Sheffield Business School: International Audit and Assurance Report

VerifiedAdded on 2023/01/12

|14

|3741

|32

Report

AI Summary

This report provides a comprehensive international audit and assurance analysis of GR8 Hols Ltd's financial statements. It critically evaluates the director's reasoning for a provision, addresses concerns about business risk through an explanatory email, and identifies eight inherent risks associated with the financial statements, explaining their impact. The report also examines audit concerns related to reported income figures and other financial information, including the impact of a new system introduction. Furthermore, it offers advice on potential acquisitions, employment of key personnel, and future audit practices, concluding with a detailed overview of the audit process and its findings.

International Audit

and Assurance

and Assurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Critical evaluation of director’s reasoning for including a provision of 20000 pounds in the

financial statements of GR8 Hols Limited..................................................................................1

PART B...........................................................................................................................................2

Content of an explanatory email to Sabrina in which all the concerns about firm’s interest in

business risk will be critically addressed.....................................................................................2

PART C...........................................................................................................................................3

Identification of EIGHT inherent risks associated with the financial statements of the

organisation along with explanation of impact of each one of them...........................................3

PART D...........................................................................................................................................4

1. Explanation of any audit concerns which are related to the reported income figures for

caravan, tent and pitch hire including occupancy rate.................................................................4

2. Explanation of other audit risks that are related to the EIGHT other areas of the reported

financial information...................................................................................................................5

PART E............................................................................................................................................5

Effect of the introduction of new system on 1st February 2019 should have upon firm’s

approach.......................................................................................................................................5

PART F............................................................................................................................................6

1. Advice in assisting GR8 Hols Ltd in the possible purchase of the Campies Ltd site..............6

2. Advice in the employment of the sire accountant currently engaged by Campies Ltd as

suggested by Reeves....................................................................................................................6

3. Advice to carry out future end of year non-current assets and inventory counts as requested

by Reeves.....................................................................................................................................6

CONCLUSION................................................................................................................................7

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Critical evaluation of director’s reasoning for including a provision of 20000 pounds in the

financial statements of GR8 Hols Limited..................................................................................1

PART B...........................................................................................................................................2

Content of an explanatory email to Sabrina in which all the concerns about firm’s interest in

business risk will be critically addressed.....................................................................................2

PART C...........................................................................................................................................3

Identification of EIGHT inherent risks associated with the financial statements of the

organisation along with explanation of impact of each one of them...........................................3

PART D...........................................................................................................................................4

1. Explanation of any audit concerns which are related to the reported income figures for

caravan, tent and pitch hire including occupancy rate.................................................................4

2. Explanation of other audit risks that are related to the EIGHT other areas of the reported

financial information...................................................................................................................5

PART E............................................................................................................................................5

Effect of the introduction of new system on 1st February 2019 should have upon firm’s

approach.......................................................................................................................................5

PART F............................................................................................................................................6

1. Advice in assisting GR8 Hols Ltd in the possible purchase of the Campies Ltd site..............6

2. Advice in the employment of the sire accountant currently engaged by Campies Ltd as

suggested by Reeves....................................................................................................................6

3. Advice to carry out future end of year non-current assets and inventory counts as requested

by Reeves.....................................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

International Audit can be defined as the process of analysing each and every element of

final accounts of an organisation so that it could be determined that it is performing well or not.

It is mainly focused by such entities that are operating business at international level. In order to

assure that all the detailed data which is mentioned in financial statements is appropriate and

accurate or not all the entities are required to follow guidelines of IAASB (International audit

and assurance, 2020). International Auditing and Assurance Standards Board is a legal body that

guides all the global entities to form all the final account in transparent and relevant manner.

Present report is based upon GR8 Hols Limited which was founded in year 1992 by Mary and

John Cougar. Now the entity is planning to expand the business in Scotland and North of

England for which the directors asked an auditing firm to advice upon different key areas. The

topics that are covered in this assignment are reasoning for including a provision, concern

regarding firm’s interest in business risk, identification of EIGHT inherent risks associated with

the financial statements, different audit concerns etc. Additionally, effect on the introduction of

the new system along with advices with rationale upon different areas are also covered in this

project.

PART A

Critical evaluation of director’s reasoning for including a provision of 20000 pounds in the

financial statements of GR8 Hols Limited

Leakage have been identified in the underground drainage pipes on the camp sides. The

Directors of GR8 Hols Ltd have claimed that it is the mistake of contractors because if they had

used large firm for drainage then this problem would not have taken place. The whole loss which

will take place due this damage is not covered by insurance. In this situation another firm of

contractors was contacted and they agreed with a sum of 120000 pounds and confirmed it in a

formal report. In this situation the entity kept 20000 pounds in the final account as provision for

the river authority claim. It is the highest amount of provision which is made by the company.

The amount which is kept by the organisation is not appropriate as it is very low as compared to

the total value of the damage which is 120000 pounds. The organisation should provide

alternative amount so that appropriate claim to the local river authority could be provided.

