Comprehensive Report on International Finance for Burberry Group Plc

VerifiedAdded on 2021/02/19

|15

|3421

|23

Report

AI Summary

This report provides a comprehensive analysis of the international finance aspects of Burberry Group Plc. It begins with an introduction to the significance of integrating international financial standards. The report is divided into three key tasks. Task 1 examines recent developments in the international financial environment, highlighting the impact of globalization and the emergence of universal banking. Task 2 details the various sources of finance available to companies like Burberry, including long-term, medium-term, and short-term financing options, alongside an overview of dividend policies. Task 3 focuses on the financial performance analysis of Burberry Group Plc, utilizing ratio analysis to evaluate profitability and efficiency using financial statements from 2018 and 2019. The analysis includes the calculation and interpretation of gross profit margin and net profit margin ratios to assess the company's financial health and performance over the specified period.

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Recent developments in international financial environment: ...................................................1

TASK 2............................................................................................................................................2

Source of finance:.......................................................................................................................2

Dividend policy: .........................................................................................................................3

TASK 3............................................................................................................................................4

Financial performance analysis:..................................................................................................4

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Recent developments in international financial environment: ...................................................1

TASK 2............................................................................................................................................2

Source of finance:.......................................................................................................................2

Dividend policy: .........................................................................................................................3

TASK 3............................................................................................................................................4

Financial performance analysis:..................................................................................................4

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

In any business environment, there is a need to integrate a nation or location specific

financial standards with international financial standards for growth perspectivev (Armijo and

Echeverri-Gent, 2014). In recent business environment, there are vast changes in the field of

international finance and hence, there is a requirement of competent management in an

organisation to cope up with such changes taking place in the environment. For better

understanding of international finance, an organisation named Burberry Group Plc is chosen.

This report is divided in three task, first task provides the details about the recent developments

in the international market. Second task describes the sources of funds and related matters

whereas third task tells about the financial performance of selected organisation.

TASK 1

Recent developments in international financial environment:

There are various developments taking places in the business environment related to

finance which has a tremendous impact on the business operations of Burberry Group Plc. For

understanding of these developments, firstly the term international financial should be

understood. International Finance means monetary interactions with two more countries for

doing business. It is concerned with economies as a whole instead of individual market of a

country. There are various institution which provides international finance for doing business

such as international monetary fund (IMF) and international finance corp. (IFC) etc. Details of

two recent developments among various developments are as follows:

Due to globalisation and rapid integration of financial markets, the geographical locations

are no more cause for obtaining finance from outside the domestic market for

diversification. Due to this, international financial market is getting smaller in every

aspect of business. It can affect the Burberry Group Plc in near future because these

developments provides more growth opportunities to the company.

The other development in this environment is existence of universal banking and as a

result, there is a active flow of international capital. There is also improvement in the

working of non banking financial institution in supporting business operations of various

organisations. Due to this it has a wide range of sources in near future for diversification

1

In any business environment, there is a need to integrate a nation or location specific

financial standards with international financial standards for growth perspectivev (Armijo and

Echeverri-Gent, 2014). In recent business environment, there are vast changes in the field of

international finance and hence, there is a requirement of competent management in an

organisation to cope up with such changes taking place in the environment. For better

understanding of international finance, an organisation named Burberry Group Plc is chosen.

This report is divided in three task, first task provides the details about the recent developments

in the international market. Second task describes the sources of funds and related matters

whereas third task tells about the financial performance of selected organisation.

TASK 1

Recent developments in international financial environment:

There are various developments taking places in the business environment related to

finance which has a tremendous impact on the business operations of Burberry Group Plc. For

understanding of these developments, firstly the term international financial should be

understood. International Finance means monetary interactions with two more countries for

doing business. It is concerned with economies as a whole instead of individual market of a

country. There are various institution which provides international finance for doing business

such as international monetary fund (IMF) and international finance corp. (IFC) etc. Details of

two recent developments among various developments are as follows:

Due to globalisation and rapid integration of financial markets, the geographical locations

are no more cause for obtaining finance from outside the domestic market for

diversification. Due to this, international financial market is getting smaller in every

aspect of business. It can affect the Burberry Group Plc in near future because these

developments provides more growth opportunities to the company.

The other development in this environment is existence of universal banking and as a

result, there is a active flow of international capital. There is also improvement in the

working of non banking financial institution in supporting business operations of various

organisations. Due to this it has a wide range of sources in near future for diversification

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of its business operations in other countries by taking loans in that country easily (Bishop

and Hill, 2014).

TASK 2

Source of finance:

In any organisation like Burberry Group Plc, for carrying out its business operations

effectively and efficiently, there is a need of finance to provide monetary assistance to its

business operations and for working capital requirements. There are various sources of finance

from where a company may take finance which are as follows:

Long term finance

Medium term finance

Short term finance

Long term finance:

These are those finance which are taken by the company for long term period generally

for more than 5 years. This is taken for financing capital expenditures like purchase of fixed

assets, land and building etc. long term financing sources can in the form of followings:

Share capital or equity shares: In this method, companies like Burberry Group Plc are

often gives a prescribed number of shares to general public (in case of public

company) or to some specified person (in case of private company) and takes the

money form such persons in lieu of shares given.

Retained earnings: In this method, company often retained its earning by not

distributing to shareholders (by way of dividend) and use this retained earning in

funding of its capital projects (Buchner and others, 2014).

Debenture/bonds: This method for obtaining fund is used when company wants to use

debt source of finance. In this method, the person who is given finance to company is

entitled to receive an income at fixed periodical intervals at fixed rate.

Medium term finance:

These are those finance which are taken by the company for medium term period which

is for 3 to 5 years. This include the followings:

2

and Hill, 2014).

