International Finance Report: Brambles and CSL Analysis

VerifiedAdded on 2021/04/21

|15

|2831

|26

Report

AI Summary

This report provides an analysis of international finance, focusing on currency exchange and investment strategies. It begins by evaluating a company's decision to invest in Thailand, considering the impact of interest rates and currency depreciation on potential returns. The report then delves into a case study of Brambles Limited and CSL Ltd, examining their foreign exchange risk management strategies, revenue generation across different geographical areas, and the correlation between their share prices and the USD/AUD exchange rate. The analysis includes recommendations for secondary listings on stock exchanges to enhance capital raising and mitigate market fluctuations. Finally, the report provides a detailed comparison of the two companies and their approaches to international financial management, supported by relevant data and references.

Running head: INTERNATIONAL FINANCE

International finance

Name of the Student:

Name of the university:

Authors note:

International finance

Name of the Student:

Name of the university:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL FINANCE

Table of Contents

PART A:.....................................................................................................................................2

Answer to question1...................................................................................................................2

Answer to question 2..................................................................................................................2

Answer to question 3..................................................................................................................3

Answer to question 4..................................................................................................................5

PART B:.....................................................................................................................................5

Answer to question 1:.................................................................................................................5

Answer to question 2..................................................................................................................8

Answer to question 3..................................................................................................................8

Reference..................................................................................................................................10

Appendices...............................................................................................................................12

Table of Contents

PART A:.....................................................................................................................................2

Answer to question1...................................................................................................................2

Answer to question 2..................................................................................................................2

Answer to question 3..................................................................................................................3

Answer to question 4..................................................................................................................5

PART B:.....................................................................................................................................5

Answer to question 1:.................................................................................................................5

Answer to question 2..................................................................................................................8

Answer to question 3..................................................................................................................8

Reference..................................................................................................................................10

Appendices...............................................................................................................................12

2INTERNATIONAL FINANCE

PART A:

Answer to question1.

The increased rate of interest present in Thailand is a testimony to the uncertainty

prevailing in its economy. Hence, it can be anticipated reasonable that the value of Baht is

going to depreciate in the near future which will result in lower amount of Australian Dollars

being received by the company in exchange of same number of Baht (Boriob et al., 2017).

Hence, it is prudent that despite the lower interest rate of investments in Australia, the

company should refrain from investing it in Thailand at a higher rate of interest. This is

because even if the company is getting a higher rate of interest the benefits of the same will

no accrue to the company if the value of Baht currency declines disproportionately in the

future.

Answer to question 2.

In case the excess funds earned in Thailand are invested back in Thailand then the

company will need more money that it might have to fulfil by taking a loan back in Australia

at the prevalent rate of 10%. The additional funds so acquired will be instrumental in

supporting the operations in Australia (Avdjiev et al., 2016). The funds that were supposed to

be remitted back to Australia for investment purposes at 8% rate of interest will no longer be

available for the same purpose. Furthermore, if the Baht’s value reduces by 5% as the studies

suggest then investments made in Thailand will be yielding an interest of 9.25%. Hence, it

PART A:

Answer to question1.

The increased rate of interest present in Thailand is a testimony to the uncertainty

prevailing in its economy. Hence, it can be anticipated reasonable that the value of Baht is

going to depreciate in the near future which will result in lower amount of Australian Dollars

being received by the company in exchange of same number of Baht (Boriob et al., 2017).

Hence, it is prudent that despite the lower interest rate of investments in Australia, the

company should refrain from investing it in Thailand at a higher rate of interest. This is

because even if the company is getting a higher rate of interest the benefits of the same will

no accrue to the company if the value of Baht currency declines disproportionately in the

future.

Answer to question 2.

In case the excess funds earned in Thailand are invested back in Thailand then the

company will need more money that it might have to fulfil by taking a loan back in Australia

at the prevalent rate of 10%. The additional funds so acquired will be instrumental in

supporting the operations in Australia (Avdjiev et al., 2016). The funds that were supposed to

be remitted back to Australia for investment purposes at 8% rate of interest will no longer be

available for the same purpose. Furthermore, if the Baht’s value reduces by 5% as the studies

suggest then investments made in Thailand will be yielding an interest of 9.25%. Hence, it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL FINANCE

can be seen that in case the company is reinvesting the excess money earned in Thailand.

Then along with borrowing money for the additional funds required for carrying out the

operations in Australia the returns that the company was, getting from Thailand will also

decrease in the near future, which will be detrimental to the interest of the company (Titman

et al., 2017).

