BUS330 - International Finance: Individual Assignment Solution

VerifiedAdded on 2022/12/27

|11

|2897

|76

Homework Assignment

AI Summary

This assignment solution addresses key concepts in international finance through the analysis of several case studies. Chapter 3 focuses on BHP Billiton, examining how Citigroup facilitates the flow of funds across international financial markets, including spot, money, and bond markets, as well as foreign branch banking and trade finance. It also explores factors influencing a British subsidiary's decision on foreign currency borrowing. Chapter 5 delves into factors affecting exchange rates, specifically analyzing how various economic indicators influence the demand and supply of a currency, using Bruin Aircraft, Pty Ltd as a case study. Chapter 6 examines the impact of currency fluctuations and inflation on Beacon Lighting's cost savings when sourcing from Alibaba, highlighting the risks associated with international trade. Chapter 7 explores covered interest arbitrage using UniSuper as an example, evaluating the risks and potential benefits of investing in foreign markets while hedging against exchange rate fluctuations. The solution provides a comprehensive overview of these topics, offering insights into the practical application of international finance principles.

Running head: INTERNATIONAL FINANCE

INTERNATIONAL FINANCE

Name of the Student

Name of the University

Author Note

INTERNATIONAL FINANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE

2

INTERNATIONAL FINANCE

Table of Contents

Chapter 3 BHP Billiton................................................................................................................3

Chapter 5 Bruin Aircraft, Pty Ltd................................................................................................4

Chapter 6 Beacon Lighting..........................................................................................................6

Chapter 7 UniSuper......................................................................................................................7

References....................................................................................................................................9

INTERNATIONAL FINANCE

Table of Contents

Chapter 3 BHP Billiton................................................................................................................3

Chapter 5 Bruin Aircraft, Pty Ltd................................................................................................4

Chapter 6 Beacon Lighting..........................................................................................................6

Chapter 7 UniSuper......................................................................................................................7

References....................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTERNATIONAL FINANCE

Chapter 3 BHP Billiton

Flow of funds is the movement of funds to and from various sectors of an economy in a given

period of time (Errico et al., 2014). In a globalised world, international flow of funds has

become more significant than ever due to the dynamic nature of business (Cavusgil et al., 2014).

Commercial banks have become important sources of facilitating flow of funds across continents

(Cohen, 2018). They undertake a variety of options which benefits both their business and the

client. Some of them are foreign branch banking, financing trade, foreign exchange services and

corporate financing (Buch & Goldberg, 2015). The markets where transactions of these kind

happen are the spot market, international money market and bond markets.

With respect to spot market, the bank can utilise instruments called spots which are used to

convert currencies of one country to currency of another (Malloy, 2013). They can either be done

on a fixed rate basis or a floating rate basis. Any excess of funds obtained from a subsidiary are

remitted to the parent company (Butler, 2016). Eurocurrency market is a popular money market

which is used to fund the growth of subsidiaries when they are in need of funds. MNCs usually

borrow from these markets from the banks when they are in need of funds on a short term basis.

In this case, Citibank serves as the creditor to BHP Billiton. With regards to the bond market,

bonds are issued in markets like Eurobond market and other stock exchanges where funds are

obtained from investors and are used in the financing of the business operations of the

subsidiary. Funds generated from the operations are used to pay the interest on these bonds

(Miyajima & Mohanty, 2015). In this case, the bank acts as a facilitator of the flow of funds.

In case of foreign branch banking, large banks like Citigroup facilitate flow of funds by acting as

affiliates to smaller banks that do not have presence in foreign countries. They help BHP Billiton

by providing a mechanism to its subsidiaries for obtaining international loans. They merely act

as a facilitator in this case. Trade finance is an aspect in which banks facilitate transactions

between individual customers and companies existing in a foreign country (Casey, O’Toole,

2014). This is usually done by issuing Letter of Credit (LOCs) which are a source of guarantee to

the company that the amount has been deposited by the customer. LOCs play an important role

in a company obtaining loans from manufacturers and is helpful in the flow of funds with

minimum risk. In this situation, Citigroup acts as a creditor on behalf of BHP Billiton as it is

INTERNATIONAL FINANCE

Chapter 3 BHP Billiton

Flow of funds is the movement of funds to and from various sectors of an economy in a given

period of time (Errico et al., 2014). In a globalised world, international flow of funds has

become more significant than ever due to the dynamic nature of business (Cavusgil et al., 2014).