TASK 2

Source of finance:

In any organisation like Burberry Group Plc, for carrying out its business operations

effectively and efficiently, there is a need of finance to provide monetary assistance to its

business operations and for working capital requirements. There are various sources of finance

from where a company may take finance which are as follows:

Long term finance

Medium term finance

Short term finance

Long term finance:

These are those finance which are taken by the company for long term period generally

for more than 5 years. This is taken for financing capital expenditures like purchase of fixed

assets, land and building etc. long term financing sources can in the form of followings:

Share capital or equity shares: In this method, companies like Burberry Group Plc are

often gives a prescribed number of shares to general public (in case of public

company) or to some specified person (in case of private company) and takes the

money form such persons in lieu of shares given.

Retained earnings: In this method, company often retained its earning by not

distributing to shareholders (by way of dividend) and use this retained earning in

funding of its capital projects (Buchner and others, 2014).

Debenture/bonds: This method for obtaining fund is used when company wants to use

debt source of finance. In this method, the person who is given finance to company is

entitled to receive an income at fixed periodical intervals at fixed rate.

Medium term finance:

These are those finance which are taken by the company for medium term period which

is for 3 to 5 years. This include the followings:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Medium term loans: In this method, Burberry Group Plc takes a loan for its business

operations from banks and financial institutions including non banking finance

companies.

Lease finance: It is one of the important sources of medium term financing where owner

of a particular asset gives right to use the assets to the company for a payment of a

predetermined periodical payments (Hieronymi, 2016).

Short term finance:

Short term finance means financing the business requirements for a period not more than

1 year. This is required to finance the current assets, to pay the current liabilities and maintain

liquidity in the company. The various sources of this are as follows:

Trade credit: This is the essential source for the company in which supplier of company

gives extended time to the company for the payment of money for purchase of goods.

Factoring services: This method is important source for maintaining its liquidity in short

period time. In this method, companies like Burberry Group Plc are often sells its account

receivables to the third party at a discount in a situation where there is a requirement of

immediate cash.

Bill discounting: In this period company gives its account receivables to the bank and in

return bank release funds to the company before credit period of account receivables end.

Dividend policy:

A dividend policy of a company depends upon the various key factors affecting its

profitability. A dividend policy determines the amount of dividend which should be given by the

company to the shareholders and determine the fixed intervals of time for dividend payments.

The some of popular policies are as follows:

Stable dividend policy

Constant dividend policy

Residual dividend policy

Stable dividend policy:

In this policy, company aims to give dividend at a steady rate of dividend every year.

This is determined by foresting the company's future earnings and accordingly determine the

stable dividend rate. In such policy, dividend is also be given even if there is any decline in the

3

operations from banks and financial institutions including non banking finance

companies.

Lease finance: It is one of the important sources of medium term financing where owner

of a particular asset gives right to use the assets to the company for a payment of a

predetermined periodical payments (Hieronymi, 2016).

Short term finance:

Short term finance means financing the business requirements for a period not more than

1 year. This is required to finance the current assets, to pay the current liabilities and maintain

liquidity in the company. The various sources of this are as follows:

Trade credit: This is the essential source for the company in which supplier of company

gives extended time to the company for the payment of money for purchase of goods.

Factoring services: This method is important source for maintaining its liquidity in short

period time. In this method, companies like Burberry Group Plc are often sells its account

receivables to the third party at a discount in a situation where there is a requirement of

immediate cash.

Bill discounting: In this period company gives its account receivables to the bank and in

return bank release funds to the company before credit period of account receivables end.

Dividend policy:

A dividend policy of a company depends upon the various key factors affecting its

profitability. A dividend policy determines the amount of dividend which should be given by the

company to the shareholders and determine the fixed intervals of time for dividend payments.

The some of popular policies are as follows:

Stable dividend policy

Constant dividend policy

Residual dividend policy

Stable dividend policy:

In this policy, company aims to give dividend at a steady rate of dividend every year.

This is determined by foresting the company's future earnings and accordingly determine the

stable dividend rate. In such policy, dividend is also be given even if there is any decline in the

3

earnings of the company and also in boom situation, dividend is not given by the organisation at

a higher rate (Huang and others, 2015).

Constant dividend policy:

Under constant dividend policy, company is given dividend at a specific constant rate of

earning of an organisation. In this case, dividend amount payable at every year is affected by the

profits earn by the company every year because in this policy, dividend is given by company is

depended on the earning and earning can not be same in each year.

Residual dividend policy:

This is also a important dividend policy where the rate of earning on retained profits are

more than cost of capital and expected rate of earning. Under this policy, profits left after it is

utilised for internal business operations and after meeting equity capital expenditure requirement

are given to shareholders as a dividend. In this, company give first priority to its investment

proposals and thereafter any residual profits is given to shareholders as a dividend (McFarland,

2015).

TASK 3

Financial performance analysis:

Financial performance of Burberry Group Plc can be evaluated by the help of ratio

analysis. Ratio analysis is a technique by which financial performance of a company can be

evaluated with the help of various ratio calculation such profitability, liquidity, investment and

efficiency ratios etc. For calculation of these ratios financial statements of Burberry Group Plc

are as follows:

