Intermediate Management Accounting Case Study: Financial Analysis

VerifiedAdded on 2023/04/19

|14

|2267

|106

Case Study

AI Summary

This case study provides a comprehensive analysis of intermediate management accounting principles, focusing on cost allocation methods and break-even analysis. The scenario involves Digital Electronics, a New Zealand manufacturer, and its Canadian subsidiary producing two products, Delta 1 and Delta 2. Part I examines traditional cost allocation, calculating break-even sales volume and target profit achievement. It identifies issues in fixed versus variable cost bifurcation and offers quantitative analysis. Part II explores activity-based costing (ABC) for more accurate overhead allocation, identifying cost drivers and recalculating product costs. The study concludes that careful process analysis is crucial for precise indirect manufacturing overhead allocation, essential for informed budgeting and decision-making. The complete solution is available on Desklib.

Intermediate Management

Accounting

Accounting

Assignment

Accounting

Accounting

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prepared By

Student’s Name:

Date:

Page 1

Student’s Name:

Date:

Page 1

Table of Contents

Introduction................................................................................................................ 3

Background................................................................................................................ 4

Main Body................................................................................................................... 4

Part-I........................................................................................................................... 4

Issue Identification..................................................................................................... 4

Identification of Key Success Factors.........................................................................5

Identification of Alternatives...................................................................................... 5

Quantitative Analysis.................................................................................................. 5

Recommendation....................................................................................................... 7

Part-II.......................................................................................................................... 8

Issue Identification..................................................................................................... 8

Identification of Key Success Factors.........................................................................8

Identification of Alternatives...................................................................................... 8

Quantitative Analysis.................................................................................................. 8

Answer to Question No.1............................................................................................ 8

Recommendation..................................................................................................... 12

Conclusion................................................................................................................ 12

References................................................................................................................... 13

Page 2

Introduction................................................................................................................ 3

Background................................................................................................................ 4

Main Body................................................................................................................... 4

Part-I........................................................................................................................... 4

Issue Identification..................................................................................................... 4

Identification of Key Success Factors.........................................................................5

Identification of Alternatives...................................................................................... 5

Quantitative Analysis.................................................................................................. 5

Recommendation....................................................................................................... 7

Part-II.......................................................................................................................... 8

Issue Identification..................................................................................................... 8

Identification of Key Success Factors.........................................................................8

Identification of Alternatives...................................................................................... 8

Quantitative Analysis.................................................................................................. 8

Answer to Question No.1............................................................................................ 8

Recommendation..................................................................................................... 12

Conclusion................................................................................................................ 12

References................................................................................................................... 13

Page 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The basis of allocation of indirect overheads is one of the most important factors in the process

of budget preparation as wrong allocation can result into the erroneous budget estimate. As per

the conventional method of Budget preparation there are primarily two main methods for the

allocation of the indirect manufacturing overheads relating to the product, which are known as

Traditional method of allocation and the allocation based on the activity-based costing. To have

an in-depth idea on the practical application and implication of these methodologies, a case study

divided into two parts has been selected in which the first part shows the application of the

Traditional based allocation of the manufacturing overhead and the second part reflects the use

of activity-based costing.

Background

Digital Electronics, a large New Zealand manufacturer of transmission equipment through its

one of the subsidiaries in Canada started production of the two-different product naming Delta 1

and the Delta 2. For which in the first part of our case study it was decided by its controller Dana

Boar to treat some expenses specifically as variable and rest as fixed on the basis of which

Break-even sales volume and the desired sales volume to earn the target profit is required to be

computed (Pamela & Tamara, 2013). Whereas in the second part she recognized the relevance of

the activity based costing and after making the requisite changes in the allocation procedure

using the ABC, the cost of the aforesaid products has been recalculated (Johan, 2018).

Main Body

Part-I

Issue Identification

In this case it is to be decided that what should be the Break-even sales volume of each of the

products naming Delta 1 and Delta 2, being manufactured by the subsidiary of the Digital

Electronics and the determination of the level of sales volume for the Subsidiary so as to ensure

that the target profit of $210000 as set by the Digital Electronics (parent Company) should be

achieved (Cundill, Smart, & Wilson, 2017).

The major problem in this case is that the break-even sales volume needs the correct estimation

of the fixed cost as well as the variable cost, to decide the correct amount of the contribution,

which are to be put finally in the formula to calculate the break-even sales and the desired

Page 3

The basis of allocation of indirect overheads is one of the most important factors in the process

of budget preparation as wrong allocation can result into the erroneous budget estimate. As per

the conventional method of Budget preparation there are primarily two main methods for the

allocation of the indirect manufacturing overheads relating to the product, which are known as

Traditional method of allocation and the allocation based on the activity-based costing. To have

an in-depth idea on the practical application and implication of these methodologies, a case study

divided into two parts has been selected in which the first part shows the application of the

Traditional based allocation of the manufacturing overhead and the second part reflects the use

of activity-based costing.

Background

Digital Electronics, a large New Zealand manufacturer of transmission equipment through its

one of the subsidiaries in Canada started production of the two-different product naming Delta 1

and the Delta 2. For which in the first part of our case study it was decided by its controller Dana

Boar to treat some expenses specifically as variable and rest as fixed on the basis of which

Break-even sales volume and the desired sales volume to earn the target profit is required to be

computed (Pamela & Tamara, 2013). Whereas in the second part she recognized the relevance of

the activity based costing and after making the requisite changes in the allocation procedure

using the ABC, the cost of the aforesaid products has been recalculated (Johan, 2018).

