Detailed Analysis of IAS 16 and IAS 37 in Financial Reporting

VerifiedAdded on 2020/09/03

|13

|3680

|65

Report

AI Summary

This report delves into two key International Accounting Standards: IAS 16, focusing on property, plant, and equipment (PPE), and IAS 37, which addresses provisions, contingent assets, and liabilities. The report begins with an overview of IAS 16, detailing asset recognition, valuation methods (cost and revaluation models), depreciation calculations, and impairment testing. It then presents a practical application of these concepts, calculating book value and depreciation for a company's ships under both the historical cost and revaluation models, followed by a discussion of the challenges encountered in the valuation process. The second part of the report evaluates IAS 37, explaining provisions, contingent liabilities, and contingent assets. It outlines the recognition criteria for provisions and discusses different types of obligations. The report concludes by emphasizing the importance of understanding and correctly applying these standards for accurate financial reporting, ensuring that financial statements reflect a true and fair view of a company's financial position and performance.

International financial

reporting

reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(I) Evaluation of property, plant and equipment related standard..............................................1

(II) Calculation of book value and depreciation.........................................................................2

QUESTION 2...................................................................................................................................4

(I) Evaluation of IAS 37..............................................................................................................4

(II) Accounting of various cases.................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(I) Evaluation of property, plant and equipment related standard..............................................1

(II) Calculation of book value and depreciation.........................................................................2

QUESTION 2...................................................................................................................................4

(I) Evaluation of IAS 37..............................................................................................................4

(II) Accounting of various cases.................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

In any organisation there are various financial aspects in respect of which reporting is

required to be made. For this purpose various international accounting standards have been made

which are required to be followed and complied with (Van Greuning, Scott and Terblanche,

2011). There are many such provisions that are specified which provides guidance so that correct

treatment can be given to all the transactions made in business. In this report two such standards

will be discussed which are related to plant and equipment that is IAS 16 and another is IAS 37

under which provisions, contingent assets and liabilities are taken into consideration. So for

proper functioning an understanding in relation to them can be obtained from below presented

report.

QUESTION 1

(I) Evaluation of property, plant and equipment related standard.

IAS 16 is the standard which has been formulated in respect of property and plant. The

main objective of this is to specify the manner in which accounting treatment shall be made of

various plants. The main issues which are faced and are dealt with in this standard includes asset

recognition, valuation, depreciation and impairment to be considered for them.

This will be applied for all the assets but those which are governed by some other rules

such as biological assets, mineral resources and others will not be included under this (Doupnik

and Perera, 2011). The recognition criteria that shall be met specifies that it shall be ensured that

future benefits will be derived from it and also it can be measured. If these conditions are

fulfilled then the respective asset shall be recognised and recorded in books. In this all the cost

shall be taken into consideration at the time they are incurred. All the cost which are made in

future for the replacement purpose will also be included in the calculation of carrying amount.

The recording shall be done on cost at initial stage. In this all the amounts which are spend to

bring the asset at stage of utilisation shall be included. There are two methods which can be used

for valuation after the initial recognition and they are cost and revaluation model.

In case of cost model value determined by deducting depreciation from cost will be

considered as carrying amount. Whereas in revaluation model the amount obtained after

deduction of depreciation from revalued value shall be used. Depreciation shall be calculated on

1

In any organisation there are various financial aspects in respect of which reporting is

required to be made. For this purpose various international accounting standards have been made

which are required to be followed and complied with (Van Greuning, Scott and Terblanche,

2011). There are many such provisions that are specified which provides guidance so that correct

treatment can be given to all the transactions made in business. In this report two such standards

will be discussed which are related to plant and equipment that is IAS 16 and another is IAS 37

under which provisions, contingent assets and liabilities are taken into consideration. So for

proper functioning an understanding in relation to them can be obtained from below presented

report.

QUESTION 1

(I) Evaluation of property, plant and equipment related standard.

IAS 16 is the standard which has been formulated in respect of property and plant. The

main objective of this is to specify the manner in which accounting treatment shall be made of

various plants. The main issues which are faced and are dealt with in this standard includes asset

recognition, valuation, depreciation and impairment to be considered for them.

This will be applied for all the assets but those which are governed by some other rules

such as biological assets, mineral resources and others will not be included under this (Doupnik

and Perera, 2011). The recognition criteria that shall be met specifies that it shall be ensured that

future benefits will be derived from it and also it can be measured. If these conditions are

fulfilled then the respective asset shall be recognised and recorded in books. In this all the cost

shall be taken into consideration at the time they are incurred. All the cost which are made in

future for the replacement purpose will also be included in the calculation of carrying amount.

