Detailed Analysis of International Financial Management Assignment

VerifiedAdded on 2022/12/15

|11

|1840

|441

Homework Assignment

AI Summary

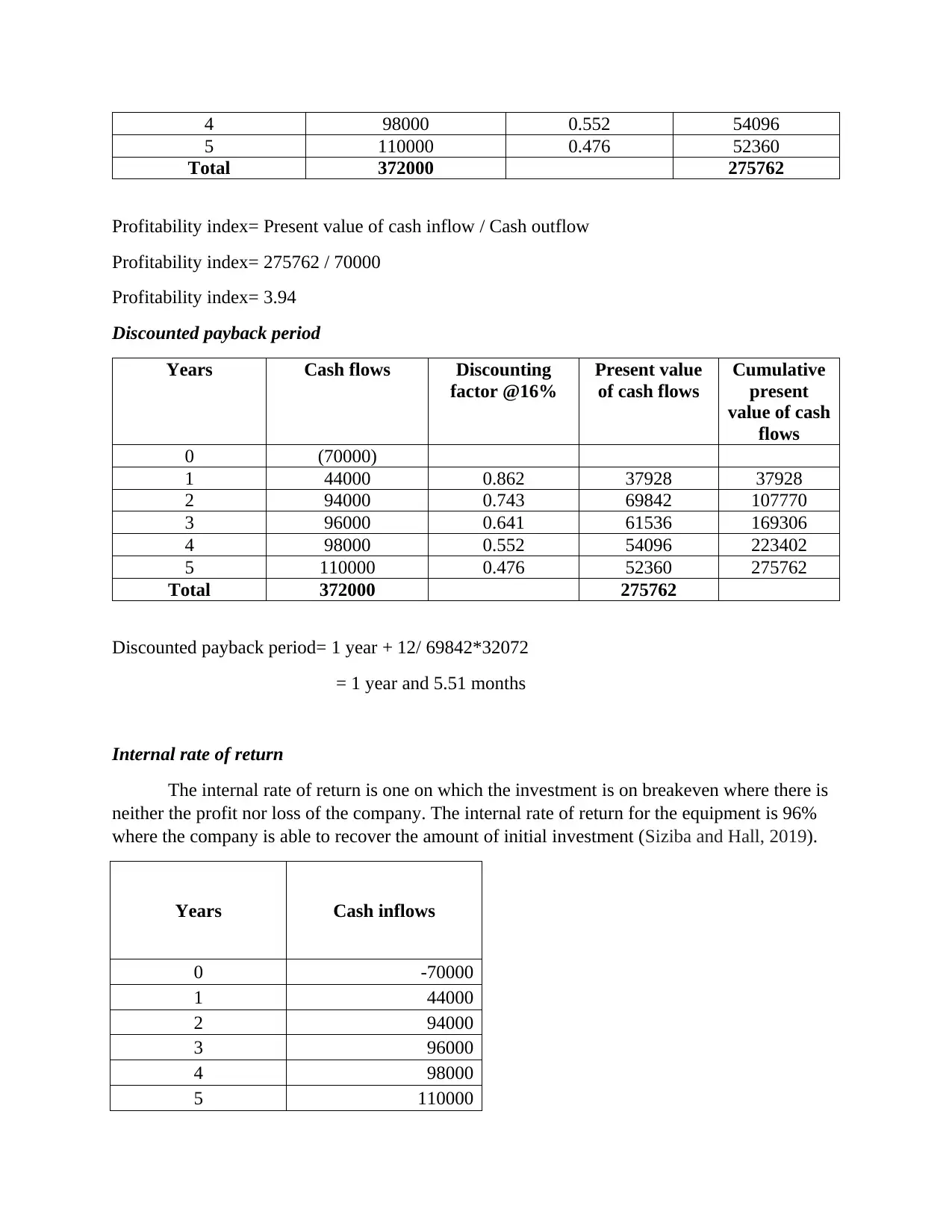

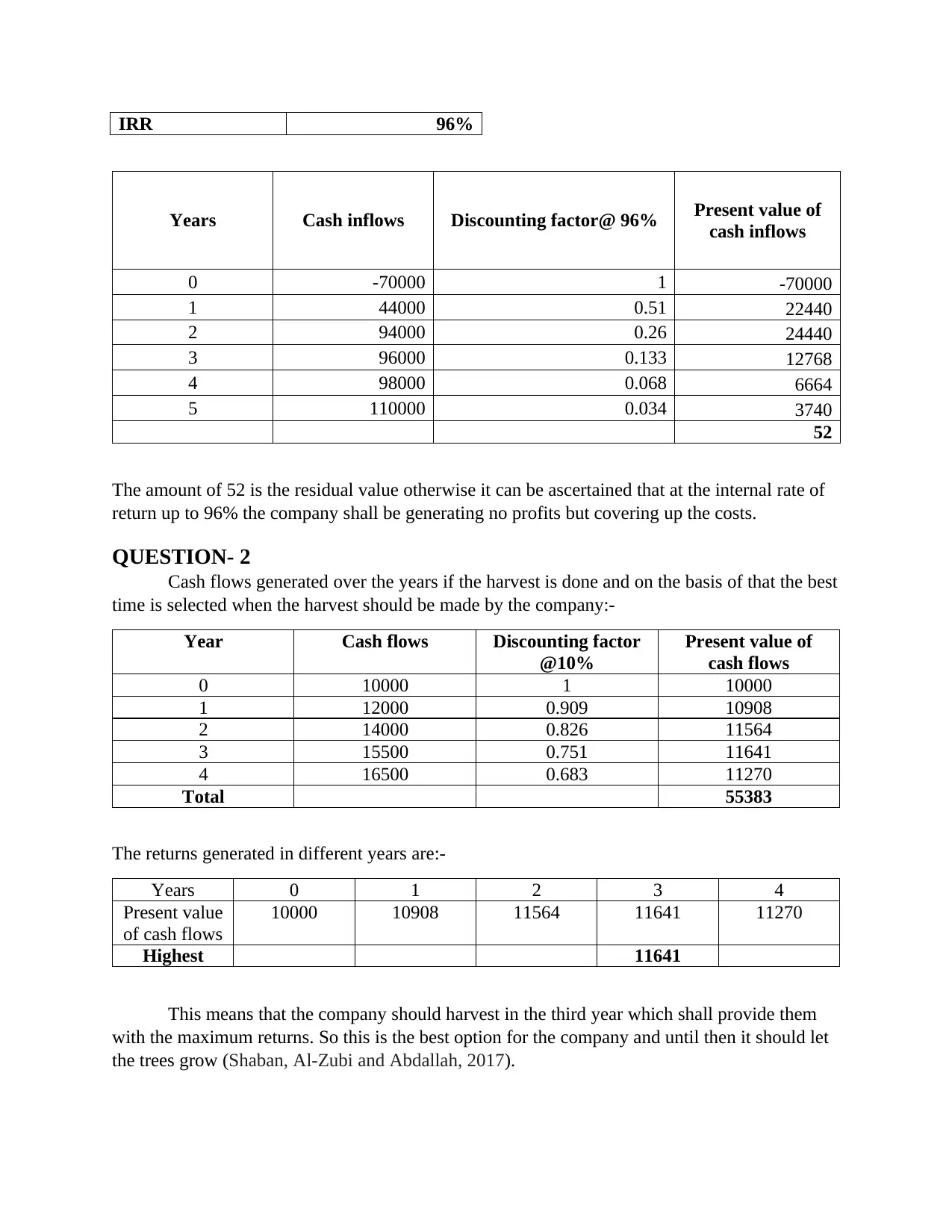

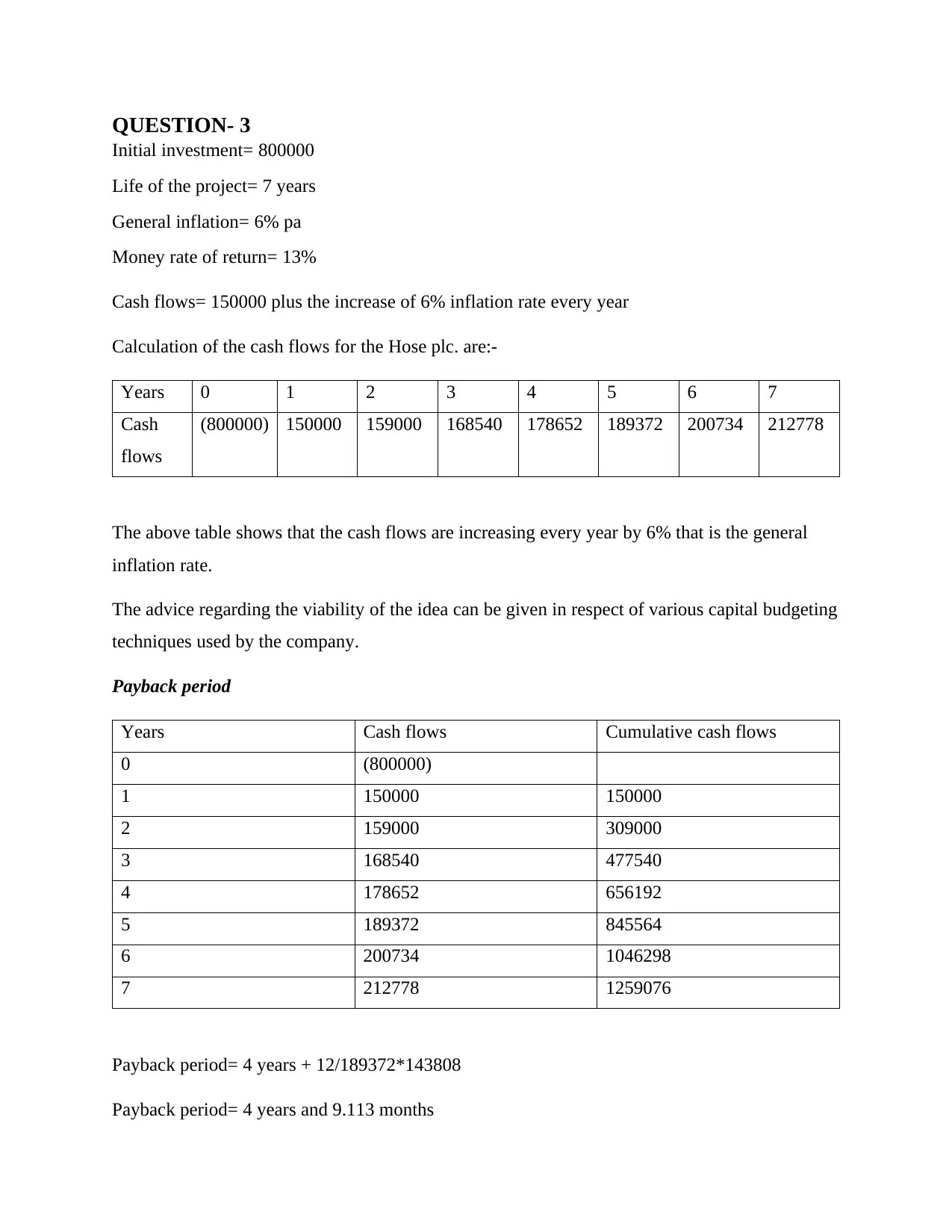