Main Body

Part-I

Issue Identification

In this case it is to be decided that what should be the Break-even sales volume of each of the

products naming Delta 1 and Delta 2, being manufactured by the subsidiary of the Digital

Electronics and the determination of the level of sales volume for the Subsidiary so as to ensure

that the target profit of $210000 as set by the Digital Electronics (parent Company) should be

achieved (Cundill, Smart, & Wilson, 2017).

The major problem in this case is that the break-even sales volume needs the correct estimation

of the fixed cost as well as the variable cost, to decide the correct amount of the contribution,

which are to be put finally in the formula to calculate the break-even sales and the desired

Page 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

volume of sales to earn the target profit. Hence in the given case the wrong bifurcation of the

expenses between fixed and variable overhead shall provide the wrong amount of the BEP sales

volume and the desired sales volume to achieve the target profit (Charles H, Giovanna, Dennis

M, & Robin W, 2015).

Identification of Key Success Factors

In the given case Dana Boar, the controller of the Digital Electronics has clearly mentioned that

the costs that are to be considered variable are Parts, direct labor and the supplies and rest of the

manufacturing costs are to be treated as fixed manufacturing cost. Hence keeping this factor as a

base, the quantitative solution to the problem is to be made.

Identification of Alternatives

In the given situation as the solution of the problem is quantitative one, hence there are no such

alternatives available to be analyzed and directly moving towards the Quantitative solution to the

problem.

Quantitative Analysis

Answer to question No. 1

Break-even sales Volume

= Fixed cost/Weighted average selling price**-weighted average variable expenses*

=$91000/$21.10-$10.98

=8992.10 units

= 8992 Units

Delta 1 Delta 2

Hence the breakeven sales volume= 8992*2/3 8992*1/3

= 5995 units 2997 units

Page 4

expenses between fixed and variable overhead shall provide the wrong amount of the BEP sales

volume and the desired sales volume to achieve the target profit (Charles H, Giovanna, Dennis

M, & Robin W, 2015).

Identification of Key Success Factors

In the given case Dana Boar, the controller of the Digital Electronics has clearly mentioned that

the costs that are to be considered variable are Parts, direct labor and the supplies and rest of the

manufacturing costs are to be treated as fixed manufacturing cost. Hence keeping this factor as a

base, the quantitative solution to the problem is to be made.

Identification of Alternatives

In the given situation as the solution of the problem is quantitative one, hence there are no such

alternatives available to be analyzed and directly moving towards the Quantitative solution to the

problem.

Quantitative Analysis

Answer to question No. 1

Break-even sales Volume

= Fixed cost/Weighted average selling price**-weighted average variable expenses*

