Comprehensive Report: BilT International Business Finance

VerifiedAdded on 2020/05/11

|22

|5440

|63

Report

AI Summary

This report provides a comprehensive analysis of BilT, an Australian body care product company, and its international finance strategy for entering the Argentine market. The report examines the company's annual cash flow projections over five years, considering factors such as sales, costs, and inflation. It also delves into hedging strategies to mitigate currency exchange risks and assesses the impact of different borrowing rates in Argentina and Australia on the company's net present value (NPV). The report further explores the cost of equity using the Capital Asset Pricing Model (CAPM) and discusses the effects of global currency and financial crises on BilT's operations. The analysis includes detailed tables and figures illustrating cash flow, hedging effectiveness, and NPV calculations, providing insights into the financial viability of BilT's international expansion plans.

Running Header: International business finance

1

INTERNATIONAL BUSINESS FINANCE

1

INTERNATIONAL BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International business finance

2

Executive Summary

The report has primarily emphasized upon BilT, which is an Australian organization that is into

the business of producing body care products. While having produced a new sunscreen, it had

aimed to capture the Argentine market, which it thinks to be promising as well as prosperous.

Therefore, the report has developed the statement for the annual cash flow of the company in

order to determine its impacts in the market for the upcoming five fiscal years. Moreover, the

report has also determined the risk associated to the exchange in the currency structure, from

conducting the trade in Australia to that in Argentina. The risk is being managed by means of

hedging, and therefore, the strategies for various forward rates are being estimated.

The report also determines the net present value for the company; both in the Argentine as well

as the Australian context, when it considers the initial investment to be split off against different

rates of borrow. Finally, the report discusses the cost of equity based on the CAPM, and the

impacts of the currency and other financial crises on the company’s trade.

2

Executive Summary

The report has primarily emphasized upon BilT, which is an Australian organization that is into

the business of producing body care products. While having produced a new sunscreen, it had

aimed to capture the Argentine market, which it thinks to be promising as well as prosperous.

Therefore, the report has developed the statement for the annual cash flow of the company in

order to determine its impacts in the market for the upcoming five fiscal years. Moreover, the

report has also determined the risk associated to the exchange in the currency structure, from

conducting the trade in Australia to that in Argentina. The risk is being managed by means of

hedging, and therefore, the strategies for various forward rates are being estimated.

The report also determines the net present value for the company; both in the Argentine as well

as the Australian context, when it considers the initial investment to be split off against different

rates of borrow. Finally, the report discusses the cost of equity based on the CAPM, and the

impacts of the currency and other financial crises on the company’s trade.

International business finance

3

Table of Contents

Introduction......................................................................................................................................5

Findings and discussions.................................................................................................................5

a. General annual cash flow.............................................................................................................5

b. Hedging and cash flow................................................................................................................8

c. Difference in borrow..................................................................................................................11

d. Cost of Equity............................................................................................................................12

e. Effect of global crisis.................................................................................................................15

Conclusion.....................................................................................................................................18

Reference List................................................................................................................................19

3

Table of Contents

Introduction......................................................................................................................................5

Findings and discussions.................................................................................................................5

a. General annual cash flow.............................................................................................................5

b. Hedging and cash flow................................................................................................................8

c. Difference in borrow..................................................................................................................11

d. Cost of Equity............................................................................................................................12

e. Effect of global crisis.................................................................................................................15

Conclusion.....................................................................................................................................18

Reference List................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International business finance

4

List of Figures

Figure 1: Cumulative cash flow for BilT.........................................................................................8

Figure 2: Cumulative hedged NPV for BilT..................................................................................10

Figure 3: Factors affecting Cost of equity.....................................................................................13

Figure 4: Estimation of risk free rate.............................................................................................14

Figure 5: Effect of global banking crises.......................................................................................15

Figure 6: Effect of global currency crises (1980-1998).................................................................16

4

List of Figures

Figure 1: Cumulative cash flow for BilT.........................................................................................8

Figure 2: Cumulative hedged NPV for BilT..................................................................................10

Figure 3: Factors affecting Cost of equity.....................................................................................13

Figure 4: Estimation of risk free rate.............................................................................................14

Figure 5: Effect of global banking crises.......................................................................................15

Figure 6: Effect of global currency crises (1980-1998).................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International business finance

