An Investigation of Interest Rate in Tajik Commercial Banks

VerifiedAdded on 2023/02/03

|113

|30790

|99

Report

AI Summary

This report presents an investigation into the impact of interest rate variations on commercial banks in Tajikistan following the country's accession to the World Trade Organization (WTO). The study examines various aspects, including the influence of liberalization on lending rates, the factors affecting interest rate determination, and the role of inflation. Data analysis includes test/retest reliability, univariate, bivariate, and multivariate statistics, along with thematic analysis to explore key questions. The findings reveal insights into how commercial banks manage interest rates, the satisfaction of online services, and the importance of asset-liability management. The report also covers the outcomes of hypothesis testing, contributions to knowledge, recommendations, limitations, and suggestions for future research. The study uses descriptive statistics, ANOVA tests, T-tests, and Chi-square tests to analyze the data collected from professionals at commercial banks in Tajikistan, providing a comprehensive overview of the financial landscape and operational practices within the banking sector.

An investigation of variation and impact of

interest rate in commercial banks in

Tajikistan after accession to WTO

interest rate in commercial banks in

Tajikistan after accession to WTO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

CHAPTER 4: FINDINGS......................................................................................................................1

4.1 Introduction......................................................................................................................1

4.2 Data analysis.....................................................................................................................1

4.2.1 Test/ Retest Reliability.............................................................................................1

4.2.2 Univariate statistics...................................................................................................8

4.2.3 Bivariate Statistics..................................................................................................19

4.2.4 Multivariate Statistics.............................................................................................27

4.3 Themes...........................................................................................................................37

4.3.1 Theme 1: How does liberalization affect lending rate of the commercial bank lending rates? 37

4.3.2 Theme 2: Does your bank has any influences due to commercial bank lending rates? 38

4.3.3 Theme 3: The cost factors affect determination of lending rates in commercial banks in Tajikistan 40

4.3.4 Theme 4: The general factors are relevant with cost of loans................................41

4.3.5 Theme 5: Influence of the inflation rate of the nation on the central bank interest rate policy and lending rate of

commercial banks............................................................................................................41

4.4 Conclusion......................................................................................................................42

CHAPTER 5: FINDINGS AND DISCUSSION.......................................................................................44

5.1 Introduction....................................................................................................................44

5.2.........................................................................................................................................48

5.2.1: Satisfaction through online services provided by bank.........................................48

5.2.2 Theme 3: Securities with making transactional operations....................................52

5.2.3 Theme 4: Role of banks’ assets and liability management for addressing financial issues 54

CHAPTER 4: FINDINGS......................................................................................................................1

4.1 Introduction......................................................................................................................1

4.2 Data analysis.....................................................................................................................1

4.2.1 Test/ Retest Reliability.............................................................................................1

4.2.2 Univariate statistics...................................................................................................8

4.2.3 Bivariate Statistics..................................................................................................19

4.2.4 Multivariate Statistics.............................................................................................27

4.3 Themes...........................................................................................................................37

4.3.1 Theme 1: How does liberalization affect lending rate of the commercial bank lending rates? 37

4.3.2 Theme 2: Does your bank has any influences due to commercial bank lending rates? 38

4.3.3 Theme 3: The cost factors affect determination of lending rates in commercial banks in Tajikistan 40

4.3.4 Theme 4: The general factors are relevant with cost of loans................................41

4.3.5 Theme 5: Influence of the inflation rate of the nation on the central bank interest rate policy and lending rate of

commercial banks............................................................................................................41

4.4 Conclusion......................................................................................................................42

CHAPTER 5: FINDINGS AND DISCUSSION.......................................................................................44

5.1 Introduction....................................................................................................................44

5.2.........................................................................................................................................48

5.2.1: Satisfaction through online services provided by bank.........................................48

5.2.2 Theme 3: Securities with making transactional operations....................................52

5.2.3 Theme 4: Role of banks’ assets and liability management for addressing financial issues 54

5.2.4 Theme 5: Satisfaction through interest rate charges on borrowed money..............61

5.3 Conclusion......................................................................................................................66

CHAPTER 6: CONCLUSION, CONTRIBUTION AND RECOMMENDATIONS......................................69

6.1 Review of aim and objective..........................................................................................69

6.2 Outcome of hypothesis tested.......................................................................................70

6.3 Contribution to knowledge.............................................................................................72

6.3.1 Theoretical contribution..........................................................................................72

6.3.2 Empirical contribution............................................................................................73

6.3.3 Practical contribution..............................................................................................73

6.4 Recommendations..........................................................................................................74

6.5 Limitations recognised in research study.......................................................................77

6.6 Further study for future research..................................................................................77

6.7 Personal reflection..........................................................................................................78

REFERENCES..............................................................................................................................79

APPENDIX....................................................................................................................................82

5.3 Conclusion......................................................................................................................66

CHAPTER 6: CONCLUSION, CONTRIBUTION AND RECOMMENDATIONS......................................69

6.1 Review of aim and objective..........................................................................................69

6.2 Outcome of hypothesis tested.......................................................................................70

6.3 Contribution to knowledge.............................................................................................72

6.3.1 Theoretical contribution..........................................................................................72

6.3.2 Empirical contribution............................................................................................73

6.3.3 Practical contribution..............................................................................................73

6.4 Recommendations..........................................................................................................74

6.5 Limitations recognised in research study.......................................................................77

6.6 Further study for future research..................................................................................77

6.7 Personal reflection..........................................................................................................78

REFERENCES..............................................................................................................................79

APPENDIX....................................................................................................................................82

