Report on Accounting Information Systems: Internal Control Weaknesses

VerifiedAdded on 2020/03/23

|8

|2252

|53

Report

AI Summary

This report provides a comprehensive analysis of internal control weaknesses within accounting information systems, focusing on a case study involving a company named Motherboards and More Pty Ltd. The report highlights the importance of proper documentation, well-defined business cycles, transaction authentication, and regular oversight and review procedures. It identifies various weaknesses, including insufficient documentation, outdated information systems, and lack of ethical policies, and their potential impact on a business. The report also addresses the threat of ransomware and its implications for data security. Furthermore, it offers recommendations for improvement, such as implementing analytical procedures, tests of controls, and substantive tests to strengthen the revenue cycle and overall financial health of the organization. The report concludes by emphasizing the significance of proactive measures to mitigate risks and ensure the consistency, transparency, and efficiency of business operations.

Running head: Accounting Information Systems 1

Accounting Information Systems

Name

Affiliate Institution

Accounting Information Systems

Name

Affiliate Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: Accounting Information Systems 2

Executive Summary

This report outlines about internal control weaknesses. They can be prevented by ensuring that

all transactions are documented correctly, key controls are documented in major business cycles,

transaction authentication is done before allocating orders, main review procedures like financial

documentation are performed, and evaluation of information system is done among others. This

will influence consistency, transparency and efficiency of the business.

Controls test for the revenue cycle involves who receives and grant credit sales; the separation of

role for documenting, recording, and shipping sales orders; correct documentation for collating

and banking cash and filing the receipts; the right authority and records to permit discounts for

cash or early payments and purchase returns; and administration authorization to identify that an

account is uncollectable debt.

Executive Summary

This report outlines about internal control weaknesses. They can be prevented by ensuring that

all transactions are documented correctly, key controls are documented in major business cycles,

transaction authentication is done before allocating orders, main review procedures like financial

documentation are performed, and evaluation of information system is done among others. This

will influence consistency, transparency and efficiency of the business.

Controls test for the revenue cycle involves who receives and grant credit sales; the separation of

role for documenting, recording, and shipping sales orders; correct documentation for collating

and banking cash and filing the receipts; the right authority and records to permit discounts for

cash or early payments and purchase returns; and administration authorization to identify that an

account is uncollectable debt.

Running head: Accounting Information Systems 3

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Internal Control weaknesses............................................................................................................4

Ransomware....................................................................................................................................7

Conclusion.......................................................................................................................................7

Recommendation.............................................................................................................................7

References........................................................................................................................................8

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Internal Control weaknesses............................................................................................................4

Ransomware....................................................................................................................................7

Conclusion.......................................................................................................................................7

Recommendation.............................................................................................................................7

References........................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: Accounting Information Systems 4

Introduction

Motherboards and More Pty Ltd is a company that deals with manufacturing of computer parts

such as motherboards, graphics card and microchips. When a client makes an order either over a

phone call, email or on the company’s website, the orders are received and forwarded to the

store. The system is designed in such a way that it only bills items shipped and not including

items on back order. The system then generates client’s invoice and a copy of it is sent to the

client. The client thus makes payment and is given a cash receipt upon payment and waits for

his/her shipment to arrive. Terms of trade include payment of the items within 14 days and if a

client pays within 3 days he/she is given a discount of 2%.

Internal Control weaknesses

Internal control insufficiency existing in small companies can lead to damage or loss of goods,

decline in revenue and loss of resources. These deficiencies can easily be corrected by slightly

modifying present processes or bringing in basic internal controls:

Insufficient documentation- documentation offers evidence of the existing transactions. It is the

input to build correct financial records. Financial files should be counted to make sure all

transactions are documented and accounted for. This will assist to avoid recording similar

transaction twice, since there should be no any redundant numbers in the system. With correct

numbering of records, tracking files that relate to questions and claims from owners or clients’

prior transactions will be simple. Correct documentation would likely offer sufficient answers to

most or all questions related to financial transactions. In addition, sufficient documentation will

simplify the process of assembling financial files and completion of tax returns. (Granof, 2016)

Wrongly defined major business cycles- some small organization processes appear easy. As

such, administrators and owners finds it unnecessary to create written procedures and policies or

primary flowcharts describing the main business processes. This however is likely to be one of

the most unutilized control techniques where the quality can be gained with little effort. An

efficient procedure can straighten business goals and aid in establishing most excellent operating

procedures. As businesses have varying focus sectors, distinct cycles will be essential to the

business, although in several businesses the following processes will be crucial. Banking

Procedures, Sales and Accounts Receivable, Accounts Payable, Cash Management, and

Purchases. For a business purchasing assets, inventory controls will be an essential cycle. Filing

key controls in every cycles will influence consistency, transparency, and particular duties and

responsibilities in every cycles can easily be allocated to particular individuals. When

improvements and adjustments are enhanced to the processes, workers can be informed quickly,

trained, and updated.

