Internal Audit Function and Corporate Governance in Libyan Context

VerifiedAdded on 2021/06/17

|25

|6963

|106

Report

AI Summary

This report provides a comprehensive overview of the internal audit function and its crucial role in corporate governance, particularly within the context of Libya. It begins with an introduction outlining the scope and objectives of the study, followed by an exploration of the conceptual evolution of internal audit, its definitions, and its significance within corporations. The report delves into the theoretical perspectives underpinning internal audit and corporate governance, focusing on agency theory and stewardship theory, analyzing their impacts, costs, and significance. It then examines the development and implementation of a well-aligned internal audit strategy, emphasizing the importance of risk assessment and internal controls. Finally, the report investigates the role of the internal audit function in the development of corporate governance codes, highlighting its contribution to ethical practices, accountability, and effective management. The report also includes a literature review summarizing relevant studies and findings, providing a solid foundation for understanding the complexities and importance of internal audit in contemporary business environments.

Running head: INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Internal Audit Function and the Development of Corporate Governance Code in Libya

University Name

Student Name

Authors’ Note

Internal Audit Function and the Development of Corporate Governance Code in Libya

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Table of Contents

1. Introduction............................................................................................................................2

2. Notions of internal audit within a corporation.......................................................................2

3. Theoretical Perspective of internal audit function and corporate governance.......................7

3. 1 Agency Theory as a theory of Corporate Governance........................................................7

3.1.1 Costs of agency model on corporate governance..........................................................9

3.1.2 Significance of agency model on corporate governance.............................................10

3.1.3 Effects of agency model on corporate governance.....................................................10

3.2 Stewardship Theory of Corporate Governance..................................................................10

3.2.1 Impacts of Stewardship Theory of Corporate Governance on Employees.................12

3.2.2 Particular Influence of Stewardship Theory of Corporate Governance on Clients....12

3.2.3 General consequence of Stewardship Theory of Corporate Governance...................12

4. Developing and implementing well-aligned internal audit strategy....................................13

5. Role of internal audit function in development of corporate governance code...................14

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Table of Contents

1. Introduction............................................................................................................................2

2. Notions of internal audit within a corporation.......................................................................2

3. Theoretical Perspective of internal audit function and corporate governance.......................7

3. 1 Agency Theory as a theory of Corporate Governance........................................................7

3.1.1 Costs of agency model on corporate governance..........................................................9

3.1.2 Significance of agency model on corporate governance.............................................10

3.1.3 Effects of agency model on corporate governance.....................................................10

3.2 Stewardship Theory of Corporate Governance..................................................................10

3.2.1 Impacts of Stewardship Theory of Corporate Governance on Employees.................12

3.2.2 Particular Influence of Stewardship Theory of Corporate Governance on Clients....12

3.2.3 General consequence of Stewardship Theory of Corporate Governance...................12

4. Developing and implementing well-aligned internal audit strategy....................................13

5. Role of internal audit function in development of corporate governance code...................14

3

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Literature Review

1. Introduction

The current study delivers a comprehensive image of the internal audit purpose. This

necessarily views the conceptual evolution of theory of internal audit, and illustrates the

necessity for the same, descriptions of the term, and the way it is inevitable to different

entities’ internal audit function operates within. In essence, this runs deeply into the prior

studies that are necessarily directly associated to the topic under consideration and delivers

their findings. This can aid the process of ascertainment of beginning point of the current

study. The present study intends to illustrate and design a conceptual framework and evaluate

overall nature and exercise of the internal audit function within companies in Libya.

2. Notions of internal audit within a corporation

Conceptual approaches concerning internal auditing

Griffiths (2016) indicates that there is a comprehensive image of the internal audit function.

The study views the conceptual transformation of the internal audit function and illustrates

the requirement for the same, descriptions of the terms and the way it is necessary to different

entities. The activities of internal auditing emerged as well as designed owing to value to

specific recipients and owing to potential of fulfilling specific requirements of different users.

Eulerich et al. (2015) assert that the activity of internal auditing is of great importance and

the article recommends specifying significance of the association between specifically section

of accounting as well as assessment. Internal auditing can be considered to be of strategic

significance, as managers, along with the Board of Directors of the reporting unit, can

understand that till there is an appropriate internal structure of control, a few error as well as

failures can be examined and eradicated in a well timed method.