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 4: FINDINGS

4.1 Introduction

In this present chapter there have been examination and test of the data base which have been used by researcher to analyse the

research issues. Moreover, with aspect to make adequate ascertainment and analyse the changes or influences commercial banks have

as per changing interest rates and governmental regulation relevant with banking operations

To analyse the impacts of changes in lending rates which affects commercial bank’s operations and growth. However, in relation

with this, there will be determination of the main factors which are affecting commercial bank operations as well as interest rate

variation in Tajikistan. There has been development of various plans and operational variation which will help in making proper

ascertainment of the operations. In this process, there will be influences of various aspects and elements which have been used to

examine the factors such as Descriptive statistics, ANOVA tests, T-test, Chi square, etc. therefore, such tests and statistical analysis

will bring accurate information relevant with data base. In addition, as per analysing the appropriate outcomes, there will be

preparation of several questions and interview with professionals at commercial banks of Tajikistan which in turn will be useful for

making appropriate participation in this aspect.

4.2 Data analysis

4.2.1 Test/ Retest Reliability

In relation with analysing the relationship between the group of variables which are has to be considered by the researcher with

approach to have adequate ascertainment of the data base. Thus, in accordance with this, 5 industrial question are prepared solely and

not taken from any research paper or magazine. These questions will be asked to 150 employees at the commercial banks of

Tajikistan. Thus, this test will be helpful in analysing the reliability of information which have been used for the further tests and

analysis. In accordance with designed data set there have been implication of Cronbach’s Alpha coefficient over the 5 variables. Thus,

there have presented information as follows:

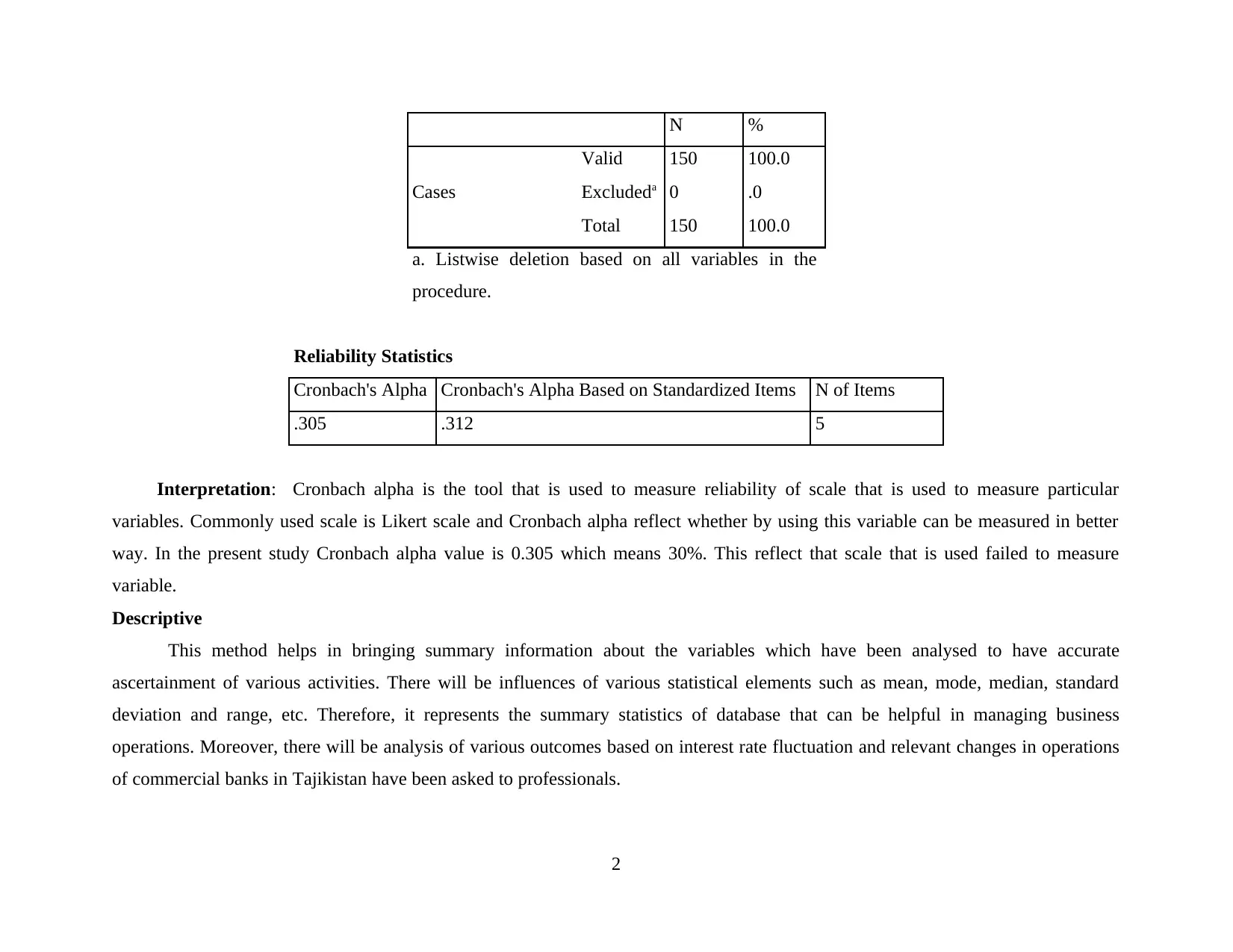

Case Processing Summary

1

4.1 Introduction

In this present chapter there have been examination and test of the data base which have been used by researcher to analyse the

research issues. Moreover, with aspect to make adequate ascertainment and analyse the changes or influences commercial banks have

as per changing interest rates and governmental regulation relevant with banking operations

To analyse the impacts of changes in lending rates which affects commercial bank’s operations and growth. However, in relation

with this, there will be determination of the main factors which are affecting commercial bank operations as well as interest rate

variation in Tajikistan. There has been development of various plans and operational variation which will help in making proper

ascertainment of the operations. In this process, there will be influences of various aspects and elements which have been used to

examine the factors such as Descriptive statistics, ANOVA tests, T-test, Chi square, etc. therefore, such tests and statistical analysis

will bring accurate information relevant with data base. In addition, as per analysing the appropriate outcomes, there will be

preparation of several questions and interview with professionals at commercial banks of Tajikistan which in turn will be useful for

making appropriate participation in this aspect.