Director’s responsibility is to make sure that they are able to find the right solution for the

1

International Audit can be defined as the process of analysing each and every element of

final accounts of an organisation so that it could be determined that it is performing well or not.

It is mainly focused by such entities that are operating business at international level. In order to

assure that all the detailed data which is mentioned in financial statements is appropriate and

accurate or not all the entities are required to follow guidelines of IAASB (International audit

and assurance, 2020). International Auditing and Assurance Standards Board is a legal body that

guides all the global entities to form all the final account in transparent and relevant manner.

Present report is based upon GR8 Hols Limited which was founded in year 1992 by Mary and

John Cougar. Now the entity is planning to expand the business in Scotland and North of

England for which the directors asked an auditing firm to advice upon different key areas. The

topics that are covered in this assignment are reasoning for including a provision, concern

regarding firm’s interest in business risk, identification of EIGHT inherent risks associated with

the financial statements, different audit concerns etc. Additionally, effect on the introduction of

the new system along with advices with rationale upon different areas are also covered in this

project.

PART A

Critical evaluation of director’s reasoning for including a provision of 20000 pounds in the

financial statements of GR8 Hols Limited

Leakage have been identified in the underground drainage pipes on the camp sides. The

Directors of GR8 Hols Ltd have claimed that it is the mistake of contractors because if they had

used large firm for drainage then this problem would not have taken place. The whole loss which

will take place due this damage is not covered by insurance. In this situation another firm of

contractors was contacted and they agreed with a sum of 120000 pounds and confirmed it in a

formal report. In this situation the entity kept 20000 pounds in the final account as provision for

the river authority claim. It is the highest amount of provision which is made by the company.

The amount which is kept by the organisation is not appropriate as it is very low as compared to

the total value of the damage which is 120000 pounds. The organisation should provide

alternative amount so that appropriate claim to the local river authority could be provided.

Director’s responsibility is to make sure that they are able to find the right solution for the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mistakes that are made by the enterprise. The provision of 20000 pounds very beneficial as it can

help to deal with all the uncertainties that are faced by the entity. There is no materiality in level

of provision so it will not be recorded.

PART B

Content of an explanatory email to Sabrina in which all the concerns about firm’s interest in

business risk will be critically addressed

Business risks are the set of various types of negative situations that may take place in

future. These are linked with audit risks as all of them will leave impact upon position of

company and its internal records which will create the issue of audit risk. It is very important for

auditors to understand the business risk as it is essential for them to make sure that they are

prepared to deal with all the unfavourable situations which may take place in future. According

to international standard on auditing 315 business risks result from significant conditions,

circumstances and events of business operations. While planning to conduct the auditing process

systematically it is very important for all the businesses to analyse the business risks as it is very

important to make accurate reports. Business risk identification is a part of audit process as it is

required to formulate the auditing records. There are various types of business risks that are

associated with GR8 Hols Limited. One of them is related with recruitment policy because the

entity is not having skilled employees and it is one of the biggest risks. There are various other

risks that are associated with the organisation all of them could be understood with the help of

following discussion:

Recruitment policy: It is one of the main business risks which may result in lower

profits and bad market image in the market. As the company have planned to recruit small

number of permanent staffs for the sites but in order to execute all the planned activities properly

it is not possible to perform them with small number of individuals. The number of temporary

workers is more than 200 and if they leave job suddenly then it will be a huge risk for the

business.

Mitigation: In order to mitigate this risk, the enterprise is required to hire more

permanent staff members reduce the number of temporary one. It will help to deal with all the

difficult situations that could be faced by the organisation in future (Denisov, Khachaturyan and

2

help to deal with all the uncertainties that are faced by the entity. There is no materiality in level

of provision so it will not be recorded.

PART B

Content of an explanatory email to Sabrina in which all the concerns about firm’s interest in

business risk will be critically addressed

Business risks are the set of various types of negative situations that may take place in

future. These are linked with audit risks as all of them will leave impact upon position of

company and its internal records which will create the issue of audit risk. It is very important for

auditors to understand the business risk as it is essential for them to make sure that they are

prepared to deal with all the unfavourable situations which may take place in future. According

to international standard on auditing 315 business risks result from significant conditions,

circumstances and events of business operations. While planning to conduct the auditing process

systematically it is very important for all the businesses to analyse the business risks as it is very

important to make accurate reports. Business risk identification is a part of audit process as it is

required to formulate the auditing records. There are various types of business risks that are

associated with GR8 Hols Limited. One of them is related with recruitment policy because the

entity is not having skilled employees and it is one of the biggest risks. There are various other

risks that are associated with the organisation all of them could be understood with the help of

following discussion:

Recruitment policy: It is one of the main business risks which may result in lower

profits and bad market image in the market. As the company have planned to recruit small

number of permanent staffs for the sites but in order to execute all the planned activities properly

it is not possible to perform them with small number of individuals. The number of temporary

workers is more than 200 and if they leave job suddenly then it will be a huge risk for the

business.

