International and Business Taxation: Singapore & China Analysis Report

VerifiedAdded on 2021/06/15

|26

|4153

|62

Report

AI Summary

This report examines the international and business taxation aspects of a private limited company based in Australia considering expansion into Singapore, with a production unit in China. It explores Singapore's tax jurisdiction, including corporate tax rates, goods and services tax, stamp duties, and property taxes, as well as various tax incentives. The report analyzes the aims and objectives of overseas expansion, focusing on Singapore's attractive investment climate, political stability, and tax benefits. It delves into the taxation of business profits, double taxation relief, tax treaties, and anti-avoidance rules, particularly transfer pricing. The report also considers the financing of business operations, the economic landscapes of Singapore and China, cultural and social norms, and the benefits of investing in Singapore, providing recommendations and a conclusion based on the analysis. The report also includes a detailed financial analysis and the impact of taxation on shareholders.

Running head: INTERNATIONAL AND BUSINESS TAXATION

International Business Taxation

Name of the Student

Name of the University

Authors Note

Course ID

International Business Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL AND BUSINESS TAXATION

Table of Contents

Introduction:...............................................................................................................................3

Aims and Objective of Overseas Expansion:.............................................................................3

Tax Jurisdiction of Singapore:...................................................................................................4

Taxation of Business Profits:.................................................................................................4

Double Taxation Relief:.............................................................................................................7

Unilateral Relief:....................................................................................................................7

Tax treaties:............................................................................................................................8

Anti-Avoidance Rules:...........................................................................................................9

Transfer pricing:.....................................................................................................................9

Transfer pricing Documentations in China:.........................................................................16

Financing of Business Operations:...........................................................................................17

Commercial Reality of Scenario:.............................................................................................18

Singapore Economy:................................................................................................................18

Economy of China................................................................................................................19

Complexity of Issues:...............................................................................................................19

Relevant Culture and Social Norms:........................................................................................19

Alternative decisions of not investing in Singapore and Staying in Australia:........................20

Benefits of Investing in Singapore:..........................................................................................21

Recommendations:...................................................................................................................21

Conclusion:..............................................................................................................................22

Table of Contents

Introduction:...............................................................................................................................3

Aims and Objective of Overseas Expansion:.............................................................................3

Tax Jurisdiction of Singapore:...................................................................................................4

Taxation of Business Profits:.................................................................................................4

Double Taxation Relief:.............................................................................................................7

Unilateral Relief:....................................................................................................................7

Tax treaties:............................................................................................................................8

Anti-Avoidance Rules:...........................................................................................................9

Transfer pricing:.....................................................................................................................9

Transfer pricing Documentations in China:.........................................................................16

Financing of Business Operations:...........................................................................................17

Commercial Reality of Scenario:.............................................................................................18

Singapore Economy:................................................................................................................18

Economy of China................................................................................................................19

Complexity of Issues:...............................................................................................................19

Relevant Culture and Social Norms:........................................................................................19

Alternative decisions of not investing in Singapore and Staying in Australia:........................20

Benefits of Investing in Singapore:..........................................................................................21

Recommendations:...................................................................................................................21

Conclusion:..............................................................................................................................22

2INTERNATIONAL AND BUSINESS TAXATION

Reference List:.........................................................................................................................23

Reference List:.........................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL AND BUSINESS TAXATION

Introduction:

Private business are spending a large number of amount on managing their existence

along with the allocation of income through permanent establishment. Frequently, numerous

business departments are engaged in dealing with the probable exposure or employing some

of the opportunities to structure the organization more effectively1. As evident in the current

station for a private limited company that is based in Australia can consider establishing the

business in Singapore. The principle taxes that are levied on the companies that conduct their

business in Singapore are the income, taxes, goods and service tax, stamp duties and property

taxes. The report would be taking into consideration the benefits of establishing the business

in Singapore with numerous tax incentive provided for the business setting up the business in

Singapore.

The report is based on the private limited company that has 40 shareholders carrying

out the business activities in cosmetics and skin care. With the management objective of

expanding the business in the Asian market and setting up the subsidiary in Singapore with

production unit china, the report would seek to understand the tax environment of Singapore

with tax incentive scheme for making investment in Singapore2.

Aims and Objective of Overseas Expansion:

The aim of the cosmetics and skin care is to expand into the Singapore market.

Singapore provides strong climate for investment, political stability, free business economy,

readily available financial and professional support service and attractive tax incentive for

1 Zwick, Eric, and James Mahon. "Tax policy and heterogeneous investment

behavior." Australian Economic Review 107.1 (2017): 217-48.

2 Liu, Qing, and Yi Lu. "Firm investment and exporting: Evidence from China's value-added

tax reform." Journal of International Economics 97.2 (2015): 392-403.

Introduction:

Private business are spending a large number of amount on managing their existence

along with the allocation of income through permanent establishment. Frequently, numerous

business departments are engaged in dealing with the probable exposure or employing some

of the opportunities to structure the organization more effectively1. As evident in the current

station for a private limited company that is based in Australia can consider establishing the

business in Singapore. The principle taxes that are levied on the companies that conduct their

business in Singapore are the income, taxes, goods and service tax, stamp duties and property

taxes. The report would be taking into consideration the benefits of establishing the business

in Singapore with numerous tax incentive provided for the business setting up the business in

Singapore.

The report is based on the private limited company that has 40 shareholders carrying

out the business activities in cosmetics and skin care. With the management objective of

expanding the business in the Asian market and setting up the subsidiary in Singapore with

production unit china, the report would seek to understand the tax environment of Singapore

with tax incentive scheme for making investment in Singapore2.

Aims and Objective of Overseas Expansion:

The aim of the cosmetics and skin care is to expand into the Singapore market.