5

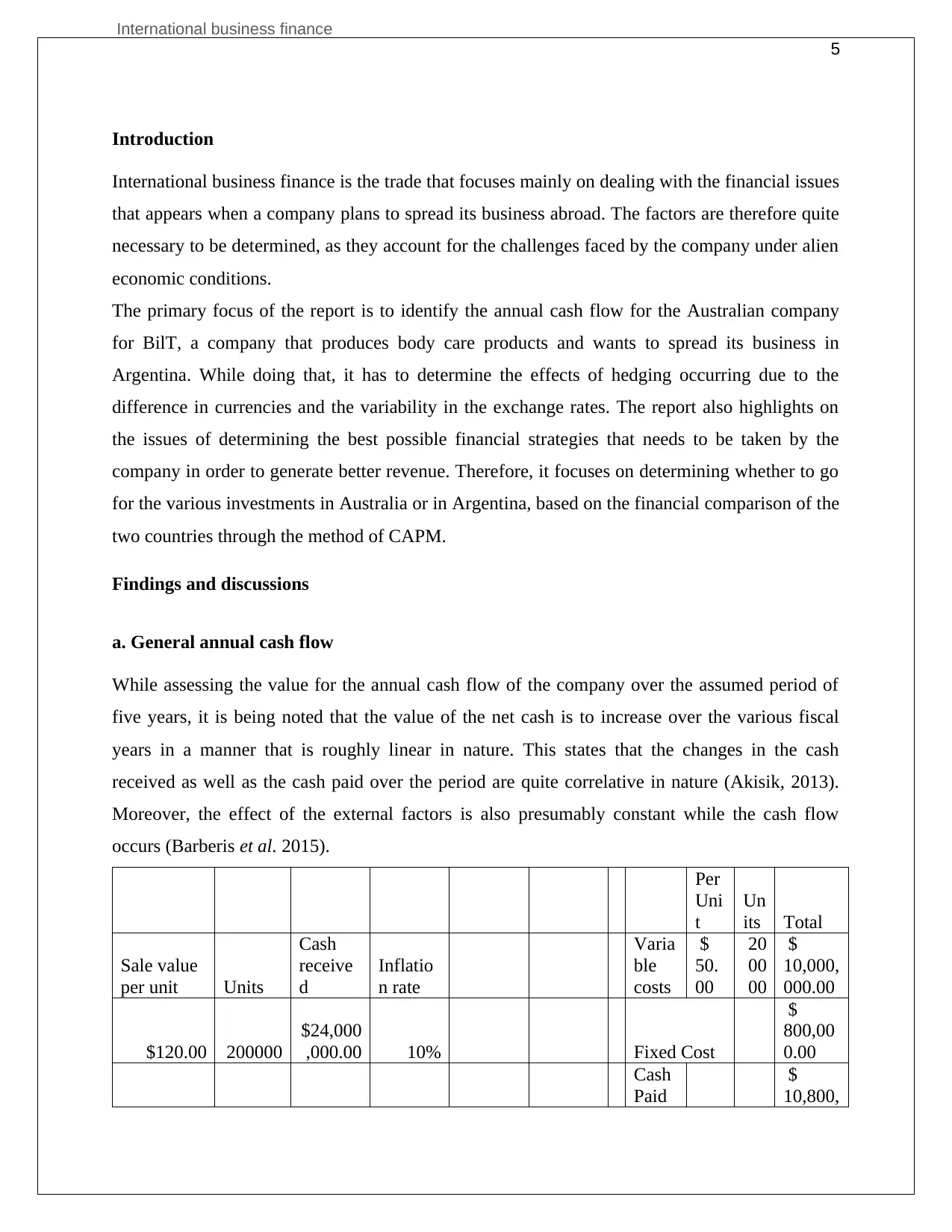

Introduction

International business finance is the trade that focuses mainly on dealing with the financial issues

that appears when a company plans to spread its business abroad. The factors are therefore quite

necessary to be determined, as they account for the challenges faced by the company under alien

economic conditions.

The primary focus of the report is to identify the annual cash flow for the Australian company

for BilT, a company that produces body care products and wants to spread its business in

Argentina. While doing that, it has to determine the effects of hedging occurring due to the

difference in currencies and the variability in the exchange rates. The report also highlights on

the issues of determining the best possible financial strategies that needs to be taken by the

company in order to generate better revenue. Therefore, it focuses on determining whether to go

for the various investments in Australia or in Argentina, based on the financial comparison of the

two countries through the method of CAPM.