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Literature Review

1. Introduction

The current study delivers a comprehensive image of the internal audit purpose. This

necessarily views the conceptual evolution of theory of internal audit, and illustrates the

necessity for the same, descriptions of the term, and the way it is inevitable to different

entities’ internal audit function operates within. In essence, this runs deeply into the prior

studies that are necessarily directly associated to the topic under consideration and delivers

their findings. This can aid the process of ascertainment of beginning point of the current

study. The present study intends to illustrate and design a conceptual framework and evaluate

overall nature and exercise of the internal audit function within companies in Libya.

2. Notions of internal audit within a corporation

Conceptual approaches concerning internal auditing

Griffiths (2016) indicates that there is a comprehensive image of the internal audit function.

The study views the conceptual transformation of the internal audit function and illustrates

the requirement for the same, descriptions of the terms and the way it is necessary to different

entities. The activities of internal auditing emerged as well as designed owing to value to

specific recipients and owing to potential of fulfilling specific requirements of different users.

Eulerich et al. (2015) assert that the activity of internal auditing is of great importance and

the article recommends specifying significance of the association between specifically section

of accounting as well as assessment. Internal auditing can be considered to be of strategic

significance, as managers, along with the Board of Directors of the reporting unit, can

understand that till there is an appropriate internal structure of control, a few error as well as

failures can be examined and eradicated in a well timed method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

The Board of Directors of the company necessarily give the impression auditing that is

internal in nature as an act for enhancing the action, in addition to an act of searching for as

well as detecting faults as well as wrongdoing. Therefore, amplification of auditing concept

that is internal in nature, and over and above than that, elucidation of the role that internal

auditing essentially plays today, is crucial. As suggested by Salvioni and Astori (2015), there

are several scholars from the specific ground have analysed the advancement of internal

auditing at the global level as well as nationwide level. A more strong utilization of the

expression audit is discovered during period of economic crisis from the period 1929, given

that then role as well as requirement of internal auditing endlessly augmented, a fact that

directed to the corporation along with standardisation of exercises of internal auditing by way

of institution in the year 1941 in Orlando, USA, of principally the Institute of Internal

Auditors (abbreviated as IIA), to which, at the instant, in excess of 120 nations are associated.

As recommended by Alzeban and Gwilliam (2014), internal audit necessarily had a

significant role within corporate governance ever since the period 1940. It certainly became

more imperative with passage of time. Ever since the period of 1940, several transformations

have taken place as regards internal auditing that was regulated by means of diverse norms as

well as corporate governance codes. McAlister and Ferrell (2016) takes into account the fact

that there are diverse basic actions of internal auditing are registered include analysis of risk,

making certain organization within the entity as well as ensuring conformity.

During the year 1942, Lenz and Hahn (2015) asserts that the first president of the entity

International Institute of Internal Auditors, announced an surprising forecast that majority of

excellent standpoint of internal auditing shall be the “managerial backing”. During the year

1991, Joseph J. Mossis that is the president of the “Institute of Internal Auditors” of Britain,

started again the same comment, however in a more a precise manner. In essence, it is quite

clear for the ones that operate within “Internal Auditing function” that this necessarily plays

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

The Board of Directors of the company necessarily give the impression auditing that is

internal in nature as an act for enhancing the action, in addition to an act of searching for as

well as detecting faults as well as wrongdoing. Therefore, amplification of auditing concept

that is internal in nature, and over and above than that, elucidation of the role that internal

auditing essentially plays today, is crucial. As suggested by Salvioni and Astori (2015), there

are several scholars from the specific ground have analysed the advancement of internal

auditing at the global level as well as nationwide level. A more strong utilization of the

expression audit is discovered during period of economic crisis from the period 1929, given

that then role as well as requirement of internal auditing endlessly augmented, a fact that

directed to the corporation along with standardisation of exercises of internal auditing by way

of institution in the year 1941 in Orlando, USA, of principally the Institute of Internal

Auditors (abbreviated as IIA), to which, at the instant, in excess of 120 nations are associated.

As recommended by Alzeban and Gwilliam (2014), internal audit necessarily had a

significant role within corporate governance ever since the period 1940. It certainly became

more imperative with passage of time. Ever since the period of 1940, several transformations

have taken place as regards internal auditing that was regulated by means of diverse norms as

well as corporate governance codes. McAlister and Ferrell (2016) takes into account the fact

that there are diverse basic actions of internal auditing are registered include analysis of risk,

making certain organization within the entity as well as ensuring conformity.