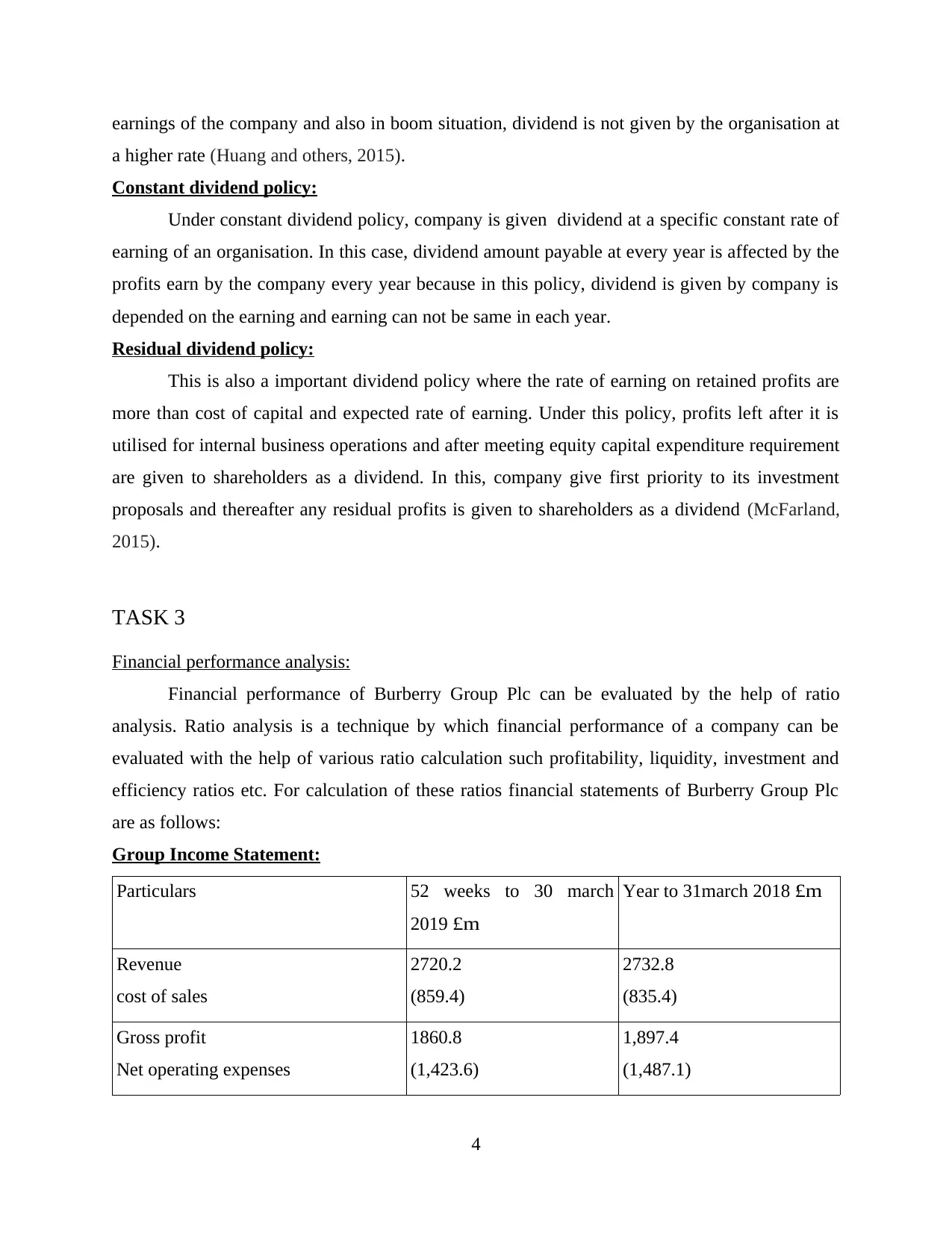

Group Income Statement:

Particulars 52 weeks to 30 march

2019 £m

Year to 31march 2018 £m

Revenue

cost of sales

2720.2

(859.4)

2732.8

(835.4)

Gross profit

Net operating expenses

1860.8

(1,423.6)

1,897.4

(1,487.1)

4

a higher rate (Huang and others, 2015).

Constant dividend policy:

Under constant dividend policy, company is given dividend at a specific constant rate of

earning of an organisation. In this case, dividend amount payable at every year is affected by the

profits earn by the company every year because in this policy, dividend is given by company is

depended on the earning and earning can not be same in each year.

Residual dividend policy:

This is also a important dividend policy where the rate of earning on retained profits are

more than cost of capital and expected rate of earning. Under this policy, profits left after it is

utilised for internal business operations and after meeting equity capital expenditure requirement

are given to shareholders as a dividend. In this, company give first priority to its investment

proposals and thereafter any residual profits is given to shareholders as a dividend (McFarland,

2015).

TASK 3

Financial performance analysis:

Financial performance of Burberry Group Plc can be evaluated by the help of ratio

analysis. Ratio analysis is a technique by which financial performance of a company can be

evaluated with the help of various ratio calculation such profitability, liquidity, investment and

efficiency ratios etc. For calculation of these ratios financial statements of Burberry Group Plc

are as follows:

Group Income Statement:

Particulars 52 weeks to 30 march

2019 £m

Year to 31march 2018 £m

Revenue

cost of sales

2720.2

(859.4)

2732.8

(835.4)

Gross profit

Net operating expenses

1860.8

(1,423.6)

1,897.4

(1,487.1)

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating profit 437.2 410.3

Financing:

Finance income

Finance expense

Other financing charge

8.7

(3.6)

(1.7)

7.8

(3.5)

(2.0)

Net finance income 3.4 2.3

Profit before taxation

Taxation

440.6

(101.5)

412.6

(119.0)

Profit for the year 339.1 293.6

Attributable to:

Owners of the Company

Non-controlling interest

339.3

(0.2)

293.5

0.1

Profit for the year 339.1 293.6

Earnings per share

:

Basic

Diluted

82.3p

81.7p

68.9p

68.4p

Group balance sheet:

Particulars As at

30 March

2019

As at

31 March

2018

5

Financing:

Finance income

Finance expense

Other financing charge

8.7

(3.6)

(1.7)

7.8

(3.5)

(2.0)

Net finance income 3.4 2.3

Profit before taxation

Taxation

440.6

(101.5)

412.6

(119.0)

Profit for the year 339.1 293.6

Attributable to:

Owners of the Company

Non-controlling interest

339.3

(0.2)

