galway Plc. The managers are concerned about the cost incurred in hiring the inputs and then

rearranging them back to increase the productivity of Galway Plc.

Explanation of cost- Volume Profit, flexible budgeting and cost variances

Cost- Volume Profit Analysis is process where Galway Plc checks the impact of varying

levels of production with the varying levels of operating profit. This method is also known as

break even point analysis. Breaks even point for any company is achieved when company comes

to the point where there is no profit and no loss for the company (Keller 2015).

Flexible Budgeting is the method for preparation of budget in which budgets are prepared

on the basis of the level of activity of the company. Galway Plc uses this method to prepare on

budget on the basis of their level of activity.

Cost Variances is the difference between the budgeted performance and actual

performance of Galway Plc. These variances are used as a standard for many management

reports.

Calculation of Absorption costing and Marginal Costing

Calculation of production cost as per the

marginal cost

particulars amount

material 8

labour 5

Production overheads 3

Total production cost per unit 16

Preparation of income statement by marginal cost for May month

Basis amount amount

Revenue 15000

Marginal costs

10

Cost means the total expenses incurred by Galway Plc for the production of one unit of

good. The cost covers all the direct and indirect expenses of the company (Pearce 2016). These

cost are known as the cost of goods sold.

Cost analysis is the measure where the company determines the cost- output relationship

of Galway Plc. The managers are concerned about the cost incurred in hiring the inputs and then

rearranging them back to increase the productivity of Galway Plc.

Explanation of cost- Volume Profit, flexible budgeting and cost variances

Cost- Volume Profit Analysis is process where Galway Plc checks the impact of varying

levels of production with the varying levels of operating profit. This method is also known as

break even point analysis. Breaks even point for any company is achieved when company comes

to the point where there is no profit and no loss for the company (Keller 2015).

Flexible Budgeting is the method for preparation of budget in which budgets are prepared

on the basis of the level of activity of the company. Galway Plc uses this method to prepare on

budget on the basis of their level of activity.

Cost Variances is the difference between the budgeted performance and actual

performance of Galway Plc. These variances are used as a standard for many management

reports.