Inadequacy of control with authentication of transactions- authentication of purchases should

happen prior to the engagement of resources. Depending on the capacity of the business, stages

of authority can be brought in to eradicate the risk of improper spending. For instance, with

orders high in some dollar value, like $1,000, several quotations should be received which could

Introduction

Motherboards and More Pty Ltd is a company that deals with manufacturing of computer parts

such as motherboards, graphics card and microchips. When a client makes an order either over a

phone call, email or on the company’s website, the orders are received and forwarded to the

store. The system is designed in such a way that it only bills items shipped and not including

items on back order. The system then generates client’s invoice and a copy of it is sent to the

client. The client thus makes payment and is given a cash receipt upon payment and waits for

his/her shipment to arrive. Terms of trade include payment of the items within 14 days and if a

client pays within 3 days he/she is given a discount of 2%.

Internal Control weaknesses

Internal control insufficiency existing in small companies can lead to damage or loss of goods,

decline in revenue and loss of resources. These deficiencies can easily be corrected by slightly

modifying present processes or bringing in basic internal controls:

Insufficient documentation- documentation offers evidence of the existing transactions. It is the

input to build correct financial records. Financial files should be counted to make sure all

transactions are documented and accounted for. This will assist to avoid recording similar

transaction twice, since there should be no any redundant numbers in the system. With correct

numbering of records, tracking files that relate to questions and claims from owners or clients’

prior transactions will be simple. Correct documentation would likely offer sufficient answers to

most or all questions related to financial transactions. In addition, sufficient documentation will

simplify the process of assembling financial files and completion of tax returns. (Granof, 2016)

Wrongly defined major business cycles- some small organization processes appear easy. As

such, administrators and owners finds it unnecessary to create written procedures and policies or

primary flowcharts describing the main business processes. This however is likely to be one of

the most unutilized control techniques where the quality can be gained with little effort. An

efficient procedure can straighten business goals and aid in establishing most excellent operating

procedures. As businesses have varying focus sectors, distinct cycles will be essential to the

business, although in several businesses the following processes will be crucial. Banking

Procedures, Sales and Accounts Receivable, Accounts Payable, Cash Management, and

Purchases. For a business purchasing assets, inventory controls will be an essential cycle. Filing

key controls in every cycles will influence consistency, transparency, and particular duties and

responsibilities in every cycles can easily be allocated to particular individuals. When

improvements and adjustments are enhanced to the processes, workers can be informed quickly,

trained, and updated.

Inadequacy of control with authentication of transactions- authentication of purchases should

happen prior to the engagement of resources. Depending on the capacity of the business, stages

of authority can be brought in to eradicate the risk of improper spending. For instance, with

orders high in some dollar value, like $1,000, several quotations should be received which could

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: Accounting Information Systems 5

minimize the general expenditure. Authenticating transactions before allocating orders offers the

owners the chance to analyze different purchasing alternatives, and ensuring services or items

received will aid the business goals. (Dauber, Shim, Siegel & Siegel, 2012)

Lack of oversight and review- small business managers normally get so occupied in the daily

operations of the business that they have a tendency of neglecting performing main review

procedures. Business managers should spare little time and interest in the financial

documentation. This is an essential aspect of deception prevention. Little time is needed to

examine monthly revenues, actual amounts versus budget, and variance, expense, and inventory

reports. prioritizing on approach will provide the owner with valueless report on how the

business is functioning and where any possible problem or inefficiency areas may exist.

Evaluation of the financial files is a crucial input and component for improved decision making.

The regularity of the analysis of financial information relies on the quantity of transactions and

the kind of business, however, the evaluation of financial information should be carried out on a

monthly basis.