The recording shall be done on cost at initial stage. In this all the amounts which are spend to

bring the asset at stage of utilisation shall be included. There are two methods which can be used

for valuation after the initial recognition and they are cost and revaluation model.

In case of cost model value determined by deducting depreciation from cost will be

considered as carrying amount. Whereas in revaluation model the amount obtained after

deduction of depreciation from revalued value shall be used. Depreciation shall be calculated on

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the basis of useful life of asset which means that whole cost shall be distributed among life and

then that shall be charged on yearly basis.

According to this standard it is required that impairment test shall be conducted at regular

interval as by this it is identified that whether assets are mentioned at correct value or not. It shall

be ensured that recognised value shall not be more than the recoverable value (Nobes, 2014). So

test will be carried out and is any excess is determined then that shall be treated as impairment

loss and shall be charged in that year.

There are various situation under which asset will have to be removed from financial

statements and that includes sale of asset or withdrawal of it from use or when it is identified that

there will be no future benefits which will be derived from it.

In respect of all the plants and properties which are held by business, it is required that

certain disclosures shall be made which have been mentioned in following standard. Under this

the carrying amount, method of depreciation used, life of asset and any other important

information shall be provided with. In case of revaluation, date on which it is made, revalued

amount, previous value and any loss or profit made by this shall be disclosed in financial

reporting.

(II) Calculation of book value and depreciation.

In LC there are four ships which are owned by them and the method which is used by

them for calculation of value is cost less depreciation. But now revaluation is carried out in

respect of them and so it wants to know the manner in which further valuation shall be carried

out. For this purpose there are various methods that can be used and of which an understanding

has been obtained above. For that various figures are required to be identified which includes

revalued amount, life which is remaining. So with the help of all of then calculation of carrying

amount and depreciation can be made. So the same is provided below:

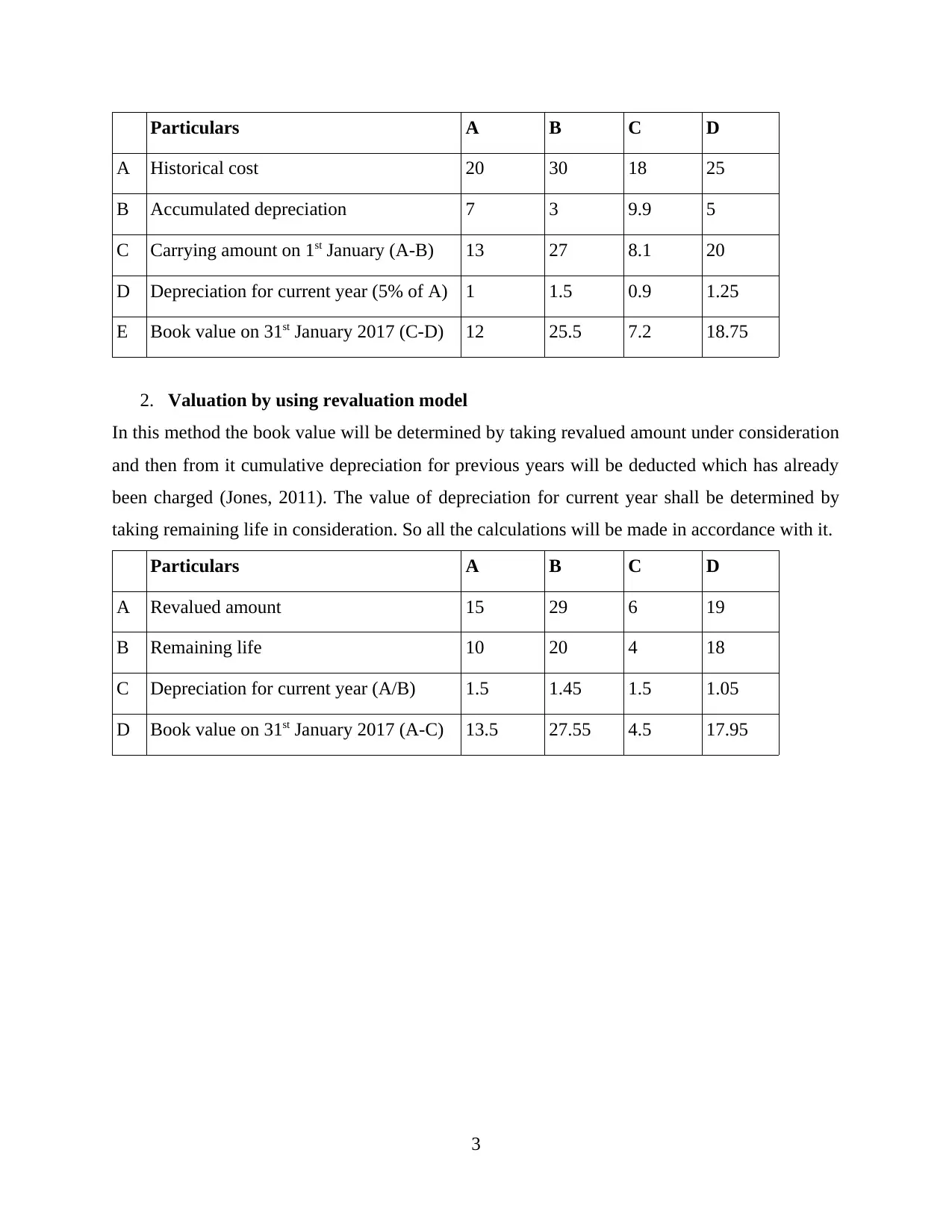

1. Valuation by deduction of depreciation from historical cost.

Under this method carrying amount is calculated by deducting accumulated depreciation from

the historical cost. Here this cost means the value for which asset has been acquired and at which

recording was made at initial stage. The depreciation is charged by company at rate of 5 percent

and so this will be used to ascertain it in respect of current year.

Calculation of book value and depreciation amount

2

then that shall be charged on yearly basis.

According to this standard it is required that impairment test shall be conducted at regular

interval as by this it is identified that whether assets are mentioned at correct value or not. It shall

be ensured that recognised value shall not be more than the recoverable value (Nobes, 2014). So

test will be carried out and is any excess is determined then that shall be treated as impairment

loss and shall be charged in that year.

There are various situation under which asset will have to be removed from financial

statements and that includes sale of asset or withdrawal of it from use or when it is identified that

there will be no future benefits which will be derived from it.

In respect of all the plants and properties which are held by business, it is required that

certain disclosures shall be made which have been mentioned in following standard. Under this

the carrying amount, method of depreciation used, life of asset and any other important

information shall be provided with. In case of revaluation, date on which it is made, revalued

amount, previous value and any loss or profit made by this shall be disclosed in financial

reporting.

(II) Calculation of book value and depreciation.

In LC there are four ships which are owned by them and the method which is used by

them for calculation of value is cost less depreciation. But now revaluation is carried out in

respect of them and so it wants to know the manner in which further valuation shall be carried

out. For this purpose there are various methods that can be used and of which an understanding

has been obtained above. For that various figures are required to be identified which includes

revalued amount, life which is remaining. So with the help of all of then calculation of carrying

amount and depreciation can be made. So the same is provided below:

1. Valuation by deduction of depreciation from historical cost.

Under this method carrying amount is calculated by deducting accumulated depreciation from

the historical cost. Here this cost means the value for which asset has been acquired and at which

recording was made at initial stage. The depreciation is charged by company at rate of 5 percent

and so this will be used to ascertain it in respect of current year.