Calculation of Absorption costing and Marginal Costing

Calculation of production cost as per the

marginal cost

particulars amount

material 8

labour 5

Production overheads 3

Total production cost per unit 16

Preparation of income statement by marginal cost for May month

Basis amount amount

Revenue 15000

Marginal costs

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

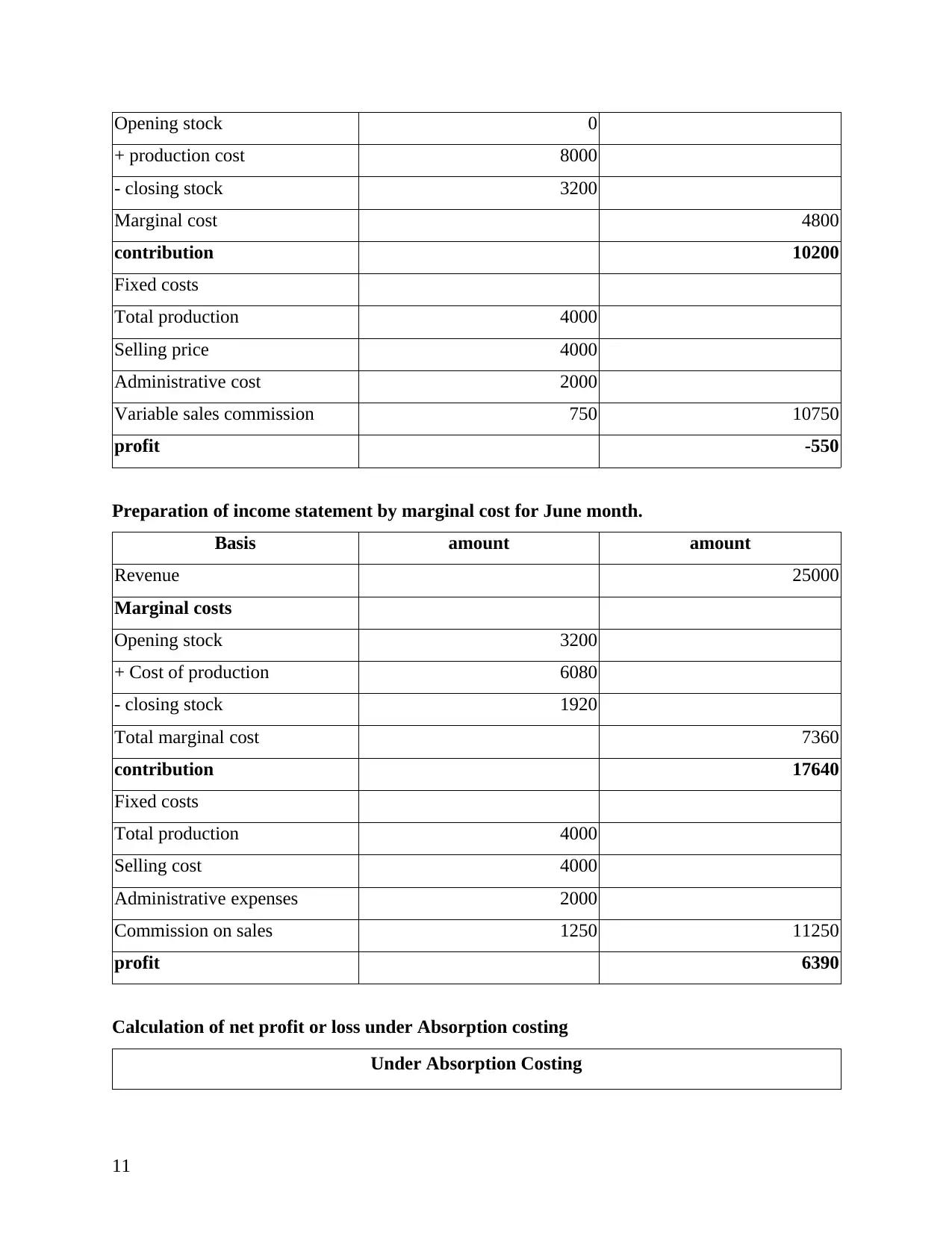

Opening stock 0

+ production cost 8000

- closing stock 3200

Marginal cost 4800

contribution 10200

Fixed costs

Total production 4000

Selling price 4000

Administrative cost 2000

Variable sales commission 750 10750

profit -550

Preparation of income statement by marginal cost for June month.

Basis amount amount

Revenue 25000

Marginal costs

Opening stock 3200

+ Cost of production 6080

- closing stock 1920

Total marginal cost 7360

contribution 17640

Fixed costs

Total production 4000

Selling cost 4000

Administrative expenses 2000

Commission on sales 1250 11250

profit 6390

Calculation of net profit or loss under Absorption costing

Under Absorption Costing

11

+ production cost 8000

- closing stock 3200

Marginal cost 4800

contribution 10200

Fixed costs

Total production 4000

Selling price 4000

Administrative cost 2000

Variable sales commission 750 10750

profit -550

Preparation of income statement by marginal cost for June month.

