Financial Analysis of Boeing's 7E7 Project: A Decision-Making Report

VerifiedAdded on 2020/06/06

|14

|3183

|22

Report

AI Summary

This report provides a comprehensive financial analysis of Boeing's 7E7 project, focusing on international finance and decision-making. It evaluates the project's viability by examining key financial metrics such as Weighted Average Cost of Capital (WACC), the applicability of the Capital Asset Pricing Model (CAPM), cost of equity and debt, and the use of risk-free rates and risk premiums. The report critiques the use of CAPM, discusses debt and its relation to commercial risk, and analyzes the project's economics, including sensitivity analysis, Average Rate of Return (ARR), and Net Present Value (NPV). It also explores capital structure weights and the implications of various financial decisions, ultimately assessing the project's potential for value creation. The report concludes with an evaluation of the project's economic viability and provides recommendations based on the financial analysis.

International Finance &

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Boeing contemplating to launch the project named 7E7........................................................1

Question 2........................................................................................................................................2

A. Appropriate required rate of return against IRR from Boeing 7E7...................................2

B and G. Appropriate reason for not using CAPM model for estimating cost of capital......2

C. Usage of CAPM to estimate cost of equity and reason for using specific beta and risk-free

rate of return...........................................................................................................................3

D. Usage of risk free rate and risk premium..........................................................................3

E. Cost of debt of company....................................................................................................4

F. Explain debt and its relation to commercial risk................................................................4

H. What is appropriate to calculate whether weighted average of all debt or a weighted

average of long-term debt with maturities that match the length of the project.....................4

I. Critically discussed use of capital structure weights ..........................................................5

Question 3........................................................................................................................................5

A. Evaluating the project of company....................................................................................5

B. Outline circumstances why the project is economically viable.........................................6

C. Sensitivity analysis of the project......................................................................................6

Question 4........................................................................................................................................7

Successful approval of project and value creation for Boeing organisation..........................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Boeing contemplating to launch the project named 7E7........................................................1

Question 2........................................................................................................................................2

A. Appropriate required rate of return against IRR from Boeing 7E7...................................2

B and G. Appropriate reason for not using CAPM model for estimating cost of capital......2

C. Usage of CAPM to estimate cost of equity and reason for using specific beta and risk-free

rate of return...........................................................................................................................3

D. Usage of risk free rate and risk premium..........................................................................3

E. Cost of debt of company....................................................................................................4

F. Explain debt and its relation to commercial risk................................................................4

H. What is appropriate to calculate whether weighted average of all debt or a weighted

average of long-term debt with maturities that match the length of the project.....................4

I. Critically discussed use of capital structure weights ..........................................................5

Question 3........................................................................................................................................5

A. Evaluating the project of company....................................................................................5

B. Outline circumstances why the project is economically viable.........................................6

C. Sensitivity analysis of the project......................................................................................6

Question 4........................................................................................................................................7

Successful approval of project and value creation for Boeing organisation..........................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

INTRODUCTION

Project evaluation is essential aspect for the company as investment should be made in

profitable project so that profits may be achieved by it. The enclosed report deals with Boeing

company which is operating in airline industry. It is planning to launch a new project named as

7E7. For this, it has to rely on investment appraisal techniques which will provide effective

results whether to invest in the project or not. Organisation need to take better decision for

evaluating the credibility and viability of the project so that it may earn better profits with much

ease. This will provide with desired results and customers' will be satisfied in the best possible

way.

Question 1

Boeing contemplating to launch the project named 7E7

Boeing organisation contemplates to launch the project so that it may be able to garner

more profits which had deteriorated in the past. The project requires effective and better

decision-making as wrong decisions may be hazardous to company and it will lose the market

share. The aircraft industry in which Boeing operates is highly competitive as Airbus is the chief

rival to it. As such, better decisions should be made so that 7E7 project may be successfully

attained with much ease (Avdjiev, McCauley and Shin, 2016). The new project named as 7E7 is

made clearer by Boeing that it will be able to travel much faster than supersonic air planes that

were implemented and created in the past.

Now coming to today's scenario, it is not good time for company to launch this project as

terrorism is at its peak and people are afraid about it. In addition to this, several countries are

facing economic recession and due to this, customers' prefer to travel in economic class. As a

result, it is not the best time to launch the project by organisation as estimated profits will not be

generated significantly (UK Aviation market).

1

Project evaluation is essential aspect for the company as investment should be made in

profitable project so that profits may be achieved by it. The enclosed report deals with Boeing

company which is operating in airline industry. It is planning to launch a new project named as

7E7. For this, it has to rely on investment appraisal techniques which will provide effective

results whether to invest in the project or not. Organisation need to take better decision for

evaluating the credibility and viability of the project so that it may earn better profits with much

ease. This will provide with desired results and customers' will be satisfied in the best possible

way.

