Intermediate Accounting I (ACCT 3311) HW 3: Cash & Inventory

VerifiedAdded on 2022/09/08

|10

|1303

|34

Homework Assignment

AI Summary

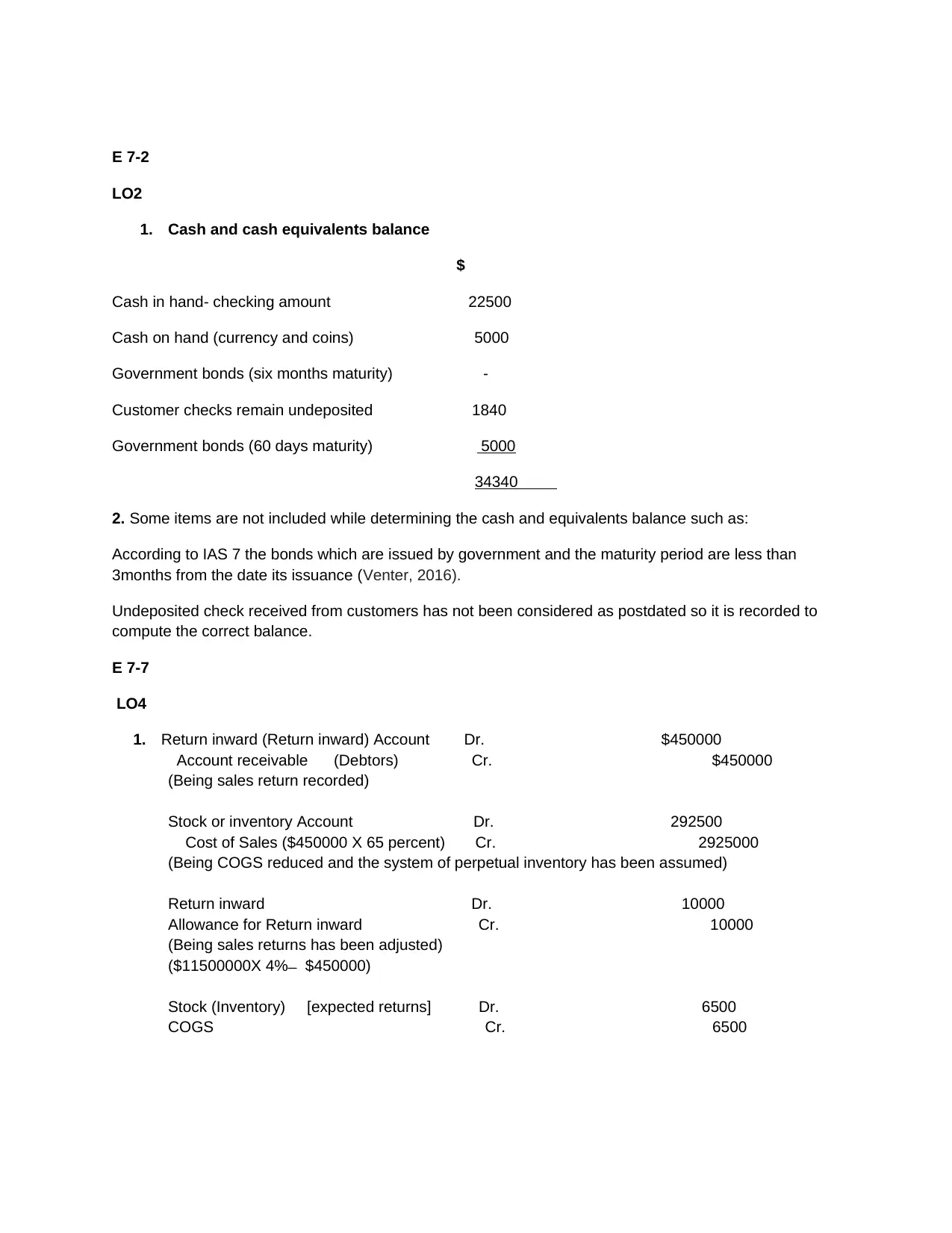