Findings and discussions

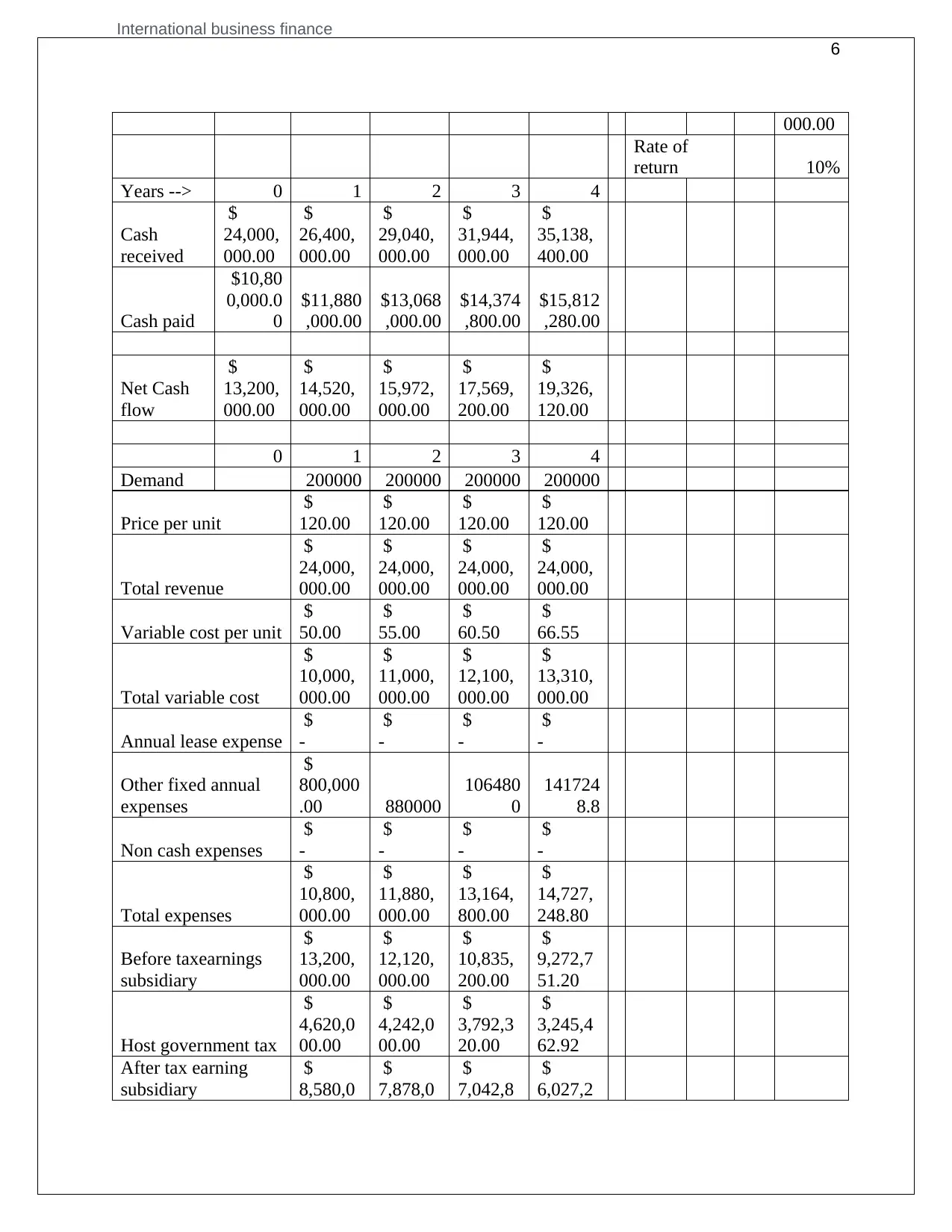

a. General annual cash flow

While assessing the value for the annual cash flow of the company over the assumed period of

five years, it is being noted that the value of the net cash is to increase over the various fiscal

years in a manner that is roughly linear in nature. This states that the changes in the cash

received as well as the cash paid over the period are quite correlative in nature (Akisik, 2013).

Moreover, the effect of the external factors is also presumably constant while the cash flow

occurs (Barberis et al. 2015).

Per

Uni

t

Un

its Total

Sale value

per unit Units

Cash

receive

d

Inflatio

n rate

Varia

ble

costs

$

50.

00

20

00

00

$

10,000,

000.00

$120.00 200000

$24,000

,000.00 10% Fixed Cost

$

800,00

0.00

Cash

Paid

$

10,800,

5

Introduction

International business finance is the trade that focuses mainly on dealing with the financial issues

that appears when a company plans to spread its business abroad. The factors are therefore quite

necessary to be determined, as they account for the challenges faced by the company under alien

economic conditions.

The primary focus of the report is to identify the annual cash flow for the Australian company

for BilT, a company that produces body care products and wants to spread its business in

Argentina. While doing that, it has to determine the effects of hedging occurring due to the

difference in currencies and the variability in the exchange rates. The report also highlights on

the issues of determining the best possible financial strategies that needs to be taken by the

company in order to generate better revenue. Therefore, it focuses on determining whether to go

for the various investments in Australia or in Argentina, based on the financial comparison of the

two countries through the method of CAPM.

Findings and discussions

a. General annual cash flow

While assessing the value for the annual cash flow of the company over the assumed period of

five years, it is being noted that the value of the net cash is to increase over the various fiscal

years in a manner that is roughly linear in nature. This states that the changes in the cash

received as well as the cash paid over the period are quite correlative in nature (Akisik, 2013).

Moreover, the effect of the external factors is also presumably constant while the cash flow

occurs (Barberis et al. 2015).

Per

Uni

t

Un

its Total

Sale value

per unit Units

Cash

receive

d

Inflatio

n rate

Varia

ble

costs

$

50.

00

20

00

00

$

10,000,

000.00

$120.00 200000

$24,000

,000.00 10% Fixed Cost

$

800,00

0.00

Cash

Paid

$

10,800,

International business finance

6

000.00

Rate of

return 10%

Years --> 0 1 2 3 4

Cash

received

$

24,000,

000.00

$

26,400,

000.00

$

29,040,

000.00

$

31,944,

000.00

$

35,138,

400.00

Cash paid

$10,80

0,000.0

0

$11,880

,000.00

$13,068

,000.00

$14,374

,800.00

$15,812

,280.00

Net Cash

flow

$

13,200,

000.00

$

14,520,

000.00

$

15,972,

000.00

$

17,569,

200.00

$

19,326,

120.00

0 1 2 3 4

Demand 200000 200000 200000 200000

Price per unit

$

120.00

$

120.00

$

120.00

$

120.00

Total revenue

$

24,000,

000.00

$

24,000,

000.00

$

24,000,

000.00

$

24,000,

000.00

Variable cost per unit

$

50.00

$

55.00

$

60.50

$

66.55

Total variable cost

$

10,000,

000.00

$

11,000,

000.00

$

12,100,

000.00

$

13,310,

000.00

Annual lease expense

$

-

$

-

$

-

$

-

Other fixed annual

expenses

$

800,000

.00 880000

106480

0

141724

8.8

Non cash expenses

$

-

$

-

$

-

$

-

Total expenses

$

10,800,

000.00

$

11,880,

000.00

$

13,164,

800.00

$

14,727,

248.80

Before taxearnings

subsidiary

$

13,200,

000.00

$

12,120,

000.00

$

10,835,

200.00

$

9,272,7

51.20

Host government tax

$

4,620,0

00.00

$

4,242,0

00.00

$

3,792,3

20.00

$

3,245,4

62.92

After tax earning

subsidiary

$

8,580,0

$

7,878,0

$

7,042,8

$

6,027,2

6

000.00

Rate of

return 10%

Years --> 0 1 2 3 4

Cash

received

$

24,000,

000.00

$

26,400,

000.00

$

29,040,

000.00

$

31,944,

000.00

$

35,138,

400.00

Cash paid

$10,80

0,000.0

0

$11,880

,000.00

$13,068

,000.00

$14,374

,800.00

$15,812

,280.00

Net Cash

flow

$

13,200,

000.00

$

14,520,

000.00

$

15,972,

000.00

$

17,569,

200.00

$

19,326,

120.00

0 1 2 3 4

Demand 200000 200000 200000 200000

Price per unit

$

120.00

$

120.00

$

120.00

$

120.00

Total revenue

$

24,000,

000.00

$

24,000,

000.00

$

24,000,

000.00

$

24,000,

000.00

Variable cost per unit

$

50.00

$

55.00

$

60.50

$

66.55

Total variable cost

$

10,000,

000.00

$

11,000,

000.00

$

12,100,

000.00

$

13,310,

000.00

Annual lease expense

$

-

$

-

$

-

$

-

Other fixed annual

expenses

$

800,000

.00 880000

106480

0

141724

8.8

Non cash expenses

$

-

$

-

$

-

$

-

Total expenses

$

10,800,

000.00

$

11,880,

000.00

$

13,164,

800.00

$

14,727,

248.80

Before taxearnings

subsidiary

$

13,200,

000.00

$

12,120,

000.00

$

10,835,

200.00

$

9,272,7

51.20

Host government tax

$

4,620,0

00.00

$

4,242,0

00.00

$

3,792,3

20.00

$

3,245,4

62.92

After tax earning

subsidiary

$

8,580,0

$

7,878,0

$

7,042,8

$

6,027,2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International business finance