Calculation of book value and depreciation amount

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars A B C D

A Historical cost 20 30 18 25

B Accumulated depreciation 7 3 9.9 5

C Carrying amount on 1st January (A-B) 13 27 8.1 20

D Depreciation for current year (5% of A) 1 1.5 0.9 1.25

E Book value on 31st January 2017 (C-D) 12 25.5 7.2 18.75

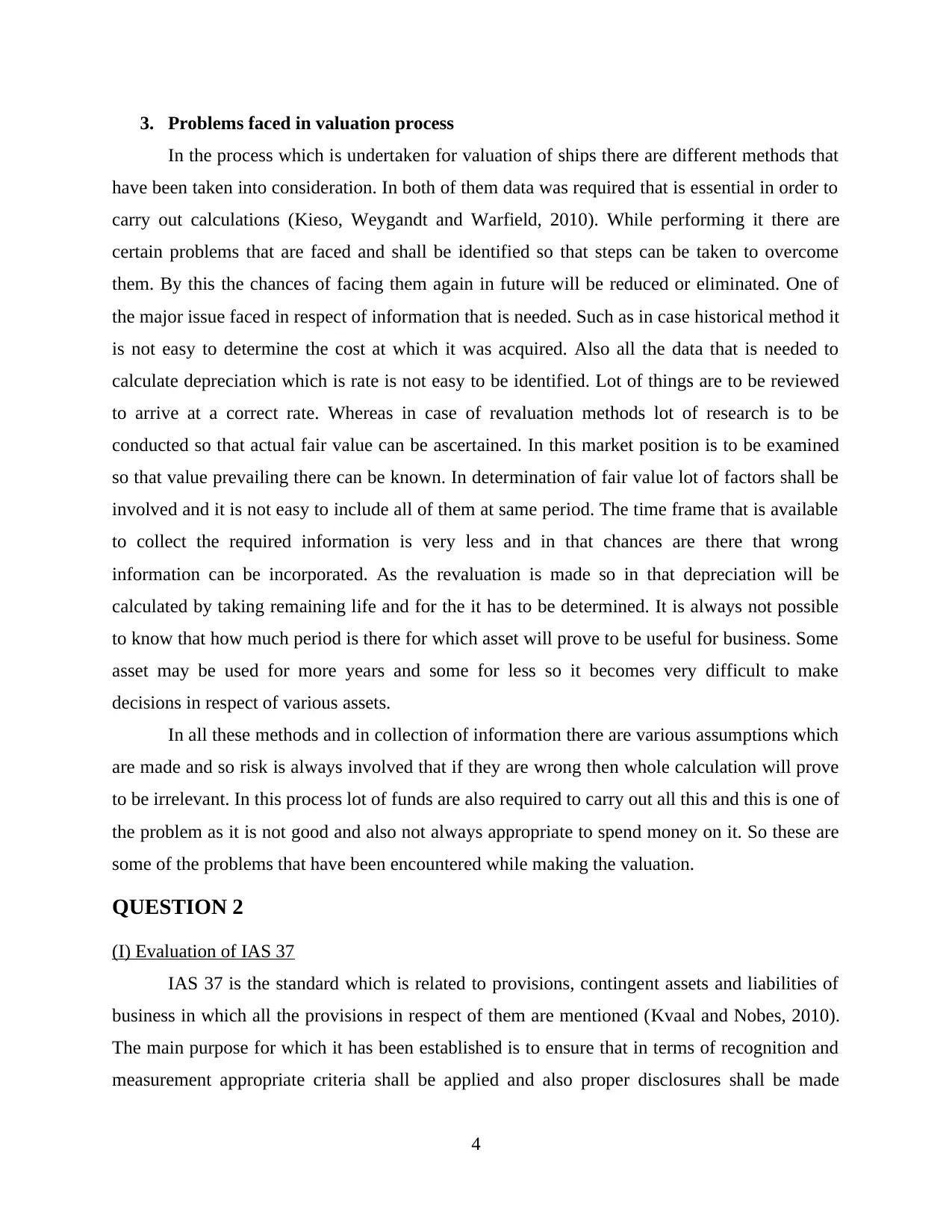

2. Valuation by using revaluation model

In this method the book value will be determined by taking revalued amount under consideration

and then from it cumulative depreciation for previous years will be deducted which has already

been charged (Jones, 2011). The value of depreciation for current year shall be determined by

taking remaining life in consideration. So all the calculations will be made in accordance with it.

Particulars A B C D

A Revalued amount 15 29 6 19

B Remaining life 10 20 4 18

C Depreciation for current year (A/B) 1.5 1.45 1.5 1.05

D Book value on 31st January 2017 (A-C) 13.5 27.55 4.5 17.95

3

A Historical cost 20 30 18 25

B Accumulated depreciation 7 3 9.9 5

C Carrying amount on 1st January (A-B) 13 27 8.1 20

D Depreciation for current year (5% of A) 1 1.5 0.9 1.25

E Book value on 31st January 2017 (C-D) 12 25.5 7.2 18.75

2. Valuation by using revaluation model

In this method the book value will be determined by taking revalued amount under consideration

and then from it cumulative depreciation for previous years will be deducted which has already

been charged (Jones, 2011). The value of depreciation for current year shall be determined by

taking remaining life in consideration. So all the calculations will be made in accordance with it.

Particulars A B C D

A Revalued amount 15 29 6 19

B Remaining life 10 20 4 18

C Depreciation for current year (A/B) 1.5 1.45 1.5 1.05

D Book value on 31st January 2017 (A-C) 13.5 27.55 4.5 17.95

3

3. Problems faced in valuation process

In the process which is undertaken for valuation of ships there are different methods that

have been taken into consideration. In both of them data was required that is essential in order to

carry out calculations (Kieso, Weygandt and Warfield, 2010). While performing it there are

certain problems that are faced and shall be identified so that steps can be taken to overcome

them. By this the chances of facing them again in future will be reduced or eliminated. One of

the major issue faced in respect of information that is needed. Such as in case historical method it

is not easy to determine the cost at which it was acquired. Also all the data that is needed to

calculate depreciation which is rate is not easy to be identified. Lot of things are to be reviewed

to arrive at a correct rate. Whereas in case of revaluation methods lot of research is to be

conducted so that actual fair value can be ascertained. In this market position is to be examined

so that value prevailing there can be known. In determination of fair value lot of factors shall be

involved and it is not easy to include all of them at same period. The time frame that is available

to collect the required information is very less and in that chances are there that wrong

information can be incorporated. As the revaluation is made so in that depreciation will be

calculated by taking remaining life and for the it has to be determined. It is always not possible

to know that how much period is there for which asset will prove to be useful for business. Some

asset may be used for more years and some for less so it becomes very difficult to make

decisions in respect of various assets.

