Finance of International Business: Transaction Exposure Analysis

VerifiedAdded on 2022/09/15

|13

|3105

|19

Case Study

AI Summary

This case study analyzes the finance of international business, focusing on transaction exposure and the value-at-risk (VAR) method. It examines how exchange rate movements impact a firm's contractual transactions in foreign currencies, emphasizing the importance of assessing and managing currency exposure. The study includes a computation of the maximum one-day loss for a company receiving Mexican pesos, considering factors like standard deviation and confidence levels. Furthermore, it explores the VAR method using a currency portfolio, calculating maximum one-month losses for different currencies and analyzing the benefits of diversification. The analysis covers various hedging methods and the drawbacks of the VAR method, providing a comprehensive overview of international finance risk management strategies. The assignment covers the concepts of transaction exposure, VAR, and their application in managing currency risk.

Running head: FINANCE OF INTERNATIONAL BUSINESS

FINANCE OF INTERNATIONAL BUSINESS

Name of the Student:

Name of the University:

Author Note:

FINANCE OF INTERNATIONAL BUSINESS

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

-

Table of Contents

Introduction................................................................................................................................2

Transaction Exposure.................................................................................................................2

Assessment of Exposure via VAR.............................................................................................4

Maximum One-Day Loss.......................................................................................................4

Factors Affecting Maximum One-Day Loss..........................................................................5

VAR Method of Currency Portfolio..........................................................................................6

Drawbacks of VAR............................................................................................................8

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

-

Table of Contents

Introduction................................................................................................................................2

Transaction Exposure.................................................................................................................2

Assessment of Exposure via VAR.............................................................................................4

Maximum One-Day Loss.......................................................................................................4

Factors Affecting Maximum One-Day Loss..........................................................................5

VAR Method of Currency Portfolio..........................................................................................6

Drawbacks of VAR............................................................................................................8

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

2FINANCE

Introduction

International finance plays a vital role in every business and more importantly there

are various factors like changes observed in exchange rate, economic change and changes in

the interest rate levels that can materially affects the business of a company. Changes on the

currency exchange rate can be one of a key and an important concern for the company, but it

becomes important for the company to well take important steps and actions for the purpose

of well hedging the forex risk. Transaction exposure is one of the key risk exposure that is

well faced by the company and this has been particularly due to the operations of the

company based on a global scale whereby it receives and pays an amount in a foreign

currency. Now changes in the value of the foreign currency can well change the receivable or

payable value and ultimately the value for the company could be affected due to the same.

Thus, it becomes important for the company to hedge its foreign currency with the help of

various derivative contracts that the company can well use in order to well hedge its

exposure. Application of various risk management strategies like VAR has been well applied

in order to well calculate or measure the loss that would be well incurring due to the

investment that has been done. Now this well shows or estimates how much a set of

investment that it might loose with a certain probability, under given set of normal market

conditions and in a specific period of time.

Transaction Exposure

The term transaction exposure is related to the uncertainty level in which the business

is involved in international trade face. The risk that will be faced by a firm after undertaking

the financial obligation concerning the fluctuation of currency exchanges is known as

translation exposure. International business can face capital losses if there is a high level of

vulnerability to shifting exchange rates (Khindanova 2015). The firm can save themselves

Introduction

International finance plays a vital role in every business and more importantly there

are various factors like changes observed in exchange rate, economic change and changes in

the interest rate levels that can materially affects the business of a company. Changes on the

currency exchange rate can be one of a key and an important concern for the company, but it

becomes important for the company to well take important steps and actions for the purpose

of well hedging the forex risk. Transaction exposure is one of the key risk exposure that is

well faced by the company and this has been particularly due to the operations of the

company based on a global scale whereby it receives and pays an amount in a foreign

currency. Now changes in the value of the foreign currency can well change the receivable or

payable value and ultimately the value for the company could be affected due to the same.

Thus, it becomes important for the company to hedge its foreign currency with the help of

various derivative contracts that the company can well use in order to well hedge its

exposure. Application of various risk management strategies like VAR has been well applied

in order to well calculate or measure the loss that would be well incurring due to the

investment that has been done. Now this well shows or estimates how much a set of

investment that it might loose with a certain probability, under given set of normal market

conditions and in a specific period of time.

Transaction Exposure

The term transaction exposure is related to the uncertainty level in which the business

is involved in international trade face. The risk that will be faced by a firm after undertaking

the financial obligation concerning the fluctuation of currency exchanges is known as

translation exposure. International business can face capital losses if there is a high level of

vulnerability to shifting exchange rates (Khindanova 2015). The firm can save themselves

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

from a high level of exposure related to exchange rate by implementing a hedging strategy.

Hedging strategy consists of currency swaps or currency future. By implementing a hedging

strategy, the firms can use forward rates that will allow the firm to choose a profitable rate of

currency exchange and will be beneficial for avoiding exposure to risk. Generally, the risk of

translation exposure is one-sided, that is business that completes a transaction in foreign

currency is only subject to vulnerability. The business that is dealing with home currency is

not subject to transaction exposure risk. In general, view the risk that are well associated in

association with fluctuation of exchange rate increases if time is more between agreement

and the contract settlement. In short, transaction exposure is the level of risk that is faced by

companies that are dealing in international trade. If the exposure is high related to exchange

rate fluctuation, then the company is going to bear a major loss in international trade.

Comparing the short-term and long-term impact on cash flow changes because of

forex fluctuation in the market will be equivalent in comparing the transaction and economic

exposure. Specific driving factors of transaction risk are future receivables or payables

related to foreign currency, whereas economic exposure is driven by future currency cash

flow or outflows (Arize et al. 2018). Often companies are exposed to cash flow variability

depending on the exchange rate fluctuations. Cash flow risk might be short-term as well as

long-term depending on their nature. Cash flow management is taken into consideration for

managing the transaction exposure (Disatnik, Duchin and Schmidt 2014). The transaction

that has contracted for drives the transaction exposure and is short-term in nature. In short,

the company has already undertaken a risk on cash flow. Risk of the exposure is limited to

the contract or as per the transaction as discussed earlier. The more easily identifiable risk

associated with foreign exchange is the transaction risk. A company faces transaction risk

only when it undertakes or enter into a contract that involves future receivables or payables in

terms of foreign currency. It is assumed that the scope of transaction risk is narrow. The

from a high level of exposure related to exchange rate by implementing a hedging strategy.