Outdated information systems- generally small businesses perform on small resources and less

time is normally spent analyzing information systems. Sparing more time in this sector could

improve efficiencies in the long run. Outline the systems in the business and the major

performance measures required. Systematic operations will aid in competitiveness and

efficiency. Various user-friendly software systems are available which could decrease operating

and processing cycles and are cheap to operate.

Lack of logical and physical safety- lack of physical safety of business goods and resources

could lead to the damage or loss to goods and resources. Access to tools, check stock and petty

cash should be confined to right individuals and stored in a proper safe location. Computer

devices and networks should have password that is protected and these passwords should be

frequently changed. Firewalls and safeguarded equipment or software is a vital component to aid

in prevention of security breaches. safety of individual and banking information is becoming

increasingly essential with the increase in threats of identity card theft. Individual and employee

information should be encoded and kept in safe folders.

Lack of formal ethical procedures and policies- this control may seem to be less important for

the growth of a business, but lack of clear procedures on the usage of business resources and

anticipations, based on ethics and integrity from working staffs, businesses can experience

ineffectiveness and misappropriation of resources. A code of conduct is an open revelation of

the way a company functions. A well-structured ethics policy can act as a communication

channel that reflects essential values and objectives of the business. It can offer procedures of

how workers should handle potential misconduct and/ or misappropriation of resources and can

offer alignment regarding to organization commitments and values. (Studer, 2009)

Lack of clearly defined job duties and responsibilities - the most essential assets are the

employees and small business rely much on their workers. They are representatives with

competitors, customers, and suppliers. For this important resource to be efficient in the business

minimize the general expenditure. Authenticating transactions before allocating orders offers the

owners the chance to analyze different purchasing alternatives, and ensuring services or items

received will aid the business goals. (Dauber, Shim, Siegel & Siegel, 2012)

Lack of oversight and review- small business managers normally get so occupied in the daily

operations of the business that they have a tendency of neglecting performing main review

procedures. Business managers should spare little time and interest in the financial

documentation. This is an essential aspect of deception prevention. Little time is needed to

examine monthly revenues, actual amounts versus budget, and variance, expense, and inventory

reports. prioritizing on approach will provide the owner with valueless report on how the

business is functioning and where any possible problem or inefficiency areas may exist.

Evaluation of the financial files is a crucial input and component for improved decision making.

The regularity of the analysis of financial information relies on the quantity of transactions and

the kind of business, however, the evaluation of financial information should be carried out on a

monthly basis.

Outdated information systems- generally small businesses perform on small resources and less

time is normally spent analyzing information systems. Sparing more time in this sector could

improve efficiencies in the long run. Outline the systems in the business and the major

performance measures required. Systematic operations will aid in competitiveness and

efficiency. Various user-friendly software systems are available which could decrease operating

and processing cycles and are cheap to operate.

Lack of logical and physical safety- lack of physical safety of business goods and resources

could lead to the damage or loss to goods and resources. Access to tools, check stock and petty

cash should be confined to right individuals and stored in a proper safe location. Computer

devices and networks should have password that is protected and these passwords should be

frequently changed. Firewalls and safeguarded equipment or software is a vital component to aid

in prevention of security breaches. safety of individual and banking information is becoming

increasingly essential with the increase in threats of identity card theft. Individual and employee

information should be encoded and kept in safe folders.

Lack of formal ethical procedures and policies- this control may seem to be less important for

the growth of a business, but lack of clear procedures on the usage of business resources and

anticipations, based on ethics and integrity from working staffs, businesses can experience

ineffectiveness and misappropriation of resources. A code of conduct is an open revelation of

the way a company functions. A well-structured ethics policy can act as a communication

channel that reflects essential values and objectives of the business. It can offer procedures of

how workers should handle potential misconduct and/ or misappropriation of resources and can

offer alignment regarding to organization commitments and values. (Studer, 2009)

Lack of clearly defined job duties and responsibilities - the most essential assets are the

employees and small business rely much on their workers. They are representatives with

competitors, customers, and suppliers. For this important resource to be efficient in the business