=$91000/$21.10-$10.98

=8992.10 units

= 8992 Units

Delta 1 Delta 2

Hence the breakeven sales volume= 8992*2/3 8992*1/3

= 5995 units 2997 units

Page 4

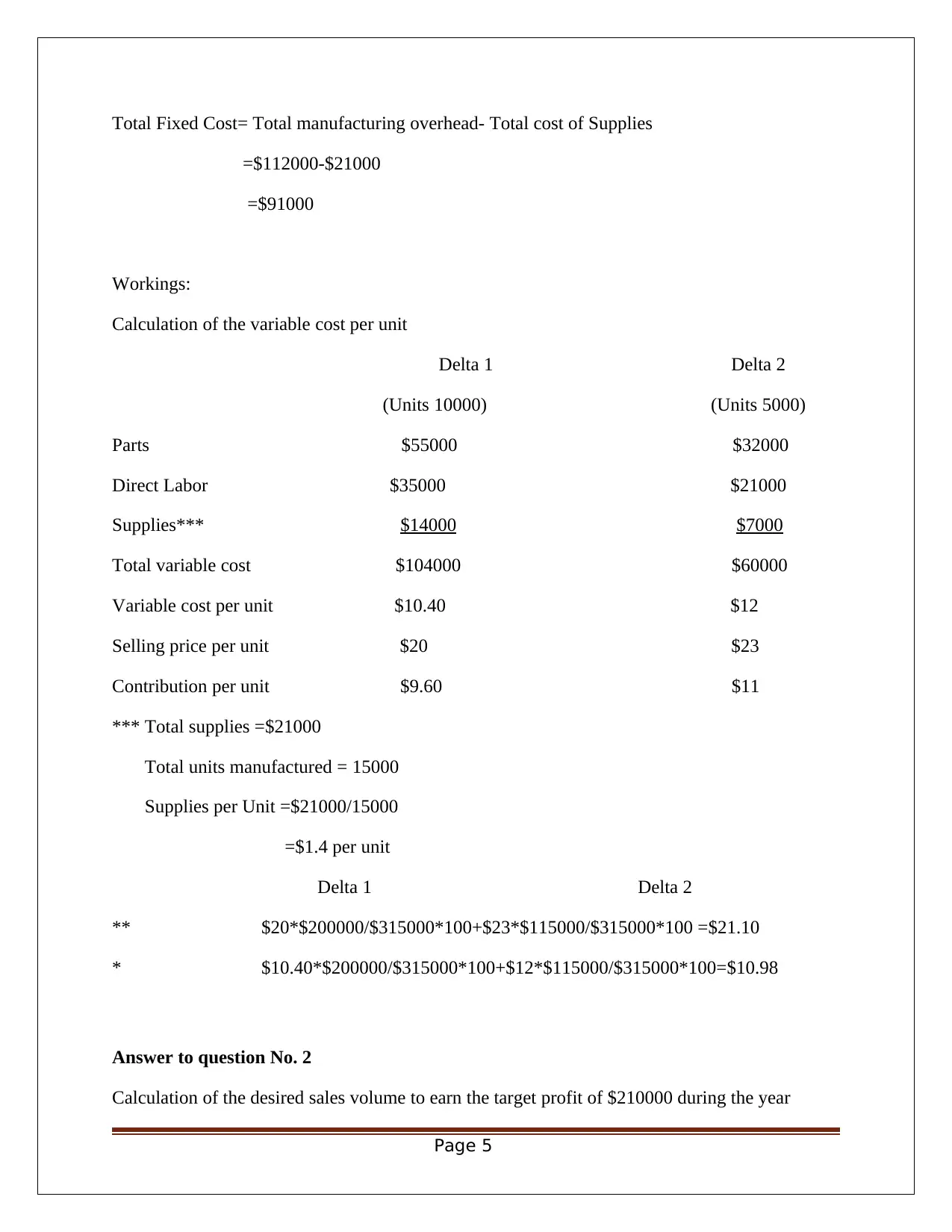

Total Fixed Cost= Total manufacturing overhead- Total cost of Supplies

=$112000-$21000

=$91000

Workings:

Calculation of the variable cost per unit

Delta 1 Delta 2

(Units 10000) (Units 5000)

Parts $55000 $32000

Direct Labor $35000 $21000

Supplies*** $14000 $7000

Total variable cost $104000 $60000

Variable cost per unit $10.40 $12

Selling price per unit $20 $23

Contribution per unit $9.60 $11

*** Total supplies =$21000

Total units manufactured = 15000

Supplies per Unit =$21000/15000

=$1.4 per unit

Delta 1 Delta 2

** $20*$200000/$315000*100+$23*$115000/$315000*100 =$21.10

* $10.40*$200000/$315000*100+$12*$115000/$315000*100=$10.98

Answer to question No. 2

Calculation of the desired sales volume to earn the target profit of $210000 during the year

Page 5

=$112000-$21000

=$91000

Workings:

Calculation of the variable cost per unit

Delta 1 Delta 2

(Units 10000) (Units 5000)

Parts $55000 $32000

Direct Labor $35000 $21000

Supplies*** $14000 $7000

Total variable cost $104000 $60000

Variable cost per unit $10.40 $12

Selling price per unit $20 $23

Contribution per unit $9.60 $11

*** Total supplies =$21000

Total units manufactured = 15000

Supplies per Unit =$21000/15000

=$1.4 per unit

Delta 1 Delta 2

** $20*$200000/$315000*100+$23*$115000/$315000*100 =$21.10

* $10.40*$200000/$315000*100+$12*$115000/$315000*100=$10.98

Answer to question No. 2

Calculation of the desired sales volume to earn the target profit of $210000 during the year