293.5

0.1

Profit for the year 339.1 293.6

Earnings per share

:

Basic

Diluted

82.3p

81.7p

68.9p

68.4p

Group balance sheet:

Particulars As at

30 March

2019

As at

31 March

2018

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

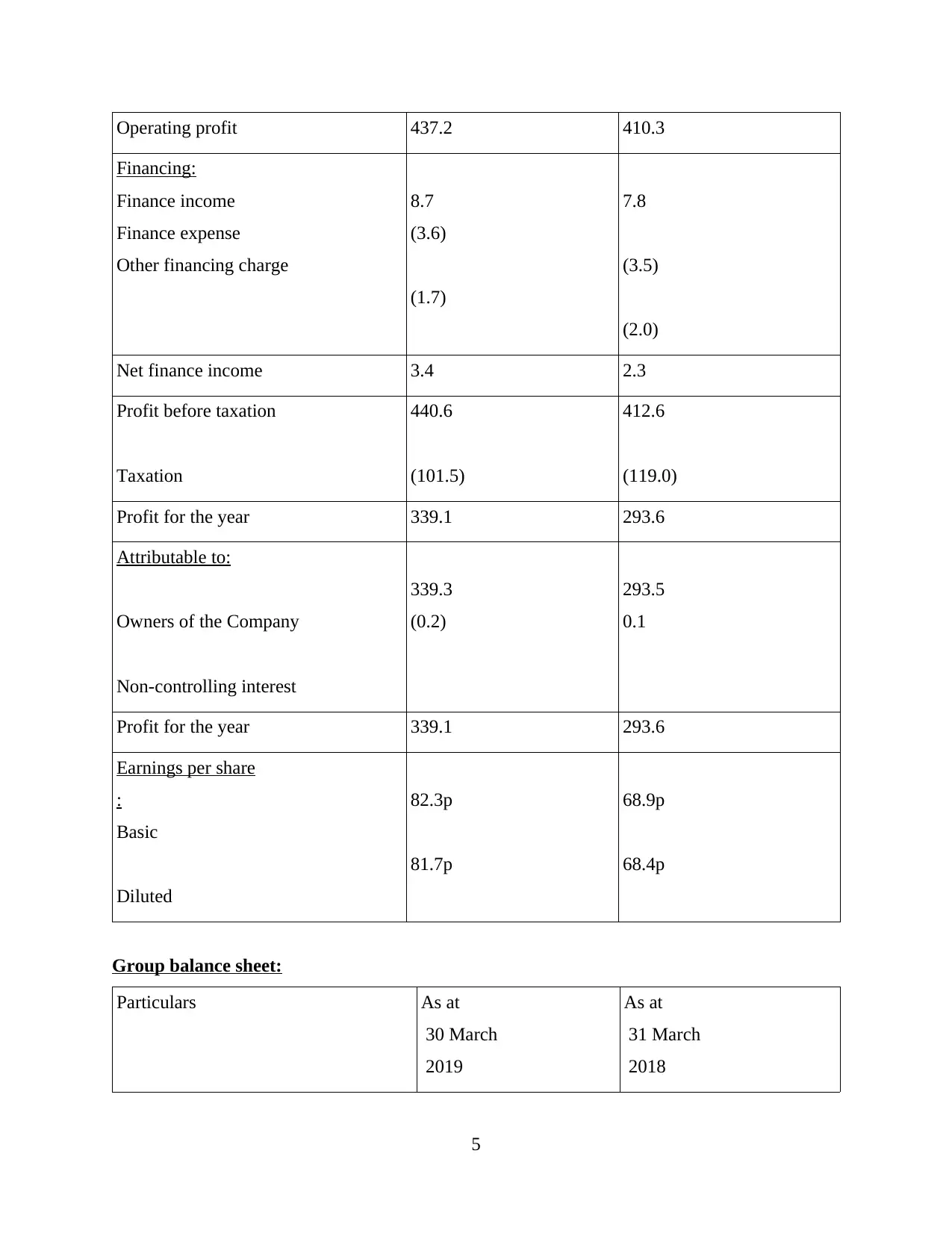

£m £m

ASSETS

:

Non-current assets

Intangible assets

Property, plant and equipment

Investment properties

Deferred tax assets

Trade and other receivables

Derivative financial assets

221.0

306.9

2.5

123.1

70.1

–

180.1

313.6

2.6

115.5

69.2

0.3

723.6 681.3

Current assets

Inventories

Trade and other receivables

Derivative financial assets

Income tax receivables

Cash and cash equivalents

465.1

251.1

3.0

14.9

874.5

411.8

206.3

1.6

6.7

915.3

1608.6 1541.7

Total assets 2332.2 2223

6

ASSETS

:

Non-current assets

Intangible assets

Property, plant and equipment

Investment properties

Deferred tax assets

Trade and other receivables

Derivative financial assets

221.0

306.9

2.5

123.1

70.1

–

180.1

313.6

2.6

115.5

69.2

0.3

723.6 681.3

Current assets

Inventories

Trade and other receivables

Derivative financial assets

Income tax receivables

Cash and cash equivalents

465.1

251.1

3.0

14.9

874.5

411.8

206.3

1.6

6.7

915.3

1608.6 1541.7

Total assets 2332.2 2223

6

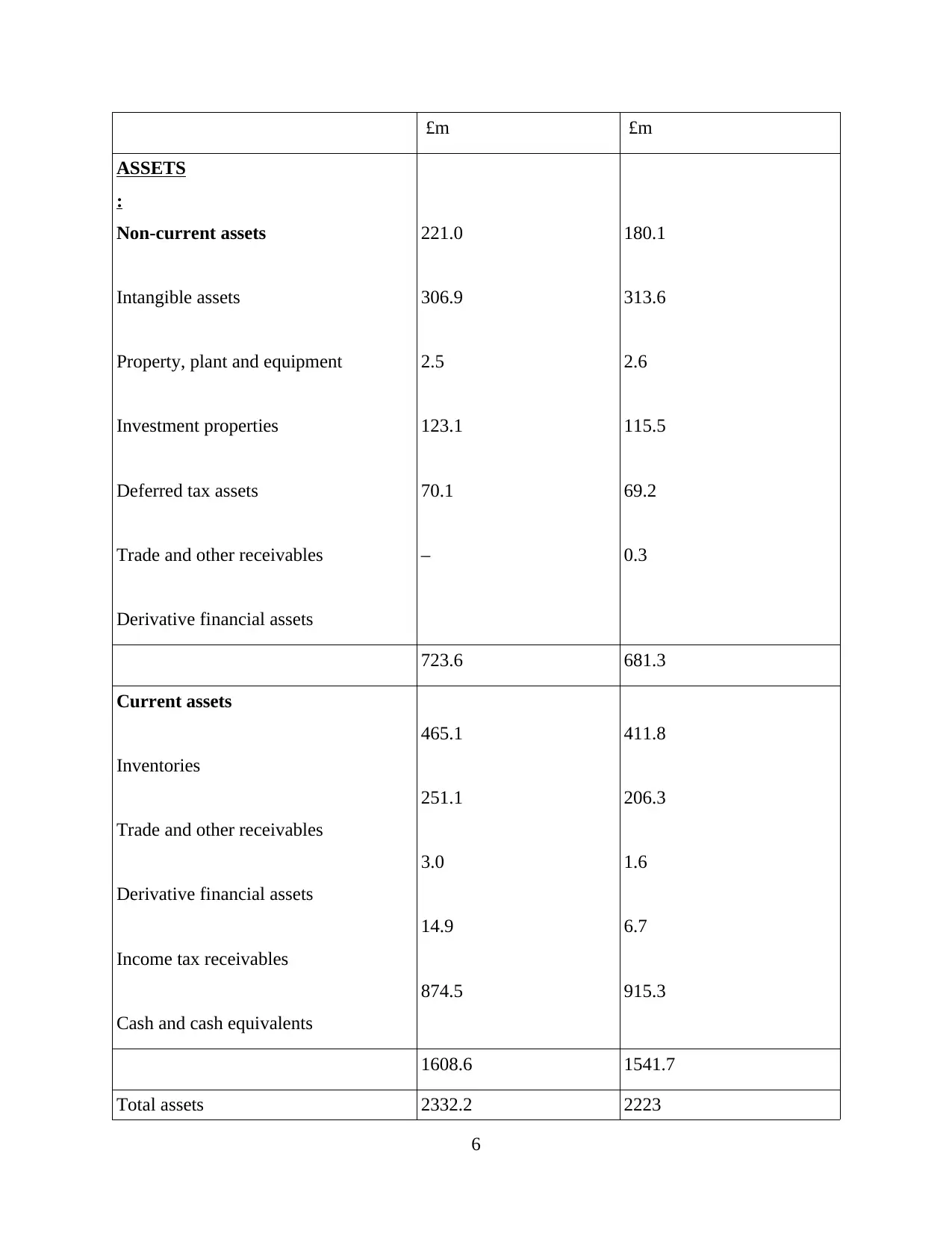

LIABILITIES

Non-current liabilities

Trade and other payables

Deferred tax liabilities

Derivative financial liabilities

Retirement benefit obligations

Provisions for other liabilities and

charges

(176.5)

(3.4)

(0.1)

(1.4)

(50.7)

(168.1)

(4.2)

(0.1)

(0.9)

(71.4)

-232.1 -244.7

Current liabilities

Bank overdrafts

Derivative financial liabilities

Trade and other payables

Provisions for other liabilities and

charges

Income tax liabilities

(37.2)

(5.5)

(525.7)

(34.6)

(37.1)

(23.2)

(3.8)

(460.9)

(32.1)

(32.9)

-640.1 -552.9

Total liabilities -872.2 -797.6

7

Non-current liabilities

Trade and other payables

Deferred tax liabilities

Derivative financial liabilities

Retirement benefit obligations

Provisions for other liabilities and

charges

(176.5)

(3.4)

(0.1)

(1.4)

(50.7)

(168.1)

(4.2)

(0.1)

(0.9)

(71.4)

-232.1 -244.7

Current liabilities

Bank overdrafts

Derivative financial liabilities

Trade and other payables

Provisions for other liabilities and

charges

Income tax liabilities

(37.2)

(5.5)

(525.7)

(34.6)

(37.1)

(23.2)

(3.8)

(460.9)

(32.1)

(32.9)

-640.1 -552.9

Total liabilities -872.2 -797.6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

