International Finance Assignment: BHP, Bruin, Beacon, UniSuper

VerifiedAdded on 2022/12/29

|13

|3328

|40

Homework Assignment

AI Summary

This document provides a comprehensive solution to an international finance assignment, addressing key concepts and scenarios across multiple chapters. Chapter 3 analyzes how Citigroup can facilitate BHP Billiton's flow of funds, identifying relevant financial markets and optimal currency choices for a British subsidiary's loan. Chapter 5 examines factors affecting exchange rates for Bruin Aircraft, Pty Ltd. Chapter 6 explores scenarios for Beacon Lighting, including cost savings and currency risks associated with its relationship with Alibaba. Finally, Chapter 7 delves into UniSuper's investment strategies, including covered interest arbitrage and the associated risks of investing in Poland. The document offers detailed explanations, calculations, and analyses to provide a complete understanding of the assignment's requirements.

Running head: INTERNATIONAL FINANCE

International Finance

Name of the Student:

Name of the University:

Authors Note:

International Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

1

Table of Contents

Chapter 3 BHP Billiton:.............................................................................................................2

a. Explaining the various ways in which Citigroup could facilitate BHP’s Flow of funds,

while identifying the type of financial market where flow of funds occurs:.............................2

b. Indicating the characteristics that would help British subsidiary determine currency to

borrow:.......................................................................................................................................3

Chapter 5 Bruin Aircraft, Pty Ltd:.............................................................................................4

Chapter 6 Beacon Lighting:.......................................................................................................5

a. Describing the scenario that could allow Beacon to save more than 20 per cent on

production cost:..........................................................................................................................5

b. Describing the scenario that could allow Beacon to incur higher production cost, where

only parts are produced in Australia:.........................................................................................6

c. Explaining whether Beacon will have stable Australian dollar outflow payments to Alibaba

over the time:..............................................................................................................................6

d. Explaining whether Beacon risk changes at all as a result of its new relationship with

Alibaba:......................................................................................................................................7

Chapter 7 UniSuper:...................................................................................................................7

a. Indicating whether investments in Poland will be conducted without covering the position:

....................................................................................................................................................7

b. Suggesting the attempt on the converted interest arbitrage, while indicating the expected

return from using covered interest arbitrage:.............................................................................8

c. Stating what are the relevant risk involved in using the covered interest arbitrage:..............8

d. Indicating the choice that would be conducted for the relevant investments:.......................9

References and Bibliography:..................................................................................................10

1

Table of Contents

Chapter 3 BHP Billiton:.............................................................................................................2

a. Explaining the various ways in which Citigroup could facilitate BHP’s Flow of funds,

while identifying the type of financial market where flow of funds occurs:.............................2

b. Indicating the characteristics that would help British subsidiary determine currency to

borrow:.......................................................................................................................................3

Chapter 5 Bruin Aircraft, Pty Ltd:.............................................................................................4

Chapter 6 Beacon Lighting:.......................................................................................................5

a. Describing the scenario that could allow Beacon to save more than 20 per cent on

production cost:..........................................................................................................................5

b. Describing the scenario that could allow Beacon to incur higher production cost, where

only parts are produced in Australia:.........................................................................................6

c. Explaining whether Beacon will have stable Australian dollar outflow payments to Alibaba

over the time:..............................................................................................................................6

d. Explaining whether Beacon risk changes at all as a result of its new relationship with

Alibaba:......................................................................................................................................7

Chapter 7 UniSuper:...................................................................................................................7

a. Indicating whether investments in Poland will be conducted without covering the position:

....................................................................................................................................................7

b. Suggesting the attempt on the converted interest arbitrage, while indicating the expected

return from using covered interest arbitrage:.............................................................................8

c. Stating what are the relevant risk involved in using the covered interest arbitrage:..............8

d. Indicating the choice that would be conducted for the relevant investments:.......................9

References and Bibliography:..................................................................................................10

INTERNATIONAL FINANCE

2

Chapter 3 BHP Billiton:

a. Explaining the various ways in which Citigroup could facilitate BHP’s Flow of funds,

while identifying the type of financial market where flow of funds occurs:

There are different ways in which Citigroup could facilitate BHP’s Flow of funds for

impacting the performance of their subsidiaries. The measure that can be taken by the

Citigroup are depicted as follows.

Citigroup could become the underwriter between the subsidiary and the parent company

for effectively utilising the relevant preference shares and common stock. The

management of Citigroup can adequately arrange capital for both the subsidiary and the

parent company for supporting their production needs.

The second measure that can be adopted by Citigroup is the repatriation of dividends

from the subsidiary to the parent company. The bank can become the mediator between

the parent company and the subsidiary, where the overall income in form of dividend can

be transferred from subsidiary company to the parent organisation.

In the similar process, the bank can adequately issue relevant levels of loans to both the

parent company and the subsidiary for adequately improving their operational capability.

Furthermore, the bank can adequately become the official creditor of BHP Billiton and its

subsidiaries (Frieden, 2015).

The Citigroup can adequately purchase relevant bonds from both BHP Billiton and its

subsidiaries for adequately supplying the relevant level of funds to the organisations. The

whole transaction will directly occur in the bond market, which can be used by the bank

for adequately supporting both BHP and its subsidiaries.

2

Chapter 3 BHP Billiton:

a. Explaining the various ways in which Citigroup could facilitate BHP’s Flow of funds,

while identifying the type of financial market where flow of funds occurs:

There are different ways in which Citigroup could facilitate BHP’s Flow of funds for

impacting the performance of their subsidiaries. The measure that can be taken by the

Citigroup are depicted as follows.

Citigroup could become the underwriter between the subsidiary and the parent company

for effectively utilising the relevant preference shares and common stock. The

management of Citigroup can adequately arrange capital for both the subsidiary and the

parent company for supporting their production needs.