Mitigation: In order to mitigate this risk, the enterprise is required to hire more

permanent staff members reduce the number of temporary one. It will help to deal with all the

difficult situations that could be faced by the organisation in future (Denisov, Khachaturyan and

2

Umnova, 2018). The auditors will have to analyse the final reports after the mitigation so that

performance of business could be analysed.

Advanced accounting system: The accounting system which is being replaced by the

company recently is very advanced and improved. The staff members who are currently working

within the entity are not able to work with it as they are not having experience of working on this

software. They need proper training to work on this or an experienced individual is required to

be hired who is having knowledge of working on it. If appropriate steps will not be taken by the

organisation then it will impact the whole organisation negatively.

Mitigation: In order to mitigate this risk appropriate training for old staff or new

accountants having knowledge of advanced software should be recruited. The auditors will be

obligated to use the new accounting systems with proper training which will help them to

generate accurate reports.

Waste in the local river: In the may month of year 2019 sewage waste of one of the sites

of the organisation was leaked in the river which resulted in water contamination. It may result in

legal actions for the entity because it is harming water of the river.

Mitigation: In order to mitigate this risk, the enterprise should make arrangements to

handle the leakage which is created by it (Farooq and De Villiers, 2019). The expenses which

will take place after taking the step of mitigation of this risk the auditor will be obligated to

analyse their impact upon the reports.

All the above described risks should be taken in to consideration by the directors of GR8

Hols Ltd as it can help to reduce the possibility of them. On the other hand, the steps to mitigate

them should also be taken as it will help to avoid their negative impact upon the business

processes.

PART C

Identification of EIGHT inherent risks associated with the financial statements of the

organisation along with explanation of impact of each one of them

All the EIGHT risks that are associated with the financial statements of the organisation

along with their impact upon the business could be understood with the help of following table:

Name of

risk

Nature

of risk

Area of financial

statement

Audit concern

3

performance of business could be analysed.

Advanced accounting system: The accounting system which is being replaced by the

company recently is very advanced and improved. The staff members who are currently working

within the entity are not able to work with it as they are not having experience of working on this

software. They need proper training to work on this or an experienced individual is required to

be hired who is having knowledge of working on it. If appropriate steps will not be taken by the

organisation then it will impact the whole organisation negatively.

Mitigation: In order to mitigate this risk appropriate training for old staff or new

accountants having knowledge of advanced software should be recruited. The auditors will be

obligated to use the new accounting systems with proper training which will help them to

generate accurate reports.

Waste in the local river: In the may month of year 2019 sewage waste of one of the sites

of the organisation was leaked in the river which resulted in water contamination. It may result in

legal actions for the entity because it is harming water of the river.

Mitigation: In order to mitigate this risk, the enterprise should make arrangements to

handle the leakage which is created by it (Farooq and De Villiers, 2019). The expenses which

will take place after taking the step of mitigation of this risk the auditor will be obligated to

analyse their impact upon the reports.

All the above described risks should be taken in to consideration by the directors of GR8

Hols Ltd as it can help to reduce the possibility of them. On the other hand, the steps to mitigate

them should also be taken as it will help to avoid their negative impact upon the business

processes.

PART C

Identification of EIGHT inherent risks associated with the financial statements of the

organisation along with explanation of impact of each one of them

All the EIGHT risks that are associated with the financial statements of the organisation

along with their impact upon the business could be understood with the help of following table:

Name of

risk

Nature

of risk

Area of financial

statement

Audit concern

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

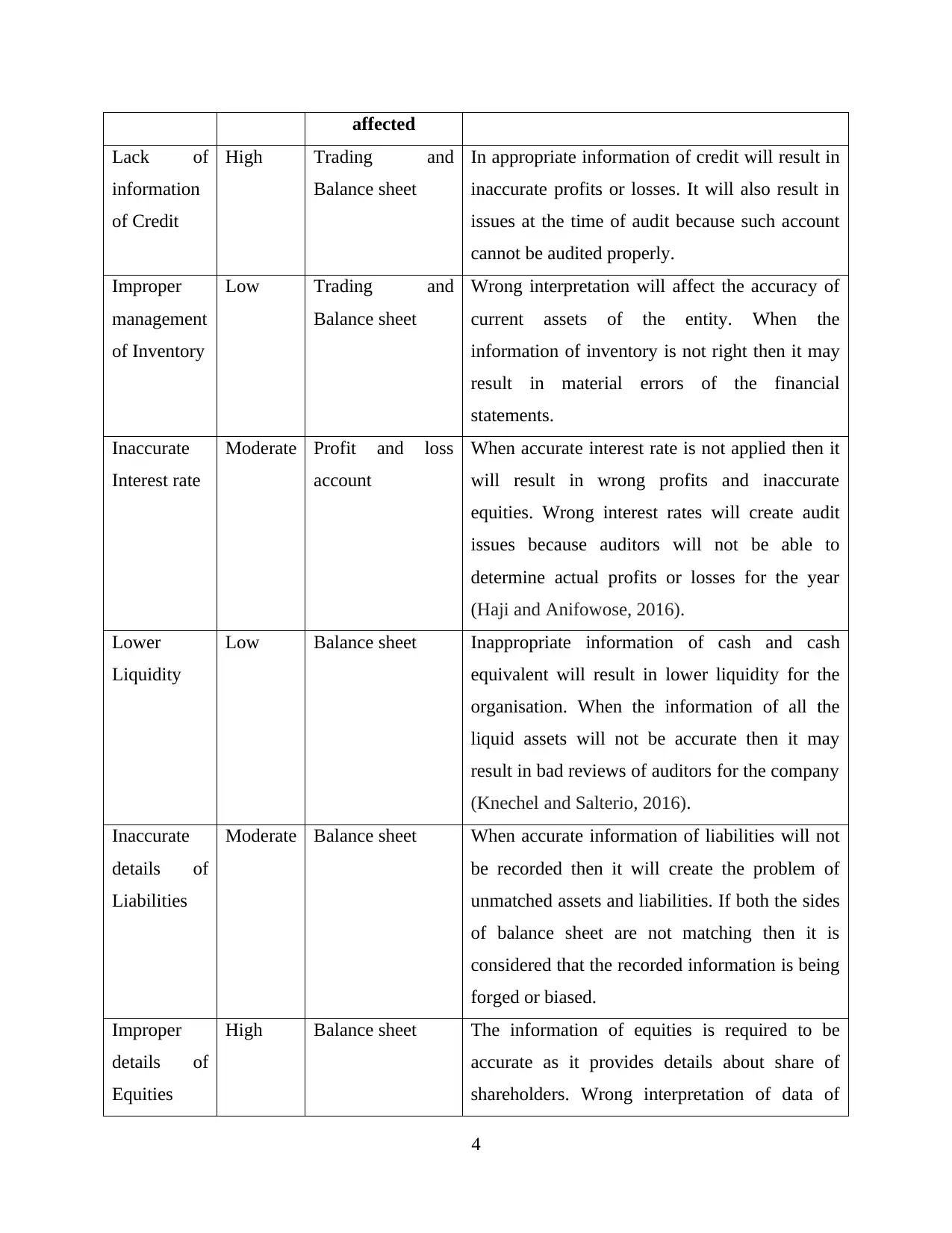

affected

Lack of

information

of Credit

High Trading and

Balance sheet

In appropriate information of credit will result in

inaccurate profits or losses. It will also result in

issues at the time of audit because such account

cannot be audited properly.

Improper

management

of Inventory

Low Trading and

Balance sheet

Wrong interpretation will affect the accuracy of

current assets of the entity. When the

information of inventory is not right then it may

result in material errors of the financial

statements.

Inaccurate

Interest rate

Moderate Profit and loss

account

When accurate interest rate is not applied then it

will result in wrong profits and inaccurate

equities. Wrong interest rates will create audit

issues because auditors will not be able to

determine actual profits or losses for the year

(Haji and Anifowose, 2016).

Lower

Liquidity

Low Balance sheet Inappropriate information of cash and cash

equivalent will result in lower liquidity for the

organisation. When the information of all the

liquid assets will not be accurate then it may

result in bad reviews of auditors for the company

(Knechel and Salterio, 2016).

Inaccurate

details of

Liabilities

Moderate Balance sheet When accurate information of liabilities will not

be recorded then it will create the problem of

unmatched assets and liabilities. If both the sides

of balance sheet are not matching then it is

considered that the recorded information is being

forged or biased.

Improper

details of

Equities

High Balance sheet The information of equities is required to be

accurate as it provides details about share of

shareholders. Wrong interpretation of data of

4

Lack of

information

of Credit

High Trading and

Balance sheet

In appropriate information of credit will result in

inaccurate profits or losses. It will also result in

issues at the time of audit because such account

cannot be audited properly.

Improper

management

of Inventory

Low Trading and

Balance sheet

Wrong interpretation will affect the accuracy of

current assets of the entity. When the

information of inventory is not right then it may

result in material errors of the financial

statements.

Inaccurate

Interest rate

Moderate Profit and loss

account

When accurate interest rate is not applied then it

will result in wrong profits and inaccurate

equities. Wrong interest rates will create audit

issues because auditors will not be able to

determine actual profits or losses for the year

(Haji and Anifowose, 2016).

Lower

Liquidity

Low Balance sheet Inappropriate information of cash and cash

equivalent will result in lower liquidity for the

organisation. When the information of all the

liquid assets will not be accurate then it may

result in bad reviews of auditors for the company

(Knechel and Salterio, 2016).

Inaccurate

details of

Liabilities

Moderate Balance sheet When accurate information of liabilities will not

be recorded then it will create the problem of

unmatched assets and liabilities. If both the sides

of balance sheet are not matching then it is

considered that the recorded information is being

forged or biased.