Commercial banks have become important sources of facilitating flow of funds across continents

(Cohen, 2018). They undertake a variety of options which benefits both their business and the

client. Some of them are foreign branch banking, financing trade, foreign exchange services and

corporate financing (Buch & Goldberg, 2015). The markets where transactions of these kind

happen are the spot market, international money market and bond markets.

With respect to spot market, the bank can utilise instruments called spots which are used to

convert currencies of one country to currency of another (Malloy, 2013). They can either be done

on a fixed rate basis or a floating rate basis. Any excess of funds obtained from a subsidiary are

remitted to the parent company (Butler, 2016). Eurocurrency market is a popular money market

which is used to fund the growth of subsidiaries when they are in need of funds. MNCs usually

borrow from these markets from the banks when they are in need of funds on a short term basis.

In this case, Citibank serves as the creditor to BHP Billiton. With regards to the bond market,

bonds are issued in markets like Eurobond market and other stock exchanges where funds are

obtained from investors and are used in the financing of the business operations of the

subsidiary. Funds generated from the operations are used to pay the interest on these bonds

(Miyajima & Mohanty, 2015). In this case, the bank acts as a facilitator of the flow of funds.

In case of foreign branch banking, large banks like Citigroup facilitate flow of funds by acting as

affiliates to smaller banks that do not have presence in foreign countries. They help BHP Billiton

by providing a mechanism to its subsidiaries for obtaining international loans. They merely act

as a facilitator in this case. Trade finance is an aspect in which banks facilitate transactions

between individual customers and companies existing in a foreign country (Casey, O’Toole,

2014). This is usually done by issuing Letter of Credit (LOCs) which are a source of guarantee to

the company that the amount has been deposited by the customer. LOCs play an important role

in a company obtaining loans from manufacturers and is helpful in the flow of funds with

minimum risk. In this situation, Citigroup acts as a creditor on behalf of BHP Billiton as it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTERNATIONAL FINANCE

responsible for collecting the funds from the customer and is responsible for the smooth flow of

business.

In terms of foreign exchange services, payments are done in the currency of a foreign

country. The currency differences are managed by the bank by making necessary payments in

the foreign country in its currency and converting the balance amount to pay to the parent

company. The bank is a facilitator here.

The other services that are provided by Citigroup include lock box system, corporate

checking accounts and currency specific credit cards. These are mainly useful in collecting the

payments from customers on a timely basis and keeping the company informed about the results.

In this case, the bank plays the role of a creditor on behalf of the company.

b) Foreign currency borrowing is a modern global phenomenon where a company borrows

funds in a currency different from that of its home currency. The main reason for taking such

loans is to benefit from the fluctuations in foreign exchange rates and a reduced cost of

borrowing due to the regulations prevailing domestically.

The factors that the British subsidiary should consider before deciding on the currency to borrow

in are the cost of the borrowing, time required to obtain the loan, size of the loan and the existing

regulations in a particular country. In case of many developing countries, the central bank aims

to reduce the foreign exchange variability which leads to the reduction in risk associated with

investing in a particular currency.

Chapter 5 Bruin Aircraft, Pty Ltd

In any given market, under normal circumstances, the demand for a foreign currency

increases when the customers of the home country realise that they can purchase a product for a

lower amount in the foreign currency than in their home currency (Twarowska & Kakol, 2014).

However, to determine the level of demand and supply for a particular currency, there are

various factors which need to be considered and their impact also needs to be measured. These

include inflation rates, interest rates, balance of payments, government’s debt, recession, political

stability and the level of speculation in the market. The demand and supply function in a manner

that maintains the equilibrium in the market.