The second measure that can be adopted by Citigroup is the repatriation of dividends

from the subsidiary to the parent company. The bank can become the mediator between

the parent company and the subsidiary, where the overall income in form of dividend can

be transferred from subsidiary company to the parent organisation.

In the similar process, the bank can adequately issue relevant levels of loans to both the

parent company and the subsidiary for adequately improving their operational capability.

Furthermore, the bank can adequately become the official creditor of BHP Billiton and its

subsidiaries (Frieden, 2015).

The Citigroup can adequately purchase relevant bonds from both BHP Billiton and its

subsidiaries for adequately supplying the relevant level of funds to the organisations. The

whole transaction will directly occur in the bond market, which can be used by the bank

for adequately supporting both BHP and its subsidiaries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

3

The Citigroup can adequately increase the relevant exposure in the short-term securities

or commercial papers of both BHP Billiton and its subsidiaries for providing all the

relevant cash to BHP and its subsidiaries.

b. Indicating the characteristics that would help British subsidiary determine currency

to borrow:

The overall analysis is relevantly based on subsidiaries that operate in United

Kingdom, where it would be better to get loans in the local currency from the Branch of Citi

Bank. In addition, the use of local currency loan format would eventually allow the

organisation to minimise the level of risk exposure from the currency market. Moreover,

from the relevant evaluation, it can be detected that gathering the loan from United Kingdom

would eventually help the subsidiary for minimising the level of exposure in the currency risk

factors and other alternations, which might be conducted on future interest rates. The

reduction in the risk parameters would ensure the organisation to continue its activity without

incurring additional levels of expenses on the risk exposure.

However, the interest rate comparison directly reduces the level of exposure in the

current risk composition of the currency market, which might negatively affect the financial

viability of an investment. The organisation tends to use loans, which has the lowest level of

interest rates, as it aims in reduce the total cash outflow. However, the organisation needs to

accommodate additional factors such as the risk on currency conversion rate that needs to be

taken into consideration, while making relevant decisions regarding the loan requirements.

Therefore, the additional level of exchange rate risk, volatility and unpredictable nature of the

currencies is directly reflecting on the financial performance of the organisation (Cairncross,

2016).

3

The Citigroup can adequately increase the relevant exposure in the short-term securities

or commercial papers of both BHP Billiton and its subsidiaries for providing all the

relevant cash to BHP and its subsidiaries.

b. Indicating the characteristics that would help British subsidiary determine currency

to borrow:

The overall analysis is relevantly based on subsidiaries that operate in United

Kingdom, where it would be better to get loans in the local currency from the Branch of Citi

Bank. In addition, the use of local currency loan format would eventually allow the

organisation to minimise the level of risk exposure from the currency market. Moreover,

from the relevant evaluation, it can be detected that gathering the loan from United Kingdom

would eventually help the subsidiary for minimising the level of exposure in the currency risk

factors and other alternations, which might be conducted on future interest rates. The

reduction in the risk parameters would ensure the organisation to continue its activity without

incurring additional levels of expenses on the risk exposure.

However, the interest rate comparison directly reduces the level of exposure in the

current risk composition of the currency market, which might negatively affect the financial

viability of an investment. The organisation tends to use loans, which has the lowest level of

interest rates, as it aims in reduce the total cash outflow. However, the organisation needs to

accommodate additional factors such as the risk on currency conversion rate that needs to be

taken into consideration, while making relevant decisions regarding the loan requirements.

Therefore, the additional level of exchange rate risk, volatility and unpredictable nature of the

currencies is directly reflecting on the financial performance of the organisation (Cairncross,