During the year 1942, Lenz and Hahn (2015) asserts that the first president of the entity

International Institute of Internal Auditors, announced an surprising forecast that majority of

excellent standpoint of internal auditing shall be the “managerial backing”. During the year

1991, Joseph J. Mossis that is the president of the “Institute of Internal Auditors” of Britain,

started again the same comment, however in a more a precise manner. In essence, it is quite

clear for the ones that operate within “Internal Auditing function” that this necessarily plays

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

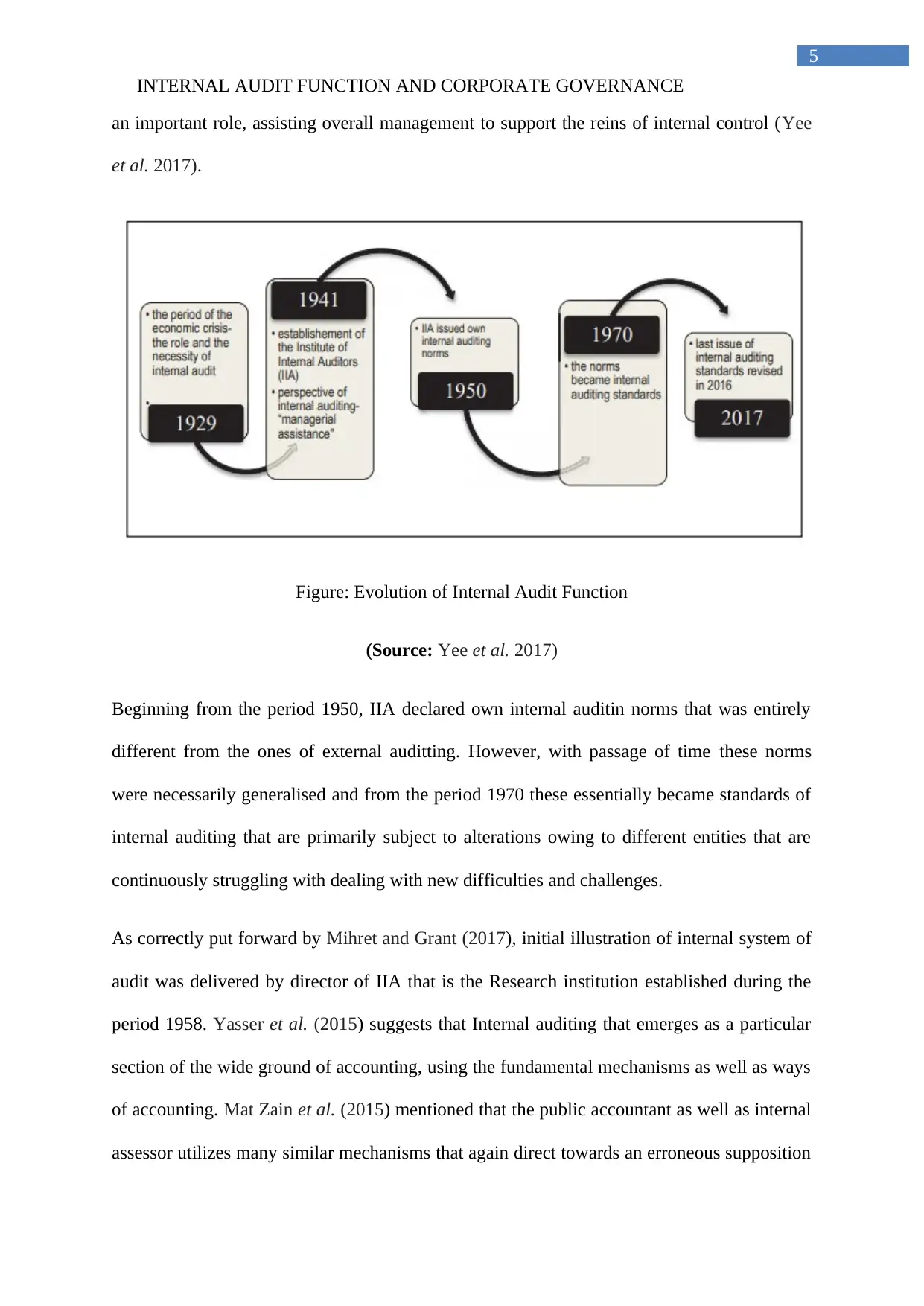

an important role, assisting overall management to support the reins of internal control (Yee

et al. 2017).

Figure: Evolution of Internal Audit Function

(Source: Yee et al. 2017)

Beginning from the period 1950, IIA declared own internal auditin norms that was entirely

different from the ones of external auditting. However, with passage of time these norms

were necessarily generalised and from the period 1970 these essentially became standards of

internal auditing that are primarily subject to alterations owing to different entities that are

continuously struggling with dealing with new difficulties and challenges.