Page 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

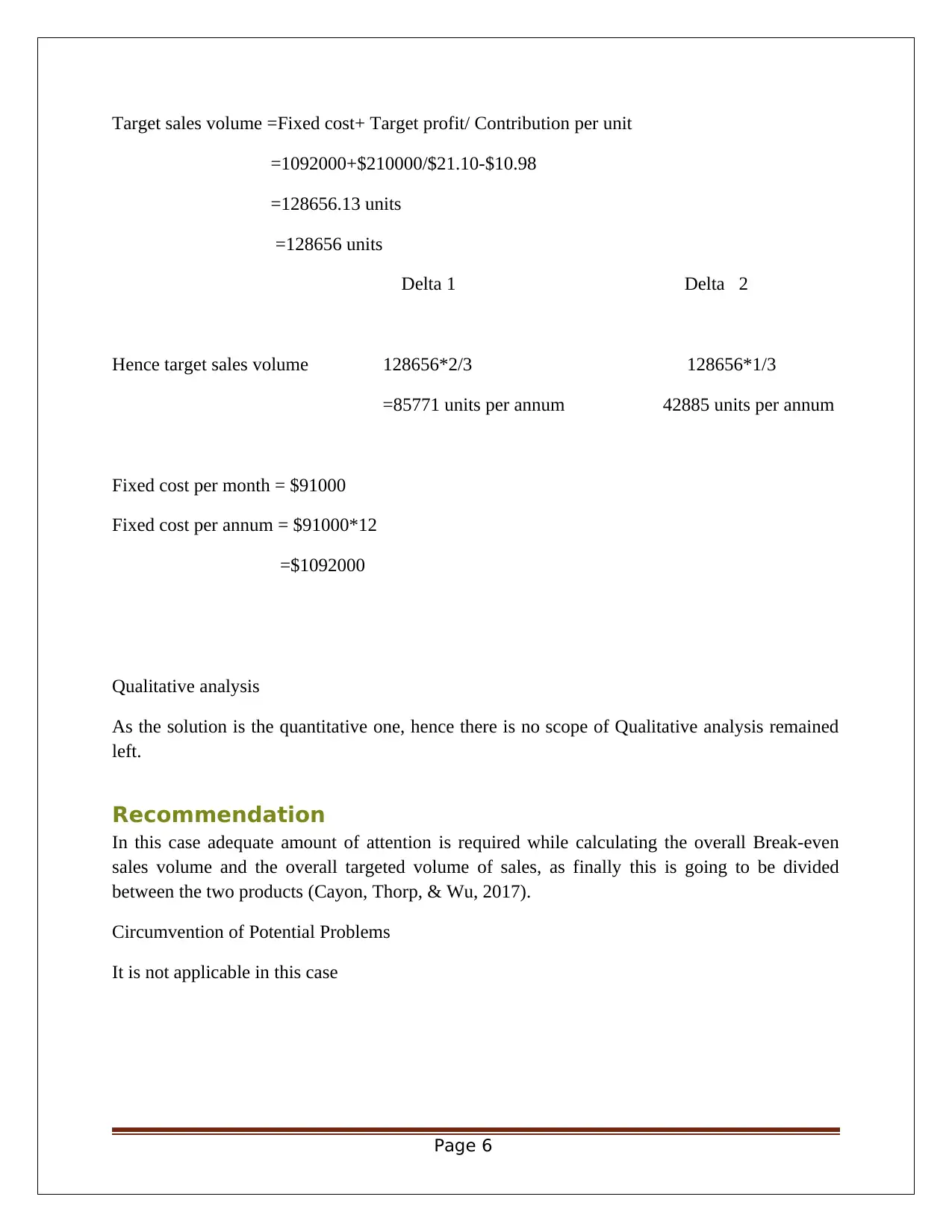

Target sales volume =Fixed cost+ Target profit/ Contribution per unit

=1092000+$210000/$21.10-$10.98

=128656.13 units

=128656 units

Delta 1 Delta 2

Hence target sales volume 128656*2/3 128656*1/3

=85771 units per annum 42885 units per annum

Fixed cost per month = $91000

Fixed cost per annum = $91000*12

=$1092000

Qualitative analysis

As the solution is the quantitative one, hence there is no scope of Qualitative analysis remained

left.

Recommendation

In this case adequate amount of attention is required while calculating the overall Break-even

sales volume and the overall targeted volume of sales, as finally this is going to be divided

between the two products (Cayon, Thorp, & Wu, 2017).

Circumvention of Potential Problems

It is not applicable in this case

Page 6

=1092000+$210000/$21.10-$10.98

=128656.13 units

=128656 units

Delta 1 Delta 2

Hence target sales volume 128656*2/3 128656*1/3

=85771 units per annum 42885 units per annum

Fixed cost per month = $91000

Fixed cost per annum = $91000*12

=$1092000

Qualitative analysis

As the solution is the quantitative one, hence there is no scope of Qualitative analysis remained

left.

Recommendation

In this case adequate amount of attention is required while calculating the overall Break-even

sales volume and the overall targeted volume of sales, as finally this is going to be divided

between the two products (Cayon, Thorp, & Wu, 2017).

Circumvention of Potential Problems

It is not applicable in this case

Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part-II

Issue Identification

In the second part Dana Boar, the controller of the Digital Electronics has recognized the

relevance of the activity based costing and found that the basis as chosen in the first part for the

allocation of the indirect manufacturing overhead is erroneous, hence now the problem is to

select the appropriate cost driver for each of the indirect manufacturing overhead and then

reallocating these overheads accordingly (Boghossian, 2017).

Identification of Key Success Factors

In this step the controller identified the three major activities or processes being carried over to

manufacture both products and hence decided that except for the supplies other indirect

manufacturing overheads are to be distributed as per the direct labor hour consumed by these

three major processes naming fabrication, assembly and packing and shipping.

Identification of Alternatives

In the given situation as the solution of the problem is quantitative one, hence there are no such

alternatives available to be analyzed and directly moving towards the Quantitative solution to the

problem (Abdullah & Said, 2017).

Quantitative Analysis

Answer to Question No.1

Statement showing the product cost

Delta 1 Delta 2

(Per Unit in $) (Per unit in $)

Parts 5.5 6.4

Direct labor 3.5 4.2

Page 7

Issue Identification

In the second part Dana Boar, the controller of the Digital Electronics has recognized the

relevance of the activity based costing and found that the basis as chosen in the first part for the

allocation of the indirect manufacturing overhead is erroneous, hence now the problem is to

select the appropriate cost driver for each of the indirect manufacturing overhead and then

reallocating these overheads accordingly (Boghossian, 2017).

Identification of Key Success Factors

In this step the controller identified the three major activities or processes being carried over to

manufacture both products and hence decided that except for the supplies other indirect

manufacturing overheads are to be distributed as per the direct labor hour consumed by these

three major processes naming fabrication, assembly and packing and shipping.

Identification of Alternatives

In the given situation as the solution of the problem is quantitative one, hence there are no such

alternatives available to be analyzed and directly moving towards the Quantitative solution to the

problem (Abdullah & Said, 2017).