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

4

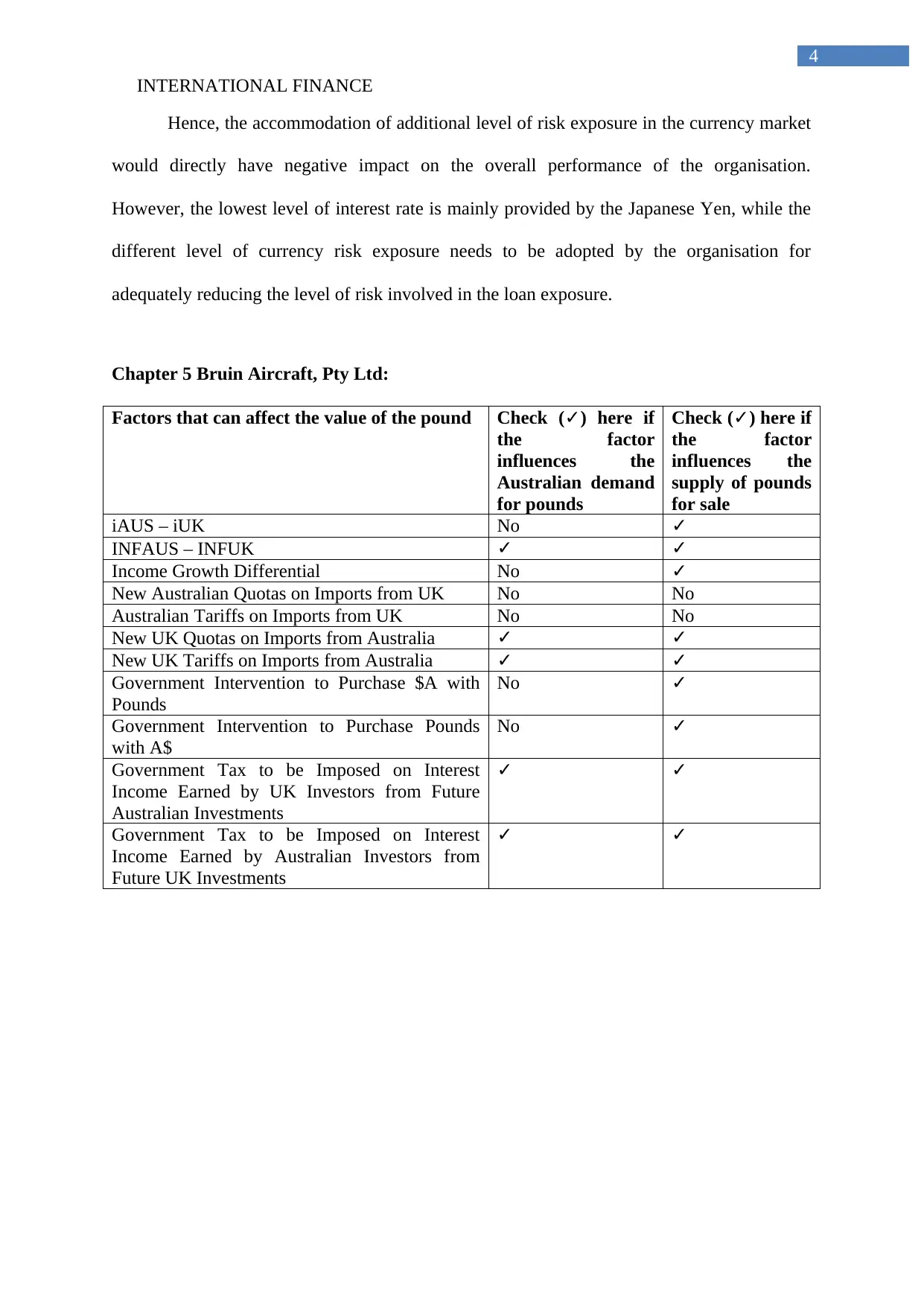

Hence, the accommodation of additional level of risk exposure in the currency market

would directly have negative impact on the overall performance of the organisation.

However, the lowest level of interest rate is mainly provided by the Japanese Yen, while the

different level of currency risk exposure needs to be adopted by the organisation for

adequately reducing the level of risk involved in the loan exposure.

Chapter 5 Bruin Aircraft, Pty Ltd:

Factors that can affect the value of the pound Check (✓) here if

the factor

influences the

Australian demand

for pounds

Check (✓) here if

the factor

influences the

supply of pounds

for sale

iAUS – iUK No ✓

INFAUS – INFUK ✓ ✓

Income Growth Differential No ✓

New Australian Quotas on Imports from UK No No

Australian Tariffs on Imports from UK No No

New UK Quotas on Imports from Australia ✓ ✓

New UK Tariffs on Imports from Australia ✓ ✓

Government Intervention to Purchase $A with

Pounds

No ✓

Government Intervention to Purchase Pounds

with A$

No ✓

Government Tax to be Imposed on Interest

Income Earned by UK Investors from Future

Australian Investments

✓ ✓

Government Tax to be Imposed on Interest

Income Earned by Australian Investors from

Future UK Investments

✓ ✓

4

Hence, the accommodation of additional level of risk exposure in the currency market

would directly have negative impact on the overall performance of the organisation.

However, the lowest level of interest rate is mainly provided by the Japanese Yen, while the

different level of currency risk exposure needs to be adopted by the organisation for

adequately reducing the level of risk involved in the loan exposure.

Chapter 5 Bruin Aircraft, Pty Ltd:

Factors that can affect the value of the pound Check (✓) here if

the factor

influences the

Australian demand

for pounds

Check (✓) here if

the factor

influences the

supply of pounds

for sale

iAUS – iUK No ✓

INFAUS – INFUK ✓ ✓

Income Growth Differential No ✓

New Australian Quotas on Imports from UK No No

Australian Tariffs on Imports from UK No No

New UK Quotas on Imports from Australia ✓ ✓

New UK Tariffs on Imports from Australia ✓ ✓

Government Intervention to Purchase $A with

Pounds

No ✓

Government Intervention to Purchase Pounds

with A$

No ✓

Government Tax to be Imposed on Interest

Income Earned by UK Investors from Future

Australian Investments

✓ ✓

Government Tax to be Imposed on Interest

Income Earned by Australian Investors from

Future UK Investments

✓ ✓

INTERNATIONAL FINANCE

5

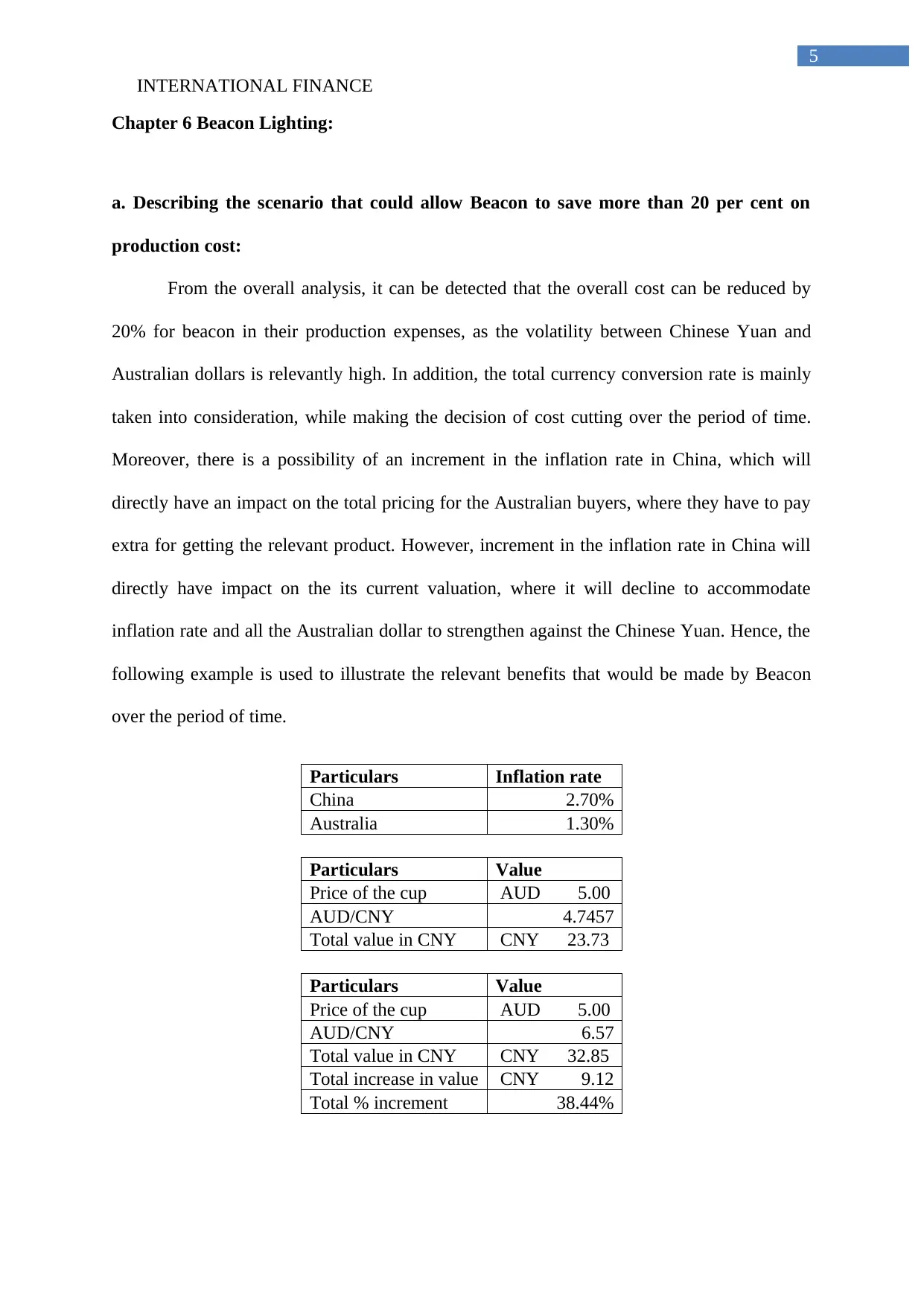

Chapter 6 Beacon Lighting:

a. Describing the scenario that could allow Beacon to save more than 20 per cent on

production cost:

From the overall analysis, it can be detected that the overall cost can be reduced by

20% for beacon in their production expenses, as the volatility between Chinese Yuan and

Australian dollars is relevantly high. In addition, the total currency conversion rate is mainly

taken into consideration, while making the decision of cost cutting over the period of time.

Moreover, there is a possibility of an increment in the inflation rate in China, which will

directly have an impact on the total pricing for the Australian buyers, where they have to pay

extra for getting the relevant product. However, increment in the inflation rate in China will

directly have impact on the its current valuation, where it will decline to accommodate

inflation rate and all the Australian dollar to strengthen against the Chinese Yuan. Hence, the

following example is used to illustrate the relevant benefits that would be made by Beacon

over the period of time.

Particulars Inflation rate

China 2.70%

Australia 1.30%

Particulars Value

Price of the cup AUD 5.00

AUD/CNY 4.7457

Total value in CNY CNY 23.73

Particulars Value

Price of the cup AUD 5.00

AUD/CNY 6.57

Total value in CNY CNY 32.85

Total increase in value CNY 9.12

Total % increment 38.44%

5

Chapter 6 Beacon Lighting:

a. Describing the scenario that could allow Beacon to save more than 20 per cent on

production cost:

From the overall analysis, it can be detected that the overall cost can be reduced by

20% for beacon in their production expenses, as the volatility between Chinese Yuan and

Australian dollars is relevantly high. In addition, the total currency conversion rate is mainly

taken into consideration, while making the decision of cost cutting over the period of time.

Moreover, there is a possibility of an increment in the inflation rate in China, which will

directly have an impact on the total pricing for the Australian buyers, where they have to pay

extra for getting the relevant product. However, increment in the inflation rate in China will

directly have impact on the its current valuation, where it will decline to accommodate

inflation rate and all the Australian dollar to strengthen against the Chinese Yuan. Hence, the

following example is used to illustrate the relevant benefits that would be made by Beacon

over the period of time.

Particulars Inflation rate

China 2.70%

Australia 1.30%

Particulars Value

Price of the cup AUD 5.00

AUD/CNY 4.7457

Total value in CNY CNY 23.73

Particulars Value

Price of the cup AUD 5.00

AUD/CNY 6.57

Total value in CNY CNY 32.85

Total increase in value CNY 9.12

Total % increment 38.44%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

6

Therefore, the above table directly provides information about the overall increment

in value of the products that needs to be paid by the Australian buyer in AUD, while

converting the values of AUD to CNY. Hence, from the analysis it can be detected that a total

increment in 38.44% has been assumed in the example. This increment has directly resulted

in a higher gain for the organisation, which is more than 20% (Frieden, 2016).

b. Describing the scenario that could allow Beacon to incur higher production cost,

where only parts are produced in Australia:

There is a relevant scenario that might have direct impact on the production cost of

beacon, which is directly related to its currency conversion rate. From the analysis, it is

detected that if the values of Chinese Yuan start to grow in comparison to AUD regardless of

the overall inflation rate. Then the total revenues that would be generated by Beacon will

have negative impact on its revenue generation capability. hence, the decline in the total

values that would be generated by the organisation will be impacted, while hampering the

total income, as the cost levels are higher and actual revenues would be lower. The company

will have lower income, as PPP wouldn’t apply and income that will be generated by the

organisation.

c. Explaining whether Beacon will have stable Australian dollar outflow payments to

Alibaba over the time:

The experience of stable Australian dollar outflow payments is directly subject to the

time value of money. From the relevant evaluation, it can be detected that Australian dollar

outflow payments will have direct impact on the performance of the organisation. Further

evaluation has stated that increment in the value of 1 AUD to CNY will directly result in

additional benefits to Beacon in comparison to the Alibaba, so he consignment will be

increase cash outflow.

