Research Proposal: Internal Audit & Corporate Governance Code in Libya

VerifiedAdded on 2023/06/12

|13

|3241

|365

Report

AI Summary

This research proposal explores the relationship between the internal audit function and the development of corporate governance codes, with a specific focus on the context of Libya and Harouge Oil Operations. It introduces the concepts of corporate governance and internal audit, highlighting the importance of internal audit in risk management, control, and governance systems. The literature review examines the agency and stewardship theories of corporate governance, emphasizing the role of internal audit in developing and implementing well-aligned strategies. It also discusses the role of internal audit in developing corporate governance codes, emphasizing the importance of transparent arrangements, risk management, and internal control principles. The research adheres to ethical standards and relies on secondary data sources, ensuring data protection and integrity.

Running head: RESEARCH PROPOSAL

Research Proposal

Internal Audit Function & the Development of Corporate Governance Code

Student’s name:

Name of the university:

Author’s note:

Research Proposal

Internal Audit Function & the Development of Corporate Governance Code

Student’s name:

Name of the university:

Author’s note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RESEARCH PROPOSAL

1. Introduction

Corporate governance can be defined as oversight of the organisation's policies,

procedures and practices. This oversight assists the organisation to ensure the operation in

best interests of the organisation and its shareholders. In addition, this method of controlling

corporate governance is done by the Board of Directors and the management can employ the

internal auditors to monitor and test the internal control (Hayes 2017). In this research

proposal, the theory of corporate governance and the relationship between corporate

governance and internal audit will be explained. The purpose of the research proposal is to

explain the adoption, introduction and application of corporate governance code in Libya,

mainly in Harouge Oil Operations. Therefore, problem statement, aim and objectives of the

study will be identified. In addition, a literature review of the scholarly articles will be done

in order to establish a theoretical understanding of the study. In the methodology section, data

collection and analysis procedure will be discussed.

4. Literature Review

The concept of internal audit function within an organisation

Internal audit is an objective assurance, independent and consulting activity and it is

designed to provide value and develop a firm’s operations (Abbott et al. 2016). Internal audit

assists an organisation to accomplish its goals by creating a systematic as well as disciplined

approach to improve and evaluate the risk management, the effectiveness of the control and

governance systems. Internal audit can be defined as the catalyst for developing corporate

governance by giving recommendations and managerial insights. This analysis is mainly

done by assessment of business processes and data. As stated by Lenz and Hahn (2015), with

a commitment towards accountability and integrity; internal auditing can share value to

senior management as well as governing bodies as an objective source of service that is

1. Introduction

Corporate governance can be defined as oversight of the organisation's policies,

procedures and practices. This oversight assists the organisation to ensure the operation in

best interests of the organisation and its shareholders. In addition, this method of controlling

corporate governance is done by the Board of Directors and the management can employ the

internal auditors to monitor and test the internal control (Hayes 2017). In this research

proposal, the theory of corporate governance and the relationship between corporate

governance and internal audit will be explained. The purpose of the research proposal is to

explain the adoption, introduction and application of corporate governance code in Libya,

mainly in Harouge Oil Operations. Therefore, problem statement, aim and objectives of the

study will be identified. In addition, a literature review of the scholarly articles will be done

in order to establish a theoretical understanding of the study. In the methodology section, data

collection and analysis procedure will be discussed.

4. Literature Review

The concept of internal audit function within an organisation

Internal audit is an objective assurance, independent and consulting activity and it is

designed to provide value and develop a firm’s operations (Abbott et al. 2016). Internal audit

assists an organisation to accomplish its goals by creating a systematic as well as disciplined

approach to improve and evaluate the risk management, the effectiveness of the control and

governance systems. Internal audit can be defined as the catalyst for developing corporate

governance by giving recommendations and managerial insights. This analysis is mainly

done by assessment of business processes and data. As stated by Lenz and Hahn (2015), with

a commitment towards accountability and integrity; internal auditing can share value to

senior management as well as governing bodies as an objective source of service that is

2RESEARCH PROPOSAL

independent. The authors further argued that within an organisation, the roles of internal

auditing are broad and it encompasses with corporate governance, management controls, risk

management, the effectiveness of the organisational operations, reliability of management

and financial reporting and it also helps the organisation to follow compliance with

regulations and laws. As opined by Pizzini et al. (2014), internal auditing is very important in

the developing countries where corruption and fraud activities are prevalent as it involves in

conducting proactive audits in fraudulent cases through investigating and participating fraud

examinations.