Question 1

Boeing contemplating to launch the project named 7E7

Boeing organisation contemplates to launch the project so that it may be able to garner

more profits which had deteriorated in the past. The project requires effective and better

decision-making as wrong decisions may be hazardous to company and it will lose the market

share. The aircraft industry in which Boeing operates is highly competitive as Airbus is the chief

rival to it. As such, better decisions should be made so that 7E7 project may be successfully

attained with much ease (Avdjiev, McCauley and Shin, 2016). The new project named as 7E7 is

made clearer by Boeing that it will be able to travel much faster than supersonic air planes that

were implemented and created in the past.

Now coming to today's scenario, it is not good time for company to launch this project as

terrorism is at its peak and people are afraid about it. In addition to this, several countries are

facing economic recession and due to this, customers' prefer to travel in economic class. As a

result, it is not the best time to launch the project by organisation as estimated profits will not be

generated significantly (UK Aviation market).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

A. Appropriate required rate of return against IRR from Boeing 7E7

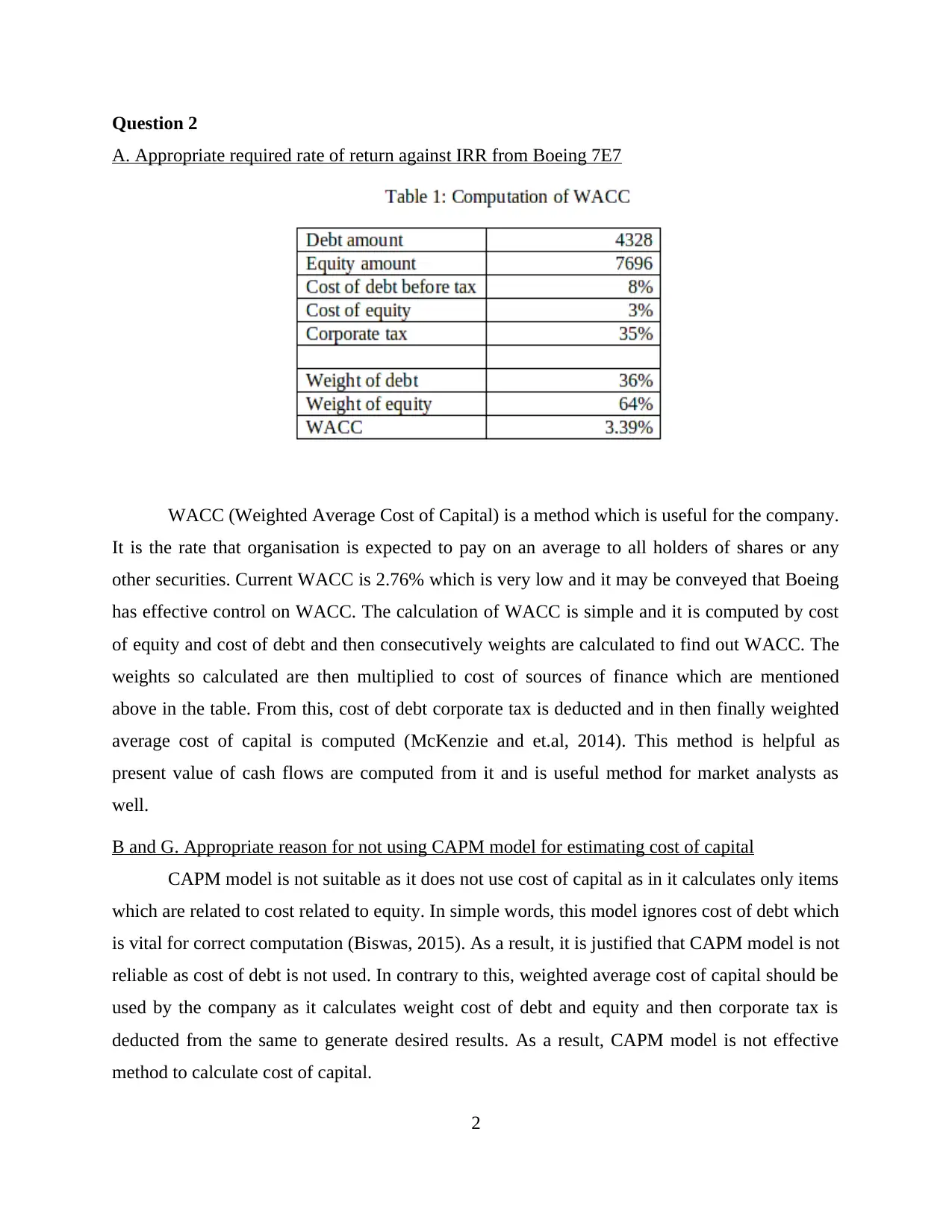

WACC (Weighted Average Cost of Capital) is a method which is useful for the company.

It is the rate that organisation is expected to pay on an average to all holders of shares or any

other securities. Current WACC is 2.76% which is very low and it may be conveyed that Boeing

has effective control on WACC. The calculation of WACC is simple and it is computed by cost

of equity and cost of debt and then consecutively weights are calculated to find out WACC. The

weights so calculated are then multiplied to cost of sources of finance which are mentioned

above in the table. From this, cost of debt corporate tax is deducted and in then finally weighted

average cost of capital is computed (McKenzie and et.al, 2014). This method is helpful as

present value of cash flows are computed from it and is useful method for market analysts as

well.