Improper

details of

Equities

High Balance sheet The information of equities is required to be

accurate as it provides details about share of

shareholders. Wrong interpretation of data of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

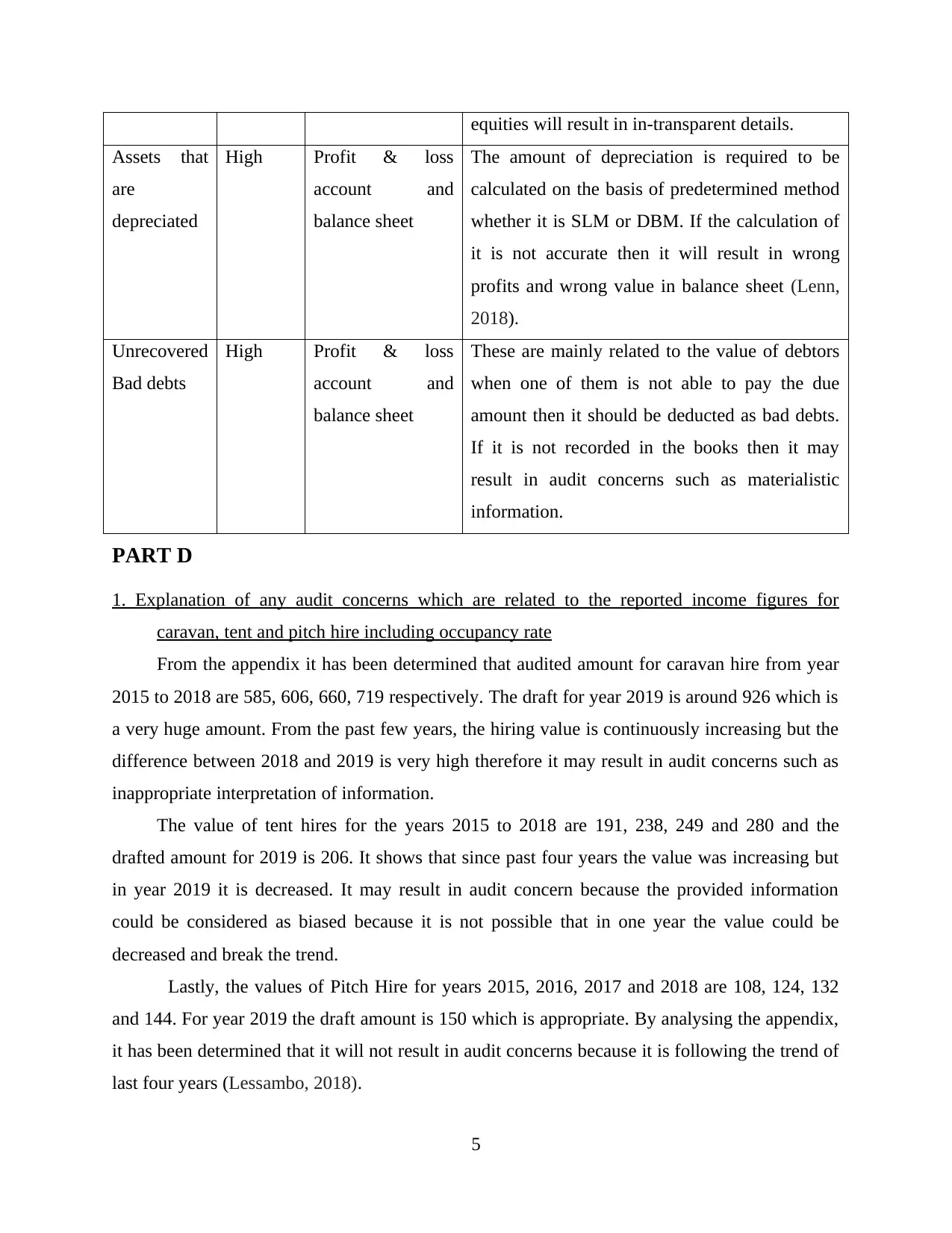

equities will result in in-transparent details.

Assets that

are

depreciated

High Profit & loss

account and

balance sheet

The amount of depreciation is required to be

calculated on the basis of predetermined method

whether it is SLM or DBM. If the calculation of

it is not accurate then it will result in wrong

profits and wrong value in balance sheet (Lenn,

2018).

Unrecovered

Bad debts

High Profit & loss

account and

balance sheet

These are mainly related to the value of debtors

when one of them is not able to pay the due

amount then it should be deducted as bad debts.

If it is not recorded in the books then it may

result in audit concerns such as materialistic

information.

PART D

1. Explanation of any audit concerns which are related to the reported income figures for

caravan, tent and pitch hire including occupancy rate

From the appendix it has been determined that audited amount for caravan hire from year

2015 to 2018 are 585, 606, 660, 719 respectively. The draft for year 2019 is around 926 which is

a very huge amount. From the past few years, the hiring value is continuously increasing but the

difference between 2018 and 2019 is very high therefore it may result in audit concerns such as

inappropriate interpretation of information.