The concept of corporate governance

Corporate governance can be defined as the practices, rules and processes through

which the firms are controlled and directed. As opined by Dodd (2017), corporate governance

is involved in balancing the interest of the company's stakeholders and the stakeholders of the

organisations are the management, shareholders, customers, financiers, suppliers and

community. Corporate governance gives the organisation a chance to provide a framework

towards gaining the company's objectives and it surrounds the practically every aspect of the

management (McCahery et al. 2016). Corporate governance encompasses from internal

controls of the performance of the organisation to the actions plan about the performance

measurement. According to Tricker (2015), the board of directors are primary stakeholders of

the corporate governance and shareholders elect the directors of the organisations. The

directors take important decisions about the business. On the other side, as stated by Allen

(2017), poor corporate governance can make doubt about the company’s integrity, reliability

and obligations towards the shareholders. In recent time, Volkswagen faced the issue of poor

corporate governance when it got caught in emission scandal of the organisation.

The theoretical perspective of the internal audit function and corporate governance

independent. The authors further argued that within an organisation, the roles of internal

auditing are broad and it encompasses with corporate governance, management controls, risk

management, the effectiveness of the organisational operations, reliability of management

and financial reporting and it also helps the organisation to follow compliance with

regulations and laws. As opined by Pizzini et al. (2014), internal auditing is very important in

the developing countries where corruption and fraud activities are prevalent as it involves in

conducting proactive audits in fraudulent cases through investigating and participating fraud

examinations.

The concept of corporate governance

Corporate governance can be defined as the practices, rules and processes through

which the firms are controlled and directed. As opined by Dodd (2017), corporate governance

is involved in balancing the interest of the company's stakeholders and the stakeholders of the

organisations are the management, shareholders, customers, financiers, suppliers and

community. Corporate governance gives the organisation a chance to provide a framework

towards gaining the company's objectives and it surrounds the practically every aspect of the

management (McCahery et al. 2016). Corporate governance encompasses from internal

controls of the performance of the organisation to the actions plan about the performance

measurement. According to Tricker (2015), the board of directors are primary stakeholders of

the corporate governance and shareholders elect the directors of the organisations. The

directors take important decisions about the business. On the other side, as stated by Allen

(2017), poor corporate governance can make doubt about the company’s integrity, reliability

and obligations towards the shareholders. In recent time, Volkswagen faced the issue of poor

corporate governance when it got caught in emission scandal of the organisation.

The theoretical perspective of the internal audit function and corporate governance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RESEARCH PROPOSAL

Agency Theory of corporate governance

Agency theory involves the issues of the directors that control the company whereas

shareholders own the company. Agency theory takes this issue into consideration to prevent

it. According to Hoenen and Kostova (2015), the key concept of agency theory is that an

agent is recruited by the principle to continue the task on their behalf and the agency is the

relationship between the agent and the principle. The authors in the article further stated that

agencies costs are given by the principles in controlling the agency behaviour just because of

the lack of trust in the belief of the agents. It is needed to undertake the task on behalf of the

agent and the agent becomes accountable to that principle. There are three separations of

ownership and control; such as principal (shareholders), agents (directors) and task

(Managing the company) (Muller 2017). The agency theory helps the company to create the

corporate governance and it starts with the companies owned and managed by the same

people. In the next stage, it expands the business through required investors and these people

could be shareholders and limited liability. In the following stage, it delegates the running of

the company and to managers (agents). In the next stage, the company goes towards the

separation of the goals. As stated by Bosse and Phillips (2016) separation of ownership in

business can lead to the potential issues between directors and shareholders and principal-

agent relationship can be dealt with corporate governance codes and that with the firm with

the auditors.