7

00.00 00.00 80.00 88.28

Net cash flow

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Amount remitted by

subsidiary

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Withholding tax on

remitted funds

$

-

$

-

$

-

$

-

Amount remitted

after withholding

taxes

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Salvage value

$

-

$

-

$

-

$

22,000,

000.00

Exchange rate 10% 10% 10% 10%

Cash flows to parent

$

858,000

.00

$

787,800

.00

$

704,288

.00

$

602,728

.83

PV of parent cash

flow

$

943,800

.00

$

953,238

.00

$

937,407

.33

$

882,455

.28

Initial

investment

by parent

$

40,000,

000.00

Cumulative NPV

$

(39,056,

200.00)

$

(38,102,

962.00)

$

(37,165,

554.67)

$

(36,283,

099.39)

Table 1: Annual cash flow for BilT

(Source: Influenced by Learner)

7

00.00 00.00 80.00 88.28

Net cash flow

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Amount remitted by

subsidiary

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Withholding tax on

remitted funds

$

-

$

-

$

-

$

-

Amount remitted

after withholding

taxes

$

8,580,0

00.00

$

7,878,0

00.00

$

7,042,8

80.00

$

6,027,2

88.28

Salvage value

$

-

$

-

$

-

$

22,000,

000.00

Exchange rate 10% 10% 10% 10%

Cash flows to parent

$

858,000

.00

$

787,800

.00

$

704,288

.00

$

602,728

.83

PV of parent cash

flow

$

943,800

.00

$

953,238

.00

$

937,407

.33

$

882,455

.28

Initial

investment

by parent

$

40,000,

000.00

Cumulative NPV

$

(39,056,

200.00)

$

(38,102,

962.00)

$

(37,165,

554.67)

$

(36,283,

099.39)

Table 1: Annual cash flow for BilT

(Source: Influenced by Learner)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International business finance

8

1 2 3 4

$(39,500,000.00)

$(39,000,000.00)

$(38,500,000.00)

$(38,000,000.00)

$(37,500,000.00)

$(37,000,000.00)

$(36,500,000.00)

$(36,000,000.00)

$(35,500,000.00)

$(35,000,000.00)

$(34,500,000.00)

