International Accounting: Business Strategies, Regulations, and Cases

VerifiedAdded on 2023/01/05

|14

|3862

|23

Homework Assignment

AI Summary

This assignment delves into key aspects of international accounting, examining the business strategies of companies like Harvey Norman and Bunnings Warehouse, and the regulatory environment in Malaysia. It explores the adoption of transnational and multi-domestic strategies, and analyzes the global business environments of the selected companies. The assignment further addresses regulatory and taxation considerations for businesses exporting to Malaysia, including operational considerations and foreign currency movements. It provides detailed accounting entries for foreign currency transactions, including forward contracts and spot deals. Finally, the assignment discusses transfer pricing regulations, focusing on the Australian Taxation Office's (ATO) scrutiny and the implications of the Chevron case, emphasizing the importance of arm's length pricing and compliance with tax avoidance standards.

International Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

MAIN BODY..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3...............................................................................................................................................6

Question 4...............................................................................................................................................7

Question 5...............................................................................................................................................8

Question 6.............................................................................................................................................10

REFERENCES..........................................................................................................................................13

MAIN BODY..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3...............................................................................................................................................6

Question 4...............................................................................................................................................7

Question 5...............................................................................................................................................8

Question 6.............................................................................................................................................10

REFERENCES..........................................................................................................................................13

MAIN BODY

Question 1

International business strategy adopted by Harvey Norman (Family business):

Transitional business strategy- The transnational market approach is one of the most complex

approaches that companies can use while expanding globally, and can be used as a mixture of the

multinational and multinational strategies (Peterson, Arregle & Martin, 2020). While this

approach maintains a business’s headquarters and key technology in its country of origin, it also

helps an organization to develop full-scale operations in international markets. The choice,

manufacturing and distribution obligations of each plant in these different markets are equally

divided, allowing businesses to have independent marketing, research and innovation divisions

to satisfy local customers ' needs. In the context of above business this approach has been applied

because it is quite helpful for a family business. By help of this approach, they are able to

manage their business in different nations. The key element of this approach is that under it

companies do not need to operate from other nation. It can be operated and managed in own

nation.

International business strategy adopted by Bunnings Warehouse:

Multi domestic strategy- For companies to follow multi-domestic business strategies, they have

to spend and customize their goods or services to local client bases to develop their position on

the international market. Companies change their services and reposition their selling strategies

in order to comply with international customs, cultural characteristics and practices rather than

marketing new goods for clients who cannot initially identify them or appreciate them. Multi-

domestic corporations also retain. Although their offices are based in their place of origin, they

normally create oversea headquarters, known as subsidiaries, best suited to deliver regional

variations of the goods and services of international customers. They often lease buildings often

abroad as distribution, development or storage facilities for housing services operations. In

regards to above company they might have adopted this approach for their international business.

Question 1

International business strategy adopted by Harvey Norman (Family business):

Transitional business strategy- The transnational market approach is one of the most complex

approaches that companies can use while expanding globally, and can be used as a mixture of the

multinational and multinational strategies (Peterson, Arregle & Martin, 2020). While this

approach maintains a business’s headquarters and key technology in its country of origin, it also

helps an organization to develop full-scale operations in international markets. The choice,

manufacturing and distribution obligations of each plant in these different markets are equally

divided, allowing businesses to have independent marketing, research and innovation divisions

to satisfy local customers ' needs. In the context of above business this approach has been applied

because it is quite helpful for a family business. By help of this approach, they are able to

manage their business in different nations. The key element of this approach is that under it

companies do not need to operate from other nation. It can be operated and managed in own

nation.

International business strategy adopted by Bunnings Warehouse:

Multi domestic strategy- For companies to follow multi-domestic business strategies, they have

to spend and customize their goods or services to local client bases to develop their position on

the international market. Companies change their services and reposition their selling strategies

in order to comply with international customs, cultural characteristics and practices rather than

marketing new goods for clients who cannot initially identify them or appreciate them. Multi-

domestic corporations also retain. Although their offices are based in their place of origin, they

normally create oversea headquarters, known as subsidiaries, best suited to deliver regional

variations of the goods and services of international customers. They often lease buildings often

abroad as distribution, development or storage facilities for housing services operations. In

regards to above company they might have adopted this approach for their international business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Business environment of both Harvey Norman and Bunnings Warehouse:

Both business entities have different business environment. In the context of Harvey Norman,

this can be found out that their business environment is favorable for operating the business. It is

so because Australia is nation which supports to family businesses for expanding the business in

different nations. There is not so much restriction for operating the family business (Rathore,

2019).

On the other hands, Bunnings Warehouse is a warehouse company. This company planned to

operate in UK and Ireland. In relation to warehouse business, there are different kinds of rules

and regulation which need to be followed by companies.