4.2 Data analysis

4.2.1 Test/ Retest Reliability

In relation with analysing the relationship between the group of variables which are has to be considered by the researcher with

approach to have adequate ascertainment of the data base. Thus, in accordance with this, 5 industrial question are prepared solely and

not taken from any research paper or magazine. These questions will be asked to 150 employees at the commercial banks of

Tajikistan. Thus, this test will be helpful in analysing the reliability of information which have been used for the further tests and

analysis. In accordance with designed data set there have been implication of Cronbach’s Alpha coefficient over the 5 variables. Thus,

there have presented information as follows:

Case Processing Summary

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

N %

Cases

Valid 150 100.0

Excludeda 0 .0

Total 150 100.0

a. Listwise deletion based on all variables in the

procedure.

Reliability Statistics

Cronbach's Alpha Cronbach's Alpha Based on Standardized Items N of Items

.305 .312 5

Interpretation: Cronbach alpha is the tool that is used to measure reliability of scale that is used to measure particular

variables. Commonly used scale is Likert scale and Cronbach alpha reflect whether by using this variable can be measured in better

way. In the present study Cronbach alpha value is 0.305 which means 30%. This reflect that scale that is used failed to measure

variable.

Descriptive

This method helps in bringing summary information about the variables which have been analysed to have accurate

ascertainment of various activities. There will be influences of various statistical elements such as mean, mode, median, standard

deviation and range, etc. Therefore, it represents the summary statistics of database that can be helpful in managing business

operations. Moreover, there will be analysis of various outcomes based on interest rate fluctuation and relevant changes in operations

of commercial banks in Tajikistan have been asked to professionals.

2

Cases

Valid 150 100.0

Excludeda 0 .0

Total 150 100.0

a. Listwise deletion based on all variables in the

procedure.

Reliability Statistics

Cronbach's Alpha Cronbach's Alpha Based on Standardized Items N of Items

.305 .312 5

Interpretation: Cronbach alpha is the tool that is used to measure reliability of scale that is used to measure particular

variables. Commonly used scale is Likert scale and Cronbach alpha reflect whether by using this variable can be measured in better

way. In the present study Cronbach alpha value is 0.305 which means 30%. This reflect that scale that is used failed to measure

variable.

Descriptive

This method helps in bringing summary information about the variables which have been analysed to have accurate

ascertainment of various activities. There will be influences of various statistical elements such as mean, mode, median, standard

deviation and range, etc. Therefore, it represents the summary statistics of database that can be helpful in managing business

operations. Moreover, there will be analysis of various outcomes based on interest rate fluctuation and relevant changes in operations

of commercial banks in Tajikistan have been asked to professionals.