Series1

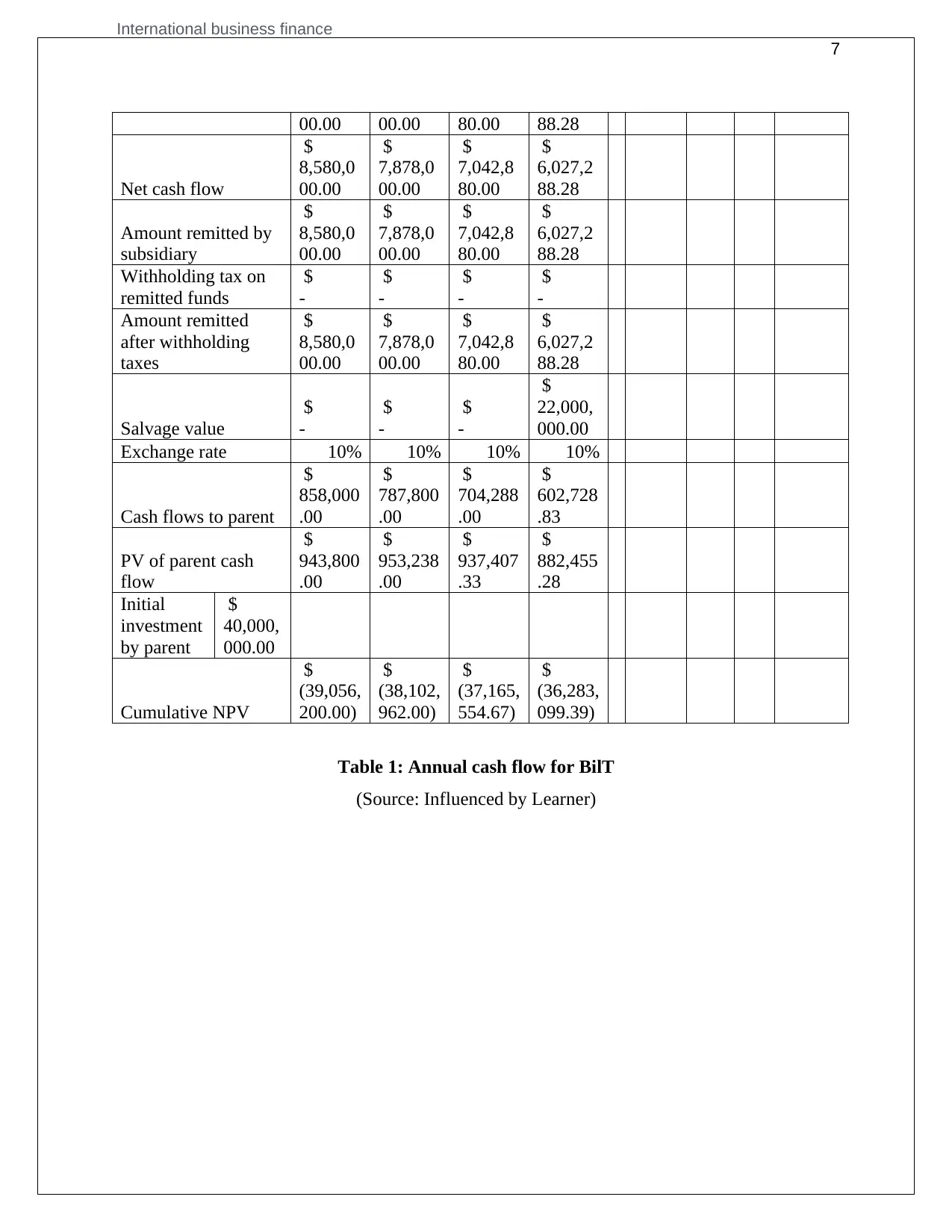

Figure 1: Cumulative cash flow for BilT

(Source: Influenced by Learner)

b. Hedging and cash flow

Hedging is considered a process to reduce the risk associated to the variability in price (Barillas

& Shanken, 2015). While a company enters a new market with a different currency structure,

there is always a risk associated to the commencement of the business as many of the rates and

scales are different, due to a different economic structure (Barth, 2015). As per Berk & Van

Binsbergen (2016), hedging is regarded as the only tool to manage and mitigate such risks.

0 1 2 3 4

Hedge rates 10.00% 10.00% 8.00% 8.00% 7.00%

Cash

$

(40,000,000.00

)

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

Hedge factor 1 1.1 1.1664 1.259712 1.31079601

Hedged cash

flow

$

(40,000,000.00

)

$

9,090,909.09

$

8,573,388.20

$

7,938,322.41

$

7,628,952.12

Net Present

value

$

(6,768,428.18)

Table 2: Effect of Hedge

8

1 2 3 4

$(39,500,000.00)

$(39,000,000.00)

$(38,500,000.00)

$(38,000,000.00)

$(37,500,000.00)

$(37,000,000.00)

$(36,500,000.00)

$(36,000,000.00)

$(35,500,000.00)

$(35,000,000.00)

$(34,500,000.00)

Series1

Figure 1: Cumulative cash flow for BilT

(Source: Influenced by Learner)

b. Hedging and cash flow

Hedging is considered a process to reduce the risk associated to the variability in price (Barillas

& Shanken, 2015). While a company enters a new market with a different currency structure,

there is always a risk associated to the commencement of the business as many of the rates and

scales are different, due to a different economic structure (Barth, 2015). As per Berk & Van

Binsbergen (2016), hedging is regarded as the only tool to manage and mitigate such risks.

0 1 2 3 4

Hedge rates 10.00% 10.00% 8.00% 8.00% 7.00%

Cash

$

(40,000,000.00

)

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

Hedge factor 1 1.1 1.1664 1.259712 1.31079601

Hedged cash

flow

$

(40,000,000.00

)

$

9,090,909.09

$

8,573,388.20

$

7,938,322.41

$

7,628,952.12

Net Present

value

$

(6,768,428.18)

Table 2: Effect of Hedge

International business finance

9

(Source: Influenced by Learner)

0 1 2 3 4

Amount remitted after

withholding taxes

$

8,580,000.00

$

7,878,000.00

$

7,042,880.00

$

6,027,288.28

Hedged cash flows after

withholding taxes

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

Unhedged cash flows

$

(1,420,000.0

0)

$

(2,122,000.0

0)

$

(2,957,120.0

0)

$

(3,972,711.7

2)

Salvage Value

$

-

$

-

$

-

$

22,000,000.0

0

Forward rate 10% 10% 8% 8% 7%

Expected future

spot rate 10% 10% 10% 10% 10%

Hedged cash flow to parent

$

1,000,000.00

$

800,000.00

$

800,000.00

$

700,000.00

Unhedged cash flows to parent

$

(142,000.00)

$

(212,200.00)

$

(295,712.00)

$

(397,271.17)

Total cash flows to parent

$

858,000.00

$

587,800.00

$

504,288.00

$

302,728.83

PV of parent cash flow

$

780,000.00

$

485,785.12

$

378,879.04

$

206,767.86

Initial investment

by parent

$

40,000,000.

00

Cumulative NPV

$

(39,220,000.

00)

$

(38,734,214.

88)

$

(38,355,335.

84)

$

(38,148,567.

97)