Singapore provides strong climate for investment, political stability, free business economy,

readily available financial and professional support service and attractive tax incentive for

1 Zwick, Eric, and James Mahon. "Tax policy and heterogeneous investment

behavior." Australian Economic Review 107.1 (2017): 217-48.

2 Liu, Qing, and Yi Lu. "Firm investment and exporting: Evidence from China's value-added

tax reform." Journal of International Economics 97.2 (2015): 392-403.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL AND BUSINESS TAXATION

subsidiaries3. The competition commission of Singapore is tasked prohibits the unfair or the

abusive pricing practices and aims to maintain the competition in the market.

Additionally Singapore may be considered as the desirable jurisdiction for the making

investment primary because of the attractive corporative tax rates and tax incentive4.

Furthermore, the absence of capital gains tax and broad network of treaty setting the business

of cosmetics and skin care is relatively easy in Singapore.

Tax Jurisdiction of Singapore:

Taxation of Business Profits:

The tax system of Singapore is based on the quasi-territorial basis which means that

companies that look forward to conduct their business in Singapore would be taxed based on

the accrued basis for the incomes derived from Singapore sources5. An important factor to

denote that Singapore does not create any differential between the business that are carried on

in Singapore by the residents or by the non-residents. Exemptions are also applicable for the

foreign sources income. All the Singapore sourced income that is earned by the non-residents

are held taxable however the tax treaty exemption between Singapore and Australia helps in

easing off the burden of taxes.

3 Poh, Simon. "R&D tax incentives in Singapore." Nexia International (2016).

4 Agarwal, Sumit, Nathan Marwell, and Leslie McGranahan. "Consumption responses to

temporary tax incentives: Evidence from state sales tax holidays." American Economic

Journal: Economic Policy 9.4 (2017): 1-27.

5 Wiedemann, Verena, and Katharina Finke. Taxing investments in the Asia-Pacific region:

The importance of cross-border taxation and tax incentives. No. 15-014. ZEW Discussion

Papers, 2015.

subsidiaries3. The competition commission of Singapore is tasked prohibits the unfair or the

abusive pricing practices and aims to maintain the competition in the market.

Additionally Singapore may be considered as the desirable jurisdiction for the making

investment primary because of the attractive corporative tax rates and tax incentive4.

Furthermore, the absence of capital gains tax and broad network of treaty setting the business

of cosmetics and skin care is relatively easy in Singapore.

Tax Jurisdiction of Singapore:

Taxation of Business Profits:

The tax system of Singapore is based on the quasi-territorial basis which means that

companies that look forward to conduct their business in Singapore would be taxed based on

the accrued basis for the incomes derived from Singapore sources5. An important factor to

denote that Singapore does not create any differential between the business that are carried on

in Singapore by the residents or by the non-residents. Exemptions are also applicable for the

foreign sources income. All the Singapore sourced income that is earned by the non-residents

are held taxable however the tax treaty exemption between Singapore and Australia helps in

easing off the burden of taxes.

3 Poh, Simon. "R&D tax incentives in Singapore." Nexia International (2016).

4 Agarwal, Sumit, Nathan Marwell, and Leslie McGranahan. "Consumption responses to

temporary tax incentives: Evidence from state sales tax holidays." American Economic

Journal: Economic Policy 9.4 (2017): 1-27.

5 Wiedemann, Verena, and Katharina Finke. Taxing investments in the Asia-Pacific region:

The importance of cross-border taxation and tax incentives. No. 15-014. ZEW Discussion

Papers, 2015.

5INTERNATIONAL AND BUSINESS TAXATION

The tax burden in Singapore is regarded as moderate in comparison to other countries

and can foreign entities business profits can be reduced with the help of numerous

incentives6. The income tax act of Singapore is regarded as the governing statute relating to

the corporate profits which is administered by the Inland Revenue authority of Singapore.

Moving fast forward to the Singapore quick tax facts for companies a corporate tax rate of

17% is applicable along with this a partial exemption is provided to the companies for the

first SGD 300,000 of the assessable income.

Singapore levies a very moderate branch tax rate of 17% with the partial exemption

is provided to the companies for the first SGD 300,000 of the taxable business profits. One

of the advantage for the business is that there is no capital gains tax in Singapore7. Singapore

provides the business with the loss relief as well. The tax system of Singapore is such that a

loss relief is provided and a business can carry forward the loss for an indefinite years. The

Singapore tax environment provides the double taxation relief as business can avoid taxing of

profits both at the source nations and at the overseas nation.

Business expenditure are generally considered as allowable deductions in computing

the taxable income, given the associated activities are directed towards the derivation of

income8. In order to promote the development of the enterprise expenditure that are incurred

entirely for the production of income might be considered deductible in determining the

assessable income. The 17% corporate rate is applicable for the subsidiary companies that are

incorporated in Singapore and to the foreign nations companies that set up the business

6 Li, Quan. "Fiscal decentralization and tax incentives in the developing world." Review of

International Political Economy23.2 (2016): 232-260.

7 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

8 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

The tax burden in Singapore is regarded as moderate in comparison to other countries

and can foreign entities business profits can be reduced with the help of numerous

incentives6. The income tax act of Singapore is regarded as the governing statute relating to

the corporate profits which is administered by the Inland Revenue authority of Singapore.

Moving fast forward to the Singapore quick tax facts for companies a corporate tax rate of

17% is applicable along with this a partial exemption is provided to the companies for the

first SGD 300,000 of the assessable income.