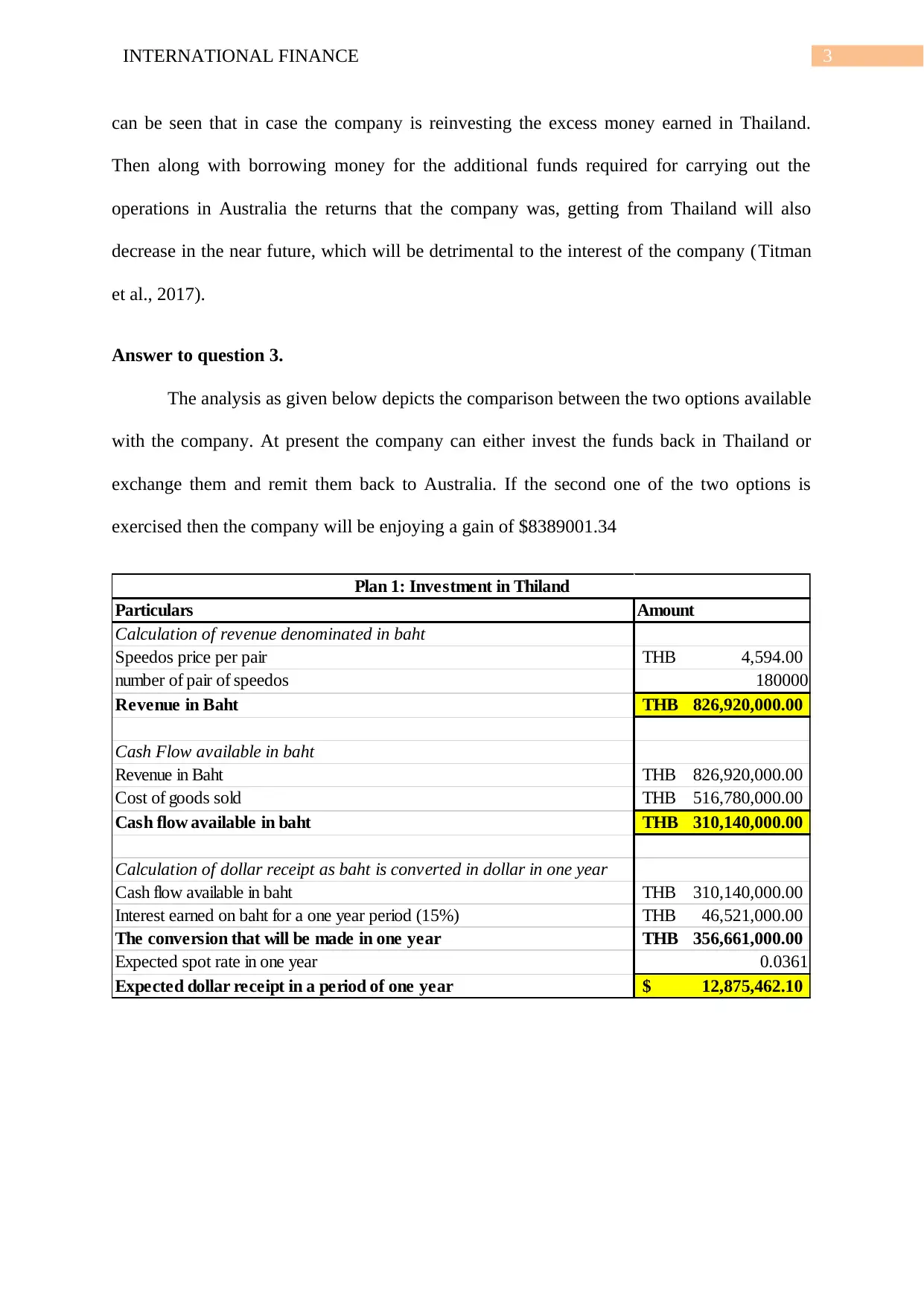

Answer to question 3.

The analysis as given below depicts the comparison between the two options available

with the company. At present the company can either invest the funds back in Thailand or

exchange them and remit them back to Australia. If the second one of the two options is

exercised then the company will be enjoying a gain of $8389001.34

Particulars Amount

Calculation of revenue denominated in baht

Speedos price per pair 4,594.00THB

number of pair of speedos 180000

Revenue in Baht 826,920,000.00THB

Cash Flow available in baht

Revenue in Baht 826,920,000.00THB

Cost of goods sold 516,780,000.00THB

Cash flow available in baht 310,140,000.00THB

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht 310,140,000.00THB

Interest earned on baht for a one year period (15%) 46,521,000.00THB

The conversion that will be made in one year 356,661,000.00THB

Expected spot rate in one year 0.0361

Expected dollar receipt in a period of one year 12,875,462.10$

Plan 1: Investment in Thiland

can be seen that in case the company is reinvesting the excess money earned in Thailand.

Then along with borrowing money for the additional funds required for carrying out the

operations in Australia the returns that the company was, getting from Thailand will also

decrease in the near future, which will be detrimental to the interest of the company (Titman

et al., 2017).

Answer to question 3.

The analysis as given below depicts the comparison between the two options available

with the company. At present the company can either invest the funds back in Thailand or

exchange them and remit them back to Australia. If the second one of the two options is