Advice due to which there is international success of Harvey Norman over Bunnings Warehouse:

The rationale due to which Harvey Norman is successful over Bunnings Warehouse is due to

different business environment of both entities. Like Harvey Norman is a family based business

which has support of government to expand. On the other hands, Bunnings Warehouse is a

company that faces issues of different regulations due to business nature. Bunnings Warehouse

needs to comply with a form of strategy which can contribute for success in different nations.

Question 2

Regulatory requirements- Usually, ad valorem Malaysian tariffs are levied with an applied rate

of 6.1 percent on industrial products on a simple average. Malaysia pays special responsibilities

which are highly efficient prices on such products such as beer, wine, chickens, salmons and

pigs. Tariff tracks, where local development is important, also have risks require. The Good and

Service Tax (GST) has been scrapped, with potential changes to the former Sales and Service

Tax (SST) beginning in September 2018. In the context of Rebecca’s “Sea Farmed Salmon” they

should consider these requirements before moving to Malaysia. It is so because in this nation,

there are different regulatory requirements in order to export the business of Salmon. In the

absence of proper following of these regulations, there can be difficult for above business in

order to operate in Malaysia.

Both business entities have different business environment. In the context of Harvey Norman,

this can be found out that their business environment is favorable for operating the business. It is

so because Australia is nation which supports to family businesses for expanding the business in

different nations. There is not so much restriction for operating the family business (Rathore,

2019).

On the other hands, Bunnings Warehouse is a warehouse company. This company planned to

operate in UK and Ireland. In relation to warehouse business, there are different kinds of rules

and regulation which need to be followed by companies.

Advice due to which there is international success of Harvey Norman over Bunnings Warehouse:

The rationale due to which Harvey Norman is successful over Bunnings Warehouse is due to

different business environment of both entities. Like Harvey Norman is a family based business

which has support of government to expand. On the other hands, Bunnings Warehouse is a

company that faces issues of different regulations due to business nature. Bunnings Warehouse

needs to comply with a form of strategy which can contribute for success in different nations.

Question 2

Regulatory requirements- Usually, ad valorem Malaysian tariffs are levied with an applied rate

of 6.1 percent on industrial products on a simple average. Malaysia pays special responsibilities

which are highly efficient prices on such products such as beer, wine, chickens, salmons and

pigs. Tariff tracks, where local development is important, also have risks require. The Good and

Service Tax (GST) has been scrapped, with potential changes to the former Sales and Service

Tax (SST) beginning in September 2018. In the context of Rebecca’s “Sea Farmed Salmon” they

should consider these requirements before moving to Malaysia. It is so because in this nation,

there are different regulatory requirements in order to export the business of Salmon. In the

absence of proper following of these regulations, there can be difficult for above business in

order to operate in Malaysia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation consideration- Malaysia is a sovereign nation of southern Mediterranean States

(ASEAN) adopting the harmonized commodity Scheme (HTS) for exports and imports products

not residing in national governments (Morais, 2020). Malaysia observes the ASEAN

Harmonized Tariff terminology (AHTN) for products imported into the country from ASEAN

Member States. Malaysia charges a tariff rate of 0 to 50%, after ad valorem prices. The average

tariff paid on foreign goods to Malaysia, even so, is 6.1%. In the case of commodities with

significant domestic production as well as so-called "sinful" products such as pork and alcohol,

Malaysians' customs apply higher tariff rates. Malaysian border control either apply a discounted

amount or an allowance from a tariff on raw resources shipped to Malaysia to be used in the

production of exporting goods – especially in cases where such material cost is hard to obtain at

home. In the context of Rebecca’s “Sea Farmed Salmon” they should consider these tax values

before exporting business in Malaysia.

Operational considerations- Malaysia has been taking advantage of its area at the intersection of

trade between East and Western countries and around the world, a heritage that goes into the 21st

century. Regionally wounded, Malaysia extends along the Strait of Malacca, one of the largest

commercial vessels in the globe, in economic and social terms. By capitalizing on Malaysia’s

business, it became a comparatively competitive, high tech country in the early 1970s that was

capable of transforming its economic system from an agricultural production and mining base, in

which service providers and production account for 73% of GDP (51% in service providers and

22% in production in 2017). In the context of Rebecca’s “Sea Farmed Salmon” they should

follow these operational considerations for doing business of Salmon.

