Platinum Manufacturing Group: Internal Control Weakness Assessment

VerifiedAdded on 2023/06/12

|12

|2319

|143

Report

AI Summary

This report identifies and assesses internal control weaknesses within Platinum Manufacturing Group's purchase process. The primary weakness identified is the lack of proper documentation and the complexity of the current process. The report recommends adopting ICT solutions, restructuring the purchase process by forming dedicated teams, implementing e-procurement, and establishing a monitoring team to oversee purchasing activities. These measures aim to improve documentation, simplify processes, reduce fraud risks, and ensure better resource utilization. The report concludes by affirming the flexibility of the recommended measures and their compatibility with modern IT infrastructure, emphasizing the importance of training and adaptability in implementing these changes for sustainable organizational improvement.

Running head: ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Name of the Student

Name of the University

Author Note

ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Executive Summary:

Purchase process is one of the most concerned process for an organisation because of the

loopholes that exists within it. The complexity with the discussed process is further enhanced

if internal control weaknesses are identified within it. The discussed paper has taken

consideration of Platinum manufacturing group and identified the internal control weakness

existing within it. Depending on the identification recommendations have been made that can

assist in mitigating the identified internal control weakness. The identified weakness was

related to the documentation and complexity of the process for which adoption of ICT and

formulating of team to monitor and carry the process has been recommended. Adopting the

discussed measures may mitigate the challenges associated with the organisational purchase

process. The discussed report has been concluded with reviewing of the flexibility of the

recommended measures and whether or not they are compatible with modern IT

infrastructure of an organisation.

Executive Summary:

Purchase process is one of the most concerned process for an organisation because of the

loopholes that exists within it. The complexity with the discussed process is further enhanced

if internal control weaknesses are identified within it. The discussed paper has taken

consideration of Platinum manufacturing group and identified the internal control weakness

existing within it. Depending on the identification recommendations have been made that can

assist in mitigating the identified internal control weakness. The identified weakness was

related to the documentation and complexity of the process for which adoption of ICT and

formulating of team to monitor and carry the process has been recommended. Adopting the

discussed measures may mitigate the challenges associated with the organisational purchase

process. The discussed report has been concluded with reviewing of the flexibility of the

recommended measures and whether or not they are compatible with modern IT

infrastructure of an organisation.

2ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Table of Contents

Overview of the Expenditure Process for special order.............................................................3

Level 0 data flow Diagram.........................................................................................................4

Identification..............................................................................................................................5

a. Internal control Weakness (ICW)...................................................................................5

b. Impact of ICW.................................................................................................................5

c. Specific Internal Controls...............................................................................................6

d. Flexibility of the recommended measures......................................................................8

Bibliography:..............................................................................................................................9

Table of Contents

Overview of the Expenditure Process for special order.............................................................3

Level 0 data flow Diagram.........................................................................................................4

Identification..............................................................................................................................5

a. Internal control Weakness (ICW)...................................................................................5

b. Impact of ICW.................................................................................................................5

c. Specific Internal Controls...............................................................................................6

d. Flexibility of the recommended measures......................................................................8

Bibliography:..............................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Overview of the Expenditure Process for special order

The head of the department forms a purchasing requisition and sent it to the

purchasing department which is then verified by one of the buyer out of five that the request

has been made by the department head. Post-verification the buyer selects appropriate vendor

and places a verbal order while demanding a price quotation. Then a “pre-numbered purchase

order (PNPO)” is processed and forwarded to different departments. On receiving the PNPO

the receiving department then validates the order and forward it along with the equipment to

the requisitioning depart while notifying the purchasing department. In the next step, the

accounts verify the vendor’s invoice and the PPNO and creates a payable check which is then

forwarded to the treasurer who verifies the demand and signs the check. The expenditure

process of the special orders from purchase to payment is thus completed.

