International Financial Analysis of Barclays Bank: A Report

VerifiedAdded on 2021/02/22

|12

|3112

|132

Report

AI Summary

This report provides a comprehensive financial analysis of Barclays Bank, focusing on its performance within the international financial environment. It examines the impact of global financial developments, such as changes in financial derivatives and market integration, on Barclays' operations. The report also delves into the essential elements of the bank's international financial and risk management strategy, including sources of finance and dividend policy, and assesses its financial performance using profitability, liquidity, efficiency, and investment ratios. The analysis covers the evaluation of financial and accounting ratios, providing insights into the bank's performance over the past two years, highlighting trends and challenges. The report concludes with an overview of the bank's strategic responses to the global financial landscape, including the management of climate-related challenges and the issuance of green mortgages.

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a) Developments in the international or global financial environment and its impact upon

Barclays bank.........................................................................................................................1

b) Essential elements of MNE’s international financial and risk management strategy........2

c) Evaluation of financial ratios and accounting ratios.........................................................3

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a) Developments in the international or global financial environment and its impact upon

Barclays bank.........................................................................................................................1

b) Essential elements of MNE’s international financial and risk management strategy........2

c) Evaluation of financial ratios and accounting ratios.........................................................3

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

International finance mainly recognized as a nation-wide business transaction among several

nations in terms of transferring of goods and services, financial transactions, foreign exchange

transactions (Frieden, 2016). There are numerous organizations that work at international stage

or are carried out as a result of changes in the global financial system. this context covers the

effect of changes throughout the global financial climate on the company's performance. As well

as key aspects on funding and risk assessment of corporations. The report is framed to execute

the financial aspects of Barclays bank. The challenges which are faced by organisation and how

it impacted the operations of entity defined in this report. financial analysis techniques are

applied in order to measure the complex business problems in international finance. Critical

evaluating and thinking process is used to concentrate towards suggested models and sections.

PART 1

a) Developments in the international or global financial environment and its impact upon

Barclays bank

Changing in international financial derivatives: The development seems to be the ongoing

growth of both the stock market on the global financial system. The transition involves expanded

use with the market for derivative (Frisari and Stadelmann, 2015). Has also increased the market

forces of diverse derivatives. Because of these developments, new businesses on the international

market could access and minimize the risks of financial instruments. Even after such positive

signs, Throughout the second half, Barclays recorded a decline in sales of than 80%. The

managing director stated banking consumers and investors had a "degree of caution," that kept

further cash in their deposits. Corporate clients were hindering on consolidation, mergers and

share market recapitalisations from important decisions. "The confusion organisation have about

Brexit obviously has an economic impact," Staley said. Jes Staley, its chief executive, informed

of both the effects of UK economic uncertainty over the coming year.

The new announcement by Barclays outweighs the additional £ 900 m that RBS put to rest

on while competitor Lloyds could announce a £ 1.8bn provision if it reports its third-quarter

results. Staley applauded the wealth management unit's results, that in the third quarter made

especially post-tax profits of £ 882 m, up 77% during the same time in 2018. Barclays was under

strain from shareholder activist Edward Bramson to restrain his competition of retail banking,

1

International finance mainly recognized as a nation-wide business transaction among several

nations in terms of transferring of goods and services, financial transactions, foreign exchange

transactions (Frieden, 2016). There are numerous organizations that work at international stage

or are carried out as a result of changes in the global financial system. this context covers the

effect of changes throughout the global financial climate on the company's performance. As well

as key aspects on funding and risk assessment of corporations. The report is framed to execute

the financial aspects of Barclays bank. The challenges which are faced by organisation and how

it impacted the operations of entity defined in this report. financial analysis techniques are

applied in order to measure the complex business problems in international finance. Critical

evaluating and thinking process is used to concentrate towards suggested models and sections.

PART 1

a) Developments in the international or global financial environment and its impact upon

Barclays bank

Changing in international financial derivatives: The development seems to be the ongoing

growth of both the stock market on the global financial system. The transition involves expanded

use with the market for derivative (Frisari and Stadelmann, 2015). Has also increased the market

forces of diverse derivatives. Because of these developments, new businesses on the international

market could access and minimize the risks of financial instruments. Even after such positive

signs, Throughout the second half, Barclays recorded a decline in sales of than 80%. The

managing director stated banking consumers and investors had a "degree of caution," that kept

further cash in their deposits. Corporate clients were hindering on consolidation, mergers and

share market recapitalisations from important decisions. "The confusion organisation have about

Brexit obviously has an economic impact," Staley said. Jes Staley, its chief executive, informed

of both the effects of UK economic uncertainty over the coming year.

The new announcement by Barclays outweighs the additional £ 900 m that RBS put to rest

on while competitor Lloyds could announce a £ 1.8bn provision if it reports its third-quarter

results. Staley applauded the wealth management unit's results, that in the third quarter made

especially post-tax profits of £ 882 m, up 77% during the same time in 2018. Barclays was under

strain from shareholder activist Edward Bramson to restrain his competition of retail banking,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that critics claim has absorbed much funds when providing stockholders less return on

investment.

Enhancing the integration and globalisation in financial market: It is one of the latest

changes throughout the global financial climate dimension. As regards it shifted, industry

liberalization has also been enhanced and technological advances was improved and the

communications infrastructure has also been strengthened (Kay, 2018). New companies can

expand their activities on a global level due to this shift in the global market in very moderate

manner. However, quicker access to the foreign marketplace allows for better allocation of

capital. Additionally, enhancements are being made to strategies that can help small and new

businesses make efficient improvements. There were three major challenges stood in front of

Barclays as climate variations extenuation investment, climate change adaptation investment and

strategic diversification and revolving business models. All these three challenges were perfectly

managed and controlled with effective change management.