6

Therefore, the above table directly provides information about the overall increment

in value of the products that needs to be paid by the Australian buyer in AUD, while

converting the values of AUD to CNY. Hence, from the analysis it can be detected that a total

increment in 38.44% has been assumed in the example. This increment has directly resulted

in a higher gain for the organisation, which is more than 20% (Frieden, 2016).

b. Describing the scenario that could allow Beacon to incur higher production cost,

where only parts are produced in Australia:

There is a relevant scenario that might have direct impact on the production cost of

beacon, which is directly related to its currency conversion rate. From the analysis, it is

detected that if the values of Chinese Yuan start to grow in comparison to AUD regardless of

the overall inflation rate. Then the total revenues that would be generated by Beacon will

have negative impact on its revenue generation capability. hence, the decline in the total

values that would be generated by the organisation will be impacted, while hampering the

total income, as the cost levels are higher and actual revenues would be lower. The company

will have lower income, as PPP wouldn’t apply and income that will be generated by the

organisation.

c. Explaining whether Beacon will have stable Australian dollar outflow payments to

Alibaba over the time:

The experience of stable Australian dollar outflow payments is directly subject to the

time value of money. From the relevant evaluation, it can be detected that Australian dollar

outflow payments will have direct impact on the performance of the organisation. Further

evaluation has stated that increment in the value of 1 AUD to CNY will directly result in

additional benefits to Beacon in comparison to the Alibaba, so he consignment will be

increase cash outflow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

7

d. Explaining whether Beacon risk changes at all as a result of its new relationship with

Alibaba:

The risk and volatility of Beacon mainly increases over the period of time, as China is

considered to be a volatile market, where Beacon is solely dependent on Alibaba for its

production goods and contractual agreement. Hence, Beacon needs to follow the contractual

agreement under 10-year time frame, where the 10-year time frame needs to be addressed.

Hence, the long term commitment will directly result in high level of risk towards the deal,

where exchange risk, market volatility, and financial corrections increase risk of Beacon for

generating high level of obligations that needs to be faced by the organisation. hence, the

tenurity of the deal can also pose relevant risk factor, which might increase risk exposure of

the organisation (Melvin & Norrbin, 2017).

Chapter 7 UniSuper:

a. Indicating whether investments in Poland will be conducted without covering the

position:

The general format for investing is to cover all the relevant positions before investing

in a country, where a single piece of information is relevantly used for detecting the

movement of volatility in a country. Therefore, from the relevant evaluation, it can be

detected that the information provided in the regarding the rates can go up and down by 40%,

which indicates about the high level of volatility that is present, as it indicates the level of

increment in both returns and risk. Hence, relevant strategy needs to be adopted by the

organisation for generating high level of income from investment. Thus, the analysis can

directly indicate that about the total level of risk that will be involved in the transaction. The

reduction in the currency conversion rate by a 40% volatility change will directly increase the

7

d. Explaining whether Beacon risk changes at all as a result of its new relationship with

Alibaba:

The risk and volatility of Beacon mainly increases over the period of time, as China is

considered to be a volatile market, where Beacon is solely dependent on Alibaba for its

production goods and contractual agreement. Hence, Beacon needs to follow the contractual

agreement under 10-year time frame, where the 10-year time frame needs to be addressed.

Hence, the long term commitment will directly result in high level of risk towards the deal,

where exchange risk, market volatility, and financial corrections increase risk of Beacon for

generating high level of obligations that needs to be faced by the organisation. hence, the

tenurity of the deal can also pose relevant risk factor, which might increase risk exposure of

the organisation (Melvin & Norrbin, 2017).

Chapter 7 UniSuper:

a. Indicating whether investments in Poland will be conducted without covering the

position:

The general format for investing is to cover all the relevant positions before investing

in a country, where a single piece of information is relevantly used for detecting the

movement of volatility in a country. Therefore, from the relevant evaluation, it can be

detected that the information provided in the regarding the rates can go up and down by 40%,

which indicates about the high level of volatility that is present, as it indicates the level of

increment in both returns and risk. Hence, relevant strategy needs to be adopted by the

organisation for generating high level of income from investment. Thus, the analysis can

directly indicate that about the total level of risk that will be involved in the transaction. The

reduction in the currency conversion rate by a 40% volatility change will directly increase the

