U23000 - Internal Auditing Effectiveness Compared to External Auditing

VerifiedAdded on 2023/06/03

|17

|5577

|303

Essay

AI Summary

This essay examines the effectiveness of internal auditing compared to external auditing, exploring the significance of auditing for business development and growth. It analyzes the differences between internal and external audit processes, addressing the research question of whether internal auditing is more effective than external auditing. The literature review covers various perspectives on auditing, internal control systems, and risk management. The essay highlights the role of internal auditing in enhancing organizational value, improving internal control, and aligning business executives' interests with shareholders. The research concludes that internal auditing is vital for a strong governance structure and minimizing material misstatements, with regular internal audits being crucial for a robust system of governance.

1

Title: Effectiveness of Internal Auditing in Comparison to External Auditing

Title: Effectiveness of Internal Auditing in Comparison to External Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Research Rationale..........................................................................................................................3

Research Objectives.........................................................................................................................3

Research Questions or Problems.....................................................................................................4

Literature Review............................................................................................................................4

Research Method.............................................................................................................................8

Conclusion & Recommendation....................................................................................................11

References......................................................................................................................................12

Contents

Research Rationale..........................................................................................................................3

Research Objectives.........................................................................................................................3

Research Questions or Problems.....................................................................................................4

Literature Review............................................................................................................................4

Research Method.............................................................................................................................8

Conclusion & Recommendation....................................................................................................11

References......................................................................................................................................12

3

Research Rationale

The present research is undertaken to examine the importance of auditing within an

organization. The activity of auditing within an organization can be regarded as the process of

independently checking the financial records of an organization so as to assure that the financial

statements prepared are accurate. The overall process of auditing is carried out by an auditor who

holds the responsibility of developing and examining the financial records. An auditor provides

opinions about the accuracy and faithful presentation of financial information that forms the

basis for decision-making of its end-users. This research holds high importance for providing an

understanding of the process of auditing that is crucial for assessing the adequacy of the control

mechanism of a firm. There are mainly two types of audit carried by an organization, that is,

internal and external audit. This research is conducted to demonstrate the importance of internal

and external auditing within a firm by providing an insight into both types of auditing

(Abdolmohammadi, 2009).

The research will help in making a comparison between the internal and external auditing

to determine which more effective for promoting the growth and development of a firm. The

difference between the internal audit, that is, reviewing the internal operational processes of a

firm and the external audit, that is, conducted by a third party to check the financial report

accuracy will be illustrated adequately with the help of research process. The research topic

selected of examining the effectiveness of internal and external auditing is selected in the context

to illustrate the nature of their processes and their relative importance for a firm. This will help

the readers in identifying and comparing effectively between the processes of internal and

external auditing.

This will help the business companies to implement the internal or external auditing

procedures for attaining the organizational goals and objectives. The research issue is selected

for exploration as there is large importance of reviewing the internal as well as external control

mechanism of a firm with the help of auditing process. The increasing fraudulent activities

within the firms is causing the need for reviewing and examining its internal as well as external

control structure to protect the interest of general public. The business companies worldwide

largely places focuses on carrying out external auditing of their firms and ignores the relative

Research Rationale

The present research is undertaken to examine the importance of auditing within an

organization. The activity of auditing within an organization can be regarded as the process of

independently checking the financial records of an organization so as to assure that the financial

statements prepared are accurate. The overall process of auditing is carried out by an auditor who

holds the responsibility of developing and examining the financial records. An auditor provides

opinions about the accuracy and faithful presentation of financial information that forms the

basis for decision-making of its end-users. This research holds high importance for providing an

understanding of the process of auditing that is crucial for assessing the adequacy of the control

mechanism of a firm. There are mainly two types of audit carried by an organization, that is,

internal and external audit. This research is conducted to demonstrate the importance of internal

and external auditing within a firm by providing an insight into both types of auditing

(Abdolmohammadi, 2009).

The research will help in making a comparison between the internal and external auditing

to determine which more effective for promoting the growth and development of a firm. The

difference between the internal audit, that is, reviewing the internal operational processes of a

firm and the external audit, that is, conducted by a third party to check the financial report

accuracy will be illustrated adequately with the help of research process. The research topic

selected of examining the effectiveness of internal and external auditing is selected in the context

to illustrate the nature of their processes and their relative importance for a firm. This will help

the readers in identifying and comparing effectively between the processes of internal and

external auditing.

This will help the business companies to implement the internal or external auditing

procedures for attaining the organizational goals and objectives. The research issue is selected

for exploration as there is large importance of reviewing the internal as well as external control

mechanism of a firm with the help of auditing process. The increasing fraudulent activities

within the firms is causing the need for reviewing and examining its internal as well as external

control structure to protect the interest of general public. The business companies worldwide

largely places focuses on carrying out external auditing of their firms and ignores the relative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

significance of internal auditing as well. The internal auditing is required by the management of

a firm to assure that it has adequately implemented the risk and governance mechanisms for

maximizing the operational efficiency (Alzeban, 2015).