Overview of the Expenditure Process for special order

The head of the department forms a purchasing requisition and sent it to the

purchasing department which is then verified by one of the buyer out of five that the request

has been made by the department head. Post-verification the buyer selects appropriate vendor

and places a verbal order while demanding a price quotation. Then a “pre-numbered purchase

order (PNPO)” is processed and forwarded to different departments. On receiving the PNPO

the receiving department then validates the order and forward it along with the equipment to

the requisitioning depart while notifying the purchasing department. In the next step, the

accounts verify the vendor’s invoice and the PPNO and creates a payable check which is then

forwarded to the treasurer who verifies the demand and signs the check. The expenditure

process of the special orders from purchase to payment is thus completed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

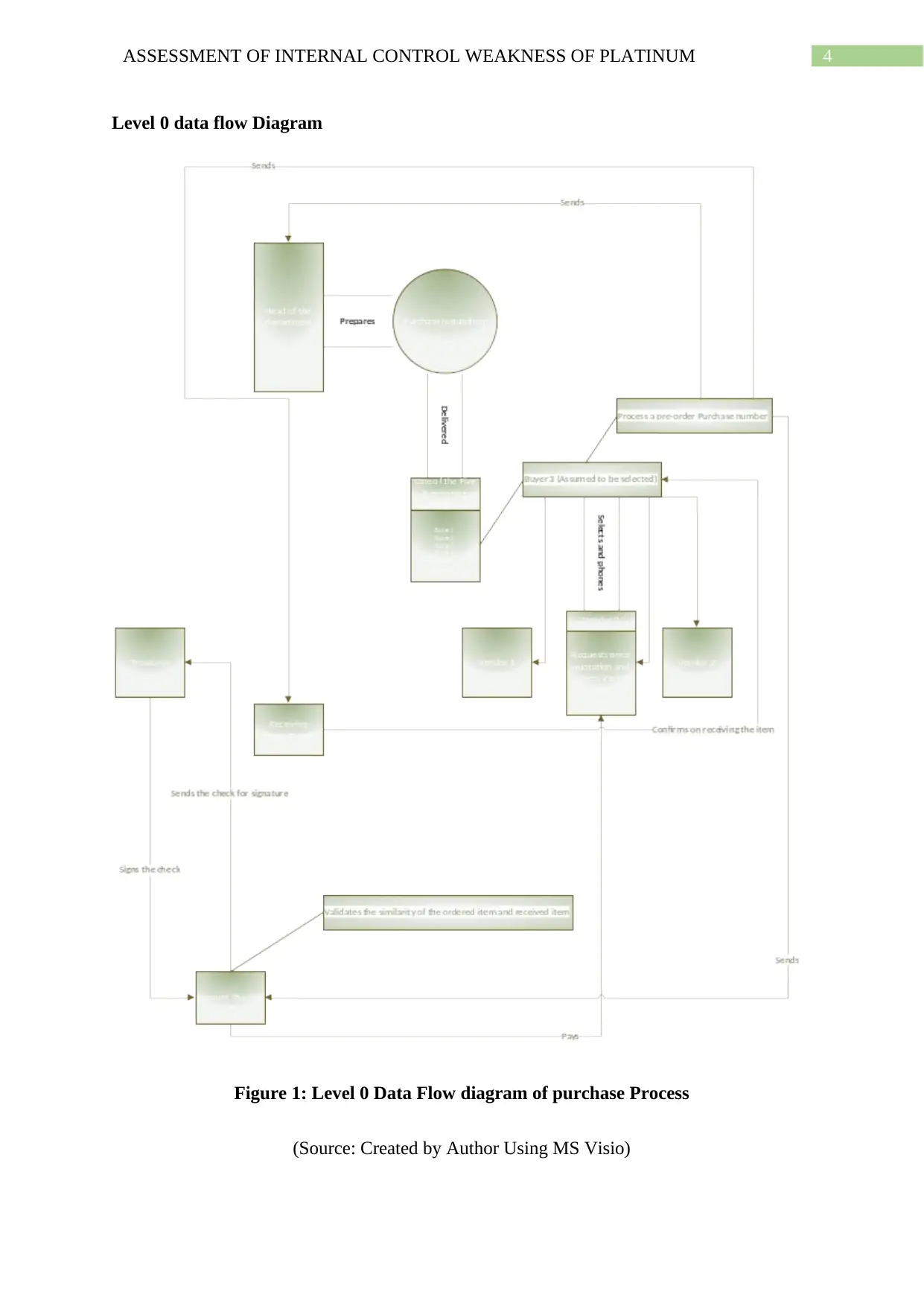

Level 0 data flow Diagram

Figure 1: Level 0 Data Flow diagram of purchase Process

(Source: Created by Author Using MS Visio)