Barclays is the first UK financial bank to deploy a Green Home Mortgage facility to its

clients. A new retail commodity which awards consumers from retail banking to buy a power-

efficient residence. Barclays provides a lower rate (compared to both the comparable key

mortgage area) for clients purchasing a new build house classified EPC A or B. This scheme

assists the banking sector to explicitly compensate people for trying an eco-friendly home,

adding real value to their spending on electricity bills. Barclays is capable to issue a UK green

mortgage worth € 500 m for the very first time, the profits of which are utilized to fund and

remortgage such green mortgages. As resulted the price of shares of Barclays plc increased by

b) Essential elements of MNE’s international financial and risk management strategy

Source of finance: There are two type of financial requirements occurs in a business as long

term and short term. Those same reports play a significant role in meeting the financial need.

However, the origin of funding can also influence the financial results of businesses. It's because

if a business does not have enough resources to finish its operations, they won't even be able to

maintain this in a competitive market (Vaubourg, 2016). At the other hand, if companies pay

economic support for higher costs, it could also affect their future growth. Financial markets are

becoming increasingly important as just a sources of corporate financing and expenditure, going

to continue its change in previous decades back from credit markets. Throughout Europe, bond

market expansion has absorbed 90 percent of the fall throughout bank credit since after the

2

investment.

Enhancing the integration and globalisation in financial market: It is one of the latest

changes throughout the global financial climate dimension. As regards it shifted, industry

liberalization has also been enhanced and technological advances was improved and the

communications infrastructure has also been strengthened (Kay, 2018). New companies can

expand their activities on a global level due to this shift in the global market in very moderate

manner. However, quicker access to the foreign marketplace allows for better allocation of

capital. Additionally, enhancements are being made to strategies that can help small and new

businesses make efficient improvements. There were three major challenges stood in front of

Barclays as climate variations extenuation investment, climate change adaptation investment and

strategic diversification and revolving business models. All these three challenges were perfectly

managed and controlled with effective change management.

Barclays is the first UK financial bank to deploy a Green Home Mortgage facility to its

clients. A new retail commodity which awards consumers from retail banking to buy a power-

efficient residence. Barclays provides a lower rate (compared to both the comparable key

mortgage area) for clients purchasing a new build house classified EPC A or B. This scheme

assists the banking sector to explicitly compensate people for trying an eco-friendly home,

adding real value to their spending on electricity bills. Barclays is capable to issue a UK green

mortgage worth € 500 m for the very first time, the profits of which are utilized to fund and

remortgage such green mortgages. As resulted the price of shares of Barclays plc increased by

b) Essential elements of MNE’s international financial and risk management strategy

Source of finance: There are two type of financial requirements occurs in a business as long

term and short term. Those same reports play a significant role in meeting the financial need.

However, the origin of funding can also influence the financial results of businesses. It's because

if a business does not have enough resources to finish its operations, they won't even be able to

maintain this in a competitive market (Vaubourg, 2016). At the other hand, if companies pay

economic support for higher costs, it could also affect their future growth. Financial markets are

becoming increasingly important as just a sources of corporate financing and expenditure, going

to continue its change in previous decades back from credit markets. Throughout Europe, bond

market expansion has absorbed 90 percent of the fall throughout bank credit since after the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial crisis. These trends will continue as the only non-US investment bank in both London

and New York to operate on a scale. Mortgage borrowing to corporations has decreased by 14

percent compared to GDP over the past few years. Around the same period, capital market

investment has been increasing, to private debt markets which is growing by 75% over the past

few years-and we are a top four participant in debt financial markets.

Dividend policy: It is an another factor that can influence financial results of companies.

Essentially, in terms of paying dividend to investors, the phrase dividends plan can be interpreted

as a rule that is linked to a structure. Here, it is important to understand that if dividends policy

does not favour investors, they would not be interested in investing in the potential period. And

also if the earnings policy is greater in order to make stakeholder payments, it can result in

business losses (Khan, 2015). It is therefore important to understand that pay out policy must be

in accordance with both investors and the firm's interest. Depending on bank's good equity base,

an increase of the dividends to 6.5p, as well as the repayment of costly subordinated bonds from

the financial recession, it is observed that a return of about £ 1.8bn of equity in 2018. Its 2018

full year dividend of 4.0p for every share will also be compensated on 5 April 2019 to

stockholders for whom the names were on the Register of Participants at the end of business on 1

March 2019. With a maximum of 2.5p per normal stock in the 2018 quarter-year dividends

payable in September 2018, the overall pay out for 2018 is 6.5p (2017: 3.0p) per ordinary share.

Dividends for the 2018 half year and full year amounted to £ 768 m (2017: £ 509 m). As the

fundamental income production, £ 4.2 billion is more than balanced by £ 2.1 billion in lawsuits

and fines for actions. As the financial institution addressed legacy issues, £ 1.7bn was

compensated and anticipated for normal dividends and AT1 discounts, and £ 1.0bn from

investment tools salvation.

c) Evaluation of financial ratios and accounting ratios.

Evaluation of financial performance of an entity is an essential term in order to meet

stakeholders and investors objectives. In organisational context evaluation of financial

performance is measured on the basis of calculated financial ratios. Financial ratios are

considered parameters that helps to calculate the performance of organisation (Ntuli, 2017).