The value of tent hires for the years 2015 to 2018 are 191, 238, 249 and 280 and the

drafted amount for 2019 is 206. It shows that since past four years the value was increasing but

in year 2019 it is decreased. It may result in audit concern because the provided information

could be considered as biased because it is not possible that in one year the value could be

decreased and break the trend.

Lastly, the values of Pitch Hire for years 2015, 2016, 2017 and 2018 are 108, 124, 132

and 144. For year 2019 the draft amount is 150 which is appropriate. By analysing the appendix,

it has been determined that it will not result in audit concerns because it is following the trend of

last four years (Lessambo, 2018).

5

Assets that

are

depreciated

High Profit & loss

account and

balance sheet

The amount of depreciation is required to be

calculated on the basis of predetermined method

whether it is SLM or DBM. If the calculation of

it is not accurate then it will result in wrong

profits and wrong value in balance sheet (Lenn,

2018).

Unrecovered

Bad debts

High Profit & loss

account and

balance sheet

These are mainly related to the value of debtors

when one of them is not able to pay the due

amount then it should be deducted as bad debts.

If it is not recorded in the books then it may

result in audit concerns such as materialistic

information.

PART D

1. Explanation of any audit concerns which are related to the reported income figures for

caravan, tent and pitch hire including occupancy rate

From the appendix it has been determined that audited amount for caravan hire from year

2015 to 2018 are 585, 606, 660, 719 respectively. The draft for year 2019 is around 926 which is

a very huge amount. From the past few years, the hiring value is continuously increasing but the

difference between 2018 and 2019 is very high therefore it may result in audit concerns such as

inappropriate interpretation of information.

The value of tent hires for the years 2015 to 2018 are 191, 238, 249 and 280 and the

drafted amount for 2019 is 206. It shows that since past four years the value was increasing but

in year 2019 it is decreased. It may result in audit concern because the provided information

could be considered as biased because it is not possible that in one year the value could be

decreased and break the trend.

Lastly, the values of Pitch Hire for years 2015, 2016, 2017 and 2018 are 108, 124, 132

and 144. For year 2019 the draft amount is 150 which is appropriate. By analysing the appendix,

it has been determined that it will not result in audit concerns because it is following the trend of

last four years (Lessambo, 2018).

5

Note: All the figures in above discussion are taken from the appendix.

2. Explanation of other audit risks that are related to the EIGHT other areas of the reported

financial information

There are various inherent risks that are associated with the financial statements of GR8

Hols Limited. All of them are credit, liquidity, inventory, liabilities, equities, interest rates, bad

debts and assets that are depreciated. All of them are focused by the entity so that possibility of

audit risks that may take place due to them could be reduced. There are several other areas that

may also create audit concerns for the organisation. One of them is repair and maintenance. If the

management is not able to record accurate amount of it or they are recording the unnecessary

information of it in financial statements then it will result in audit concern. For example, if the

value of repair is 400 pounds and 600 pounds are recorded in the books without any proof then

auditor will declare the statements in accurate. Another area of risk that may result in audit

concern is insurance of assets. Insurance premium is paid on yearly, half yearly, quarterly or

monthly basis. If the value of it which is recorded in the books is not accurate then it will result

in material misstatement of final account that may also result in strict action of auditor (Mock,

Ragothaman and Srivastava, 2018).

PART E

Effect of the introduction of new system on 1st February 2019 should have upon firm’s approach

GR8 Hols Limited planned to replace its old accounting system with a new and advanced

version from 1st February 2019. It will be used on parallel basis with the old one in three months

period. It is highly advanced, tailor made and designed for the organisation. According to the

director Sabina is an improved and highly advanced version of the old accounting system. It will

handle the transactions in more quick manner. The level of reliability of it is very high and by

using it the organisation will be able to keep detailed information of all the transactions that will

be made by it in upcoming period. This new system will be beneficial for the organisation and

also leave positive impact upon the approach of the company as the difficult tasks could be

performed easily with the help of it.

Issues and concerns: The main concern which is required to be focused by Sabina as a

director is lack of knowledge to the old staff regarding use of it. In order to take proper

advantage of it the organisation is required to hire some experienced employees so that they can

6

2. Explanation of other audit risks that are related to the EIGHT other areas of the reported

financial information

There are various inherent risks that are associated with the financial statements of GR8

Hols Limited. All of them are credit, liquidity, inventory, liabilities, equities, interest rates, bad

debts and assets that are depreciated. All of them are focused by the entity so that possibility of

audit risks that may take place due to them could be reduced. There are several other areas that

may also create audit concerns for the organisation. One of them is repair and maintenance. If the

management is not able to record accurate amount of it or they are recording the unnecessary

information of it in financial statements then it will result in audit concern. For example, if the

value of repair is 400 pounds and 600 pounds are recorded in the books without any proof then

auditor will declare the statements in accurate. Another area of risk that may result in audit

concern is insurance of assets. Insurance premium is paid on yearly, half yearly, quarterly or

monthly basis. If the value of it which is recorded in the books is not accurate then it will result

in material misstatement of final account that may also result in strict action of auditor (Mock,

Ragothaman and Srivastava, 2018).

