UAEU Internal Auditing: Chapter 1 Introduction and Key Components

VerifiedAdded on 2022/07/08

|25

|2439

|12

Report

AI Summary

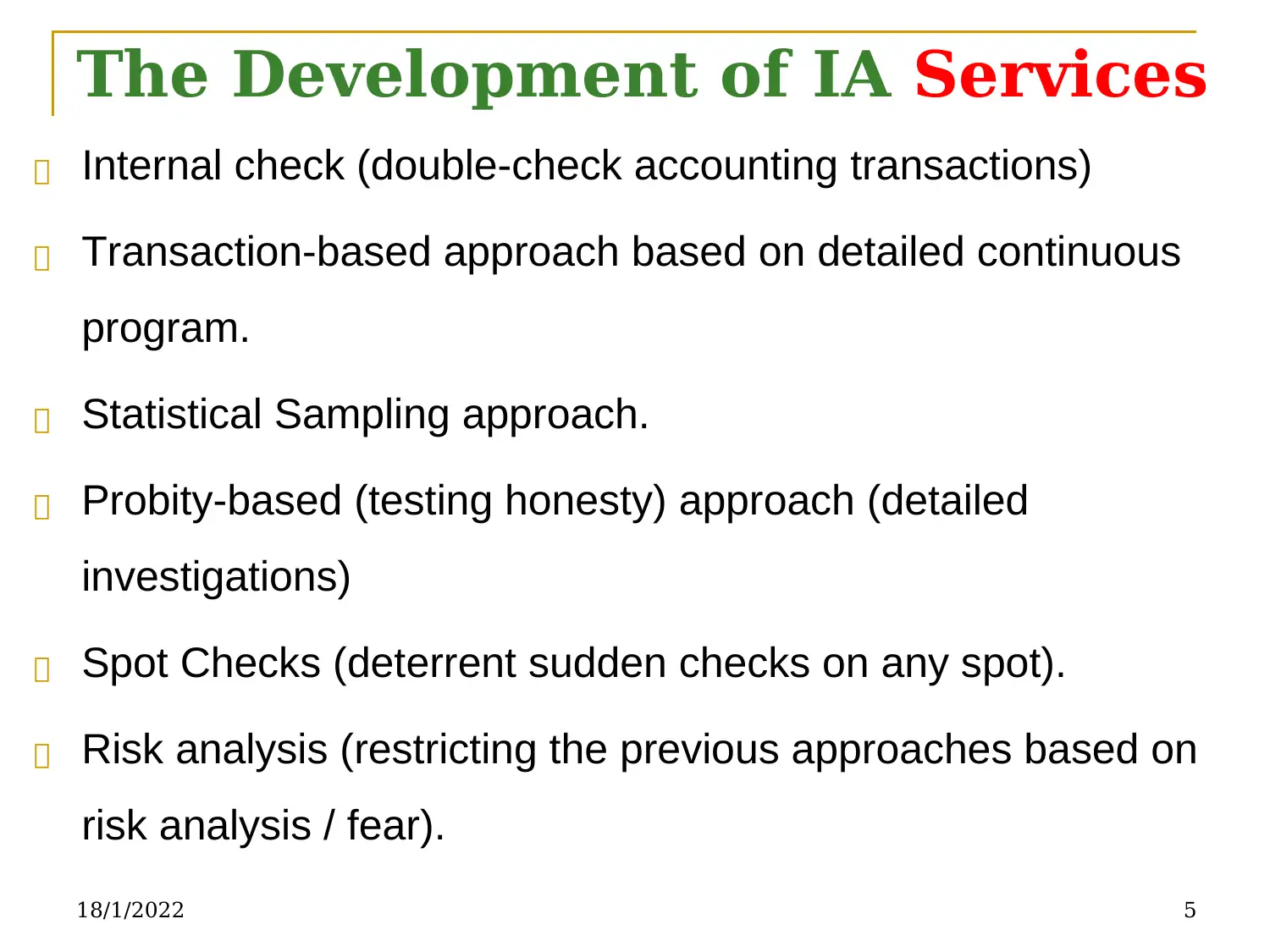

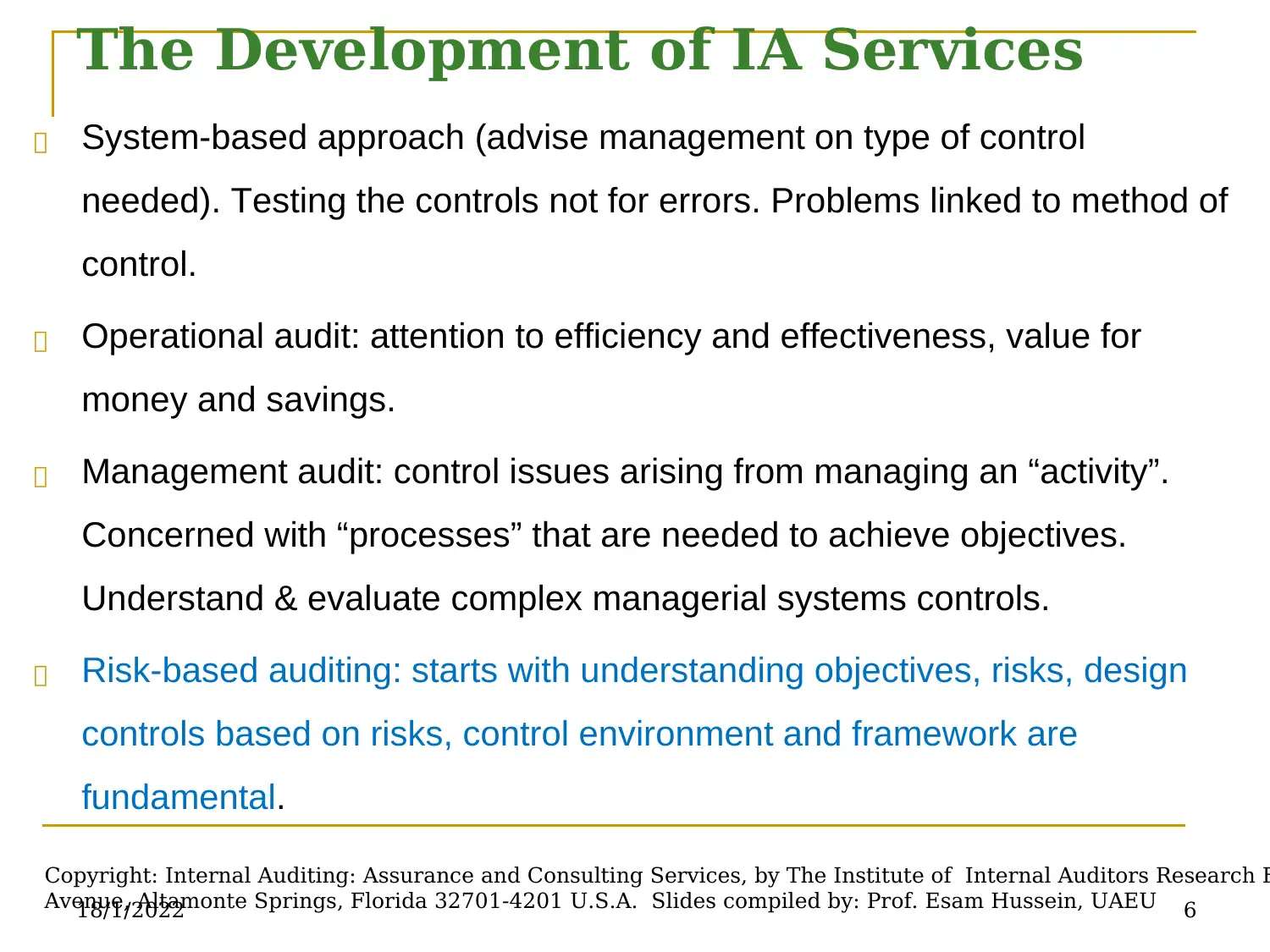

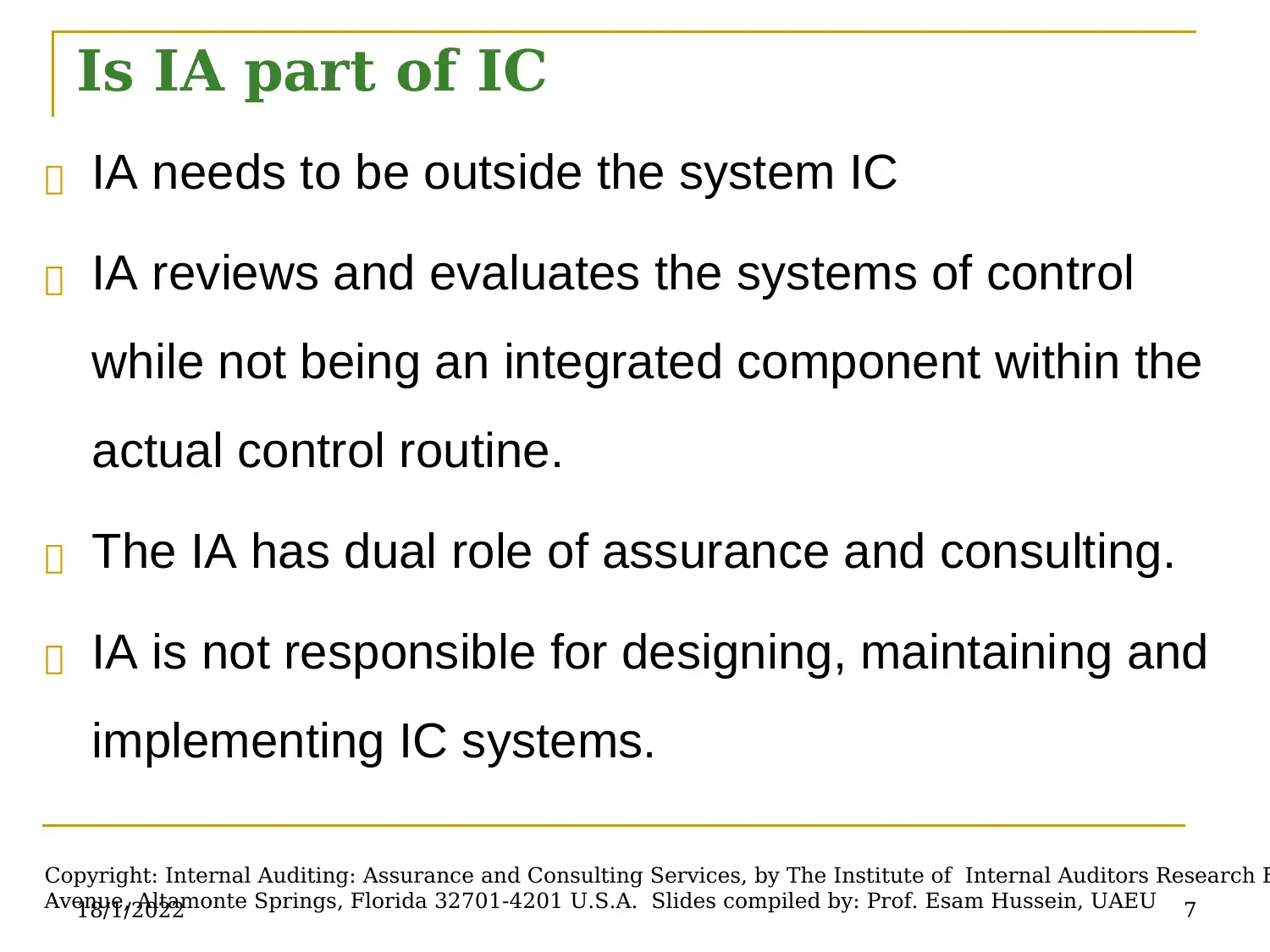