Financial figures are collecting form balance sheets, income statements and formed in a

synchronised format to figure out financial ratios. Financial performance of Barclays will be

3

and New York to operate on a scale. Mortgage borrowing to corporations has decreased by 14

percent compared to GDP over the past few years. Around the same period, capital market

investment has been increasing, to private debt markets which is growing by 75% over the past

few years-and we are a top four participant in debt financial markets.

Dividend policy: It is an another factor that can influence financial results of companies.

Essentially, in terms of paying dividend to investors, the phrase dividends plan can be interpreted

as a rule that is linked to a structure. Here, it is important to understand that if dividends policy

does not favour investors, they would not be interested in investing in the potential period. And

also if the earnings policy is greater in order to make stakeholder payments, it can result in

business losses (Khan, 2015). It is therefore important to understand that pay out policy must be

in accordance with both investors and the firm's interest. Depending on bank's good equity base,

an increase of the dividends to 6.5p, as well as the repayment of costly subordinated bonds from

the financial recession, it is observed that a return of about £ 1.8bn of equity in 2018. Its 2018

full year dividend of 4.0p for every share will also be compensated on 5 April 2019 to

stockholders for whom the names were on the Register of Participants at the end of business on 1

March 2019. With a maximum of 2.5p per normal stock in the 2018 quarter-year dividends

payable in September 2018, the overall pay out for 2018 is 6.5p (2017: 3.0p) per ordinary share.

Dividends for the 2018 half year and full year amounted to £ 768 m (2017: £ 509 m). As the

fundamental income production, £ 4.2 billion is more than balanced by £ 2.1 billion in lawsuits

and fines for actions. As the financial institution addressed legacy issues, £ 1.7bn was

compensated and anticipated for normal dividends and AT1 discounts, and £ 1.0bn from

investment tools salvation.

c) Evaluation of financial ratios and accounting ratios.

Evaluation of financial performance of an entity is an essential term in order to meet

stakeholders and investors objectives. In organisational context evaluation of financial

performance is measured on the basis of calculated financial ratios. Financial ratios are

considered parameters that helps to calculate the performance of organisation (Ntuli, 2017).

Financial figures are collecting form balance sheets, income statements and formed in a

synchronised format to figure out financial ratios. Financial performance of Barclays will be

3

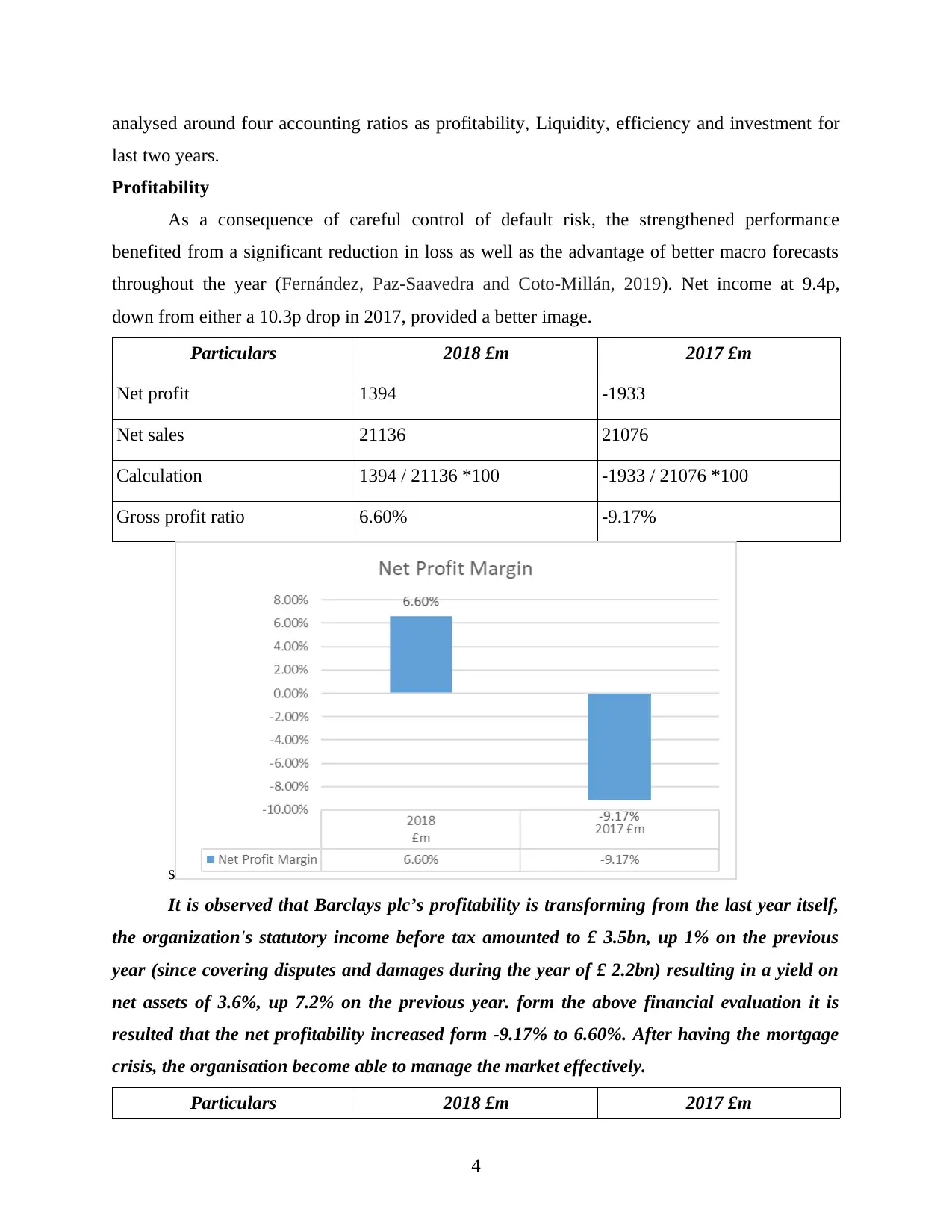

analysed around four accounting ratios as profitability, Liquidity, efficiency and investment for

last two years.