Quantitative Analysis

Answer to Question No.1

Statement showing the product cost

Delta 1 Delta 2

(Per Unit in $) (Per unit in $)

Parts 5.5 6.4

Direct labor 3.5 4.2

Page 7

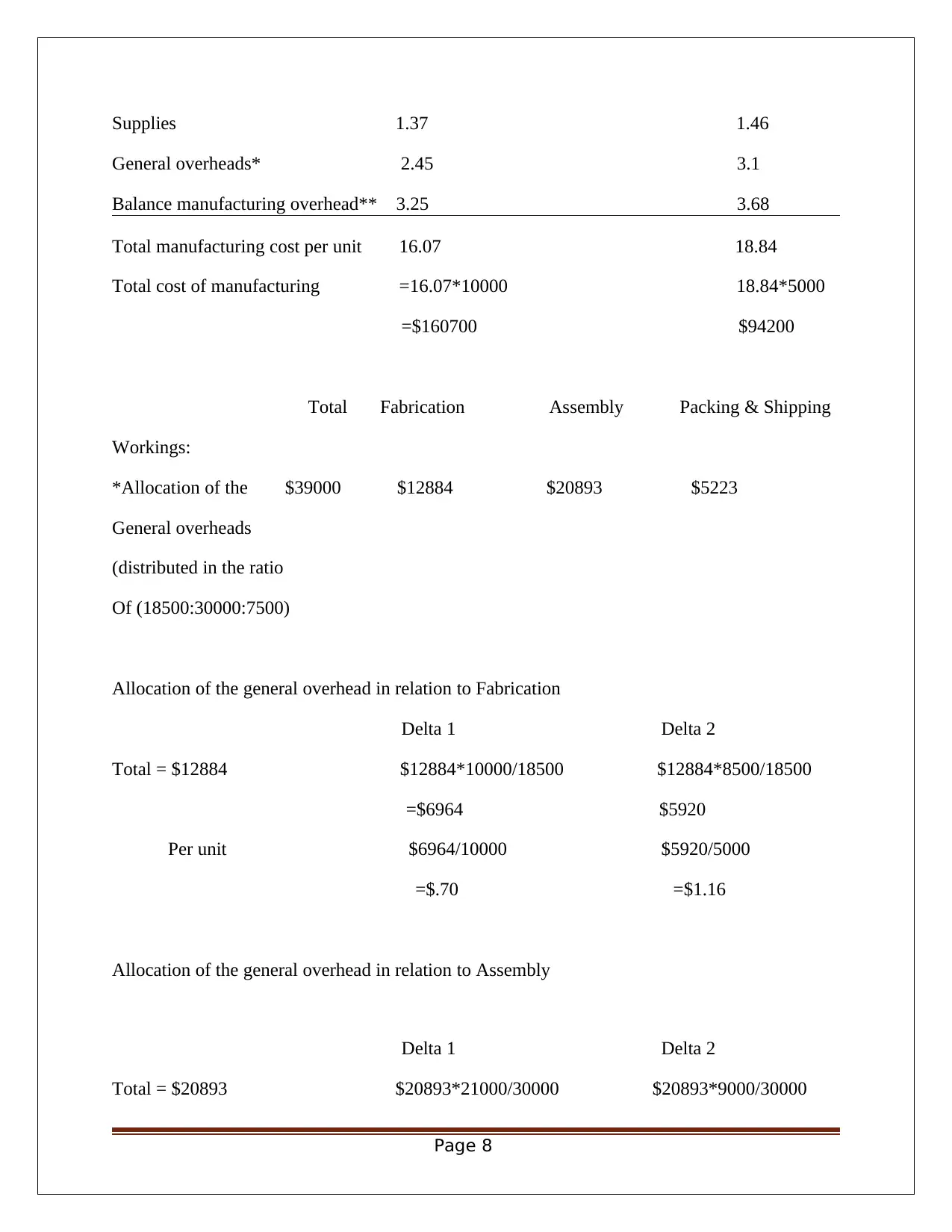

Supplies 1.37 1.46

General overheads* 2.45 3.1

Balance manufacturing overhead** 3.25 3.68

Total manufacturing cost per unit 16.07 18.84

Total cost of manufacturing =16.07*10000 18.84*5000

=$160700 $94200

Total Fabrication Assembly Packing & Shipping

Workings:

*Allocation of the $39000 $12884 $20893 $5223

General overheads

(distributed in the ratio

Of (18500:30000:7500)

Allocation of the general overhead in relation to Fabrication

Delta 1 Delta 2

Total = $12884 $12884*10000/18500 $12884*8500/18500

=$6964 $5920

Per unit $6964/10000 $5920/5000

=$.70 =$1.16

Allocation of the general overhead in relation to Assembly

Delta 1 Delta 2

Total = $20893 $20893*21000/30000 $20893*9000/30000

Page 8

General overheads* 2.45 3.1

Balance manufacturing overhead** 3.25 3.68

Total manufacturing cost per unit 16.07 18.84

Total cost of manufacturing =16.07*10000 18.84*5000

=$160700 $94200

Total Fabrication Assembly Packing & Shipping

Workings:

*Allocation of the $39000 $12884 $20893 $5223

General overheads

(distributed in the ratio

Of (18500:30000:7500)