Research Objectives

The present research will aim to attain the following objectives:

To develop an understanding of the importance of auditing process for the development

and growth of the businesses

To examine and analyze the difference between internal and external auditing process

To gain an understanding into the effectiveness of the internal auditing over external

auditing

Research Questions or Problems

In the context of the above stated objectives, this research will mainly aim to achieve the

following research question “Does internal auditing is effective over the external auditing

processes carried out by businesses at a global level?” This research will also attain the answer

for the following sub-research questions in context of this main research question as follows:

What is the significance of auditing process carried out by firms for achieving their stated

goals and objectives?

How the process of internal auditing within a firm does is different from that of external

auditing?

Literature Review

Savcuk (2007) stated that the process of auditing can be regarded as independently

reviewing and examining the records and activities of an organization for assessing the

appropriateness of system controls. This is done to ensure that businesses are complying

effectively with the established policies and procedures that are essential for their sustained

growth and development. In this context, Karagiorgos (2009) also explained that the auditing

process is mainly undertaken by a firm for ensuring that all business processes are carried out in

a transparent and ethical manner. The business firms are required to continually review their

significance of internal auditing as well. The internal auditing is required by the management of

a firm to assure that it has adequately implemented the risk and governance mechanisms for

maximizing the operational efficiency (Alzeban, 2015).

Research Objectives

The present research will aim to attain the following objectives:

To develop an understanding of the importance of auditing process for the development

and growth of the businesses

To examine and analyze the difference between internal and external auditing process

To gain an understanding into the effectiveness of the internal auditing over external

auditing

Research Questions or Problems

In the context of the above stated objectives, this research will mainly aim to achieve the

following research question “Does internal auditing is effective over the external auditing

processes carried out by businesses at a global level?” This research will also attain the answer

for the following sub-research questions in context of this main research question as follows:

What is the significance of auditing process carried out by firms for achieving their stated

goals and objectives?

How the process of internal auditing within a firm does is different from that of external

auditing?

Literature Review

Savcuk (2007) stated that the process of auditing can be regarded as independently

reviewing and examining the records and activities of an organization for assessing the

appropriateness of system controls. This is done to ensure that businesses are complying

effectively with the established policies and procedures that are essential for their sustained

growth and development. In this context, Karagiorgos (2009) also explained that the auditing

process is mainly undertaken by a firm for ensuring that all business processes are carried out in

a transparent and ethical manner. The business firms are required to continually review their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

internal as well as external control and systems for developing their competitive strength by

gaining credibility and reliability in the mind of the investors. The increasing globalization and

complexity of businesses is causing the increase in the number of cases related to fraudulent

financial reporting. This has caused the development of role of auditing within businesses to

overcome the increases cases related to fraudulent activities within a firm due to weak internal or

external control structure (Karagiorgos, 2009).

According to Boţa-Avram & Palfi (2009), there are mainly two types of audit carried out

by a business firm, that are, external and internal auditing. External audit can be regarded as the

process of examining the financial records and books of a company from the perspective of the

shareholders to determine their accuracy and reliability. The function of an external audit is

carried out by an independent body known as auditor who possesses the responsibility of

determining the accuracy of the financial statements developed by a firm. Similarly, Candreva

(2006) also stated that the primary responsibility of an auditor is to express a neutral opinion as

per the generally accepted accounting principles. The external auditor can be regarded as an

independent contractor while major role is to the reports on the financial statements of an

organization. Rittenberg (2006) also stated that the businesses carry out the external auditing of

their financial reports on an annual basis for assuring that their financial statements prepared are

free from any type of materialistic error and represents a true and fair view of the actual financial

position to the investors. It is required that external auditing needs to be carried out as per the

international auditing standards for examination and evaluation of the financial statements of an

organization.

On the other hand, Savcuk (2007) has argued that internal audit is carried out for

reviewing the financial and operational activities of a firm on a continuous basis to assess the

effectiveness of its internal control systems and procedures. It refers to the unbiased and

systematic analysis of business activities to identifying the areas of improvement and thus

strengthening the internal control systems and processes within a firm. The different type of

activities that are performed within internal auditing can be stated as follows:

Evaluation of the accounting and internal control system

Examining the daily operational activities

Evaluating the financial and non-financial information within an organization

internal as well as external control and systems for developing their competitive strength by

gaining credibility and reliability in the mind of the investors. The increasing globalization and

complexity of businesses is causing the increase in the number of cases related to fraudulent

financial reporting. This has caused the development of role of auditing within businesses to

overcome the increases cases related to fraudulent activities within a firm due to weak internal or

external control structure (Karagiorgos, 2009).