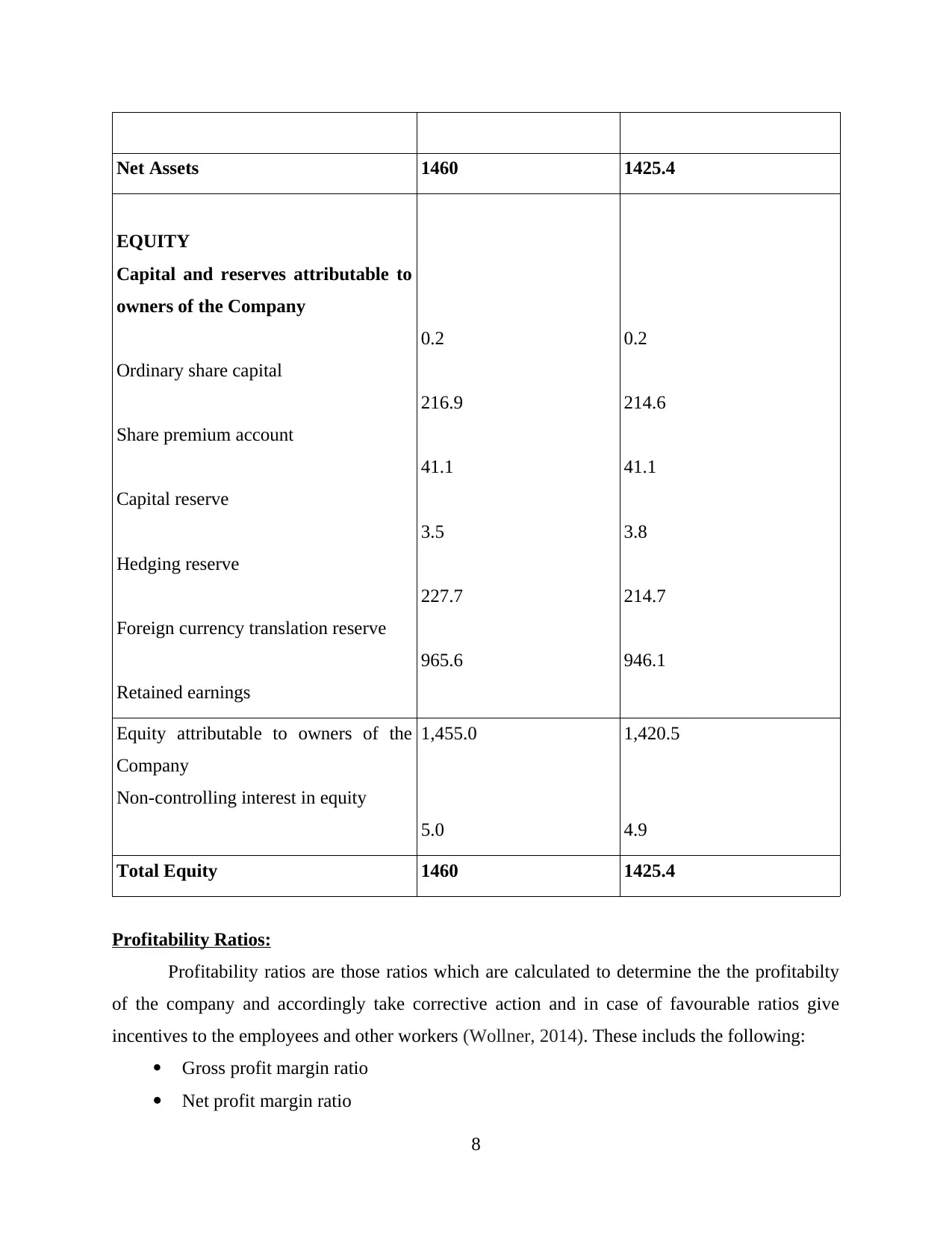

Net Assets 1460 1425.4

EQUITY

Capital and reserves attributable to

owners of the Company

Ordinary share capital

Share premium account

Capital reserve

Hedging reserve

Foreign currency translation reserve

Retained earnings

0.2

216.9

41.1

3.5

227.7

965.6

0.2

214.6

41.1

3.8

214.7

946.1

Equity attributable to owners of the

Company

Non-controlling interest in equity

1,455.0

5.0

1,420.5

4.9

Total Equity 1460 1425.4

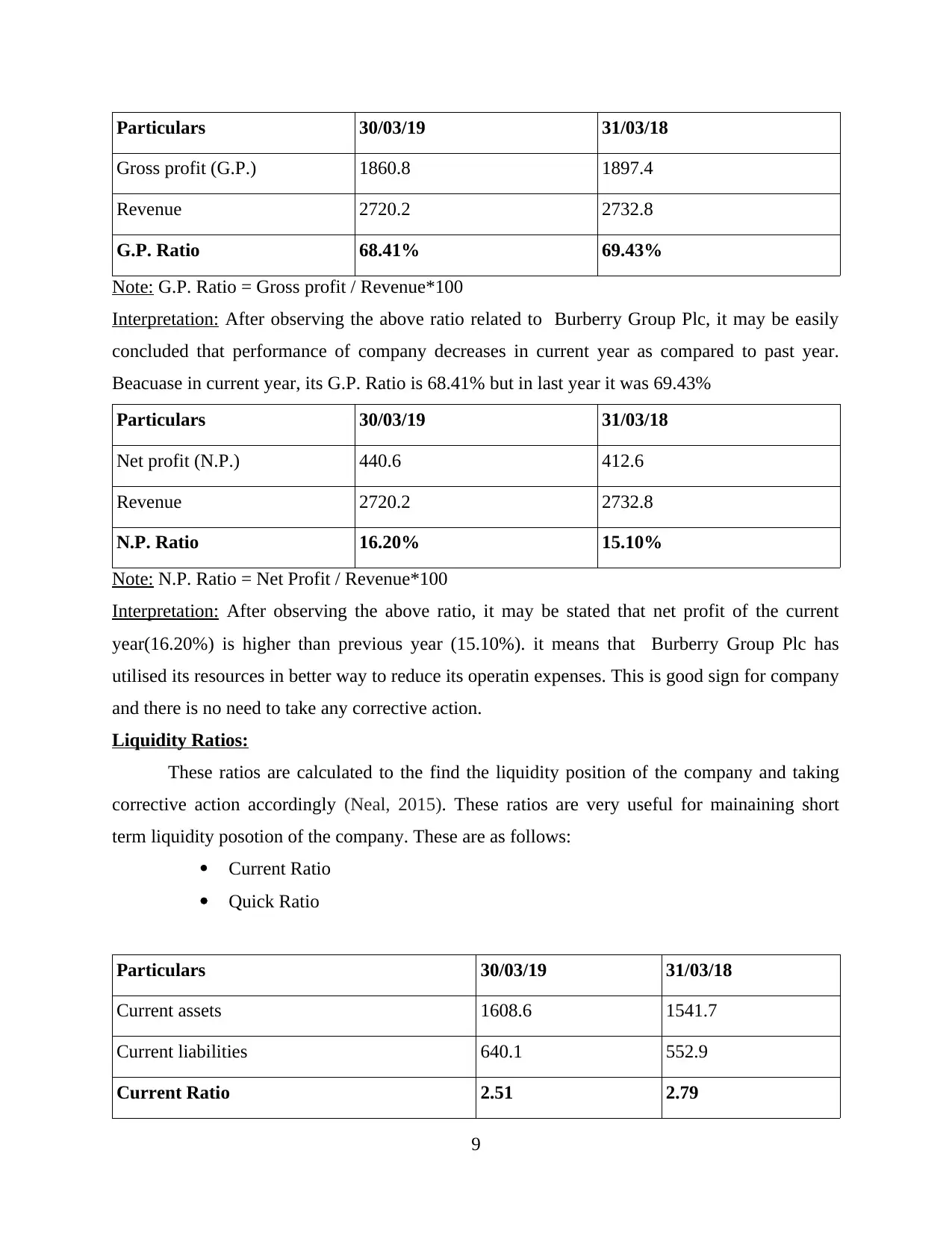

Profitability Ratios:

Profitability ratios are those ratios which are calculated to determine the the profitabilty

of the company and accordingly take corrective action and in case of favourable ratios give

incentives to the employees and other workers (Wollner, 2014). These includs the following:

Gross profit margin ratio

Net profit margin ratio

8

EQUITY

Capital and reserves attributable to

owners of the Company

Ordinary share capital

Share premium account

Capital reserve

Hedging reserve

Foreign currency translation reserve

Retained earnings

0.2

216.9

41.1

3.5

227.7

965.6

0.2

214.6

41.1

3.8

214.7

946.1

Equity attributable to owners of the

Company

Non-controlling interest in equity

1,455.0

5.0

1,420.5

4.9

Total Equity 1460 1425.4

Profitability Ratios:

Profitability ratios are those ratios which are calculated to determine the the profitabilty

of the company and accordingly take corrective action and in case of favourable ratios give

incentives to the employees and other workers (Wollner, 2014). These includs the following:

Gross profit margin ratio

Net profit margin ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars 30/03/19 31/03/18

Gross profit (G.P.) 1860.8 1897.4

Revenue 2720.2 2732.8

G.P. Ratio 68.41% 69.43%

Note: G.P. Ratio = Gross profit / Revenue*100

Interpretation: After observing the above ratio related to Burberry Group Plc, it may be easily

concluded that performance of company decreases in current year as compared to past year.

Beacuase in current year, its G.P. Ratio is 68.41% but in last year it was 69.43%