As correctly put forward by Mihret and Grant (2017), initial illustration of internal system of

audit was delivered by director of IIA that is the Research institution established during the

period 1958. Yasser et al. (2015) suggests that Internal auditing that emerges as a particular

section of the wide ground of accounting, using the fundamental mechanisms as well as ways

of accounting. Mat Zain et al. (2015) mentioned that the public accountant as well as internal

assessor utilizes many similar mechanisms that again direct towards an erroneous supposition

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

an important role, assisting overall management to support the reins of internal control (Yee

et al. 2017).

Figure: Evolution of Internal Audit Function

(Source: Yee et al. 2017)

Beginning from the period 1950, IIA declared own internal auditin norms that was entirely

different from the ones of external auditting. However, with passage of time these norms

were necessarily generalised and from the period 1970 these essentially became standards of

internal auditing that are primarily subject to alterations owing to different entities that are

continuously struggling with dealing with new difficulties and challenges.

As correctly put forward by Mihret and Grant (2017), initial illustration of internal system of

audit was delivered by director of IIA that is the Research institution established during the

period 1958. Yasser et al. (2015) suggests that Internal auditing that emerges as a particular

section of the wide ground of accounting, using the fundamental mechanisms as well as ways

of accounting. Mat Zain et al. (2015) mentioned that the public accountant as well as internal

assessor utilizes many similar mechanisms that again direct towards an erroneous supposition

6

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

that there subsists minute inconsistency in firm’s operation. Essentially, firm’s internal

assessor, similar to any evaluator, is worried regarding evaluation of legitimacy of depiction.

However, as regards the current case under consideration, the illustration with which

particular evaluator is disturbed takes into account fairly broader choice. Also, there is

requirement to accomplish different themes in which the association to particular accounting

items is frequently to some extent isolated. Also, the internal assessor is relatively more

intensely concerned in assisting to carrying out the operations profitably (Christopher 2015).

As recommended by El-Kassar et al. (2014), internal auditing can be referred to as

Professional rules declared by the “Institute of Audit and Internal Control”. This rule refers to

a specific purpose along with independent activities that confer to a business concern an

cover concerning the stage of specific controls regarding different functions. This shows the

way to the business concern and helps in enhancement of business functions that in turn can

add plus value. In addition to this, this has the requirement to be state that internal audit also

assists the business concern to attain its aims since the same evaluates the administrative

process, controls in addition to processes of governance. However, there exists a risk to

which the business concern is exposed. In addition to this, internal audit presents

explanations and solutions for enhancement of effectiveness of these procedures, or else to

mask drawbacks (Ruud 2013).

As mentioned by Alzeban (2015), internal auditing action appreciates and directs the

corporate governance procedure, in a bid to achieve particular aims associated to ethics,

accountability as well as effectiveness in management. Fundamentally, in this regard, it can

be said that for the purpose of tracking and making certain compliance to the pertinent code

of corporate governance. Essentially, it is crucial to illustrate the notion of corporate

governance. In particular, corporate governance as per OECD, reflects different procedures

according to which a corporation is directed and at the same time controlled (Drogalas et al.

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

that there subsists minute inconsistency in firm’s operation. Essentially, firm’s internal

assessor, similar to any evaluator, is worried regarding evaluation of legitimacy of depiction.

However, as regards the current case under consideration, the illustration with which

particular evaluator is disturbed takes into account fairly broader choice. Also, there is

requirement to accomplish different themes in which the association to particular accounting

items is frequently to some extent isolated. Also, the internal assessor is relatively more

intensely concerned in assisting to carrying out the operations profitably (Christopher 2015).

As recommended by El-Kassar et al. (2014), internal auditing can be referred to as

Professional rules declared by the “Institute of Audit and Internal Control”. This rule refers to

a specific purpose along with independent activities that confer to a business concern an

cover concerning the stage of specific controls regarding different functions. This shows the

way to the business concern and helps in enhancement of business functions that in turn can

add plus value. In addition to this, this has the requirement to be state that internal audit also

assists the business concern to attain its aims since the same evaluates the administrative

process, controls in addition to processes of governance. However, there exists a risk to

which the business concern is exposed. In addition to this, internal audit presents

explanations and solutions for enhancement of effectiveness of these procedures, or else to

mask drawbacks (Ruud 2013).

As mentioned by Alzeban (2015), internal auditing action appreciates and directs the

corporate governance procedure, in a bid to achieve particular aims associated to ethics,

accountability as well as effectiveness in management. Fundamentally, in this regard, it can

be said that for the purpose of tracking and making certain compliance to the pertinent code

of corporate governance. Essentially, it is crucial to illustrate the notion of corporate

governance. In particular, corporate governance as per OECD, reflects different procedures

according to which a corporation is directed and at the same time controlled (Drogalas et al.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

2016). There are different aspects of corporate governance attained distribution of powers as

well as obligations between mainly the Board of Director, firm’s managers, different

shareholders as well as stakeholders, in order to make certain coordination of diverse actions

and attainment of objectives of the business concern.