According to Boţa-Avram & Palfi (2009), there are mainly two types of audit carried out

by a business firm, that are, external and internal auditing. External audit can be regarded as the

process of examining the financial records and books of a company from the perspective of the

shareholders to determine their accuracy and reliability. The function of an external audit is

carried out by an independent body known as auditor who possesses the responsibility of

determining the accuracy of the financial statements developed by a firm. Similarly, Candreva

(2006) also stated that the primary responsibility of an auditor is to express a neutral opinion as

per the generally accepted accounting principles. The external auditor can be regarded as an

independent contractor while major role is to the reports on the financial statements of an

organization. Rittenberg (2006) also stated that the businesses carry out the external auditing of

their financial reports on an annual basis for assuring that their financial statements prepared are

free from any type of materialistic error and represents a true and fair view of the actual financial

position to the investors. It is required that external auditing needs to be carried out as per the

international auditing standards for examination and evaluation of the financial statements of an

organization.

On the other hand, Savcuk (2007) has argued that internal audit is carried out for

reviewing the financial and operational activities of a firm on a continuous basis to assess the

effectiveness of its internal control systems and procedures. It refers to the unbiased and

systematic analysis of business activities to identifying the areas of improvement and thus

strengthening the internal control systems and processes within a firm. The different type of

activities that are performed within internal auditing can be stated as follows:

Evaluation of the accounting and internal control system

Examining the daily operational activities

Evaluating the financial and non-financial information within an organization

6

Identification of frauds and errors

As per the views of Bogonko (2016) the internal auditing is mainly carried out by a

business firm with the aim of enhancing the organizational value by ensuring that there is

presence of effective internal control and risk management system. The process of internal

auditing is carried out by the internal auditors who are mainly the management people of an

organization. The business largely develops a separate department for performing continuous

audit to increase the effectiveness of organizational systems and policies. Thus, it can be stated

that internal audit is an independent and consulting activity of an organization that is carried out

mainly to improve the internal control system for achieving the organizational aims and

objectives (Bogonko, 2016).

Van Staden & Steyn (2009) has also stated that the demand for external as well as

internal audit has been increased largely with the increasing complexity in the business

environment. The audit carried out by businesses helps in carrying out its independent

verification for reducing the chances of error and fraudulent activities. External auditing carried

out by an independent external auditor has been placed large importance by the business

corporations for enhancing the credibility of their financial reports in the mind of their

stakeholders. However, Roziani (2011) has also stated that with the increasing fraudulent cases

within the business firms related to their weak governance mad control structure has largely

placed importance on internal auditing activities as well. The occurrence of corporate accounting

scandals such as Enron, WorldCom and others have shaken the investors’ confidence and caused

many changes within the accounting regulations to tighten the internal control structure of the

firms.

Hammad & Imdadullah (2012) has also argued that the businesses are also realizing that

the fraudulent activities that occurred within their firms can result in causing significant long-

term damage to their reputation besides the financial losses. Internal auditing deals with

improving the internal control within the firms for restoring the public trusts and overcoming the

occurrence of fraudulent activities. The primary objective of the internal audit is to provide

suggestions to the management for carrying out their roles in an effectively by reviewing of its

overall internal control systems and processes. Abbott, Parker & Peters (2010) has stated that the

deficiencies present within the internal control systems such as governance or risk management

Identification of frauds and errors

As per the views of Bogonko (2016) the internal auditing is mainly carried out by a

business firm with the aim of enhancing the organizational value by ensuring that there is

presence of effective internal control and risk management system. The process of internal

auditing is carried out by the internal auditors who are mainly the management people of an

organization. The business largely develops a separate department for performing continuous

audit to increase the effectiveness of organizational systems and policies. Thus, it can be stated

that internal audit is an independent and consulting activity of an organization that is carried out

mainly to improve the internal control system for achieving the organizational aims and

objectives (Bogonko, 2016).

Van Staden & Steyn (2009) has also stated that the demand for external as well as

internal audit has been increased largely with the increasing complexity in the business

environment. The audit carried out by businesses helps in carrying out its independent

verification for reducing the chances of error and fraudulent activities. External auditing carried

out by an independent external auditor has been placed large importance by the business

corporations for enhancing the credibility of their financial reports in the mind of their

stakeholders. However, Roziani (2011) has also stated that with the increasing fraudulent cases

within the business firms related to their weak governance mad control structure has largely

placed importance on internal auditing activities as well. The occurrence of corporate accounting

scandals such as Enron, WorldCom and others have shaken the investors’ confidence and caused

many changes within the accounting regulations to tighten the internal control structure of the

firms.