Hedging strategy consists of currency swaps or currency future. By implementing a hedging

strategy, the firms can use forward rates that will allow the firm to choose a profitable rate of

currency exchange and will be beneficial for avoiding exposure to risk. Generally, the risk of

translation exposure is one-sided, that is business that completes a transaction in foreign

currency is only subject to vulnerability. The business that is dealing with home currency is

not subject to transaction exposure risk. In general, view the risk that are well associated in

association with fluctuation of exchange rate increases if time is more between agreement

and the contract settlement. In short, transaction exposure is the level of risk that is faced by

companies that are dealing in international trade. If the exposure is high related to exchange

rate fluctuation, then the company is going to bear a major loss in international trade.

Comparing the short-term and long-term impact on cash flow changes because of

forex fluctuation in the market will be equivalent in comparing the transaction and economic

exposure. Specific driving factors of transaction risk are future receivables or payables

related to foreign currency, whereas economic exposure is driven by future currency cash

flow or outflows (Arize et al. 2018). Often companies are exposed to cash flow variability

depending on the exchange rate fluctuations. Cash flow risk might be short-term as well as

long-term depending on their nature. Cash flow management is taken into consideration for

managing the transaction exposure (Disatnik, Duchin and Schmidt 2014). The transaction

that has contracted for drives the transaction exposure and is short-term in nature. In short,

the company has already undertaken a risk on cash flow. Risk of the exposure is limited to

the contract or as per the transaction as discussed earlier. The more easily identifiable risk

associated with foreign exchange is the transaction risk. A company faces transaction risk

only when it undertakes or enter into a contract that involves future receivables or payables in

terms of foreign currency. It is assumed that the scope of transaction risk is narrow. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

nature of transaction exposure is tactical and technical in nature. Most company usually

prefers to hedge transaction exposure to experience less risk.

Companies trading in international investment would be well creating an exposure in

terms of currency volatility. The movement in the exchange rate affect the returns when there

is a change in the value of one currency when compared against another currency, and

ultimately, this leads to an increase or decrease in the value of an asset. Dealing in the

domestic market will only need to evaluate only the increase or decrease in the asset value.

However, while dealing in international trade, the company needs to analyze the impact of

exchange rate on the contract. In short, we can say that if domestic currency depreciates we

can purchase less of foreign currency and it ultimately reduces the purchasing power (Dong,

Kouvelis and Su 2014). If the domestic currency appreciates, we can buy more foreign

currency, thus, increasing purchasing power. Hedging can be done by various methods such

as forward contracts, options, exchange-traded fund, and contract for difference. The

companies try to hedge the currency risks as it can rapidly dissolve profits and mainly in

times of high volatility.

