International Finance: Evaluating Hedging Strategies for Pomo Limited

VerifiedAdded on 2023/05/29

|11

|1974

|271

Homework Assignment

AI Summary

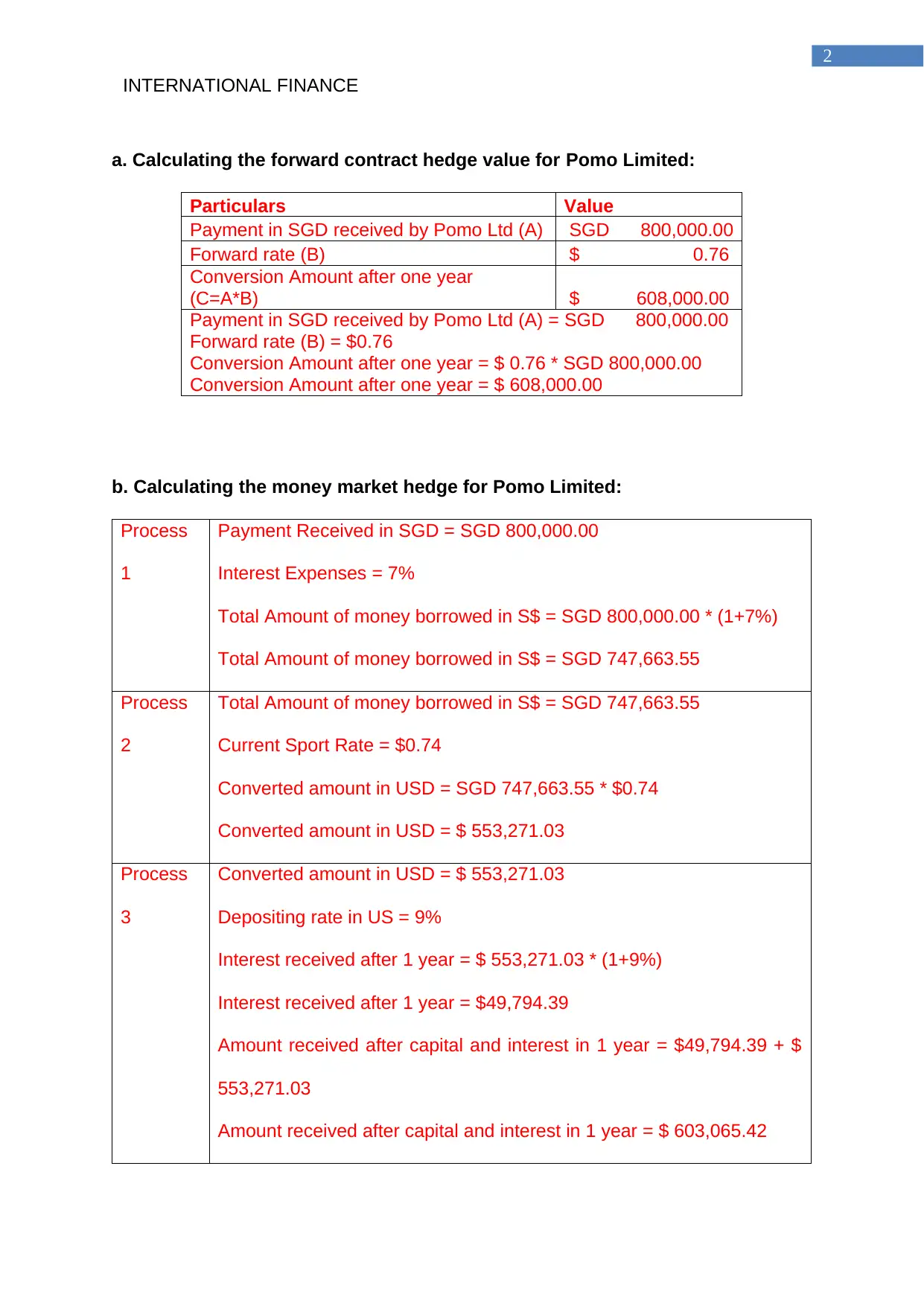

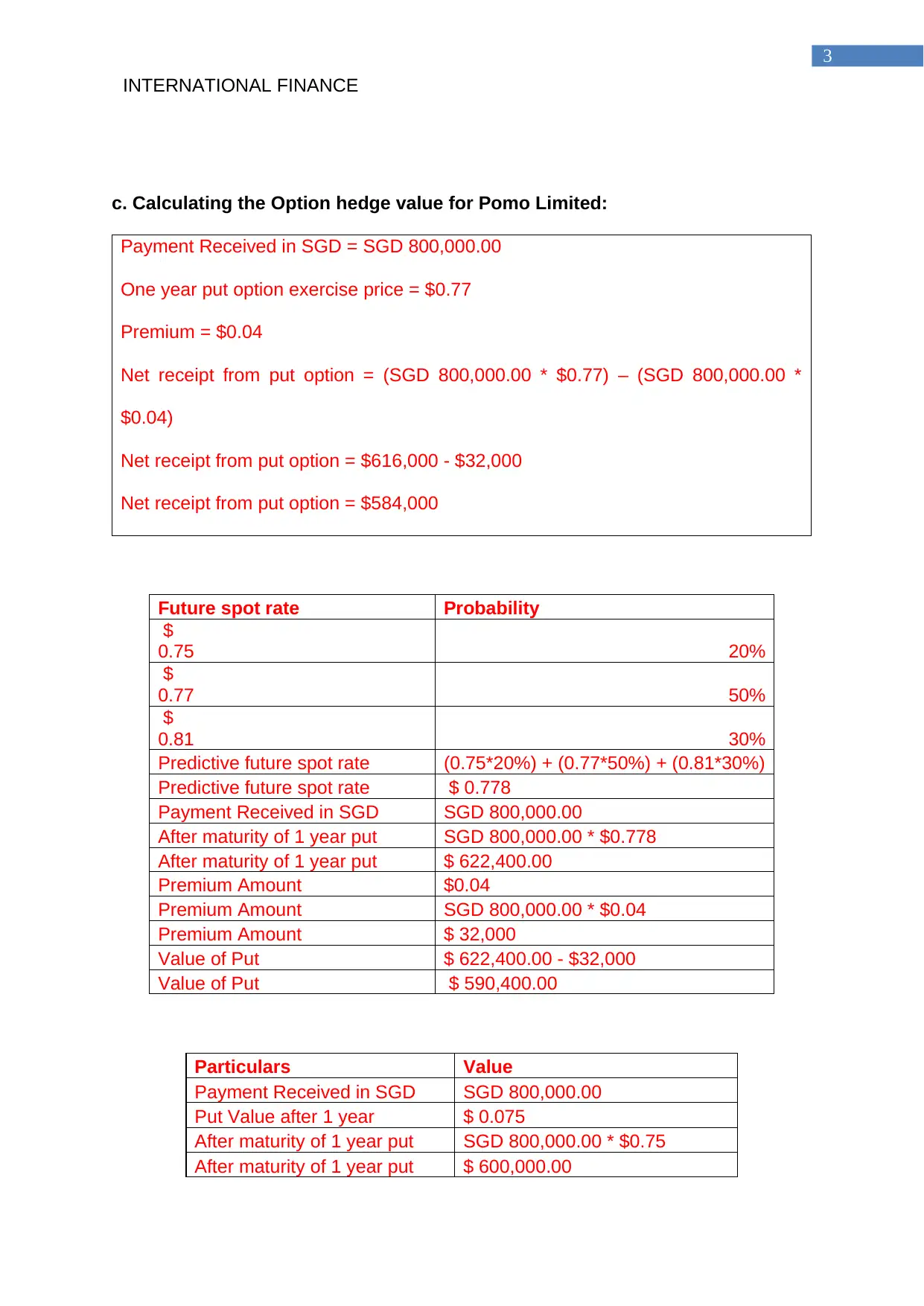

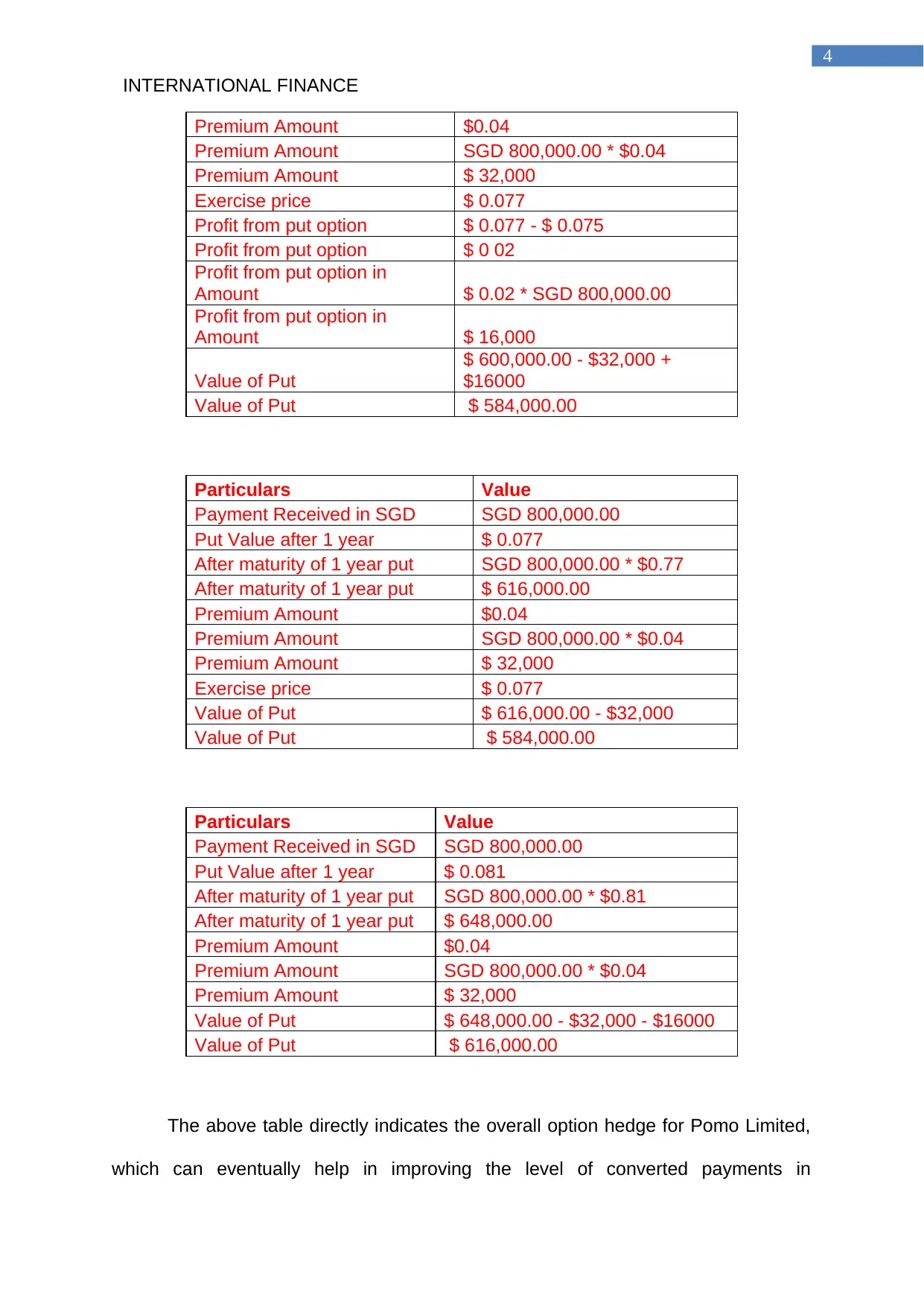

This assignment focuses on international finance and hedging strategies, specifically analyzing the case of Pomo Limited. It calculates the values of forward contract, money market, and option hedges, comparing their effectiveness in mitigating currency risk. The analysis includes detailed calculations for each hedging method, considering factors like forward rates, interest expenses, spot rates, and option premiums. Furthermore, the assignment briefly discusses the optimal hedge against a no-hedge position, recommending forward contract hedging as the most advantageous. It also explores financial hedging in general, outlining its advantages, disadvantages, and recommending alternative methods like operational hedging and cross-hedging. The assignment references several academic sources to support its findings and recommendations, providing a comprehensive overview of hedging techniques in international finance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.