Singapore levies a very moderate branch tax rate of 17% with the partial exemption

is provided to the companies for the first SGD 300,000 of the taxable business profits. One

of the advantage for the business is that there is no capital gains tax in Singapore7. Singapore

provides the business with the loss relief as well. The tax system of Singapore is such that a

loss relief is provided and a business can carry forward the loss for an indefinite years. The

Singapore tax environment provides the double taxation relief as business can avoid taxing of

profits both at the source nations and at the overseas nation.

Business expenditure are generally considered as allowable deductions in computing

the taxable income, given the associated activities are directed towards the derivation of

income8. In order to promote the development of the enterprise expenditure that are incurred

entirely for the production of income might be considered deductible in determining the

assessable income. The 17% corporate rate is applicable for the subsidiary companies that are

incorporated in Singapore and to the foreign nations companies that set up the business

6 Li, Quan. "Fiscal decentralization and tax incentives in the developing world." Review of

International Political Economy23.2 (2016): 232-260.

7 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

8 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL AND BUSINESS TAXATION

operations in Singapore. Setting the business in Singapore is regarded as beneficial as

Singapore performs the one-tire corporate tax rate system where the corporate taxes are paid

on the profits of the company.

The private companies that set up the business in Singapore are provided exemption

on tax for the first 100,000 SGD on the normal assessable income with 50% exemption on

the subsequent 200,000 of the assessable income9. The exemption is applicable to the new

business that looks forward to set up the business in Singapore and the exemptions are

provided for the first three years of the business operations.

First Three Years of Tax Filing

Taxable Income (S$) Tax Rate

0 – 100,000 0%

100,001 – 300,000 8.50%

300,001 – 2,000,000 17%

AFTER FIRST THREE YEARS OF INCOME TAX FILINGS

TAXABLE INCOME (S$) Tax Rate

0 – 300,000 8.50%

300,001 – 2,000,000 17%

As evident from the above stated tabular representation 17% corporate tax rates would

be applicable to the company since it is a subsidiaries to Australia that are incorporated in

Singapore10. The cosmetics and skin care business of the private company would also be able

to a partial exemption of 75% on the first SGD 10,000 based on the normal taxable income

and cosmetics business would also be entitled to 50% exemption on the following SGD

9 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

10 Tan, Lin Mei, Valerie Braithwaite, and Monika Reinhart. "Why do small business

taxpayers stay with their practitioners? Trust, competence and aggressive

advice." International Small Business Journal 34.3 (2016): 329-344.

operations in Singapore. Setting the business in Singapore is regarded as beneficial as

Singapore performs the one-tire corporate tax rate system where the corporate taxes are paid

on the profits of the company.

The private companies that set up the business in Singapore are provided exemption

on tax for the first 100,000 SGD on the normal assessable income with 50% exemption on

the subsequent 200,000 of the assessable income9. The exemption is applicable to the new

business that looks forward to set up the business in Singapore and the exemptions are

provided for the first three years of the business operations.

First Three Years of Tax Filing

Taxable Income (S$) Tax Rate

0 – 100,000 0%

100,001 – 300,000 8.50%

300,001 – 2,000,000 17%

AFTER FIRST THREE YEARS OF INCOME TAX FILINGS

TAXABLE INCOME (S$) Tax Rate

0 – 300,000 8.50%

300,001 – 2,000,000 17%

As evident from the above stated tabular representation 17% corporate tax rates would

be applicable to the company since it is a subsidiaries to Australia that are incorporated in

Singapore10. The cosmetics and skin care business of the private company would also be able

to a partial exemption of 75% on the first SGD 10,000 based on the normal taxable income

and cosmetics business would also be entitled to 50% exemption on the following SGD

9 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

10 Tan, Lin Mei, Valerie Braithwaite, and Monika Reinhart. "Why do small business

taxpayers stay with their practitioners? Trust, competence and aggressive

advice." International Small Business Journal 34.3 (2016): 329-344.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL AND BUSINESS TAXATION

290,000. Furthermore the cosmetics business would be granted a partial tax exemption for the

first SGD 300,000 of the normal assessable income. For example if the cosmetics and skin

care business reports an annual turnover of SGD 2 million with net assessable income of

500,000 SGG then the applicable tax for the private business would be SGS 85,000.

First Year Income Tax Filings

Particulars Tax Rate Amount

Taxable Income (S$) 5,00,000

Tax on Taxable Income 17.50% 85000

Total tax payable 85000

Double Taxation Relief:

Unilateral Relief:

Singapore provides unilateral tax credits for the foreign tax paid by the overseas

companies deriving foreign income. The credit is restricted to the tax that is payable in

Singapore even though foreign tax liability is higher11. If the cosmetics and the skin care

business owns a minimum of 25 per cent of the share capital then the foreign tax credit would

take into the consideration the underlying amount of corporate that would be paid by the

business on the profits generated. The foreign tax credit system would allow the cosmetics

and skin Care Company to pool the foreign tax that is paid in Australia and the same can be

offset against the Singapore tax that would be payable on the same pool of foreign source

income.

Tax treaties:

Setting up the Cosmetics and Skin Care Company in Singapore could be considered

as the viable options since Singapore has wide range of tax treaty network. The treaties of

11 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

290,000. Furthermore the cosmetics business would be granted a partial tax exemption for the

first SGD 300,000 of the normal assessable income. For example if the cosmetics and skin

care business reports an annual turnover of SGD 2 million with net assessable income of

500,000 SGG then the applicable tax for the private business would be SGS 85,000.