In all these methods and in collection of information there are various assumptions which

are made and so risk is always involved that if they are wrong then whole calculation will prove

to be irrelevant. In this process lot of funds are also required to carry out all this and this is one of

the problem as it is not good and also not always appropriate to spend money on it. So these are

some of the problems that have been encountered while making the valuation.

QUESTION 2

(I) Evaluation of IAS 37

IAS 37 is the standard which is related to provisions, contingent assets and liabilities of

business in which all the provisions in respect of them are mentioned (Kvaal and Nobes, 2010).

The main purpose for which it has been established is to ensure that in terms of recognition and

measurement appropriate criteria shall be applied and also proper disclosures shall be made

4

In the process which is undertaken for valuation of ships there are different methods that

have been taken into consideration. In both of them data was required that is essential in order to

carry out calculations (Kieso, Weygandt and Warfield, 2010). While performing it there are

certain problems that are faced and shall be identified so that steps can be taken to overcome

them. By this the chances of facing them again in future will be reduced or eliminated. One of

the major issue faced in respect of information that is needed. Such as in case historical method it

is not easy to determine the cost at which it was acquired. Also all the data that is needed to

calculate depreciation which is rate is not easy to be identified. Lot of things are to be reviewed

to arrive at a correct rate. Whereas in case of revaluation methods lot of research is to be

conducted so that actual fair value can be ascertained. In this market position is to be examined

so that value prevailing there can be known. In determination of fair value lot of factors shall be

involved and it is not easy to include all of them at same period. The time frame that is available

to collect the required information is very less and in that chances are there that wrong

information can be incorporated. As the revaluation is made so in that depreciation will be

calculated by taking remaining life and for the it has to be determined. It is always not possible

to know that how much period is there for which asset will prove to be useful for business. Some

asset may be used for more years and some for less so it becomes very difficult to make

decisions in respect of various assets.

In all these methods and in collection of information there are various assumptions which

are made and so risk is always involved that if they are wrong then whole calculation will prove

to be irrelevant. In this process lot of funds are also required to carry out all this and this is one of

the problem as it is not good and also not always appropriate to spend money on it. So these are

some of the problems that have been encountered while making the valuation.

QUESTION 2

(I) Evaluation of IAS 37

IAS 37 is the standard which is related to provisions, contingent assets and liabilities of

business in which all the provisions in respect of them are mentioned (Kvaal and Nobes, 2010).

The main purpose for which it has been established is to ensure that in terms of recognition and

measurement appropriate criteria shall be applied and also proper disclosures shall be made

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

about them in accounts and by that the persons who will be using them can have the knowledge

regarding nature, time and amount of them.

By this it can be ensured that only those liabilities which are genuine will be included in

financial statements and due to this recognition of provisions is made when it is sure that there is

certain liability to be met in relation to them.

Under this all those obligations which are dealt by other standards such as in respect of

financial instruments, insurance contracts and other onerous contracts are not covered under this

standard (Byard, Li and Yu, 2011). In order to understand this in better manner it is required that

knowledge shall be there about various terms that are involved under it. Due to this some of the

key terms are explained below:

Provisions: This is the liability which is arising due to any past event and in which although time

and amount is not certain but then also it is known that liability will be arising and it is probable

that payments will have to be made.

Contingent liability: In this the probability of liability is dependent on some vent which will be

occurring in future period or the liability is related to present event but is payment is not

probable and also amount is not ascertainable.

Contingent assets: This is the asset which arise due to some event in past but confirmation of

existence will be dependent of occurrence of any event in future which is uncertain.

So these are some of the terms that shall be known by all in order to provide correct

treatment of them in process of financial reporting. There are certain regulations which are made

by which recognition shall be considered and that says that any provision will be recognised only

when the obligation which is there in present is outcome of some past event and also it is

probable that amount is to be paid and it can also be ascertained in most appropriate manner.

In business there are two types of obligations which are faced and have been mentioned

in this standard and they are constructive in which liability is due to past and third party is

involved in this and another is possible obligation which has been disclosed but has not accrued.

In this if the payment to be made is of small amount then there will be no requirement to make

any disclosures.