B and G. Appropriate reason for not using CAPM model for estimating cost of capital

CAPM model is not suitable as it does not use cost of capital as in it calculates only items

which are related to cost related to equity. In simple words, this model ignores cost of debt which

is vital for correct computation (Biswas, 2015). As a result, it is justified that CAPM model is not

reliable as cost of debt is not used. In contrary to this, weighted average cost of capital should be

used by the company as it calculates weight cost of debt and equity and then corporate tax is

deducted from the same to generate desired results. As a result, CAPM model is not effective

method to calculate cost of capital.

2

A. Appropriate required rate of return against IRR from Boeing 7E7

WACC (Weighted Average Cost of Capital) is a method which is useful for the company.

It is the rate that organisation is expected to pay on an average to all holders of shares or any

other securities. Current WACC is 2.76% which is very low and it may be conveyed that Boeing

has effective control on WACC. The calculation of WACC is simple and it is computed by cost

of equity and cost of debt and then consecutively weights are calculated to find out WACC. The

weights so calculated are then multiplied to cost of sources of finance which are mentioned

above in the table. From this, cost of debt corporate tax is deducted and in then finally weighted

average cost of capital is computed (McKenzie and et.al, 2014). This method is helpful as

present value of cash flows are computed from it and is useful method for market analysts as

well.

B and G. Appropriate reason for not using CAPM model for estimating cost of capital

CAPM model is not suitable as it does not use cost of capital as in it calculates only items

which are related to cost related to equity. In simple words, this model ignores cost of debt which

is vital for correct computation (Biswas, 2015). As a result, it is justified that CAPM model is not

reliable as cost of debt is not used. In contrary to this, weighted average cost of capital should be

used by the company as it calculates weight cost of debt and equity and then corporate tax is

deducted from the same to generate desired results. As a result, CAPM model is not effective

method to calculate cost of capital.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C. Usage of CAPM to estimate cost of equity and reason for using specific beta and risk-free rate

of return

From the above table of cost of equity, it may be said that CAPM model is essential

method that is used by company for computing cost of equity (Papadopoulos and Heslop, 2014).

It may be interpreted from the above table that cost of equity is 3 % which is low and it may be

said that company has low cost of equity. Risk free rate of 0.85 % is applied as cost of equity is

not estimated for a longer period and consecutively rate of long term bond is not suitable for

Boeing company and it is justified that it is not much worth to the company.

Furthermore, coming to beta which is taken as 60 days. It is taken at these days as stocks

changes rapidly and are liable to change and moreover, volatile in nature. As a result, beta for

more than 60 trading are not taken into account.

D. Usage of risk free rate and risk premium

The risk-free rate is taken as 1.85 % and some concrete reasons are behind it. From the

above computed table of cost of equity, it may be conveyed that risk-free rate is taken for a

shorter period. This is the reason to use CAPM model for estimating cost of capital for effective

analysis in the best possible way (Vishny and Zingales, 2017). Furthermore, risk premium

applied is 1.15 %. This is calculated by deducting risk-free rate of return from that of market

return by the company.

The market rate of return is estimated at 2 % as market conditions are not appropriate

because of the economic recession prevailing in the market. This is the reason behind using

lower market rate of return. By computing risk free rate of return from that of market return, it

may be analysed that there is not much difference between the both aspect.

E. Cost of debt of company

3

of return

From the above table of cost of equity, it may be said that CAPM model is essential

method that is used by company for computing cost of equity (Papadopoulos and Heslop, 2014).

It may be interpreted from the above table that cost of equity is 3 % which is low and it may be

said that company has low cost of equity. Risk free rate of 0.85 % is applied as cost of equity is

not estimated for a longer period and consecutively rate of long term bond is not suitable for

Boeing company and it is justified that it is not much worth to the company.

Furthermore, coming to beta which is taken as 60 days. It is taken at these days as stocks

changes rapidly and are liable to change and moreover, volatile in nature. As a result, beta for

more than 60 trading are not taken into account.

D. Usage of risk free rate and risk premium

The risk-free rate is taken as 1.85 % and some concrete reasons are behind it. From the

above computed table of cost of equity, it may be conveyed that risk-free rate is taken for a

shorter period. This is the reason to use CAPM model for estimating cost of capital for effective

analysis in the best possible way (Vishny and Zingales, 2017). Furthermore, risk premium

applied is 1.15 %. This is calculated by deducting risk-free rate of return from that of market

return by the company.

The market rate of return is estimated at 2 % as market conditions are not appropriate

because of the economic recession prevailing in the market. This is the reason behind using

lower market rate of return. By computing risk free rate of return from that of market return, it

may be analysed that there is not much difference between the both aspect.