The report published by Preda reveals the fact that companies registered at different stock

exchange believes that corporate governance is essentially the outcome of specific norms,

varied traditions along with behavioural themes designed by each and every system of

legislative (Jiang et al. 2017). As published by IIA during the period of July in the year 2006

in their guide on Organisational Governance directed for Internal Auditors of the firm, the

association between internal auditing as well as its advisory service role can be essentially

strengthened in definite aspects of principally corporate governance.

As suggested by Jiang et al. (2017), internal auditing primarily has a more significant part

since the declaration of the law that is the Sarbanes Oxley Law on apparition. Although the

directives stipulated under this Sarbanes Oxley Law do not necessarily attend to the definite

role of the internal auditing mainly within corporate governance of businesses, but there are

different obligations of corporate governance for mainly the audit committees as well as

external auditors and there are also recommendations as regards the significance of internal

auditing. Nickell and Roberts (2014) assert that progression of internal audit indicates

towards orientation towards enhancement of the effectiveness of management of risk,

escalating satisfaction level of stakeholders, improvement of the capabilities that different

internal assessors need to have, mounting concern in enumerating and analysing overall

performance of internal audit. These studies also talk about enhancement of the level of

progression of technology in the studies of internal audit (Lenz et al. 2014). In recent times,

internal evaluators have also participated more and more in different works of functional

auditing, management of risk, several internal controls, and specific requirements of

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

2016). There are different aspects of corporate governance attained distribution of powers as

well as obligations between mainly the Board of Director, firm’s managers, different

shareholders as well as stakeholders, in order to make certain coordination of diverse actions

and attainment of objectives of the business concern.

The report published by Preda reveals the fact that companies registered at different stock

exchange believes that corporate governance is essentially the outcome of specific norms,

varied traditions along with behavioural themes designed by each and every system of

legislative (Jiang et al. 2017). As published by IIA during the period of July in the year 2006

in their guide on Organisational Governance directed for Internal Auditors of the firm, the

association between internal auditing as well as its advisory service role can be essentially

strengthened in definite aspects of principally corporate governance.

As suggested by Jiang et al. (2017), internal auditing primarily has a more significant part

since the declaration of the law that is the Sarbanes Oxley Law on apparition. Although the

directives stipulated under this Sarbanes Oxley Law do not necessarily attend to the definite

role of the internal auditing mainly within corporate governance of businesses, but there are

different obligations of corporate governance for mainly the audit committees as well as

external auditors and there are also recommendations as regards the significance of internal

auditing. Nickell and Roberts (2014) assert that progression of internal audit indicates

towards orientation towards enhancement of the effectiveness of management of risk,

escalating satisfaction level of stakeholders, improvement of the capabilities that different

internal assessors need to have, mounting concern in enumerating and analysing overall

performance of internal audit. These studies also talk about enhancement of the level of

progression of technology in the studies of internal audit (Lenz et al. 2014). In recent times,

internal evaluators have also participated more and more in different works of functional

auditing, management of risk, several internal controls, and specific requirements of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

governance as well as IT notions. As such, it is extremely crucial to monitor the direction in

which function of internal auditing shall head towards in the upcoming period.

3. Theoretical Perspective of internal audit function and corporate governance

Nickell and Roberts (2014) suggested that corporate governance can be considered as

oversight of policies, processes as well as exercises. This oversight aids to make certain that

the business concern is exercised in the best interests of the firm as well as its shareholders.

The procedures of handling corporate governance are normally handled by a board of

directors. In addition to this, business concern might employ different staff of assessors to

examine and scrutinize internal controls.

Ackermann and Marx (2016) mentioned that the ultimate accountability for corporate

governance in majority of business concerns lies directly with the board of directors. In

essence, internal assessors are mainly charged with making certain that corporate procedures

along with related controls are functioning as intended.

3. 1 Agency Theory as a theory of Corporate Governance

Baharud-din et al. (2014) advocates that agency theory indicates towards issues of directors

that control firms and shareholders own the business concern. Agency theory considers this

specific subject matter into account for preventing the same. As per Tsai et al. (2015), the

main notion of agency notion is that a specific agent gets recruited by primarily the principle

to keeping on the task and the agency is the association between mainly agent as well as the

principle. In addition to this, agency costs are mainly provided by the principle for the

purpose of controlling overall behaviour of the agency owing of deficiency of trust in the

conviction of the agents. Al-Matari et al. (2014) suggests that it is important to assume the

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

governance as well as IT notions. As such, it is extremely crucial to monitor the direction in

which function of internal auditing shall head towards in the upcoming period.