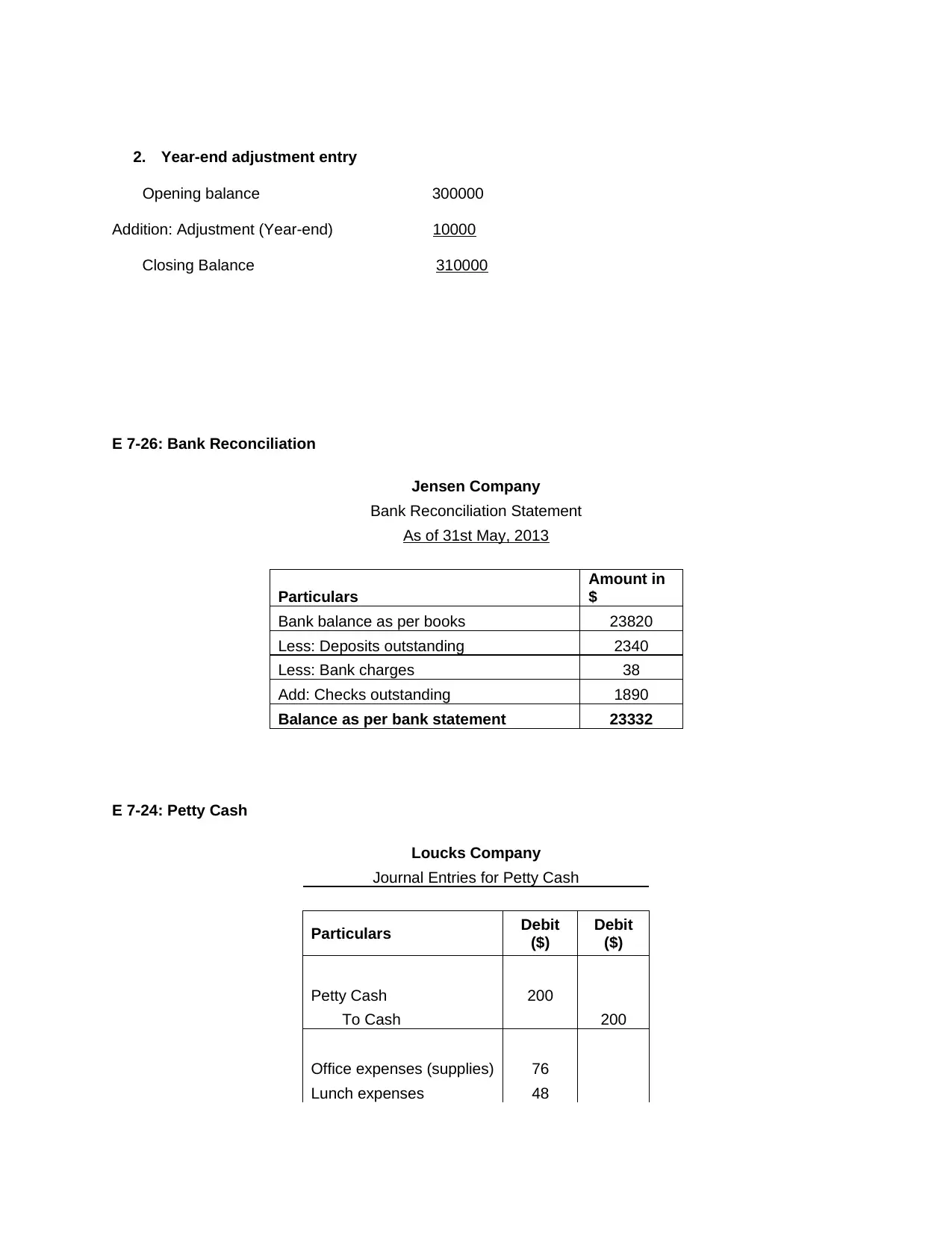

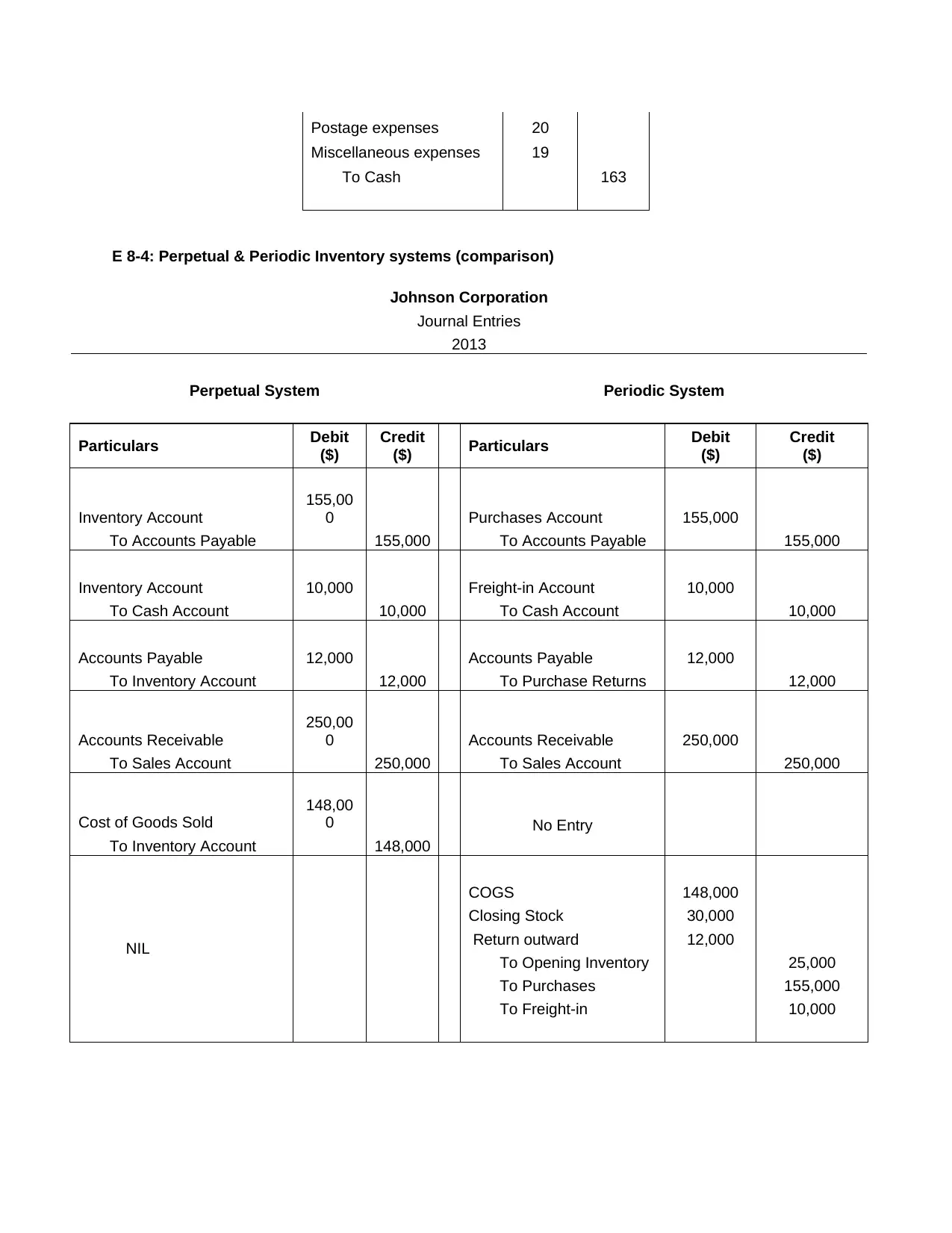

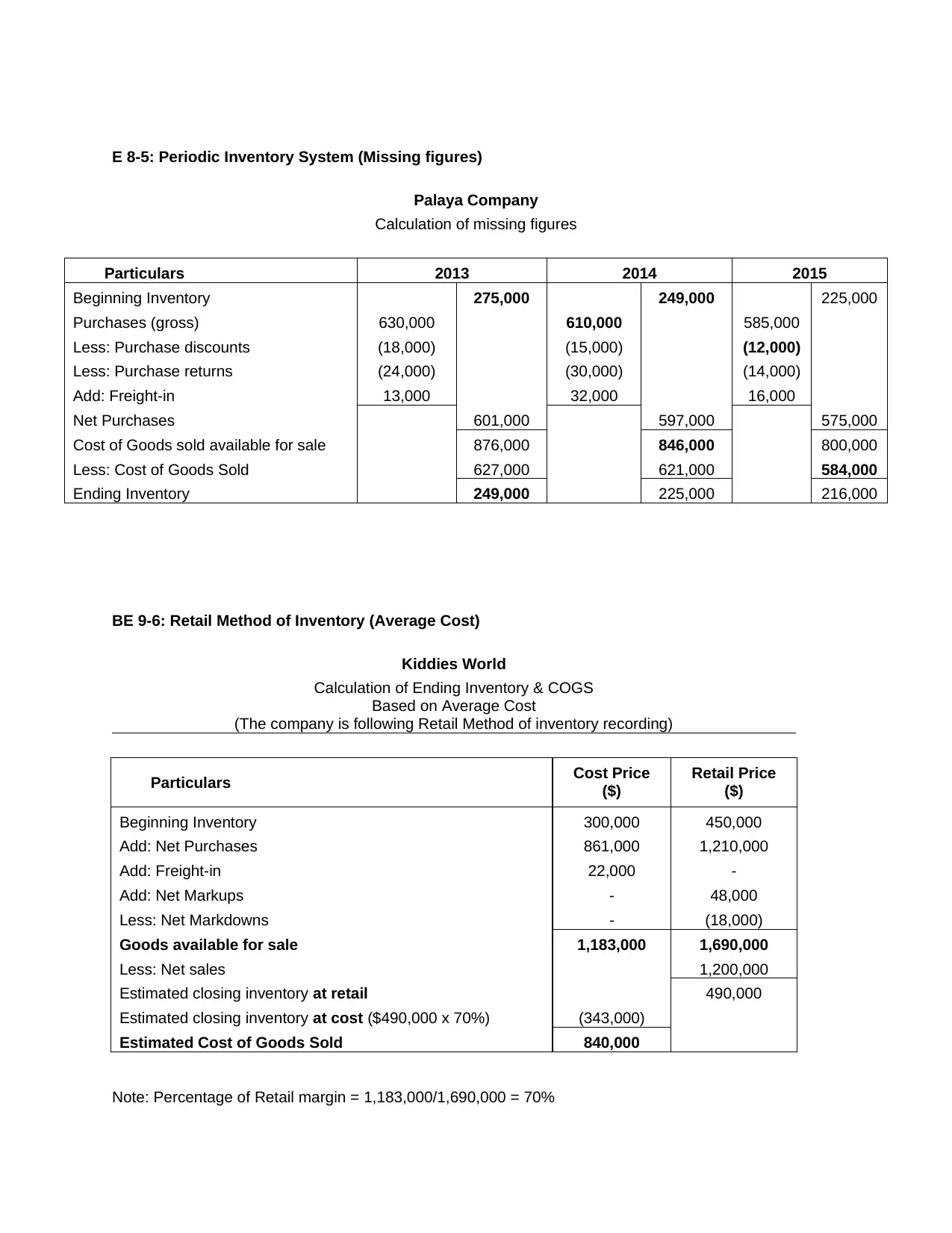

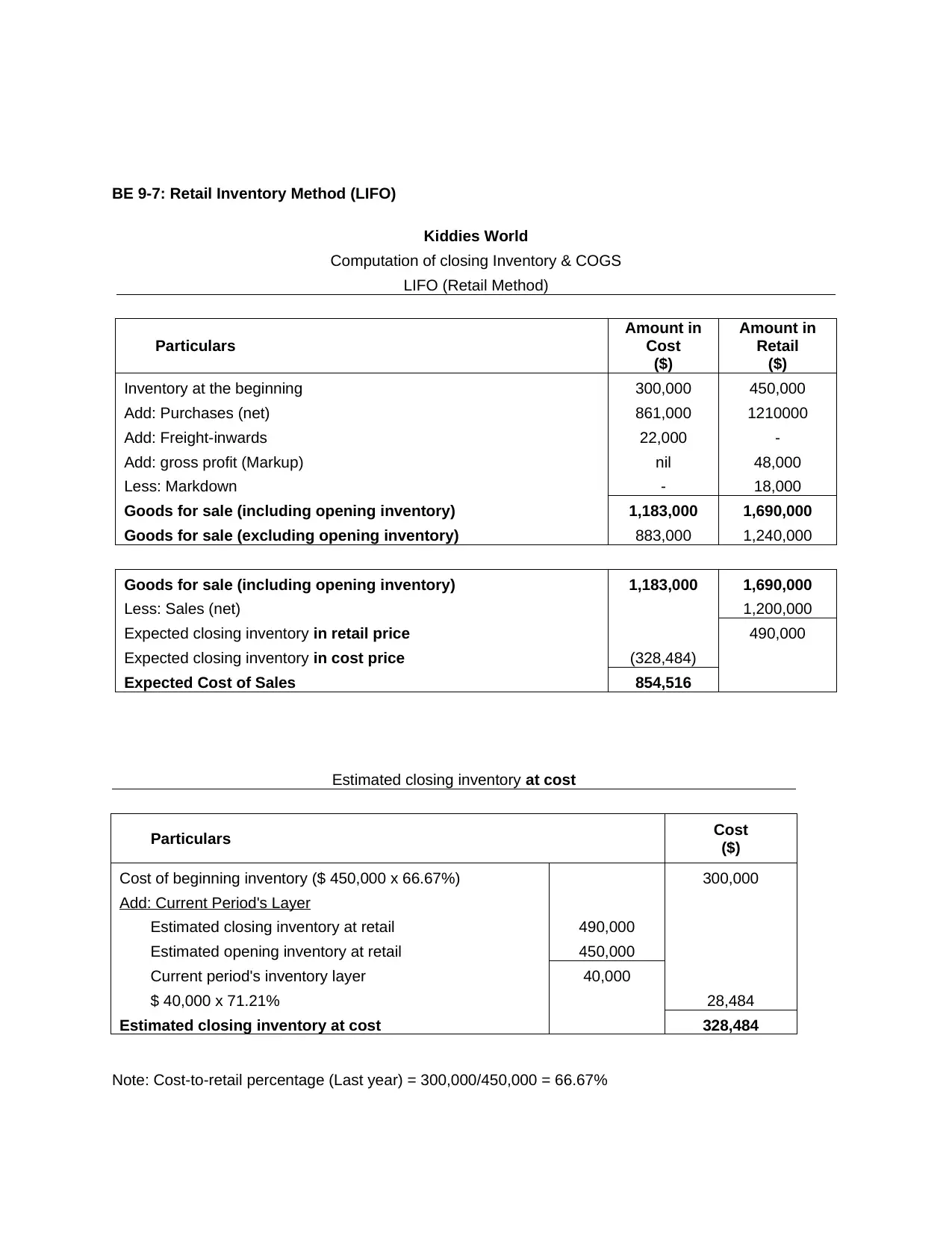