2

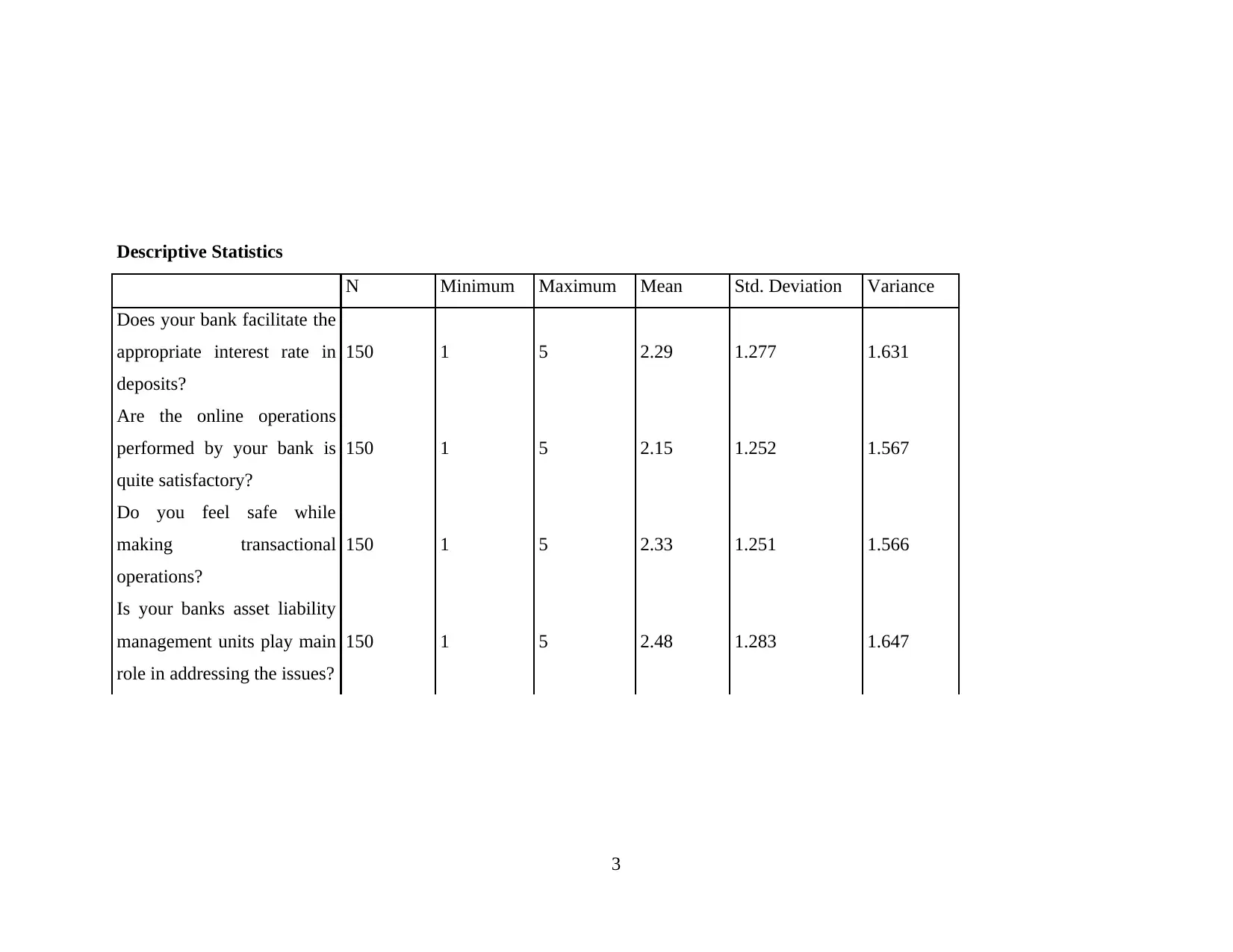

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation Variance

Does your bank facilitate the

appropriate interest rate in

deposits?

150 1 5 2.29 1.277 1.631

Are the online operations

performed by your bank is

quite satisfactory?

150 1 5 2.15 1.252 1.567

Do you feel safe while

making transactional

operations?

150 1 5 2.33 1.251 1.566

Is your banks asset liability

management units play main

role in addressing the issues?

150 1 5 2.48 1.283 1.647

3

N Minimum Maximum Mean Std. Deviation Variance

Does your bank facilitate the

appropriate interest rate in

deposits?

150 1 5 2.29 1.277 1.631

Are the online operations

performed by your bank is

quite satisfactory?

150 1 5 2.15 1.252 1.567

Do you feel safe while

making transactional

operations?

150 1 5 2.33 1.251 1.566

Is your banks asset liability

management units play main

role in addressing the issues?

150 1 5 2.48 1.283 1.647

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

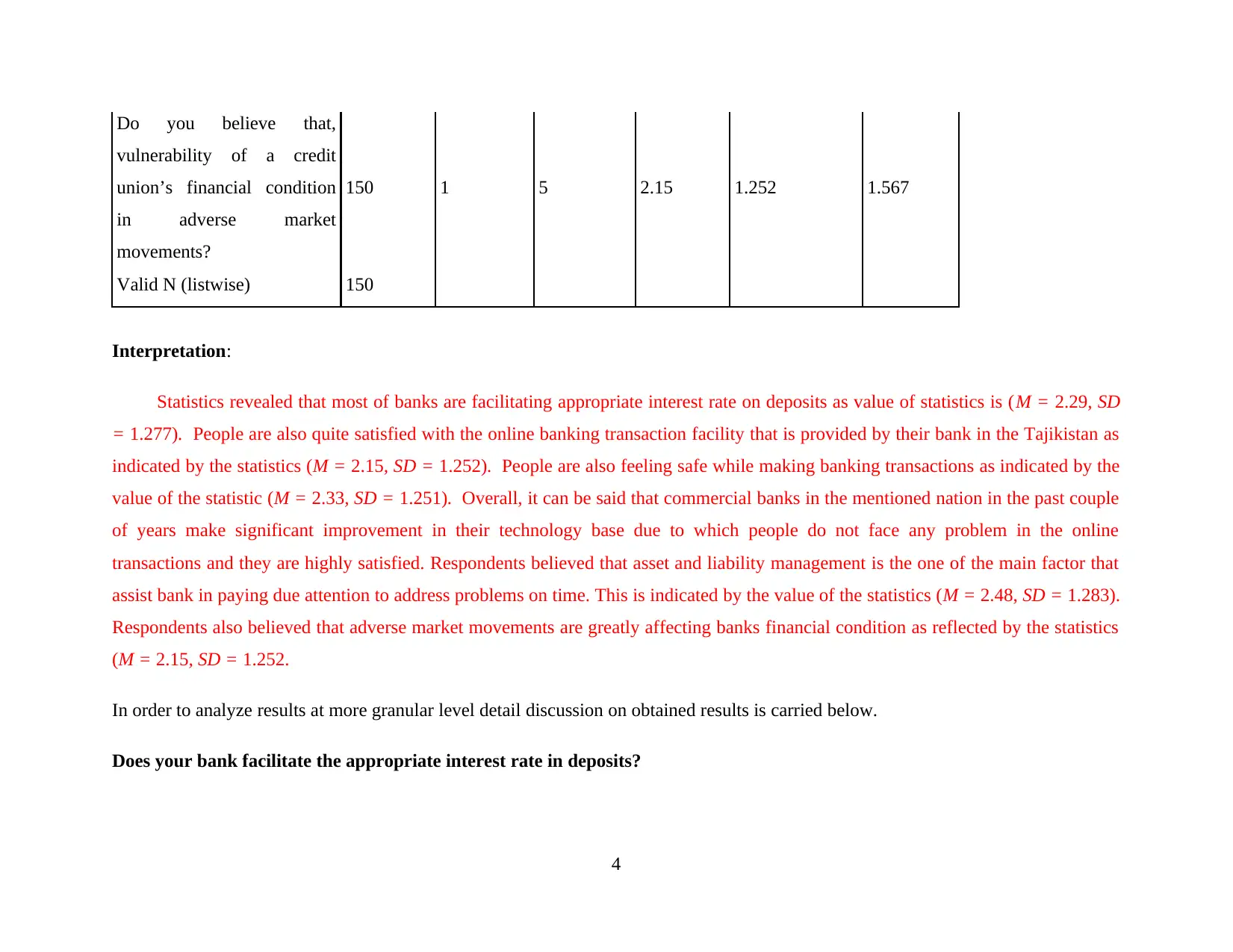

Do you believe that,

vulnerability of a credit

union’s financial condition

in adverse market

movements?