Running head: Accounting Information Systems 6

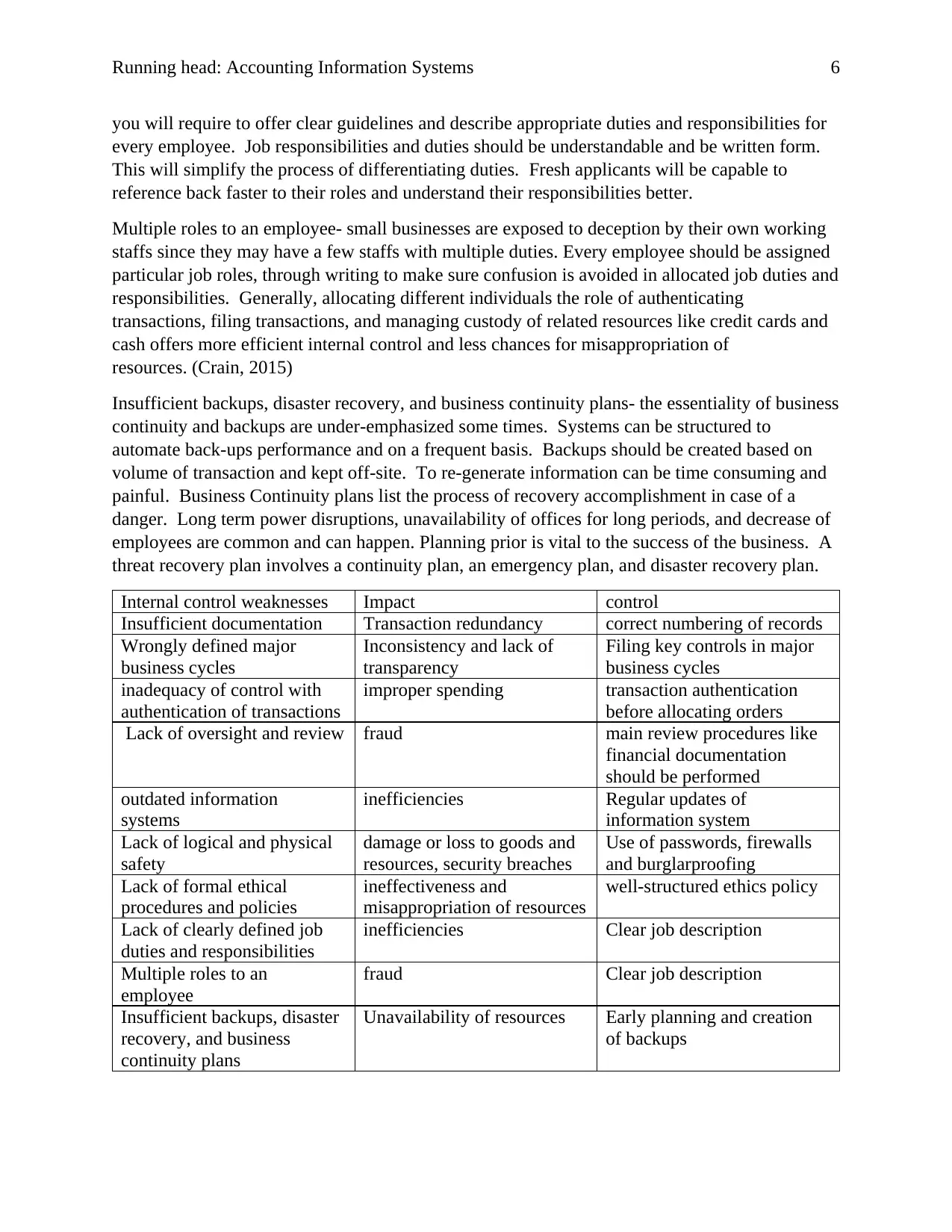

you will require to offer clear guidelines and describe appropriate duties and responsibilities for

every employee. Job responsibilities and duties should be understandable and be written form.

This will simplify the process of differentiating duties. Fresh applicants will be capable to

reference back faster to their roles and understand their responsibilities better.

Multiple roles to an employee- small businesses are exposed to deception by their own working

staffs since they may have a few staffs with multiple duties. Every employee should be assigned

particular job roles, through writing to make sure confusion is avoided in allocated job duties and

responsibilities. Generally, allocating different individuals the role of authenticating

transactions, filing transactions, and managing custody of related resources like credit cards and

cash offers more efficient internal control and less chances for misappropriation of

resources. (Crain, 2015)

Insufficient backups, disaster recovery, and business continuity plans- the essentiality of business

continuity and backups are under-emphasized some times. Systems can be structured to

automate back-ups performance and on a frequent basis. Backups should be created based on

volume of transaction and kept off-site. To re-generate information can be time consuming and

painful. Business Continuity plans list the process of recovery accomplishment in case of a

danger. Long term power disruptions, unavailability of offices for long periods, and decrease of

employees are common and can happen. Planning prior is vital to the success of the business. A

threat recovery plan involves a continuity plan, an emergency plan, and disaster recovery plan.