E. Cost of debt of company

3

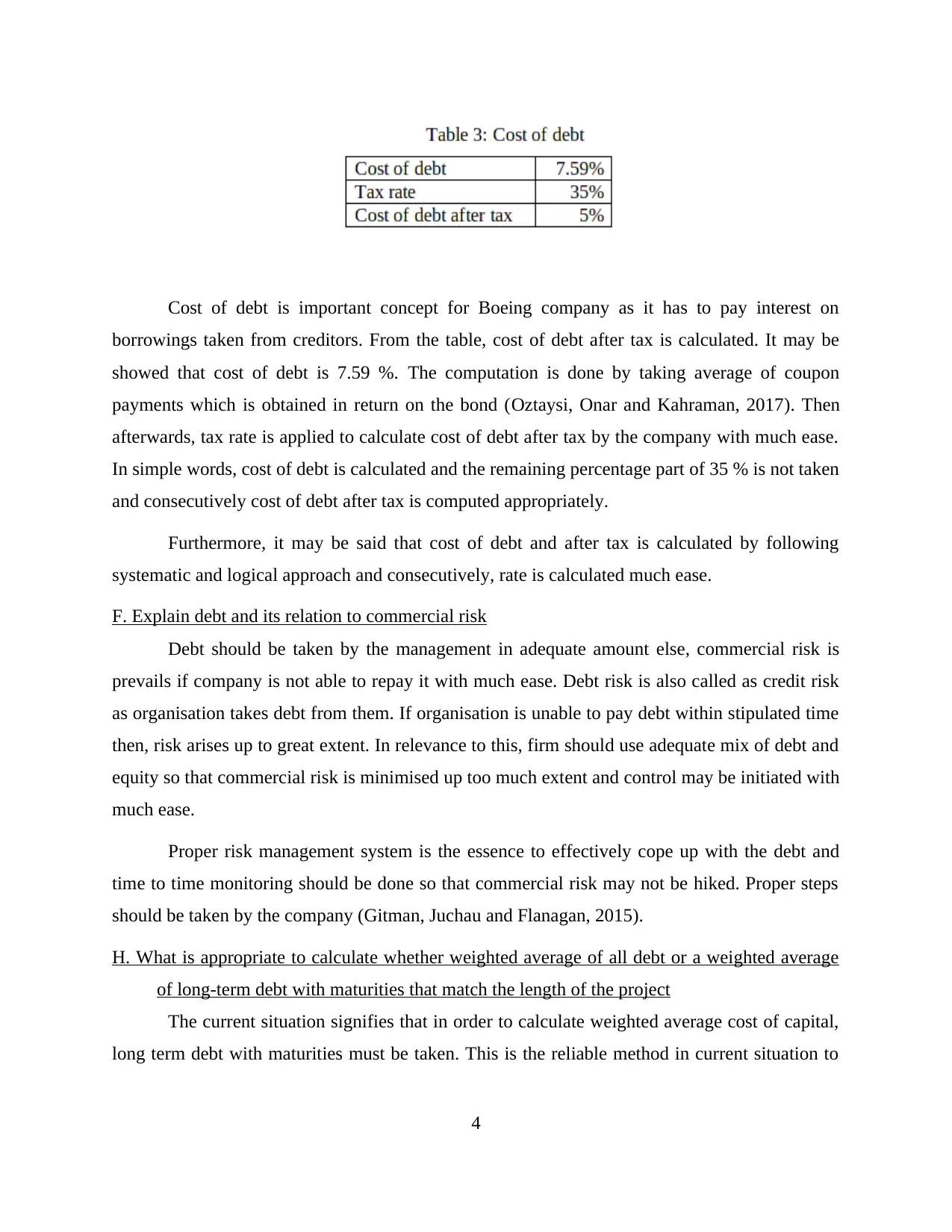

Cost of debt is important concept for Boeing company as it has to pay interest on

borrowings taken from creditors. From the table, cost of debt after tax is calculated. It may be

showed that cost of debt is 7.59 %. The computation is done by taking average of coupon

payments which is obtained in return on the bond (Oztaysi, Onar and Kahraman, 2017). Then

afterwards, tax rate is applied to calculate cost of debt after tax by the company with much ease.

In simple words, cost of debt is calculated and the remaining percentage part of 35 % is not taken

and consecutively cost of debt after tax is computed appropriately.

Furthermore, it may be said that cost of debt and after tax is calculated by following

systematic and logical approach and consecutively, rate is calculated much ease.

F. Explain debt and its relation to commercial risk

Debt should be taken by the management in adequate amount else, commercial risk is

prevails if company is not able to repay it with much ease. Debt risk is also called as credit risk

as organisation takes debt from them. If organisation is unable to pay debt within stipulated time

then, risk arises up to great extent. In relevance to this, firm should use adequate mix of debt and

equity so that commercial risk is minimised up too much extent and control may be initiated with

much ease.

Proper risk management system is the essence to effectively cope up with the debt and

time to time monitoring should be done so that commercial risk may not be hiked. Proper steps

should be taken by the company (Gitman, Juchau and Flanagan, 2015).