Allocation of the general overhead in relation to Fabrication

Delta 1 Delta 2

Total = $12884 $12884*10000/18500 $12884*8500/18500

=$6964 $5920

Per unit $6964/10000 $5920/5000

=$.70 =$1.16

Allocation of the general overhead in relation to Assembly

Delta 1 Delta 2

Total = $20893 $20893*21000/30000 $20893*9000/30000

Page 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

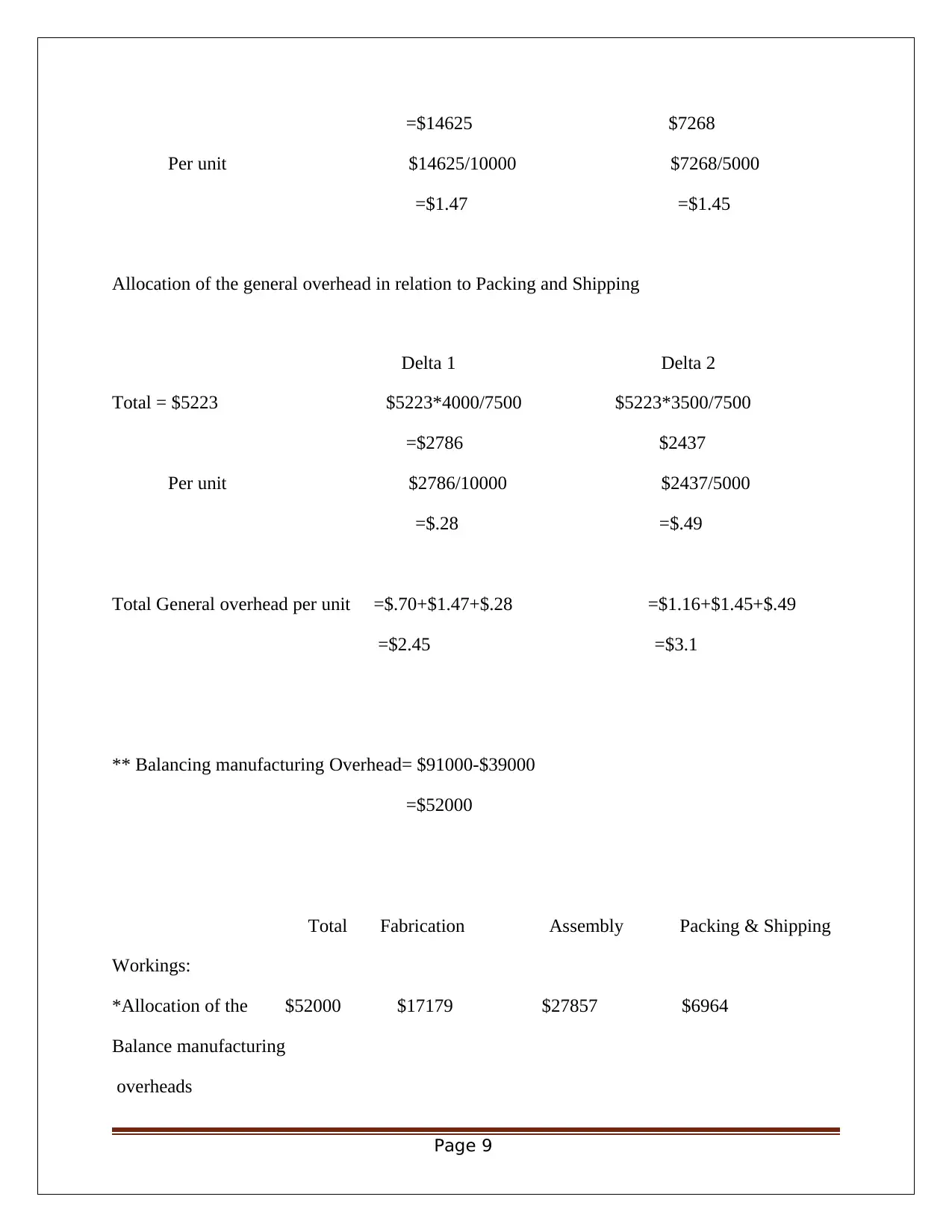

=$14625 $7268

Per unit $14625/10000 $7268/5000

=$1.47 =$1.45

Allocation of the general overhead in relation to Packing and Shipping

Delta 1 Delta 2

Total = $5223 $5223*4000/7500 $5223*3500/7500

=$2786 $2437

Per unit $2786/10000 $2437/5000

=$.28 =$.49

Total General overhead per unit =$.70+$1.47+$.28 =$1.16+$1.45+$.49

=$2.45 =$3.1

** Balancing manufacturing Overhead= $91000-$39000

=$52000

Total Fabrication Assembly Packing & Shipping

Workings:

*Allocation of the $52000 $17179 $27857 $6964

Balance manufacturing

overheads

Page 9

Per unit $14625/10000 $7268/5000

=$1.47 =$1.45

Allocation of the general overhead in relation to Packing and Shipping

Delta 1 Delta 2

Total = $5223 $5223*4000/7500 $5223*3500/7500

=$2786 $2437

Per unit $2786/10000 $2437/5000

=$.28 =$.49

Total General overhead per unit =$.70+$1.47+$.28 =$1.16+$1.45+$.49

=$2.45 =$3.1

** Balancing manufacturing Overhead= $91000-$39000

=$52000

Total Fabrication Assembly Packing & Shipping

Workings:

*Allocation of the $52000 $17179 $27857 $6964

Balance manufacturing

overheads

Page 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

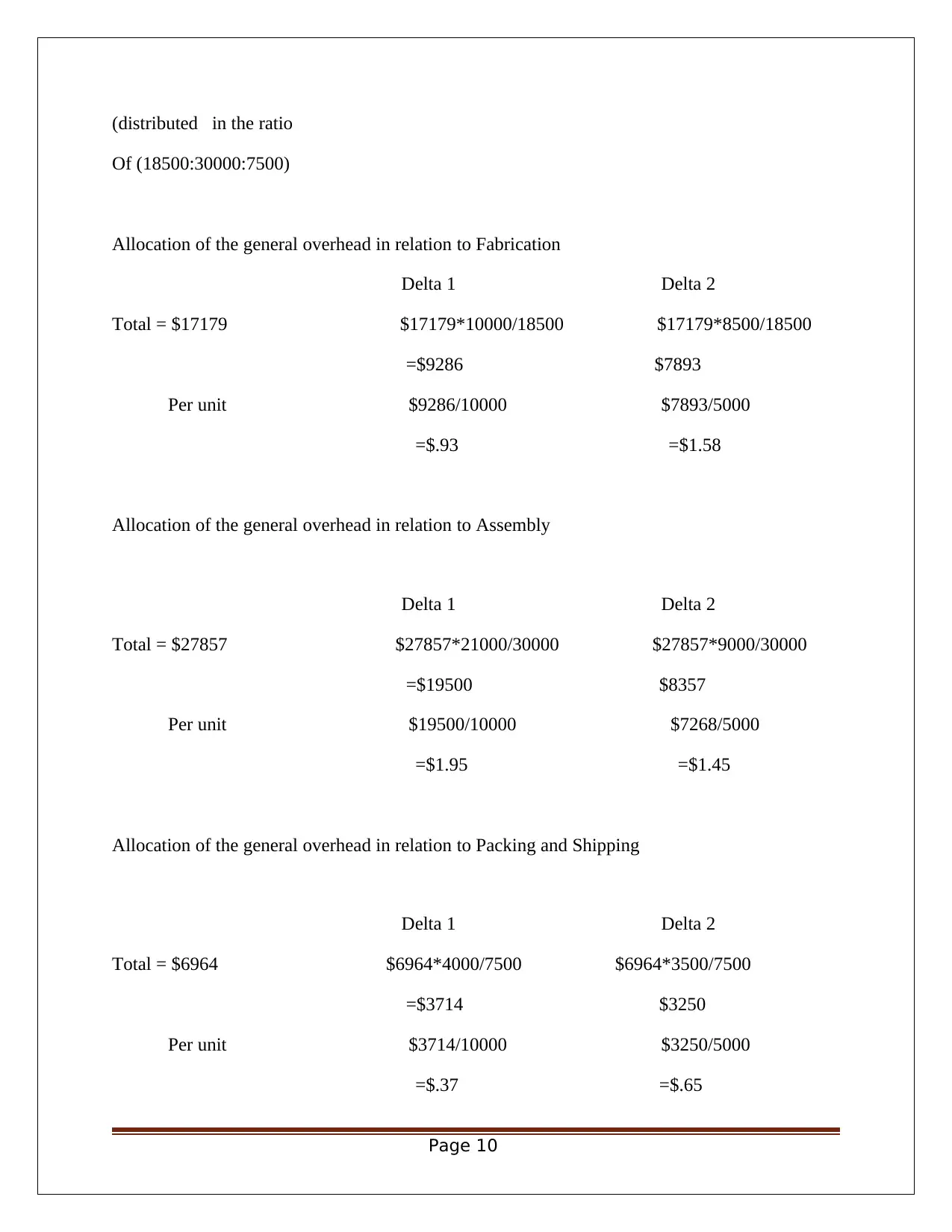

(distributed in the ratio

Of (18500:30000:7500)

Allocation of the general overhead in relation to Fabrication

Delta 1 Delta 2

Total = $17179 $17179*10000/18500 $17179*8500/18500

=$9286 $7893

Per unit $9286/10000 $7893/5000

=$.93 =$1.58

Allocation of the general overhead in relation to Assembly

Delta 1 Delta 2

Total = $27857 $27857*21000/30000 $27857*9000/30000

=$19500 $8357

Per unit $19500/10000 $7268/5000

=$1.95 =$1.45

Allocation of the general overhead in relation to Packing and Shipping

Delta 1 Delta 2

Total = $6964 $6964*4000/7500 $6964*3500/7500

=$3714 $3250

Per unit $3714/10000 $3250/5000

=$.37 =$.65

Page 10

Of (18500:30000:7500)