Internal control weaknesses Impact control

Insufficient documentation Transaction redundancy correct numbering of records

Wrongly defined major

business cycles

Inconsistency and lack of

transparency

Filing key controls in major

business cycles

inadequacy of control with

authentication of transactions

improper spending transaction authentication

before allocating orders

Lack of oversight and review fraud main review procedures like

financial documentation

should be performed

outdated information

systems

inefficiencies Regular updates of

information system

Lack of logical and physical

safety

damage or loss to goods and

resources, security breaches

Use of passwords, firewalls

and burglarproofing

Lack of formal ethical

procedures and policies

ineffectiveness and

misappropriation of resources

well-structured ethics policy

Lack of clearly defined job

duties and responsibilities

inefficiencies Clear job description

Multiple roles to an

employee

fraud Clear job description

Insufficient backups, disaster

recovery, and business

continuity plans

Unavailability of resources Early planning and creation

of backups

you will require to offer clear guidelines and describe appropriate duties and responsibilities for

every employee. Job responsibilities and duties should be understandable and be written form.

This will simplify the process of differentiating duties. Fresh applicants will be capable to

reference back faster to their roles and understand their responsibilities better.

Multiple roles to an employee- small businesses are exposed to deception by their own working

staffs since they may have a few staffs with multiple duties. Every employee should be assigned

particular job roles, through writing to make sure confusion is avoided in allocated job duties and

responsibilities. Generally, allocating different individuals the role of authenticating

transactions, filing transactions, and managing custody of related resources like credit cards and

cash offers more efficient internal control and less chances for misappropriation of

resources. (Crain, 2015)

Insufficient backups, disaster recovery, and business continuity plans- the essentiality of business

continuity and backups are under-emphasized some times. Systems can be structured to

automate back-ups performance and on a frequent basis. Backups should be created based on

volume of transaction and kept off-site. To re-generate information can be time consuming and

painful. Business Continuity plans list the process of recovery accomplishment in case of a

danger. Long term power disruptions, unavailability of offices for long periods, and decrease of

employees are common and can happen. Planning prior is vital to the success of the business. A

threat recovery plan involves a continuity plan, an emergency plan, and disaster recovery plan.

Internal control weaknesses Impact control

Insufficient documentation Transaction redundancy correct numbering of records

Wrongly defined major

business cycles

Inconsistency and lack of

transparency

Filing key controls in major

business cycles

inadequacy of control with

authentication of transactions

improper spending transaction authentication

before allocating orders

Lack of oversight and review fraud main review procedures like

financial documentation

should be performed

outdated information

systems

inefficiencies Regular updates of

information system

Lack of logical and physical

safety

damage or loss to goods and

resources, security breaches

Use of passwords, firewalls

and burglarproofing

Lack of formal ethical

procedures and policies

ineffectiveness and

misappropriation of resources

well-structured ethics policy

Lack of clearly defined job

duties and responsibilities

inefficiencies Clear job description

Multiple roles to an

employee

fraud Clear job description

Insufficient backups, disaster

recovery, and business

continuity plans

Unavailability of resources Early planning and creation

of backups

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: Accounting Information Systems 7

Ransomware

Ransomware is a subset of cyber-attacks in which the information on a victim's computer device

is blocked, by encoding, and payment is needed before the ransomed information is decoded and

access granted to the victim. The intentions for ransomware threats focuses on money, and unlike

other kinds of threats, the victim is normally alerted that an abuse has happened and is given

directions on how to recover from the threat. Payment is normally required in a virtual currency,

like bitcoin, to hide the cybercriminal's identity. Examples of ransomware are Wannacry and

CryptoLocker.

Conclusion

In conclusion, internal control weakness can be prevented by ensuring that all transactions are

documented correctly, key controls are documented in major business cycles, transaction

authentication is done before allocating orders, main review procedures like financial

documentation are performed, and evaluation of information system is done among others. This

will influence consistency, transparency and efficiency of the business.