H. What is appropriate to calculate whether weighted average of all debt or a weighted average

of long-term debt with maturities that match the length of the project

The current situation signifies that in order to calculate weighted average cost of capital,

long term debt with maturities must be taken. This is the reliable method in current situation to

4

borrowings taken from creditors. From the table, cost of debt after tax is calculated. It may be

showed that cost of debt is 7.59 %. The computation is done by taking average of coupon

payments which is obtained in return on the bond (Oztaysi, Onar and Kahraman, 2017). Then

afterwards, tax rate is applied to calculate cost of debt after tax by the company with much ease.

In simple words, cost of debt is calculated and the remaining percentage part of 35 % is not taken

and consecutively cost of debt after tax is computed appropriately.

Furthermore, it may be said that cost of debt and after tax is calculated by following

systematic and logical approach and consecutively, rate is calculated much ease.

F. Explain debt and its relation to commercial risk

Debt should be taken by the management in adequate amount else, commercial risk is

prevails if company is not able to repay it with much ease. Debt risk is also called as credit risk

as organisation takes debt from them. If organisation is unable to pay debt within stipulated time

then, risk arises up to great extent. In relevance to this, firm should use adequate mix of debt and

equity so that commercial risk is minimised up too much extent and control may be initiated with

much ease.

Proper risk management system is the essence to effectively cope up with the debt and

time to time monitoring should be done so that commercial risk may not be hiked. Proper steps

should be taken by the company (Gitman, Juchau and Flanagan, 2015).

H. What is appropriate to calculate whether weighted average of all debt or a weighted average

of long-term debt with maturities that match the length of the project

The current situation signifies that in order to calculate weighted average cost of capital,

long term debt with maturities must be taken. This is the reliable method in current situation to

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compute for cost of capital with much ease by taking weighted average of long- term debt with

maturities.

This fact is observed long term loan amount is taken into account while making certain

projections about cash flows (Zhang and et.al, 2014). This is the main reason for taking long-

term maturities and short-term loan amount is dropped significantly by the company. But the

long term as well as short-term or both depends upon the requirement of company. As a result,

Boeing company can use effective option to make appropriate decisions. This will provide with

better and effective results in the most proficient way.

I. Critically discussed use of capital structure weights

The capital structure weights are important to company so that it may analyse and assume

that capital comes from either debt or equity and is a simple method for calculating total capital

on an weighted average with much ease. The capital structure used by the company is 36% and

64% respectively. The ratio may also be interpreted as 36 : 64 which implies that 36 % is debt

and 64 % is equity. This is not good situation as Boeing organisation has more proportion of

equity which is not suitable for it.

The company should have a perfect mix of both of debt and equity so that it may be able

to utilise both sources of finance with much ease in the best possible way. Moreover, if equity

ratio is increased in near future, then shareholders' will have less control on organisation and it

will affect firm's performance negatively. As a result, more debt should be taken to make perfect

balance between debt and equity (Davidson and et.al, 2015).

