International Finance Assignment - Finance 101, University Name, 2024

VerifiedAdded on 2021/06/17

|13

|2738

|27

Homework Assignment

AI Summary

This international finance assignment solution covers a range of topics, starting with the theory of comparative advantage and its relevance in the current economic context. It then delves into the comparison of corporate governance regimes, including market-based, family-based, bank-based, and government-affiliated models. The assignment also explores the balance of payments through various transactions, the impossible trinity and its implications, and calculations of currency exchange rates and hedging strategies. Several questions analyze scenarios involving currency conversions, option trading, and the application of purchasing power parity. Furthermore, the assignment compares the effectiveness of forward rate, no hedge, and money market hedging techniques, with a recommendation on the most viable hedging option for an Australian-based company. The provided solution is designed to assist students with their understanding of key concepts in international finance.

Running head: INTERNATIONAL FINANCE

International Finance

Name of the Student:

Name of the University:

Authors Note:

International Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

1

Table of Contents

Question 1:.................................................................................................................................2

Question 2:.................................................................................................................................2

Question 3:.................................................................................................................................4

Question 4:.................................................................................................................................4

Question 5:.................................................................................................................................5

Question 6:.................................................................................................................................6

Question 7:.................................................................................................................................7

Question 8:.................................................................................................................................8

Question 9:.................................................................................................................................9

Question 10:...............................................................................................................................9

Reference and Bibliography:....................................................................................................12

1

Table of Contents

Question 1:.................................................................................................................................2

Question 2:.................................................................................................................................2

Question 3:.................................................................................................................................4

Question 4:.................................................................................................................................4

Question 5:.................................................................................................................................5

Question 6:.................................................................................................................................6

Question 7:.................................................................................................................................7

Question 8:.................................................................................................................................8

Question 9:.................................................................................................................................9

Question 10:...............................................................................................................................9

Reference and Bibliography:....................................................................................................12

INTERNATIONAL FINANCE

2

Question 1:

The theory of comparative advantage relevantly indicates the ability of a producer to

provide goods and services at lower opportunity cost in comparisons to other producers. In

addition, the principle of comparative advantage relevantly indicates the positive attribute,

where agents are willing to produce more and consume less of the goods, who have a

comparative advantage in the economic reality. Furthermore, the comparative advantage can

be identified as the overall progress obtained by industry such as technological progress,

endowments, and economic model, who increases the opportunity cost of the company or

producer.

In addition, David Ricardo developed the comparative advantage theory, where he

explained the efficiency of workers of developing an edge for the industry in the country. The

theory is effectively applicable in the current context, where the with the competitive hedge

companies can minimise the opportunity cost of goods and services. This increases their

competitive edge in the market and improves the level of profits that could be generated from

operations. The companies with competitive advantages are able to improve the level of

revenues, while reducing nay kind of extra expenses incurred from operations. In this context,

Borio, Gambacorta & Hofmann (2017) stated that with the use of skilled labour organisations

can reduce opportunity cost of production and maximise the profits from operations.

Question 2:

There are four corporate governance regimes such as Market-based, Family-based,

Bank-based and Government Affiliated, which has adequate difference and comparison for

the companies. The difference between the corporate regimes are depicted as follows.

.

2

Question 1:

The theory of comparative advantage relevantly indicates the ability of a producer to

provide goods and services at lower opportunity cost in comparisons to other producers. In

addition, the principle of comparative advantage relevantly indicates the positive attribute,

where agents are willing to produce more and consume less of the goods, who have a

comparative advantage in the economic reality. Furthermore, the comparative advantage can

be identified as the overall progress obtained by industry such as technological progress,

endowments, and economic model, who increases the opportunity cost of the company or

producer.

In addition, David Ricardo developed the comparative advantage theory, where he

explained the efficiency of workers of developing an edge for the industry in the country. The

theory is effectively applicable in the current context, where the with the competitive hedge

companies can minimise the opportunity cost of goods and services. This increases their

competitive edge in the market and improves the level of profits that could be generated from

operations. The companies with competitive advantages are able to improve the level of

revenues, while reducing nay kind of extra expenses incurred from operations. In this context,

Borio, Gambacorta & Hofmann (2017) stated that with the use of skilled labour organisations

can reduce opportunity cost of production and maximise the profits from operations.

Question 2:

There are four corporate governance regimes such as Market-based, Family-based,

Bank-based and Government Affiliated, which has adequate difference and comparison for

the companies. The difference between the corporate regimes are depicted as follows.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

3

Regimes Difference

Market based The characteristics of the regime relevantly

indicates the efficient market and dispersed

ownership of the regime

Family based This regime mainly combines both family

ownership and minority shareholders

Bank based The bank-based regimes are controlled by

governments and have lack of transparency

Government affiliated There are state ownership enterprises, where there

is lack of transparency

The major comparison between the overall regimes is the rule of corporate

governance, which needs to be followed by the companies operating in the region. In

addition, the laws and situations in the regimes could be conducted for improving the level of

returns that could be generated from operations. In addition, the regimes are a function of

financial market developments, with a degree of separation of owners and managers. In

addition, the regimes also have disclosure and transparency condition with a historical

development of legal system.

MNCs needs to be concerned regarding the difference in corporate governance

regimes, as it will affect their operational capability. In addition, the subsidiary in that region

will have to follow the rules and regulations of that country, while the actual mother company

will have different set of rules and corporate governance regimes. This increases the

difficulty for the company for effectively conducting its operations in all its companies

situated in different regimes (Frieden, 2015).