exercised then the company will be enjoying a gain of $8389001.34

Particulars Amount

Calculation of revenue denominated in baht

Speedos price per pair 4,594.00THB

number of pair of speedos 180000

Revenue in Baht 826,920,000.00THB

Cash Flow available in baht

Revenue in Baht 826,920,000.00THB

Cost of goods sold 516,780,000.00THB

Cash flow available in baht 310,140,000.00THB

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht 310,140,000.00THB

Interest earned on baht for a one year period (15%) 46,521,000.00THB

The conversion that will be made in one year 356,661,000.00THB

Expected spot rate in one year 0.0361

Expected dollar receipt in a period of one year 12,875,462.10$

Plan 1: Investment in Thiland

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL FINANCE

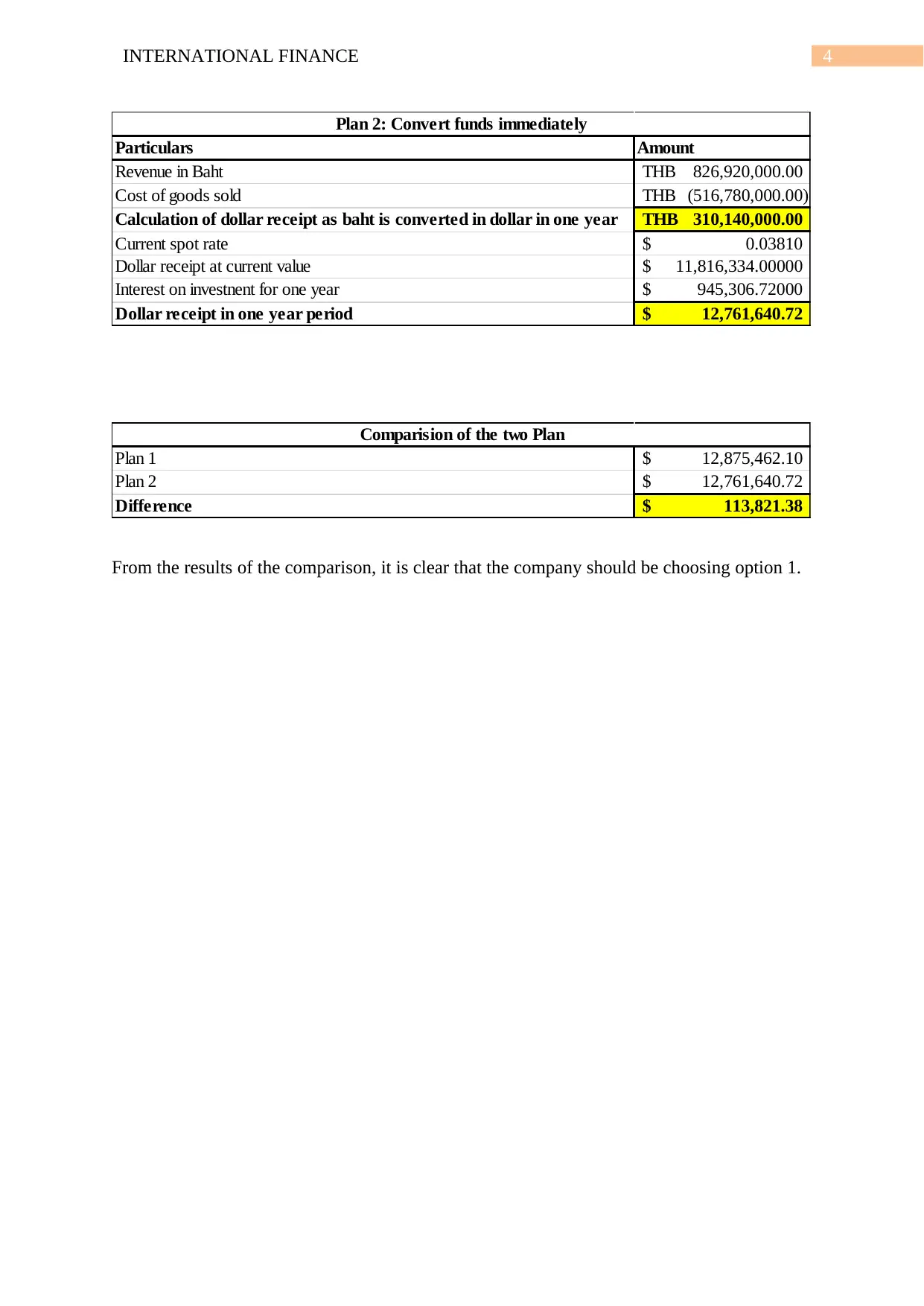

Particulars Amount

Revenue in Baht 826,920,000.00THB

Cost of goods sold (516,780,000.00)THB

Calculation of dollar receipt as baht is converted in dollar in one year 310,140,000.00THB

Current spot rate 0.03810$

Dollar receipt at current value 11,816,334.00000$

Interest on investnent for one year 945,306.72000$

Dollar receipt in one year period 12,761,640.72$

Plan 2: Convert funds immediately

Plan 1 12,875,462.10$

Plan 2 12,761,640.72$

Difference 113,821.38$

Comparision of the two Plan

From the results of the comparison, it is clear that the company should be choosing option 1.

Particulars Amount

Revenue in Baht 826,920,000.00THB

Cost of goods sold (516,780,000.00)THB

Calculation of dollar receipt as baht is converted in dollar in one year 310,140,000.00THB

Current spot rate 0.03810$

Dollar receipt at current value 11,816,334.00000$

Interest on investnent for one year 945,306.72000$

Dollar receipt in one year period 12,761,640.72$

Plan 2: Convert funds immediately

Plan 1 12,875,462.10$

Plan 2 12,761,640.72$

Difference 113,821.38$

Comparision of the two Plan

From the results of the comparison, it is clear that the company should be choosing option 1.