Profitability

As a consequence of careful control of default risk, the strengthened performance

benefited from a significant reduction in loss as well as the advantage of better macro forecasts

throughout the year (Fernández, Paz-Saavedra and Coto-Millán, 2019). Net income at 9.4p,

down from either a 10.3p drop in 2017, provided a better image.

Particulars 2018 £m 2017 £m

Net profit 1394 -1933

Net sales 21136 21076

Calculation 1394 / 21136 *100 -1933 / 21076 *100

Gross profit ratio 6.60% -9.17%

s

It is observed that Barclays plc’s profitability is transforming from the last year itself,

the organization's statutory income before tax amounted to £ 3.5bn, up 1% on the previous

year (since covering disputes and damages during the year of £ 2.2bn) resulting in a yield on

net assets of 3.6%, up 7.2% on the previous year. form the above financial evaluation it is

resulted that the net profitability increased form -9.17% to 6.60%. After having the mortgage

crisis, the organisation become able to manage the market effectively.

Particulars 2018 £m 2017 £m

4

last two years.

Profitability

As a consequence of careful control of default risk, the strengthened performance

benefited from a significant reduction in loss as well as the advantage of better macro forecasts

throughout the year (Fernández, Paz-Saavedra and Coto-Millán, 2019). Net income at 9.4p,

down from either a 10.3p drop in 2017, provided a better image.

Particulars 2018 £m 2017 £m

Net profit 1394 -1933

Net sales 21136 21076

Calculation 1394 / 21136 *100 -1933 / 21076 *100

Gross profit ratio 6.60% -9.17%

s

It is observed that Barclays plc’s profitability is transforming from the last year itself,

the organization's statutory income before tax amounted to £ 3.5bn, up 1% on the previous

year (since covering disputes and damages during the year of £ 2.2bn) resulting in a yield on

net assets of 3.6%, up 7.2% on the previous year. form the above financial evaluation it is

resulted that the net profitability increased form -9.17% to 6.60%. After having the mortgage

crisis, the organisation become able to manage the market effectively.