First Year Income Tax Filings

Particulars Tax Rate Amount

Taxable Income (S$) 5,00,000

Tax on Taxable Income 17.50% 85000

Total tax payable 85000

Double Taxation Relief:

Unilateral Relief:

Singapore provides unilateral tax credits for the foreign tax paid by the overseas

companies deriving foreign income. The credit is restricted to the tax that is payable in

Singapore even though foreign tax liability is higher11. If the cosmetics and the skin care

business owns a minimum of 25 per cent of the share capital then the foreign tax credit would

take into the consideration the underlying amount of corporate that would be paid by the

business on the profits generated. The foreign tax credit system would allow the cosmetics

and skin Care Company to pool the foreign tax that is paid in Australia and the same can be

offset against the Singapore tax that would be payable on the same pool of foreign source

income.

Tax treaties:

Setting up the Cosmetics and Skin Care Company in Singapore could be considered

as the viable options since Singapore has wide range of tax treaty network. The treaties of

11 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

8INTERNATIONAL AND BUSINESS TAXATION

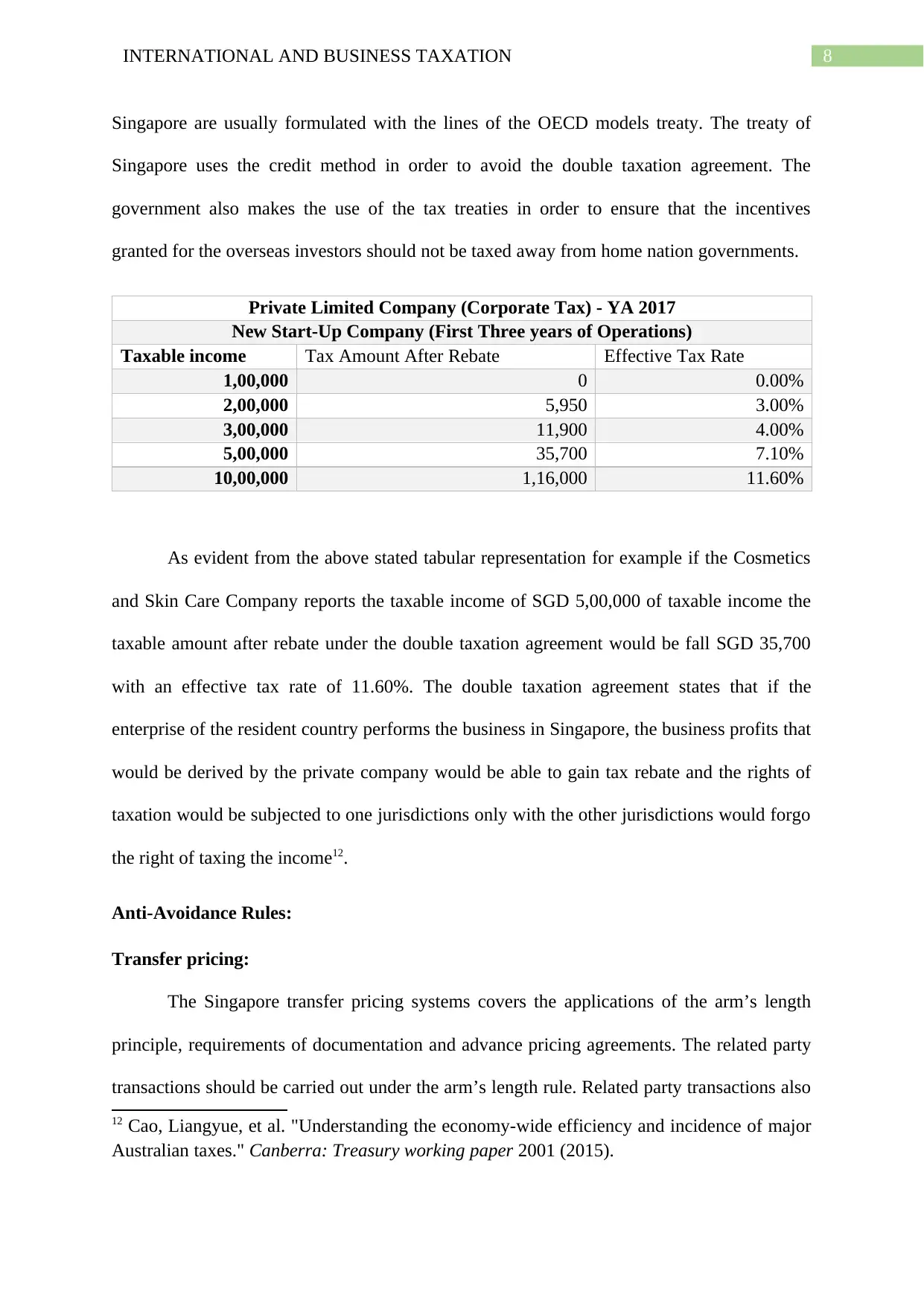

Singapore are usually formulated with the lines of the OECD models treaty. The treaty of

Singapore uses the credit method in order to avoid the double taxation agreement. The

government also makes the use of the tax treaties in order to ensure that the incentives

granted for the overseas investors should not be taxed away from home nation governments.

Private Limited Company (Corporate Tax) - YA 2017

New Start-Up Company (First Three years of Operations)

Taxable income Tax Amount After Rebate Effective Tax Rate

1,00,000 0 0.00%

2,00,000 5,950 3.00%

3,00,000 11,900 4.00%

5,00,000 35,700 7.10%

10,00,000 1,16,000 11.60%

As evident from the above stated tabular representation for example if the Cosmetics

and Skin Care Company reports the taxable income of SGD 5,00,000 of taxable income the

taxable amount after rebate under the double taxation agreement would be fall SGD 35,700

with an effective tax rate of 11.60%. The double taxation agreement states that if the

enterprise of the resident country performs the business in Singapore, the business profits that

would be derived by the private company would be able to gain tax rebate and the rights of

taxation would be subjected to one jurisdictions only with the other jurisdictions would forgo

the right of taxing the income12.