3

Regimes Difference

Market based The characteristics of the regime relevantly

indicates the efficient market and dispersed

ownership of the regime

Family based This regime mainly combines both family

ownership and minority shareholders

Bank based The bank-based regimes are controlled by

governments and have lack of transparency

Government affiliated There are state ownership enterprises, where there

is lack of transparency

The major comparison between the overall regimes is the rule of corporate

governance, which needs to be followed by the companies operating in the region. In

addition, the laws and situations in the regimes could be conducted for improving the level of

returns that could be generated from operations. In addition, the regimes are a function of

financial market developments, with a degree of separation of owners and managers. In

addition, the regimes also have disclosure and transparency condition with a historical

development of legal system.

MNCs needs to be concerned regarding the difference in corporate governance

regimes, as it will affect their operational capability. In addition, the subsidiary in that region

will have to follow the rules and regulations of that country, while the actual mother company

will have different set of rules and corporate governance regimes. This increases the

difficulty for the company for effectively conducting its operations in all its companies

situated in different regimes (Frieden, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

4

Question 3:

An Australian firm purchases a web hosting service from a US firm: Debt to the Australian

firm current account, while credit to the US firm current account.

Singaporean parents pay for their son’s study at an Australian university: Debit to the

Singaporean parents in the current account, while credit to the Australian university current

account.

A German company buys an insurance policy from a US insurer: Debit to the German

company financial account, while credit to the US insurer balance of payment.

An Indian firm pays the salary of its executive working for a subsidiary in Australia: Debit

to the current account of Indian firm, while credit to the executive working in subsidiary

Australian subsidiary.

An Australian firm buys 100% shares of a Malaysian company: Debt to the Australian

financial account, while credit to the financial account of the Malaysian company.

Question 4:

The impossible trinity is considered one of the unholy trinity, which is not possible by

the government to comply with all the three symptoms. The counties that have broken the

rules set by the impossible trinity has faced financial crisis, where the country faced cash

stagnation and investment problems. In addition, the impossible trinity relevantly indicates

that the government cannot implement a fixed foreign exchange rate, free capital movement

and an independent monetary policy at the same time, as it will directly have a negative

impact on its fiscal position. Moreover, it is also understood that impossible trinity hypothesis

is not possible theoretically and in real world practices, where the countries ignoring the

negative impact of impossible trinity has failed (Moffett, Stonehill & Eiteman, 2014).

4

Question 3:

An Australian firm purchases a web hosting service from a US firm: Debt to the Australian

firm current account, while credit to the US firm current account.

Singaporean parents pay for their son’s study at an Australian university: Debit to the

Singaporean parents in the current account, while credit to the Australian university current

account.

A German company buys an insurance policy from a US insurer: Debit to the German

company financial account, while credit to the US insurer balance of payment.

An Indian firm pays the salary of its executive working for a subsidiary in Australia: Debit

to the current account of Indian firm, while credit to the executive working in subsidiary

Australian subsidiary.

An Australian firm buys 100% shares of a Malaysian company: Debt to the Australian

financial account, while credit to the financial account of the Malaysian company.

Question 4:

The impossible trinity is considered one of the unholy trinity, which is not possible by

the government to comply with all the three symptoms. The counties that have broken the

rules set by the impossible trinity has faced financial crisis, where the country faced cash

stagnation and investment problems. In addition, the impossible trinity relevantly indicates

that the government cannot implement a fixed foreign exchange rate, free capital movement

and an independent monetary policy at the same time, as it will directly have a negative

impact on its fiscal position. Moreover, it is also understood that impossible trinity hypothesis

is not possible theoretically and in real world practices, where the countries ignoring the

negative impact of impossible trinity has failed (Moffett, Stonehill & Eiteman, 2014).

INTERNATIONAL FINANCE

5

In addition, the impossible trinity is considered to be one of the dilemmas, which

cannot be followed by governments in improving their economic growth. From the

experience of government, it could be identified that any two of impossible trinity could be

conducted for improving economic growth of the country. The violation of impossible trinity

measure was conducted by the Asian countries during the Asian crisis, which involved

Singapore, Thailand, Hong Kong, Malaysia, South Korea, Indonesia, and Philippines.

Moreover, the violation of impossible trinity has affected the Debt to GDP ratio of the

country, which substantially rose from 100% to 167%. This relevantly indicates that ignoring

the impossible trinity factors would lead to cash crunch and liquidity problems for the

government.

Therefore, from the evaluation of impossible trinity factors it could be identified that

the government and central banks needs to follow the measure of impossible trinity and

should not violate the factors. However, any violation of The Impossible Trinity would result

in economic crisis which was previously seen by the Asian countries (Avdjiev, McCauley &

Shin, 2016).