3. Theoretical Perspective of internal audit function and corporate governance

Nickell and Roberts (2014) suggested that corporate governance can be considered as

oversight of policies, processes as well as exercises. This oversight aids to make certain that

the business concern is exercised in the best interests of the firm as well as its shareholders.

The procedures of handling corporate governance are normally handled by a board of

directors. In addition to this, business concern might employ different staff of assessors to

examine and scrutinize internal controls.

Ackermann and Marx (2016) mentioned that the ultimate accountability for corporate

governance in majority of business concerns lies directly with the board of directors. In

essence, internal assessors are mainly charged with making certain that corporate procedures

along with related controls are functioning as intended.

3. 1 Agency Theory as a theory of Corporate Governance

Baharud-din et al. (2014) advocates that agency theory indicates towards issues of directors

that control firms and shareholders own the business concern. Agency theory considers this

specific subject matter into account for preventing the same. As per Tsai et al. (2015), the

main notion of agency notion is that a specific agent gets recruited by primarily the principle

to keeping on the task and the agency is the association between mainly agent as well as the

principle. In addition to this, agency costs are mainly provided by the principle for the

purpose of controlling overall behaviour of the agency owing of deficiency of trust in the

conviction of the agents. Al-Matari et al. (2014) suggests that it is important to assume the

9

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

assignment on behalf of different agents and in this case agent becomes liable to that specific

principle. Fundamentally, there is three different segregations of ownership as well as

control; namely principal (referring to shareholders of a firm), agents (indicating to the

directors of a firm) and task under consideration (indicating towards management of the

corporation) (Lee 2017).

In essence, the agency theory aids business enterprises to develop the corporate governance

and this necessarily starts off with the business enterprises owned as well as managed by the

same individuals. However, in the following phase, it necessarily expands the entire business

by means of contributions of requisite financiers. As such, these individuals can be

essentially the shareholders having restricted liability. Thereafter, in the subsequent stage, it

delegates the responsibility of continuing the operations of the business to principally

managers of the firm (referring to the agents). Further, in the following stage, the business

undertakes separation of business goals. Martin (2015) mention that separation/ division of

business ownership can show the way to probable notions between firm’s directors, firm’s

shareholders along with relationship with principal-agent that can be handled with different

codes of corporate governance.

Ali and Ahmad (2017) suggested that agency theory comparative to corporate governance

supposes a two-tier sketch of firm control and this includes managers as well as owners.

Again, agency theory supports the view that there might be some sort of friction as well as

doubt between these two different groups. As such, the fundamental framework of the

business concern, thus, is the netting of contractual associations among diverse interest

groups having a stake in the business concern.

On the whole, there are essentially three different clusters of interest groups within the

business concern namely, Managers, shareholders as well as creditors (primarily the banks).

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

assignment on behalf of different agents and in this case agent becomes liable to that specific

principle. Fundamentally, there is three different segregations of ownership as well as

control; namely principal (referring to shareholders of a firm), agents (indicating to the

directors of a firm) and task under consideration (indicating towards management of the

corporation) (Lee 2017).

In essence, the agency theory aids business enterprises to develop the corporate governance

and this necessarily starts off with the business enterprises owned as well as managed by the

same individuals. However, in the following phase, it necessarily expands the entire business

by means of contributions of requisite financiers. As such, these individuals can be

essentially the shareholders having restricted liability. Thereafter, in the subsequent stage, it

delegates the responsibility of continuing the operations of the business to principally

managers of the firm (referring to the agents). Further, in the following stage, the business

undertakes separation of business goals. Martin (2015) mention that separation/ division of

business ownership can show the way to probable notions between firm’s directors, firm’s

shareholders along with relationship with principal-agent that can be handled with different

codes of corporate governance.

Ali and Ahmad (2017) suggested that agency theory comparative to corporate governance

supposes a two-tier sketch of firm control and this includes managers as well as owners.

Again, agency theory supports the view that there might be some sort of friction as well as

doubt between these two different groups. As such, the fundamental framework of the

business concern, thus, is the netting of contractual associations among diverse interest

groups having a stake in the business concern.