Hammad & Imdadullah (2012) has also argued that the businesses are also realizing that

the fraudulent activities that occurred within their firms can result in causing significant long-

term damage to their reputation besides the financial losses. Internal auditing deals with

improving the internal control within the firms for restoring the public trusts and overcoming the

occurrence of fraudulent activities. The primary objective of the internal audit is to provide

suggestions to the management for carrying out their roles in an effectively by reviewing of its

overall internal control systems and processes. Abbott, Parker & Peters (2010) has stated that the

deficiencies present within the internal control systems such as governance or risk management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

structure are highlighted adequately within the internal audit. The internal auditing can be

categorized as more effective over external auditing as the presence of a strong governance

structure within a firm will help in reducing the materials misstatement errors during the

financial reporting process.

Prawitt (2009) in this context also stated that businesses need to place importance on

carrying out internal auditors in a regular manner besides only focusing on carrying out external

audit of their financial records. The fact has been highlighted by the occurrence of corporate

accounting scandals such as Enron that have highlighted the importance of having a robust

system of governing within the firms. The major benefit as per Holt & Deborah (2008) that the

management of a firm realizes by carrying out internal audit is developing a sound base for

judgment, identifying the weaknesses in control and performance. Developing suggestions for

improvement and disseminating information about the business processes that is required by all

level of management for better decision-making. It helps in examining the compliance of firms

with the established policies, plans, procedures, laws and regulations to determine that business

operations are carried out in an ethical manner (Holt & Deborah, 2008).

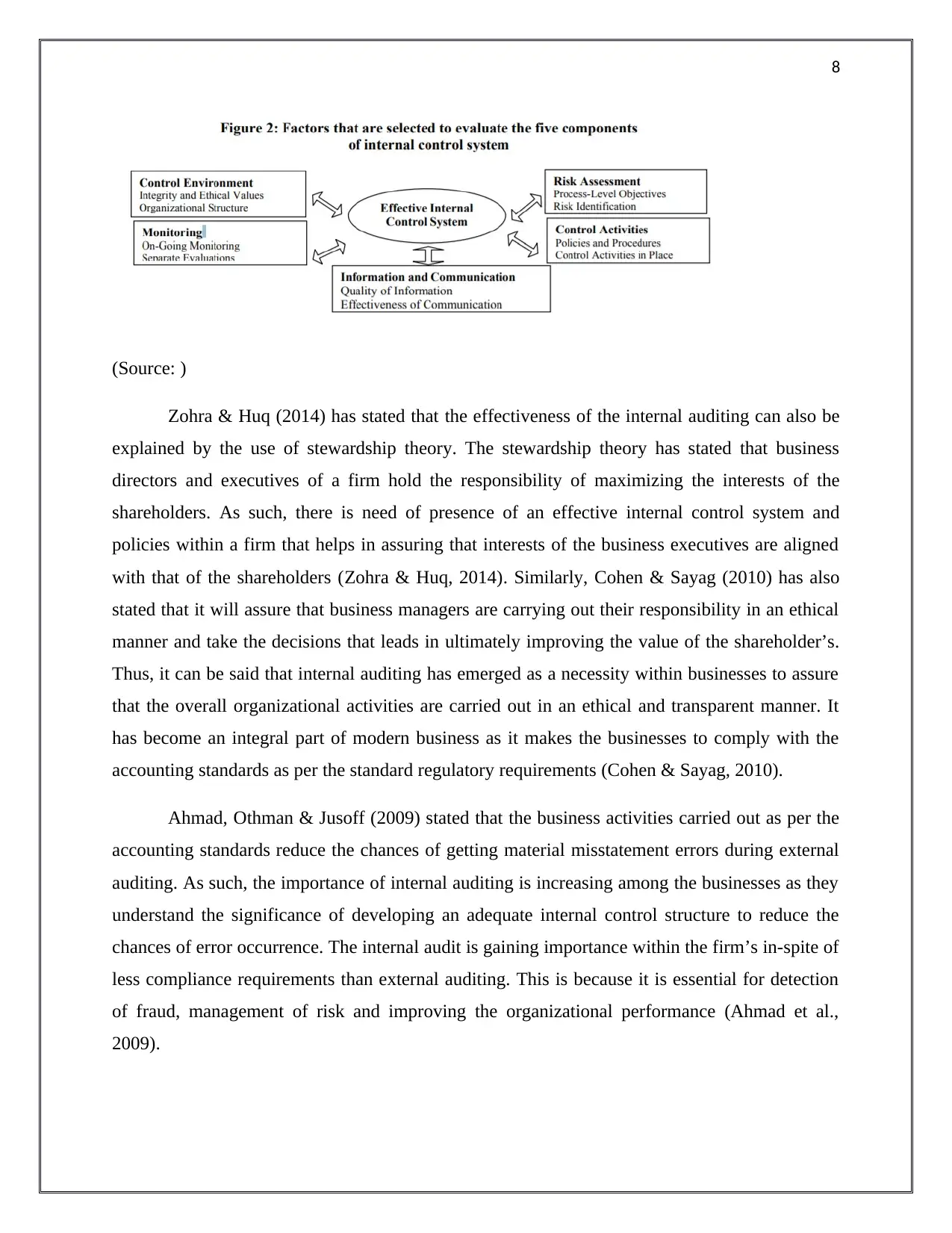

According to Rezaee (2009) the growing importance of developing an effective internal