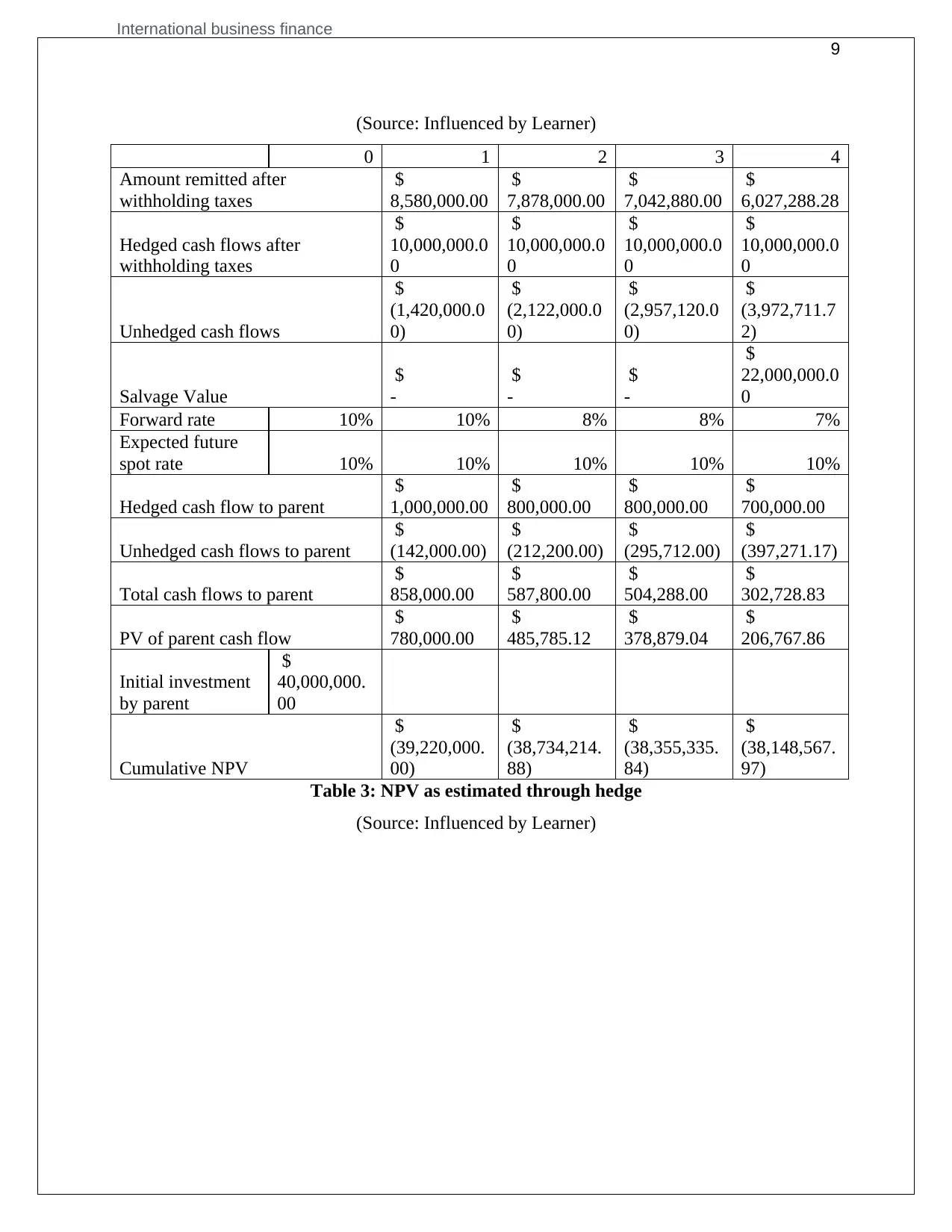

Table 3: NPV as estimated through hedge

(Source: Influenced by Learner)

9

(Source: Influenced by Learner)

0 1 2 3 4

Amount remitted after

withholding taxes

$

8,580,000.00

$

7,878,000.00

$

7,042,880.00

$

6,027,288.28

Hedged cash flows after

withholding taxes

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

$

10,000,000.0

0

Unhedged cash flows

$

(1,420,000.0

0)

$

(2,122,000.0

0)

$

(2,957,120.0

0)

$

(3,972,711.7

2)

Salvage Value

$

-

$

-

$

-

$

22,000,000.0

0

Forward rate 10% 10% 8% 8% 7%

Expected future

spot rate 10% 10% 10% 10% 10%

Hedged cash flow to parent

$

1,000,000.00

$

800,000.00

$

800,000.00

$

700,000.00

Unhedged cash flows to parent

$

(142,000.00)

$

(212,200.00)

$

(295,712.00)

$

(397,271.17)

Total cash flows to parent

$

858,000.00

$

587,800.00

$

504,288.00

$

302,728.83

PV of parent cash flow

$

780,000.00

$

485,785.12

$

378,879.04

$

206,767.86

Initial investment

by parent

$

40,000,000.

00

Cumulative NPV

$

(39,220,000.

00)

$

(38,734,214.

88)

$

(38,355,335.

84)

$

(38,148,567.

97)

Table 3: NPV as estimated through hedge

(Source: Influenced by Learner)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International business finance

10

1 2 3 4

$(39,400,000.00)

$(39,200,000.00)

$(39,000,000.00)

$(38,800,000.00)

$(38,600,000.00)

$(38,400,000.00)

$(38,200,000.00)

$(38,000,000.00)

$(37,800,000.00)

$(37,600,000.00)