5INTERNATIONAL FINANCE

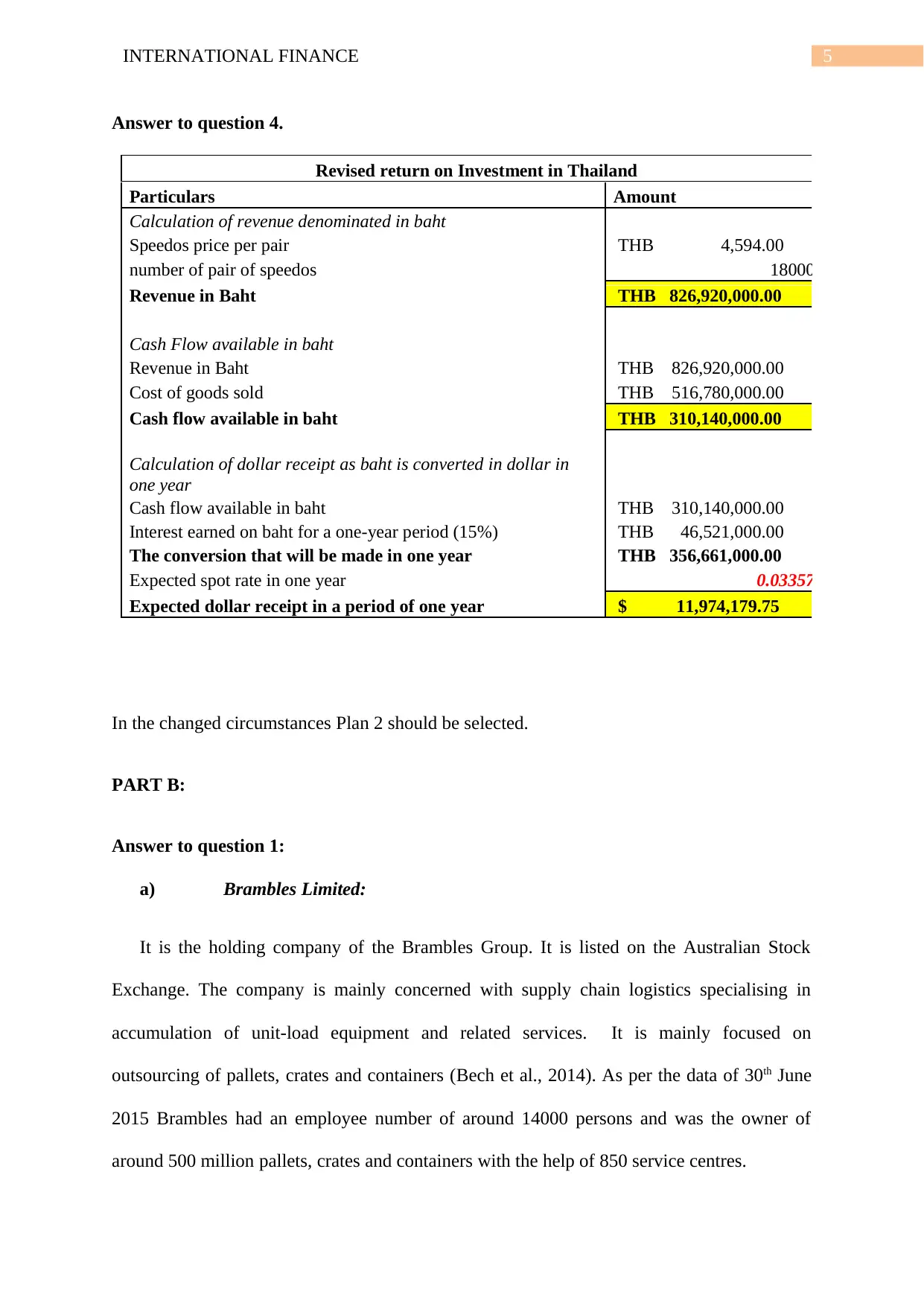

Answer to question 4.

Revised return on Investment in Thailand

Particulars Amount

Calculation of revenue denominated in baht

Speedos price per pair THB 4,594.00

number of pair of speedos 180000

Revenue in Baht THB 826,920,000.00

Cash Flow available in baht

Revenue in Baht THB 826,920,000.00

Cost of goods sold THB 516,780,000.00

Cash flow available in baht THB 310,140,000.00

Calculation of dollar receipt as baht is converted in dollar in

one year

Cash flow available in baht THB 310,140,000.00

Interest earned on baht for a one-year period (15%) THB 46,521,000.00

The conversion that will be made in one year THB 356,661,000.00

Expected spot rate in one year 0.033573

Expected dollar receipt in a period of one year $ 11,974,179.75

In the changed circumstances Plan 2 should be selected.

PART B:

Answer to question 1:

a) Brambles Limited:

It is the holding company of the Brambles Group. It is listed on the Australian Stock

Exchange. The company is mainly concerned with supply chain logistics specialising in

accumulation of unit-load equipment and related services. It is mainly focused on

outsourcing of pallets, crates and containers (Bech et al., 2014). As per the data of 30th June

2015 Brambles had an employee number of around 14000 persons and was the owner of

around 500 million pallets, crates and containers with the help of 850 service centres.

Answer to question 4.