Foreign currency movements- The currency unit is the RM Malaysian Ringgit. The Malaysian

economy is mainly dependent on manufactured goods like electrical and electronics goods,

textiles, and rubber goods and on the industrial and mineral industries as a one of ASEAN's most

industrialized economies. The Ringgit (RM) has faced an inflationary pressure in recent years,

the Malaysian currency. During the first three months of 2019, the rate of exchange from

Malaysian Ringgit to the US currency was roughly RM 4.1 per dollar. In the first quarter of

2018, the slight exception to price pressure and relaxation rose to 1 USD = 3.92 RM. The

estimated yearly RM versus USD for 2018 was 4.05 (About regulatory requirement to do

business in Malaysia, 2020). It peaked at about RM4.30, averaging about 2017, and was around

(ASEAN) adopting the harmonized commodity Scheme (HTS) for exports and imports products

not residing in national governments (Morais, 2020). Malaysia observes the ASEAN

Harmonized Tariff terminology (AHTN) for products imported into the country from ASEAN

Member States. Malaysia charges a tariff rate of 0 to 50%, after ad valorem prices. The average

tariff paid on foreign goods to Malaysia, even so, is 6.1%. In the case of commodities with

significant domestic production as well as so-called "sinful" products such as pork and alcohol,

Malaysians' customs apply higher tariff rates. Malaysian border control either apply a discounted

amount or an allowance from a tariff on raw resources shipped to Malaysia to be used in the

production of exporting goods – especially in cases where such material cost is hard to obtain at

home. In the context of Rebecca’s “Sea Farmed Salmon” they should consider these tax values

before exporting business in Malaysia.

Operational considerations- Malaysia has been taking advantage of its area at the intersection of

trade between East and Western countries and around the world, a heritage that goes into the 21st

century. Regionally wounded, Malaysia extends along the Strait of Malacca, one of the largest

commercial vessels in the globe, in economic and social terms. By capitalizing on Malaysia’s

business, it became a comparatively competitive, high tech country in the early 1970s that was

capable of transforming its economic system from an agricultural production and mining base, in

which service providers and production account for 73% of GDP (51% in service providers and

22% in production in 2017). In the context of Rebecca’s “Sea Farmed Salmon” they should

follow these operational considerations for doing business of Salmon.

Foreign currency movements- The currency unit is the RM Malaysian Ringgit. The Malaysian

economy is mainly dependent on manufactured goods like electrical and electronics goods,

textiles, and rubber goods and on the industrial and mineral industries as a one of ASEAN's most

industrialized economies. The Ringgit (RM) has faced an inflationary pressure in recent years,

the Malaysian currency. During the first three months of 2019, the rate of exchange from

Malaysian Ringgit to the US currency was roughly RM 4.1 per dollar. In the first quarter of

2018, the slight exception to price pressure and relaxation rose to 1 USD = 3.92 RM. The

estimated yearly RM versus USD for 2018 was 4.05 (About regulatory requirement to do

business in Malaysia, 2020). It peaked at about RM4.30, averaging about 2017, and was around

US$ 1 to RM4.15 in 2016. Malaysia’s prosperity was influenced by the lower dollar, and

financial policy initiatives were taken by the policy to boost its currency. The Central Bank of

Malaysia, Bank of Negara, accepts the negative risks associated with current market conditions

and the effect on the Malaysian economy and recognizes growing growth risks as modest

shipments due to a decline in global demand. US – Chinese trade disputes are still alarming,

while some see it as a possibility.