Series1

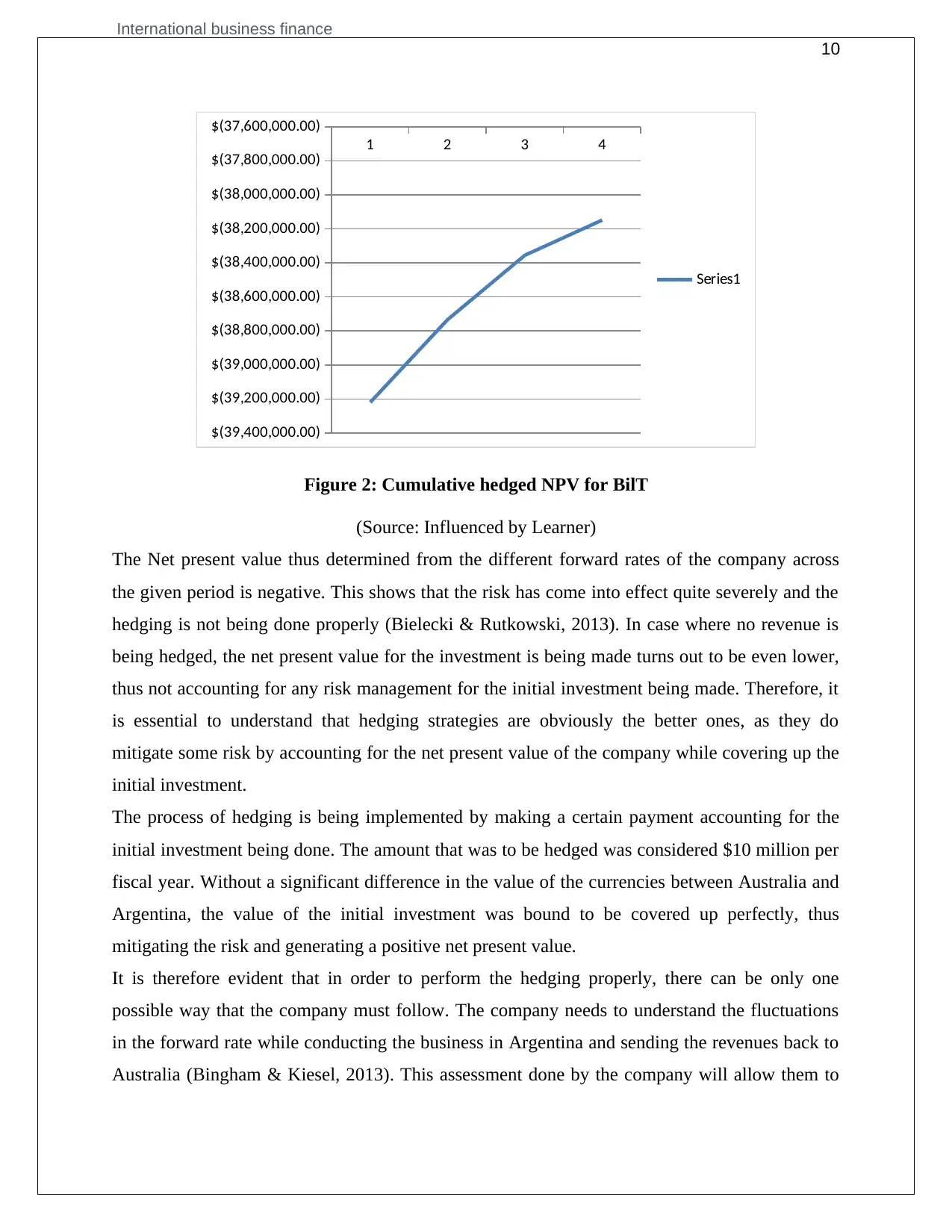

Figure 2: Cumulative hedged NPV for BilT

(Source: Influenced by Learner)

The Net present value thus determined from the different forward rates of the company across

the given period is negative. This shows that the risk has come into effect quite severely and the

hedging is not being done properly (Bielecki & Rutkowski, 2013). In case where no revenue is

being hedged, the net present value for the investment is being made turns out to be even lower,

thus not accounting for any risk management for the initial investment being made. Therefore, it

is essential to understand that hedging strategies are obviously the better ones, as they do

mitigate some risk by accounting for the net present value of the company while covering up the

initial investment.

The process of hedging is being implemented by making a certain payment accounting for the

initial investment being done. The amount that was to be hedged was considered $10 million per

fiscal year. Without a significant difference in the value of the currencies between Australia and

Argentina, the value of the initial investment was bound to be covered up perfectly, thus

mitigating the risk and generating a positive net present value.

It is therefore evident that in order to perform the hedging properly, there can be only one

possible way that the company must follow. The company needs to understand the fluctuations

in the forward rate while conducting the business in Argentina and sending the revenues back to

Australia (Bingham & Kiesel, 2013). This assessment done by the company will allow them to

10

1 2 3 4

$(39,400,000.00)

$(39,200,000.00)

$(39,000,000.00)

$(38,800,000.00)

$(38,600,000.00)

$(38,400,000.00)

$(38,200,000.00)

$(38,000,000.00)

$(37,800,000.00)

$(37,600,000.00)

Series1

Figure 2: Cumulative hedged NPV for BilT

(Source: Influenced by Learner)

The Net present value thus determined from the different forward rates of the company across

the given period is negative. This shows that the risk has come into effect quite severely and the

hedging is not being done properly (Bielecki & Rutkowski, 2013). In case where no revenue is

being hedged, the net present value for the investment is being made turns out to be even lower,

thus not accounting for any risk management for the initial investment being made. Therefore, it

is essential to understand that hedging strategies are obviously the better ones, as they do

mitigate some risk by accounting for the net present value of the company while covering up the

initial investment.

The process of hedging is being implemented by making a certain payment accounting for the

initial investment being done. The amount that was to be hedged was considered $10 million per

fiscal year. Without a significant difference in the value of the currencies between Australia and

Argentina, the value of the initial investment was bound to be covered up perfectly, thus

mitigating the risk and generating a positive net present value.

It is therefore evident that in order to perform the hedging properly, there can be only one

possible way that the company must follow. The company needs to understand the fluctuations

in the forward rate while conducting the business in Argentina and sending the revenues back to

Australia (Bingham & Kiesel, 2013). This assessment done by the company will allow them to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International business finance

11

reshape the hedge amount according to the forward rate, which will in turn help to generate a

positive net present value against the initial investment that has been made (Bodie, 2013).

c. Difference in borrow

While assessing the investment strategy for BilT, it is evident that 60% value for the initial

investment is to be considered as the initial investment for the company under the revised

circumstances. The company has already planned to cover 40% of the initial investment value

through their existing funds. Due to the revised initial investment value being recovered through

the issuance of debts, there has to be a certain involvement for borrow. The borrow rate for the

two different countries, Argentina and Australia are being mentioned to be 6% and 12%

respectively. This difference in the rate of borrow has caused the amount paid as interest to be

different. The rate of return for the investment has developed the cash flow for the company

accordingly, for the period of five fiscal years and the corresponding net present values are

determined accordingly, by adding up all the discounted cash flow amounts.