Level 0 data flow Diagram

Figure 1: Level 0 Data Flow diagram of purchase Process

(Source: Created by Author Using MS Visio)

5ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Identification

a. Internal control Weakness (ICW)

The internal control weakness of a purchasing process is defined as the deficiency or

deficiencies cited by the organisation in their financial transaction processes (Zakaria,

Nawawi & Salin, 2016). It forms the perception that the organisation suffering from ICW is

unaware of its financial situation and can cite a negative impact on the goodwill of the

organisation (De Simone, Ege & Stomberg, 2014). The purchase to payment process of the

deemed organisation is full of internal control weakness and the foremost among them is the

lack of proper documentation. On evaluation, it is evident that the organisation uses verbal

notification very much in their purchase process rather than using written notification. The

lack of written notification leads to lack of documentation/records which can create

challenges for different financial operation including tax returns, tracing of data and similar

others.

Additionally, the process of purchasing to payment process is very complexed in the

case of Platinum and the role of the involved stakeholders are even not clear which is evident

from the level 0 data flow diagram attached above. The organisation has different sections for

different purchase processes however, shifting the process from multiple level increases the

complexity and with lack of documentation, in dire situations no one will take the

responsibility for the processes. Hence, it can be stated that there is a need for restructuring of

the purchase to payment procedure of special orders of the deemed organisation.

b. Impact of ICW

The impact of ICW is significance on any organisation and the deemed organisation is no

exception. The identification of purchase details during the auditing process will be very

Identification

a. Internal control Weakness (ICW)

The internal control weakness of a purchasing process is defined as the deficiency or

deficiencies cited by the organisation in their financial transaction processes (Zakaria,

Nawawi & Salin, 2016). It forms the perception that the organisation suffering from ICW is

unaware of its financial situation and can cite a negative impact on the goodwill of the

organisation (De Simone, Ege & Stomberg, 2014). The purchase to payment process of the

deemed organisation is full of internal control weakness and the foremost among them is the

lack of proper documentation. On evaluation, it is evident that the organisation uses verbal

notification very much in their purchase process rather than using written notification. The

lack of written notification leads to lack of documentation/records which can create

challenges for different financial operation including tax returns, tracing of data and similar

others.

Additionally, the process of purchasing to payment process is very complexed in the

case of Platinum and the role of the involved stakeholders are even not clear which is evident

from the level 0 data flow diagram attached above. The organisation has different sections for

different purchase processes however, shifting the process from multiple level increases the

complexity and with lack of documentation, in dire situations no one will take the

responsibility for the processes. Hence, it can be stated that there is a need for restructuring of

the purchase to payment procedure of special orders of the deemed organisation.

b. Impact of ICW

The impact of ICW is significance on any organisation and the deemed organisation is no

exception. The identification of purchase details during the auditing process will be very

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

difficult for the organisation because the organisation believes in verbal notifications and no

data is maintained adequately. Additionally, the auditing assist in devising plans for the

future financial investment that ensures the sustainability of the organisation and as the

auditing process would be inadequate due to the ICW, it will cite negative impact on the

organisational sustainability. The purchase data are also needed for filing tax returns and as

the deemed organisation lacks in the discussed field, hence, it can lead the organisation to

face legal constraints which are time consuming and cites very strong negative impact on the

organisation both internally and externally. Additionally, the complexity involved in the

purchase process leads to improper utilisation of the organisational resources which is also

undesirable for an organisation. The improper utilisation refers to the extra effort invested by

the human resources, inadequate informational resources and others (Clinton, Pinello &

Skaife, 2014). Hence, it can be emphasised that the ICW should be omitted in the shortest

possible time to ensure a long-time organisational run.

c. Specific Internal Controls

The following internal control measures can be implemented by the organisation to

mitigate the threats posed by the above-identified ICW.