On the whole, there are essentially three different clusters of interest groups within the

business concern namely, Managers, shareholders as well as creditors (primarily the banks).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Setiawan and Djajadikerta (2017) asserts that shareholders often have disagreements with

both banks as well as managers, because their common priorities are unlike. Managers hunt

for quick profits that amplify their own riches, power and status, whilst shareholders are

further fascinated in unhurried and stable growth over period. The rationale of agency theory

is to recognize points of disagreement among corporate clusters of interest groups. As such,

Banks intend to lessen risk whilst shareholders wish for to reasonably maximization of

profits. Managers are relatively more risky in the area of profit maximization, as their careers

are founded on the capability to generate proceeds and present the results to the board. In

essence, this fact that contemporary corporations are founded on these associations that

generates costs and each and every group has the intent to control the other (Ravjee and Marx

2015).

3.1.1 Costs of agency model on corporate governance

One of the most important insights of essentially agency theory is the notion of costs of

keeping up with the labour division among various credit holders, varied shareholders as well

as managers. In essence, managers necessarily have the benefit of information, as they

understand close up of the firm. Also, they can necessarily utilize this for enhancement of

their own status at the cost of shareholders. Restricting overall control of different managers

itself involves costs (namely decreased profits), whilst profit seeking in various risky

ventures might possibly alienate different banks along with other financial institutions (Al-

Matari et al. 2017). Keeping track and restricting managers itself also involves now and then

considerable amounts of costs to the business concern.

3.1.2 Significance of agency model on corporate governance

As suggested by Ruud (2013), agency model on corporate governance upholds the view that

that business enterprises are principally units of disagreement in place of unitary, profit-

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

Setiawan and Djajadikerta (2017) asserts that shareholders often have disagreements with

both banks as well as managers, because their common priorities are unlike. Managers hunt

for quick profits that amplify their own riches, power and status, whilst shareholders are

further fascinated in unhurried and stable growth over period. The rationale of agency theory

is to recognize points of disagreement among corporate clusters of interest groups. As such,

Banks intend to lessen risk whilst shareholders wish for to reasonably maximization of

profits. Managers are relatively more risky in the area of profit maximization, as their careers

are founded on the capability to generate proceeds and present the results to the board. In

essence, this fact that contemporary corporations are founded on these associations that

generates costs and each and every group has the intent to control the other (Ravjee and Marx

2015).

3.1.1 Costs of agency model on corporate governance

One of the most important insights of essentially agency theory is the notion of costs of

keeping up with the labour division among various credit holders, varied shareholders as well

as managers. In essence, managers necessarily have the benefit of information, as they

understand close up of the firm. Also, they can necessarily utilize this for enhancement of

their own status at the cost of shareholders. Restricting overall control of different managers

itself involves costs (namely decreased profits), whilst profit seeking in various risky

ventures might possibly alienate different banks along with other financial institutions (Al-

Matari et al. 2017). Keeping track and restricting managers itself also involves now and then

considerable amounts of costs to the business concern.

3.1.2 Significance of agency model on corporate governance

As suggested by Ruud (2013), agency model on corporate governance upholds the view that

that business enterprises are principally units of disagreement in place of unitary, profit-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

seeking equipment. This disagreement is not unusual but embedded within the framework of

contemporary business enterprises.

3.1.3 Effects of agency model on corporate governance

Drogalas et al. (2016) asserts that it is quite possible that in case if one accepts the notion of

agency theory, that business enterprises are in point of fact groups of associated fiefs.

Alzeban (2015) states that each one of the fief has own specific interest as well as culture and

opinions regarding the purpose of the firm in a different way. In evaluating the purpose of a

corporation, one can suppose that managers shall behave in a manner to make best use of

their own profit as well as reputation, even at the costs of firm’s shareholders. Also, one

might perhaps even comprehend the role of managers as one of institutionalized

deceitfulness, in which the irregularity of knowledge allows managers to function operate

with more or less total sovereignty.

3.2 Stewardship Theory of Corporate Governance

As suggested by Stewardship theory is regarding the manager who can operate as

accountable stewards of specific principle as well as assets that they manage (Jiang et al.

2017). Furthermore, stewardship theory can be considered as the alternative opinion of the

agency theory in which the managers are considered to act in their own eagerness. It can be

hereby mentioned that specified that stewardship is a definite mechanism to lessen loss of

agency. This strategy incorporated the compensation, retention policy of executives of the

firm, ascertaining different benefits as well as incentives of the managers of the corporation

by means of financial rewards and delivering shares by the process of maintenance of

alignment. In essence, this offers pecuniary interest to the members of the staffs and this can

inspire employees to perform better. Lenz et al. (2014) suggests that the steward can be

considered to be one who pays attention and looks after the requirements of others as well as

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

seeking equipment. This disagreement is not unusual but embedded within the framework of

contemporary business enterprises.