control environment within an organization is causing the need for business to carry out the

internal audit in a regular manner. The control environment can be analyzed on the basis of the

factors such as integrity and ethical values, board committee management philosophy and

organizational structure. Alzeban (2014) has stated that the risk assessment within internal audit

can be evaluated on the basis of the factors such as process-level objectives and risk

identification. The monitoring of the governance and risk structure during the internal audit helps

the businesses for evaluating the quality of the internal system and analyzes its internal

performance (Alzeban, 2014). The factors that help in assessment of the components of an

internal control system can be depicted as follows:

structure are highlighted adequately within the internal audit. The internal auditing can be

categorized as more effective over external auditing as the presence of a strong governance

structure within a firm will help in reducing the materials misstatement errors during the

financial reporting process.

Prawitt (2009) in this context also stated that businesses need to place importance on

carrying out internal auditors in a regular manner besides only focusing on carrying out external

audit of their financial records. The fact has been highlighted by the occurrence of corporate

accounting scandals such as Enron that have highlighted the importance of having a robust

system of governing within the firms. The major benefit as per Holt & Deborah (2008) that the

management of a firm realizes by carrying out internal audit is developing a sound base for

judgment, identifying the weaknesses in control and performance. Developing suggestions for

improvement and disseminating information about the business processes that is required by all

level of management for better decision-making. It helps in examining the compliance of firms

with the established policies, plans, procedures, laws and regulations to determine that business

operations are carried out in an ethical manner (Holt & Deborah, 2008).

According to Rezaee (2009) the growing importance of developing an effective internal

control environment within an organization is causing the need for business to carry out the

internal audit in a regular manner. The control environment can be analyzed on the basis of the

factors such as integrity and ethical values, board committee management philosophy and

organizational structure. Alzeban (2014) has stated that the risk assessment within internal audit

can be evaluated on the basis of the factors such as process-level objectives and risk

identification. The monitoring of the governance and risk structure during the internal audit helps

the businesses for evaluating the quality of the internal system and analyzes its internal

performance (Alzeban, 2014). The factors that help in assessment of the components of an

internal control system can be depicted as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

(Source: )

Zohra & Huq (2014) has stated that the effectiveness of the internal auditing can also be

explained by the use of stewardship theory. The stewardship theory has stated that business

directors and executives of a firm hold the responsibility of maximizing the interests of the

shareholders. As such, there is need of presence of an effective internal control system and

policies within a firm that helps in assuring that interests of the business executives are aligned

with that of the shareholders (Zohra & Huq, 2014). Similarly, Cohen & Sayag (2010) has also

stated that it will assure that business managers are carrying out their responsibility in an ethical

manner and take the decisions that leads in ultimately improving the value of the shareholder’s.

Thus, it can be said that internal auditing has emerged as a necessity within businesses to assure

that the overall organizational activities are carried out in an ethical and transparent manner. It

has become an integral part of modern business as it makes the businesses to comply with the

accounting standards as per the standard regulatory requirements (Cohen & Sayag, 2010).

Ahmad, Othman & Jusoff (2009) stated that the business activities carried out as per the

accounting standards reduce the chances of getting material misstatement errors during external

auditing. As such, the importance of internal auditing is increasing among the businesses as they

understand the significance of developing an adequate internal control structure to reduce the

chances of error occurrence. The internal audit is gaining importance within the firm’s in-spite of

less compliance requirements than external auditing. This is because it is essential for detection

of fraud, management of risk and improving the organizational performance (Ahmad et al.,

2009).

(Source: )

Zohra & Huq (2014) has stated that the effectiveness of the internal auditing can also be

explained by the use of stewardship theory. The stewardship theory has stated that business

directors and executives of a firm hold the responsibility of maximizing the interests of the

shareholders. As such, there is need of presence of an effective internal control system and

policies within a firm that helps in assuring that interests of the business executives are aligned

with that of the shareholders (Zohra & Huq, 2014). Similarly, Cohen & Sayag (2010) has also

stated that it will assure that business managers are carrying out their responsibility in an ethical

manner and take the decisions that leads in ultimately improving the value of the shareholder’s.