INTERNATIONAL FINANCE

responsible for collecting the funds from the customer and is responsible for the smooth flow of

business.

In terms of foreign exchange services, payments are done in the currency of a foreign

country. The currency differences are managed by the bank by making necessary payments in

the foreign country in its currency and converting the balance amount to pay to the parent

company. The bank is a facilitator here.

The other services that are provided by Citigroup include lock box system, corporate

checking accounts and currency specific credit cards. These are mainly useful in collecting the

payments from customers on a timely basis and keeping the company informed about the results.

In this case, the bank plays the role of a creditor on behalf of the company.

b) Foreign currency borrowing is a modern global phenomenon where a company borrows

funds in a currency different from that of its home currency. The main reason for taking such

loans is to benefit from the fluctuations in foreign exchange rates and a reduced cost of

borrowing due to the regulations prevailing domestically.

The factors that the British subsidiary should consider before deciding on the currency to borrow

in are the cost of the borrowing, time required to obtain the loan, size of the loan and the existing

regulations in a particular country. In case of many developing countries, the central bank aims

to reduce the foreign exchange variability which leads to the reduction in risk associated with

investing in a particular currency.

Chapter 5 Bruin Aircraft, Pty Ltd

In any given market, under normal circumstances, the demand for a foreign currency

increases when the customers of the home country realise that they can purchase a product for a

lower amount in the foreign currency than in their home currency (Twarowska & Kakol, 2014).

However, to determine the level of demand and supply for a particular currency, there are

various factors which need to be considered and their impact also needs to be measured. These

include inflation rates, interest rates, balance of payments, government’s debt, recession, political

stability and the level of speculation in the market. The demand and supply function in a manner

that maintains the equilibrium in the market.