Proper documentation: The first and foremost measure that the organisation direly

needs to adopt is proper documentation. To achieve the discussed measure, the

organisation should take assistance of the ICT (Information Communication &

Technology) (Sadiq & Governatori, 2015). The organisation should adopt and

more importantly enforce non-verbal communication by forcing the internal

stakeholders to make their conversation over non-verbal media such as the

emailing services, instant chats and similar tools. A monthly, audit of the

communication among the internal stakeholders should also be done to ensure that

difficult for the organisation because the organisation believes in verbal notifications and no

data is maintained adequately. Additionally, the auditing assist in devising plans for the

future financial investment that ensures the sustainability of the organisation and as the

auditing process would be inadequate due to the ICW, it will cite negative impact on the

organisational sustainability. The purchase data are also needed for filing tax returns and as

the deemed organisation lacks in the discussed field, hence, it can lead the organisation to

face legal constraints which are time consuming and cites very strong negative impact on the

organisation both internally and externally. Additionally, the complexity involved in the

purchase process leads to improper utilisation of the organisational resources which is also

undesirable for an organisation. The improper utilisation refers to the extra effort invested by

the human resources, inadequate informational resources and others (Clinton, Pinello &

Skaife, 2014). Hence, it can be emphasised that the ICW should be omitted in the shortest

possible time to ensure a long-time organisational run.

c. Specific Internal Controls

The following internal control measures can be implemented by the organisation to

mitigate the threats posed by the above-identified ICW.

Proper documentation: The first and foremost measure that the organisation direly

needs to adopt is proper documentation. To achieve the discussed measure, the

organisation should take assistance of the ICT (Information Communication &

Technology) (Sadiq & Governatori, 2015). The organisation should adopt and

more importantly enforce non-verbal communication by forcing the internal

stakeholders to make their conversation over non-verbal media such as the

emailing services, instant chats and similar tools. A monthly, audit of the

communication among the internal stakeholders should also be done to ensure that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

they are using the tools for productive means and are not using it to fulfil personal

agenda or interests.

Structuring the Purchase process: Another notable measure that the organisation

can adopt to mitigate the ICW risk is restructuring the purchase process and

instead of letting the purchase process run around all the departments, the

organisation can strictly allocate the job to particular staffs or teams (Ballesteros,

pan, batten & Li, 2015). Another measure that the organisation can adopt is that it

can provide full authority for a purchase process to a specific team consisting of a

manager, an accounting clerk, a buyer, a professional (of the subject that the

organisation is buying) and other necessary staffs. It would ensure that the

purchase process is simple and the data will be collective which the senior

officials should audit post completion of the purchase process to identify the

validity and ethnicity of the whole purchase procedure.

Adopting e-procurement: The organisation can also move towards adoption of e-

procurement. In the deemed process the purchasing process between organisations

are done electronically (Wicaksono, Urumsah & Asmui, 2017). Adopting the

deemed method will enable the organisation to automate the process and in the

process reduce the complexity along with maintaining the documentation. As the

process are performed electronically, so the documents are safe-kept automatically

and it also reduces the effort involved by the human resources which further

reduces the chance of frauds. However, it should be kept in mind that the

organisation should hire adequate skill to manage the deemed process because

wrong inputs can increase the complexity associated with the purchase process.

Monitoring team: The organisation should also formulate a monitoring team that

will monitor the organisational procedures that demands attention of external

they are using the tools for productive means and are not using it to fulfil personal

agenda or interests.