Stewardship Theory of corporate governance

Stewardship theory is about the managers who can act as responsible stewards of the

principle and assets that they control (Kruitwagen et al. 2017). In addition, stewardship

theory is the alternative view of the agency theory where the managers are taken as to act in

their own enthusiasm and self-interest. It can be specified that stewardship is a certain

Agency Theory of corporate governance

Agency theory involves the issues of the directors that control the company whereas

shareholders own the company. Agency theory takes this issue into consideration to prevent

it. According to Hoenen and Kostova (2015), the key concept of agency theory is that an

agent is recruited by the principle to continue the task on their behalf and the agency is the

relationship between the agent and the principle. The authors in the article further stated that

agencies costs are given by the principles in controlling the agency behaviour just because of

the lack of trust in the belief of the agents. It is needed to undertake the task on behalf of the

agent and the agent becomes accountable to that principle. There are three separations of

ownership and control; such as principal (shareholders), agents (directors) and task

(Managing the company) (Muller 2017). The agency theory helps the company to create the

corporate governance and it starts with the companies owned and managed by the same

people. In the next stage, it expands the business through required investors and these people

could be shareholders and limited liability. In the following stage, it delegates the running of

the company and to managers (agents). In the next stage, the company goes towards the

separation of the goals. As stated by Bosse and Phillips (2016) separation of ownership in

business can lead to the potential issues between directors and shareholders and principal-

agent relationship can be dealt with corporate governance codes and that with the firm with

the auditors.

Stewardship Theory of corporate governance

Stewardship theory is about the managers who can act as responsible stewards of the

principle and assets that they control (Kruitwagen et al. 2017). In addition, stewardship

theory is the alternative view of the agency theory where the managers are taken as to act in

their own enthusiasm and self-interest. It can be specified that stewardship is a certain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RESEARCH PROPOSAL

mechanism to reduce agency loss. This policy is included the compensation, keeping

executive, levels of benefits and managers' incentives schemes through rewarding the

financially and it offers shares through alignment. It offers financial interest to the staffs to

motivate them in order to offer better performance. As stated by Allen (2017), the steward is

someone who takes care and protects of the needs of others and firms' executives try to take

care of the interest of the shareholders and they make a decision about the firms.

Developing and implementing well-aligned internal audit strategy

Internal audit function has an annual budget plan and the corporate governance asks

the internal auditors to have a specific strategic plan. As stated by Alless et al. (2018),

internal audit strategy should be three to five years plan and roadmap of the organisation will

be based on the overall strategy and stakeholders' expectation from the organisation. A well-

aligned strategy has four steps to create an internal-audit specific strategic plan. In African

countries and in large organisations; developing formal internal audit strategy needs planning

as the corruption is much there. At first, the organisations need to develop or refine the

internal audit's strategic vision and the roles and responsibilities of the stakeholders should be

well described. The vision of the internal auditors should be mandated clearly. The

organisation needs to accomplish this in long-term period. As stated by Chan and Vasarhelyi

(2018), in the next stage of the well-defined plan; the organisations need to recognise and

prioritise the key strategic initiatives to mandate the strategic vision of the internal audit and

initiatives must be taken to smaller the key business risks of the organisation. In addition, in

the next stage, the organisation can design the appropriate KPI for the stakeholders. The

shareholders or the board of directors can determine the success of internal audit through key

performance indicators against the prioritised initiatives. The organisation can track the

value-driven measure and the productivity (Chambers and Odar 2015). Lastly, the

organisations need to develop the operating strategy through tracking the activities to gain the

mechanism to reduce agency loss. This policy is included the compensation, keeping

executive, levels of benefits and managers' incentives schemes through rewarding the

financially and it offers shares through alignment. It offers financial interest to the staffs to

motivate them in order to offer better performance. As stated by Allen (2017), the steward is

someone who takes care and protects of the needs of others and firms' executives try to take

care of the interest of the shareholders and they make a decision about the firms.

Developing and implementing well-aligned internal audit strategy

Internal audit function has an annual budget plan and the corporate governance asks

the internal auditors to have a specific strategic plan. As stated by Alless et al. (2018),

internal audit strategy should be three to five years plan and roadmap of the organisation will

be based on the overall strategy and stakeholders' expectation from the organisation. A well-

aligned strategy has four steps to create an internal-audit specific strategic plan. In African

countries and in large organisations; developing formal internal audit strategy needs planning

as the corruption is much there. At first, the organisations need to develop or refine the

internal audit's strategic vision and the roles and responsibilities of the stakeholders should be

well described. The vision of the internal auditors should be mandated clearly. The

organisation needs to accomplish this in long-term period. As stated by Chan and Vasarhelyi