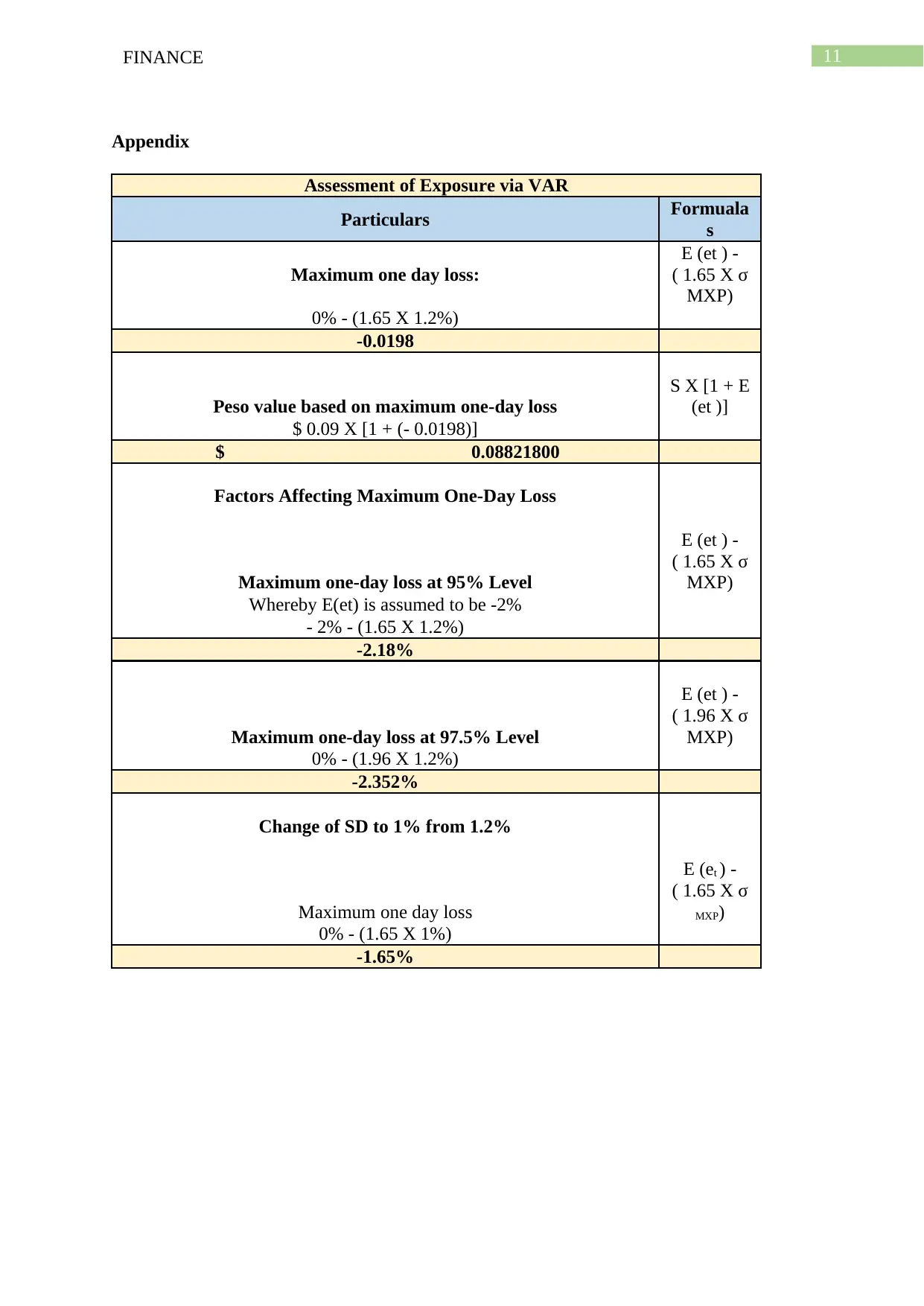

Assessment of Exposure via VAR

Maximum One-Day Loss

The Celia Company has provided consulting services to a Mexican firm and for this;

the company will receive 10 million Mexican pesos (MXP). The company is interested to

evaluate the maximum one-day loss that is because of the decline in the peso value and the

analysis will be done on 95% confidence level. The level of standard deviation that is related

to the daily percentage of Mexican is expected to be 1.2% during the last 100 days. The

maximum one-day loss can be estimated by left tail of the probability distribution if the daily

level of percentage changes are distributed on a normality basis. The standard deviation is

nature of transaction exposure is tactical and technical in nature. Most company usually

prefers to hedge transaction exposure to experience less risk.

Companies trading in international investment would be well creating an exposure in

terms of currency volatility. The movement in the exchange rate affect the returns when there

is a change in the value of one currency when compared against another currency, and

ultimately, this leads to an increase or decrease in the value of an asset. Dealing in the

domestic market will only need to evaluate only the increase or decrease in the asset value.

However, while dealing in international trade, the company needs to analyze the impact of

exchange rate on the contract. In short, we can say that if domestic currency depreciates we

can purchase less of foreign currency and it ultimately reduces the purchasing power (Dong,

Kouvelis and Su 2014). If the domestic currency appreciates, we can buy more foreign

currency, thus, increasing purchasing power. Hedging can be done by various methods such

as forward contracts, options, exchange-traded fund, and contract for difference. The

companies try to hedge the currency risks as it can rapidly dissolve profits and mainly in

times of high volatility.

Assessment of Exposure via VAR

Maximum One-Day Loss

The Celia Company has provided consulting services to a Mexican firm and for this;

the company will receive 10 million Mexican pesos (MXP). The company is interested to

evaluate the maximum one-day loss that is because of the decline in the peso value and the

analysis will be done on 95% confidence level. The level of standard deviation that is related

to the daily percentage of Mexican is expected to be 1.2% during the last 100 days. The

maximum one-day loss can be estimated by left tail of the probability distribution if the daily

level of percentage changes are distributed on a normality basis. The standard deviation is