Allocation of the general overhead in relation to Fabrication

Delta 1 Delta 2

Total = $17179 $17179*10000/18500 $17179*8500/18500

=$9286 $7893

Per unit $9286/10000 $7893/5000

=$.93 =$1.58

Allocation of the general overhead in relation to Assembly

Delta 1 Delta 2

Total = $27857 $27857*21000/30000 $27857*9000/30000

=$19500 $8357

Per unit $19500/10000 $7268/5000

=$1.95 =$1.45

Allocation of the general overhead in relation to Packing and Shipping

Delta 1 Delta 2

Total = $6964 $6964*4000/7500 $6964*3500/7500

=$3714 $3250

Per unit $3714/10000 $3250/5000

=$.37 =$.65

Page 10

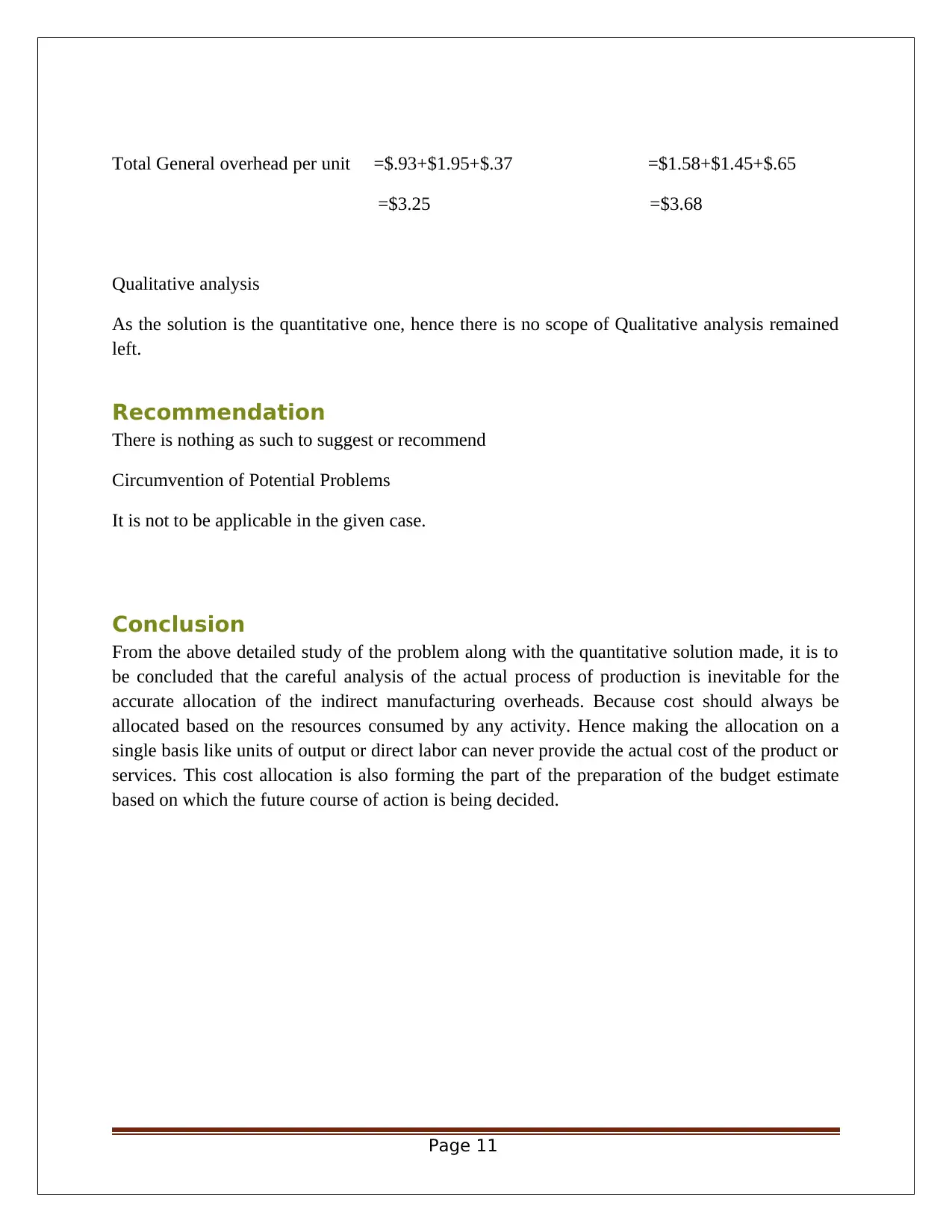

Total General overhead per unit =$.93+$1.95+$.37 =$1.58+$1.45+$.65

=$3.25 =$3.68

Qualitative analysis

As the solution is the quantitative one, hence there is no scope of Qualitative analysis remained

left.

Recommendation

There is nothing as such to suggest or recommend

Circumvention of Potential Problems

It is not to be applicable in the given case.

Conclusion

From the above detailed study of the problem along with the quantitative solution made, it is to

be concluded that the careful analysis of the actual process of production is inevitable for the

accurate allocation of the indirect manufacturing overheads. Because cost should always be

allocated based on the resources consumed by any activity. Hence making the allocation on a

single basis like units of output or direct labor can never provide the actual cost of the product or

services. This cost allocation is also forming the part of the preparation of the budget estimate

based on which the future course of action is being decided.

Page 11

=$3.25 =$3.68

Qualitative analysis

As the solution is the quantitative one, hence there is no scope of Qualitative analysis remained

left.

Recommendation

There is nothing as such to suggest or recommend

Circumvention of Potential Problems

It is not to be applicable in the given case.

Conclusion

From the above detailed study of the problem along with the quantitative solution made, it is to

be concluded that the careful analysis of the actual process of production is inevitable for the

accurate allocation of the indirect manufacturing overheads. Because cost should always be

allocated based on the resources consumed by any activity. Hence making the allocation on a

single basis like units of output or direct labor can never provide the actual cost of the product or

services. This cost allocation is also forming the part of the preparation of the budget estimate

based on which the future course of action is being decided.

Page 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.