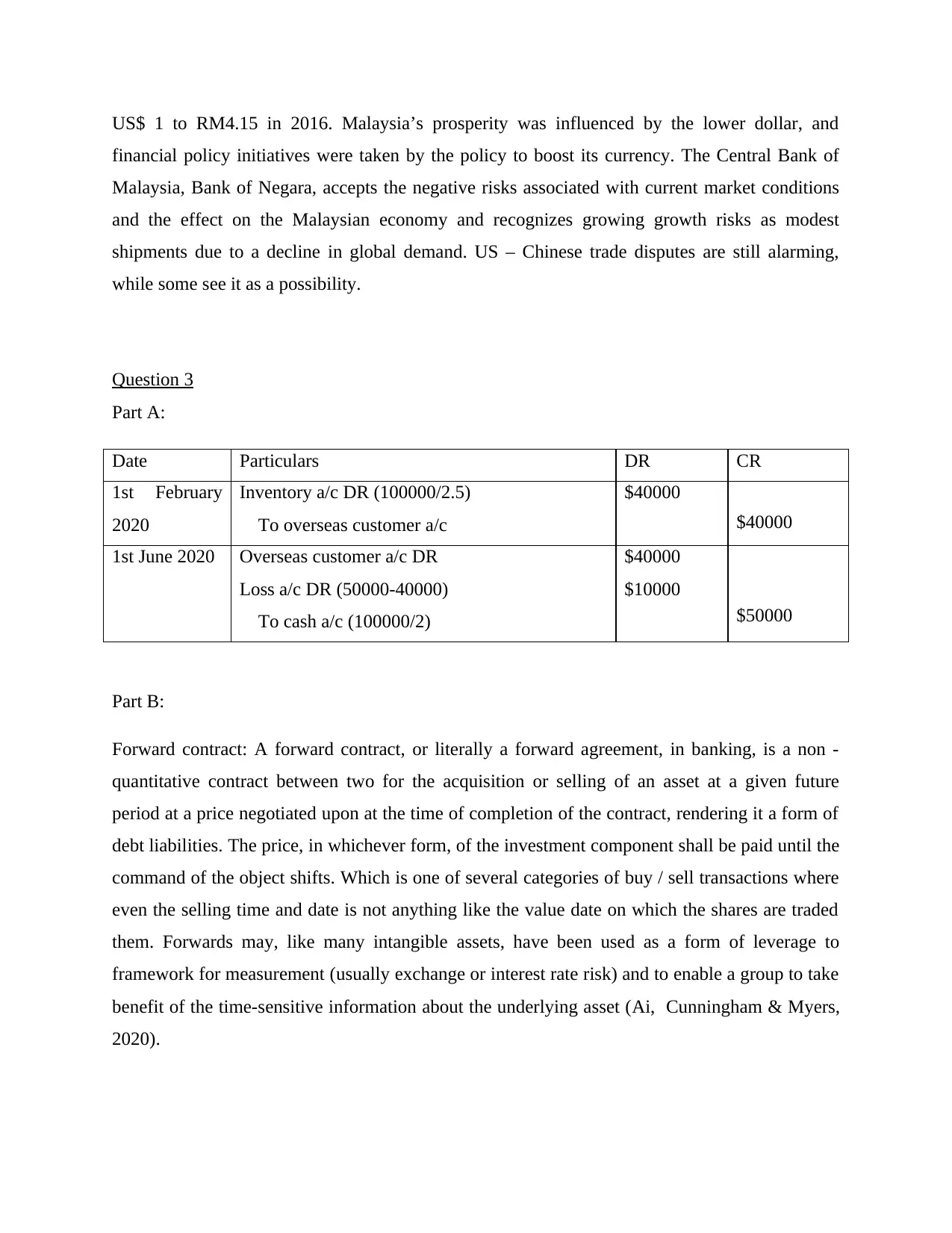

Question 3

Part A:

Date Particulars DR CR

1st February

2020

Inventory a/c DR (100000/2.5)

To overseas customer a/c

$40000

$40000

1st June 2020 Overseas customer a/c DR

Loss a/c DR (50000-40000)

To cash a/c (100000/2)

$40000

$10000

$50000

Part B:

Forward contract: A forward contract, or literally a forward agreement, in banking, is a non -

quantitative contract between two for the acquisition or selling of an asset at a given future

period at a price negotiated upon at the time of completion of the contract, rendering it a form of

debt liabilities. The price, in whichever form, of the investment component shall be paid until the

command of the object shifts. Which is one of several categories of buy / sell transactions where

even the selling time and date is not anything like the value date on which the shares are traded

them. Forwards may, like many intangible assets, have been used as a form of leverage to

framework for measurement (usually exchange or interest rate risk) and to enable a group to take

benefit of the time-sensitive information about the underlying asset (Ai, Cunningham & Myers,

2020).

financial policy initiatives were taken by the policy to boost its currency. The Central Bank of

Malaysia, Bank of Negara, accepts the negative risks associated with current market conditions

and the effect on the Malaysian economy and recognizes growing growth risks as modest

shipments due to a decline in global demand. US – Chinese trade disputes are still alarming,

while some see it as a possibility.

Question 3

Part A:

Date Particulars DR CR

1st February

2020

Inventory a/c DR (100000/2.5)

To overseas customer a/c

$40000

$40000

1st June 2020 Overseas customer a/c DR

Loss a/c DR (50000-40000)

To cash a/c (100000/2)

$40000

$10000

$50000

Part B:

Forward contract: A forward contract, or literally a forward agreement, in banking, is a non -

quantitative contract between two for the acquisition or selling of an asset at a given future

period at a price negotiated upon at the time of completion of the contract, rendering it a form of

debt liabilities. The price, in whichever form, of the investment component shall be paid until the

command of the object shifts. Which is one of several categories of buy / sell transactions where

even the selling time and date is not anything like the value date on which the shares are traded

them. Forwards may, like many intangible assets, have been used as a form of leverage to

framework for measurement (usually exchange or interest rate risk) and to enable a group to take

benefit of the time-sensitive information about the underlying asset (Ai, Cunningham & Myers,