Anti-Avoidance Rules:

Transfer pricing:

The Singapore transfer pricing systems covers the applications of the arm’s length

principle, requirements of documentation and advance pricing agreements. The related party

transactions should be carried out under the arm’s length rule. Related party transactions also

12 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Canberra: Treasury working paper 2001 (2015).

Singapore are usually formulated with the lines of the OECD models treaty. The treaty of

Singapore uses the credit method in order to avoid the double taxation agreement. The

government also makes the use of the tax treaties in order to ensure that the incentives

granted for the overseas investors should not be taxed away from home nation governments.

Private Limited Company (Corporate Tax) - YA 2017

New Start-Up Company (First Three years of Operations)

Taxable income Tax Amount After Rebate Effective Tax Rate

1,00,000 0 0.00%

2,00,000 5,950 3.00%

3,00,000 11,900 4.00%

5,00,000 35,700 7.10%

10,00,000 1,16,000 11.60%

As evident from the above stated tabular representation for example if the Cosmetics

and Skin Care Company reports the taxable income of SGD 5,00,000 of taxable income the

taxable amount after rebate under the double taxation agreement would be fall SGD 35,700

with an effective tax rate of 11.60%. The double taxation agreement states that if the

enterprise of the resident country performs the business in Singapore, the business profits that

would be derived by the private company would be able to gain tax rebate and the rights of

taxation would be subjected to one jurisdictions only with the other jurisdictions would forgo

the right of taxing the income12.

Anti-Avoidance Rules:

Transfer pricing:

The Singapore transfer pricing systems covers the applications of the arm’s length

principle, requirements of documentation and advance pricing agreements. The related party

transactions should be carried out under the arm’s length rule. Related party transactions also

12 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Canberra: Treasury working paper 2001 (2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL AND BUSINESS TAXATION

comprises of the enterprise that are taxed separately at the entity level and generally includes

the permanent establishment of the enterprise13. For a private company that is carrying on the

business of cosmetics and skin care is required to make sure that the intercompany

transactions are carried out based on the arm’s length principles.

The transfer pricing agreements also requires preparation of the documents to avoid

any probable tax adjustment by the Inland Revenue Authority of Singapore14. The tax

jurisdictional of Singapore requires preparation of transfer pricing documentation that would

form the part of the record-keeping requirements for taxation purpose and companies are

prepare such documents no later than the tax filing date.