Particulars 2018 £m 2017 £m

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

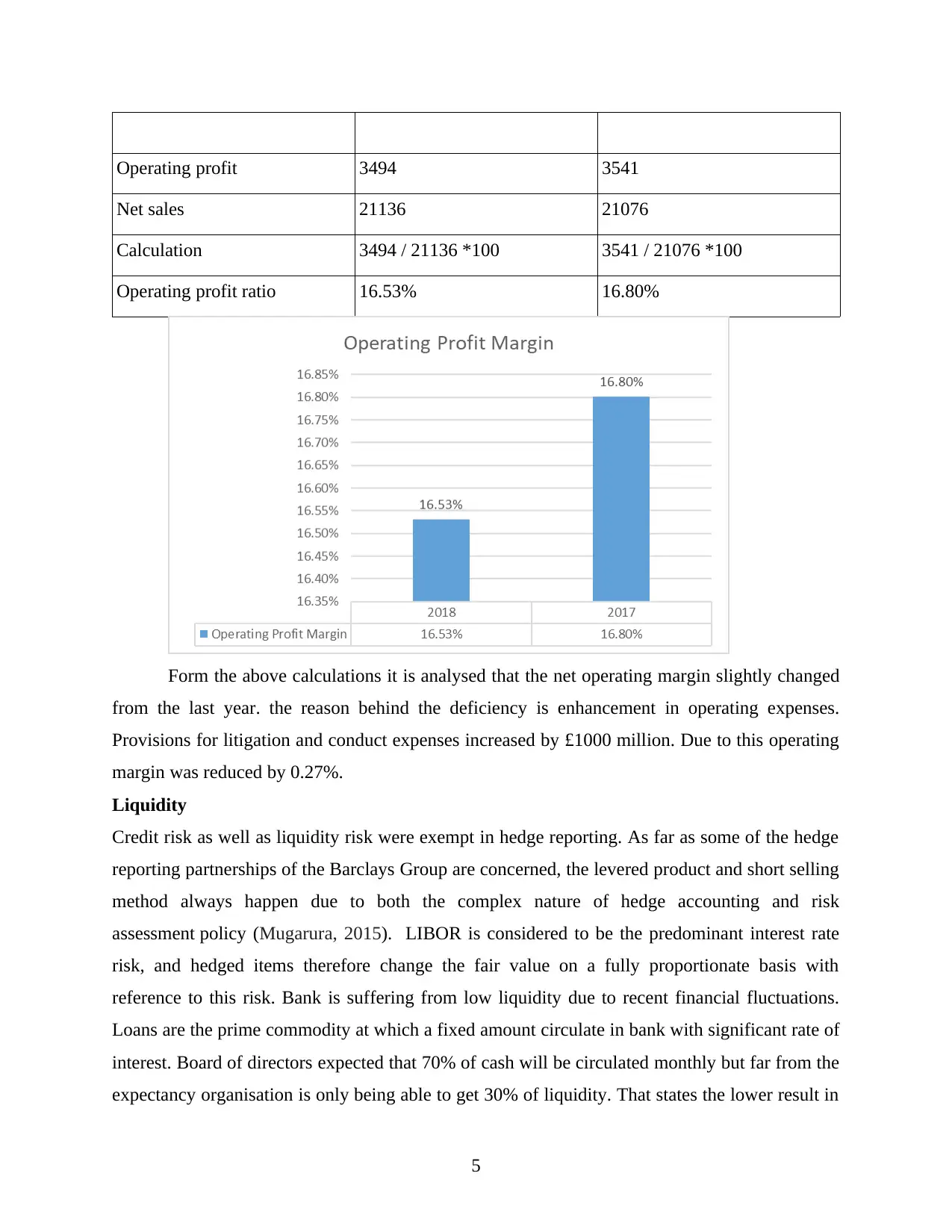

Operating profit 3494 3541

Net sales 21136 21076

Calculation 3494 / 21136 *100 3541 / 21076 *100

Operating profit ratio 16.53% 16.80%

Form the above calculations it is analysed that the net operating margin slightly changed

from the last year. the reason behind the deficiency is enhancement in operating expenses.

Provisions for litigation and conduct expenses increased by £1000 million. Due to this operating

margin was reduced by 0.27%.

Liquidity

Credit risk as well as liquidity risk were exempt in hedge reporting. As far as some of the hedge

reporting partnerships of the Barclays Group are concerned, the levered product and short selling

method always happen due to both the complex nature of hedge accounting and risk

assessment policy (Mugarura, 2015). LIBOR is considered to be the predominant interest rate

risk, and hedged items therefore change the fair value on a fully proportionate basis with

reference to this risk. Bank is suffering from low liquidity due to recent financial fluctuations.

Loans are the prime commodity at which a fixed amount circulate in bank with significant rate of

interest. Board of directors expected that 70% of cash will be circulated monthly but far from the

expectancy organisation is only being able to get 30% of liquidity. That states the lower result in

5

Net sales 21136 21076

Calculation 3494 / 21136 *100 3541 / 21076 *100

Operating profit ratio 16.53% 16.80%

Form the above calculations it is analysed that the net operating margin slightly changed

from the last year. the reason behind the deficiency is enhancement in operating expenses.

Provisions for litigation and conduct expenses increased by £1000 million. Due to this operating

margin was reduced by 0.27%.

Liquidity

Credit risk as well as liquidity risk were exempt in hedge reporting. As far as some of the hedge

reporting partnerships of the Barclays Group are concerned, the levered product and short selling

method always happen due to both the complex nature of hedge accounting and risk

assessment policy (Mugarura, 2015). LIBOR is considered to be the predominant interest rate

risk, and hedged items therefore change the fair value on a fully proportionate basis with

reference to this risk. Bank is suffering from low liquidity due to recent financial fluctuations.

Loans are the prime commodity at which a fixed amount circulate in bank with significant rate of

interest. Board of directors expected that 70% of cash will be circulated monthly but far from the

expectancy organisation is only being able to get 30% of liquidity. That states the lower result in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

terms of liquidity. The reason behind the low liquidity is low interest on short term loans

compare to other short term loans and advances.

Efficiency ratios

This ratio evaluates the capital and assets structure that how much the assets are being

used in operations to generate the returns (Goudkamp, 2017).