Question 3

A. Evaluating the project of company

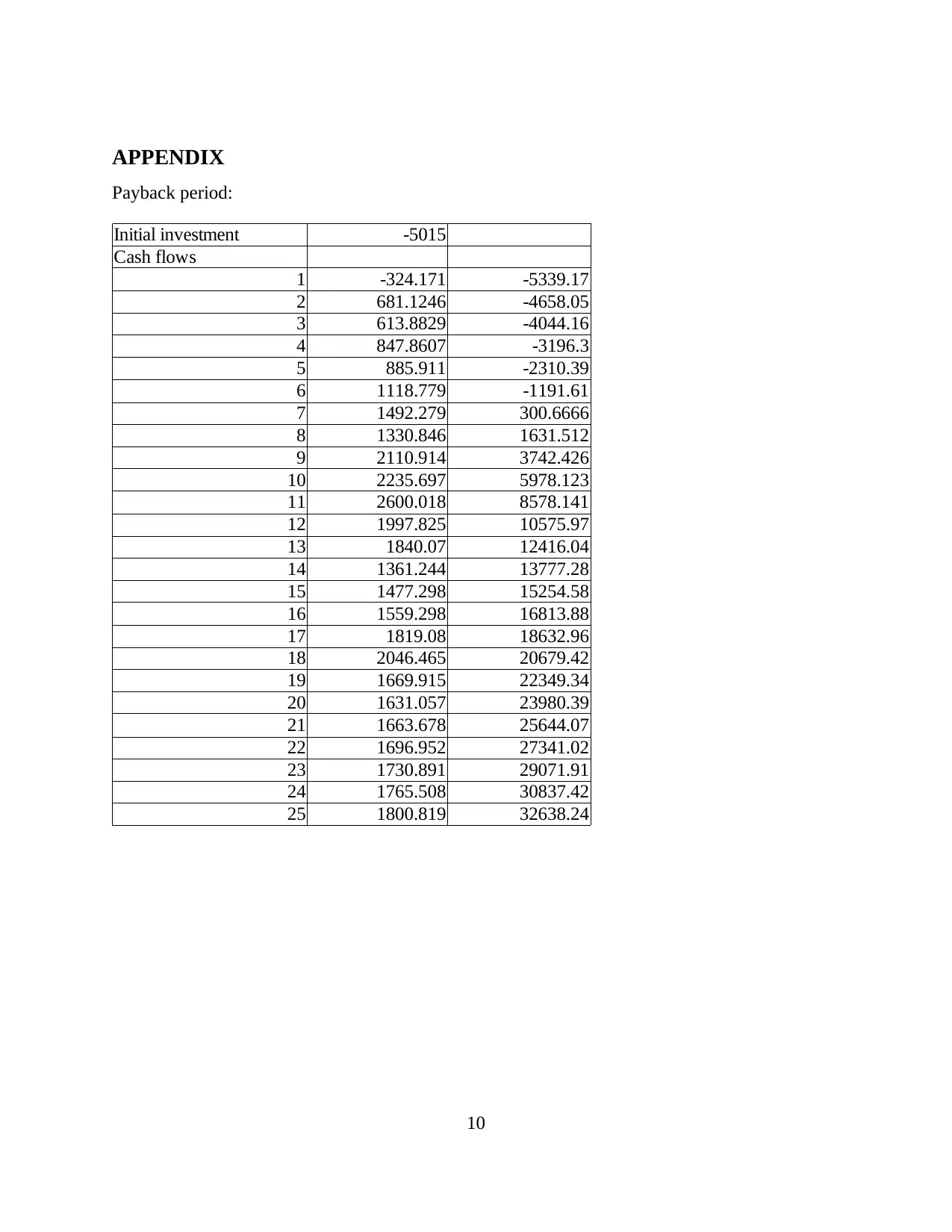

The project may be evaluated that it may be able to cover the cost in forthcoming 6 years

which is made clearer by looking at the provided appendix. This is low as project full life is 25

years and by analysing this, cost of the new project 7E7 will be covered in short duration. For

project evaluation, ARR (Average Rate of Return) is another method which can be used by the

organisation.

ARR calculation conveys that 7E7 is profitable for Boeing as it is 30 % which is regarded

as good percentage for profitability purpose on the investment. Next method provided in the

5

maturities.

This fact is observed long term loan amount is taken into account while making certain

projections about cash flows (Zhang and et.al, 2014). This is the main reason for taking long-

term maturities and short-term loan amount is dropped significantly by the company. But the

long term as well as short-term or both depends upon the requirement of company. As a result,

Boeing company can use effective option to make appropriate decisions. This will provide with

better and effective results in the most proficient way.

I. Critically discussed use of capital structure weights

The capital structure weights are important to company so that it may analyse and assume

that capital comes from either debt or equity and is a simple method for calculating total capital

on an weighted average with much ease. The capital structure used by the company is 36% and

64% respectively. The ratio may also be interpreted as 36 : 64 which implies that 36 % is debt

and 64 % is equity. This is not good situation as Boeing organisation has more proportion of

equity which is not suitable for it.

The company should have a perfect mix of both of debt and equity so that it may be able

to utilise both sources of finance with much ease in the best possible way. Moreover, if equity

ratio is increased in near future, then shareholders' will have less control on organisation and it

will affect firm's performance negatively. As a result, more debt should be taken to make perfect

balance between debt and equity (Davidson and et.al, 2015).

Question 3

A. Evaluating the project of company

The project may be evaluated that it may be able to cover the cost in forthcoming 6 years

which is made clearer by looking at the provided appendix. This is low as project full life is 25

years and by analysing this, cost of the new project 7E7 will be covered in short duration. For

project evaluation, ARR (Average Rate of Return) is another method which can be used by the

organisation.

ARR calculation conveys that 7E7 is profitable for Boeing as it is 30 % which is regarded

as good percentage for profitability purpose on the investment. Next method provided in the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appendix is NPV which shows net present value of the 7E7 project and it is 18547.91 value

reflected from the table. Higher NPV, better for the company as returns are higher. It may be

evaluated that investment return on the new project will be higher and as a result, it is profitable

for the organisation.

B. Outline circumstances why the project is economically viable

There are various circumstances which shows that the project is economically profitable

and viable for the company (Graham and et.al, 2017). The low cost of capital is taken and this

implies that cost of project will be reduced leading more profits. Thus, it is profitable for Boeing.

It should also may not raise fund through equity because it already has more equity and further

will increase dividend rate as well which will be provided to shareholders'.

Reducing cost of the project is another circumstance which may be profitable for the firm

as cutting down the cost will make ensure that firm will achieve more of the profits in the most

productive way. This is possible when operating cost is reduced, that will have impact on the

cash flow as it will increase eventually and firm will be profitable. Furthermore, if more orders

are received for manufacturing, then also cash flow will positively increase and as a result, these

all circumstances are profitable for the company and 7E7 project is economically viable.

C. Sensitivity analysis of the project

The sensitivity analysis may be carried out that cost of capital is 3.39 %, NPV of 7E7

project is 18547.91 and if this rate is changed to 2 %, then revised NPV may be 28347.

Similarly, discounting rate is also changed to 4 %, NPV will be 21775. Therefore, it may be

analysed that more the cost of capital is decreased, more NPV is increased and as a result, more

profit may be earned by the company concerning on low cost of capital (Borio, James and Shin,

2014). In the same way, COGS(Cost Of Goods Sold) to sales is also decreased to 70 %, in this

case NPV will be 43070.