150 1 5 2.15 1.252 1.567

Valid N (listwise) 150

Interpretation:

Statistics revealed that most of banks are facilitating appropriate interest rate on deposits as value of statistics is (M = 2.29, SD

= 1.277). People are also quite satisfied with the online banking transaction facility that is provided by their bank in the Tajikistan as

indicated by the statistics (M = 2.15, SD = 1.252). People are also feeling safe while making banking transactions as indicated by the

value of the statistic (M = 2.33, SD = 1.251). Overall, it can be said that commercial banks in the mentioned nation in the past couple

of years make significant improvement in their technology base due to which people do not face any problem in the online

transactions and they are highly satisfied. Respondents believed that asset and liability management is the one of the main factor that

assist bank in paying due attention to address problems on time. This is indicated by the value of the statistics (M = 2.48, SD = 1.283).

Respondents also believed that adverse market movements are greatly affecting banks financial condition as reflected by the statistics

(M = 2.15, SD = 1.252.

In order to analyze results at more granular level detail discussion on obtained results is carried below.

Does your bank facilitate the appropriate interest rate in deposits?

4

vulnerability of a credit

union’s financial condition

in adverse market

movements?

150 1 5 2.15 1.252 1.567

Valid N (listwise) 150

Interpretation:

Statistics revealed that most of banks are facilitating appropriate interest rate on deposits as value of statistics is (M = 2.29, SD

= 1.277). People are also quite satisfied with the online banking transaction facility that is provided by their bank in the Tajikistan as

indicated by the statistics (M = 2.15, SD = 1.252). People are also feeling safe while making banking transactions as indicated by the

value of the statistic (M = 2.33, SD = 1.251). Overall, it can be said that commercial banks in the mentioned nation in the past couple

of years make significant improvement in their technology base due to which people do not face any problem in the online

transactions and they are highly satisfied. Respondents believed that asset and liability management is the one of the main factor that

assist bank in paying due attention to address problems on time. This is indicated by the value of the statistics (M = 2.48, SD = 1.283).

Respondents also believed that adverse market movements are greatly affecting banks financial condition as reflected by the statistics

(M = 2.15, SD = 1.252.

In order to analyze results at more granular level detail discussion on obtained results is carried below.

Does your bank facilitate the appropriate interest rate in deposits?

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It has been asked to the professionals that their bank faciality the appropriate interest rates in deposits from commercial banks.

On the basis for above listed outcomes where 37.3% of professionals believes that there will be appropriate interest rates in deposits of

banks. Therefore, there are appropriate rates which have been awarded to consumers on their savings account and deposits they make

in banks. Moreover, due to such charging rates they will retain appropriate gains on such investments. Along with this, there are

various reviews from professionals on which majority are in favor. It can be said that, commercial banks in Tajikistan are charging

satisfactory interest rates on deposits. In accordance with pension scheme which have been offered by government to its employees on

the basis of their job and level of remuneration retained by them. There have been influences of government policy development

which in turn have negative and positive impacts over schemes and offered by banking industries. Thus, the motive of government in

bringing appropriate revenue gains to the citizens on the basis of their performed duties and jobs in a particular sector. It basically

depends on the level of operations performed by a bank as well as the number of consumers associated with banking activities. Thus,

it can be said that, governmental plans and policies are less affecting the banking sector in Tajikistan which are in turn have

facilitating proper wealth to society. It will be based on changing effective rates of interest among consumers in saving their implied

funds.

Are the online operations performed by your bank quite satisfactory?

By considering the online transactional activities performed by banks for soothing banking activities. Thus, it has been asked

to 150 professionals at commercial banks in Tajikistan based on satisfaction through making online operations. Hence, on which

majority of them have presented their reviews in favor. It states that, there are 41.35% of professionals are strongly agree with this

statement, 25.3% are agree, 16.75 are neutral while same percentage of individual are disagree this statement. As per analyzing the

variations in the outcome on which it can be said that, currently the banking operations has been enhanced in Tajikistan which are

bringing proper satisfaction. Moreover, in relation which such outcomes it can be said that, online transaction of money and financial

terms are comparatively secure. Thus, the confidentiality of data base is managed well in the commercial banks of Tajikistan. The

separate risks management system is needed to be existed in a banking industry. It helps in securing time as well as perfectly

5

On the basis for above listed outcomes where 37.3% of professionals believes that there will be appropriate interest rates in deposits of

banks. Therefore, there are appropriate rates which have been awarded to consumers on their savings account and deposits they make

in banks. Moreover, due to such charging rates they will retain appropriate gains on such investments. Along with this, there are

various reviews from professionals on which majority are in favor. It can be said that, commercial banks in Tajikistan are charging

satisfactory interest rates on deposits. In accordance with pension scheme which have been offered by government to its employees on

the basis of their job and level of remuneration retained by them. There have been influences of government policy development

which in turn have negative and positive impacts over schemes and offered by banking industries. Thus, the motive of government in

bringing appropriate revenue gains to the citizens on the basis of their performed duties and jobs in a particular sector. It basically

depends on the level of operations performed by a bank as well as the number of consumers associated with banking activities. Thus,

it can be said that, governmental plans and policies are less affecting the banking sector in Tajikistan which are in turn have

facilitating proper wealth to society. It will be based on changing effective rates of interest among consumers in saving their implied

funds.