Structuring the Purchase process: Another notable measure that the organisation

can adopt to mitigate the ICW risk is restructuring the purchase process and

instead of letting the purchase process run around all the departments, the

organisation can strictly allocate the job to particular staffs or teams (Ballesteros,

pan, batten & Li, 2015). Another measure that the organisation can adopt is that it

can provide full authority for a purchase process to a specific team consisting of a

manager, an accounting clerk, a buyer, a professional (of the subject that the

organisation is buying) and other necessary staffs. It would ensure that the

purchase process is simple and the data will be collective which the senior

officials should audit post completion of the purchase process to identify the

validity and ethnicity of the whole purchase procedure.

Adopting e-procurement: The organisation can also move towards adoption of e-

procurement. In the deemed process the purchasing process between organisations

are done electronically (Wicaksono, Urumsah & Asmui, 2017). Adopting the

deemed method will enable the organisation to automate the process and in the

process reduce the complexity along with maintaining the documentation. As the

process are performed electronically, so the documents are safe-kept automatically

and it also reduces the effort involved by the human resources which further

reduces the chance of frauds. However, it should be kept in mind that the

organisation should hire adequate skill to manage the deemed process because

wrong inputs can increase the complexity associated with the purchase process.

Monitoring team: The organisation should also formulate a monitoring team that

will monitor the organisational procedures that demands attention of external

8ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

presence like purchasing processes (DeFond & Lennox, 2017). It will enable the

organisation to prevent any potential frauds in the purchasing process and will

also enable the former in maintaining the quality standard of the purchasing

procedure and the purchased item. However, it should be ensured that the

monitoring team is unbiased in their working pattern and also documents their

findings adequately. In other words, an auditing of the monitoring team should be

conducted on a regular basis to ensure their vitality and verify the reliability of the

reports submitted by them (Abbott, Daugherty, Parker & Peters, 2016). Another

notable fact that the organisation should keep in mind that the monitoring team

should be skilled in IT terminologies as the above recommended measures would

require a monitoring team capable of understanding IT and factors associated with

it.

Other minor measures such as awareness sessions relevant to the organisation operations,

policies & procedures and the results that can be associated with not following the

organisational guidelines can be adopted to ensure stakeholders ethical response to a process

and will even ensure that the processes will offer sustainable results for the organisation.

Platinum can also adopt measures other measures depending on the outcome they wish from

the organisational operations.

d. Flexibility of the recommended measures

The proposed measures have taken consideration of human factors and strategies which

can be easily modified with the system. The humans can learn to work with different tools

and techniques, after taking training of the proposed tools and hence the measures do offer

flexibility with changing IT structure of the organisation (Mnih et al., 2015). Additionally,

the e-procurement is electronic process of doing things and can be integrated with the

organisational changing IT infrastructure (Svidronova & Mikus, 2015). Finally, the paper has

presence like purchasing processes (DeFond & Lennox, 2017). It will enable the

organisation to prevent any potential frauds in the purchasing process and will

also enable the former in maintaining the quality standard of the purchasing

procedure and the purchased item. However, it should be ensured that the

monitoring team is unbiased in their working pattern and also documents their

findings adequately. In other words, an auditing of the monitoring team should be

conducted on a regular basis to ensure their vitality and verify the reliability of the

reports submitted by them (Abbott, Daugherty, Parker & Peters, 2016). Another

notable fact that the organisation should keep in mind that the monitoring team

should be skilled in IT terminologies as the above recommended measures would

require a monitoring team capable of understanding IT and factors associated with

it.

Other minor measures such as awareness sessions relevant to the organisation operations,

policies & procedures and the results that can be associated with not following the

organisational guidelines can be adopted to ensure stakeholders ethical response to a process

and will even ensure that the processes will offer sustainable results for the organisation.