2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

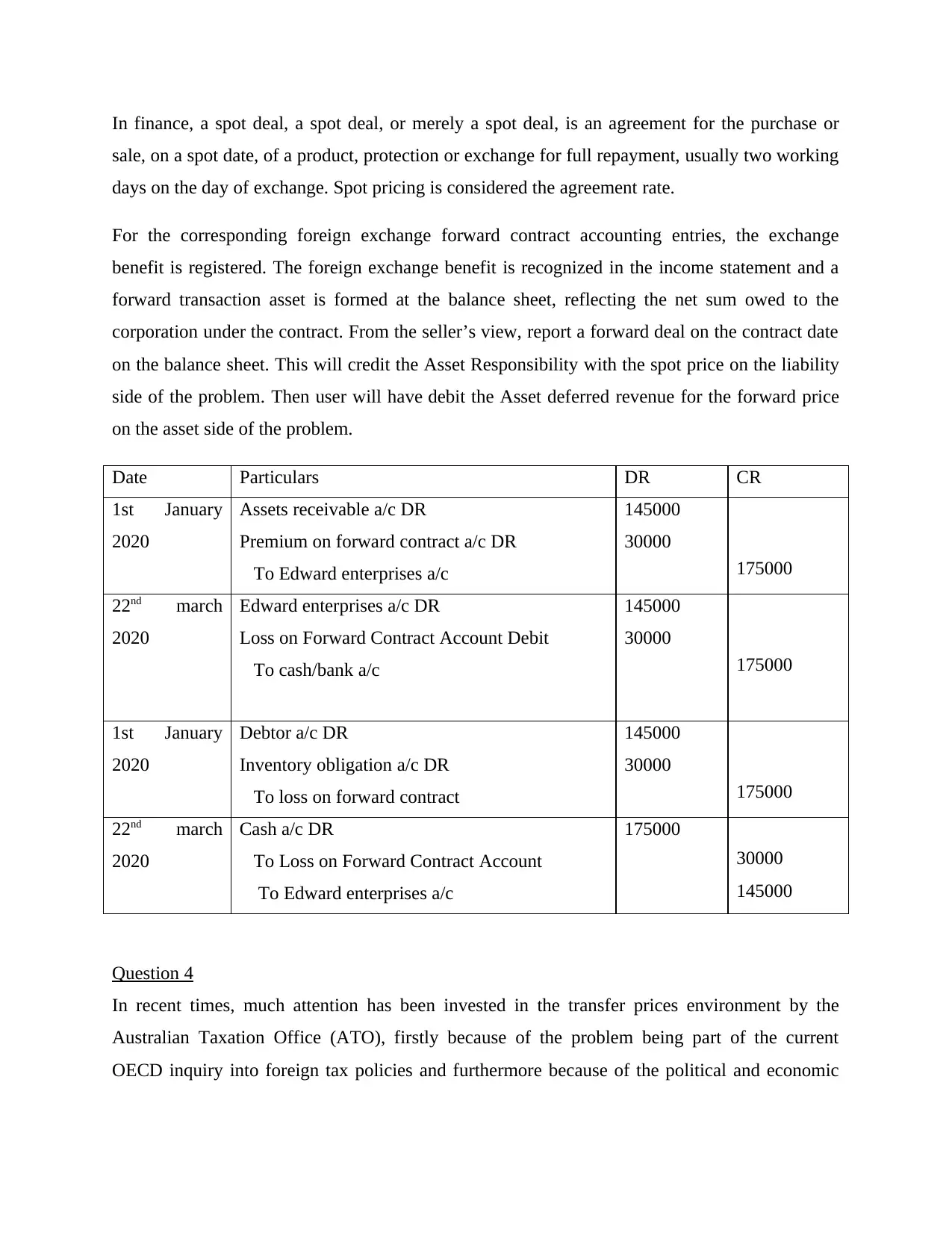

In finance, a spot deal, a spot deal, or merely a spot deal, is an agreement for the purchase or

sale, on a spot date, of a product, protection or exchange for full repayment, usually two working

days on the day of exchange. Spot pricing is considered the agreement rate.

For the corresponding foreign exchange forward contract accounting entries, the exchange

benefit is registered. The foreign exchange benefit is recognized in the income statement and a

forward transaction asset is formed at the balance sheet, reflecting the net sum owed to the

corporation under the contract. From the seller’s view, report a forward deal on the contract date

on the balance sheet. This will credit the Asset Responsibility with the spot price on the liability

side of the problem. Then user will have debit the Asset deferred revenue for the forward price

on the asset side of the problem.

Date Particulars DR CR

1st January

2020

Assets receivable a/c DR

Premium on forward contract a/c DR

To Edward enterprises a/c

145000

30000

175000

22nd march

2020

Edward enterprises a/c DR

Loss on Forward Contract Account Debit

To cash/bank a/c

145000

30000

175000

1st January

2020

Debtor a/c DR

Inventory obligation a/c DR

To loss on forward contract

145000

30000

175000

22nd march

2020

Cash a/c DR

To Loss on Forward Contract Account

To Edward enterprises a/c

175000

30000

145000

Question 4

In recent times, much attention has been invested in the transfer prices environment by the

Australian Taxation Office (ATO), firstly because of the problem being part of the current

OECD inquiry into foreign tax policies and furthermore because of the political and economic

sale, on a spot date, of a product, protection or exchange for full repayment, usually two working

days on the day of exchange. Spot pricing is considered the agreement rate.