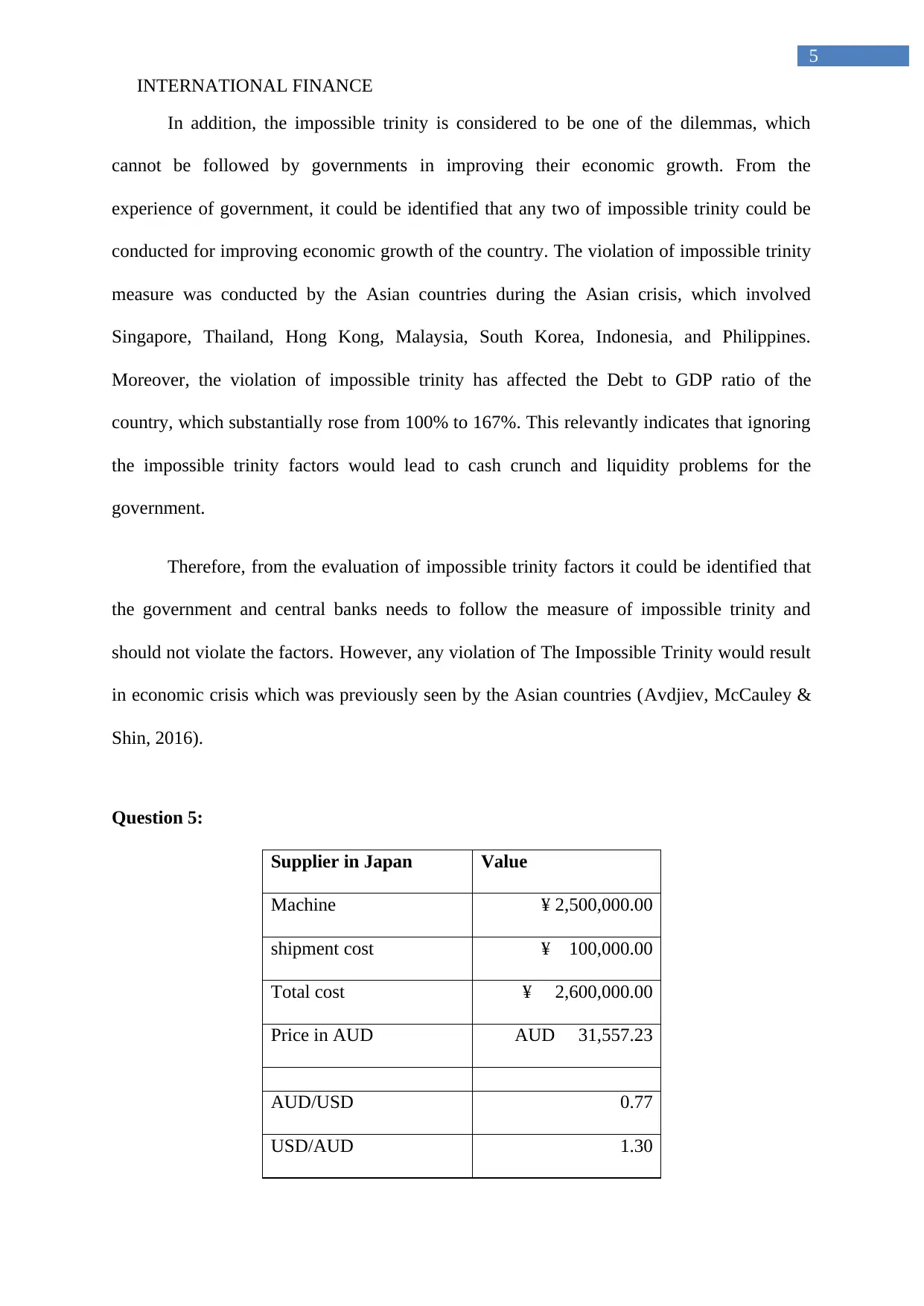

Question 5:

Supplier in Japan Value

Machine ¥ 2,500,000.00

shipment cost ¥ 100,000.00

Total cost ¥ 2,600,000.00

Price in AUD AUD 31,557.23

AUD/USD 0.77

USD/AUD 1.30

5

In addition, the impossible trinity is considered to be one of the dilemmas, which

cannot be followed by governments in improving their economic growth. From the

experience of government, it could be identified that any two of impossible trinity could be

conducted for improving economic growth of the country. The violation of impossible trinity

measure was conducted by the Asian countries during the Asian crisis, which involved

Singapore, Thailand, Hong Kong, Malaysia, South Korea, Indonesia, and Philippines.

Moreover, the violation of impossible trinity has affected the Debt to GDP ratio of the

country, which substantially rose from 100% to 167%. This relevantly indicates that ignoring

the impossible trinity factors would lead to cash crunch and liquidity problems for the

government.

Therefore, from the evaluation of impossible trinity factors it could be identified that

the government and central banks needs to follow the measure of impossible trinity and

should not violate the factors. However, any violation of The Impossible Trinity would result

in economic crisis which was previously seen by the Asian countries (Avdjiev, McCauley &

Shin, 2016).

Question 5:

Supplier in Japan Value

Machine ¥ 2,500,000.00

shipment cost ¥ 100,000.00

Total cost ¥ 2,600,000.00

Price in AUD AUD 31,557.23

AUD/USD 0.77

USD/AUD 1.30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

6

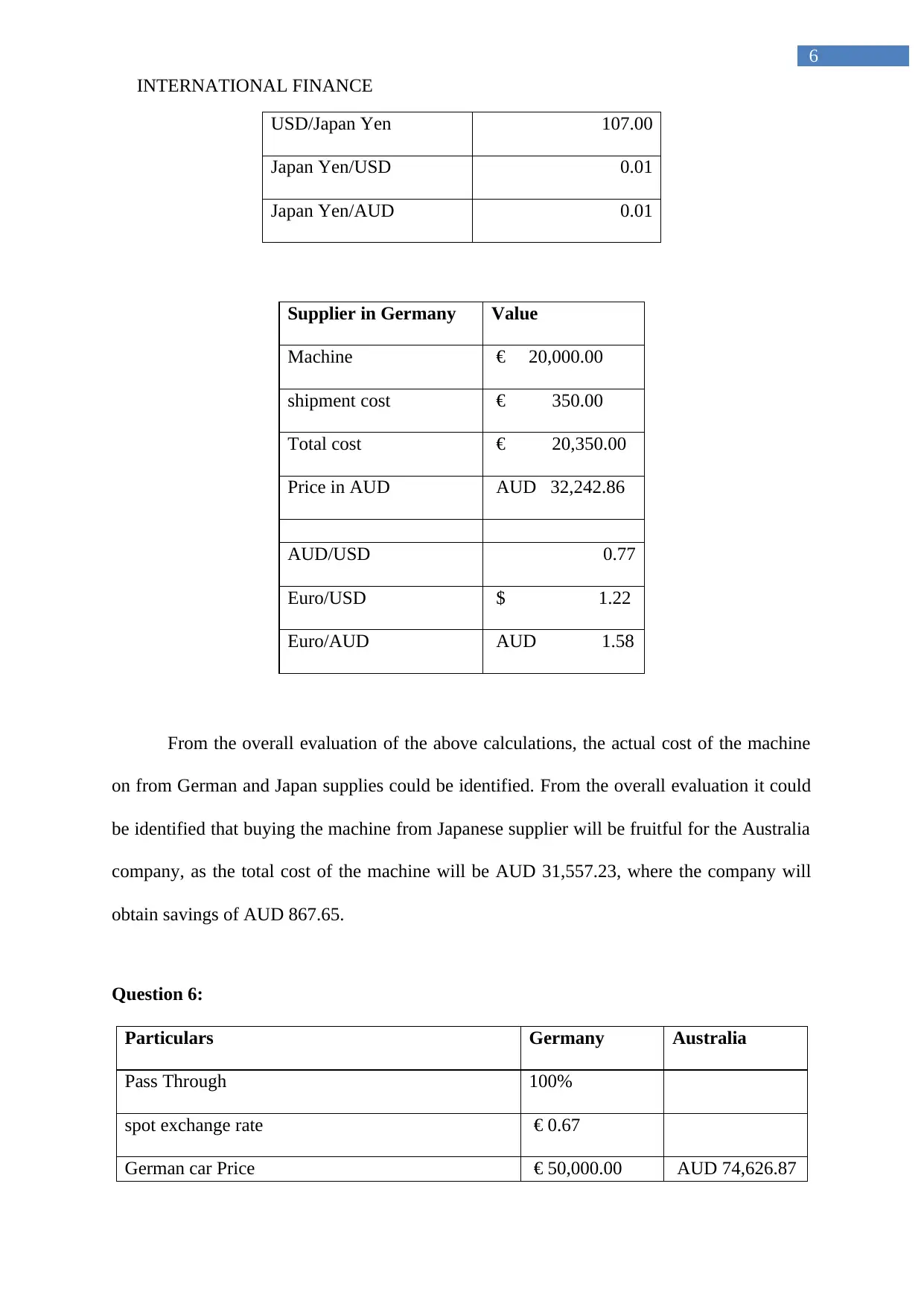

USD/Japan Yen 107.00

Japan Yen/USD 0.01

Japan Yen/AUD 0.01

Supplier in Germany Value

Machine € 20,000.00

shipment cost € 350.00

Total cost € 20,350.00

Price in AUD AUD 32,242.86

AUD/USD 0.77

Euro/USD $ 1.22

Euro/AUD AUD 1.58

From the overall evaluation of the above calculations, the actual cost of the machine

on from German and Japan supplies could be identified. From the overall evaluation it could

be identified that buying the machine from Japanese supplier will be fruitful for the Australia

company, as the total cost of the machine will be AUD 31,557.23, where the company will

obtain savings of AUD 867.65.

Question 6:

Particulars Germany Australia

Pass Through 100%

spot exchange rate € 0.67

German car Price € 50,000.00 AUD 74,626.87

6

USD/Japan Yen 107.00

Japan Yen/USD 0.01

Japan Yen/AUD 0.01

Supplier in Germany Value

Machine € 20,000.00

shipment cost € 350.00

Total cost € 20,350.00

Price in AUD AUD 32,242.86

AUD/USD 0.77

Euro/USD $ 1.22

Euro/AUD AUD 1.58

From the overall evaluation of the above calculations, the actual cost of the machine

on from German and Japan supplies could be identified. From the overall evaluation it could

be identified that buying the machine from Japanese supplier will be fruitful for the Australia

company, as the total cost of the machine will be AUD 31,557.23, where the company will

obtain savings of AUD 867.65.

Question 6:

Particulars Germany Australia

Pass Through 100%

spot exchange rate € 0.67

German car Price € 50,000.00 AUD 74,626.87

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

7

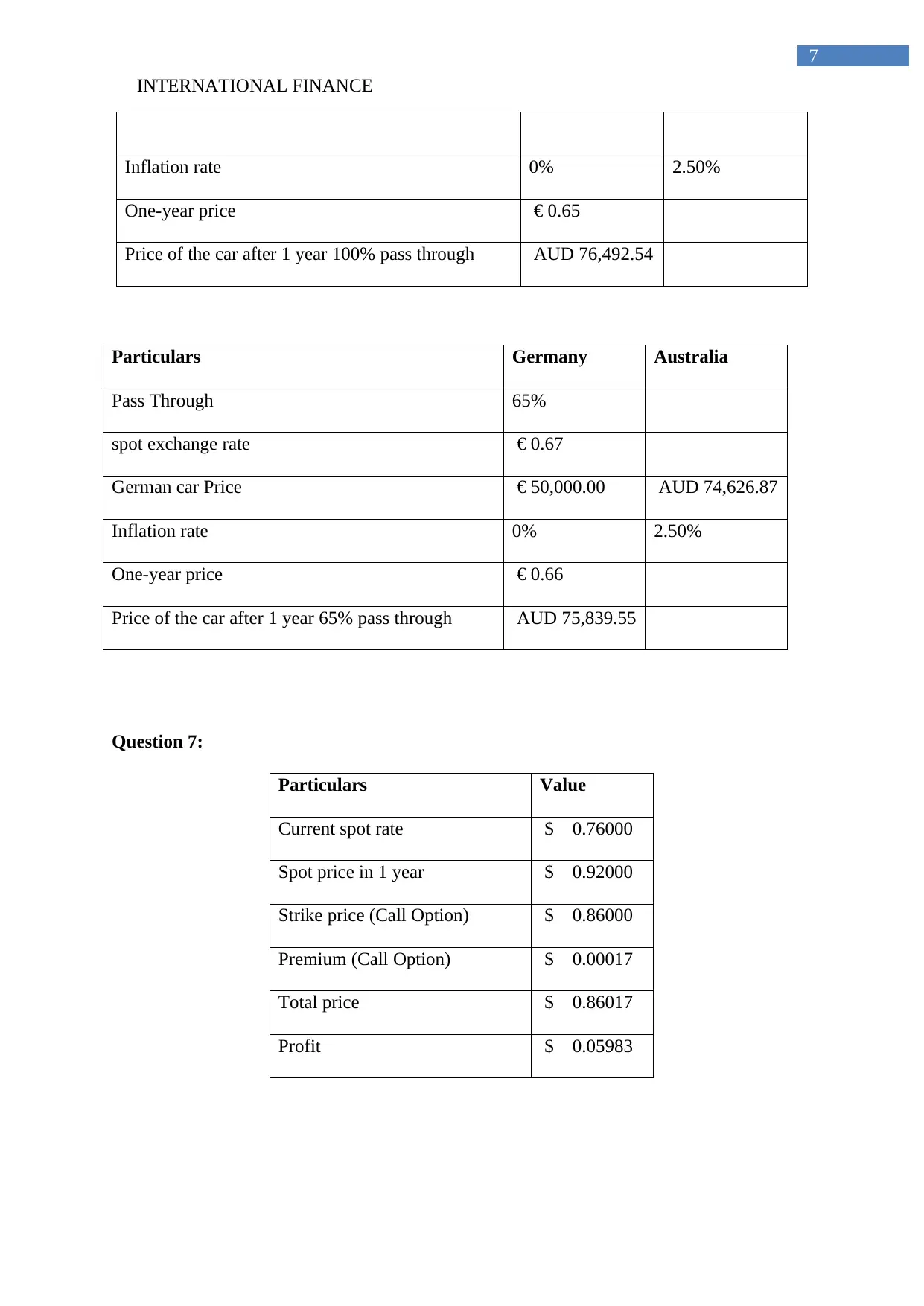

Inflation rate 0% 2.50%

One-year price € 0.65

Price of the car after 1 year 100% pass through AUD 76,492.54

Particulars Germany Australia

Pass Through 65%

spot exchange rate € 0.67

German car Price € 50,000.00 AUD 74,626.87

Inflation rate 0% 2.50%

One-year price € 0.66

Price of the car after 1 year 65% pass through AUD 75,839.55

Question 7:

Particulars Value

Current spot rate $ 0.76000

Spot price in 1 year $ 0.92000

Strike price (Call Option) $ 0.86000

Premium (Call Option) $ 0.00017

Total price $ 0.86017

Profit $ 0.05983

7

Inflation rate 0% 2.50%

One-year price € 0.65

Price of the car after 1 year 100% pass through AUD 76,492.54

Particulars Germany Australia

Pass Through 65%

spot exchange rate € 0.67

German car Price € 50,000.00 AUD 74,626.87

Inflation rate 0% 2.50%

One-year price € 0.66

Price of the car after 1 year 65% pass through AUD 75,839.55

Question 7:

Particulars Value

Current spot rate $ 0.76000

Spot price in 1 year $ 0.92000

Strike price (Call Option) $ 0.86000

Premium (Call Option) $ 0.00017

Total price $ 0.86017

Profit $ 0.05983

INTERNATIONAL FINANCE

8

From the overall evaluation it could be identified that using the call option will be

better for the forex trader, as increment in price is anticipated. Therefore, using the call option

could allow the forex trader to maximise the profits from investment. In addition, the net

profit that will be generated from trade is $ 0.05983.

Question 8:

The purchasing power parity is not an accurate estimator of future exchange rates, as

it is a theoretical measure, which is not possible in the real-world process. The purchasing

power parity only focuses on the exchange rate value, which aims in bringing parity towards

products sold between different nations. The currency exchange rate directly plays a vital role

in nullifying the purchasing power parity theory, as the demand for currency increases the

purchasing power conferred position of the currency relatively decline. In addition, the

purchasing power parity is also not able to comprehend the export and transportation charges

that is incurred by the importing country and is charged to the product. Therefore, it could be

assumed that the purchasing power parity is not able to estimate the actual future exchange

rates of country due to the lack of incorporating different factors affecting the prices of a

particular product (Titman, Keown & Martin, 2017).

The other reason that could be identified for the negative impact of purchasing power

parity is the use of derivatives, which allows the organization to minimize the negative

impact from rising currency value. Due to the presence of complicated financial instruments

the purchasing power parity is not able to subdue the actual theoretical value of a particular

currency. the presence of continuous hedging measure used by companies to reduce there is

from volatile currency market is directly affecting the accurateness of the purchasing power

parity theory. In the modern world the inflation rate does not accurately affect the currency

value of a country was different factors such as interest rates, demand, and supply of the

8

From the overall evaluation it could be identified that using the call option will be

better for the forex trader, as increment in price is anticipated. Therefore, using the call option

could allow the forex trader to maximise the profits from investment. In addition, the net

profit that will be generated from trade is $ 0.05983.

Question 8:

The purchasing power parity is not an accurate estimator of future exchange rates, as

it is a theoretical measure, which is not possible in the real-world process. The purchasing

power parity only focuses on the exchange rate value, which aims in bringing parity towards

products sold between different nations. The currency exchange rate directly plays a vital role

in nullifying the purchasing power parity theory, as the demand for currency increases the

purchasing power conferred position of the currency relatively decline. In addition, the

purchasing power parity is also not able to comprehend the export and transportation charges

that is incurred by the importing country and is charged to the product. Therefore, it could be

assumed that the purchasing power parity is not able to estimate the actual future exchange

rates of country due to the lack of incorporating different factors affecting the prices of a

particular product (Titman, Keown & Martin, 2017).