5

INTERNATIONAL FINANCE

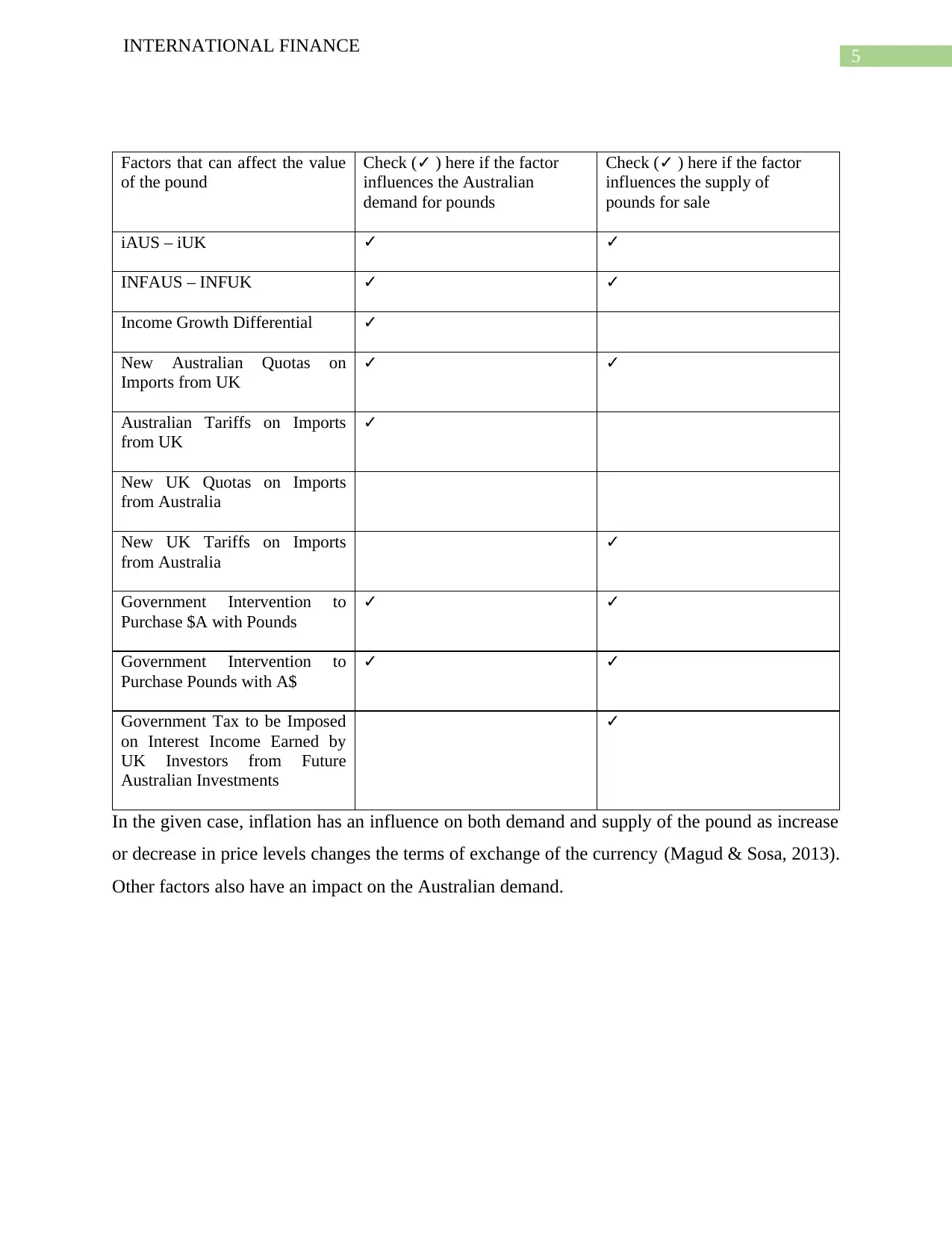

Factors that can affect the value

of the pound

Check (✓ ) here if the factor

influences the Australian

demand for pounds

Check (✓ ) here if the factor

influences the supply of

pounds for sale

iAUS – iUK ✓ ✓

INFAUS – INFUK ✓ ✓

Income Growth Differential ✓

New Australian Quotas on

Imports from UK

✓ ✓

Australian Tariffs on Imports

from UK

✓

New UK Quotas on Imports

from Australia

New UK Tariffs on Imports

from Australia

✓

Government Intervention to

Purchase $A with Pounds

✓ ✓

Government Intervention to

Purchase Pounds with A$

✓ ✓

Government Tax to be Imposed

on Interest Income Earned by

UK Investors from Future

Australian Investments

✓

In the given case, inflation has an influence on both demand and supply of the pound as increase

or decrease in price levels changes the terms of exchange of the currency (Magud & Sosa, 2013).

Other factors also have an impact on the Australian demand.

INTERNATIONAL FINANCE

Factors that can affect the value

of the pound

Check (✓ ) here if the factor

influences the Australian

demand for pounds

Check (✓ ) here if the factor

influences the supply of

pounds for sale

iAUS – iUK ✓ ✓

INFAUS – INFUK ✓ ✓

Income Growth Differential ✓

New Australian Quotas on

Imports from UK

✓ ✓

Australian Tariffs on Imports

from UK

✓

New UK Quotas on Imports

from Australia

New UK Tariffs on Imports

from Australia

✓

Government Intervention to

Purchase $A with Pounds

✓ ✓

Government Intervention to

Purchase Pounds with A$

✓ ✓

Government Tax to be Imposed

on Interest Income Earned by

UK Investors from Future

Australian Investments

✓

In the given case, inflation has an influence on both demand and supply of the pound as increase

or decrease in price levels changes the terms of exchange of the currency (Magud & Sosa, 2013).

Other factors also have an impact on the Australian demand.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTERNATIONAL FINANCE

Chapter 6 Beacon Lighting

It has been mentioned that the price paid by Beacon to Alibaba will be in Chinese Yuan.