3.1.3 Effects of agency model on corporate governance

Drogalas et al. (2016) asserts that it is quite possible that in case if one accepts the notion of

agency theory, that business enterprises are in point of fact groups of associated fiefs.

Alzeban (2015) states that each one of the fief has own specific interest as well as culture and

opinions regarding the purpose of the firm in a different way. In evaluating the purpose of a

corporation, one can suppose that managers shall behave in a manner to make best use of

their own profit as well as reputation, even at the costs of firm’s shareholders. Also, one

might perhaps even comprehend the role of managers as one of institutionalized

deceitfulness, in which the irregularity of knowledge allows managers to function operate

with more or less total sovereignty.

3.2 Stewardship Theory of Corporate Governance

As suggested by Stewardship theory is regarding the manager who can operate as

accountable stewards of specific principle as well as assets that they manage (Jiang et al.

2017). Furthermore, stewardship theory can be considered as the alternative opinion of the

agency theory in which the managers are considered to act in their own eagerness. It can be

hereby mentioned that specified that stewardship is a definite mechanism to lessen loss of

agency. This strategy incorporated the compensation, retention policy of executives of the

firm, ascertaining different benefits as well as incentives of the managers of the corporation

by means of financial rewards and delivering shares by the process of maintenance of

alignment. In essence, this offers pecuniary interest to the members of the staffs and this can

inspire employees to perform better. Lenz et al. (2014) suggests that the steward can be

considered to be one who pays attention and looks after the requirements of others as well as

12

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

executives of the business enterprise intends to look after interest of firm’s shareholders and

they necessarily arrive at a decision regarding the business enterprise.

Whilst profit drives any sort of business, certain businesses might perhaps take into account

fraction of something greater. In essence, stewardship theory supports that ownership doesn’t

in reality own a business; it is only just holding it in a specific trust. As such, this reflects the

manner in which business. Nickell and Roberts (2014) suggests that the processes might

prove to be a medium for a advanced calling or else are devised to honour a initial vision of a

founder, therefore generating a profit that essentially takes a back seat to satisfying a social

standards of a company.

Ackermann and Marx (2016) put forward the view that stewardship models might perhaps

involve different environmental issues, in which a business thinks that it should function with

as slight influence as possible on the entire world. Again, other business concerns might

perhaps champion specific human else wise animal rights, abstaining from utilizing products

that necessarily are completed in sweatshops or else are examined on various live subjects.

However, there are still others who might honour religious beliefs of the owners and

represent themselves as servant leadership. In essence, these models have the tendency to be

prejudiced, with administration ascertaining boundary between socially accountable or

irresponsible behaviour (Baharud-din et al. 2014).

A business concern that is committed to a greater purpose shall attract clients who share the

same idea. Nevertheless, in case if the holders indicate towards stewardship else wise social

accountability in the area of corporate governance, company’s customers cautiously weigh

this alongside the manner in which the business concern actually function. Inconsistency

between words and action estrange base of the client (Tsai et al. 2015).

INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCE

executives of the business enterprise intends to look after interest of firm’s shareholders and

they necessarily arrive at a decision regarding the business enterprise.

Whilst profit drives any sort of business, certain businesses might perhaps take into account

fraction of something greater. In essence, stewardship theory supports that ownership doesn’t

in reality own a business; it is only just holding it in a specific trust. As such, this reflects the

manner in which business. Nickell and Roberts (2014) suggests that the processes might

prove to be a medium for a advanced calling or else are devised to honour a initial vision of a

founder, therefore generating a profit that essentially takes a back seat to satisfying a social

standards of a company.

Ackermann and Marx (2016) put forward the view that stewardship models might perhaps

involve different environmental issues, in which a business thinks that it should function with

as slight influence as possible on the entire world. Again, other business concerns might

perhaps champion specific human else wise animal rights, abstaining from utilizing products

that necessarily are completed in sweatshops or else are examined on various live subjects.

However, there are still others who might honour religious beliefs of the owners and

represent themselves as servant leadership. In essence, these models have the tendency to be

prejudiced, with administration ascertaining boundary between socially accountable or

irresponsible behaviour (Baharud-din et al. 2014).

A business concern that is committed to a greater purpose shall attract clients who share the

same idea. Nevertheless, in case if the holders indicate towards stewardship else wise social

accountability in the area of corporate governance, company’s customers cautiously weigh

this alongside the manner in which the business concern actually function. Inconsistency

between words and action estrange base of the client (Tsai et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.