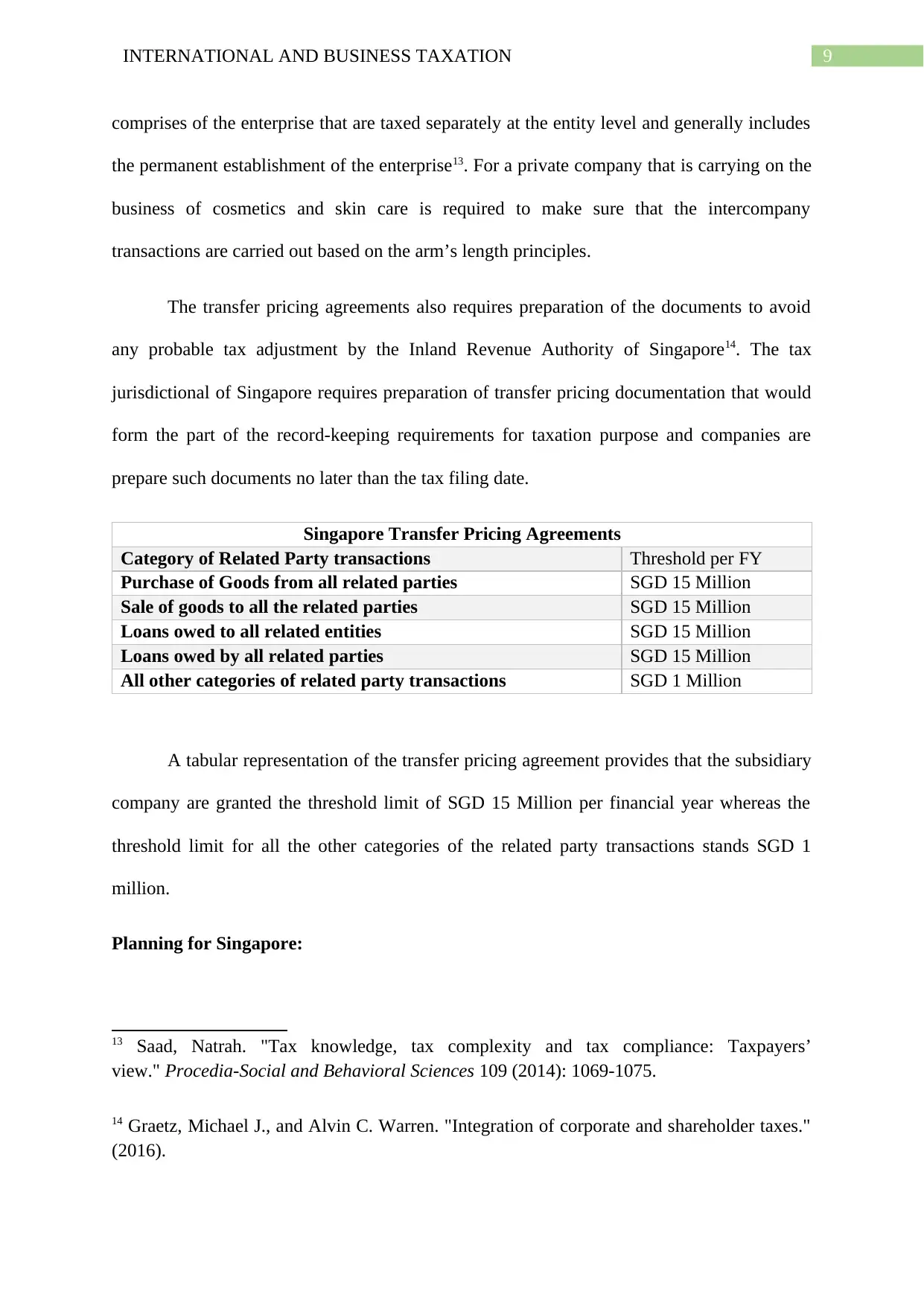

Singapore Transfer Pricing Agreements

Category of Related Party transactions Threshold per FY

Purchase of Goods from all related parties SGD 15 Million

Sale of goods to all the related parties SGD 15 Million

Loans owed to all related entities SGD 15 Million

Loans owed by all related parties SGD 15 Million

All other categories of related party transactions SGD 1 Million

A tabular representation of the transfer pricing agreement provides that the subsidiary

company are granted the threshold limit of SGD 15 Million per financial year whereas the

threshold limit for all the other categories of the related party transactions stands SGD 1

million.

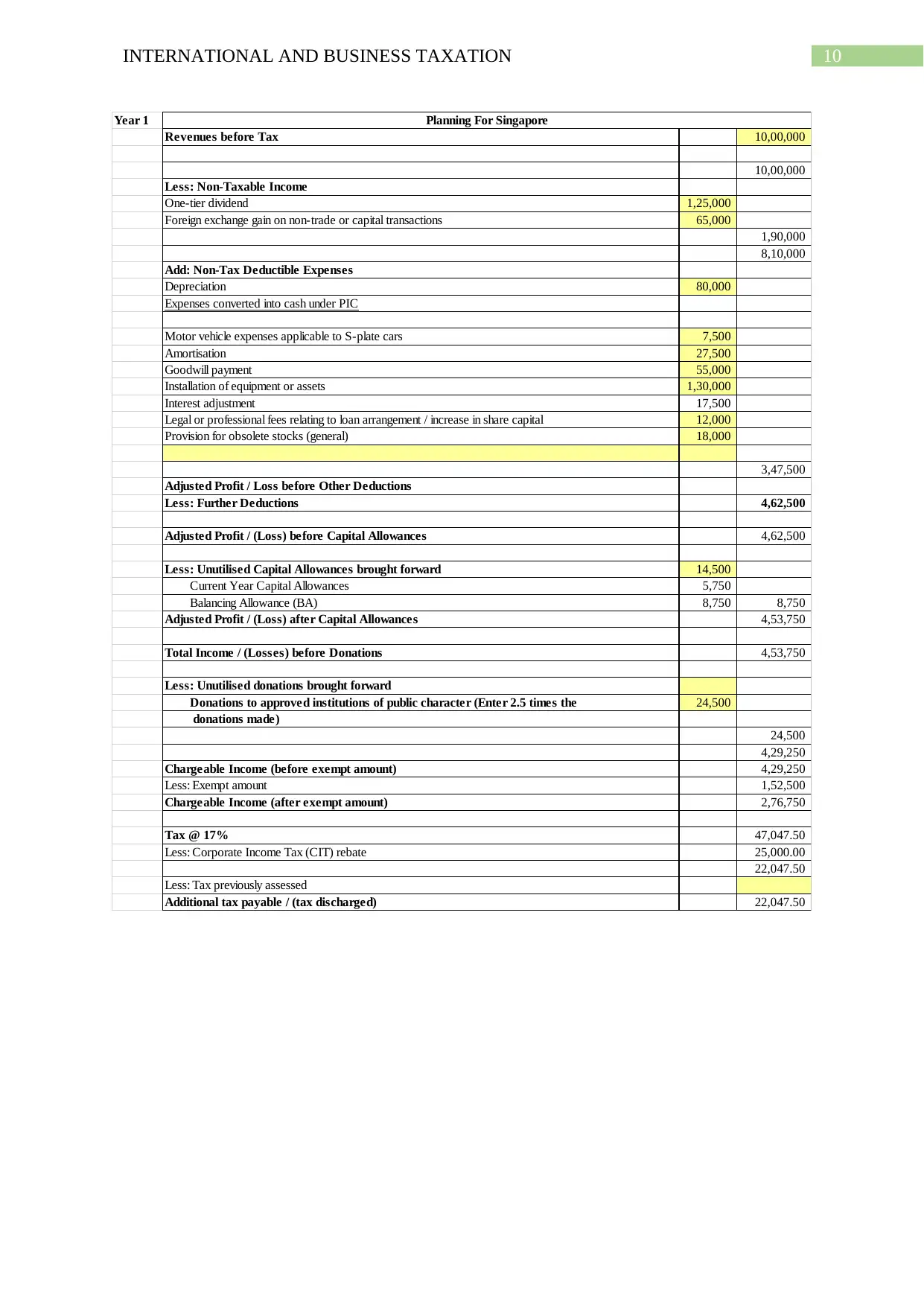

Planning for Singapore:

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

14 Graetz, Michael J., and Alvin C. Warren. "Integration of corporate and shareholder taxes."

(2016).

comprises of the enterprise that are taxed separately at the entity level and generally includes

the permanent establishment of the enterprise13. For a private company that is carrying on the

business of cosmetics and skin care is required to make sure that the intercompany

transactions are carried out based on the arm’s length principles.

The transfer pricing agreements also requires preparation of the documents to avoid

any probable tax adjustment by the Inland Revenue Authority of Singapore14. The tax

jurisdictional of Singapore requires preparation of transfer pricing documentation that would

form the part of the record-keeping requirements for taxation purpose and companies are

prepare such documents no later than the tax filing date.