In order to disclose the provision it is needed that amount of it shall be measured which

will be recorded. In this it is determined by taking estimates on the balance sheet date about the

amount which can be incurred for the obligations (Cotter, 2012). Most likely amount will be

5

regarding nature, time and amount of them.

By this it can be ensured that only those liabilities which are genuine will be included in

financial statements and due to this recognition of provisions is made when it is sure that there is

certain liability to be met in relation to them.

Under this all those obligations which are dealt by other standards such as in respect of

financial instruments, insurance contracts and other onerous contracts are not covered under this

standard (Byard, Li and Yu, 2011). In order to understand this in better manner it is required that

knowledge shall be there about various terms that are involved under it. Due to this some of the

key terms are explained below:

Provisions: This is the liability which is arising due to any past event and in which although time

and amount is not certain but then also it is known that liability will be arising and it is probable

that payments will have to be made.

Contingent liability: In this the probability of liability is dependent on some vent which will be

occurring in future period or the liability is related to present event but is payment is not

probable and also amount is not ascertainable.

Contingent assets: This is the asset which arise due to some event in past but confirmation of

existence will be dependent of occurrence of any event in future which is uncertain.

So these are some of the terms that shall be known by all in order to provide correct

treatment of them in process of financial reporting. There are certain regulations which are made

by which recognition shall be considered and that says that any provision will be recognised only

when the obligation which is there in present is outcome of some past event and also it is

probable that amount is to be paid and it can also be ascertained in most appropriate manner.

In business there are two types of obligations which are faced and have been mentioned

in this standard and they are constructive in which liability is due to past and third party is

involved in this and another is possible obligation which has been disclosed but has not accrued.

In this if the payment to be made is of small amount then there will be no requirement to make

any disclosures.

In order to disclose the provision it is needed that amount of it shall be measured which

will be recorded. In this it is determined by taking estimates on the balance sheet date about the

amount which can be incurred for the obligations (Cotter, 2012). Most likely amount will be

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

taken for provisions of those events which are one off and for large populations, expected value

on basis of probability are taken. To bring the amount in terms of present condition, discounting

will be done for which rate at which time value of money and risk are considered are used.

All the uncertainty and risk which is involved in events shall be taken into consideration

while making estimates so that best among them can be selected (Herrmann, Saudagaran and

Thomas, 2006). If the case is such in which all the amount of liability will be reimbursed by

some other person than that value will be not have to be shown as deduction rather it will be

recognised as a separate asset. While the provisions are measured, then at that time future events

shall be considered such as any change that may take place in terms of technology and in this any

gain or loss which can be made on sale will have to be ignored. Also if there are nay legal

changes then they will be incorporated only when there is virtual certainty that they shall be

enacted.

All the provisions which have been made will have to be reviewed at the end of each year

and if it is found that there is no probable event in which outflow will be made then that amount

which is related to it shall be reversed.

The last part of this standard states rules of disclosure in which it is needed that all the

accounts of provisions shall be reconciled in which opening balance and any addition or

deduction shall be adjusted so that closing figure can be matched. Also all the assumptions,

nature, timing and uncertainties related to any provision shall be disclosed.

(II) Accounting of various cases.

(A)

In this case a service is provided to customers in respect of repairs that will be done if any

defect is found in construction within a time span of three months. If such condition arises the

repair service will be provided on immediate basis (IAS 37 PROVISIONS, CONTINGENT

LIABILITIES, AND CONTINGENT ASSETS, 2017). According to the regulations which are

described above in respect of provisions it has been stated that recognition will be done only

when specified conditions are met. In this it is to be identified that whether the liability is result

of any past event and it is probable that amount will have to be spend and also that amount can

be ascertained. If all the conditions are met then provision is to be made otherwise contingent

liability shall be made.

6

on basis of probability are taken. To bring the amount in terms of present condition, discounting

will be done for which rate at which time value of money and risk are considered are used.

All the uncertainty and risk which is involved in events shall be taken into consideration

while making estimates so that best among them can be selected (Herrmann, Saudagaran and

Thomas, 2006). If the case is such in which all the amount of liability will be reimbursed by

some other person than that value will be not have to be shown as deduction rather it will be

recognised as a separate asset. While the provisions are measured, then at that time future events

shall be considered such as any change that may take place in terms of technology and in this any

gain or loss which can be made on sale will have to be ignored. Also if there are nay legal

changes then they will be incorporated only when there is virtual certainty that they shall be

enacted.

All the provisions which have been made will have to be reviewed at the end of each year

and if it is found that there is no probable event in which outflow will be made then that amount

which is related to it shall be reversed.