Thus, it can be said that internal auditing has emerged as a necessity within businesses to assure

that the overall organizational activities are carried out in an ethical and transparent manner. It

has become an integral part of modern business as it makes the businesses to comply with the

accounting standards as per the standard regulatory requirements (Cohen & Sayag, 2010).

Ahmad, Othman & Jusoff (2009) stated that the business activities carried out as per the

accounting standards reduce the chances of getting material misstatement errors during external

auditing. As such, the importance of internal auditing is increasing among the businesses as they

understand the significance of developing an adequate internal control structure to reduce the

chances of error occurrence. The internal audit is gaining importance within the firm’s in-spite of

less compliance requirements than external auditing. This is because it is essential for detection

of fraud, management of risk and improving the organizational performance (Ahmad et al.,

2009).

9

In the opinion of Mihret & Yismaw (2007), the significance of the internal audit is

increasing within the accounting environment to attain the objectives of external auditing. The

occurrence of the global financial crisis in the year 2008 and the regulatory and economic

pressures is causing the businesses to carry out wide risk assessment and increase the

effectiveness of their internal control structures. The internal auditing helps in developing a

holistic approach for risk management by adequately addressing all the business risks. The

significant business risks such as social, ethical, financial, operational and environmental can be

adequately identified through the use of internal audit that will significantly lead in improving

the external reporting structures of the firm (Mihret & Yismaw, 2007).

Ali, Gloeck, Ali, Ahmi & Sahdan (2007) also stated in this context that the businesses

have largely understood that internal auditing is essential for them to enhance the value of their

business activities subsides only reviewing the internal control systems and processes. This is

because it leads to identification of the competent personnel and internal strengths and weakness

of a firm. The increasing efficiency of the risk management structures help in promoting the

fairness of business activities and adding value to the business outcomes. As per Zamzulaila,

Zarina & Dalila, (2007), the development of having effective internal control systems will

ultimately lead in preventing the occurrence of any financial uncertainty. The prevention of

occurrence of any financial uncertain condition begins with improving the transparency and

integrity within the business systems. This can be achieved adequately with the use of internal

auditing by the business firms and therefore it is increasing in effectiveness as compared with the

external auditing.

The overall discussion helps in the literature review has highlighted the line of difference

that exist between internal and external auditing. The internal auditing is carried out by the

internal management people of a firm while external auditing is carried out by hiring an

independent contractor know as auditor. Also, there is difference between their objectives as

internal auditing aims to review the internal control systems while external auditing evaluates the

accuracy and reliability of the external financial reports developed by a business firm. The

growing importance of internal auditing within businesses as compared to external auditing can

be attributed to developing an integrated system of internal control that will ultimately lead in

In the opinion of Mihret & Yismaw (2007), the significance of the internal audit is

increasing within the accounting environment to attain the objectives of external auditing. The

occurrence of the global financial crisis in the year 2008 and the regulatory and economic

pressures is causing the businesses to carry out wide risk assessment and increase the

effectiveness of their internal control structures. The internal auditing helps in developing a

holistic approach for risk management by adequately addressing all the business risks. The

significant business risks such as social, ethical, financial, operational and environmental can be

adequately identified through the use of internal audit that will significantly lead in improving

the external reporting structures of the firm (Mihret & Yismaw, 2007).

Ali, Gloeck, Ali, Ahmi & Sahdan (2007) also stated in this context that the businesses

have largely understood that internal auditing is essential for them to enhance the value of their

business activities subsides only reviewing the internal control systems and processes. This is

because it leads to identification of the competent personnel and internal strengths and weakness

of a firm. The increasing efficiency of the risk management structures help in promoting the

fairness of business activities and adding value to the business outcomes. As per Zamzulaila,

Zarina & Dalila, (2007), the development of having effective internal control systems will

ultimately lead in preventing the occurrence of any financial uncertainty. The prevention of

occurrence of any financial uncertain condition begins with improving the transparency and

integrity within the business systems. This can be achieved adequately with the use of internal

auditing by the business firms and therefore it is increasing in effectiveness as compared with the

external auditing.

The overall discussion helps in the literature review has highlighted the line of difference

that exist between internal and external auditing. The internal auditing is carried out by the

internal management people of a firm while external auditing is carried out by hiring an

independent contractor know as auditor. Also, there is difference between their objectives as

internal auditing aims to review the internal control systems while external auditing evaluates the

accuracy and reliability of the external financial reports developed by a business firm. The

growing importance of internal auditing within businesses as compared to external auditing can

be attributed to developing an integrated system of internal control that will ultimately lead in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

reducing the error occurrence within the external financial reports developed (Azzali & Mazza,

2018).