Are the online operations performed by your bank quite satisfactory?

By considering the online transactional activities performed by banks for soothing banking activities. Thus, it has been asked

to 150 professionals at commercial banks in Tajikistan based on satisfaction through making online operations. Hence, on which

majority of them have presented their reviews in favor. It states that, there are 41.35% of professionals are strongly agree with this

statement, 25.3% are agree, 16.75 are neutral while same percentage of individual are disagree this statement. As per analyzing the

variations in the outcome on which it can be said that, currently the banking operations has been enhanced in Tajikistan which are

bringing proper satisfaction. Moreover, in relation which such outcomes it can be said that, online transaction of money and financial

terms are comparatively secure. Thus, the confidentiality of data base is managed well in the commercial banks of Tajikistan. The

separate risks management system is needed to be existed in a banking industry. It helps in securing time as well as perfectly

5

executing the business operations. It ensures addressing the issues with proper consideration of all causes and impacts. Currently this

technique has been presented by banks in making appropriate operational analysis and efficiency of the issues which in turn will be

useful and adhesive for attaining favorable banking operations. Obstacles are mainly relevant with transferring the funds as well as

confidentiality of data base in online operations. On the other side, as per considering the above analyzed outcomes on which it can be

said that, there are major positive reviews obtained from the professionals at commercial banks. Thus, with respect with this,

maximum positive reviews have been considered by the professionals which emphasized on the outcomes as there are satisfactory risk

management system in the organization.

Do you feel safe while making transactional operations?

It has been asked to the professionals regarding the securities of the transactional activities they perform in the banking

operations make them feel safe. Thus. On which various reviews had been gathered by the researchers. on which it can be said that

there are 33.3% professionals are strongly agree with the statements, 26.7% are only agree while 20% are neutral at this approach.

Majority of opinion are in favour of this statement on which it can be said that, they are well confident in terms of having appropriate

analysis over the data base and appropriate determination of practices. In this case it can be said that the banking firms has to be more

focused in terms of improving security at transactional level. The details relevant with accounts, amount as well as destination needed

to be kept confidential as it will not affect the wealth of any individual. Thus, the inter-banking operations has been analysed and

determined by the researcher on which banks lend money to each other with a fixed interest rate to be charges. It helps them in

operating activities as well as improving banking functions in the environment. In analysing the outcomes there are approx. However,

it has been analysed that the borrowing interest rates are needed to be reformulated which will bring the positive rise to the income

generation as well as operational performance of the bank. There will be development of various policies and changes in activities

which can make suitable development in the operational practices. It creates opportunities to banking firms in terms of retaining

appropriate amount of revenue as well as make proper changes in operations.

Is your bank’s asset liability management units play main role in addressing the issues?

6

technique has been presented by banks in making appropriate operational analysis and efficiency of the issues which in turn will be

useful and adhesive for attaining favorable banking operations. Obstacles are mainly relevant with transferring the funds as well as

confidentiality of data base in online operations. On the other side, as per considering the above analyzed outcomes on which it can be

said that, there are major positive reviews obtained from the professionals at commercial banks. Thus, with respect with this,

maximum positive reviews have been considered by the professionals which emphasized on the outcomes as there are satisfactory risk

management system in the organization.

Do you feel safe while making transactional operations?

It has been asked to the professionals regarding the securities of the transactional activities they perform in the banking

operations make them feel safe. Thus. On which various reviews had been gathered by the researchers. on which it can be said that

there are 33.3% professionals are strongly agree with the statements, 26.7% are only agree while 20% are neutral at this approach.

Majority of opinion are in favour of this statement on which it can be said that, they are well confident in terms of having appropriate

analysis over the data base and appropriate determination of practices. In this case it can be said that the banking firms has to be more

focused in terms of improving security at transactional level. The details relevant with accounts, amount as well as destination needed

to be kept confidential as it will not affect the wealth of any individual. Thus, the inter-banking operations has been analysed and

determined by the researcher on which banks lend money to each other with a fixed interest rate to be charges. It helps them in

operating activities as well as improving banking functions in the environment. In analysing the outcomes there are approx. However,

it has been analysed that the borrowing interest rates are needed to be reformulated which will bring the positive rise to the income

generation as well as operational performance of the bank. There will be development of various policies and changes in activities

which can make suitable development in the operational practices. It creates opportunities to banking firms in terms of retaining

appropriate amount of revenue as well as make proper changes in operations.

Is your bank’s asset liability management units play main role in addressing the issues?

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of above listed analysis on which it has been asked to the professionals ate commercial banks of Tajikistan that,

their banks is capable of facilitating adequate asset-liability management is addressing the financial issues. Thus, the question arises

after considering the issues in the operations which have been faced by society after impacts of global financial crisis. Professionals

have presented the views on which large number of reviews are in favour which states theta their bank is capable of facilitating the

most adequate services to them. Main role of asset-liability department is mainly associated with facilitating the institution a strength

in terms of meeting debt challenges in the environment. There can be rise in operational gains and business motive which will help in

meeting the targets at the right time. Moreover, the commercial banks in Tajikistan are having the most convenient and appropriate

asset liability management. In relation with making additional gains banks usually offer term deposits. It is based on different rates for

several terms of borrowed amount. There will be revenue generation and adequate increment in the profitability of the banking sector

in Tajikistan. The long-term loans will have less rates while short period loans have higher interest rates. On a psychological manner it

can be said that, there are higher number of short term loan borrowers stated in the market. They usually take loans for specific task

such as purchasing home, vehicle and education. These loans are basically for a short period of time and that helps banks in retaining

higher gains. In relation with above listed analysis there are various favourable outcomes have been addressed by the researchers.