Beacon also estimates a saving of around 20 percent on the cost of production. However, there

are a few conditions which are to be satisfied for this to happen (Yin & Li, 2014). It is expected

that the cost to Alibaba will increase over time due to the inflation in China. Hence, there is a

risk of savings being lower than that expected by Beacon.

a) For Beacon to be able to manage to save more than 20 percent on its cost of production,

the value of Yuan should decrease in value more than the differences in inflation of both

the countries (Gelb & Diofasi, 2016). Another situation would be the lack of increase in

the cost of production of Alibaba in proportion to the increase in the rate of inflation.

This would help Beacon to save more than 20 percent on its cost of production.

b) In order for Beacon to pay more costs than it currently does, the inflation in Australia

should increase on an uncontrolled rate and result in the depreciation of the Australian

dollar against the Chinese Yuan to a great extent. This would substantially increase the

payments made by Beacon to Alibaba. The strengthening of the Yuan due to the

improvement of the condition of the Chinese economy would also decrease the savings

made by Beacon.

c) It is not expected that Beacon would experience stable payments over time to Alibaba

because of the high inflation rate prevalent in China during recent years. Australia has a

stronger currency than Yuan and due to the inflation in China, it is expected that there

would be significant changes in the payments made by Beacon to Alibaba (Lothian,

2016). The most probable situation is a decrease in the value of the payments over years.

But a payment of stable dollar outflows does not seem possible.

d) There is a significant chance for Beacon’s risk to change due to the concept of

Purchasing Power Parity ((Joliffe & Prydz, 2015). As it is estimated that the inflation and

market conditions in China are unstable, it is a risky proposition for Beacon to enter into.

Any situation which is not favourable to Beacon will increase the pressure on it due to the

shortage of cash available. Hence, for Beacon to benefit from the current deal, the market

conditions should remain the way they currently are (Beckmann & Stix, 2015). It can be

interpreted that the risk of Beacon has increased more than what it previously faced.

INTERNATIONAL FINANCE

Chapter 6 Beacon Lighting

It has been mentioned that the price paid by Beacon to Alibaba will be in Chinese Yuan.

Beacon also estimates a saving of around 20 percent on the cost of production. However, there

are a few conditions which are to be satisfied for this to happen (Yin & Li, 2014). It is expected

that the cost to Alibaba will increase over time due to the inflation in China. Hence, there is a

risk of savings being lower than that expected by Beacon.

a) For Beacon to be able to manage to save more than 20 percent on its cost of production,

the value of Yuan should decrease in value more than the differences in inflation of both

the countries (Gelb & Diofasi, 2016). Another situation would be the lack of increase in

the cost of production of Alibaba in proportion to the increase in the rate of inflation.

This would help Beacon to save more than 20 percent on its cost of production.

b) In order for Beacon to pay more costs than it currently does, the inflation in Australia

should increase on an uncontrolled rate and result in the depreciation of the Australian

dollar against the Chinese Yuan to a great extent. This would substantially increase the

payments made by Beacon to Alibaba. The strengthening of the Yuan due to the

improvement of the condition of the Chinese economy would also decrease the savings

made by Beacon.

c) It is not expected that Beacon would experience stable payments over time to Alibaba

because of the high inflation rate prevalent in China during recent years. Australia has a

stronger currency than Yuan and due to the inflation in China, it is expected that there

would be significant changes in the payments made by Beacon to Alibaba (Lothian,

2016). The most probable situation is a decrease in the value of the payments over years.

But a payment of stable dollar outflows does not seem possible.

d) There is a significant chance for Beacon’s risk to change due to the concept of

Purchasing Power Parity ((Joliffe & Prydz, 2015). As it is estimated that the inflation and

market conditions in China are unstable, it is a risky proposition for Beacon to enter into.