Research Method

Research method aims to provide the structure using which the research can be conducted

in systematic way. It is highly important to give proper consideration and importance to research

methods as it helps in providing the smoother platform for carrying out the research. Research

method is complete guiding map necessary for organizing, arranging and conducting the research

process in right manner so that it can completed in specified manner and in estimated time frame.

After framing the research question or questions, it is essential to collect the desired data

and information related to research question. The data and information helps research to

understand the research topic further and it also paves the path of achieving the research

objectives. The role of research methods is to set the research tools that can be used to gather the

data and information in proper manner so that no ethical violations can be done. As research

methodology deals with various aspects of research, it has been divided in various sub parts such

as research approach, research design, research method, data collection process, sample selection

process, methods of data of analysis and lastly ethical considerations (Gliner & Morgan, 2012).

Research Approach

There are mainly two types of research approaches that can be applied in research and

these research approaches are inductive and deductive research approach. In order to select the

correct research approach there is need to have adequate understanding of research objectives.

Both these research approaches differs on ground of their movement and manner used for

gathering data and evidences. Inductive research approach is known as bottom up research

approach and it moves from specific to general theory i.e. it collect facts and evidences for

specific context and analyze them to provide general observations. On the other hand, deductive

research approach moves from general to specific and it is the reason why it is known as top

down approach. It means general evidences and information is gathered to draw the conclusion

regarding the specific topic and subject (Hendricks, 2011).

reducing the error occurrence within the external financial reports developed (Azzali & Mazza,

2018).

Research Method

Research method aims to provide the structure using which the research can be conducted

in systematic way. It is highly important to give proper consideration and importance to research

methods as it helps in providing the smoother platform for carrying out the research. Research

method is complete guiding map necessary for organizing, arranging and conducting the research

process in right manner so that it can completed in specified manner and in estimated time frame.

After framing the research question or questions, it is essential to collect the desired data

and information related to research question. The data and information helps research to

understand the research topic further and it also paves the path of achieving the research

objectives. The role of research methods is to set the research tools that can be used to gather the

data and information in proper manner so that no ethical violations can be done. As research

methodology deals with various aspects of research, it has been divided in various sub parts such

as research approach, research design, research method, data collection process, sample selection

process, methods of data of analysis and lastly ethical considerations (Gliner & Morgan, 2012).

Research Approach

There are mainly two types of research approaches that can be applied in research and

these research approaches are inductive and deductive research approach. In order to select the

correct research approach there is need to have adequate understanding of research objectives.

Both these research approaches differs on ground of their movement and manner used for

gathering data and evidences. Inductive research approach is known as bottom up research

approach and it moves from specific to general theory i.e. it collect facts and evidences for

specific context and analyze them to provide general observations. On the other hand, deductive

research approach moves from general to specific and it is the reason why it is known as top

down approach. It means general evidences and information is gathered to draw the conclusion

regarding the specific topic and subject (Hendricks, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

In this research study the focus is use the inductive research approach as helps to satisfy

the research objectives. As the purpose of the research study is to provide the general views on

effectiveness of internal auditing and compare it with the external auditing, so it is required to

gather data from some of large companies in Singapore and analyze them to provide arguments

in favor and against the framed research question. Inductive research approach will provide

proper platform to gather the specific data and information in relation to the research objectives.

Further it will help to analyze the gather data in required manner to make general comment on

research questions.

Research Design

Research design is the most important part in the whole research study as this research

tools provides the basis for defining the manner through data and information can be collected.

Research design provides the framework on which entire process of data collection and analysis

depends. It means research design is the way to get the reliable and valid research outcomes

(Gillham, 2010).

According to research question, it is important to use the exploratory research design as it

best research design for this research study. Exploratory research design aims to investigate the

facts and information in detailed manner so that proper understanding of concerned research

topic can be made. Explorative research provide a platform through which each single aspect of

research can be investigate thoroughly so to conduct the research in optimum manner. Research

topic selected is very vast and requires exploring multiple aspects in minimum time and it can be

done only when exploratory research design has been selected (Fowler, 2012).

Research method for data collection

The tools and techniques used to collect the information have been defined under

research method area of the research study. The proper selection of research method helps to

gather both qualitative and quantitative research data. The two main research methods that are

viable for this research study are primary and secondary methods. Both these research methods

differ on the grounds of manner of collection the data and information. Primary research method

of data collection aims to provide original nature of data collection as it collects data directly

from the source it generates. So it can be said that primary research method of data collection

In this research study the focus is use the inductive research approach as helps to satisfy

the research objectives. As the purpose of the research study is to provide the general views on

effectiveness of internal auditing and compare it with the external auditing, so it is required to

gather data from some of large companies in Singapore and analyze them to provide arguments

in favor and against the framed research question. Inductive research approach will provide

proper platform to gather the specific data and information in relation to the research objectives.