Revised return on Investment in Thailand

Particulars Amount

Calculation of revenue denominated in baht

Speedos price per pair THB 4,594.00

number of pair of speedos 180000

Revenue in Baht THB 826,920,000.00

Cash Flow available in baht

Revenue in Baht THB 826,920,000.00

Cost of goods sold THB 516,780,000.00

Cash flow available in baht THB 310,140,000.00

Calculation of dollar receipt as baht is converted in dollar in

one year

Cash flow available in baht THB 310,140,000.00

Interest earned on baht for a one-year period (15%) THB 46,521,000.00

The conversion that will be made in one year THB 356,661,000.00

Expected spot rate in one year 0.033573

Expected dollar receipt in a period of one year $ 11,974,179.75

In the changed circumstances Plan 2 should be selected.

PART B:

Answer to question 1:

a) Brambles Limited:

It is the holding company of the Brambles Group. It is listed on the Australian Stock

Exchange. The company is mainly concerned with supply chain logistics specialising in

accumulation of unit-load equipment and related services. It is mainly focused on

outsourcing of pallets, crates and containers (Bech et al., 2014). As per the data of 30th June

2015 Brambles had an employee number of around 14000 persons and was the owner of

around 500 million pallets, crates and containers with the help of 850 service centres.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL FINANCE

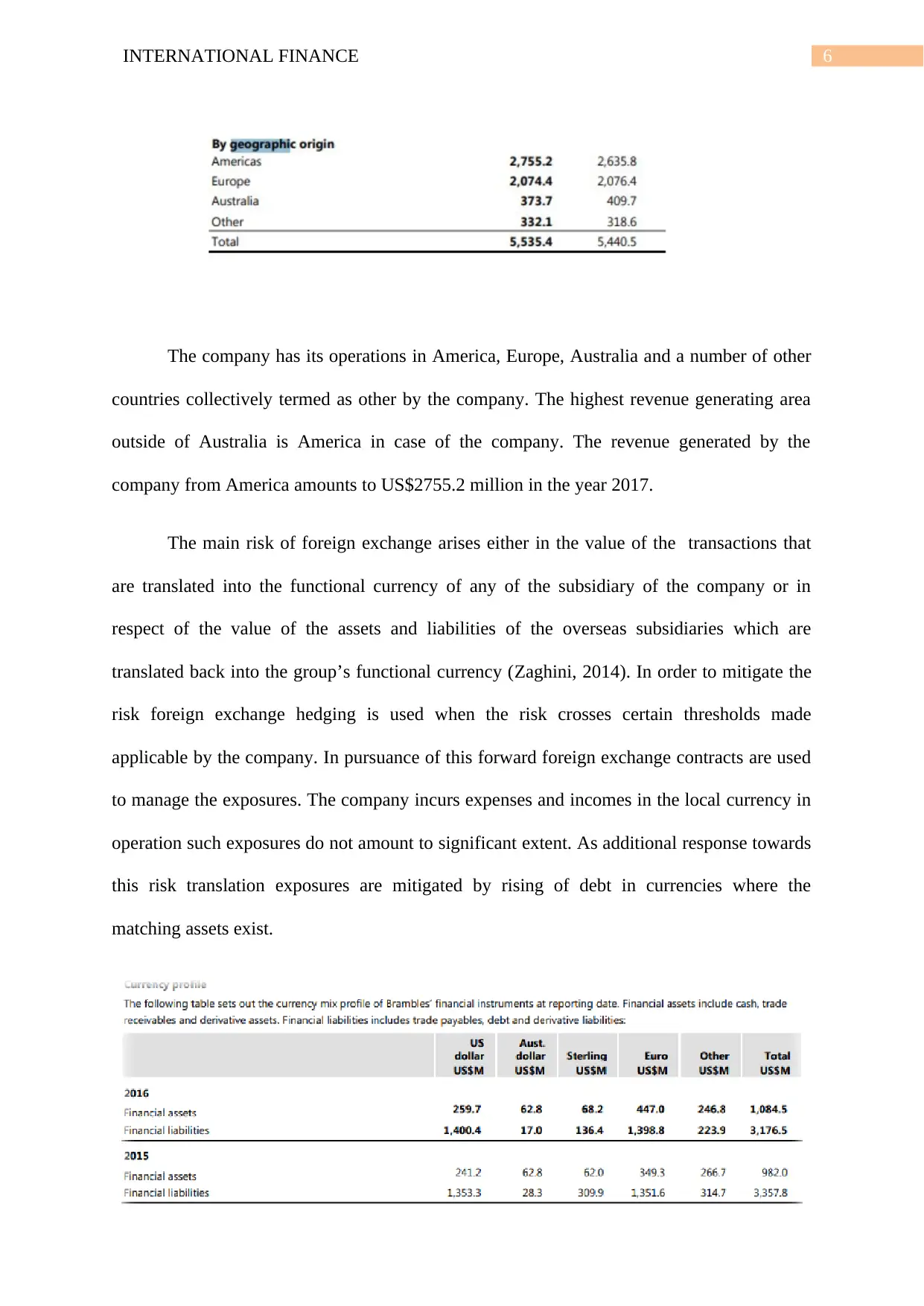

The company has its operations in America, Europe, Australia and a number of other

countries collectively termed as other by the company. The highest revenue generating area

outside of Australia is America in case of the company. The revenue generated by the

company from America amounts to US$2755.2 million in the year 2017.