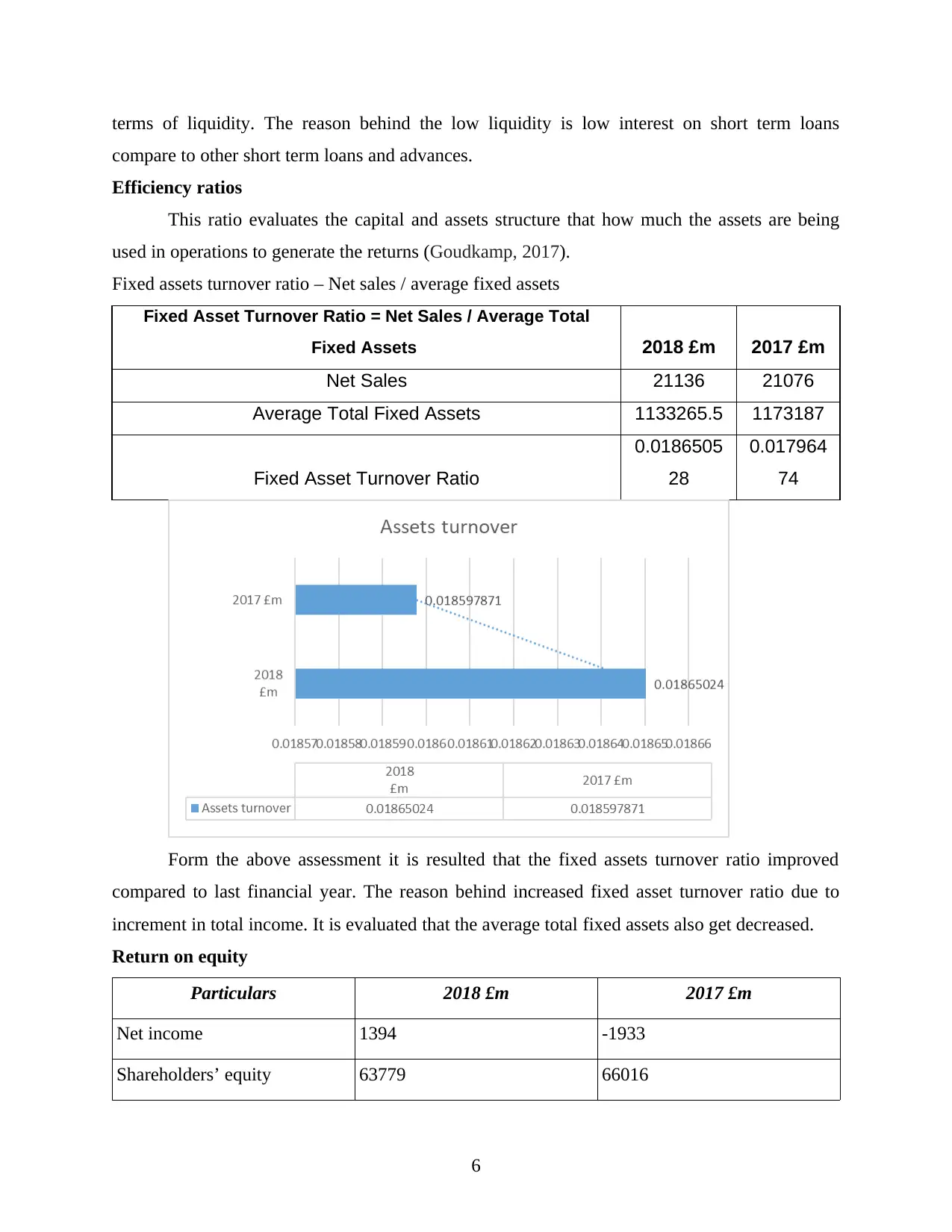

Fixed assets turnover ratio – Net sales / average fixed assets

Fixed Asset Turnover Ratio = Net Sales / Average Total

Fixed Assets 2018 £m 2017 £m

Net Sales 21136 21076

Average Total Fixed Assets 1133265.5 1173187

Fixed Asset Turnover Ratio

0.0186505

28

0.017964

74

Form the above assessment it is resulted that the fixed assets turnover ratio improved

compared to last financial year. The reason behind increased fixed asset turnover ratio due to

increment in total income. It is evaluated that the average total fixed assets also get decreased.

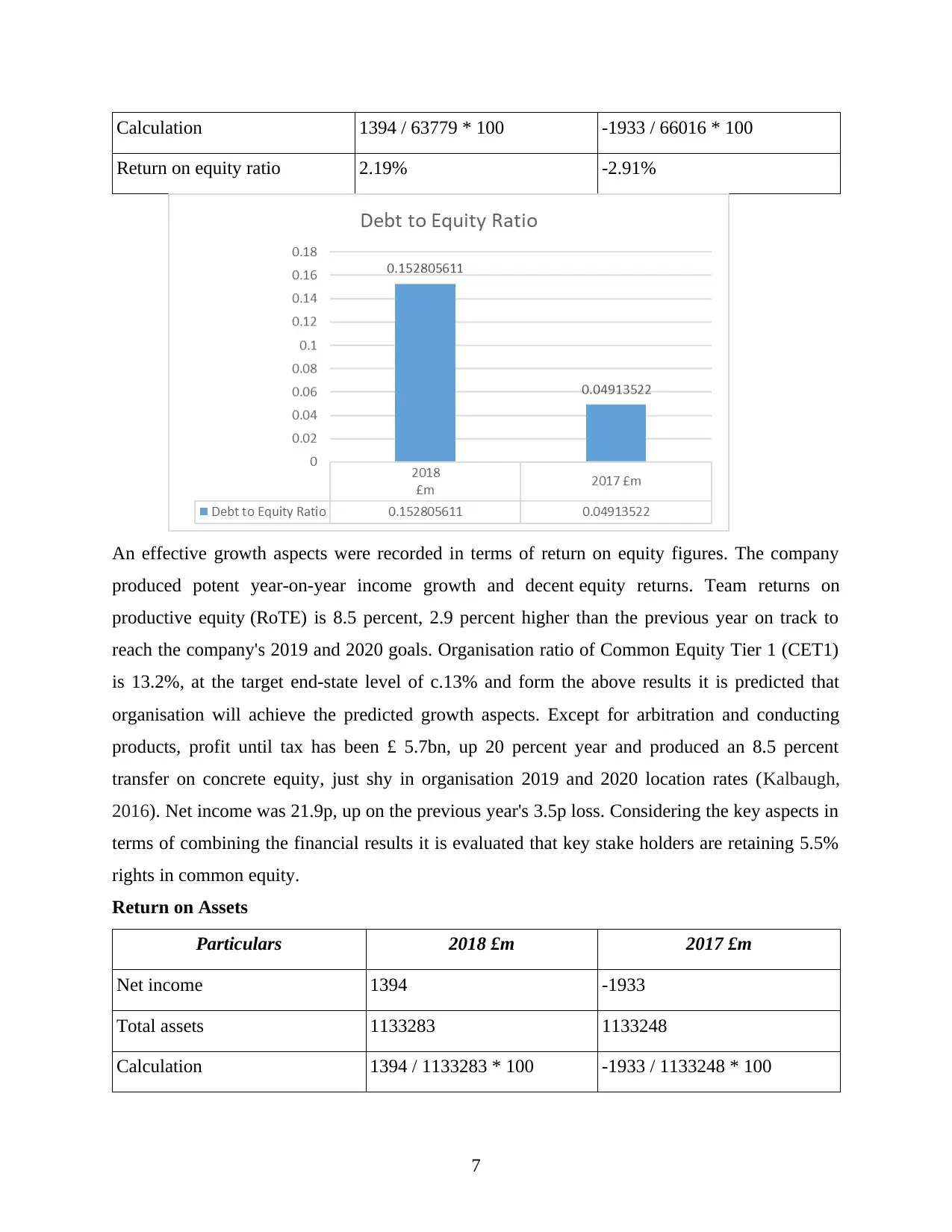

Return on equity

Particulars 2018 £m 2017 £m

Net income 1394 -1933

Shareholders’ equity 63779 66016

6

compare to other short term loans and advances.