INTERNATIONAL FINANCE

8

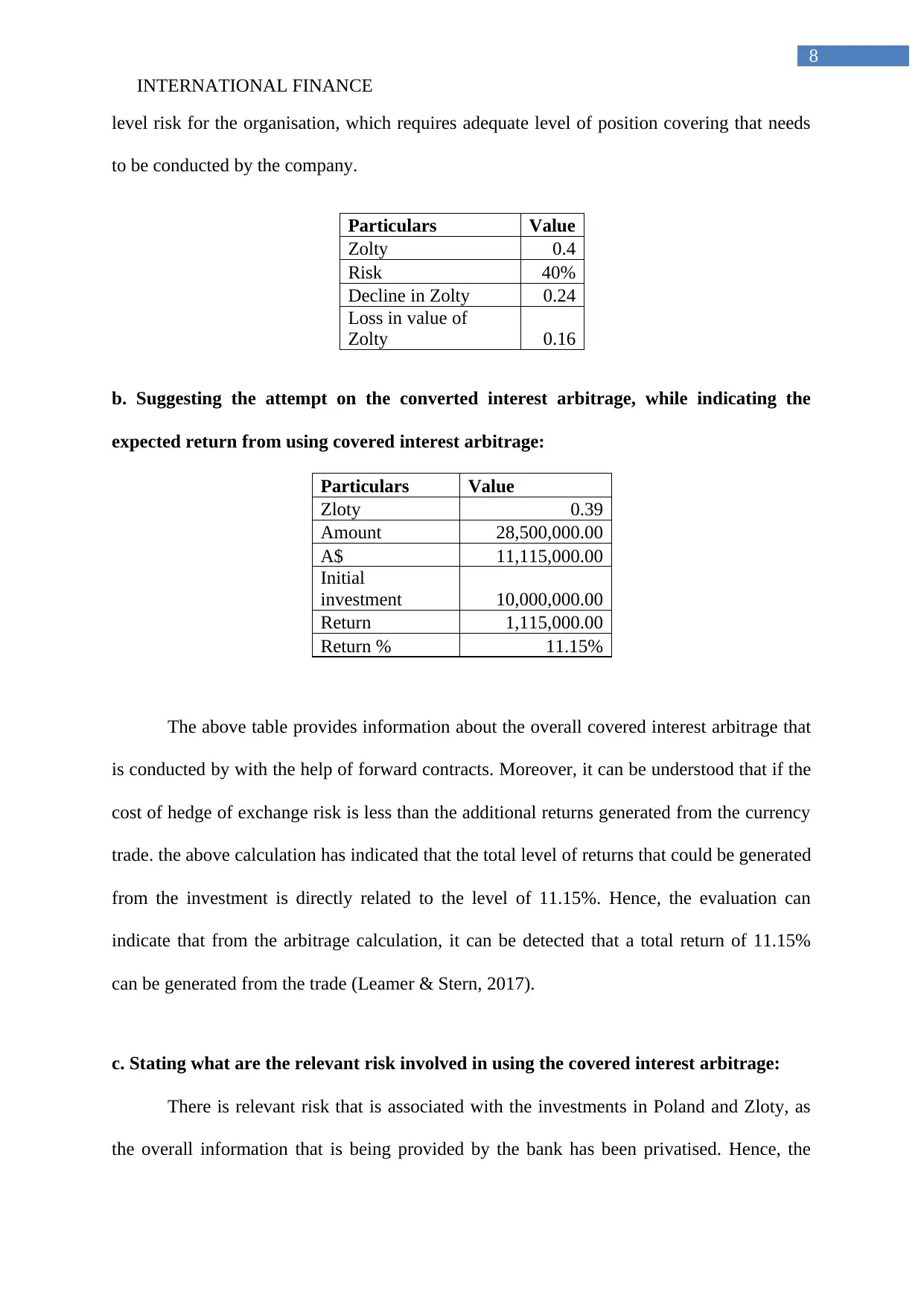

level risk for the organisation, which requires adequate level of position covering that needs

to be conducted by the company.

Particulars Value

Zolty 0.4

Risk 40%

Decline in Zolty 0.24

Loss in value of

Zolty 0.16

b. Suggesting the attempt on the converted interest arbitrage, while indicating the

expected return from using covered interest arbitrage:

Particulars Value

Zloty 0.39

Amount 28,500,000.00

A$ 11,115,000.00

Initial

investment 10,000,000.00

Return 1,115,000.00

Return % 11.15%

The above table provides information about the overall covered interest arbitrage that

is conducted by with the help of forward contracts. Moreover, it can be understood that if the

cost of hedge of exchange risk is less than the additional returns generated from the currency

trade. the above calculation has indicated that the total level of returns that could be generated

from the investment is directly related to the level of 11.15%. Hence, the evaluation can

indicate that from the arbitrage calculation, it can be detected that a total return of 11.15%

can be generated from the trade (Leamer & Stern, 2017).

c. Stating what are the relevant risk involved in using the covered interest arbitrage:

There is relevant risk that is associated with the investments in Poland and Zloty, as

the overall information that is being provided by the bank has been privatised. Hence, the

8

level risk for the organisation, which requires adequate level of position covering that needs

to be conducted by the company.

Particulars Value

Zolty 0.4

Risk 40%

Decline in Zolty 0.24

Loss in value of

Zolty 0.16

b. Suggesting the attempt on the converted interest arbitrage, while indicating the

expected return from using covered interest arbitrage:

Particulars Value

Zloty 0.39

Amount 28,500,000.00

A$ 11,115,000.00

Initial

investment 10,000,000.00

Return 1,115,000.00

Return % 11.15%

The above table provides information about the overall covered interest arbitrage that

is conducted by with the help of forward contracts. Moreover, it can be understood that if the

cost of hedge of exchange risk is less than the additional returns generated from the currency

trade. the above calculation has indicated that the total level of returns that could be generated

from the investment is directly related to the level of 11.15%. Hence, the evaluation can

indicate that from the arbitrage calculation, it can be detected that a total return of 11.15%

can be generated from the trade (Leamer & Stern, 2017).

c. Stating what are the relevant risk involved in using the covered interest arbitrage:

There is relevant risk that is associated with the investments in Poland and Zloty, as

the overall information that is being provided by the bank has been privatised. Hence, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