For the corresponding foreign exchange forward contract accounting entries, the exchange

benefit is registered. The foreign exchange benefit is recognized in the income statement and a

forward transaction asset is formed at the balance sheet, reflecting the net sum owed to the

corporation under the contract. From the seller’s view, report a forward deal on the contract date

on the balance sheet. This will credit the Asset Responsibility with the spot price on the liability

side of the problem. Then user will have debit the Asset deferred revenue for the forward price

on the asset side of the problem.

Date Particulars DR CR

1st January

2020

Assets receivable a/c DR

Premium on forward contract a/c DR

To Edward enterprises a/c

145000

30000

175000

22nd march

2020

Edward enterprises a/c DR

Loss on Forward Contract Account Debit

To cash/bank a/c

145000

30000

175000

1st January

2020

Debtor a/c DR

Inventory obligation a/c DR

To loss on forward contract

145000

30000

175000

22nd march

2020

Cash a/c DR

To Loss on Forward Contract Account

To Edward enterprises a/c

175000

30000

145000

Question 4

In recent times, much attention has been invested in the transfer prices environment by the

Australian Taxation Office (ATO), firstly because of the problem being part of the current

OECD inquiry into foreign tax policies and furthermore because of the political and economic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concerns resulting from the view that "big business" struggles to pay its "good proportion" of tax

in Australia.

For the ATO, it is an overwhelming result and the Chevron choice can have wider implications

for big global taxpaying citizens where loans is supplied either through a financial services hub

or through other organizational by affiliated companies. While the case was provably restricted

to inter group debt arrangements, it is likely that the concepts especially in relation to arms -

length costs of goods will have larger implications (Garzella, Fiorentino & Paolone, 2019). The

case illustrates a need for limited partnership transfers to be worked out in a way compatible with

the standards of tax avoidance, both in respect of arm's reach and economic terms. The

regulatory reporting criteria for taxpayers to show that their stance on transfer pricing is fair are

strict and can impose a heavy burden of enforcement on multinational businesses. However,

following the result of the Chevron ruling, the presumption must be that, with renewed energy,

the ATO will continue to apply the enforcement of the regulations on transfer pricing.

From the point of view of regulation, businesses based on a cross border basis with Australia

must examine their prices of intergroup payments in order to ensure full conformity with the

marketing and paperwork framework that supports them.

The Court dismissed CAHPL’s decision concerning the mortgage interest deduction of USD

2.45 billion (comparable to AUD 3.7 billion) of its interest payments from the Credit Facility

Agreement (About Chevron case, 2020). The Court focused on the political and financial

efficiency of the requirements found in the relevant laws in making its decision. The Court has

addressed, among other aspects, the price of the loan and the interest rate relevant to the

provisions for cross-border funding. By selling a corporate debt in the United States, CFC

collected USD2.45 billion at an interest’s average of nearly 1.25 percent and loaned those funds

to CAHPL at a considerably higher rate (nearly 8 percent) for a five-year period without

collateral or promise. The Court ruled that when deciding whether the deal is at arm's length, an

Australian division of a multinational corporation must not be regarded as a separate body.

Question 5

in Australia.

For the ATO, it is an overwhelming result and the Chevron choice can have wider implications

for big global taxpaying citizens where loans is supplied either through a financial services hub

or through other organizational by affiliated companies. While the case was provably restricted

to inter group debt arrangements, it is likely that the concepts especially in relation to arms -

length costs of goods will have larger implications (Garzella, Fiorentino & Paolone, 2019). The

case illustrates a need for limited partnership transfers to be worked out in a way compatible with

the standards of tax avoidance, both in respect of arm's reach and economic terms. The

regulatory reporting criteria for taxpayers to show that their stance on transfer pricing is fair are

strict and can impose a heavy burden of enforcement on multinational businesses. However,

following the result of the Chevron ruling, the presumption must be that, with renewed energy,

the ATO will continue to apply the enforcement of the regulations on transfer pricing.

From the point of view of regulation, businesses based on a cross border basis with Australia

must examine their prices of intergroup payments in order to ensure full conformity with the

marketing and paperwork framework that supports them.

The Court dismissed CAHPL’s decision concerning the mortgage interest deduction of USD

2.45 billion (comparable to AUD 3.7 billion) of its interest payments from the Credit Facility

Agreement (About Chevron case, 2020). The Court focused on the political and financial

efficiency of the requirements found in the relevant laws in making its decision. The Court has

addressed, among other aspects, the price of the loan and the interest rate relevant to the

provisions for cross-border funding. By selling a corporate debt in the United States, CFC

collected USD2.45 billion at an interest’s average of nearly 1.25 percent and loaned those funds

to CAHPL at a considerably higher rate (nearly 8 percent) for a five-year period without

collateral or promise. The Court ruled that when deciding whether the deal is at arm's length, an

Australian division of a multinational corporation must not be regarded as a separate body.