Efficiency ratios

This ratio evaluates the capital and assets structure that how much the assets are being

used in operations to generate the returns (Goudkamp, 2017).

Fixed assets turnover ratio – Net sales / average fixed assets

Fixed Asset Turnover Ratio = Net Sales / Average Total

Fixed Assets 2018 £m 2017 £m

Net Sales 21136 21076

Average Total Fixed Assets 1133265.5 1173187

Fixed Asset Turnover Ratio

0.0186505

28

0.017964

74

Form the above assessment it is resulted that the fixed assets turnover ratio improved

compared to last financial year. The reason behind increased fixed asset turnover ratio due to

increment in total income. It is evaluated that the average total fixed assets also get decreased.

Return on equity

Particulars 2018 £m 2017 £m

Net income 1394 -1933

Shareholders’ equity 63779 66016

6

Calculation 1394 / 63779 * 100 -1933 / 66016 * 100

Return on equity ratio 2.19% -2.91%

An effective growth aspects were recorded in terms of return on equity figures. The company

produced potent year-on-year income growth and decent equity returns. Team returns on

productive equity (RoTE) is 8.5 percent, 2.9 percent higher than the previous year on track to

reach the company's 2019 and 2020 goals. Organisation ratio of Common Equity Tier 1 (CET1)

is 13.2%, at the target end-state level of c.13% and form the above results it is predicted that

organisation will achieve the predicted growth aspects. Except for arbitration and conducting

products, profit until tax has been £ 5.7bn, up 20 percent year and produced an 8.5 percent

transfer on concrete equity, just shy in organisation 2019 and 2020 location rates (Kalbaugh,

2016). Net income was 21.9p, up on the previous year's 3.5p loss. Considering the key aspects in

terms of combining the financial results it is evaluated that key stake holders are retaining 5.5%

rights in common equity.

Return on Assets

Particulars 2018 £m 2017 £m

Net income 1394 -1933

Total assets 1133283 1133248

Calculation 1394 / 1133283 * 100 -1933 / 1133248 * 100

7

Return on equity ratio 2.19% -2.91%

An effective growth aspects were recorded in terms of return on equity figures. The company

produced potent year-on-year income growth and decent equity returns. Team returns on

productive equity (RoTE) is 8.5 percent, 2.9 percent higher than the previous year on track to

reach the company's 2019 and 2020 goals. Organisation ratio of Common Equity Tier 1 (CET1)

is 13.2%, at the target end-state level of c.13% and form the above results it is predicted that

organisation will achieve the predicted growth aspects. Except for arbitration and conducting

products, profit until tax has been £ 5.7bn, up 20 percent year and produced an 8.5 percent

transfer on concrete equity, just shy in organisation 2019 and 2020 location rates (Kalbaugh,

2016). Net income was 21.9p, up on the previous year's 3.5p loss. Considering the key aspects in

terms of combining the financial results it is evaluated that key stake holders are retaining 5.5%

rights in common equity.

Return on Assets

Particulars 2018 £m 2017 £m

Net income 1394 -1933

Total assets 1133283 1133248

Calculation 1394 / 1133283 * 100 -1933 / 1133248 * 100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on assets ratio 0.123% 0.17%

From the above evaluation it is resulted that the return on assets were decreased for 2018

comparative to last financial year. Deduction in acquiring fixed assets and run down of non-core

units is considering major reason of decreased return on assets ratio. Barclays disregarded £90bn

of risk weighted assets during the last year. this action brings the ratio down by 0.05%.

Corporate investments and operations run down in subsidiary states may decrease the ratio more

significantly. Barclays UK remains an important benefit to the Company with non-tax profits of

£ 2.4 billion and a high return on shareholder assets of 16.7%.

Return on capital employed

Particulars 2018 £m 2017 £m

Operating profit 3494 3541

Capital employed 63779 66016

Calculation 3494 / 63779 *100 3541 / 66016 *100

Return on capital employed

ratio

5.47% 5.36%

Driven by a number of financial market purchases as well as an increasing amount through

organisation is committed green product range, overall ecological funding grew 11 percent to £

5.3bn. Form the evaluation states that the return on capital employed increased by 0.11% form

the last year. the change in capital market is predicted the reason of increased return on capital

8

From the above evaluation it is resulted that the return on assets were decreased for 2018

comparative to last financial year. Deduction in acquiring fixed assets and run down of non-core

units is considering major reason of decreased return on assets ratio. Barclays disregarded £90bn

of risk weighted assets during the last year. this action brings the ratio down by 0.05%.

Corporate investments and operations run down in subsidiary states may decrease the ratio more

significantly. Barclays UK remains an important benefit to the Company with non-tax profits of

£ 2.4 billion and a high return on shareholder assets of 16.7%.

Return on capital employed

Particulars 2018 £m 2017 £m

Operating profit 3494 3541

Capital employed 63779 66016

Calculation 3494 / 63779 *100 3541 / 66016 *100

Return on capital employed

ratio

5.47% 5.36%

Driven by a number of financial market purchases as well as an increasing amount through

organisation is committed green product range, overall ecological funding grew 11 percent to £

5.3bn. Form the evaluation states that the return on capital employed increased by 0.11% form

the last year. the change in capital market is predicted the reason of increased return on capital

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

introduced in investment funds and bonds. Some of the shareholders reinvested in Barclays and

showed a positive interest towards enhancing the market growth and development in near future.