9

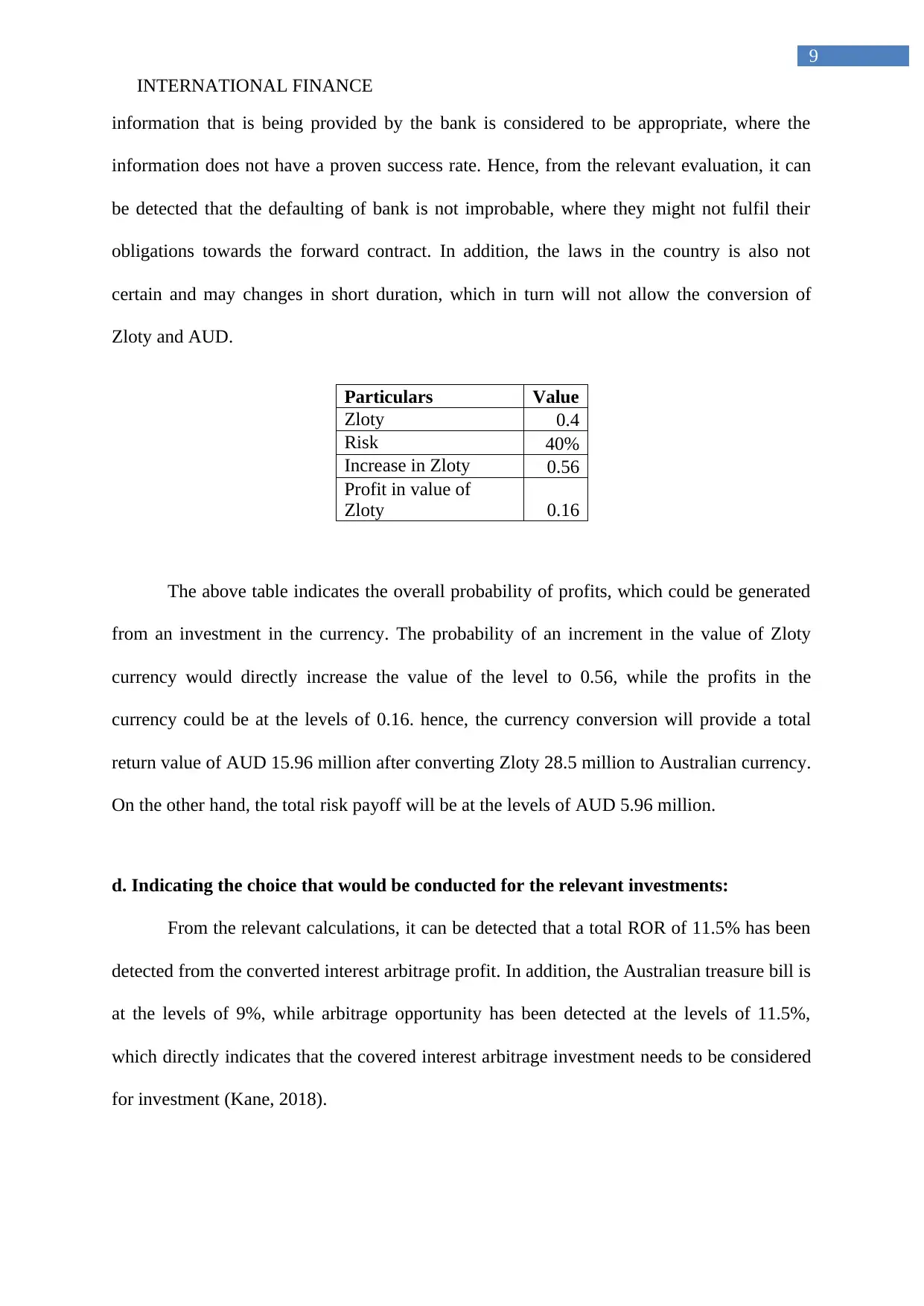

information that is being provided by the bank is considered to be appropriate, where the

information does not have a proven success rate. Hence, from the relevant evaluation, it can

be detected that the defaulting of bank is not improbable, where they might not fulfil their

obligations towards the forward contract. In addition, the laws in the country is also not

certain and may changes in short duration, which in turn will not allow the conversion of

Zloty and AUD.

Particulars Value

Zloty 0.4

Risk 40%

Increase in Zloty 0.56

Profit in value of

Zloty 0.16

The above table indicates the overall probability of profits, which could be generated

from an investment in the currency. The probability of an increment in the value of Zloty

currency would directly increase the value of the level to 0.56, while the profits in the

currency could be at the levels of 0.16. hence, the currency conversion will provide a total

return value of AUD 15.96 million after converting Zloty 28.5 million to Australian currency.

On the other hand, the total risk payoff will be at the levels of AUD 5.96 million.

d. Indicating the choice that would be conducted for the relevant investments:

From the relevant calculations, it can be detected that a total ROR of 11.5% has been

detected from the converted interest arbitrage profit. In addition, the Australian treasure bill is

at the levels of 9%, while arbitrage opportunity has been detected at the levels of 11.5%,

which directly indicates that the covered interest arbitrage investment needs to be considered

for investment (Kane, 2018).

9

information that is being provided by the bank is considered to be appropriate, where the

information does not have a proven success rate. Hence, from the relevant evaluation, it can

be detected that the defaulting of bank is not improbable, where they might not fulfil their

obligations towards the forward contract. In addition, the laws in the country is also not

certain and may changes in short duration, which in turn will not allow the conversion of

Zloty and AUD.

Particulars Value

Zloty 0.4

Risk 40%

Increase in Zloty 0.56

Profit in value of

Zloty 0.16

The above table indicates the overall probability of profits, which could be generated

from an investment in the currency. The probability of an increment in the value of Zloty

currency would directly increase the value of the level to 0.56, while the profits in the

currency could be at the levels of 0.16. hence, the currency conversion will provide a total

return value of AUD 15.96 million after converting Zloty 28.5 million to Australian currency.