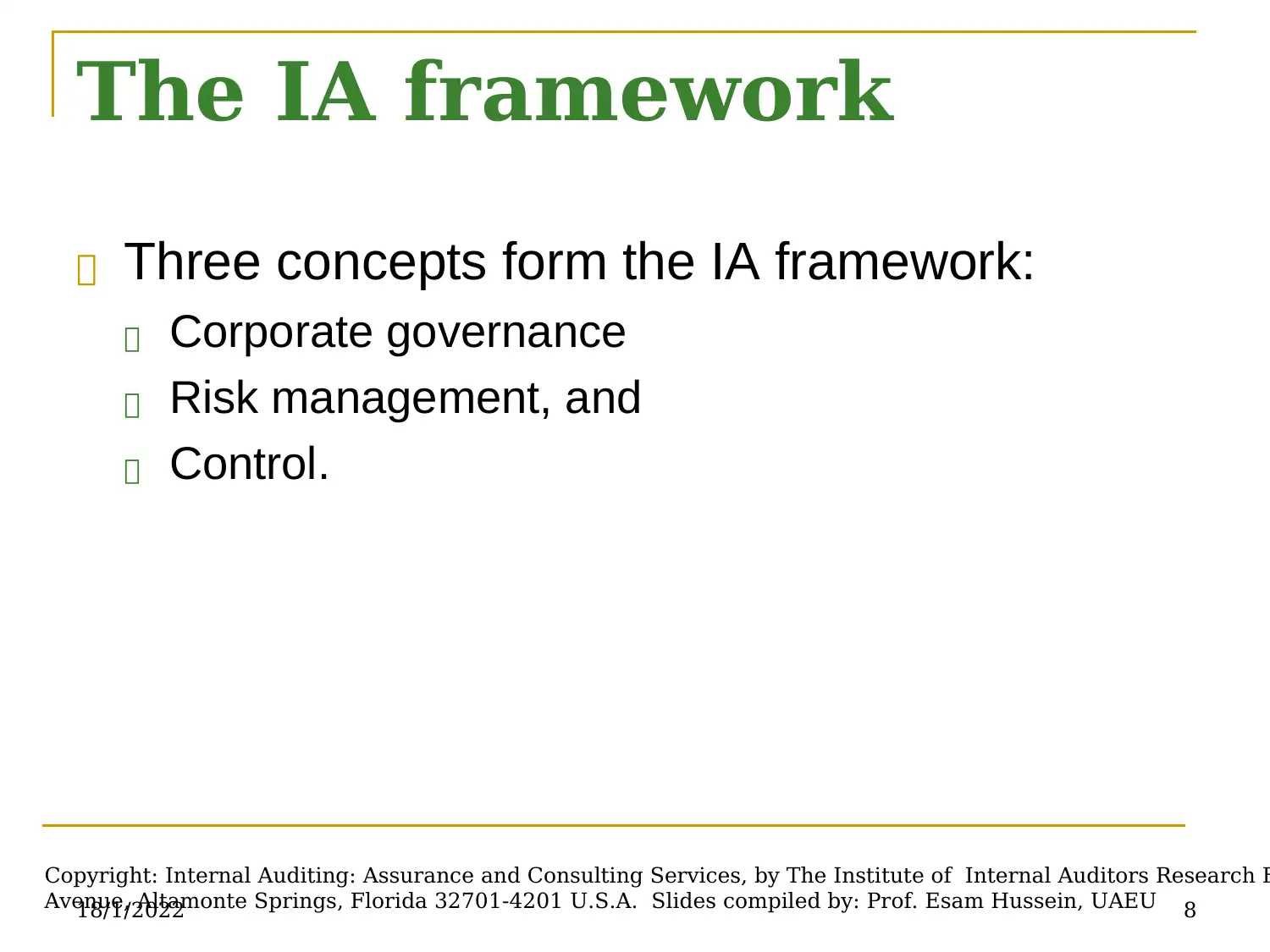

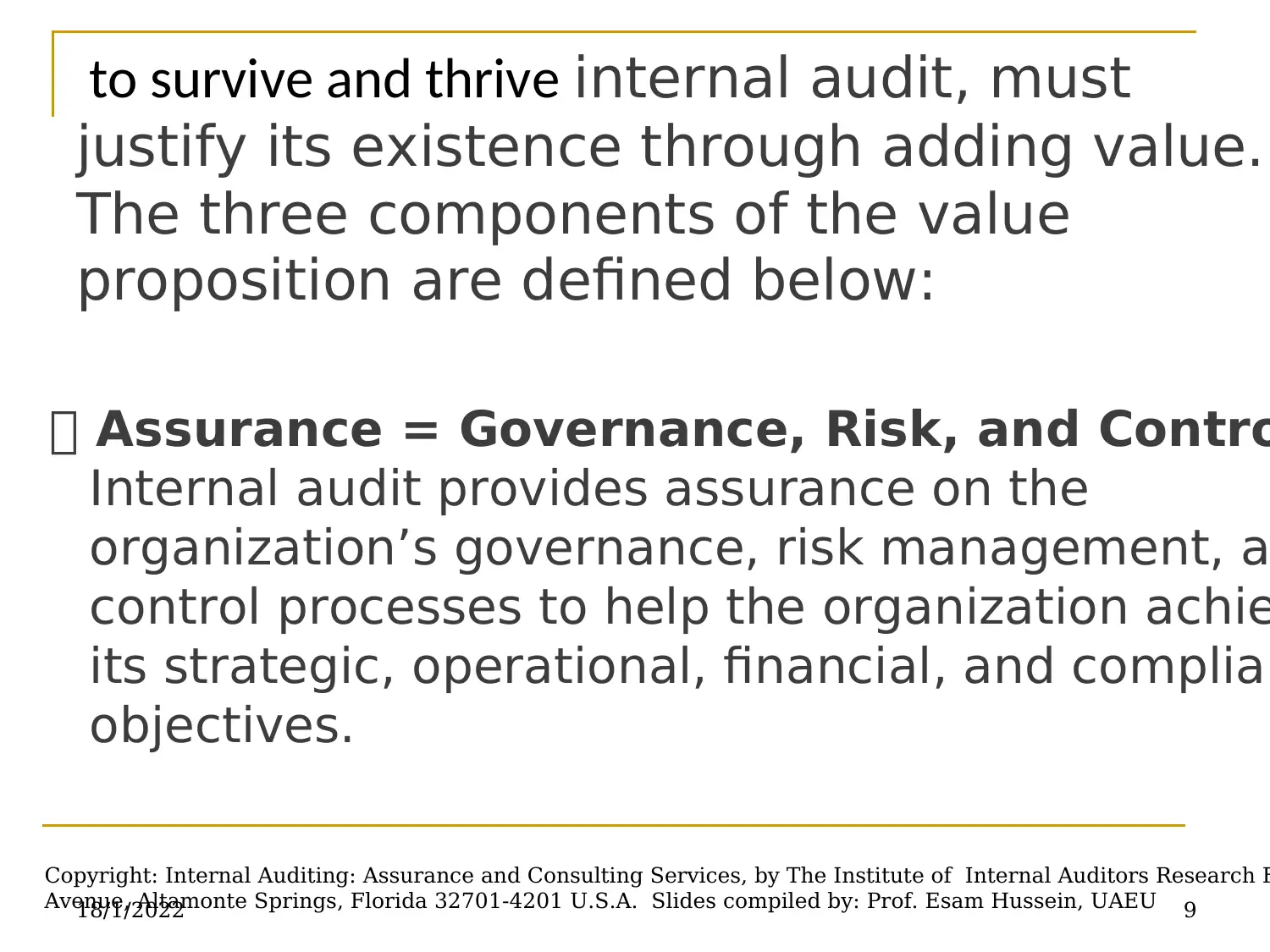

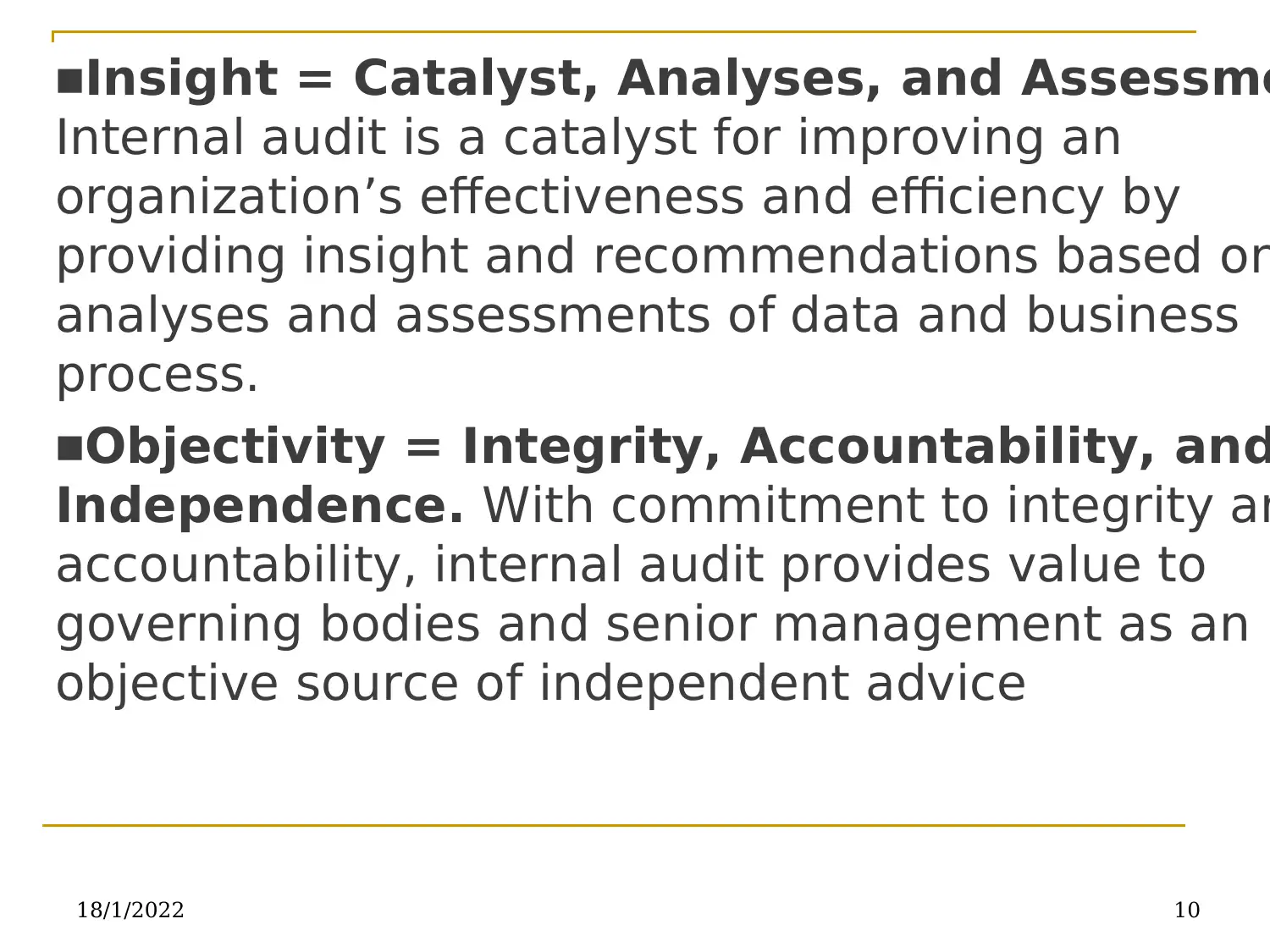

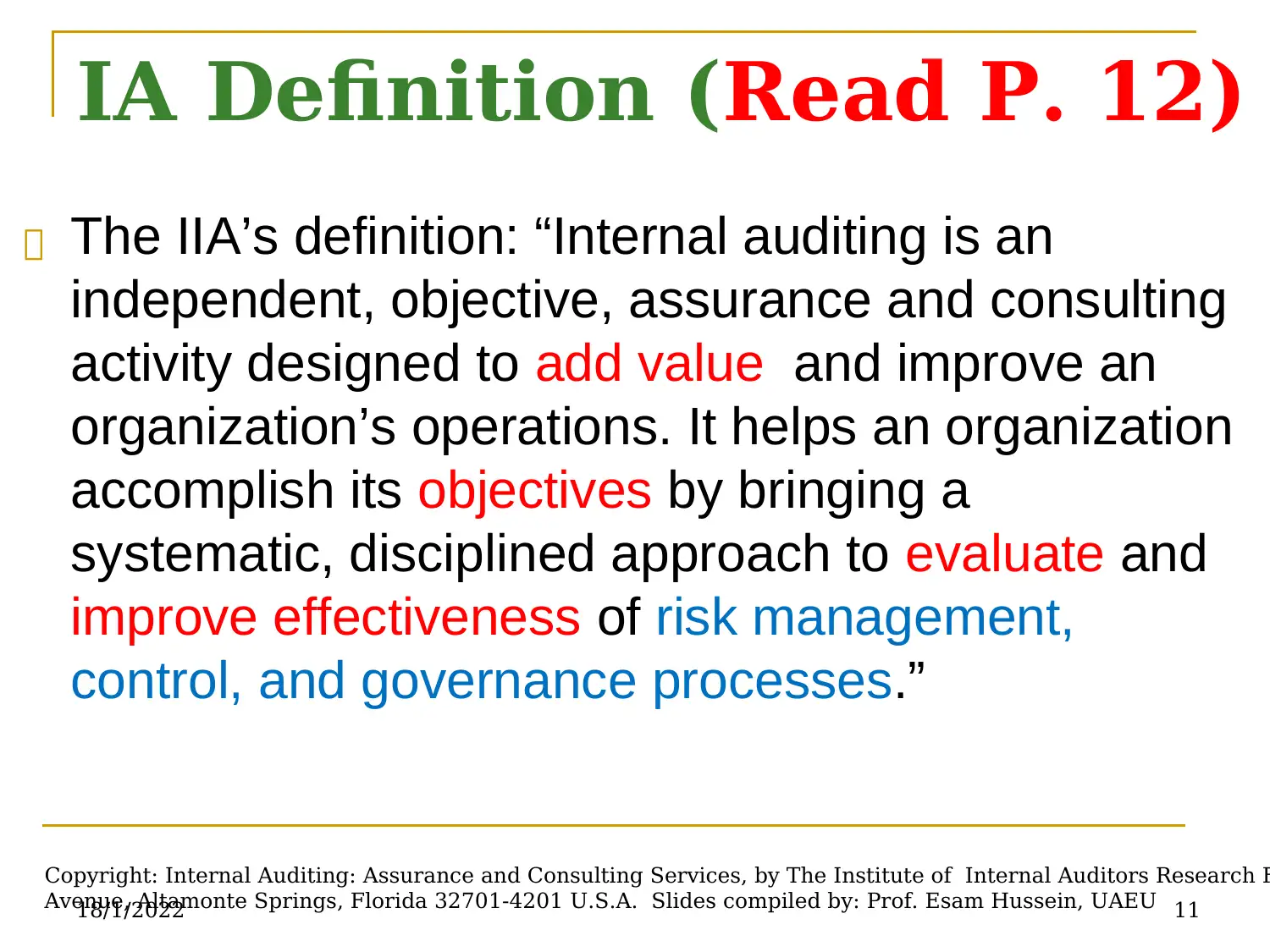

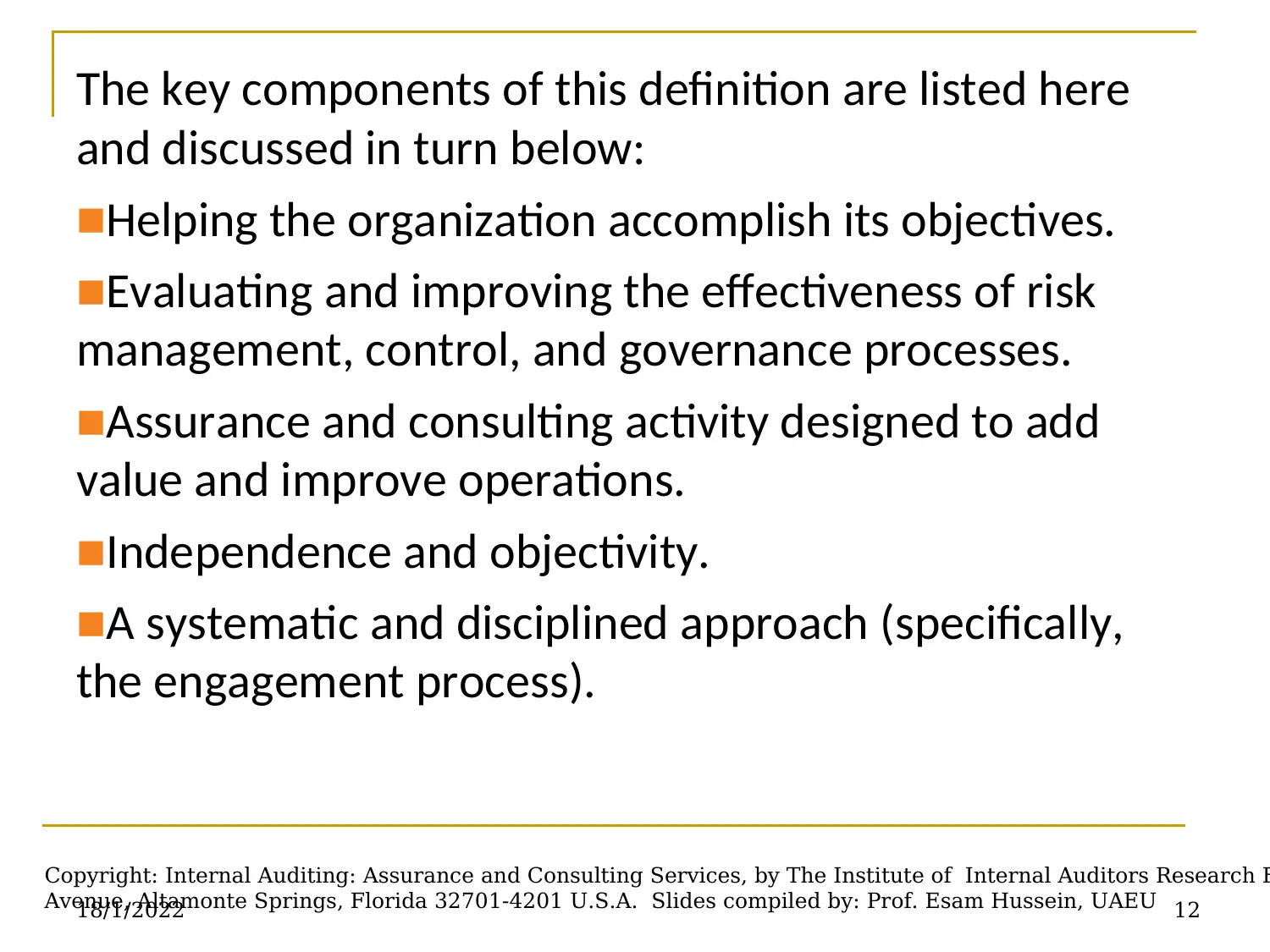

This document provides a comprehensive overview of internal auditing, drawing from Chapter 1 of the Internal Auditing: Assurance and Consulting Services textbook. It begins by outlining the learning objectives, which include understanding the internal audit process, its relationship to accounting, and the distinction between internal and external auditing. The document traces the historical development of internal auditing, from its origins as an extension of external audits to its evolution into a critical function focused on assurance and consulting. It delves into the various services offered by internal auditing, including transaction-based, system-based, and risk-based approaches, and clarifies the role of internal auditing within the framework of corporate governance, risk management, and control. The definition of internal auditing, as provided by The Institute of Internal Auditors (IIA), is examined, highlighting its key components such as adding value and improving operations, independence, and objectivity. The document also explores the objectives, strategy, and functions of internal auditing, including assurance and consulting services, and the three fundamental phases of the internal audit engagement process: planning, performing, and communicating outcomes. The differences between internal and external auditing are clarified, as are the procedures employed by internal auditors. Finally, the document touches upon co-sourcing in internal auditing.

1 out of 25

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.