PART E

Effect of the introduction of new system on 1st February 2019 should have upon firm’s approach

GR8 Hols Limited planned to replace its old accounting system with a new and advanced

version from 1st February 2019. It will be used on parallel basis with the old one in three months

period. It is highly advanced, tailor made and designed for the organisation. According to the

director Sabina is an improved and highly advanced version of the old accounting system. It will

handle the transactions in more quick manner. The level of reliability of it is very high and by

using it the organisation will be able to keep detailed information of all the transactions that will

be made by it in upcoming period. This new system will be beneficial for the organisation and

also leave positive impact upon the approach of the company as the difficult tasks could be

performed easily with the help of it.

Issues and concerns: The main concern which is required to be focused by Sabina as a

director is lack of knowledge to the old staff regarding use of it. In order to take proper

advantage of it the organisation is required to hire some experienced employees so that they can

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

training the existing ones about the way in which it is used. Without hiring experienced

individuals, it will be impossible to take advantage of the new, improved and advanced

accounting system (Simnett, Carson and Vanstraelen, 2016).

PART F

1. Advice in assisting GR8 Hols Ltd in the possible purchase of the Campies Ltd site

GR8 Hols Ltd was approached by the director of Campies Ltd to buy its sites that it is

willing to sell. It has been advised to Sabina that the sites should be bought as it will help to

expand the business in local area and reduce the competition. If the sites of the entity will be

purchased then there will a large area which will be covered by GR8 Hols to perform all its

operational activities. The decision of purchasing it will result positively for the entity as it will

provide it a large platform to operate business activities (Soh and Martinov‐Bennie, 2018). It is

suggested to the auditors to have detailed information of code of ethics for professional

accountants. It will help to respond to all the issues that could eb faced by them while recording

information of new machine purchased by the enterprise.

2. Advice in the employment of the accountant currently engaged by Campies Ltd as suggested

by Reeves

Reeves suggested that the accountant who is currently working in Campies Ltd should be

employed by GR8 Hols Limited as he is having experience of working at sites and having

detailed information about the camp sites. Sabina is suggested that the accountant of the

organisation should be employed by her as the experience of working and past experience of

accountant will be beneficial for the organisation. It will reduce the load of the enterprise to hire

a new individual who can handle all the details of new sites that will be bought by it.

3. Advice to carry out future end of year non-current assets and inventory counts as requested by

Reeves

The last request that are made by Reeves was related to the carry out no-current assets and

inventory’s count so that the goal of firm of reducing the overhead expenses should be reduced.

Sabina is advised that these non-current assets and inventory should not be counted because it

will increase the work load of staff members and may also result in lower productivity of them.

As Campies Ltd’s sites will be bought by GR8 Hols Limited so the employees who are currently

working within the entity will have more responsibilities. In case of counting the inventory and

7

individuals, it will be impossible to take advantage of the new, improved and advanced

accounting system (Simnett, Carson and Vanstraelen, 2016).

PART F

1. Advice in assisting GR8 Hols Ltd in the possible purchase of the Campies Ltd site

GR8 Hols Ltd was approached by the director of Campies Ltd to buy its sites that it is

willing to sell. It has been advised to Sabina that the sites should be bought as it will help to

expand the business in local area and reduce the competition. If the sites of the entity will be

purchased then there will a large area which will be covered by GR8 Hols to perform all its

operational activities. The decision of purchasing it will result positively for the entity as it will

provide it a large platform to operate business activities (Soh and Martinov‐Bennie, 2018). It is

suggested to the auditors to have detailed information of code of ethics for professional

accountants. It will help to respond to all the issues that could eb faced by them while recording

information of new machine purchased by the enterprise.

2. Advice in the employment of the accountant currently engaged by Campies Ltd as suggested

by Reeves

Reeves suggested that the accountant who is currently working in Campies Ltd should be

employed by GR8 Hols Limited as he is having experience of working at sites and having

detailed information about the camp sites. Sabina is suggested that the accountant of the

organisation should be employed by her as the experience of working and past experience of

accountant will be beneficial for the organisation. It will reduce the load of the enterprise to hire

a new individual who can handle all the details of new sites that will be bought by it.

3. Advice to carry out future end of year non-current assets and inventory counts as requested by

Reeves

The last request that are made by Reeves was related to the carry out no-current assets and

inventory’s count so that the goal of firm of reducing the overhead expenses should be reduced.

Sabina is advised that these non-current assets and inventory should not be counted because it

will increase the work load of staff members and may also result in lower productivity of them.

As Campies Ltd’s sites will be bought by GR8 Hols Limited so the employees who are currently

working within the entity will have more responsibilities. In case of counting the inventory and

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

non-current assets their work load will be at a higher level which may affect the work quality of

them. It is the main reason for providing this advice to Sabina (Barr-Pulliam, Brown-Liburd and

Sanderson, 2017).