The other reason that could be identified for the negative impact of purchasing power

parity is the use of derivatives, which allows the organization to minimize the negative

impact from rising currency value. Due to the presence of complicated financial instruments

the purchasing power parity is not able to subdue the actual theoretical value of a particular

currency. the presence of continuous hedging measure used by companies to reduce there is

from volatile currency market is directly affecting the accurateness of the purchasing power

parity theory. In the modern world the inflation rate does not accurately affect the currency

value of a country was different factors such as interest rates, demand, and supply of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

9

currency in the currency market is used to determine the actual value of a particular currency.

Hence, the purchasing power parity is not able to accurately define the actual currency rate of

a country due to the lack of accommodating different external factors in evaluating the

currency value (Chinn & Kucko, 2015).

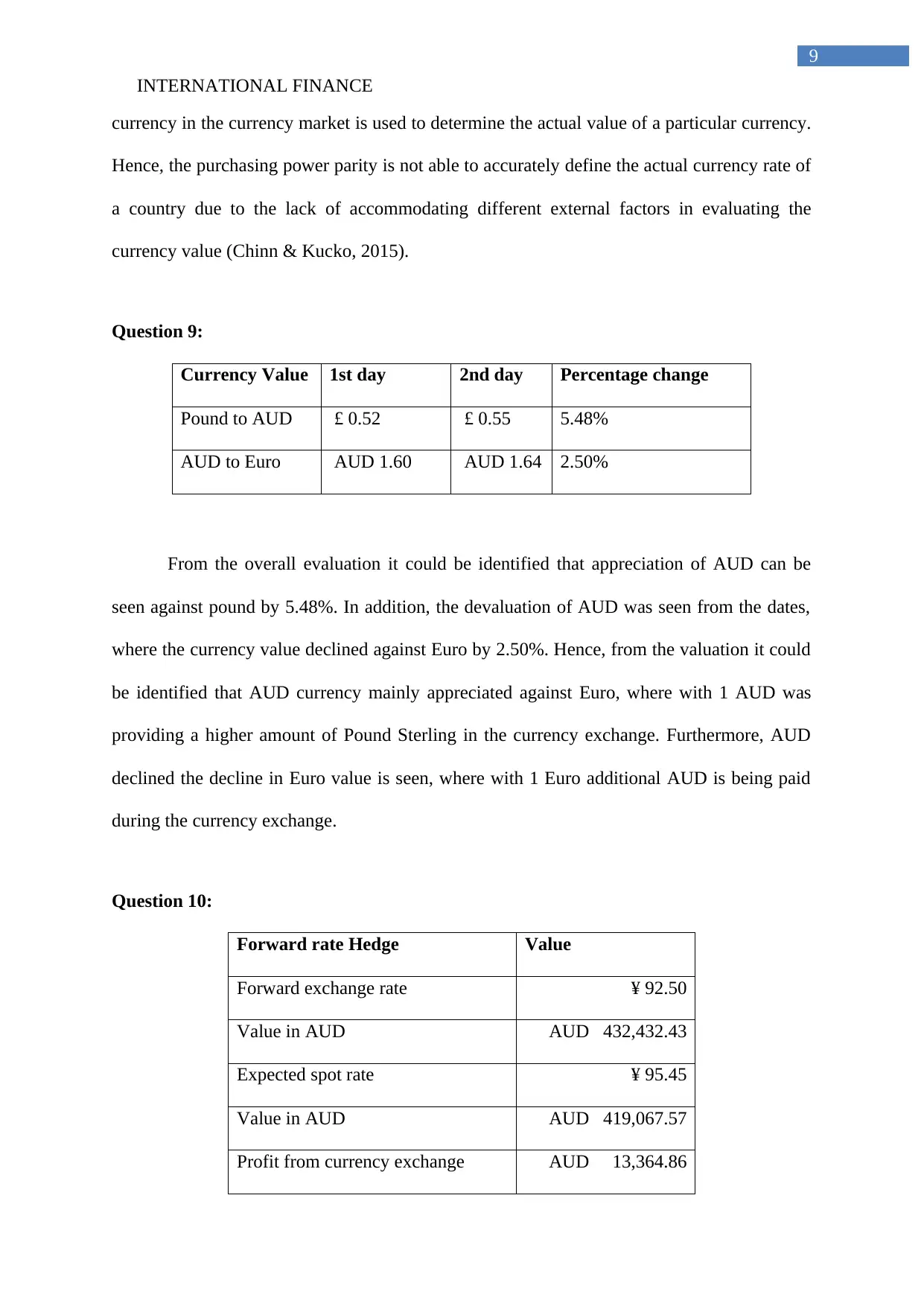

Question 9:

Currency Value 1st day 2nd day Percentage change

Pound to AUD £ 0.52 £ 0.55 5.48%

AUD to Euro AUD 1.60 AUD 1.64 2.50%

From the overall evaluation it could be identified that appreciation of AUD can be

seen against pound by 5.48%. In addition, the devaluation of AUD was seen from the dates,

where the currency value declined against Euro by 2.50%. Hence, from the valuation it could

be identified that AUD currency mainly appreciated against Euro, where with 1 AUD was

providing a higher amount of Pound Sterling in the currency exchange. Furthermore, AUD

declined the decline in Euro value is seen, where with 1 Euro additional AUD is being paid

during the currency exchange.

Question 10:

Forward rate Hedge Value

Forward exchange rate ¥ 92.50

Value in AUD AUD 432,432.43

Expected spot rate ¥ 95.45

Value in AUD AUD 419,067.57

Profit from currency exchange AUD 13,364.86

9

currency in the currency market is used to determine the actual value of a particular currency.

Hence, the purchasing power parity is not able to accurately define the actual currency rate of

a country due to the lack of accommodating different external factors in evaluating the

currency value (Chinn & Kucko, 2015).