5FINANCE

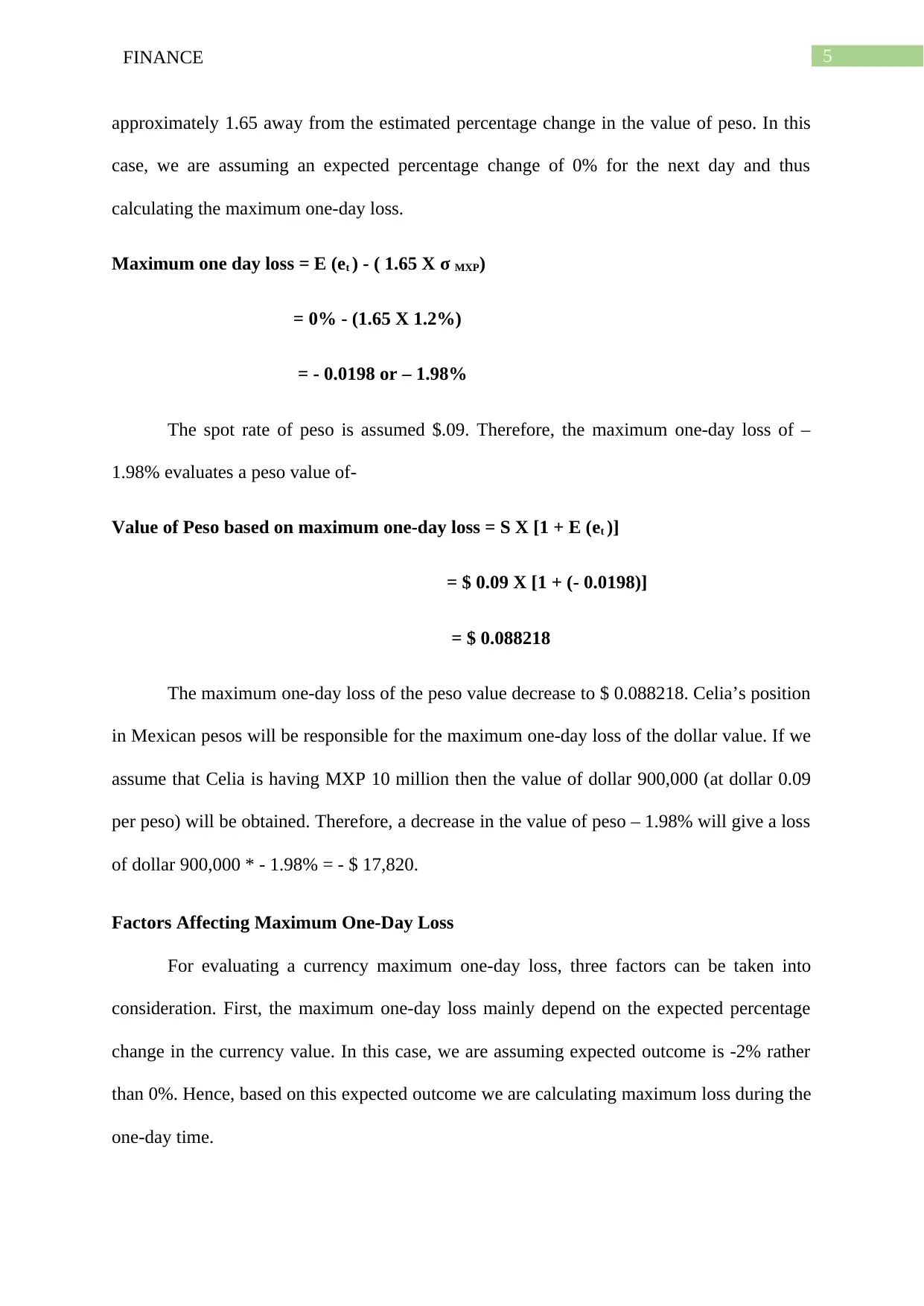

approximately 1.65 away from the estimated percentage change in the value of peso. In this

case, we are assuming an expected percentage change of 0% for the next day and thus

calculating the maximum one-day loss.

Maximum one day loss = E (et ) - ( 1.65 X σ MXP)

= 0% - (1.65 X 1.2%)

= - 0.0198 or – 1.98%

The spot rate of peso is assumed $.09. Therefore, the maximum one-day loss of –

1.98% evaluates a peso value of-

Value of Peso based on maximum one-day loss = S X [1 + E (et )]

= $ 0.09 X [1 + (- 0.0198)]

= $ 0.088218

The maximum one-day loss of the peso value decrease to $ 0.088218. Celia’s position

in Mexican pesos will be responsible for the maximum one-day loss of the dollar value. If we

assume that Celia is having MXP 10 million then the value of dollar 900,000 (at dollar 0.09

per peso) will be obtained. Therefore, a decrease in the value of peso – 1.98% will give a loss

of dollar 900,000 * - 1.98% = - $ 17,820.

Factors Affecting Maximum One-Day Loss

For evaluating a currency maximum one-day loss, three factors can be taken into

consideration. First, the maximum one-day loss mainly depend on the expected percentage

change in the currency value. In this case, we are assuming expected outcome is -2% rather

than 0%. Hence, based on this expected outcome we are calculating maximum loss during the

one-day time.

approximately 1.65 away from the estimated percentage change in the value of peso. In this

case, we are assuming an expected percentage change of 0% for the next day and thus

calculating the maximum one-day loss.

Maximum one day loss = E (et ) - ( 1.65 X σ MXP)

= 0% - (1.65 X 1.2%)

= - 0.0198 or – 1.98%

The spot rate of peso is assumed $.09. Therefore, the maximum one-day loss of –

1.98% evaluates a peso value of-

Value of Peso based on maximum one-day loss = S X [1 + E (et )]

= $ 0.09 X [1 + (- 0.0198)]

= $ 0.088218

The maximum one-day loss of the peso value decrease to $ 0.088218. Celia’s position

in Mexican pesos will be responsible for the maximum one-day loss of the dollar value. If we

assume that Celia is having MXP 10 million then the value of dollar 900,000 (at dollar 0.09

per peso) will be obtained. Therefore, a decrease in the value of peso – 1.98% will give a loss

of dollar 900,000 * - 1.98% = - $ 17,820.

Factors Affecting Maximum One-Day Loss

For evaluating a currency maximum one-day loss, three factors can be taken into

consideration. First, the maximum one-day loss mainly depend on the expected percentage

change in the currency value. In this case, we are assuming expected outcome is -2% rather

than 0%. Hence, based on this expected outcome we are calculating maximum loss during the