Question 5

1. Business model of company:

A business model is the central strategy of a corporation for doing business profitably.

Star Entertainment Group consists below mentioned strategies:

Cost differentiation strategy- A differentiation strategy is a strategy which businesses

build by selling anything specific, differentiated and different to consumers from goods

that their rivals can sell in the marketplace (Gordon, 2019). Increasing competitive edge

is the primary goal of executing a differentiation strategy. In the context of above Star

Entertainment Group, they adopt such strategy in accordance of selling their services.

2. Goods and services:

The Star Entertainment Group in Queensland and New South Wales manages and runs

gaming, leisure, lodging and hotel services. The Star Entertainment organization is able

to maximising its resources, promoting the neighbourhoods wherein they reside, and

trying to capitalize on the possibilities provided by our world-class Sydney, Brisbane and

Gold Coast sites. The ambition of the Star Entertainment Empire, of becoming the

leading industrial resort corporation in Australia, is backed by multi-billion - dollar

infrastructure projects expected or in development through its property.

Source of income- The source of income for above company is sales revenues, loans,

investment etc.

3. SWOT analysis of company:

Strengths: Technology of operations brought quality coherence to the product lines of

The Star Entertainment Group Limited and helps the organization to scale up and scale

down on the basis of market growth circumstances (Ravselj & Aristovnik, 2019). They

have proven record through merger and acquisition & acquisition to integrate

complimentary companies.

A business model is the central strategy of a corporation for doing business profitably.

Star Entertainment Group consists below mentioned strategies:

Cost differentiation strategy- A differentiation strategy is a strategy which businesses

build by selling anything specific, differentiated and different to consumers from goods

that their rivals can sell in the marketplace (Gordon, 2019). Increasing competitive edge

is the primary goal of executing a differentiation strategy. In the context of above Star

Entertainment Group, they adopt such strategy in accordance of selling their services.

2. Goods and services:

The Star Entertainment Group in Queensland and New South Wales manages and runs

gaming, leisure, lodging and hotel services. The Star Entertainment organization is able

to maximising its resources, promoting the neighbourhoods wherein they reside, and

trying to capitalize on the possibilities provided by our world-class Sydney, Brisbane and

Gold Coast sites. The ambition of the Star Entertainment Empire, of becoming the

leading industrial resort corporation in Australia, is backed by multi-billion - dollar

infrastructure projects expected or in development through its property.

Source of income- The source of income for above company is sales revenues, loans,

investment etc.

3. SWOT analysis of company:

Strengths: Technology of operations brought quality coherence to the product lines of

The Star Entertainment Group Limited and helps the organization to scale up and scale

down on the basis of market growth circumstances (Ravselj & Aristovnik, 2019). They

have proven record through merger and acquisition & acquisition to integrate

complimentary companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Weakness: The organisation has not been able to overcome the demands of the new

entrants in the sector and has lost a limited market share in the product areas. To

overcome these problems, Star Entertainment Company Limited must create a personal

input process directly from of the sales staff on the field.

Opportunity: The growth of the industry would result in the concentration of the

competitor’s edge which will allow The Star Entertainment Group Limited to improve its

competition relative to other rivals.

Threats: The organisation has produced various products in the market, but these are

mostly a reaction to the success of other players. Lastly, the availability of new goods is

not normal, which results in high and low fluctuations over time in the amount of

transactions.

4. The source of income can be identified by tax authorities. It is so because by help of

different kinds of financial statements, this becomes feasible for tax authorities to assess

what is the source of income for a company (Lind & Nordlund, 2019).

5. In year 2018-19, this can be find out that company paid tax of 62.3 and 80.7 million.

While net income was of 148.1 and 198 million. This tax was the 42.06% and 45%.

In UK, the tax rate is of 19%, in USA, it is of 21% and in Australia it is of 30%. It shows

that there is difference in paid tax rate of Star Entertainment Group Limited as compared

to government tax rate of various nations.

Question 6

Advantages/disadvantages of having the financial reports for the company audited.

A financial audit — sometimes referred to as a financial statement audit — is the formal report

arising from a competent inspector's analysis of the firm's books — usually a registered public

entrants in the sector and has lost a limited market share in the product areas. To

overcome these problems, Star Entertainment Company Limited must create a personal

input process directly from of the sales staff on the field.

Opportunity: The growth of the industry would result in the concentration of the

competitor’s edge which will allow The Star Entertainment Group Limited to improve its

competition relative to other rivals.

Threats: The organisation has produced various products in the market, but these are

mostly a reaction to the success of other players. Lastly, the availability of new goods is

not normal, which results in high and low fluctuations over time in the amount of

transactions.

