Comprehensive Evaluation of Internal Control Systems in Finance

VerifiedAdded on 2020/04/01

|8

|1690

|110

Report

AI Summary

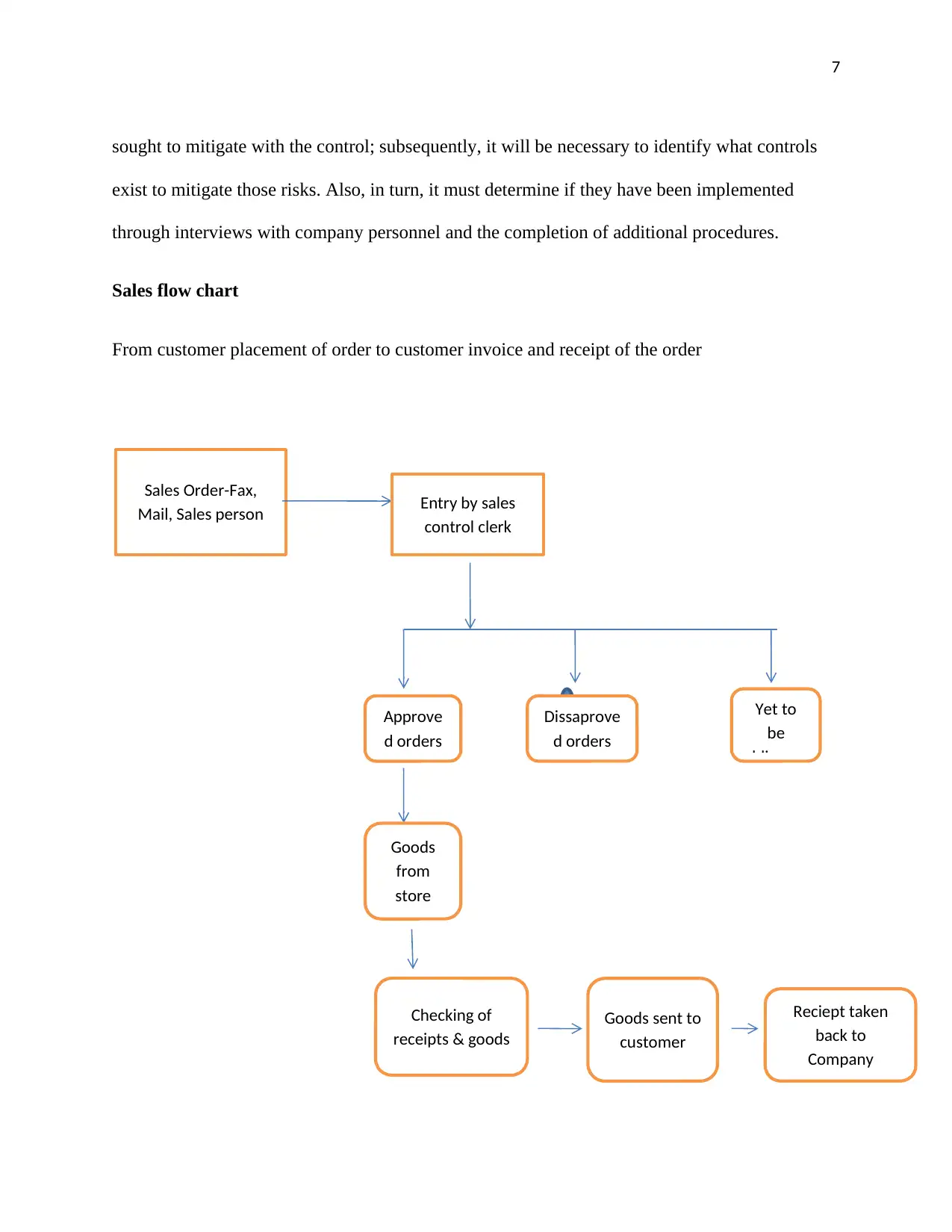

This report provides an evaluation of a company's internal control processes, focusing on the sales system. It begins with an introduction to the auditor's responsibility in assessing and testing internal controls. The report identifies and analyzes strengths, such as robust order processing and verification mechanisms, and weaknesses, including potential staff collusion and lack of backup systems. It discusses the implications of these weaknesses, including potential financial losses and data integrity issues. Furthermore, the report addresses control risk assessment, emphasizing the importance of mitigating significant risks that could affect financial statements. The analysis covers the five key components of internal control, as defined by the COSO framework, including the control environment, risk assessment, control activities, information and communication, and monitoring activities. The report concludes by reiterating the auditor's role in evaluating the design and implementation of internal controls and includes a sales flow chart illustrating the order process. The report draws upon various references related to auditing, internal control, and security management.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.