one-day time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

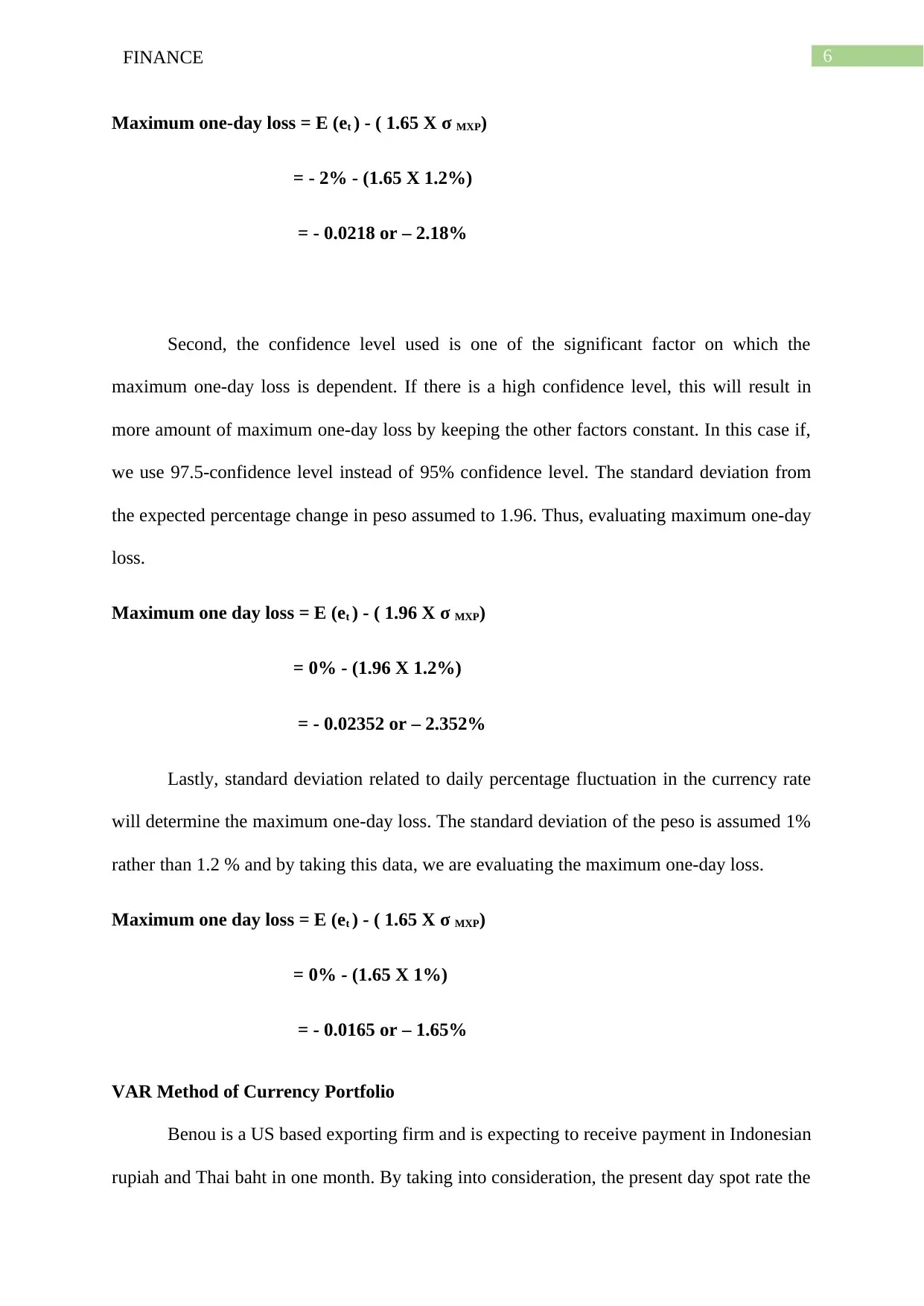

Maximum one-day loss = E (et ) - ( 1.65 X σ MXP)

= - 2% - (1.65 X 1.2%)

= - 0.0218 or – 2.18%

Second, the confidence level used is one of the significant factor on which the

maximum one-day loss is dependent. If there is a high confidence level, this will result in

more amount of maximum one-day loss by keeping the other factors constant. In this case if,

we use 97.5-confidence level instead of 95% confidence level. The standard deviation from

the expected percentage change in peso assumed to 1.96. Thus, evaluating maximum one-day

loss.

Maximum one day loss = E (et ) - ( 1.96 X σ MXP)

= 0% - (1.96 X 1.2%)

= - 0.02352 or – 2.352%

Lastly, standard deviation related to daily percentage fluctuation in the currency rate

will determine the maximum one-day loss. The standard deviation of the peso is assumed 1%

rather than 1.2 % and by taking this data, we are evaluating the maximum one-day loss.

Maximum one day loss = E (et ) - ( 1.65 X σ MXP)

= 0% - (1.65 X 1%)

= - 0.0165 or – 1.65%

VAR Method of Currency Portfolio

Benou is a US based exporting firm and is expecting to receive payment in Indonesian

rupiah and Thai baht in one month. By taking into consideration, the present day spot rate the

Maximum one-day loss = E (et ) - ( 1.65 X σ MXP)

= - 2% - (1.65 X 1.2%)

= - 0.0218 or – 2.18%

Second, the confidence level used is one of the significant factor on which the

maximum one-day loss is dependent. If there is a high confidence level, this will result in

more amount of maximum one-day loss by keeping the other factors constant. In this case if,

we use 97.5-confidence level instead of 95% confidence level. The standard deviation from

the expected percentage change in peso assumed to 1.96. Thus, evaluating maximum one-day

loss.

Maximum one day loss = E (et ) - ( 1.96 X σ MXP)

= 0% - (1.96 X 1.2%)

= - 0.02352 or – 2.352%

Lastly, standard deviation related to daily percentage fluctuation in the currency rate

will determine the maximum one-day loss. The standard deviation of the peso is assumed 1%

rather than 1.2 % and by taking this data, we are evaluating the maximum one-day loss.

Maximum one day loss = E (et ) - ( 1.65 X σ MXP)

= 0% - (1.65 X 1%)

= - 0.0165 or – 1.65%

VAR Method of Currency Portfolio

Benou is a US based exporting firm and is expecting to receive payment in Indonesian

rupiah and Thai baht in one month. By taking into consideration, the present day spot rate the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