Particulars 30/03/19 31/03/18

Net profit (N.P.) 440.6 412.6

Revenue 2720.2 2732.8

N.P. Ratio 16.20% 15.10%

Note: N.P. Ratio = Net Profit / Revenue*100

Interpretation: After observing the above ratio, it may be stated that net profit of the current

year(16.20%) is higher than previous year (15.10%). it means that Burberry Group Plc has

utilised its resources in better way to reduce its operatin expenses. This is good sign for company

and there is no need to take any corrective action.

Liquidity Ratios:

These ratios are calculated to the find the liquidity position of the company and taking

corrective action accordingly (Neal, 2015). These ratios are very useful for mainaining short

term liquidity posotion of the company. These are as follows:

Current Ratio

Quick Ratio

Particulars 30/03/19 31/03/18

Current assets 1608.6 1541.7

Current liabilities 640.1 552.9

Current Ratio 2.51 2.79

9

Gross profit (G.P.) 1860.8 1897.4

Revenue 2720.2 2732.8

G.P. Ratio 68.41% 69.43%

Note: G.P. Ratio = Gross profit / Revenue*100

Interpretation: After observing the above ratio related to Burberry Group Plc, it may be easily

concluded that performance of company decreases in current year as compared to past year.

Beacuase in current year, its G.P. Ratio is 68.41% but in last year it was 69.43%

Particulars 30/03/19 31/03/18

Net profit (N.P.) 440.6 412.6

Revenue 2720.2 2732.8

N.P. Ratio 16.20% 15.10%

Note: N.P. Ratio = Net Profit / Revenue*100

Interpretation: After observing the above ratio, it may be stated that net profit of the current

year(16.20%) is higher than previous year (15.10%). it means that Burberry Group Plc has

utilised its resources in better way to reduce its operatin expenses. This is good sign for company

and there is no need to take any corrective action.

Liquidity Ratios:

These ratios are calculated to the find the liquidity position of the company and taking

corrective action accordingly (Neal, 2015). These ratios are very useful for mainaining short

term liquidity posotion of the company. These are as follows:

Current Ratio

Quick Ratio

Particulars 30/03/19 31/03/18

Current assets 1608.6 1541.7

Current liabilities 640.1 552.9

Current Ratio 2.51 2.79

9

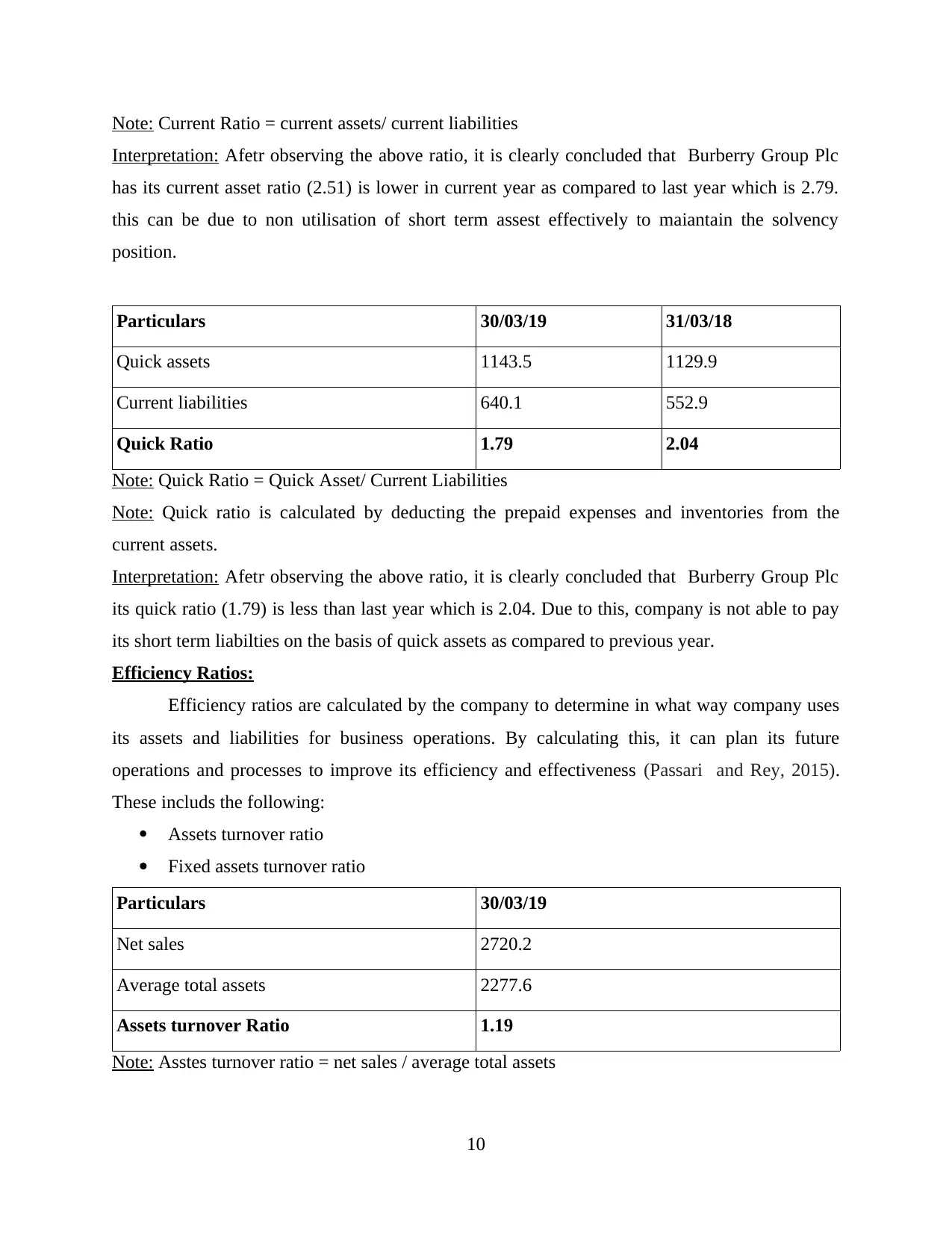

Note: Current Ratio = current assets/ current liabilities

Interpretation: Afetr observing the above ratio, it is clearly concluded that Burberry Group Plc

has its current asset ratio (2.51) is lower in current year as compared to last year which is 2.79.

this can be due to non utilisation of short term assest effectively to maiantain the solvency

position.

Particulars 30/03/19 31/03/18

Quick assets 1143.5 1129.9

Current liabilities 640.1 552.9

Quick Ratio 1.79 2.04

Note: Quick Ratio = Quick Asset/ Current Liabilities

Note: Quick ratio is calculated by deducting the prepaid expenses and inventories from the

current assets.

Interpretation: Afetr observing the above ratio, it is clearly concluded that Burberry Group Plc

its quick ratio (1.79) is less than last year which is 2.04. Due to this, company is not able to pay

its short term liabilties on the basis of quick assets as compared to previous year.

Efficiency Ratios:

Efficiency ratios are calculated by the company to determine in what way company uses

its assets and liabilities for business operations. By calculating this, it can plan its future

operations and processes to improve its efficiency and effectiveness (Passari and Rey, 2015).

These includs the following:

Assets turnover ratio

Fixed assets turnover ratio

Particulars 30/03/19

Net sales 2720.2

Average total assets 2277.6

Assets turnover Ratio 1.19

Note: Asstes turnover ratio = net sales / average total assets

10

Interpretation: Afetr observing the above ratio, it is clearly concluded that Burberry Group Plc

has its current asset ratio (2.51) is lower in current year as compared to last year which is 2.79.

this can be due to non utilisation of short term assest effectively to maiantain the solvency

position.

Particulars 30/03/19 31/03/18

Quick assets 1143.5 1129.9

Current liabilities 640.1 552.9

Quick Ratio 1.79 2.04

Note: Quick Ratio = Quick Asset/ Current Liabilities

Note: Quick ratio is calculated by deducting the prepaid expenses and inventories from the

current assets.

Interpretation: Afetr observing the above ratio, it is clearly concluded that Burberry Group Plc

its quick ratio (1.79) is less than last year which is 2.04. Due to this, company is not able to pay

its short term liabilties on the basis of quick assets as compared to previous year.

Efficiency Ratios:

Efficiency ratios are calculated by the company to determine in what way company uses

its assets and liabilities for business operations. By calculating this, it can plan its future

operations and processes to improve its efficiency and effectiveness (Passari and Rey, 2015).

These includs the following:

Assets turnover ratio

Fixed assets turnover ratio

Particulars 30/03/19

Net sales 2720.2

Average total assets 2277.6

Assets turnover Ratio 1.19

Note: Asstes turnover ratio = net sales / average total assets

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.