Professionals at commercial bank represented that, majority of them are charging rates with respect to variations in terms and time of

industry. Thus, again there are positive reviews from banks that they are adopting such techniques which will benefit them in getting

higher revenue through banking operations.

Do you believe that vulnerability of a credit union’s financial condition is same in adverse market movements?

In analysing influences of credit union are in context with helping each other fin the financial operations. they facilitate loans

or borrowing services to each other which in turn provides appropriate operational gains on lower interest rates. Thus, there have been

influences of various conditions which destructs such as adverse market condition like GFC, inflation or recession. In analysing such

outcomes, it can be said that, such factors will affect economy and which results changes in interest rates. On the other side, the above

listed analysis represents that there are 41.3% strongly believes that credit union’s financial condition fluctuates as per the changes

7

their banks is capable of facilitating adequate asset-liability management is addressing the financial issues. Thus, the question arises

after considering the issues in the operations which have been faced by society after impacts of global financial crisis. Professionals

have presented the views on which large number of reviews are in favour which states theta their bank is capable of facilitating the

most adequate services to them. Main role of asset-liability department is mainly associated with facilitating the institution a strength

in terms of meeting debt challenges in the environment. There can be rise in operational gains and business motive which will help in

meeting the targets at the right time. Moreover, the commercial banks in Tajikistan are having the most convenient and appropriate

asset liability management. In relation with making additional gains banks usually offer term deposits. It is based on different rates for

several terms of borrowed amount. There will be revenue generation and adequate increment in the profitability of the banking sector

in Tajikistan. The long-term loans will have less rates while short period loans have higher interest rates. On a psychological manner it

can be said that, there are higher number of short term loan borrowers stated in the market. They usually take loans for specific task

such as purchasing home, vehicle and education. These loans are basically for a short period of time and that helps banks in retaining

higher gains. In relation with above listed analysis there are various favourable outcomes have been addressed by the researchers.

Professionals at commercial bank represented that, majority of them are charging rates with respect to variations in terms and time of

industry. Thus, again there are positive reviews from banks that they are adopting such techniques which will benefit them in getting

higher revenue through banking operations.

Do you believe that vulnerability of a credit union’s financial condition is same in adverse market movements?

In analysing influences of credit union are in context with helping each other fin the financial operations. they facilitate loans

or borrowing services to each other which in turn provides appropriate operational gains on lower interest rates. Thus, there have been

influences of various conditions which destructs such as adverse market condition like GFC, inflation or recession. In analysing such

outcomes, it can be said that, such factors will affect economy and which results changes in interest rates. On the other side, the above

listed analysis represents that there are 41.3% strongly believes that credit union’s financial condition fluctuates as per the changes

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

incurred in market conditions. Therefore, it can be said that, to retain higher profits and securing capital funds in business. Moreover,

such variations had been done in accordance with making changes in the operational activities and business activities which has have

lead the organisation in retaining higher returns. Thus, these factors influence interest rates risk of such industries in a way of reducing

the level of sales and operational activities performed by them. There are various obstacles and issues which are affecting operations

of firm that helps in managing certain activities for adequate operational analysis. Therefore, these are the banking operations which

are needed to be considered seriously and administratively which will bring certain changes in the operations of the firm and that will

help them in making adequate operational changes.

Therefore, in this respect there are various strategic operations and decisions have been made by the banking professionals

which allows them in meeting the obstacles. Addressing such issues will be beneficial in retaining higher amount of profits through

operations as well as gathering large number of consumers. In formal process there will be analysis based on making proper auditing

of all accounts and analysis over causes which have affected the operational practices of banking firm.

4.2.2 Univariate statistics

This is the concept which will help in analysing the types of data and observations that argue to single attribute or characteristic.

However, analysing the univariate data on which researcher have denoted the independent variable as interest rates and dependent

variable as revenue in banking industries. In addition, there will be use of various data base which will be analysed, collected and

measured for accurate data analysis.

Hypothesis:

Null hypothesis: There is no mean significant difference between interest rates and revenue of commercial banks in Tajikistan

Alternative Hypothesis: There is a mean significant difference between interest rates and revenue of commercial banks in

Tajikistan

8

such variations had been done in accordance with making changes in the operational activities and business activities which has have

lead the organisation in retaining higher returns. Thus, these factors influence interest rates risk of such industries in a way of reducing

the level of sales and operational activities performed by them. There are various obstacles and issues which are affecting operations

of firm that helps in managing certain activities for adequate operational analysis. Therefore, these are the banking operations which

are needed to be considered seriously and administratively which will bring certain changes in the operations of the firm and that will

help them in making adequate operational changes.

Therefore, in this respect there are various strategic operations and decisions have been made by the banking professionals

which allows them in meeting the obstacles. Addressing such issues will be beneficial in retaining higher amount of profits through

operations as well as gathering large number of consumers. In formal process there will be analysis based on making proper auditing

of all accounts and analysis over causes which have affected the operational practices of banking firm.

4.2.2 Univariate statistics

This is the concept which will help in analysing the types of data and observations that argue to single attribute or characteristic.

However, analysing the univariate data on which researcher have denoted the independent variable as interest rates and dependent

variable as revenue in banking industries. In addition, there will be use of various data base which will be analysed, collected and

measured for accurate data analysis.