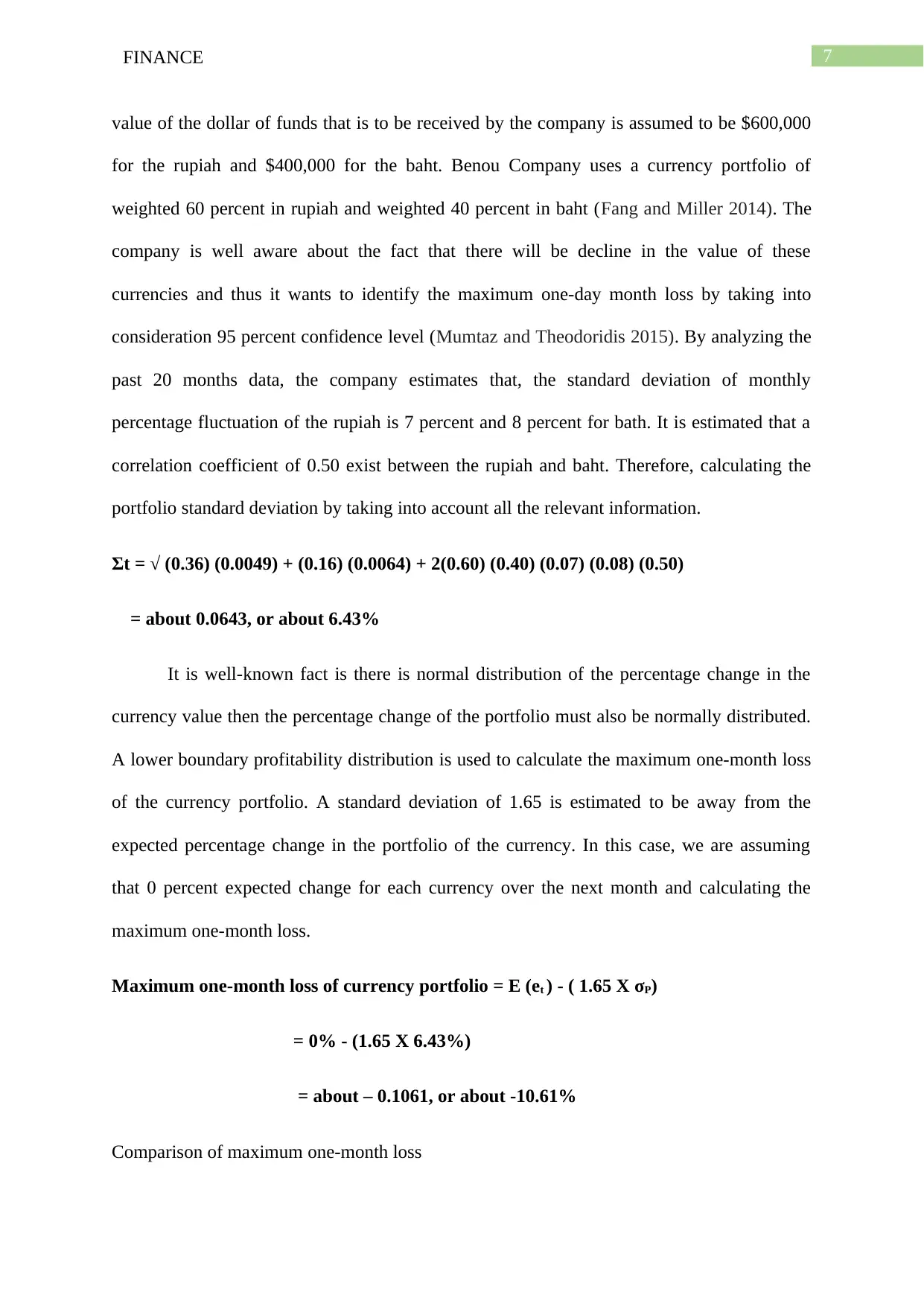

value of the dollar of funds that is to be received by the company is assumed to be $600,000

for the rupiah and $400,000 for the baht. Benou Company uses a currency portfolio of

weighted 60 percent in rupiah and weighted 40 percent in baht (Fang and Miller 2014). The

company is well aware about the fact that there will be decline in the value of these

currencies and thus it wants to identify the maximum one-day month loss by taking into

consideration 95 percent confidence level (Mumtaz and Theodoridis 2015). By analyzing the

past 20 months data, the company estimates that, the standard deviation of monthly

percentage fluctuation of the rupiah is 7 percent and 8 percent for bath. It is estimated that a

correlation coefficient of 0.50 exist between the rupiah and baht. Therefore, calculating the

portfolio standard deviation by taking into account all the relevant information.

Σt = √ (0.36) (0.0049) + (0.16) (0.0064) + 2(0.60) (0.40) (0.07) (0.08) (0.50)

= about 0.0643, or about 6.43%

It is well-known fact is there is normal distribution of the percentage change in the

currency value then the percentage change of the portfolio must also be normally distributed.

A lower boundary profitability distribution is used to calculate the maximum one-month loss

of the currency portfolio. A standard deviation of 1.65 is estimated to be away from the

expected percentage change in the portfolio of the currency. In this case, we are assuming

that 0 percent expected change for each currency over the next month and calculating the

maximum one-month loss.

Maximum one-month loss of currency portfolio = E (et ) - ( 1.65 X σP)

= 0% - (1.65 X 6.43%)

= about – 0.1061, or about -10.61%

Comparison of maximum one-month loss

value of the dollar of funds that is to be received by the company is assumed to be $600,000

for the rupiah and $400,000 for the baht. Benou Company uses a currency portfolio of

weighted 60 percent in rupiah and weighted 40 percent in baht (Fang and Miller 2014). The

company is well aware about the fact that there will be decline in the value of these

currencies and thus it wants to identify the maximum one-day month loss by taking into

consideration 95 percent confidence level (Mumtaz and Theodoridis 2015). By analyzing the

past 20 months data, the company estimates that, the standard deviation of monthly

percentage fluctuation of the rupiah is 7 percent and 8 percent for bath. It is estimated that a

correlation coefficient of 0.50 exist between the rupiah and baht. Therefore, calculating the

portfolio standard deviation by taking into account all the relevant information.

Σt = √ (0.36) (0.0049) + (0.16) (0.0064) + 2(0.60) (0.40) (0.07) (0.08) (0.50)

= about 0.0643, or about 6.43%

It is well-known fact is there is normal distribution of the percentage change in the

currency value then the percentage change of the portfolio must also be normally distributed.

A lower boundary profitability distribution is used to calculate the maximum one-month loss

of the currency portfolio. A standard deviation of 1.65 is estimated to be away from the

expected percentage change in the portfolio of the currency. In this case, we are assuming

that 0 percent expected change for each currency over the next month and calculating the

maximum one-month loss.

Maximum one-month loss of currency portfolio = E (et ) - ( 1.65 X σP)

= 0% - (1.65 X 6.43%)