(2018), in the next stage of the well-defined plan; the organisations need to recognise and

prioritise the key strategic initiatives to mandate the strategic vision of the internal audit and

initiatives must be taken to smaller the key business risks of the organisation. In addition, in

the next stage, the organisation can design the appropriate KPI for the stakeholders. The

shareholders or the board of directors can determine the success of internal audit through key

performance indicators against the prioritised initiatives. The organisation can track the

value-driven measure and the productivity (Chambers and Odar 2015). Lastly, the

organisations need to develop the operating strategy through tracking the activities to gain the

5RESEARCH PROPOSAL

strategic initiatives. The internal auditors can determine the key milestones through

communicating these to the external stakeholders. In the article named Internal Audits and

Its Role in Corporate Governance, Al Jabali et al. (2011) stated that corporate governance

has two essential activities, one is crystallises the risk control and other one is audit assurance

regarding the regulatory control. Supervisor controls check the effectiveness of submission

reports and internal audit standards check the effectiveness of corporate governance. The

authors also stated the view that internal auditors need to be fully prepared in order to audit

the operations of the organisations and control the accounting system, tactical operations and

administrative process.

Role of internal audit function in developing corporate governance code

As opined by Griffiths (2016), corporate governance is the system through which the

organisations are controlled and directed; the accurate corporate governance structure has

specified the distributions of responsibilities and rights among the various stakeholders and

departments within the organisation. The organisations mainly have a multi-layered system

through which it controls the overall system of organisations. The first layered of the

corporate governance lies within departments where the process of working ensures the

controls targeting the errors of misconduct. The CEO of the organisation gets the internal

assurance from the internal audit system and board of directors use the internal audit system

to ensure that all the stakeholders and departments within the organisation must be

trustworthy and accurate. Shareholders can make sure whether their interests and money are

well-protected. The various systems within the companies are functioning and sufficient the

way it works within the organisation (Chambers and Odar 2015). Therefore, sometimes,

external auditors come to evaluate the system to provide recommendations to the owners. The

board of directors need to establish the transparent arrangements and formal presentation to

strategic initiatives. The internal auditors can determine the key milestones through

communicating these to the external stakeholders. In the article named Internal Audits and

Its Role in Corporate Governance, Al Jabali et al. (2011) stated that corporate governance

has two essential activities, one is crystallises the risk control and other one is audit assurance

regarding the regulatory control. Supervisor controls check the effectiveness of submission

reports and internal audit standards check the effectiveness of corporate governance. The

authors also stated the view that internal auditors need to be fully prepared in order to audit

the operations of the organisations and control the accounting system, tactical operations and

administrative process.

Role of internal audit function in developing corporate governance code

As opined by Griffiths (2016), corporate governance is the system through which the

organisations are controlled and directed; the accurate corporate governance structure has

specified the distributions of responsibilities and rights among the various stakeholders and

departments within the organisation. The organisations mainly have a multi-layered system

through which it controls the overall system of organisations. The first layered of the

corporate governance lies within departments where the process of working ensures the

controls targeting the errors of misconduct. The CEO of the organisation gets the internal

assurance from the internal audit system and board of directors use the internal audit system

to ensure that all the stakeholders and departments within the organisation must be

trustworthy and accurate. Shareholders can make sure whether their interests and money are

well-protected. The various systems within the companies are functioning and sufficient the

way it works within the organisation (Chambers and Odar 2015). Therefore, sometimes,

external auditors come to evaluate the system to provide recommendations to the owners. The

board of directors need to establish the transparent arrangements and formal presentation to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RESEARCH PROPOSAL

apply the risk management, task reporting and internal control principles so that it can

maintain a relationship with auditors of the organisation.

In the article named Internal audit and its role in improving the corporate

governance systems, authors Tabara and Ungureanu (2012) opined that corporate governance

implies the cycle that goes from the monitoring role to the steering of the operational and

administrative activities. The authors also stated that the objective of the corporate

governance is to make a balance between various actors to implement power control

instrument and interested parties in the capital of entity. Internal auditors bring the systematic

and disciplines aspects towards improvement and evaluate the effectiveness of the

organisational system and governance process (Christ et al. 2015). The positive role of

internal audit goes beyond the safeguarding and controlling of the corporate assets, enforcing

corporate liabilities and regulatory compliance; the role of the internal auditor is to create the

value and suggesting the development of the organisational corporate governance. On the

other hand, as contradicted by Hayes (2017), internal auditors ensure the effective internal

control and adequacy of the control system which ensures the responsible governance.