Any situation which is not favourable to Beacon will increase the pressure on it due to the

shortage of cash available. Hence, for Beacon to benefit from the current deal, the market

conditions should remain the way they currently are (Beckmann & Stix, 2015). It can be

interpreted that the risk of Beacon has increased more than what it previously faced.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTERNATIONAL FINANCE

Chapter 7 UniSuper

Covered interest arbitrage is a safety measure where an investor undertakes a forward contract to

protect himself against the risk of exchange rate fluctuations ((Wong, Leung & Ng, 2017). It is

generally advisable in many situations as it protects the investor against any unforeseen

circumstances which are directly against the terms of the investment made by him.

a) In the given scenario, the interest rate being provided in Poland at 14% is much higher

than the 9% being provided in Australia. However, the fluctuations in Zloty is as high as

up to 40%. This is a significant amount and any movement towards the downward

direction will make the investment a big loss ((Ross, 2013). Hence it would be a massive

risk to invest funds in Poland without covering one’s position (Du, Tepper & Verdelhan,

2018). So, as an investor, I would not invest in the Poland market without covering my

position and hence the loss of $0.01 would still be feasible to maintain the safety of the

investment.

b) The interest arbitrage is done by investing the A$10 million by converting it into Zloty

and investing it in the Polish market. The forward contract is entered into with the bank

to cover the risks of fluctuations in the currency value ((Rime, Schrimpf & Syrstad,

2017). After the completion of one year, the amount earned by UniSuper is expected to

be A$11.1 million approximately. This is a safe situation for UniSuper as it is earning a

profit of more than 11 percent on its investment. Making the investment without interest

arbitrage would leave the investment vulnerable to the market fluctuations and significant

losses may be incurred on the investment.

c) The major risks involved in using covered interest arbitrage in this case is the chance to

earn additional profits that is not being taken up by UniSuper by leaving the investment

uncovered by arbitrage (Van Deventer, Imai & Mesler, 2013). As per the expected values

in changes in the currency, the company could have earned additional profits of 5 million

due to an increase in the value of the currency. However, by entering into the covered

interest agreement, the company is limiting its profits to the amount of A$11.1 million

only. Another risk that the company faces is not taking up the benefits which can be

earned by using speculation to gain short term benefits on an investment. This is the

opportunity cost of the company to the safety of the returns that it has opted for.

INTERNATIONAL FINANCE

Chapter 7 UniSuper

Covered interest arbitrage is a safety measure where an investor undertakes a forward contract to

protect himself against the risk of exchange rate fluctuations ((Wong, Leung & Ng, 2017). It is

generally advisable in many situations as it protects the investor against any unforeseen

circumstances which are directly against the terms of the investment made by him.

a) In the given scenario, the interest rate being provided in Poland at 14% is much higher

than the 9% being provided in Australia. However, the fluctuations in Zloty is as high as

up to 40%. This is a significant amount and any movement towards the downward

direction will make the investment a big loss ((Ross, 2013). Hence it would be a massive

risk to invest funds in Poland without covering one’s position (Du, Tepper & Verdelhan,

2018). So, as an investor, I would not invest in the Poland market without covering my

position and hence the loss of $0.01 would still be feasible to maintain the safety of the

investment.

b) The interest arbitrage is done by investing the A$10 million by converting it into Zloty

and investing it in the Polish market. The forward contract is entered into with the bank

to cover the risks of fluctuations in the currency value ((Rime, Schrimpf & Syrstad,

2017). After the completion of one year, the amount earned by UniSuper is expected to

be A$11.1 million approximately. This is a safe situation for UniSuper as it is earning a

profit of more than 11 percent on its investment. Making the investment without interest

arbitrage would leave the investment vulnerable to the market fluctuations and significant

losses may be incurred on the investment.

c) The major risks involved in using covered interest arbitrage in this case is the chance to

earn additional profits that is not being taken up by UniSuper by leaving the investment

uncovered by arbitrage (Van Deventer, Imai & Mesler, 2013). As per the expected values

in changes in the currency, the company could have earned additional profits of 5 million

due to an increase in the value of the currency. However, by entering into the covered

interest agreement, the company is limiting its profits to the amount of A$11.1 million

only. Another risk that the company faces is not taking up the benefits which can be

earned by using speculation to gain short term benefits on an investment. This is the

opportunity cost of the company to the safety of the returns that it has opted for.