Further it will help to analyze the gather data in required manner to make general comment on

research questions.

Research Design

Research design is the most important part in the whole research study as this research

tools provides the basis for defining the manner through data and information can be collected.

Research design provides the framework on which entire process of data collection and analysis

depends. It means research design is the way to get the reliable and valid research outcomes

(Gillham, 2010).

According to research question, it is important to use the exploratory research design as it

best research design for this research study. Exploratory research design aims to investigate the

facts and information in detailed manner so that proper understanding of concerned research

topic can be made. Explorative research provide a platform through which each single aspect of

research can be investigate thoroughly so to conduct the research in optimum manner. Research

topic selected is very vast and requires exploring multiple aspects in minimum time and it can be

done only when exploratory research design has been selected (Fowler, 2012).

Research method for data collection

The tools and techniques used to collect the information have been defined under

research method area of the research study. The proper selection of research method helps to

gather both qualitative and quantitative research data. The two main research methods that are

viable for this research study are primary and secondary methods. Both these research methods

differ on the grounds of manner of collection the data and information. Primary research method

of data collection aims to provide original nature of data collection as it collects data directly

from the source it generates. So it can be said that primary research method of data collection

12

provide first hand (exclusive) information as this data has not been used by anyone else. On the

other hand secondary research method provides data and information that has already been

collected by someone and has been analyzed to reach at some conclusion. It means data and

information provided in already completed researches are used in secondary research method to

extract the required information. Some of important secondary sources of finance are research

articles, journals, research reports, online articles, newspapers, published articles etc. The main

reason why the secondary sources of data is collected and analyzed is to support the primary

data.

Primary research method for data collection is very important for this research study and

it has been decided to use survey method through applying interview technique. So detailed

survey questions will be drafted and asked with internal auditors as well as external auditors of

large firms in Singapore. Survey questions will be defined and same for all the respondents so to

make sure that data analysis can be performed in systematic manner. Interview questions are

framed in such a manner that they would be helpful in extracting the information that is useful

for this research. All the questions will be open ended as it would help to gain maximum

information those respondents. The purpose of using the open ended questions in survey research

data collection method is because it gives respondents a freedom to express their views, opinions

and perspectives. The questions list is build in a manner that it can to achieve the maximum

information from the respondents. Some questions will be general and some will specific to

ensure that desirable information can be gathered to achieve the research objectives (Fink, 2015).

Secondary research method for data collection is used to perform the literature review in

order to support facts and information that has been gathered for primary research purpose. As

this research is on effectiveness of internal auditing and how it more important than the external

reporting, there is need to make sure that all relevant literatures should be gathered and analyzed

in literature review.

Sample selection is an important criterion to decide how respondents for the purpose of

primary research will be decided so that research can be performed in proper manner. It has been

decided to use random sampling for the purpose of primary data collection. Request for

interview will be sent to all the members of selected for the sample and those members are

selected that answer the request. Total 50 respondents will be selected from the list of

provide first hand (exclusive) information as this data has not been used by anyone else. On the

other hand secondary research method provides data and information that has already been

collected by someone and has been analyzed to reach at some conclusion. It means data and

information provided in already completed researches are used in secondary research method to

extract the required information. Some of important secondary sources of finance are research

articles, journals, research reports, online articles, newspapers, published articles etc. The main

reason why the secondary sources of data is collected and analyzed is to support the primary

data.

Primary research method for data collection is very important for this research study and

it has been decided to use survey method through applying interview technique. So detailed

survey questions will be drafted and asked with internal auditors as well as external auditors of

large firms in Singapore. Survey questions will be defined and same for all the respondents so to

make sure that data analysis can be performed in systematic manner. Interview questions are

framed in such a manner that they would be helpful in extracting the information that is useful

for this research. All the questions will be open ended as it would help to gain maximum

information those respondents. The purpose of using the open ended questions in survey research

data collection method is because it gives respondents a freedom to express their views, opinions

and perspectives. The questions list is build in a manner that it can to achieve the maximum

information from the respondents. Some questions will be general and some will specific to

ensure that desirable information can be gathered to achieve the research objectives (Fink, 2015).

Secondary research method for data collection is used to perform the literature review in

order to support facts and information that has been gathered for primary research purpose. As

this research is on effectiveness of internal auditing and how it more important than the external

reporting, there is need to make sure that all relevant literatures should be gathered and analyzed

in literature review.

Sample selection is an important criterion to decide how respondents for the purpose of

primary research will be decided so that research can be performed in proper manner. It has been

decided to use random sampling for the purpose of primary data collection. Request for

interview will be sent to all the members of selected for the sample and those members are

selected that answer the request. Total 50 respondents will be selected from the list of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.