According to Alzeban and Gwilliam (2014), internal audit assists the Board and stakeholders

in protecting the reputation, assets, sustainability of the company. The responsibility of the

internal audit is just not to extend the financial control and to maintain the surrounding of the

non-financial performance as well.

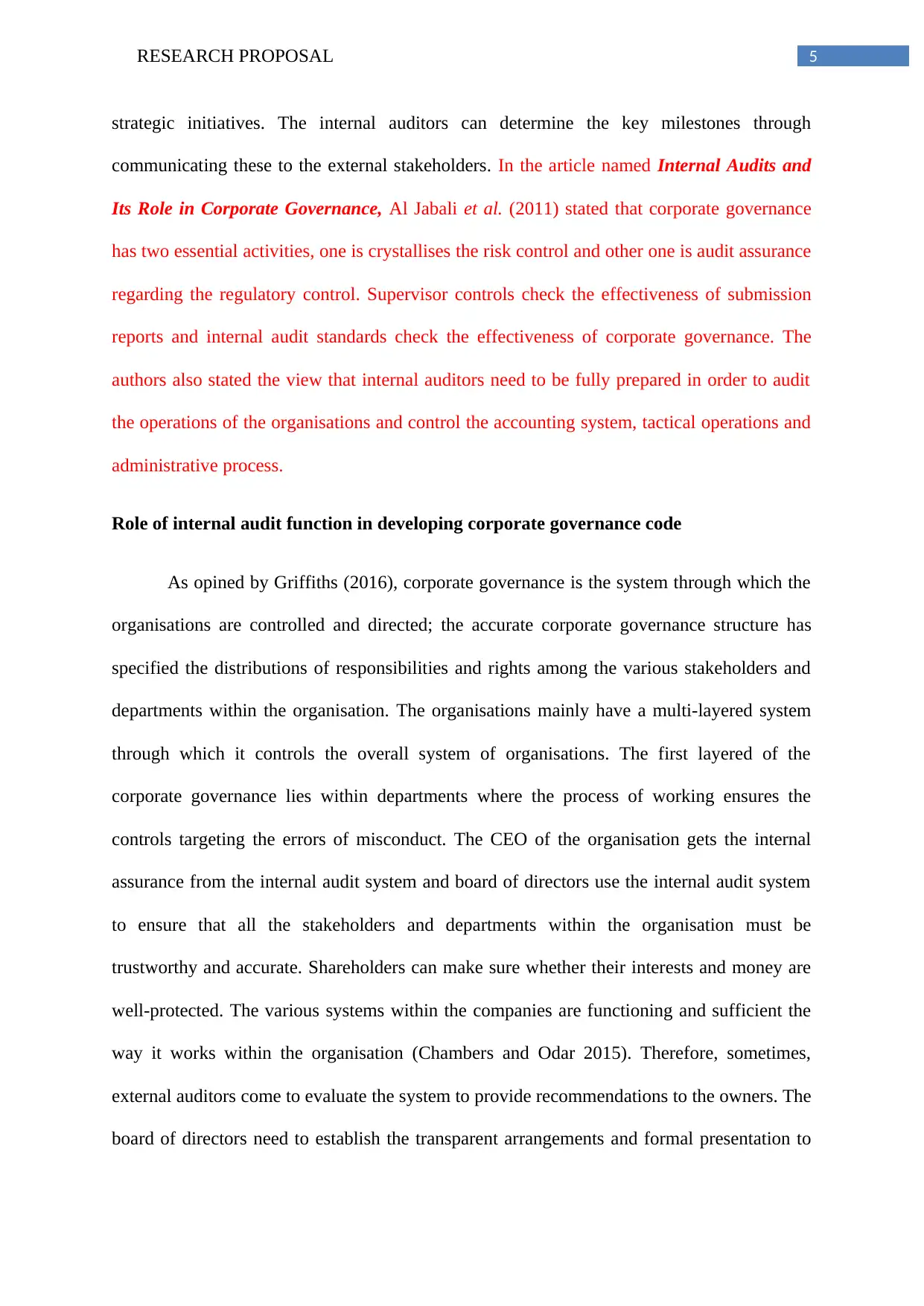

Conceptual framework

apply the risk management, task reporting and internal control principles so that it can

maintain a relationship with auditors of the organisation.