8

INTERNATIONAL FINANCE

a) In the given situation, taking up covered interest arbitrage earns the company a total

return of A$11.1. Investing the same amount in Australian Treasury Bills would limit the

profit to A$10.9 million. Hence to earn a higher profit, the company should invest its

funds in the Polish market. This would help in increasing the overall value of the

company in the long run.

INTERNATIONAL FINANCE

a) In the given situation, taking up covered interest arbitrage earns the company a total

return of A$11.1. Investing the same amount in Australian Treasury Bills would limit the

profit to A$10.9 million. Hence to earn a higher profit, the company should invest its

funds in the Polish market. This would help in increasing the overall value of the

company in the long run.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTERNATIONAL FINANCE

References

Beckmann, E., & Stix, H. (2015). Foreign currency borrowing and knowledge about exchange

rate risk. Journal of Economic Behavior & Organization, 112, 1-16.

Buch, C. M., & Goldberg, L. S. (2015). International banking and liquidity risk transmission:

Lessons from across countries. IMF Economic Review, 63(3), 377-410.

Butler, K. C. (2016). Multinational Finance: Evaluating the Opportunities, Costs, and Risks of

Multinational Operations. John Wiley & Sons.

Casey, E., & O'Toole, C. M. (2014). Bank lending constraints, trade credit and alternative

financing during the financial crisis: Evidence from European SMEs. Journal of

Corporate Finance, 27, 173-193.

Cavusgil, S. T., Knight, G., Riesenberger, J. R., Rammal, H. G., & Rose, E. L.

(2014). International business. Pearson Australia.

Cohen, R. B. (2018). 12 The new international division of labor, multinational corporations and

urban hierarchy. Urbanization and urban planning in capitalist society, 7.

Du, W., Tepper, A., & Verdelhan, A. (2018). Deviations from covered interest rate parity. The

Journal of Finance, 73(3), 915-957.

Errico, M. L., Harutyunyan, A., Loukoianova, E., Walton, R., Korniyenko, M. Y., AbuShanab,

H., & Shin, M. H. S. (2014). Mapping the shadow banking system through a global flow

of funds analysis. International Monetary Fund.

Gelb, A., & Diofasi, A. (2016). What Determines Purchasing-Power-Parity Exchange

Rates?. Revue d’économie du développement, 24(2), 93-141.

Jolliffe, D., & Prydz, E. B. (2015). Global poverty goals and prices: how purchasing power

parity matters. The World Bank.

Lothian, J. R. (2016). Purchasing power parity and the behavior of prices and nominal exchange

rates across exchange-rate regimes. Journal of International Money and Finance, 69, 5-

21.

Magud, N., & Sosa, S. (2013). When and why worry about real exchange rate appreciation? The

missing link between Dutch disease and growth. Journal of International Commerce,

Economics and Policy, 4(02), 1350009.

Malloy, M. M. S. (2013). Factors influencing emerging market central banks’ decision to

intervene in foreign exchange markets (No. 13-70). International Monetary Fund.

INTERNATIONAL FINANCE

References

Beckmann, E., & Stix, H. (2015). Foreign currency borrowing and knowledge about exchange

rate risk. Journal of Economic Behavior & Organization, 112, 1-16.

Buch, C. M., & Goldberg, L. S. (2015). International banking and liquidity risk transmission:

Lessons from across countries. IMF Economic Review, 63(3), 377-410.

Butler, K. C. (2016). Multinational Finance: Evaluating the Opportunities, Costs, and Risks of

Multinational Operations. John Wiley & Sons.

Casey, E., & O'Toole, C. M. (2014). Bank lending constraints, trade credit and alternative

financing during the financial crisis: Evidence from European SMEs. Journal of

Corporate Finance, 27, 173-193.

Cavusgil, S. T., Knight, G., Riesenberger, J. R., Rammal, H. G., & Rose, E. L.

(2014). International business. Pearson Australia.

Cohen, R. B. (2018). 12 The new international division of labor, multinational corporations and

urban hierarchy. Urbanization and urban planning in capitalist society, 7.