The main risk of foreign exchange arises either in the value of the transactions that

are translated into the functional currency of any of the subsidiary of the company or in

respect of the value of the assets and liabilities of the overseas subsidiaries which are

translated back into the group’s functional currency (Zaghini, 2014). In order to mitigate the

risk foreign exchange hedging is used when the risk crosses certain thresholds made

applicable by the company. In pursuance of this forward foreign exchange contracts are used

to manage the exposures. The company incurs expenses and incomes in the local currency in

operation such exposures do not amount to significant extent. As additional response towards

this risk translation exposures are mitigated by rising of debt in currencies where the

matching assets exist.

The company has its operations in America, Europe, Australia and a number of other

countries collectively termed as other by the company. The highest revenue generating area

outside of Australia is America in case of the company. The revenue generated by the

company from America amounts to US$2755.2 million in the year 2017.

The main risk of foreign exchange arises either in the value of the transactions that

are translated into the functional currency of any of the subsidiary of the company or in

respect of the value of the assets and liabilities of the overseas subsidiaries which are

translated back into the group’s functional currency (Zaghini, 2014). In order to mitigate the

risk foreign exchange hedging is used when the risk crosses certain thresholds made

applicable by the company. In pursuance of this forward foreign exchange contracts are used

to manage the exposures. The company incurs expenses and incomes in the local currency in

operation such exposures do not amount to significant extent. As additional response towards

this risk translation exposures are mitigated by rising of debt in currencies where the

matching assets exist.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCE

b) CSL LTD.

The company operates in the field of bio-technology and its operations are wide

ranging like research, manufacture, development and marketing of products which

prevent and are able to cure people suffering or prone to diseases that can cause serious

medical conditions to the person (Gambacorta et al., 2015). The company mainly

produces antivenom, blood plasma derivatives and vaccines.

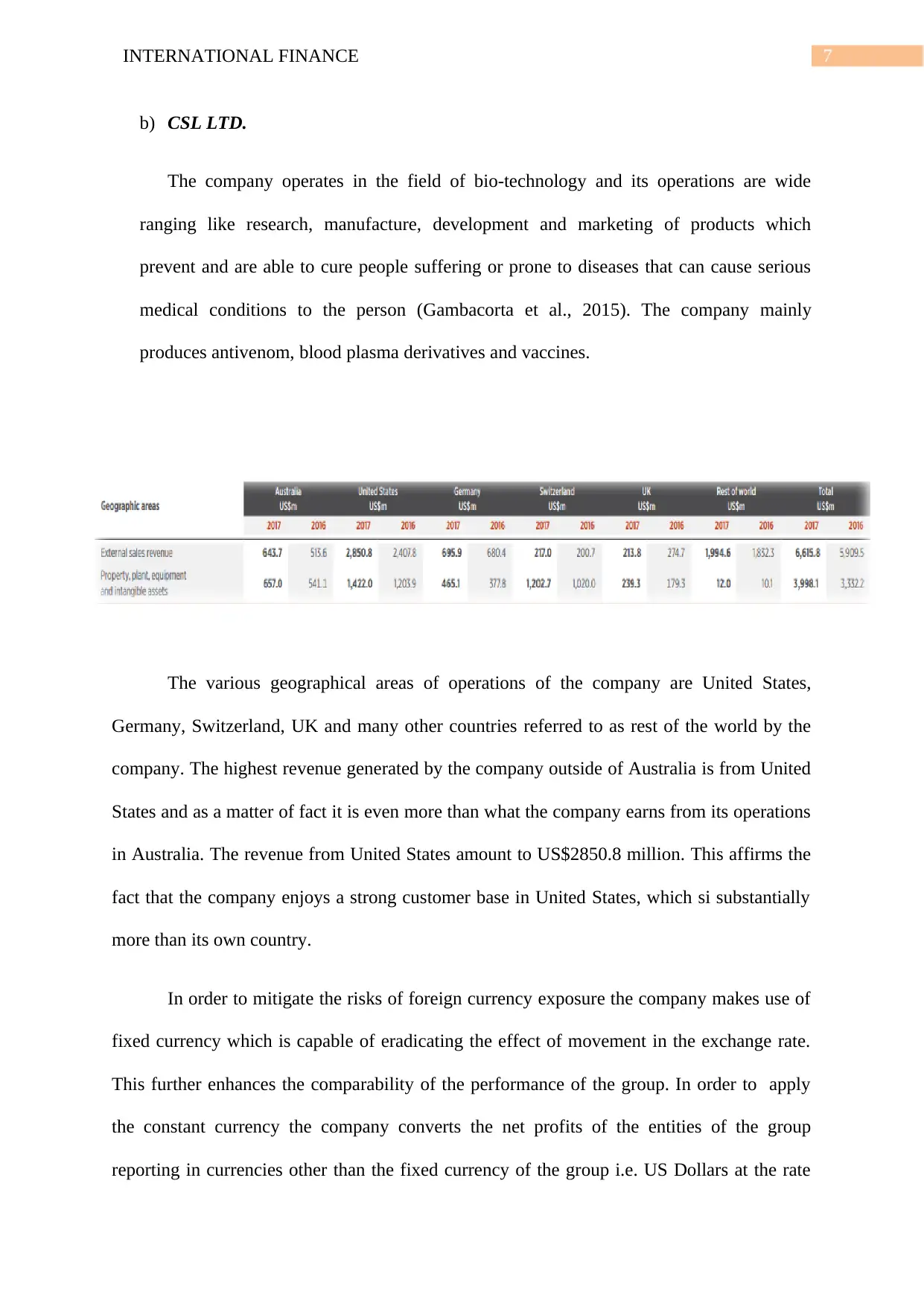

The various geographical areas of operations of the company are United States,

Germany, Switzerland, UK and many other countries referred to as rest of the world by the

company. The highest revenue generated by the company outside of Australia is from United