= about – 0.1061, or about -10.61%

Comparison of maximum one-month loss

8FINANCE

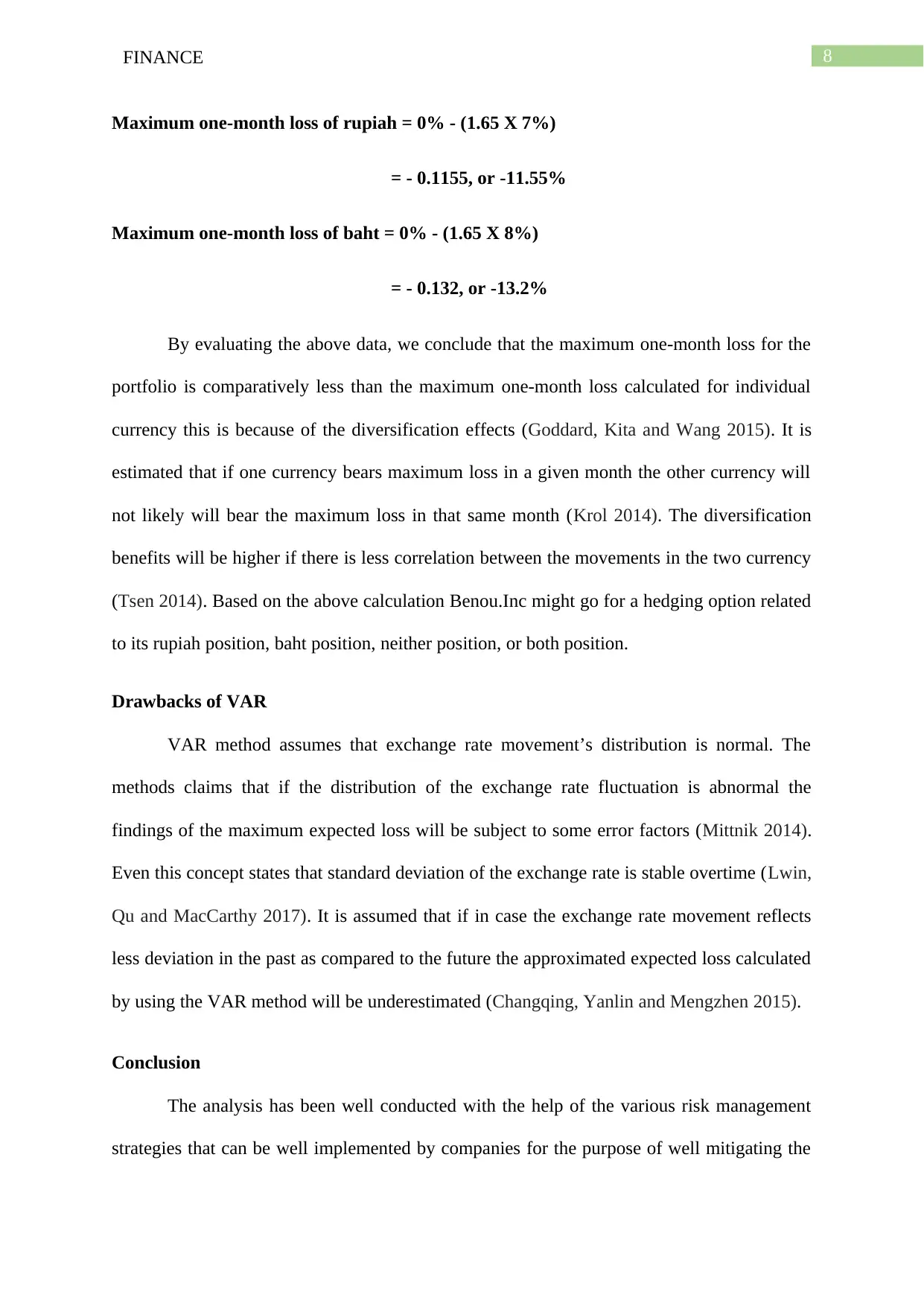

Maximum one-month loss of rupiah = 0% - (1.65 X 7%)

= - 0.1155, or -11.55%

Maximum one-month loss of baht = 0% - (1.65 X 8%)

= - 0.132, or -13.2%

By evaluating the above data, we conclude that the maximum one-month loss for the

portfolio is comparatively less than the maximum one-month loss calculated for individual

currency this is because of the diversification effects (Goddard, Kita and Wang 2015). It is

estimated that if one currency bears maximum loss in a given month the other currency will

not likely will bear the maximum loss in that same month (Krol 2014). The diversification

benefits will be higher if there is less correlation between the movements in the two currency

(Tsen 2014). Based on the above calculation Benou.Inc might go for a hedging option related

to its rupiah position, baht position, neither position, or both position.

Drawbacks of VAR

VAR method assumes that exchange rate movement’s distribution is normal. The

methods claims that if the distribution of the exchange rate fluctuation is abnormal the

findings of the maximum expected loss will be subject to some error factors (Mittnik 2014).

Even this concept states that standard deviation of the exchange rate is stable overtime (Lwin,

Qu and MacCarthy 2017). It is assumed that if in case the exchange rate movement reflects

less deviation in the past as compared to the future the approximated expected loss calculated

by using the VAR method will be underestimated (Changqing, Yanlin and Mengzhen 2015).

Conclusion

The analysis has been well conducted with the help of the various risk management

strategies that can be well implemented by companies for the purpose of well mitigating the

Maximum one-month loss of rupiah = 0% - (1.65 X 7%)

= - 0.1155, or -11.55%

Maximum one-month loss of baht = 0% - (1.65 X 8%)

= - 0.132, or -13.2%

By evaluating the above data, we conclude that the maximum one-month loss for the

portfolio is comparatively less than the maximum one-month loss calculated for individual

currency this is because of the diversification effects (Goddard, Kita and Wang 2015). It is

estimated that if one currency bears maximum loss in a given month the other currency will

not likely will bear the maximum loss in that same month (Krol 2014). The diversification

benefits will be higher if there is less correlation between the movements in the two currency

(Tsen 2014). Based on the above calculation Benou.Inc might go for a hedging option related

to its rupiah position, baht position, neither position, or both position.

Drawbacks of VAR

VAR method assumes that exchange rate movement’s distribution is normal. The

methods claims that if the distribution of the exchange rate fluctuation is abnormal the

findings of the maximum expected loss will be subject to some error factors (Mittnik 2014).

Even this concept states that standard deviation of the exchange rate is stable overtime (Lwin,

Qu and MacCarthy 2017). It is assumed that if in case the exchange rate movement reflects

less deviation in the past as compared to the future the approximated expected loss calculated

by using the VAR method will be underestimated (Changqing, Yanlin and Mengzhen 2015).

Conclusion

The analysis has been well conducted with the help of the various risk management

strategies that can be well implemented by companies for the purpose of well mitigating the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

forex risk that the company faces in their operation. VAR as a key risk management tool can

be well applied for the purpose of well managing or estimating a loss given a set of

probability.