Argentina @ 6%

0 1 2 3 4

Investment

$

(24,000,000.00

)

$

1,440,000.0

0

$

2,966,400.0

0

$

4,584,384.00

$

6,299,447.04

Rate of Return 10% 10% 10% 10% 10%

Discounted

cash flow

$

(24,000,000.00

)

$

1,584,000.0

0

$

3,589,344.0

0

$

6,101,815.10

$

9,223,020.41

NPV

$

(3,501,820.48)

Australia @ 12%

0 1 2 3 4

Investment

$

(24,000,000.00

)

$

2,880,000.0

0

$

6,105,600.0

0

$

9,718,272.00

$

13,764,464.6

4

Rate of Return 10% 10% 10% 10% 10%

Discounted

cash flow

$

(24,000,000.00

)

$

3,168,000.0

0

$

7,387,776.0

0

$

12,935,020.0

3

$

20,152,552.6

8

11

reshape the hedge amount according to the forward rate, which will in turn help to generate a

positive net present value against the initial investment that has been made (Bodie, 2013).

c. Difference in borrow

While assessing the investment strategy for BilT, it is evident that 60% value for the initial

investment is to be considered as the initial investment for the company under the revised

circumstances. The company has already planned to cover 40% of the initial investment value

through their existing funds. Due to the revised initial investment value being recovered through

the issuance of debts, there has to be a certain involvement for borrow. The borrow rate for the

two different countries, Argentina and Australia are being mentioned to be 6% and 12%

respectively. This difference in the rate of borrow has caused the amount paid as interest to be

different. The rate of return for the investment has developed the cash flow for the company

accordingly, for the period of five fiscal years and the corresponding net present values are

determined accordingly, by adding up all the discounted cash flow amounts.

Argentina @ 6%

0 1 2 3 4

Investment

$

(24,000,000.00

)

$

1,440,000.0

0

$

2,966,400.0

0

$

4,584,384.00

$

6,299,447.04

Rate of Return 10% 10% 10% 10% 10%

Discounted

cash flow

$

(24,000,000.00

)

$

1,584,000.0

0

$

3,589,344.0

0

$

6,101,815.10

$

9,223,020.41

NPV

$

(3,501,820.48)

Australia @ 12%

0 1 2 3 4

Investment

$

(24,000,000.00

)

$

2,880,000.0

0

$

6,105,600.0

0

$

9,718,272.00

$

13,764,464.6

4

Rate of Return 10% 10% 10% 10% 10%

Discounted

cash flow

$

(24,000,000.00

)

$

3,168,000.0

0

$

7,387,776.0

0

$

12,935,020.0

3

$

20,152,552.6

8

International business finance

12

NPV

$

19,643,348.71

Table 4: Calculation of borrow amount

(Source: Influenced by Learner)

While assessing the net present value for both the countries under different rates of borrow, it is

evident that the Argentine economy offers a negative value of NPV against the initial

investment, whereas the Australian economy offers the chance for a positive NPV against the

initial amount that is being debited. The positive value of the NPV therefore concludes the loan

to be taken from the Australia, by issuing the debt in any bank of Australia over the likeness of

Argentina.

d. Cost of Equity

While analyzing the cost of equity for BilT, the method of Capital Asset Pricing Model is being

implemented in order to determine the risk associated with making the investment in Australia or

in Argentina. The Capital Asset Pricing Model determines the overall value of the payback being

affected by the associated risk (Camfferman & Zeff, 2015). This accounts for the assessment of

the weighted average of the amount of debt as well as the amount of equity, and finally adding

them up (Chegut, Eichholtz & Kok, 2014).

The weighted average is being estimated by multiplying the systematic risk probability to the

cost of the debt or the equity (Chui, Fender & Sushko, 2014). This helps in determining the

return from a hybrid fund that consists mainly of both the debt as well as equity instruments in a

specific proportion (Devlin, 2014).

The cost of equity however, determines the return that the company has decided to generate in

order to provide to the shareholders (Dong, Kouvelis & Su, 2014). Moreover, it also accounts for

the compensation that the market demands in exchange for owing the assets as well as bearing

the systematic risk of owning the company (Du & Schreger, 2016). The capital asset pricing

model determines the cost of equity for a firm to be the sum of the risk free rate of return and the

product of volatility and risk premium for the particular stock with respect to the market

(Fernandez, 2015).

12

NPV

$

19,643,348.71

Table 4: Calculation of borrow amount

(Source: Influenced by Learner)

While assessing the net present value for both the countries under different rates of borrow, it is

evident that the Argentine economy offers a negative value of NPV against the initial

investment, whereas the Australian economy offers the chance for a positive NPV against the

initial amount that is being debited. The positive value of the NPV therefore concludes the loan

to be taken from the Australia, by issuing the debt in any bank of Australia over the likeness of

Argentina.

d. Cost of Equity

While analyzing the cost of equity for BilT, the method of Capital Asset Pricing Model is being

implemented in order to determine the risk associated with making the investment in Australia or

in Argentina. The Capital Asset Pricing Model determines the overall value of the payback being

affected by the associated risk (Camfferman & Zeff, 2015). This accounts for the assessment of

the weighted average of the amount of debt as well as the amount of equity, and finally adding

them up (Chegut, Eichholtz & Kok, 2014).

The weighted average is being estimated by multiplying the systematic risk probability to the

cost of the debt or the equity (Chui, Fender & Sushko, 2014). This helps in determining the

return from a hybrid fund that consists mainly of both the debt as well as equity instruments in a

specific proportion (Devlin, 2014).

The cost of equity however, determines the return that the company has decided to generate in

order to provide to the shareholders (Dong, Kouvelis & Su, 2014). Moreover, it also accounts for

the compensation that the market demands in exchange for owing the assets as well as bearing

the systematic risk of owning the company (Du & Schreger, 2016). The capital asset pricing

model determines the cost of equity for a firm to be the sum of the risk free rate of return and the

product of volatility and risk premium for the particular stock with respect to the market

(Fernandez, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.