As the above financial evaluation of Barclays states the mixed results and aspects. It is

recorded during the financial crisis capital structure get rigid but the management was ready to

evolve and reform the capital structure of business with a critical approach of investing in less

risk holding assets and liabilities. the variations among fluctuations was tremendously made

structure with proper structure and evaluative control. At last, organisation be able to present the

strong market hold throughout the years and adapted the global changes in sustainable growth

direction.

CONCLUSION

Based on above project study, this can be inferred it is important for businesses to analyse

the global financial climate because it can impact their financial performance. The report cites

two latest changes in the global financial climate that influence the financial results of the

selected organization. Included are key components of international finance, such as funding

origin and dividends strategy. The other part of both the project study suggests on the evaluation

of the selected firm's quality by measuring various proportions like productivity ratio, efficiency

proportion and much more.

9

showed a positive interest towards enhancing the market growth and development in near future.

As the above financial evaluation of Barclays states the mixed results and aspects. It is

recorded during the financial crisis capital structure get rigid but the management was ready to

evolve and reform the capital structure of business with a critical approach of investing in less

risk holding assets and liabilities. the variations among fluctuations was tremendously made

structure with proper structure and evaluative control. At last, organisation be able to present the

strong market hold throughout the years and adapted the global changes in sustainable growth

direction.

CONCLUSION

Based on above project study, this can be inferred it is important for businesses to analyse

the global financial climate because it can impact their financial performance. The report cites

two latest changes in the global financial climate that influence the financial results of the

selected organization. Included are key components of international finance, such as funding

origin and dividends strategy. The other part of both the project study suggests on the evaluation

of the selected firm's quality by measuring various proportions like productivity ratio, efficiency

proportion and much more.

9

REFERENCES

Books and Journals:

Frieden, J., 2016. The governance of international finance. Annual Review of Political Science.

19. pp.33-48.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging markets:

The role of policies and international finance institutions. Energy Policy. 82. pp.12-22.

Kay, K., 2018. A hostile takeover of nature? Placing value in conservation

finance. Antipode, 50(1), pp.164-183.

Vaubourg, A. G., 2016. Finance and international trade: A review of the literature. Revue

d'économie politique. 126(1). pp.57-87.

Khan, M. M., 2015. Sources of finance available for SME sector in Pakistan. International

Letters of Social and Humanistic Sciences. 47. pp.184-194.

Ntuli, M. G., 2017. An evaluation of bank acquisition using an accounting based measure: a case

of Amalgamated Bank of South Africa and Barclays Bank Plc. Banks and Bank Systems.

12(1). p.160.

Fernández, X. L., Paz-Saavedra, D. and Coto-Millán, P., 2019. THE IMPACT OF BREXIT ON

BANK EFFICIENCY: EVIDENCE FROM UK AND IRELAND. Finance Research

Letters. p.101338.

Mugarura, N., 2015. The jeopardy of the bank in enforcement of normative anti-money

laundering and countering financing of terrorism regimes. Journal of Money Laundering

Control. 18(3). pp.352-370.

Goudkamp, J. L. M., 2017. Various claimants v Barclays Bank Plc. Journal of Personal Injury

Law, 2017(4).

Kalbaugh, G., 2016. FERC v. Barclays Bank PLC Shines a Light on CFTC and FERC

Jurisdiction. Futures and Derivatives Law Report. 36(11). pp.2017-05.

Online

Current and liquid ratios, 2019. [online]. Available through:

<https://www.macrotrends.net/stocks/charts/BCS/barclays/current-ratio>

10

Books and Journals:

Frieden, J., 2016. The governance of international finance. Annual Review of Political Science.

19. pp.33-48.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging markets:

The role of policies and international finance institutions. Energy Policy. 82. pp.12-22.

Kay, K., 2018. A hostile takeover of nature? Placing value in conservation

finance. Antipode, 50(1), pp.164-183.

Vaubourg, A. G., 2016. Finance and international trade: A review of the literature. Revue

d'économie politique. 126(1). pp.57-87.

Khan, M. M., 2015. Sources of finance available for SME sector in Pakistan. International

Letters of Social and Humanistic Sciences. 47. pp.184-194.

Ntuli, M. G., 2017. An evaluation of bank acquisition using an accounting based measure: a case

of Amalgamated Bank of South Africa and Barclays Bank Plc. Banks and Bank Systems.

12(1). p.160.

Fernández, X. L., Paz-Saavedra, D. and Coto-Millán, P., 2019. THE IMPACT OF BREXIT ON

BANK EFFICIENCY: EVIDENCE FROM UK AND IRELAND. Finance Research

Letters. p.101338.

Mugarura, N., 2015. The jeopardy of the bank in enforcement of normative anti-money

laundering and countering financing of terrorism regimes. Journal of Money Laundering

Control. 18(3). pp.352-370.

Goudkamp, J. L. M., 2017. Various claimants v Barclays Bank Plc. Journal of Personal Injury

Law, 2017(4).

Kalbaugh, G., 2016. FERC v. Barclays Bank PLC Shines a Light on CFTC and FERC

Jurisdiction. Futures and Derivatives Law Report. 36(11). pp.2017-05.

Online

Current and liquid ratios, 2019. [online]. Available through:

<https://www.macrotrends.net/stocks/charts/BCS/barclays/current-ratio>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.