International Financial Management Homework: Risk Hedging

VerifiedAdded on 2022/09/23

|7

|1224

|22

Homework Assignment

AI Summary

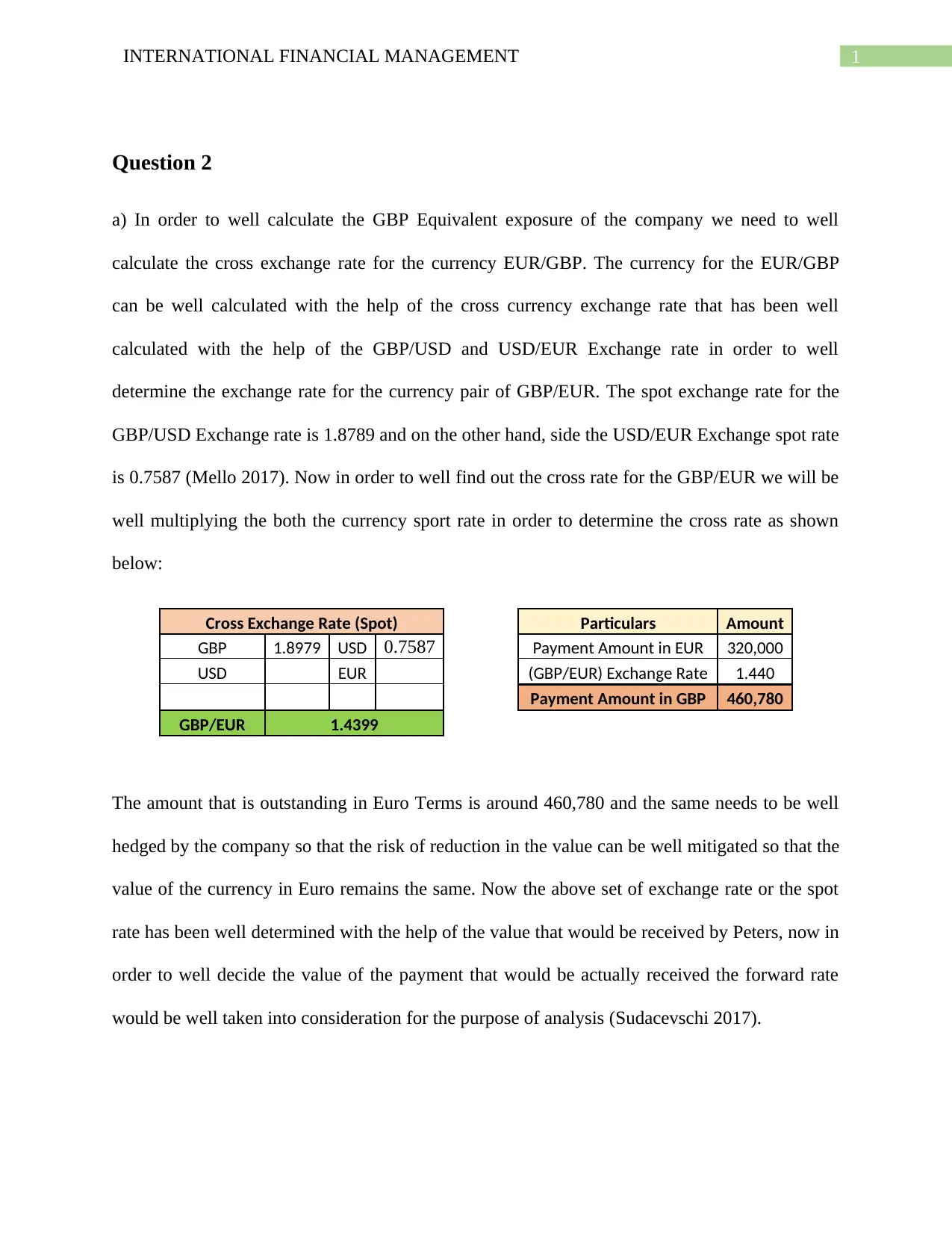

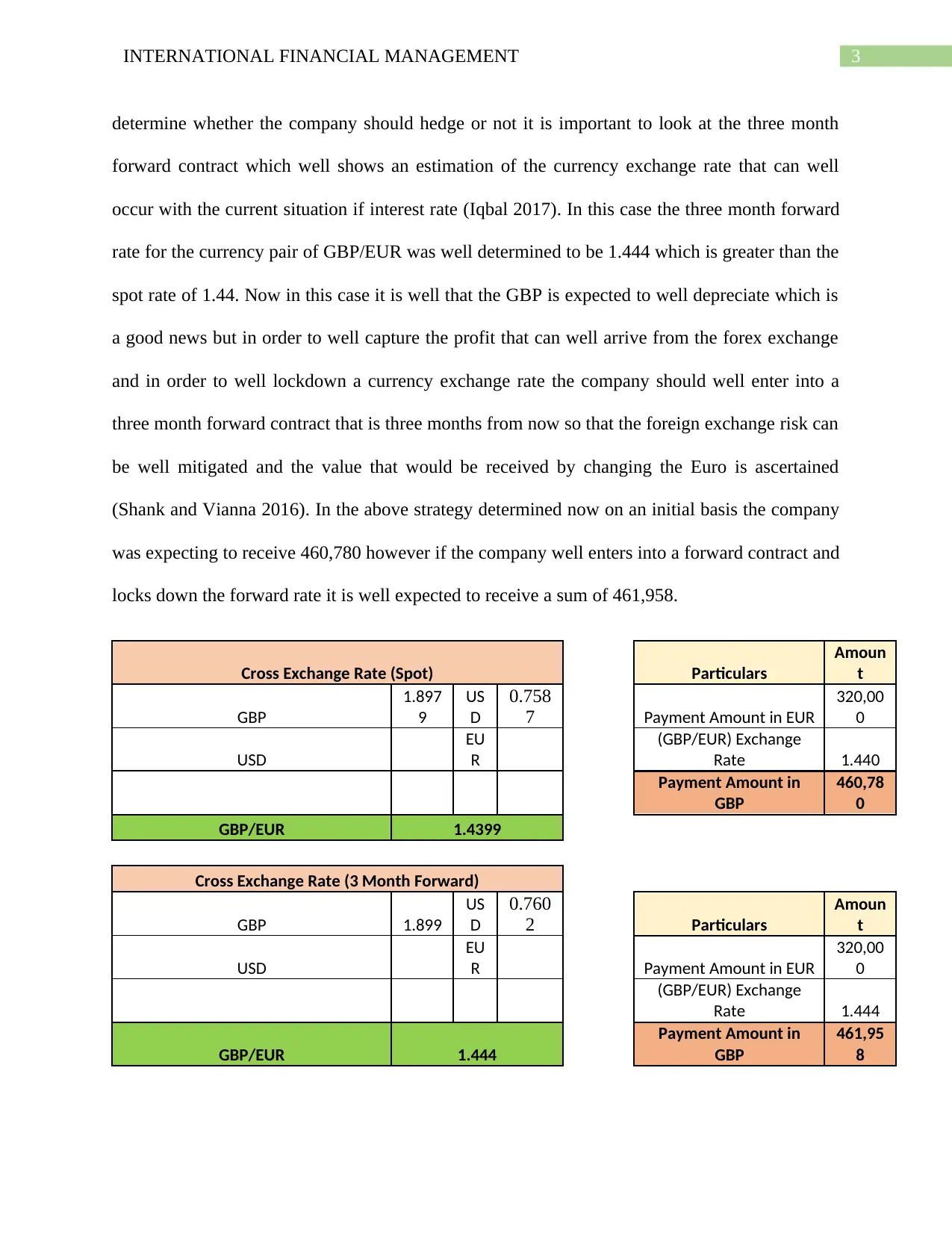

This homework assignment analyzes a foreign exchange transaction faced by Shrewsbury Herbal, focusing on the currency exposure related to a sale invoiced in British Pounds Sterling to a customer in France. The student calculates the cross exchange rate between GBP/EUR, determines the foreign exchange exposure, and evaluates the risk associated with fluctuations in the currency values. The assignment explores the use of hedging strategies, specifically a three-month forward contract, to mitigate the risk of pound appreciation and its impact on the receivable value. The analysis compares the outcomes of the spot rate versus the forward rate to determine the optimal hedging strategy for the company. The assignment references several academic articles to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.