Hypothesis:

Null hypothesis: There is no mean significant difference between interest rates and revenue of commercial banks in Tajikistan

Alternative Hypothesis: There is a mean significant difference between interest rates and revenue of commercial banks in

Tajikistan

8

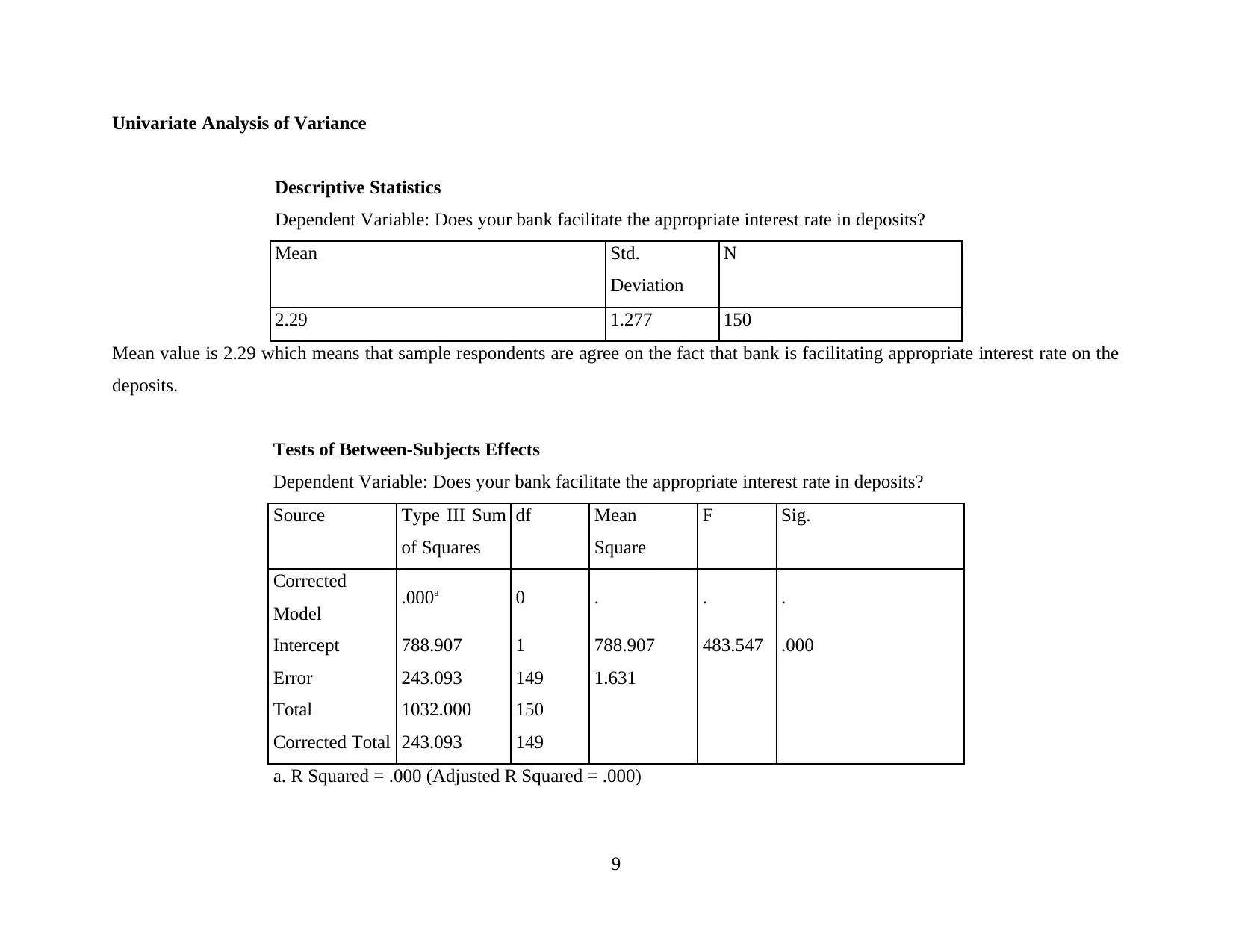

Univariate Analysis of Variance

Descriptive Statistics

Dependent Variable: Does your bank facilitate the appropriate interest rate in deposits?

Mean Std.

Deviation

N

2.29 1.277 150

Mean value is 2.29 which means that sample respondents are agree on the fact that bank is facilitating appropriate interest rate on the

deposits.

Tests of Between-Subjects Effects

Dependent Variable: Does your bank facilitate the appropriate interest rate in deposits?

Source Type III Sum

of Squares

df Mean

Square

F Sig.

Corrected

Model .000a 0 . . .

Intercept 788.907 1 788.907 483.547 .000

Error 243.093 149 1.631

Total 1032.000 150

Corrected Total 243.093 149

a. R Squared = .000 (Adjusted R Squared = .000)

9

Descriptive Statistics

Dependent Variable: Does your bank facilitate the appropriate interest rate in deposits?

Mean Std.

Deviation

N

2.29 1.277 150

Mean value is 2.29 which means that sample respondents are agree on the fact that bank is facilitating appropriate interest rate on the

deposits.

Tests of Between-Subjects Effects

Dependent Variable: Does your bank facilitate the appropriate interest rate in deposits?

Source Type III Sum

of Squares

df Mean

Square

F Sig.

Corrected

Model .000a 0 . . .

Intercept 788.907 1 788.907 483.547 .000

Error 243.093 149 1.631

Total 1032.000 150

Corrected Total 243.093 149

a. R Squared = .000 (Adjusted R Squared = .000)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 113

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.