4. The source of income can be identified by tax authorities. It is so because by help of

different kinds of financial statements, this becomes feasible for tax authorities to assess

what is the source of income for a company (Lind & Nordlund, 2019).

5. In year 2018-19, this can be find out that company paid tax of 62.3 and 80.7 million.

While net income was of 148.1 and 198 million. This tax was the 42.06% and 45%.

In UK, the tax rate is of 19%, in USA, it is of 21% and in Australia it is of 30%. It shows

that there is difference in paid tax rate of Star Entertainment Group Limited as compared

to government tax rate of various nations.

Question 6

Advantages/disadvantages of having the financial reports for the company audited.

A financial audit — sometimes referred to as a financial statement audit — is the formal report

arising from a competent inspector's analysis of the firm's books — usually a registered public

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting or a financial accounting firm hiring competent specialists. The study states that the

provided financial statements and records are truthful and reasonable. In the context of T & T

limited, auditing of financial reports may lead to below mentioned advantages and disadvantages

which are as follows:

Advantage: Several separate people profit from a competent audit. For a company's officers, the

examination includes an external assurance of the financial stability of the company that supports

their effective management (Kieso, Weygandt & Warfield, 2020). The financial audit is a vital

way for shareholders to determine the business's valuation. For the corporate sector, annual

audits boost the image of the enterprise and make it a successful business partner. Financial

assessments are a requirement for virtually every sort of corporate loan for the company's

lenders.

Disadvantage: The benefits of an audit well outweigh the risks under certain cases, which is why

most organizations undergo routine audits and reviews are a legal necessity for any public

corporation. However, audits are not in any way free. A survey commissioned by the Financial

Officers Research Foundation (FERF) concluded that there was an estimate of more than $7

million in 2013 audit costs for public corporations. This isn't the only burden. An audit is a

required but substantial disturbance to the working of the organization and may decrease morale

for the duration of the audit when workers delay other duties to fulfill the demands of the auditor.

Borrowing of USD $30 million for expansion into a new market in Dubai UAE.

As per the given information, this is mentioned that T& T limited wants to expand its business in

Dubai. For this purpose, they want to take loan of $30 million. In this aspect, it is important for

them that they should take loan from a source whose interest rate is lower (McEnroe & Mindak,

2020).They might take loan from bank. It is so because taking loan from bank is suitable method

for each company. Banks offer loan at very low cost and there is an easy process for taking loan.

Apart from the taking the financial assistance, it is necessary for T& T limited that they should

assess Dubai’s business environment, regulations and many other aspects. This is so because

before entering in a nation for business, it is important to assess their rules and regulations so that

provided financial statements and records are truthful and reasonable. In the context of T & T

limited, auditing of financial reports may lead to below mentioned advantages and disadvantages

which are as follows:

Advantage: Several separate people profit from a competent audit. For a company's officers, the

examination includes an external assurance of the financial stability of the company that supports

their effective management (Kieso, Weygandt & Warfield, 2020). The financial audit is a vital

way for shareholders to determine the business's valuation. For the corporate sector, annual

audits boost the image of the enterprise and make it a successful business partner. Financial

assessments are a requirement for virtually every sort of corporate loan for the company's

lenders.

Disadvantage: The benefits of an audit well outweigh the risks under certain cases, which is why

most organizations undergo routine audits and reviews are a legal necessity for any public

corporation. However, audits are not in any way free. A survey commissioned by the Financial

Officers Research Foundation (FERF) concluded that there was an estimate of more than $7

million in 2013 audit costs for public corporations. This isn't the only burden. An audit is a

required but substantial disturbance to the working of the organization and may decrease morale

for the duration of the audit when workers delay other duties to fulfill the demands of the auditor.

Borrowing of USD $30 million for expansion into a new market in Dubai UAE.

As per the given information, this is mentioned that T& T limited wants to expand its business in

Dubai. For this purpose, they want to take loan of $30 million. In this aspect, it is important for

them that they should take loan from a source whose interest rate is lower (McEnroe & Mindak,

2020).They might take loan from bank. It is so because taking loan from bank is suitable method

for each company. Banks offer loan at very low cost and there is an easy process for taking loan.

Apart from the taking the financial assistance, it is necessary for T& T limited that they should

assess Dubai’s business environment, regulations and many other aspects. This is so because

before entering in a nation for business, it is important to assess their rules and regulations so that

they can sustain in that country (Svynous, Shepel & Lytvynenko, 2019). Hence, above company

needs to assess complete PESTEL analysis of engineering steel fabrication sector in the Dubai.

In addition, above company should make proper analysis of competitive environment in that

country so that they can survive.

needs to assess complete PESTEL analysis of engineering steel fabrication sector in the Dubai.

In addition, above company should make proper analysis of competitive environment in that

country so that they can survive.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.