Platinum can also adopt measures other measures depending on the outcome they wish from

the organisational operations.

d. Flexibility of the recommended measures

The proposed measures have taken consideration of human factors and strategies which

can be easily modified with the system. The humans can learn to work with different tools

and techniques, after taking training of the proposed tools and hence the measures do offer

flexibility with changing IT structure of the organisation (Mnih et al., 2015). Additionally,

the e-procurement is electronic process of doing things and can be integrated with the

organisational changing IT infrastructure (Svidronova & Mikus, 2015). Finally, the paper has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

taken consideration of ICT in another proposed measure which can easily be integrated with

new It techniques and hence, it can be stated that the recommended measures offers

flexibility with the changing IT infrastructure of the organisation.

taken consideration of ICT in another proposed measure which can easily be integrated with

new It techniques and hence, it can be stated that the recommended measures offers

flexibility with the changing IT infrastructure of the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Bibliography:

Abbott, L. J., Daugherty, B., Parker, S., & Peters, G. F. (2016). Internal audit quality and

financial reporting quality: The joint importance of independence and

competence. Journal of Accounting Research, 54(1), 3-40.

Ballesteros, S., Pan, L., Batten, L., & Li, G. (2015, January). Segregation-of-duties conflicts

in the insider threat landscape: an overview and case study. In ERMM 2015:

Proceedings of the 2015 International Conference on Education Reform and Modern

Management (pp. 367-370). Atlantis Press.

Clinton, S. B., Pinello, A. S., & Skaife, H. A. (2014). The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and

Public Policy, 33(4), 303-327.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

Hall, J. A. (2012). Accounting information systems. Cengage Learning.

Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., ... &

Petersen, S. (2015). Human-level control through deep reinforcement

learning. Nature, 518(7540), 529.

Sadiq, S., & Governatori, G. (2015). Managing regulatory compliance in business processes.

In Handbook on Business Process Management 2 (pp. 265-288). Springer, Berlin,

Heidelberg.

Bibliography:

Abbott, L. J., Daugherty, B., Parker, S., & Peters, G. F. (2016). Internal audit quality and

financial reporting quality: The joint importance of independence and

competence. Journal of Accounting Research, 54(1), 3-40.

Ballesteros, S., Pan, L., Batten, L., & Li, G. (2015, January). Segregation-of-duties conflicts

in the insider threat landscape: an overview and case study. In ERMM 2015:

Proceedings of the 2015 International Conference on Education Reform and Modern

Management (pp. 367-370). Atlantis Press.

Clinton, S. B., Pinello, A. S., & Skaife, H. A. (2014). The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and

Public Policy, 33(4), 303-327.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

Hall, J. A. (2012). Accounting information systems. Cengage Learning.

Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., ... &

Petersen, S. (2015). Human-level control through deep reinforcement

learning. Nature, 518(7540), 529.

Sadiq, S., & Governatori, G. (2015). Managing regulatory compliance in business processes.

In Handbook on Business Process Management 2 (pp. 265-288). Springer, Berlin,

Heidelberg.

11ASSESSMENT OF INTERNAL CONTROL WEAKNESS OF PLATINUM

Svidronova, M. M., & Mikus, T. (2015). E-procurement as the ICT innovation in the public

services management: case of Slovakia. Journal of public procurement, 15(3), 317-

340.

Weske, M. (2012). Business process management architectures. In Business Process

Management (pp. 333-371). Springer, Berlin, Heidelberg.

Wicaksono, A. P., Urumsah, D., & Asmui, F. (2017). The Implementation of E-procurement

System: Indonesia Evidence. In SHS Web of Conferences (Vol. 34). EDP Sciences.

Zakaria, K. M., Nawawi, A., & Salin, A. S. A. P. (2016). Internal controls and fraud–

empirical evidence from oil and gas company. Journal of Financial crime, 23(4),

1154-1168.

Svidronova, M. M., & Mikus, T. (2015). E-procurement as the ICT innovation in the public

services management: case of Slovakia. Journal of public procurement, 15(3), 317-

340.

Weske, M. (2012). Business process management architectures. In Business Process

Management (pp. 333-371). Springer, Berlin, Heidelberg.

Wicaksono, A. P., Urumsah, D., & Asmui, F. (2017). The Implementation of E-procurement

System: Indonesia Evidence. In SHS Web of Conferences (Vol. 34). EDP Sciences.

Zakaria, K. M., Nawawi, A., & Salin, A. S. A. P. (2016). Internal controls and fraud–

empirical evidence from oil and gas company. Journal of Financial crime, 23(4),

1154-1168.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.