Question 9:

Currency Value 1st day 2nd day Percentage change

Pound to AUD £ 0.52 £ 0.55 5.48%

AUD to Euro AUD 1.60 AUD 1.64 2.50%

From the overall evaluation it could be identified that appreciation of AUD can be

seen against pound by 5.48%. In addition, the devaluation of AUD was seen from the dates,

where the currency value declined against Euro by 2.50%. Hence, from the valuation it could

be identified that AUD currency mainly appreciated against Euro, where with 1 AUD was

providing a higher amount of Pound Sterling in the currency exchange. Furthermore, AUD

declined the decline in Euro value is seen, where with 1 Euro additional AUD is being paid

during the currency exchange.

Question 10:

Forward rate Hedge Value

Forward exchange rate ¥ 92.50

Value in AUD AUD 432,432.43

Expected spot rate ¥ 95.45

Value in AUD AUD 419,067.57

Profit from currency exchange AUD 13,364.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

10

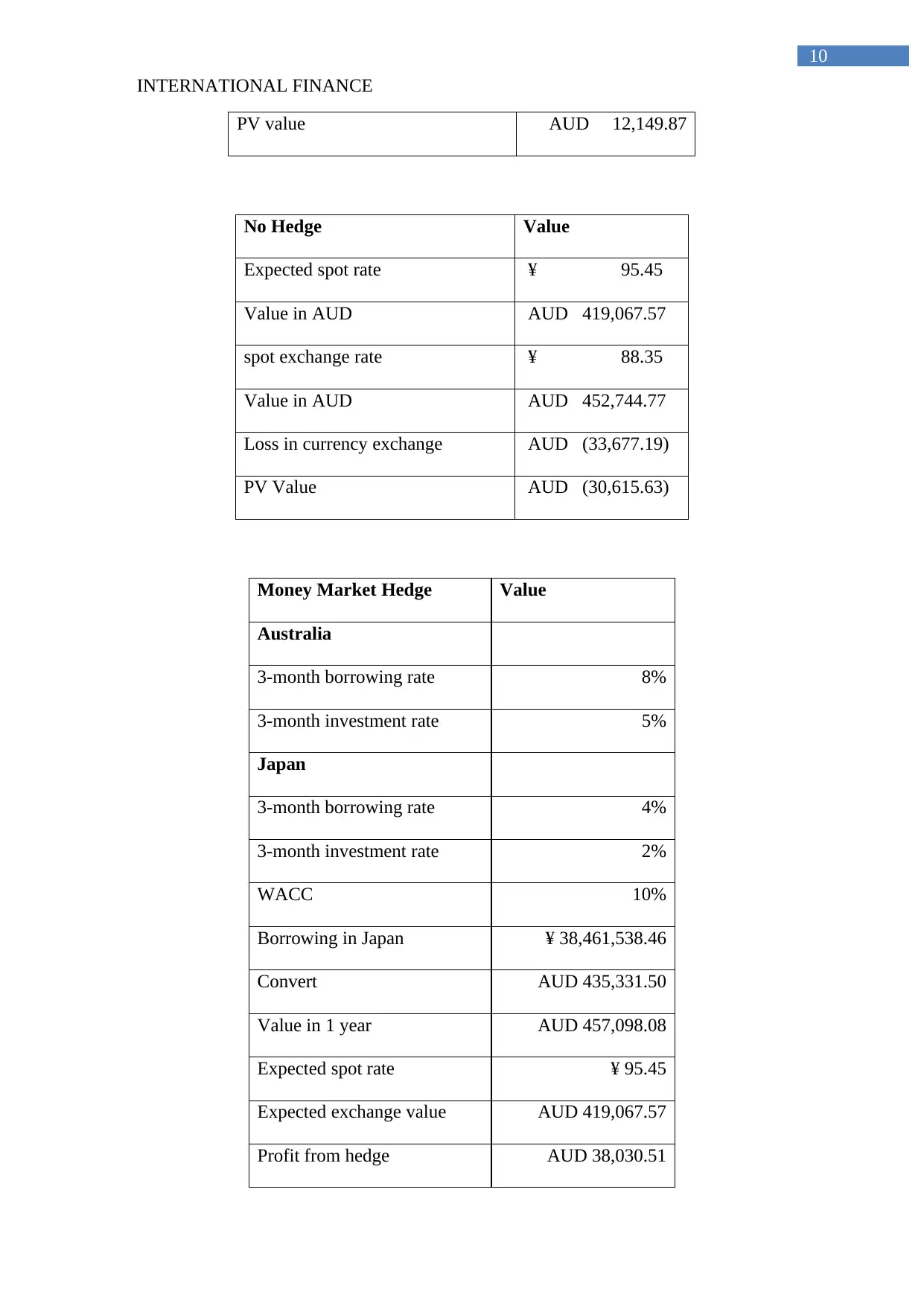

PV value AUD 12,149.87

No Hedge Value

Expected spot rate ¥ 95.45

Value in AUD AUD 419,067.57

spot exchange rate ¥ 88.35

Value in AUD AUD 452,744.77

Loss in currency exchange AUD (33,677.19)

PV Value AUD (30,615.63)

Money Market Hedge Value

Australia

3-month borrowing rate 8%

3-month investment rate 5%

Japan

3-month borrowing rate 4%

3-month investment rate 2%

WACC 10%

Borrowing in Japan ¥ 38,461,538.46

Convert AUD 435,331.50

Value in 1 year AUD 457,098.08

Expected spot rate ¥ 95.45

Expected exchange value AUD 419,067.57

Profit from hedge AUD 38,030.51

10

PV value AUD 12,149.87

No Hedge Value

Expected spot rate ¥ 95.45

Value in AUD AUD 419,067.57

spot exchange rate ¥ 88.35

Value in AUD AUD 452,744.77

Loss in currency exchange AUD (33,677.19)

PV Value AUD (30,615.63)