Singapore Transfer Pricing Agreements

Category of Related Party transactions Threshold per FY

Purchase of Goods from all related parties SGD 15 Million

Sale of goods to all the related parties SGD 15 Million

Loans owed to all related entities SGD 15 Million

Loans owed by all related parties SGD 15 Million

All other categories of related party transactions SGD 1 Million

A tabular representation of the transfer pricing agreement provides that the subsidiary

company are granted the threshold limit of SGD 15 Million per financial year whereas the

threshold limit for all the other categories of the related party transactions stands SGD 1

million.

Planning for Singapore:

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

14 Graetz, Michael J., and Alvin C. Warren. "Integration of corporate and shareholder taxes."

(2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNATIONAL AND BUSINESS TAXATION

Year 1

Revenues before Tax 10,00,000

10,00,000

Less: Non-Taxable Income

One-tier dividend 1,25,000

Foreign exchange gain on non-trade or capital transactions 65,000

1,90,000

8,10,000

Add: Non-Tax Deductible Expenses

Depreciation 80,000

Expenses converted into cash under PIC

Motor vehicle expenses applicable to S-plate cars 7,500

Amortisation 27,500

Goodwill payment 55,000

Installation of equipment or assets 1,30,000

Interest adjustment 17,500

Legal or professional fees relating to loan arrangement / increase in share capital 12,000

Provision for obsolete stocks (general) 18,000

3,47,500

Adjusted Profit / Loss before Other Deductions

Less: Further Deductions 4,62,500

Adjusted Profit / (Loss) before Capital Allowances 4,62,500

Less: Unutilised Capital Allowances brought forward 14,500

Current Year Capital Allowances 5,750

Balancing Allowance (BA) 8,750 8,750

Adjusted Profit / (Loss) after Capital Allowances 4,53,750

Total Income / (Losses) before Donations 4,53,750

Less: Unutilised donations brought forward

Donations to approved institutions of public character (Enter 2.5 times the 24,500

donations made)

24,500

4,29,250

Chargeable Income (before exempt amount) 4,29,250

Less: Exempt amount 1,52,500

Chargeable Income (after exempt amount) 2,76,750

Tax @ 17% 47,047.50

Less: Corporate Income Tax (CIT) rebate 25,000.00

22,047.50

Less: Tax previously assessed

Additional tax payable / (tax discharged) 22,047.50

Planning For Singapore

Year 1

Revenues before Tax 10,00,000

10,00,000

Less: Non-Taxable Income

One-tier dividend 1,25,000

Foreign exchange gain on non-trade or capital transactions 65,000

1,90,000

8,10,000

Add: Non-Tax Deductible Expenses

Depreciation 80,000

Expenses converted into cash under PIC

Motor vehicle expenses applicable to S-plate cars 7,500

Amortisation 27,500

Goodwill payment 55,000

Installation of equipment or assets 1,30,000

Interest adjustment 17,500

Legal or professional fees relating to loan arrangement / increase in share capital 12,000

Provision for obsolete stocks (general) 18,000

3,47,500

Adjusted Profit / Loss before Other Deductions

Less: Further Deductions 4,62,500

Adjusted Profit / (Loss) before Capital Allowances 4,62,500

Less: Unutilised Capital Allowances brought forward 14,500

Current Year Capital Allowances 5,750

Balancing Allowance (BA) 8,750 8,750

Adjusted Profit / (Loss) after Capital Allowances 4,53,750

Total Income / (Losses) before Donations 4,53,750

Less: Unutilised donations brought forward

Donations to approved institutions of public character (Enter 2.5 times the 24,500

donations made)