Basis amount amount

Revenue 25000

Marginal costs

Opening stock 3200

+ Cost of production 6080

- closing stock 1920

Total marginal cost 7360

contribution 17640

Fixed costs

Total production 4000

Selling cost 4000

Administrative expenses 2000

Commission on sales 1250 11250

profit 6390

Calculation of net profit or loss under Absorption costing

Under Absorption Costing

11

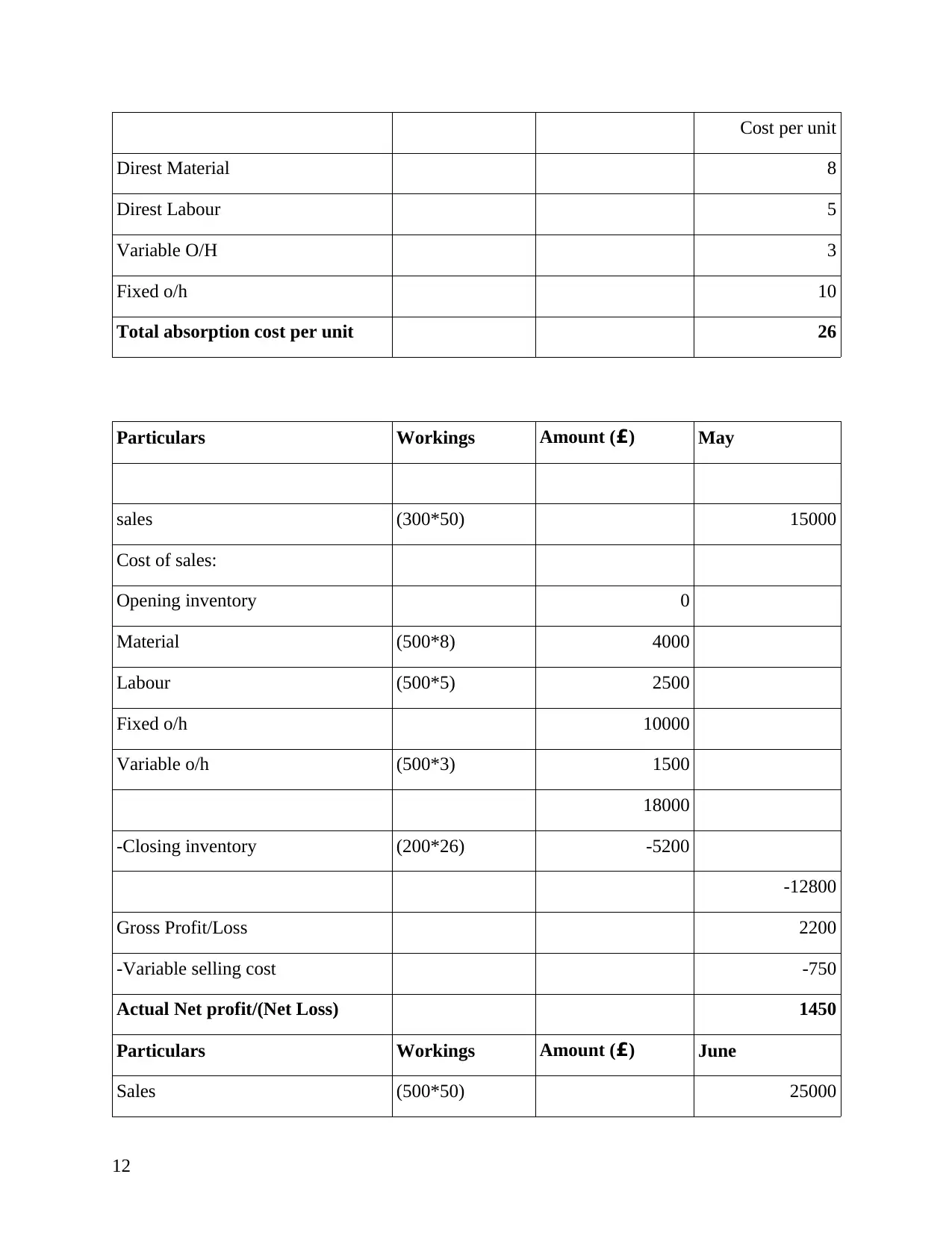

Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

Particulars Workings Amount (£) May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

Particulars Workings Amount (£) June

Sales (500*50) 25000

12

Direst Material 8

Direst Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

Particulars Workings Amount (£) May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

Particulars Workings Amount (£) June

Sales (500*50) 25000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.