The last part of this standard states rules of disclosure in which it is needed that all the

accounts of provisions shall be reconciled in which opening balance and any addition or

deduction shall be adjusted so that closing figure can be matched. Also all the assumptions,

nature, timing and uncertainties related to any provision shall be disclosed.

(II) Accounting of various cases.

(A)

In this case a service is provided to customers in respect of repairs that will be done if any

defect is found in construction within a time span of three months. If such condition arises the

repair service will be provided on immediate basis (IAS 37 PROVISIONS, CONTINGENT

LIABILITIES, AND CONTINGENT ASSETS, 2017). According to the regulations which are

described above in respect of provisions it has been stated that recognition will be done only

when specified conditions are met. In this it is to be identified that whether the liability is result

of any past event and it is probable that amount will have to be spend and also that amount can

be ascertained. If all the conditions are met then provision is to be made otherwise contingent

liability shall be made.

6

Here the obligation is result of the construction activity which has ben performed in past

and then th offer is given to customer to inform about any defect to company so that repair can

be made. Also by looking to the past amounts and trends it is probable that liability will be

arising and will have to be met. The last condition which is that amount can be estimated is also

met as it has been provided that last year provision was at 180000 which in 2016 is estimated at

120000. so as all the conditions which have been mentioned in this respect are met therefore

recognition will be made of provision. That will be shown in the liability side of statements of

financial provision under the head of current liability. The amount in given case in respect of it is

120000 which shall be mentioned in balance sheet and when liability will be arising in actual the

it will have to be written off or can be reversed.

(B)

The case which is presented is related to the complaint that has been lodged against a

engineering firm as there was delay which was made by it in construction. For this it has been

agreed by company that payment of compensation will be made. According to the rules an

amount which is probable to be received and it is due to some event which has taken place in

past then that shall be recognised as contingent asset (Carmona and Trombetta, 2008). But in

addition to all this another condition which also shall be met is that amount of receipt should be

identifiable. Here as the construction has been made in past so it will be treated as past event and

the compensation to be paid by firm is present obligation or can say receipt for company so all of

these two conditions are satisfied. Also the amount which is to be received by it is also

determined. As all the three demands to be met are fulfilled so there is no doubt regarding it and

the amount of 230 shall be recognised as contingent asset.

The amount of contingent asset can never be shown in statements of financial position. It

will have to be disclosed in notes which are prepared together with financial statements. In that

the amount which will be received, its nature and time within which it is expected shall be

mentioned.

By all the discussion an understanding is obtained and it can be said that this will be

helpful in achieving the common objective of financial reporting. The aim is to make the

disclosures in such manner by which true and fair position of business is reflected. This help in

knowing the exact positions and if any issue are there then they can be dealt with in most

appropriate manner. Also as accounts are made to be used by others who will be placing their

7

and then th offer is given to customer to inform about any defect to company so that repair can

be made. Also by looking to the past amounts and trends it is probable that liability will be

arising and will have to be met. The last condition which is that amount can be estimated is also

met as it has been provided that last year provision was at 180000 which in 2016 is estimated at

120000. so as all the conditions which have been mentioned in this respect are met therefore

recognition will be made of provision. That will be shown in the liability side of statements of

financial provision under the head of current liability. The amount in given case in respect of it is

120000 which shall be mentioned in balance sheet and when liability will be arising in actual the

it will have to be written off or can be reversed.

(B)

The case which is presented is related to the complaint that has been lodged against a

engineering firm as there was delay which was made by it in construction. For this it has been

agreed by company that payment of compensation will be made. According to the rules an

amount which is probable to be received and it is due to some event which has taken place in

past then that shall be recognised as contingent asset (Carmona and Trombetta, 2008). But in

addition to all this another condition which also shall be met is that amount of receipt should be

identifiable. Here as the construction has been made in past so it will be treated as past event and

the compensation to be paid by firm is present obligation or can say receipt for company so all of

these two conditions are satisfied. Also the amount which is to be received by it is also

determined. As all the three demands to be met are fulfilled so there is no doubt regarding it and

the amount of 230 shall be recognised as contingent asset.

The amount of contingent asset can never be shown in statements of financial position. It

will have to be disclosed in notes which are prepared together with financial statements. In that

the amount which will be received, its nature and time within which it is expected shall be

mentioned.

By all the discussion an understanding is obtained and it can be said that this will be

helpful in achieving the common objective of financial reporting. The aim is to make the

disclosures in such manner by which true and fair position of business is reflected. This help in

knowing the exact positions and if any issue are there then they can be dealt with in most

appropriate manner. Also as accounts are made to be used by others who will be placing their

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reliance on then so they shall represent fair condition (Ampofo and Sellani, 2005). This will help

them in making all the proper decisions which are required by them. also they will be able to

form a positive image of company as true facts are disclosed and this will give them confidence

to trust on it and make investments in business. So there will be overall growth and development

which will be achieved by company with the help of it.