24,500

4,29,250

Chargeable Income (before exempt amount) 4,29,250

Less: Exempt amount 1,52,500

Chargeable Income (after exempt amount) 2,76,750

Tax @ 17% 47,047.50

Less: Corporate Income Tax (CIT) rebate 25,000.00

22,047.50

Less: Tax previously assessed

Additional tax payable / (tax discharged) 22,047.50

Planning For Singapore

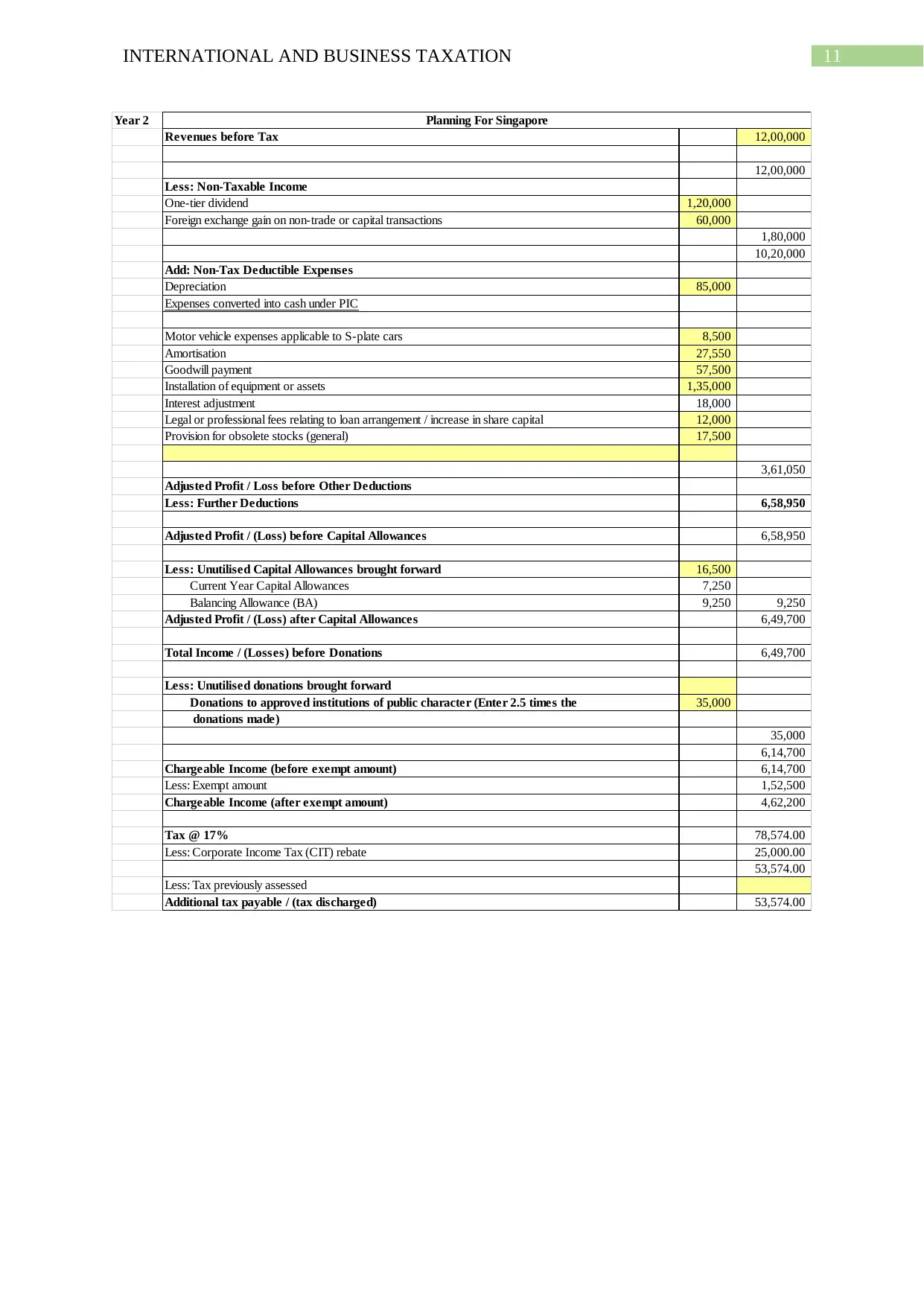

11INTERNATIONAL AND BUSINESS TAXATION

Year 2

Revenues before Tax 12,00,000

12,00,000

Less: Non-Taxable Income

One-tier dividend 1,20,000

Foreign exchange gain on non-trade or capital transactions 60,000

1,80,000

10,20,000

Add: Non-Tax Deductible Expenses

Depreciation 85,000

Expenses converted into cash under PIC

Motor vehicle expenses applicable to S-plate cars 8,500

Amortisation 27,550

Goodwill payment 57,500

Installation of equipment or assets 1,35,000

Interest adjustment 18,000

Legal or professional fees relating to loan arrangement / increase in share capital 12,000

Provision for obsolete stocks (general) 17,500

3,61,050

Adjusted Profit / Loss before Other Deductions

Less: Further Deductions 6,58,950

Adjusted Profit / (Loss) before Capital Allowances 6,58,950

Less: Unutilised Capital Allowances brought forward 16,500

Current Year Capital Allowances 7,250

Balancing Allowance (BA) 9,250 9,250

Adjusted Profit / (Loss) after Capital Allowances 6,49,700

Total Income / (Losses) before Donations 6,49,700

Less: Unutilised donations brought forward

Donations to approved institutions of public character (Enter 2.5 times the 35,000

donations made)

35,000

6,14,700

Chargeable Income (before exempt amount) 6,14,700

Less: Exempt amount 1,52,500

Chargeable Income (after exempt amount) 4,62,200

Tax @ 17% 78,574.00

Less: Corporate Income Tax (CIT) rebate 25,000.00

53,574.00

Less: Tax previously assessed

Additional tax payable / (tax discharged) 53,574.00

Planning For Singapore

Year 2

Revenues before Tax 12,00,000

12,00,000

Less: Non-Taxable Income

One-tier dividend 1,20,000

Foreign exchange gain on non-trade or capital transactions 60,000

1,80,000

10,20,000

Add: Non-Tax Deductible Expenses

Depreciation 85,000

Expenses converted into cash under PIC

Motor vehicle expenses applicable to S-plate cars 8,500

Amortisation 27,550

Goodwill payment 57,500

Installation of equipment or assets 1,35,000

Interest adjustment 18,000

Legal or professional fees relating to loan arrangement / increase in share capital 12,000

Provision for obsolete stocks (general) 17,500

3,61,050

Adjusted Profit / Loss before Other Deductions

Less: Further Deductions 6,58,950

Adjusted Profit / (Loss) before Capital Allowances 6,58,950

Less: Unutilised Capital Allowances brought forward 16,500

Current Year Capital Allowances 7,250

Balancing Allowance (BA) 9,250 9,250

Adjusted Profit / (Loss) after Capital Allowances 6,49,700

Total Income / (Losses) before Donations 6,49,700

Less: Unutilised donations brought forward

Donations to approved institutions of public character (Enter 2.5 times the 35,000

donations made)

35,000

6,14,700

Chargeable Income (before exempt amount) 6,14,700

Less: Exempt amount 1,52,500

Chargeable Income (after exempt amount) 4,62,200

Tax @ 17% 78,574.00

Less: Corporate Income Tax (CIT) rebate 25,000.00

53,574.00

Less: Tax previously assessed

Additional tax payable / (tax discharged) 53,574.00

Planning For Singapore

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.