By analysing this, it may be said that COGS are one of the factor that influence

profitability for the firm. This is because it affects cash flows of the business. As a result, firm

should be able to control expenditures by taking necessary steps. This can be done by purchasing

raw materials at low price from suppliers.

6

reflected from the table. Higher NPV, better for the company as returns are higher. It may be

evaluated that investment return on the new project will be higher and as a result, it is profitable

for the organisation.

B. Outline circumstances why the project is economically viable

There are various circumstances which shows that the project is economically profitable

and viable for the company (Graham and et.al, 2017). The low cost of capital is taken and this

implies that cost of project will be reduced leading more profits. Thus, it is profitable for Boeing.

It should also may not raise fund through equity because it already has more equity and further

will increase dividend rate as well which will be provided to shareholders'.

Reducing cost of the project is another circumstance which may be profitable for the firm

as cutting down the cost will make ensure that firm will achieve more of the profits in the most

productive way. This is possible when operating cost is reduced, that will have impact on the

cash flow as it will increase eventually and firm will be profitable. Furthermore, if more orders

are received for manufacturing, then also cash flow will positively increase and as a result, these

all circumstances are profitable for the company and 7E7 project is economically viable.

C. Sensitivity analysis of the project

The sensitivity analysis may be carried out that cost of capital is 3.39 %, NPV of 7E7

project is 18547.91 and if this rate is changed to 2 %, then revised NPV may be 28347.

Similarly, discounting rate is also changed to 4 %, NPV will be 21775. Therefore, it may be

analysed that more the cost of capital is decreased, more NPV is increased and as a result, more

profit may be earned by the company concerning on low cost of capital (Borio, James and Shin,

2014). In the same way, COGS(Cost Of Goods Sold) to sales is also decreased to 70 %, in this

case NPV will be 43070.

By analysing this, it may be said that COGS are one of the factor that influence

profitability for the firm. This is because it affects cash flows of the business. As a result, firm

should be able to control expenditures by taking necessary steps. This can be done by purchasing

raw materials at low price from suppliers.

6

Question 4

Successful approval of project and value creation for Boeing organisation

The 7E7 project is approved by taking evidences from various investment appraisal

techniques. This can be shown by payback period which is good and project will cover the cost

in less time. Another technique used is ARR is also effective and adequate amount will be earned

by Boeing by investing in it (Joo and Durri 2015). Even more, NPV is also higher. These

techniques reveal that 7E7 aircraft project will be successful for the company.

Value creation will be made by the company. This may be achieved as travellers are

demanding for faster routes so that they may reach destination in less time with such supersonic

planes. Moreover, it will also benefit stakeholders of the company. Customers' will also be

benefited and satisfied and in turn, company will be benefited by earning revenue. Hence, it can

be said that 7E7 project will create value for Boeing to achieve objectives by garnering profits

with much ease.

CONCLUSION

Hereby it may be concluded that project evaluation is vital for the firm as wrong

decisions may ruin entire profits of the company. The methods stated while evaluating project to

check the viability of it are of much importance as they provide concrete conclusions to company

whether to invest in a particular project or not. By using these techniques, better and effective

decisions may be taken with much ease. Moreover, appropriate discount rate should be taken by

the company as wrong discount rate will provide false evaluation. As such, discount rate must be

taken appropriately in the best possible way.

7

Successful approval of project and value creation for Boeing organisation

The 7E7 project is approved by taking evidences from various investment appraisal

techniques. This can be shown by payback period which is good and project will cover the cost

in less time. Another technique used is ARR is also effective and adequate amount will be earned

by Boeing by investing in it (Joo and Durri 2015). Even more, NPV is also higher. These

techniques reveal that 7E7 aircraft project will be successful for the company.

Value creation will be made by the company. This may be achieved as travellers are

demanding for faster routes so that they may reach destination in less time with such supersonic

planes. Moreover, it will also benefit stakeholders of the company. Customers' will also be

benefited and satisfied and in turn, company will be benefited by earning revenue. Hence, it can

be said that 7E7 project will create value for Boeing to achieve objectives by garnering profits

with much ease.

CONCLUSION

Hereby it may be concluded that project evaluation is vital for the firm as wrong

decisions may ruin entire profits of the company. The methods stated while evaluating project to

check the viability of it are of much importance as they provide concrete conclusions to company

whether to invest in a particular project or not. By using these techniques, better and effective

decisions may be taken with much ease. Moreover, appropriate discount rate should be taken by

the company as wrong discount rate will provide false evaluation. As such, discount rate must be

taken appropriately in the best possible way.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Avdjiev, S., McCauley, R. N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance.Economic Policy. 31(87). pp.409-451.

McKenzie, E. and et.al, 2014. Understanding the use of ecosystem service knowledge in decision

making: lessons from international experiences of spatial planning.Environment and Planning C:

Government and Policy. 32(2). pp.320-340.

Papadopoulos, N. and Heslop, L. A., 2014. Product-country images: Impact and role in

international marketing. Routledge.