States and as a matter of fact it is even more than what the company earns from its operations

in Australia. The revenue from United States amount to US$2850.8 million. This affirms the

fact that the company enjoys a strong customer base in United States, which si substantially

more than its own country.

In order to mitigate the risks of foreign currency exposure the company makes use of

fixed currency which is capable of eradicating the effect of movement in the exchange rate.

This further enhances the comparability of the performance of the group. In order to apply

the constant currency the company converts the net profits of the entities of the group

reporting in currencies other than the fixed currency of the group i.e. US Dollars at the rate

b) CSL LTD.

The company operates in the field of bio-technology and its operations are wide

ranging like research, manufacture, development and marketing of products which

prevent and are able to cure people suffering or prone to diseases that can cause serious

medical conditions to the person (Gambacorta et al., 2015). The company mainly

produces antivenom, blood plasma derivatives and vaccines.

The various geographical areas of operations of the company are United States,

Germany, Switzerland, UK and many other countries referred to as rest of the world by the

company. The highest revenue generated by the company outside of Australia is from United

States and as a matter of fact it is even more than what the company earns from its operations

in Australia. The revenue from United States amount to US$2850.8 million. This affirms the

fact that the company enjoys a strong customer base in United States, which si substantially

more than its own country.

In order to mitigate the risks of foreign currency exposure the company makes use of

fixed currency which is capable of eradicating the effect of movement in the exchange rate.

This further enhances the comparability of the performance of the group. In order to apply

the constant currency the company converts the net profits of the entities of the group

reporting in currencies other than the fixed currency of the group i.e. US Dollars at the rate

8INTERNATIONAL FINANCE

which was prevalent in the prior comparable period (Frieden, 2016). Further the company

makes adjustments in respect of the material transactions that were affected by the

fluctuations of the exchange rate at a rate which would have been applicable if the transaction

had taken place in the prior comparable period.

Answer to question 2.

The analysis of the chart comparing the correlation between the exchange rate of the

USD to AUD and the two companies it is found that corresponding share prices of both the

companies are in negative correlation with the exchange rate (Frisari & Stadelmann, 2015). It

implies if the exchange rate is going upwards then the share prices of the companies would

go down and when the exchange rate is going downward the share prices of both the

companies would go up. Among the two companies CSL LTD. has a higher degree of

negative correlation as compared to Brambles Ltd.

Answer to question 3.

Both the companies under study do not have a secondary listing on the stock

exchange any other countries except the Australian Stock Exchange. This is deterring for

both the companies as the revenue patterns of both companies suggest that they have

significant sources of revenue accruing overseas (Van den Berg, 2016). The companies are

losing on the opportunity of gaining the confidence of the customers and raising more capital

in the form of share capital and debt funds from other countries.

Getting itself listed on a secondary stock exchange will help both the companies in

increasing their flexibility with respect of raising additional capital. The company becomes

capable of raising capital in different time zones along with the ability to do so in multiple

currencies. The company can also reduce its overall cost of capital by adhering to the

disclosure requirements of the overseas stock exchanges diligently. This is because with

which was prevalent in the prior comparable period (Frieden, 2016). Further the company

makes adjustments in respect of the material transactions that were affected by the

fluctuations of the exchange rate at a rate which would have been applicable if the transaction

had taken place in the prior comparable period.

Answer to question 2.

The analysis of the chart comparing the correlation between the exchange rate of the

USD to AUD and the two companies it is found that corresponding share prices of both the

companies are in negative correlation with the exchange rate (Frisari & Stadelmann, 2015). It

implies if the exchange rate is going upwards then the share prices of the companies would

go down and when the exchange rate is going downward the share prices of both the

companies would go up. Among the two companies CSL LTD. has a higher degree of

negative correlation as compared to Brambles Ltd.

Answer to question 3.

Both the companies under study do not have a secondary listing on the stock

exchange any other countries except the Australian Stock Exchange. This is deterring for

both the companies as the revenue patterns of both companies suggest that they have

significant sources of revenue accruing overseas (Van den Berg, 2016). The companies are

losing on the opportunity of gaining the confidence of the customers and raising more capital

in the form of share capital and debt funds from other countries.