CONCLUSION

From the above project report it has been concluded that audit and assurance are two main

elements that are required to be focused by all the organisations so that they can perform all the

operation properly. In order to determine the audit concerns that may take place in future all the

companies are required to analyse the business risks such as recruitment policy, unexperienced

staff etc. There are various inherent risks that should also be focused by organisations to

determine audit related difficulties that may take place in future. Some of them are credit,

liquidity, assets, liabilities, equities, insurance, etc. While taking any decision for betterment of

business in future it is very important for all the organisations to make sure that they are

analysing each and every factor properly.

8

them. It is the main reason for providing this advice to Sabina (Barr-Pulliam, Brown-Liburd and

Sanderson, 2017).

CONCLUSION

From the above project report it has been concluded that audit and assurance are two main

elements that are required to be focused by all the organisations so that they can perform all the

operation properly. In order to determine the audit concerns that may take place in future all the

companies are required to analyse the business risks such as recruitment policy, unexperienced

staff etc. There are various inherent risks that should also be focused by organisations to

determine audit related difficulties that may take place in future. Some of them are credit,

liquidity, assets, liabilities, equities, insurance, etc. While taking any decision for betterment of

business in future it is very important for all the organisations to make sure that they are

analysing each and every factor properly.

8

REFERENCES

Books and Journals:

Barr-Pulliam, D., Brown-Liburd, H. L. and Sanderson, K. A., 2017. The Effects of the Internal

Control Opinion and Use of Audit Data Analytics on Perceptions of Audit Quality,

Assurance, and Auditor Negligence. Assurance, and Auditor Negligence (August 17.

2017).

Denisov, I. V., Khachaturyan, M. V. and Umnova, M. G., 2018. Corporate social responsibility

in Russian companies: Introduction of social audit as assurance of

quality. Calitatea. 19(164). pp.63-73.

Farooq, M. B. and De Villiers, C., 2019. Sustainability assurance: Who are the assurance

providers and what do they do?. In Challenges in Managing Sustainable Business (pp.

137-154). Palgrave Macmillan, Cham.

Haji, A. A. and Anifowose, M., 2016. Audit committee and integrated reporting practice: does

internal assurance matter?. Managerial Auditing Journal.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Lenn, M. P., 2018. International linkages and quality assurance: a shifting paradigm.

In International Developments in Assuring Quality in Higher Education (pp. 127-133).

Routledge.

Lessambo, F. I., 2018. The International Auditing and Assurance Standards Board. In Auditing,

Assurance Services, and Forensics (pp. 35-39). Palgrave Macmillan, Cham.

Mock, T. J., Ragothaman, S. C. and Srivastava, R. P., 2018. Using Evidential Reasoning

Technology to Enhance the Audit Quality Assurance Inspection Process. Journal of

Emerging Technologies in Accounting. 15(1). pp.29-43.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory. 35(3). pp.1-32.

Soh, D. S. and Martinov‐Bennie, N., 2018. Factors associated with internal audit's involvement

in environmental and social assurance and consulting. International Journal of Auditing.

22(3). pp.404-421.

Online

International audit and assurance. 2020. [Online]. Available through:

< https://www.iaasb.org/>

9

Books and Journals:

Barr-Pulliam, D., Brown-Liburd, H. L. and Sanderson, K. A., 2017. The Effects of the Internal

Control Opinion and Use of Audit Data Analytics on Perceptions of Audit Quality,

Assurance, and Auditor Negligence. Assurance, and Auditor Negligence (August 17.

2017).

Denisov, I. V., Khachaturyan, M. V. and Umnova, M. G., 2018. Corporate social responsibility

in Russian companies: Introduction of social audit as assurance of

quality. Calitatea. 19(164). pp.63-73.

Farooq, M. B. and De Villiers, C., 2019. Sustainability assurance: Who are the assurance

providers and what do they do?. In Challenges in Managing Sustainable Business (pp.

137-154). Palgrave Macmillan, Cham.

Haji, A. A. and Anifowose, M., 2016. Audit committee and integrated reporting practice: does

internal assurance matter?. Managerial Auditing Journal.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Lenn, M. P., 2018. International linkages and quality assurance: a shifting paradigm.

In International Developments in Assuring Quality in Higher Education (pp. 127-133).

Routledge.

Lessambo, F. I., 2018. The International Auditing and Assurance Standards Board. In Auditing,

Assurance Services, and Forensics (pp. 35-39). Palgrave Macmillan, Cham.

Mock, T. J., Ragothaman, S. C. and Srivastava, R. P., 2018. Using Evidential Reasoning

Technology to Enhance the Audit Quality Assurance Inspection Process. Journal of

Emerging Technologies in Accounting. 15(1). pp.29-43.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory. 35(3). pp.1-32.

Soh, D. S. and Martinov‐Bennie, N., 2018. Factors associated with internal audit's involvement

in environmental and social assurance and consulting. International Journal of Auditing.

22(3). pp.404-421.

Online

International audit and assurance. 2020. [Online]. Available through:

< https://www.iaasb.org/>

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.