CONCLUSION

From the above mentioned report it can be concluded that in order to run the business in

successful manner and make proper disclosures, it is very important that all the standards shall be

followed. In this the manner in which plant and property shall be valued is determined. Also

treatment which shall be made about the provisions and assets, liabilities which are contingent s

described. The conditions to be met in order to recognise them and manner in which disclosure

shall be made is determined by this report.

8

them in making all the proper decisions which are required by them. also they will be able to

form a positive image of company as true facts are disclosed and this will give them confidence

to trust on it and make investments in business. So there will be overall growth and development

which will be achieved by company with the help of it.

CONCLUSION

From the above mentioned report it can be concluded that in order to run the business in

successful manner and make proper disclosures, it is very important that all the standards shall be

followed. In this the manner in which plant and property shall be valued is determined. Also

treatment which shall be made about the provisions and assets, liabilities which are contingent s

described. The conditions to be met in order to recognise them and manner in which disclosure

shall be made is determined by this report.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Journals and Books

Ampofo, A.A. and Sellani, R.J., 2005, June. Examining the differences between United States

Generally Accepted Accounting Principles (US GAAP) and International Accounting

Standards (IAS): implications for the harmonization of accounting standards. In

Accounting forum (Vol. 29, No. 2, pp. 219-231). Elsevier.

Byard, D., Li, Y. and Yu, Y., 2011. The effect of mandatory IFRS adoption on financial

analysts’ information environment. Journal of accounting research. 49(1). pp.69-96.

Carmona, S. and Trombetta, M., 2008. On the global acceptance of IAS/IFRS accounting

standards: The logic and implications of the principles-based system. Journal of

Accounting and Public Policy. 27(6). pp.455-461.

Cotter, D., 2012. Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Doupnik, T. and Perera, H., 2011. International accounting.

Herrmann, D., Saudagaran, S.M. and Thomas, W.B., 2006, March. The quality of fair value

measures for property, plant, and equipment. In Accounting Forum (Vol. 30, No. 1, pp.

43-59). Elsevier.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2010. Intermediate accounting: IFRS edition

(Vol. 2). John Wiley & Sons.

Kvaal, E. and Nobes, C., 2010. International differences in IFRS policy choice: a research note.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Van Greuning, H., Scott, D. and Terblanche, S., 2011. International financial reporting

standards: a practical guide. World Bank Publications.

Online

IAS 37 PROVISIONS, CONTINGENT LIABILITIES, AND CONTINGENT ASSETS. 2017.

[Online]. Available through<https://www.safaribooksonline.com/library/view/ifrs-

essentials/9781118501344/OEBPS/9781118501344_epub_c_26.htm> [Accessed on 4th

October 2017].

9

Journals and Books

Ampofo, A.A. and Sellani, R.J., 2005, June. Examining the differences between United States

Generally Accepted Accounting Principles (US GAAP) and International Accounting

Standards (IAS): implications for the harmonization of accounting standards. In

Accounting forum (Vol. 29, No. 2, pp. 219-231). Elsevier.

Byard, D., Li, Y. and Yu, Y., 2011. The effect of mandatory IFRS adoption on financial

analysts’ information environment. Journal of accounting research. 49(1). pp.69-96.

Carmona, S. and Trombetta, M., 2008. On the global acceptance of IAS/IFRS accounting

standards: The logic and implications of the principles-based system. Journal of

Accounting and Public Policy. 27(6). pp.455-461.

Cotter, D., 2012. Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Doupnik, T. and Perera, H., 2011. International accounting.

Herrmann, D., Saudagaran, S.M. and Thomas, W.B., 2006, March. The quality of fair value

measures for property, plant, and equipment. In Accounting Forum (Vol. 30, No. 1, pp.

43-59). Elsevier.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2010. Intermediate accounting: IFRS edition

(Vol. 2). John Wiley & Sons.

Kvaal, E. and Nobes, C., 2010. International differences in IFRS policy choice: a research note.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Van Greuning, H., Scott, D. and Terblanche, S., 2011. International financial reporting

standards: a practical guide. World Bank Publications.

Online

IAS 37 PROVISIONS, CONTINGENT LIABILITIES, AND CONTINGENT ASSETS. 2017.

[Online]. Available through<https://www.safaribooksonline.com/library/view/ifrs-

essentials/9781118501344/OEBPS/9781118501344_epub_c_26.htm> [Accessed on 4th

October 2017].

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.