Getting itself listed on a secondary stock exchange will help both the companies in

increasing their flexibility with respect of raising additional capital. The company becomes

capable of raising capital in different time zones along with the ability to do so in multiple

currencies. The company can also reduce its overall cost of capital by adhering to the

disclosure requirements of the overseas stock exchanges diligently. This is because with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL FINANCE

accurate and diligent disclosure practices the company will be enjoying the goodwill and

reputation both from foreign country’s statutory bodies as well as the investors who will be

ever more ready to invest their funds in the company (Frieden & Lake, 2015). The cross

listing comes with the added advantage of media coverage which increases the goodwill of

the company. In spite of these advantages however, there are various costs associated with

the process of secondary listing like registration costs, reports and disclosure requirements

etc.

As per the revenue patterns of both the companies it is recommended that CSL and

BXB should get listed on the stock exchange of United States. As, both the companies have

significant revenues accruing out of the country (Buchholz & Tonzer, 2016). This will help

the countries in further expanding the operations in the country by utilising the funds raised

from that country itself. The companies will enjoy the benefit of established business and will

be able to garner the faith of the shareholders. The company will get the opportunity of

hedging the market fluctuation in and out of its own country. diversification of operations

along with getting listed on a secondary stock exchange will not only improve the operational

capability of the organisation but also the financial performance and security of the company

by providing the company more than one platform to trade its securities (McCauley &

Schenk, 2015).

accurate and diligent disclosure practices the company will be enjoying the goodwill and

reputation both from foreign country’s statutory bodies as well as the investors who will be

ever more ready to invest their funds in the company (Frieden & Lake, 2015). The cross

listing comes with the added advantage of media coverage which increases the goodwill of

the company. In spite of these advantages however, there are various costs associated with

the process of secondary listing like registration costs, reports and disclosure requirements

etc.

As per the revenue patterns of both the companies it is recommended that CSL and

BXB should get listed on the stock exchange of United States. As, both the companies have

significant revenues accruing out of the country (Buchholz & Tonzer, 2016). This will help

the countries in further expanding the operations in the country by utilising the funds raised

from that country itself. The companies will enjoy the benefit of established business and will

be able to garner the faith of the shareholders. The company will get the opportunity of

hedging the market fluctuation in and out of its own country. diversification of operations

along with getting listed on a secondary stock exchange will not only improve the operational

capability of the organisation but also the financial performance and security of the company

by providing the company more than one platform to trade its securities (McCauley &

Schenk, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNATIONAL FINANCE

Reference

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Bech, M. L., Gambacorta, L., & Kharroubi, E. (2014). Monetary policy in a downturn: are

financial crises special?. International Finance, 17(1), 99-119.

Borio, C., Gambacorta, L., & Hofmann, B. (2017). The influence of monetary policy on bank

profitability. International Finance, 20(1), 48-63.

Buchholz, M., & Tonzer, L. (2016). Sovereign Credit Risk Co‐Movements in the Eurozone:

Simple Interdependence or Contagion?. International Finance, 19(3), 246-268.

Frieden, J. (2016). The governance of international finance. Annual Review of Political

Science, 19.

Frieden, J. A., & Lake, D. A. (2015). World Politics: Interests, Interactions, Institutions:

Third International Student Edition. WW Norton & Company.

Frisari, G., & Stadelmann, M. (2015). De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82,

12-22.

Gambacorta, L., Illes, A., & Lombardi, M. J. (2015). Has the Transmission of Policy Rates to

Lending Rates Changed in the Wake of the Global Financial Crisis?. International

Finance, 18(3), 263-280.

McCauley, R. N., & Schenk, C. R. (2015). Reforming the International Monetary System in

the 1970s and 2000s: Would a Special Drawing Right Substitution Account Have

Worked?. International Finance, 18(2), 187-206.

Reference

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Bech, M. L., Gambacorta, L., & Kharroubi, E. (2014). Monetary policy in a downturn: are

financial crises special?. International Finance, 17(1), 99-119.

Borio, C., Gambacorta, L., & Hofmann, B. (2017). The influence of monetary policy on bank

profitability. International Finance, 20(1), 48-63.

Buchholz, M., & Tonzer, L. (2016). Sovereign Credit Risk Co‐Movements in the Eurozone:

Simple Interdependence or Contagion?. International Finance, 19(3), 246-268.

Frieden, J. (2016). The governance of international finance. Annual Review of Political

Science, 19.

Frieden, J. A., & Lake, D. A. (2015). World Politics: Interests, Interactions, Institutions:

Third International Student Edition. WW Norton & Company.

Frisari, G., & Stadelmann, M. (2015). De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82,

12-22.

Gambacorta, L., Illes, A., & Lombardi, M. J. (2015). Has the Transmission of Policy Rates to

Lending Rates Changed in the Wake of the Global Financial Crisis?. International

Finance, 18(3), 263-280.

McCauley, R. N., & Schenk, C. R. (2015). Reforming the International Monetary System in

the 1970s and 2000s: Would a Special Drawing Right Substitution Account Have

Worked?. International Finance, 18(2), 187-206.

11INTERNATIONAL FINANCE

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Van den Berg, H. (2016). Economic growth and development. World Scientific Publishing

Company.

Zaghini, A. (2014). Bank bonds: size, systemic relevance and the sovereign. International

Finance, 17(2), 161-184.

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Van den Berg, H. (2016). Economic growth and development. World Scientific Publishing

Company.

Zaghini, A. (2014). Bank bonds: size, systemic relevance and the sovereign. International

Finance, 17(2), 161-184.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.