References

Arize, A.C., Andreopoulos, G.C., Kallianiotis, I.N. and Malindretos, J., 2018. MNC

transactions foreign exchange exposure: An application. International Journal of Economics

& Business Administration (IJEBA), 6(1), pp.54-60.

Changqing, L., Yanlin, L. and Mengzhen, L., 2015. Credit portfolio risk evaluation based on

the pair copula VaR models. Journal of Finance and Economics, 3(1), pp.15-30.

Disatnik, D., Duchin, R. and Schmidt, B., 2014. Cash flow hedging and liquidity

choices. Review of Finance, 18(2), pp.715-748.

Dong, L., Kouvelis, P. and Su, P., 2014. Operational hedging strategies and competitive

exposure to exchange rates. International Journal of Production Economics, 153, pp.215-

229.

Fang, W. and Miller, S.M., 2014. Does financial development volatility affect industrial

growth volatility?. International Review of Economics & Finance, 29, pp.307-320.

Goddard, J., Kita, A. and Wang, Q., 2015. Investor attention and FX market

volatility. Journal of International Financial Markets, Institutions and Money, 38, pp.79-96.

Khindanova, I., 2015. Analysis of Foreign Currency Transaction Exposure Using

Simulations. The Journal of Applied Business and Economics, 17(4), p.46.

Krol, R., 2014. Economic policy uncertainty and exchange rate volatility. International

Finance, 17(2), pp.241-256.

forex risk that the company faces in their operation. VAR as a key risk management tool can

be well applied for the purpose of well managing or estimating a loss given a set of

probability.

References

Arize, A.C., Andreopoulos, G.C., Kallianiotis, I.N. and Malindretos, J., 2018. MNC

transactions foreign exchange exposure: An application. International Journal of Economics

& Business Administration (IJEBA), 6(1), pp.54-60.

Changqing, L., Yanlin, L. and Mengzhen, L., 2015. Credit portfolio risk evaluation based on

the pair copula VaR models. Journal of Finance and Economics, 3(1), pp.15-30.

Disatnik, D., Duchin, R. and Schmidt, B., 2014. Cash flow hedging and liquidity

choices. Review of Finance, 18(2), pp.715-748.

Dong, L., Kouvelis, P. and Su, P., 2014. Operational hedging strategies and competitive

exposure to exchange rates. International Journal of Production Economics, 153, pp.215-

229.

Fang, W. and Miller, S.M., 2014. Does financial development volatility affect industrial

growth volatility?. International Review of Economics & Finance, 29, pp.307-320.

Goddard, J., Kita, A. and Wang, Q., 2015. Investor attention and FX market

volatility. Journal of International Financial Markets, Institutions and Money, 38, pp.79-96.

Khindanova, I., 2015. Analysis of Foreign Currency Transaction Exposure Using

Simulations. The Journal of Applied Business and Economics, 17(4), p.46.

Krol, R., 2014. Economic policy uncertainty and exchange rate volatility. International

Finance, 17(2), pp.241-256.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

Lwin, K.T., Qu, R. and MacCarthy, B.L., 2017. Mean-VaR portfolio optimization: A

nonparametric approach. European Journal of Operational Research, 260(2), pp.751-766.

Mittnik, S., 2014. VaR-implied tail-correlation matrices. Economics Letters, 122(1), pp.69-

73.

Mumtaz, H. and Theodoridis, K., 2015. The international transmission of volatility shocks:

An empirical analysis. Journal of the European Economic Association, 13(3), pp.512-533.

Tsen, W.H., 2014. Exchange rate volatility and international trade. J Stock Forex Trad, 3(2).

Lwin, K.T., Qu, R. and MacCarthy, B.L., 2017. Mean-VaR portfolio optimization: A

nonparametric approach. European Journal of Operational Research, 260(2), pp.751-766.

Mittnik, S., 2014. VaR-implied tail-correlation matrices. Economics Letters, 122(1), pp.69-

73.

Mumtaz, H. and Theodoridis, K., 2015. The international transmission of volatility shocks:

An empirical analysis. Journal of the European Economic Association, 13(3), pp.512-533.

Tsen, W.H., 2014. Exchange rate volatility and international trade. J Stock Forex Trad, 3(2).

11FINANCE

Appendix

Assessment of Exposure via VAR

Particulars Formuala

s

Maximum one day loss:

E (et ) -

( 1.65 X σ

MXP)

0% - (1.65 X 1.2%)

-0.0198

Peso value based on maximum one-day loss

S X [1 + E

(et )]

$ 0.09 X [1 + (- 0.0198)]

$ 0.08821800

Factors Affecting Maximum One-Day Loss

Maximum one-day loss at 95% Level

E (et ) -

( 1.65 X σ

MXP)

Whereby E(et) is assumed to be -2%

- 2% - (1.65 X 1.2%)

-2.18%

Maximum one-day loss at 97.5% Level

E (et ) -

( 1.96 X σ

MXP)

0% - (1.96 X 1.2%)

-2.352%

Change of SD to 1% from 1.2%

Maximum one day loss

E (et ) -

( 1.65 X σ

MXP)

0% - (1.65 X 1%)

-1.65%

Appendix

Assessment of Exposure via VAR

Particulars Formuala

s

Maximum one day loss:

E (et ) -

( 1.65 X σ

MXP)

0% - (1.65 X 1.2%)

-0.0198

Peso value based on maximum one-day loss

S X [1 + E

(et )]

$ 0.09 X [1 + (- 0.0198)]

$ 0.08821800

Factors Affecting Maximum One-Day Loss

Maximum one-day loss at 95% Level

E (et ) -

( 1.65 X σ

MXP)

Whereby E(et) is assumed to be -2%

- 2% - (1.65 X 1.2%)

-2.18%

Maximum one-day loss at 97.5% Level

E (et ) -

( 1.96 X σ

MXP)

0% - (1.96 X 1.2%)

-2.352%

Change of SD to 1% from 1.2%

Maximum one day loss

E (et ) -

( 1.65 X σ

MXP)

0% - (1.65 X 1%)

-1.65%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.