Recommendation

The following are some of the recommendation for Motherboard;

Analytical Procedures- the auditor must test the accounts receivable account to make sure it is

not exceeding sales. If it is, this could show that the organization is a risk to credit and may lead

to cash flow challenges in the future.

Tests of Controls- controls test for the revenue cycle involves who receives and grant credit

sales; the separation of role for documenting, recording, and shipping sales orders; correct

documentation for collating and banking cash and filing the receipts; the right authority and

records to permit discounts for cash or early payments and purchase returns; and administration

authorization to identify that an account is uncollectable debt.

Substantive Tests- These tests involve analyzing the trial balance generated by the accountant at

the end of the cycle, approving receivable amounts with the organization or individuals with

debts and assessing the correctness of the allowance for written-off accounts by inspecting the

past entity.

Ransomware

Ransomware is a subset of cyber-attacks in which the information on a victim's computer device

is blocked, by encoding, and payment is needed before the ransomed information is decoded and

access granted to the victim. The intentions for ransomware threats focuses on money, and unlike

other kinds of threats, the victim is normally alerted that an abuse has happened and is given

directions on how to recover from the threat. Payment is normally required in a virtual currency,

like bitcoin, to hide the cybercriminal's identity. Examples of ransomware are Wannacry and

CryptoLocker.

Conclusion

In conclusion, internal control weakness can be prevented by ensuring that all transactions are

documented correctly, key controls are documented in major business cycles, transaction

authentication is done before allocating orders, main review procedures like financial

documentation are performed, and evaluation of information system is done among others. This

will influence consistency, transparency and efficiency of the business.

Recommendation

The following are some of the recommendation for Motherboard;

Analytical Procedures- the auditor must test the accounts receivable account to make sure it is

not exceeding sales. If it is, this could show that the organization is a risk to credit and may lead

to cash flow challenges in the future.

Tests of Controls- controls test for the revenue cycle involves who receives and grant credit

sales; the separation of role for documenting, recording, and shipping sales orders; correct

documentation for collating and banking cash and filing the receipts; the right authority and

records to permit discounts for cash or early payments and purchase returns; and administration

authorization to identify that an account is uncollectable debt.

Substantive Tests- These tests involve analyzing the trial balance generated by the accountant at

the end of the cycle, approving receivable amounts with the organization or individuals with

debts and assessing the correctness of the allowance for written-off accounts by inspecting the

past entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: Accounting Information Systems 8

References

Granof, M. H. (2016). Government and not-for-profit accounting, binder ready version:

Concepts and practices. John Wiley & Sons Inc.

Dauber, N. A., Shim, J. K., Siegel, J. G., & Siegel, J. G. (2012). The complete CPA reference.

Hoboken, N.J: John Wiley & Sons.

Studer, Q. (2009). Straight A leadership: Alignment, action, accountability. Gulf Breeze, FL:

Fire Starter Publishing.

Bragg, S. M. (2014). Bookkeeping guidebook: A practitioner's guide.

Crain, M. A. (2015). Essentials of forensic accounting.

Albrecht, W. S. (2012). Fraud examination. Mason, OH: South Western, Cengage Learning.

CRUMBLEY, D. L. (2017). FORENSIC AND INVESTIGATIVE ACCOUNTING. S.l.: CCH

INCORPORATED.

Kim, W. C., & Mauborgne, R. (2015). Blue ocean strategy: How to create uncontested market

space and make the competition irrelevant.

References

Granof, M. H. (2016). Government and not-for-profit accounting, binder ready version:

Concepts and practices. John Wiley & Sons Inc.

Dauber, N. A., Shim, J. K., Siegel, J. G., & Siegel, J. G. (2012). The complete CPA reference.

Hoboken, N.J: John Wiley & Sons.

Studer, Q. (2009). Straight A leadership: Alignment, action, accountability. Gulf Breeze, FL:

Fire Starter Publishing.

Bragg, S. M. (2014). Bookkeeping guidebook: A practitioner's guide.

Crain, M. A. (2015). Essentials of forensic accounting.

Albrecht, W. S. (2012). Fraud examination. Mason, OH: South Western, Cengage Learning.

CRUMBLEY, D. L. (2017). FORENSIC AND INVESTIGATIVE ACCOUNTING. S.l.: CCH

INCORPORATED.

Kim, W. C., & Mauborgne, R. (2015). Blue ocean strategy: How to create uncontested market

space and make the competition irrelevant.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.