Du, W., Tepper, A., & Verdelhan, A. (2018). Deviations from covered interest rate parity. The

Journal of Finance, 73(3), 915-957.

Errico, M. L., Harutyunyan, A., Loukoianova, E., Walton, R., Korniyenko, M. Y., AbuShanab,

H., & Shin, M. H. S. (2014). Mapping the shadow banking system through a global flow

of funds analysis. International Monetary Fund.

Gelb, A., & Diofasi, A. (2016). What Determines Purchasing-Power-Parity Exchange

Rates?. Revue d’économie du développement, 24(2), 93-141.

Jolliffe, D., & Prydz, E. B. (2015). Global poverty goals and prices: how purchasing power

parity matters. The World Bank.

Lothian, J. R. (2016). Purchasing power parity and the behavior of prices and nominal exchange

rates across exchange-rate regimes. Journal of International Money and Finance, 69, 5-

21.

Magud, N., & Sosa, S. (2013). When and why worry about real exchange rate appreciation? The

missing link between Dutch disease and growth. Journal of International Commerce,

Economics and Policy, 4(02), 1350009.

Malloy, M. M. S. (2013). Factors influencing emerging market central banks’ decision to

intervene in foreign exchange markets (No. 13-70). International Monetary Fund.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTERNATIONAL FINANCE

Miyajima, K., Mohanty, M. S., & Chan, T. (2015). Emerging market local currency bonds:

diversification and stability. Emerging Markets Review, 22, 126-139.

Rime, D., Schrimpf, A., & Syrstad, O. (2017). Segmented money markets and covered interest

parity arbitrage.

Ross, S. A. (2013). The arbitrage theory of capital asset pricing. In Handbook of the

fundamentals of financial decision making: Part I (pp. 11-30).

Twarowska, K., & Kakol, M. (2014). Analysis of Factors Affecting Fluctuations in the Exchange

Rate of Polish Zloty against Euro. In Human Capital without Borders: Knowledge and

Learning for Quality of Life; Proceedings of the Management, Knowledge and Learning

International Conference 2014 (pp. 889-896). ToKnowPress.

Van Deventer, D. R., Imai, K., & Mesler, M. (2013). Advanced financial risk management: tools

and techniques for integrated credit risk and interest rate risk management. John Wiley

& Sons.

Wong, A., Leung, D., & Ng, C. (2017). Risk-adjusted covered interest parity: theory and

evidence. Available at SSRN 2834798.

Yin, W., & Li, J. (2014). Macroeconomic fundamentals and the exchange rate dynamics: A no-

arbitrage macro-finance approach. Journal of International Money and Finance, 41, 46-

64.

INTERNATIONAL FINANCE

Miyajima, K., Mohanty, M. S., & Chan, T. (2015). Emerging market local currency bonds:

diversification and stability. Emerging Markets Review, 22, 126-139.

Rime, D., Schrimpf, A., & Syrstad, O. (2017). Segmented money markets and covered interest

parity arbitrage.

Ross, S. A. (2013). The arbitrage theory of capital asset pricing. In Handbook of the

fundamentals of financial decision making: Part I (pp. 11-30).

Twarowska, K., & Kakol, M. (2014). Analysis of Factors Affecting Fluctuations in the Exchange

Rate of Polish Zloty against Euro. In Human Capital without Borders: Knowledge and

Learning for Quality of Life; Proceedings of the Management, Knowledge and Learning

International Conference 2014 (pp. 889-896). ToKnowPress.

Van Deventer, D. R., Imai, K., & Mesler, M. (2013). Advanced financial risk management: tools

and techniques for integrated credit risk and interest rate risk management. John Wiley

& Sons.

Wong, A., Leung, D., & Ng, C. (2017). Risk-adjusted covered interest parity: theory and

evidence. Available at SSRN 2834798.

Yin, W., & Li, J. (2014). Macroeconomic fundamentals and the exchange rate dynamics: A no-

arbitrage macro-finance approach. Journal of International Money and Finance, 41, 46-

64.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.