International Finance Report: Financial Analysis and Risk Assessment

VerifiedAdded on 2021/04/21

|11

|1218

|120

Report

AI Summary

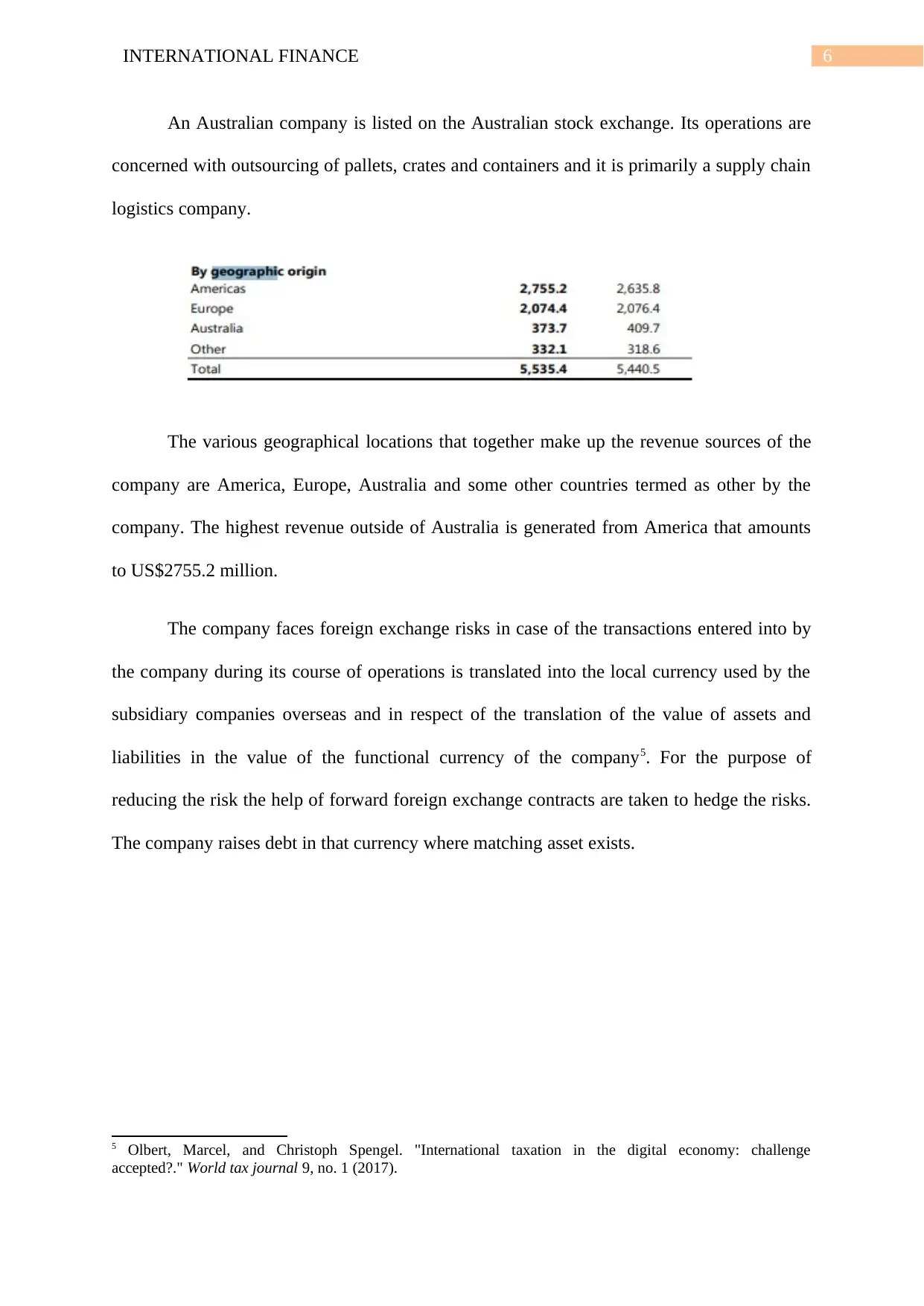

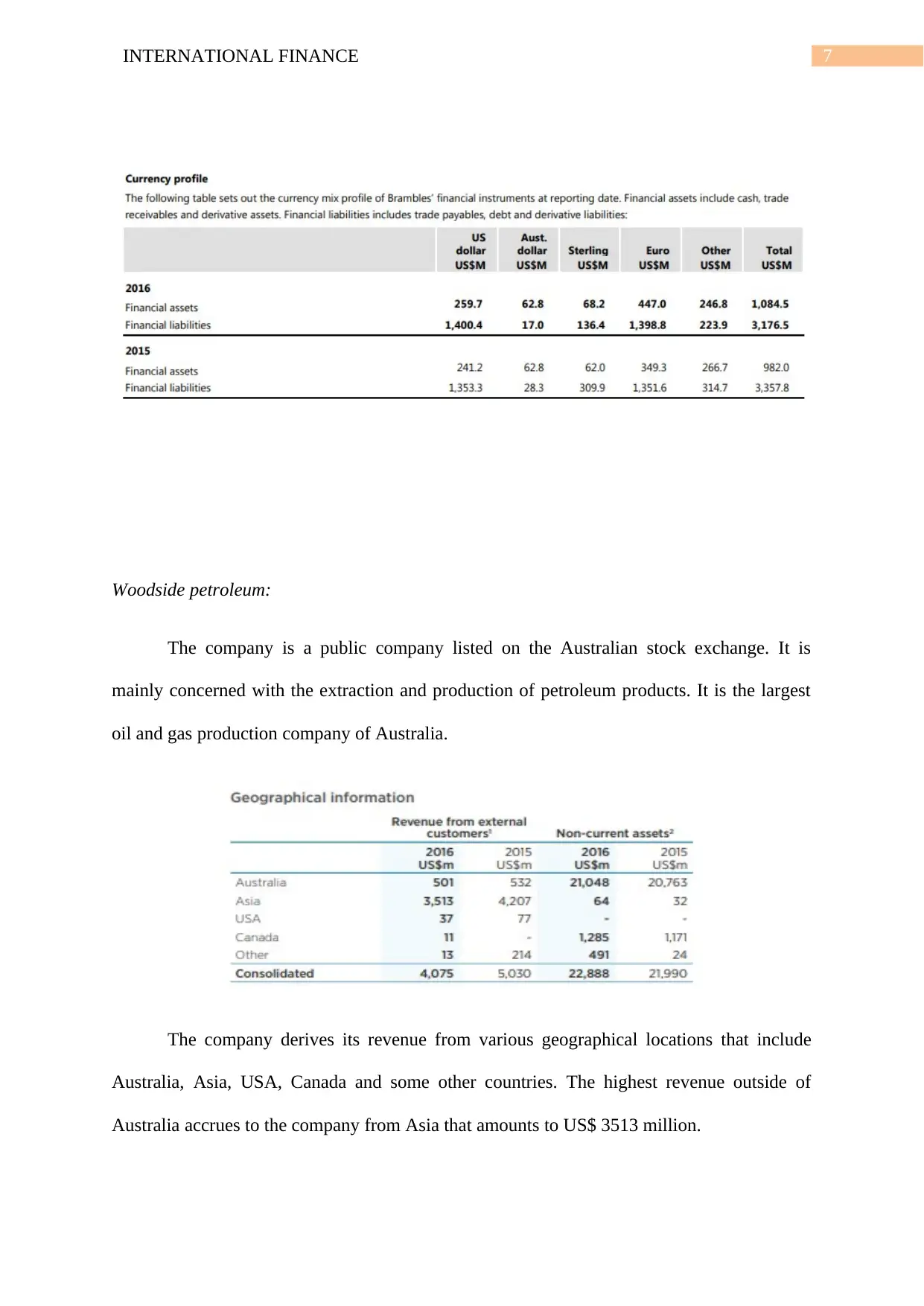

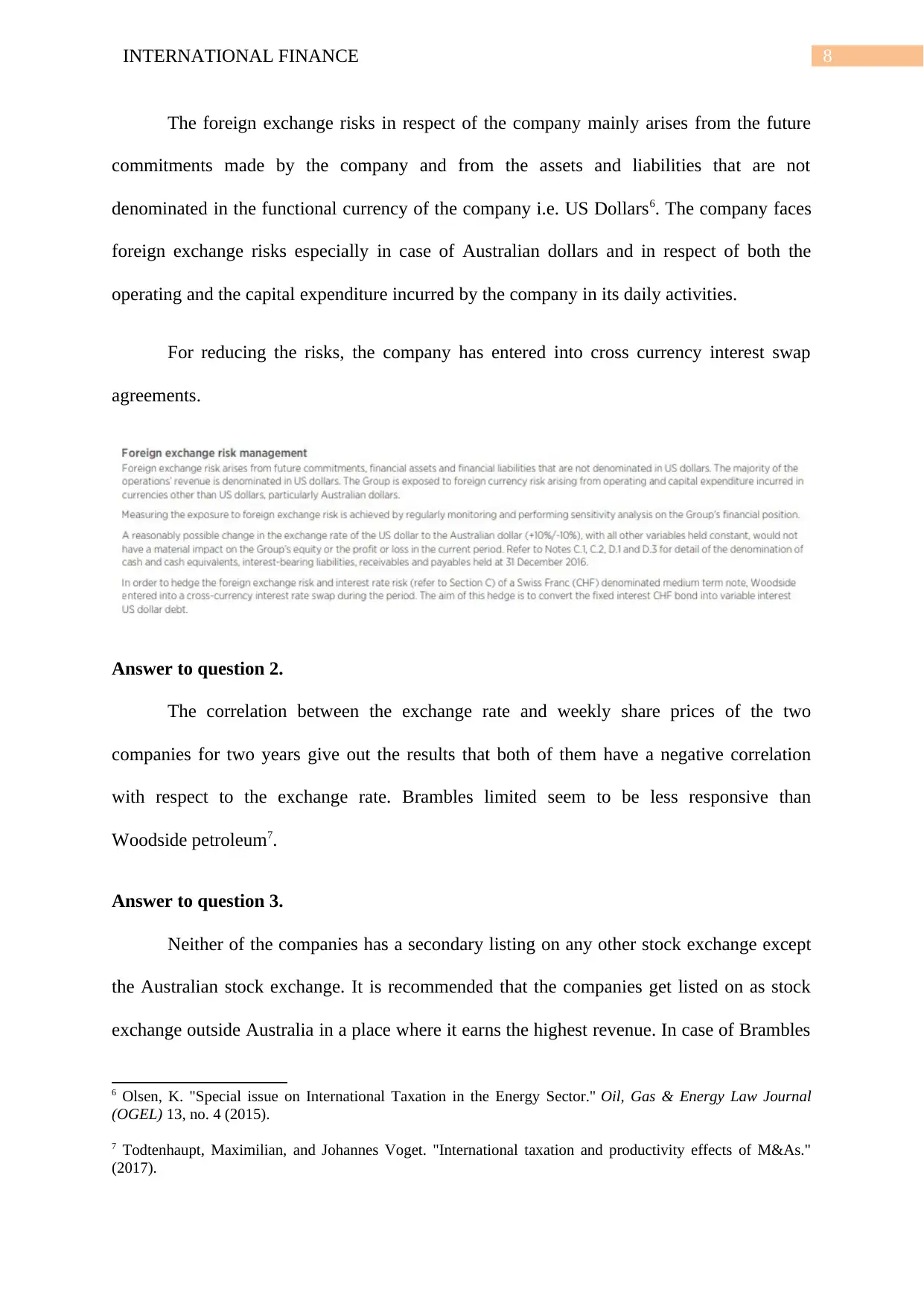

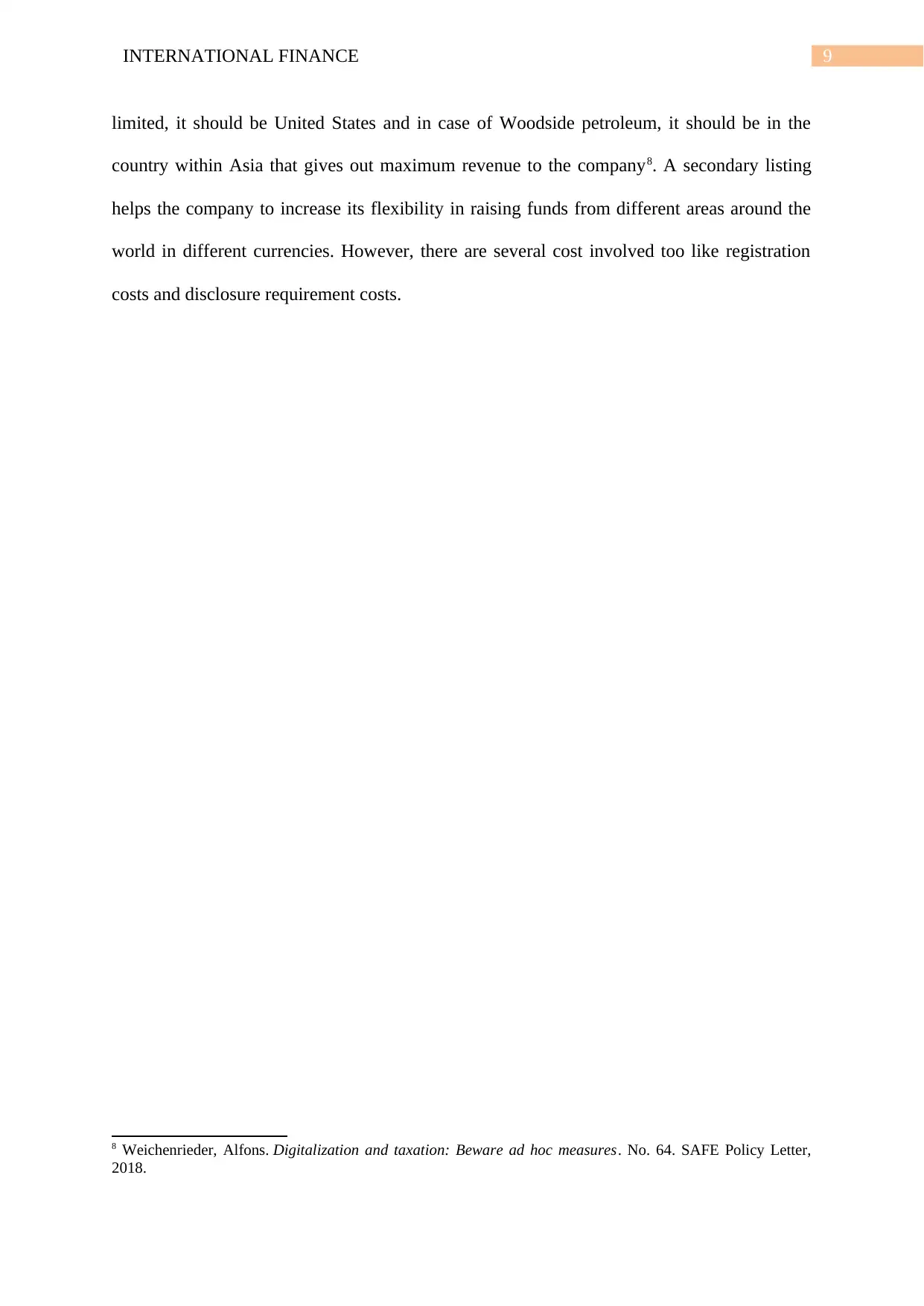

This report analyzes international finance, focusing on the financial strategies of companies operating internationally. Part A addresses questions related to investment returns in different countries (Thailand and Australia), currency depreciation, and the optimal allocation of funds to maximize returns while mitigating risks. Part B examines the foreign exchange risks faced by two Australian companies, Brambles Limited and Woodside Petroleum, detailing their revenue sources, risk management strategies (including forward contracts and cross-currency swaps), and the correlation between exchange rates and share prices. The report recommends secondary listings on international stock exchanges for increased flexibility in raising funds. It uses financial data, including interest rates, currency depreciation scenarios, and company performance metrics to support its analysis and recommendations. The report also includes a reference list of relevant academic sources.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.