Vishny, R. and Zingales, L., 2017. Corporate Finance. Journal of Political Economy. 125(6).

pp.1805-1812.

Oztaysi, B., Onar, S. C. and Kahraman, C., 2017. SELECTION AMONG INNOVATIVE

PROJECT PROPOSALS USING A HESITANT FUZZY MULTIPLE CRITERIA DECISION

MAKING METHOD. Journal of Economics Finance and Accounting. 4(2). pp.194-202.

Gitman, L. J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Zhang, K. Z. and et.al, 2014. Examining the influence of online reviews on consumers' decision-

making: A heuristic–systematic model. Decision Support Systems. 67. pp.78-89.

Davidson, G. and et.al,, 2015. Supported decision making: a review of the international

literature. International journal of law and psychiatry. 38. pp.61-67.

Graham, J. R. and et.al,, 2017. Tax rates and corporate decision-making. The Review of

Financial Studies. 30(9). pp.3128-3175.

Borio, C. E., James, H. and Shin, H. S., 2014. The international monetary and financial system: a

capital account historical perspective.

8

Books and Journals

Avdjiev, S., McCauley, R. N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance.Economic Policy. 31(87). pp.409-451.

McKenzie, E. and et.al, 2014. Understanding the use of ecosystem service knowledge in decision

making: lessons from international experiences of spatial planning.Environment and Planning C:

Government and Policy. 32(2). pp.320-340.

Papadopoulos, N. and Heslop, L. A., 2014. Product-country images: Impact and role in

international marketing. Routledge.

Vishny, R. and Zingales, L., 2017. Corporate Finance. Journal of Political Economy. 125(6).

pp.1805-1812.

Oztaysi, B., Onar, S. C. and Kahraman, C., 2017. SELECTION AMONG INNOVATIVE

PROJECT PROPOSALS USING A HESITANT FUZZY MULTIPLE CRITERIA DECISION

MAKING METHOD. Journal of Economics Finance and Accounting. 4(2). pp.194-202.

Gitman, L. J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Zhang, K. Z. and et.al, 2014. Examining the influence of online reviews on consumers' decision-

making: A heuristic–systematic model. Decision Support Systems. 67. pp.78-89.

Davidson, G. and et.al,, 2015. Supported decision making: a review of the international

literature. International journal of law and psychiatry. 38. pp.61-67.

Graham, J. R. and et.al,, 2017. Tax rates and corporate decision-making. The Review of

Financial Studies. 30(9). pp.3128-3175.

Borio, C. E., James, H. and Shin, H. S., 2014. The international monetary and financial system: a

capital account historical perspective.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joo, B. A. and Durri, K., 2015. COMPREHENSIVE REVIEW OF LITERATURE ON

BEHAVIOURAL FINANCE. Indian Journal of Commerce and Management Studies. 6(2). p.11.

Biswas, R., 2015. Reshaping the financial architecture for development finance: the new

development banks.

Online

UK Aviation market, 2017. [Online]. Available through:< https://www.caa.co.uk/Data-and-

analysis/UK-aviation-market/>.

9

BEHAVIOURAL FINANCE. Indian Journal of Commerce and Management Studies. 6(2). p.11.

Biswas, R., 2015. Reshaping the financial architecture for development finance: the new

development banks.

Online

UK Aviation market, 2017. [Online]. Available through:< https://www.caa.co.uk/Data-and-

analysis/UK-aviation-market/>.

9

APPENDIX

Payback period:

Initial investment -5015

Cash flows

1 -324.171 -5339.17

2 681.1246 -4658.05

3 613.8829 -4044.16

4 847.8607 -3196.3

5 885.911 -2310.39

6 1118.779 -1191.61

7 1492.279 300.6666

8 1330.846 1631.512

9 2110.914 3742.426

10 2235.697 5978.123

11 2600.018 8578.141

12 1997.825 10575.97

13 1840.07 12416.04

14 1361.244 13777.28

15 1477.298 15254.58

16 1559.298 16813.88

17 1819.08 18632.96

18 2046.465 20679.42

19 1669.915 22349.34

20 1631.057 23980.39

21 1663.678 25644.07

22 1696.952 27341.02

23 1730.891 29071.91

24 1765.508 30837.42

25 1800.819 32638.24

10

Payback period:

Initial investment -5015

Cash flows

1 -324.171 -5339.17

2 681.1246 -4658.05

3 613.8829 -4044.16

4 847.8607 -3196.3

5 885.911 -2310.39

6 1118.779 -1191.61

7 1492.279 300.6666

8 1330.846 1631.512

9 2110.914 3742.426

10 2235.697 5978.123

11 2600.018 8578.141

12 1997.825 10575.97

13 1840.07 12416.04

14 1361.244 13777.28

15 1477.298 15254.58

16 1559.298 16813.88

17 1819.08 18632.96

18 2046.465 20679.42

19 1669.915 22349.34

20 1631.057 23980.39

21 1663.678 25644.07

22 1696.952 27341.02

23 1730.891 29071.91

24 1765.508 30837.42

25 1800.819 32638.24

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.