In the article named Internal audit and its role in improving the corporate

governance systems, authors Tabara and Ungureanu (2012) opined that corporate governance

implies the cycle that goes from the monitoring role to the steering of the operational and

administrative activities. The authors also stated that the objective of the corporate

governance is to make a balance between various actors to implement power control

instrument and interested parties in the capital of entity. Internal auditors bring the systematic

and disciplines aspects towards improvement and evaluate the effectiveness of the

organisational system and governance process (Christ et al. 2015). The positive role of

internal audit goes beyond the safeguarding and controlling of the corporate assets, enforcing

corporate liabilities and regulatory compliance; the role of the internal auditor is to create the

value and suggesting the development of the organisational corporate governance. On the

other hand, as contradicted by Hayes (2017), internal auditors ensure the effective internal

control and adequacy of the control system which ensures the responsible governance.

According to Alzeban and Gwilliam (2014), internal audit assists the Board and stakeholders

in protecting the reputation, assets, sustainability of the company. The responsibility of the

internal audit is just not to extend the financial control and to maintain the surrounding of the

non-financial performance as well.

Conceptual framework

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESEARCH PROPOSAL

Figure: Conceptual framework

(Source: Self-developed)

7. Ethics

This research will not be done using primary data; therefore, no human participants

will be associated with this research. This research will follow Data Protection Act 1998. The

research would follow the ethical standards, rules and norms. The ethics describe that the

researcher will not follow any wrong practice while researching. The researcher will not

break any ethical norms and the researcher will strictly adhere to the policy of the research.

The researcher will complete the ethical checklist and most importantly, the researcher will

do the research using secondary data. The researcher will collect the data through books,

Figure: Conceptual framework

(Source: Self-developed)

7. Ethics

This research will not be done using primary data; therefore, no human participants

will be associated with this research. This research will follow Data Protection Act 1998. The

research would follow the ethical standards, rules and norms. The ethics describe that the

researcher will not follow any wrong practice while researching. The researcher will not

break any ethical norms and the researcher will strictly adhere to the policy of the research.

The researcher will complete the ethical checklist and most importantly, the researcher will

do the research using secondary data. The researcher will collect the data through books,

8RESEARCH PROPOSAL

journals, online articles, government websites, company website and online reports. The

researcher will not fabricate or modify any data those would be collected through the

secondary sources. The fundamental ethics issues to the secondary data are related to

remaining same and with the advent of new technologies; the literature becomes more

pressing. The ethics are related to the data sharing, storage, compiling and these are

becoming more faster. The researcher is aware of the fact about the data confidentiality and

security of the data breaches. The researcher will put in-text citation throughout the write-up.

Secondary data do not need permission to take as the researcher will collect the secondary

data through archive notes, documentary notes and case notes. It will be assumed that the

ethical consideration is less in secondary data as it draws the experience of the collaborative

of the research project. Internal audit and corporate governance related information are scarce

in literature; therefore, the researcher will collect the information from secondary sources

with the purpose of the present study.

journals, online articles, government websites, company website and online reports. The

researcher will not fabricate or modify any data those would be collected through the

secondary sources. The fundamental ethics issues to the secondary data are related to

remaining same and with the advent of new technologies; the literature becomes more

pressing. The ethics are related to the data sharing, storage, compiling and these are

becoming more faster. The researcher is aware of the fact about the data confidentiality and

security of the data breaches. The researcher will put in-text citation throughout the write-up.

Secondary data do not need permission to take as the researcher will collect the secondary

data through archive notes, documentary notes and case notes. It will be assumed that the

ethical consideration is less in secondary data as it draws the experience of the collaborative

of the research project. Internal audit and corporate governance related information are scarce

in literature; therefore, the researcher will collect the information from secondary sources

with the purpose of the present study.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RESEARCH PROPOSAL

Reference List

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and

financial reporting quality: The joint importance of independence and competence. Journal of

Accounting Research, 54(1), pp.3-40.

Al-jabali, M.A., Abdalmanam, O. and Ziadat, K.N., 2011. Internal Audit and its Role in

Corporate Governance. Middle Eastern Finance and Economics, 11, pp.161-176.

Allen, W.T., 2017. Our schizophrenic conception of the business corporation. In Corporate

Governance (pp. 79-99). Gower.

Alles, M.G., Kogan, A. and Vasarhelyi, M.A., 2018. Putting continuous auditing theory into

practice: Lessons from two pilot implementations. In Continuous Auditing: Theory and

Application (pp. 247-270). Emerald Publishing Limited.