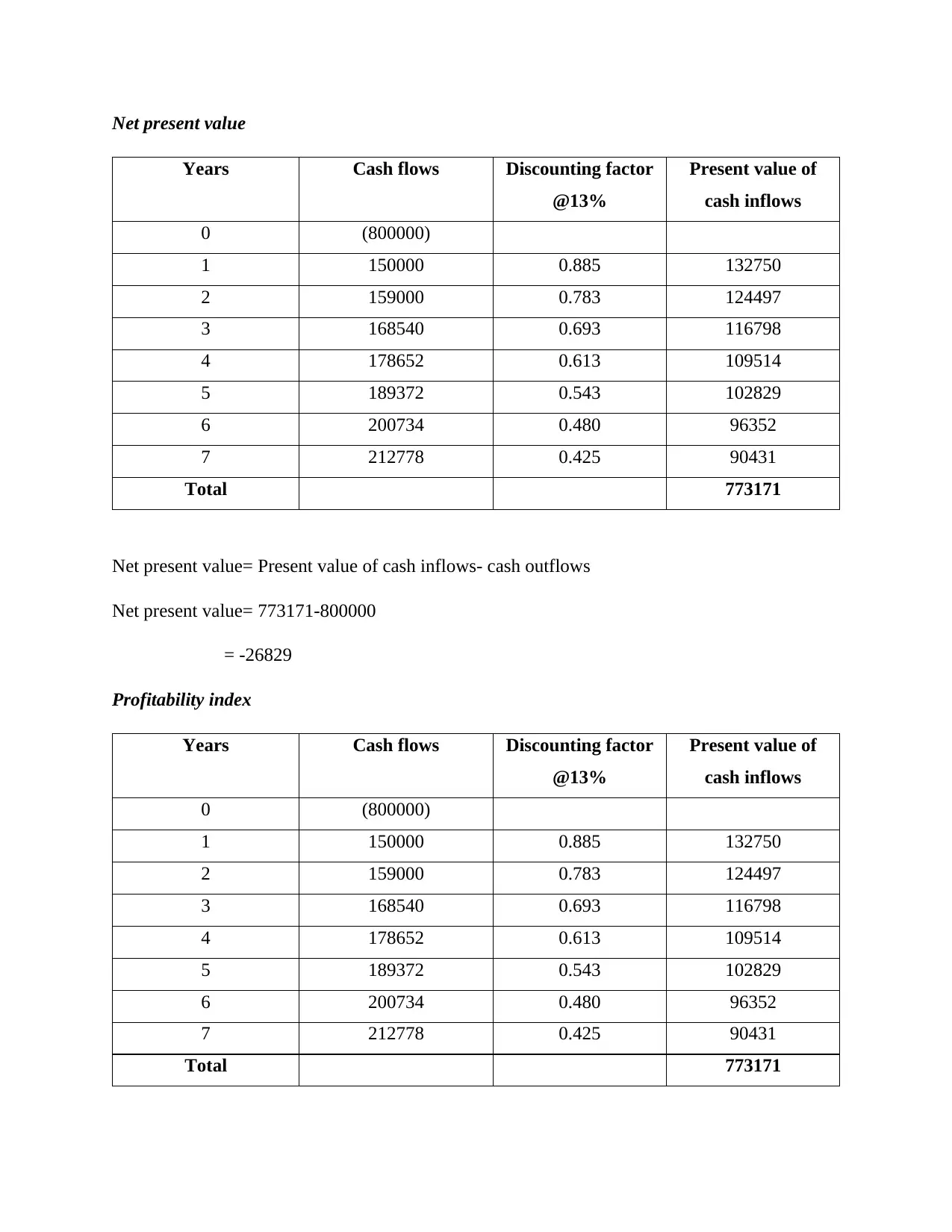

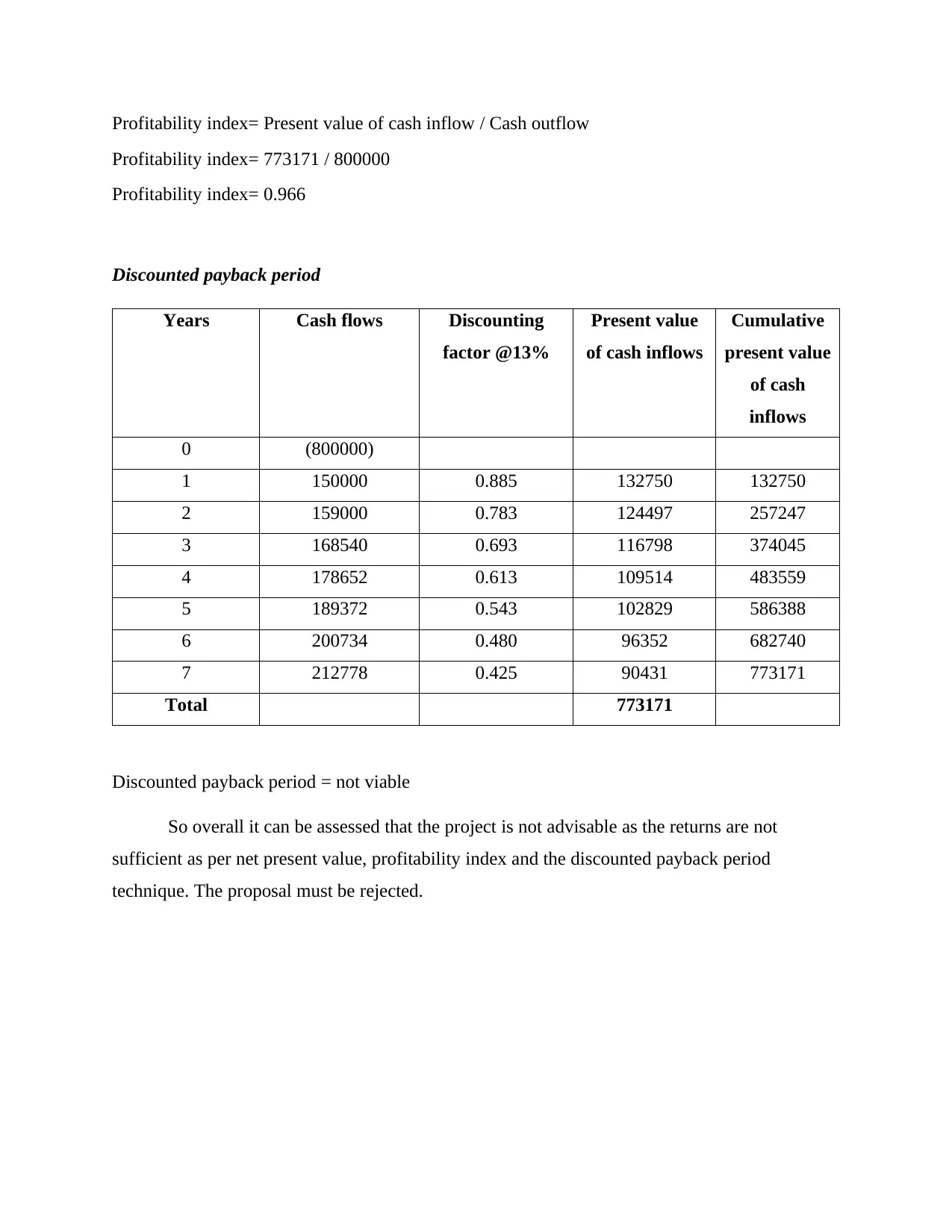

This assignment delves into International Financial Management (IFM), analyzing capital budgeting techniques for investment decisions. It presents three questions, each exploring different scenarios and financial tools. Question 1 evaluates whether a company should manufacture or procure widgets, using payback period, Net Present Value (NPV), Profitability Index, Discounted Payback Period, and Internal Rate of Return (IRR). Question 2 assesses the optimal time to harvest a resource based on present value calculations. Question 3 analyzes a project's viability, considering inflation and money rate of return, using similar capital budgeting methods as Question 1. The assignment provides detailed calculations and recommendations based on the financial analysis, offering insights into investment appraisal and decision-making in an international context.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.