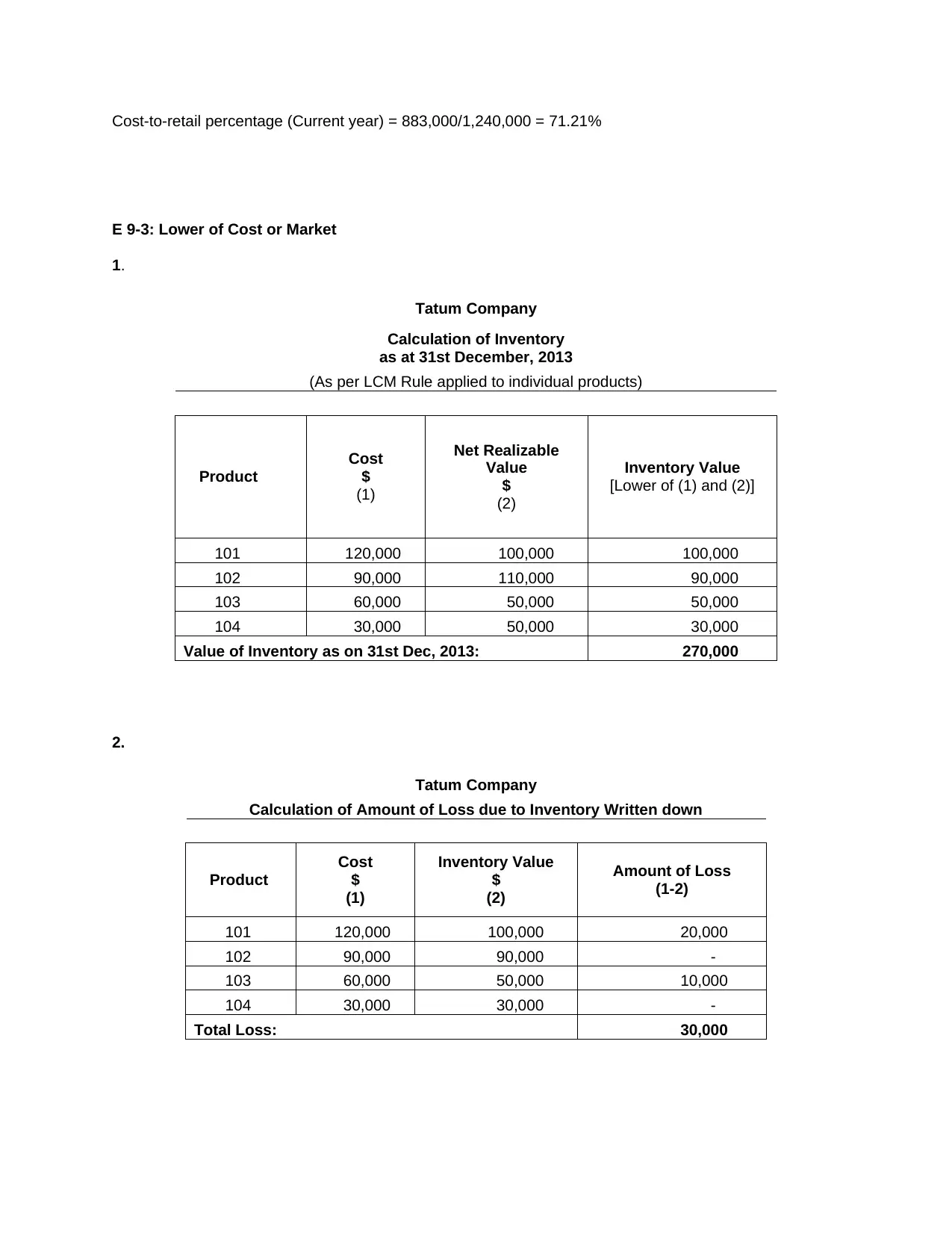

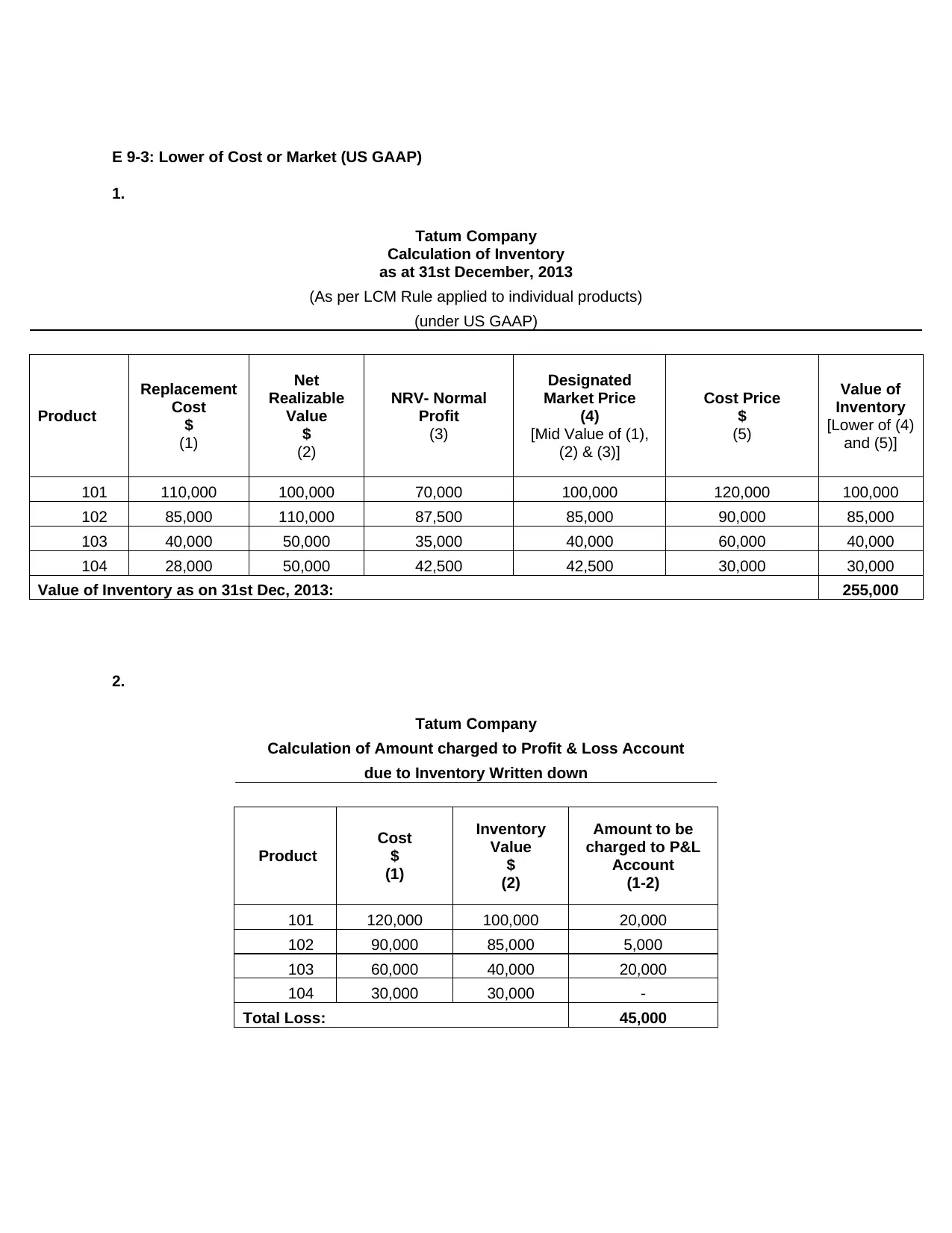

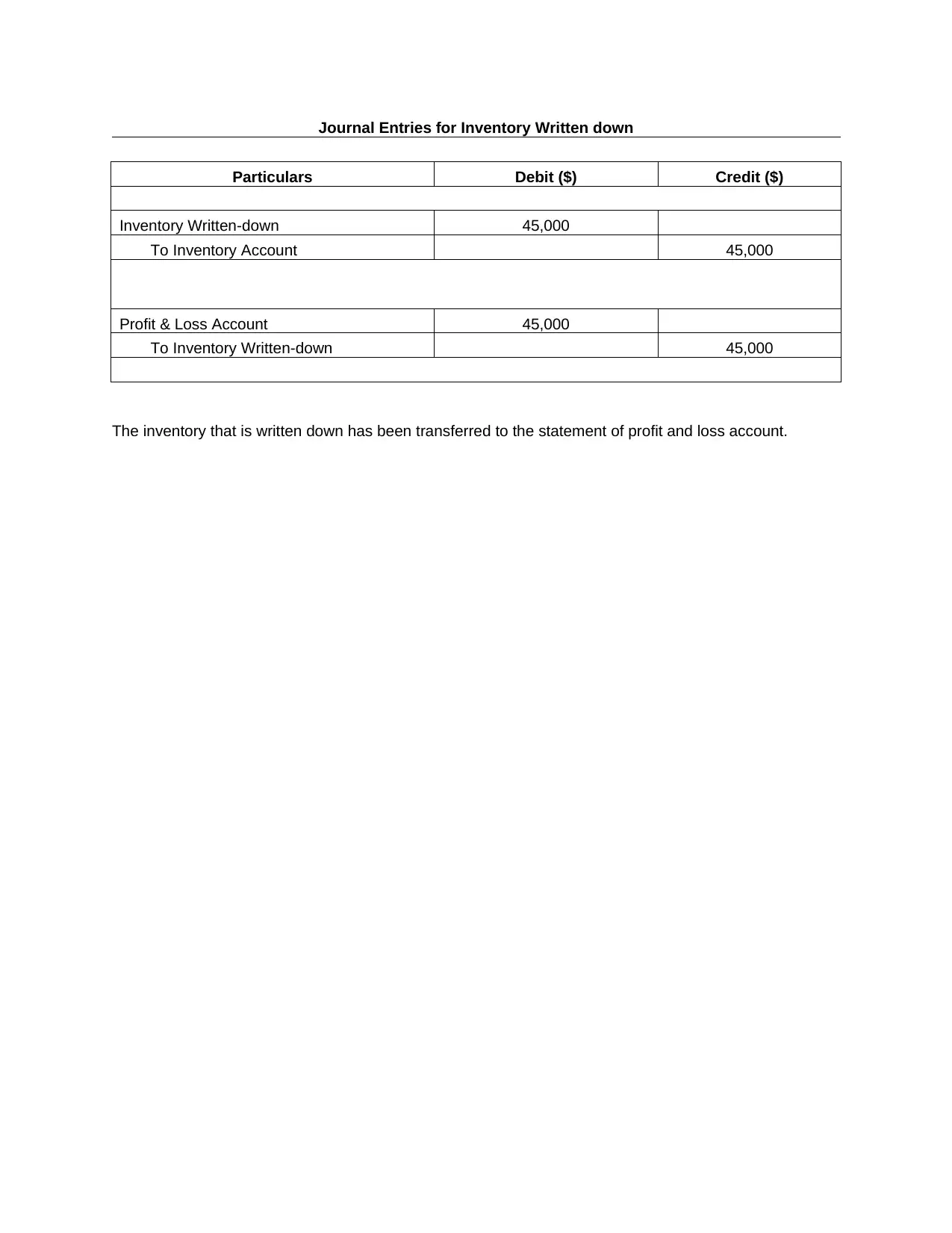

This document presents solutions for Homework 3 of the Intermediate Accounting I course (ACCT 3311), covering key concepts from Chapters 7, 8, and 9. The assignment includes detailed calculations and journal entries related to cash and cash equivalents, including the determination of the cash balance and items excluded from the calculation. It also addresses sales returns, inventory valuation using both perpetual and periodic inventory systems, and calculation of missing figures within the periodic inventory system. Furthermore, the solutions demonstrate the retail method of inventory valuation (average cost and LIFO), and the application of the lower of cost or market (LCM) rule, including its application under both IFRS and US GAAP. The document contains journal entries, calculations, and explanations to provide comprehensive solutions to the homework problems.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.