Alzeban, A. and Gwilliam, D., 2014. Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.74-86.

Bosse, D.A. and Phillips, R.A., 2016. Agency theory and bounded self-interest. Academy of

Management Review, 41(2), pp.276-297.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Reference List

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and

financial reporting quality: The joint importance of independence and competence. Journal of

Accounting Research, 54(1), pp.3-40.

Al-jabali, M.A., Abdalmanam, O. and Ziadat, K.N., 2011. Internal Audit and its Role in

Corporate Governance. Middle Eastern Finance and Economics, 11, pp.161-176.

Allen, W.T., 2017. Our schizophrenic conception of the business corporation. In Corporate

Governance (pp. 79-99). Gower.

Alles, M.G., Kogan, A. and Vasarhelyi, M.A., 2018. Putting continuous auditing theory into

practice: Lessons from two pilot implementations. In Continuous Auditing: Theory and

Application (pp. 247-270). Emerald Publishing Limited.

Alzeban, A. and Gwilliam, D., 2014. Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.74-86.

Bosse, D.A. and Phillips, R.A., 2016. Agency theory and bounded self-interest. Academy of

Management Review, 41(2), pp.276-297.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RESEARCH PROPOSAL

Christ, M.H., Masli, A., Sharp, N.Y. and Wood, D.A., 2015. Rotational internal audit

programs and financial reporting quality: Do compensate controls help?. Accounting,

Organizations and Society, 44, pp.37-59.

Dodd, E.M., 2017. For whom are corporate managers trustees?. In Corporate

Governance (pp. 29-47). Gower.

Griffiths, P., 2016. Risk-based auditing. Abingdon: Routledge.

Hayes, C.H., 2017. Internal audit as police: perhaps it's time to embrace our image as

corporate protectors rather than fighting against it. Internal Auditor, 74(3), pp.68-69.

Hoenen, A.K. and Kostova, T., 2015. Utilizing the broader agency perspective for studying

headquarters–subsidiary relations in multinational companies. Journal of International

Business Studies, 46(1), pp.104-113.

Kruitwagen, L., Madani, K., Caldecott, B. and Workman, M.H., 2017. Game theory and

corporate governance: conditions for effective stewardship of companies exposed to climate

change risks. Journal of Sustainable Finance & Investment, 7(1), pp.14-36.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

McCahery, J.A., Sautner, Z. and Starks, L.T., 2016. Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-

2932.

Muller, R., 2017. Project governance. Abingdon: Routledge.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

Christ, M.H., Masli, A., Sharp, N.Y. and Wood, D.A., 2015. Rotational internal audit

programs and financial reporting quality: Do compensate controls help?. Accounting,

Organizations and Society, 44, pp.37-59.

Dodd, E.M., 2017. For whom are corporate managers trustees?. In Corporate

Governance (pp. 29-47). Gower.

Griffiths, P., 2016. Risk-based auditing. Abingdon: Routledge.

Hayes, C.H., 2017. Internal audit as police: perhaps it's time to embrace our image as

corporate protectors rather than fighting against it. Internal Auditor, 74(3), pp.68-69.

Hoenen, A.K. and Kostova, T., 2015. Utilizing the broader agency perspective for studying

headquarters–subsidiary relations in multinational companies. Journal of International

Business Studies, 46(1), pp.104-113.

Kruitwagen, L., Madani, K., Caldecott, B. and Workman, M.H., 2017. Game theory and

corporate governance: conditions for effective stewardship of companies exposed to climate

change risks. Journal of Sustainable Finance & Investment, 7(1), pp.14-36.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

McCahery, J.A., Sautner, Z. and Starks, L.T., 2016. Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-

2932.

Muller, R., 2017. Project governance. Abingdon: Routledge.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

11RESEARCH PROPOSAL

Tabara, N. and Ungureanu, M., 2012. Internal audit and its role in improving corporate

governance systems. Annales Universitatis Apulensis: Series Oeconomica, 14(1), pp.139-

145.

Tricker, R.B. 2015. Corporate Governance: Principles, policies, and practices. Oxford

University Press, USA.

Tabara, N. and Ungureanu, M., 2012. Internal audit and its role in improving corporate

governance systems. Annales Universitatis Apulensis: Series Oeconomica, 14(1), pp.139-

145.

Tricker, R.B. 2015. Corporate Governance: Principles, policies, and practices. Oxford

University Press, USA.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.