Money Market Hedge Value

Australia

3-month borrowing rate 8%

3-month investment rate 5%

Japan

3-month borrowing rate 4%

3-month investment rate 2%

WACC 10%

Borrowing in Japan ¥ 38,461,538.46

Convert AUD 435,331.50

Value in 1 year AUD 457,098.08

Expected spot rate ¥ 95.45

Expected exchange value AUD 419,067.57

Profit from hedge AUD 38,030.51

INTERNATIONAL FINANCE

11

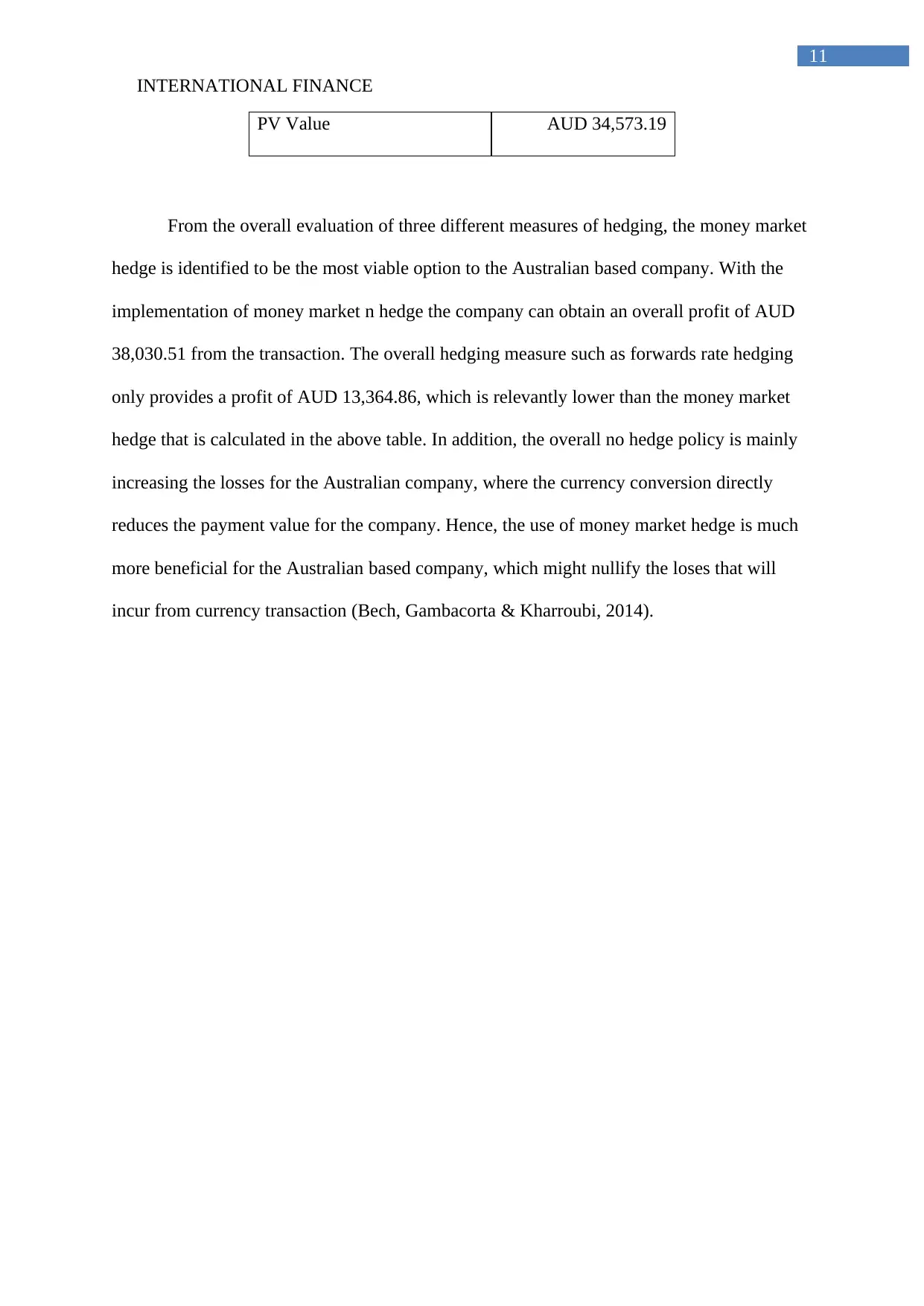

PV Value AUD 34,573.19

From the overall evaluation of three different measures of hedging, the money market

hedge is identified to be the most viable option to the Australian based company. With the

implementation of money market n hedge the company can obtain an overall profit of AUD

38,030.51 from the transaction. The overall hedging measure such as forwards rate hedging

only provides a profit of AUD 13,364.86, which is relevantly lower than the money market

hedge that is calculated in the above table. In addition, the overall no hedge policy is mainly

increasing the losses for the Australian company, where the currency conversion directly

reduces the payment value for the company. Hence, the use of money market hedge is much

more beneficial for the Australian based company, which might nullify the loses that will

incur from currency transaction (Bech, Gambacorta & Kharroubi, 2014).

11

PV Value AUD 34,573.19

From the overall evaluation of three different measures of hedging, the money market

hedge is identified to be the most viable option to the Australian based company. With the

implementation of money market n hedge the company can obtain an overall profit of AUD

38,030.51 from the transaction. The overall hedging measure such as forwards rate hedging

only provides a profit of AUD 13,364.86, which is relevantly lower than the money market

hedge that is calculated in the above table. In addition, the overall no hedge policy is mainly

increasing the losses for the Australian company, where the currency conversion directly

reduces the payment value for the company. Hence, the use of money market hedge is much

more beneficial for the Australian based company, which might nullify the loses that will

incur from currency transaction (Bech, Gambacorta & Kharroubi, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.