On the other hand, the total risk payoff will be at the levels of AUD 5.96 million.

d. Indicating the choice that would be conducted for the relevant investments:

From the relevant calculations, it can be detected that a total ROR of 11.5% has been

detected from the converted interest arbitrage profit. In addition, the Australian treasure bill is

at the levels of 9%, while arbitrage opportunity has been detected at the levels of 11.5%,

which directly indicates that the covered interest arbitrage investment needs to be considered

for investment (Kane, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

10

References and Bibliography:

Al-Tamimi, H. A. H., Lafi, A. S., & Uddin, M. H. (2016). Bank image in the UAE:

Comparing Islamic and conventional banks. In Islamic Finance (pp. 46-65). Palgrave

Macmillan, Cham.

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Berger, A. N., El Ghoul, S., Guedhami, O., & Roman, R. A. (2016). Internationalization and

bank risk. Management Science, 63(7), 2283-2301.

Block, J. H., Cumming, D. J., & Vismara, S. (2017). International perspectives on venture

capital and bank finance for entrepreneurial firms. Economia e Politica

Industriale, 44(1), 3-22.

Borio, C., Gambacorta, L., & Hofmann, B. (2017). The influence of monetary policy on bank

profitability. International Finance, 20(1), 48-63.

Cairncross, A. (2016). Inflation, Growth and International Finance. Routledge.

Clemens, M. A., & Kremer, M. (2016). The new role for the World Bank. Journal of

Economic Perspectives, 30(1), 53-76.

Dagher, J. (2016). Benefits and costs of bank capital. International Monetary Fund.

10

References and Bibliography:

Al-Tamimi, H. A. H., Lafi, A. S., & Uddin, M. H. (2016). Bank image in the UAE:

Comparing Islamic and conventional banks. In Islamic Finance (pp. 46-65). Palgrave

Macmillan, Cham.

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Avdjiev, S., McCauley, R. N., & Shin, H. S. (2016). Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), 409-451.

Berger, A. N., El Ghoul, S., Guedhami, O., & Roman, R. A. (2016). Internationalization and

bank risk. Management Science, 63(7), 2283-2301.

Block, J. H., Cumming, D. J., & Vismara, S. (2017). International perspectives on venture

capital and bank finance for entrepreneurial firms. Economia e Politica

Industriale, 44(1), 3-22.

Borio, C., Gambacorta, L., & Hofmann, B. (2017). The influence of monetary policy on bank

profitability. International Finance, 20(1), 48-63.

Cairncross, A. (2016). Inflation, Growth and International Finance. Routledge.

Clemens, M. A., & Kremer, M. (2016). The new role for the World Bank. Journal of

Economic Perspectives, 30(1), 53-76.

Dagher, J. (2016). Benefits and costs of bank capital. International Monetary Fund.

INTERNATIONAL FINANCE

11

De Jonghe, O., & Öztekin, Ö. (2015). Bank capital management: International

evidence. Journal of Financial Intermediation, 24(2), 154-177.

Frieden, J. (2015). Banking on the world: the politics of American international finance.

Routledge.

Frieden, J. (2015). Banking on the world: the politics of American international finance.

Routledge.

Frieden, J. (2016). The governance of international finance. Annual Review of Political

Science, 19, 33-48.

Gandhi, P., & Lustig, H. (2015). Size anomalies in US bank stock returns. The Journal of

Finance, 70(2), 733-768.

García-Meca, E., García-Sánchez, I. M., & Martínez-Ferrero, J. (2015). Board diversity and

its effects on bank performance: An international analysis. Journal of Banking &

Finance, 53, 202-214.

Kane, D. R. (2018). Principles of international finance. Routledge.

Laeven, L., Ratnovski, L., & Tong, H. (2016). Bank size, capital, and systemic risk: Some

international evidence. Journal of Banking & Finance, 69, S25-S34.

Leamer, E. E., & Stern, R. M. (2017). Quantitative international economics. Routledge.

Melvin, M., & Norrbin, S. (2017). International money and finance. Academic Press.

Morais, B., Peydró, J. L., Roldán‐Peña, J., & Ruiz‐Ortega, C. (2019). The International Bank

Lending Channel of Monetary Policy Rates and QE: Credit Supply, Reach‐for‐Yield,

and Real Effects. The Journal of Finance, 74(1), 55-90.

11

De Jonghe, O., & Öztekin, Ö. (2015). Bank capital management: International

evidence. Journal of Financial Intermediation, 24(2), 154-177.

Frieden, J. (2015). Banking on the world: the politics of American international finance.

Routledge.

Frieden, J. (2015). Banking on the world: the politics of American international finance.

Routledge.

Frieden, J. (2016). The governance of international finance. Annual Review of Political

Science, 19, 33-48.

Gandhi, P., & Lustig, H. (2015). Size anomalies in US bank stock returns. The Journal of

Finance, 70(2), 733-768.

García-Meca, E., García-Sánchez, I. M., & Martínez-Ferrero, J. (2015). Board diversity and

its effects on bank performance: An international analysis. Journal of Banking &

Finance, 53, 202-214.

Kane, D. R. (2018). Principles of international finance. Routledge.

Laeven, L., Ratnovski, L., & Tong, H. (2016). Bank size, capital, and systemic risk: Some

international evidence. Journal of Banking & Finance, 69, S25-S34.

Leamer, E. E., & Stern, R. M. (2017). Quantitative international economics. Routledge.

Melvin, M., & Norrbin, S. (2017). International money and finance. Academic Press.

Morais, B., Peydró, J. L., Roldán‐Peña, J., & Ruiz‐Ortega, C. (2019). The International Bank

Lending Channel of Monetary Policy Rates and QE: Credit Supply, Reach‐for‐Yield,

and Real Effects. The Journal of Finance, 74(1), 55-90.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.