International Finance: Analysis of Company Risk and Strategies

VerifiedAdded on 2021/04/21

|14

|2795

|16

Report

AI Summary

This report delves into the realm of international finance, examining the financial strategies and risk management practices of multinational corporations. It begins with a case study exploring the reinvestment decisions of a company, considering factors like interest rates and currency exchange fluctuations between Australia and Thailand. The report then shifts its focus to a comparative analysis of Rio Tinto and Brambles Limited, two major companies operating globally. It investigates their foreign exchange risks, particularly the impact of currency fluctuations on their financial performance, and assesses the correlation between exchange rates and their respective share prices. Furthermore, the report evaluates the companies' listing strategies and provides recommendations for Brambles Limited regarding potential stock exchange listings to enhance its financial flexibility and risk diversification. The report concludes with a reference list and appendices containing relevant data, offering a comprehensive overview of the complexities and challenges inherent in international finance.

Running head: INTERNATIONAL FINANCE

International finance

Name of the Student:

Name of the University:

Authors Note:

International finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2INTERNATIONAL FINANCE

Table of Contents

PART A:.....................................................................................................................................3

Answer to question 1..................................................................................................................3

Answer to question 2..................................................................................................................3

Answer to question 3..................................................................................................................4

PART B:.....................................................................................................................................6

Answer to question 1..................................................................................................................6

Answer to question 2..................................................................................................................8

Reference..................................................................................................................................10

Appendices...............................................................................................................................12

Table of Contents

PART A:.....................................................................................................................................3

Answer to question 1..................................................................................................................3

Answer to question 2..................................................................................................................3

Answer to question 3..................................................................................................................4

PART B:.....................................................................................................................................6

Answer to question 1..................................................................................................................6

Answer to question 2..................................................................................................................8

Reference..................................................................................................................................10

Appendices...............................................................................................................................12

3INTERNATIONAL FINANCE

PART A:

Answer to question 1.

The company is faced with a situation wherein it has an option of reinvesting its

excess funds back into Thailand which will yield returns at a higher rate of interest than what

the company will be earning if the amount is invested back in Australia i.e. its own country.

The interest rates on investments in Australia and Thailand are 8% and 15% respectively.

Apparently it might seem that it is reasonable to invest back the amount in Thailand but, the

company should factor in the fact that such high rates of interest suggest that the economic

condition of Thailand is uncertain (Borio et al. 2017). This uncertainty may lead to the

depreciation of Baht currency in the near future which will reduce the overall exchange rate

of the currency i.e. the company will get fewer amount of Australian Dollars in exchange of

same number of Baht. Hence, it is prudent that the company its excess funds in Australia at a

lower rates of interest than in Thailand.

Answer to question 2.

The company needs additional funds for the supporting its operations back in

Australia. If the company reinvests the excess amount earned in Thailand instead of remitting

it back to Australia, it will have to borrow additional funds at an interest rate of 10% back in

Australia. Further, if the value of Baht depreciates by 5%, which is very reasonably possible

sighting the uncertainty in its economy, the returns earned from Thailand will reduce to

9.25%. Further, the company will not be investing the excess funds at a return of 8% in

Australia (Avdjiev et al. 2016). Hence it is seen that the company reinvests the funds back in

Thailand it will have to incur extra debt expenditure for the additional funds raised via

borrowing and furthermore the return that s earned in Thailand will reduce in the near future

to 9.25%.

PART A:

Answer to question 1.

The company is faced with a situation wherein it has an option of reinvesting its

excess funds back into Thailand which will yield returns at a higher rate of interest than what

the company will be earning if the amount is invested back in Australia i.e. its own country.

The interest rates on investments in Australia and Thailand are 8% and 15% respectively.

Apparently it might seem that it is reasonable to invest back the amount in Thailand but, the

company should factor in the fact that such high rates of interest suggest that the economic

condition of Thailand is uncertain (Borio et al. 2017). This uncertainty may lead to the

depreciation of Baht currency in the near future which will reduce the overall exchange rate

of the currency i.e. the company will get fewer amount of Australian Dollars in exchange of

same number of Baht. Hence, it is prudent that the company its excess funds in Australia at a

lower rates of interest than in Thailand.

Answer to question 2.

The company needs additional funds for the supporting its operations back in

Australia. If the company reinvests the excess amount earned in Thailand instead of remitting

it back to Australia, it will have to borrow additional funds at an interest rate of 10% back in

Australia. Further, if the value of Baht depreciates by 5%, which is very reasonably possible

sighting the uncertainty in its economy, the returns earned from Thailand will reduce to

9.25%. Further, the company will not be investing the excess funds at a return of 8% in

Australia (Avdjiev et al. 2016). Hence it is seen that the company reinvests the funds back in

Thailand it will have to incur extra debt expenditure for the additional funds raised via

borrowing and furthermore the return that s earned in Thailand will reduce in the near future

to 9.25%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4INTERNATIONAL FINANCE

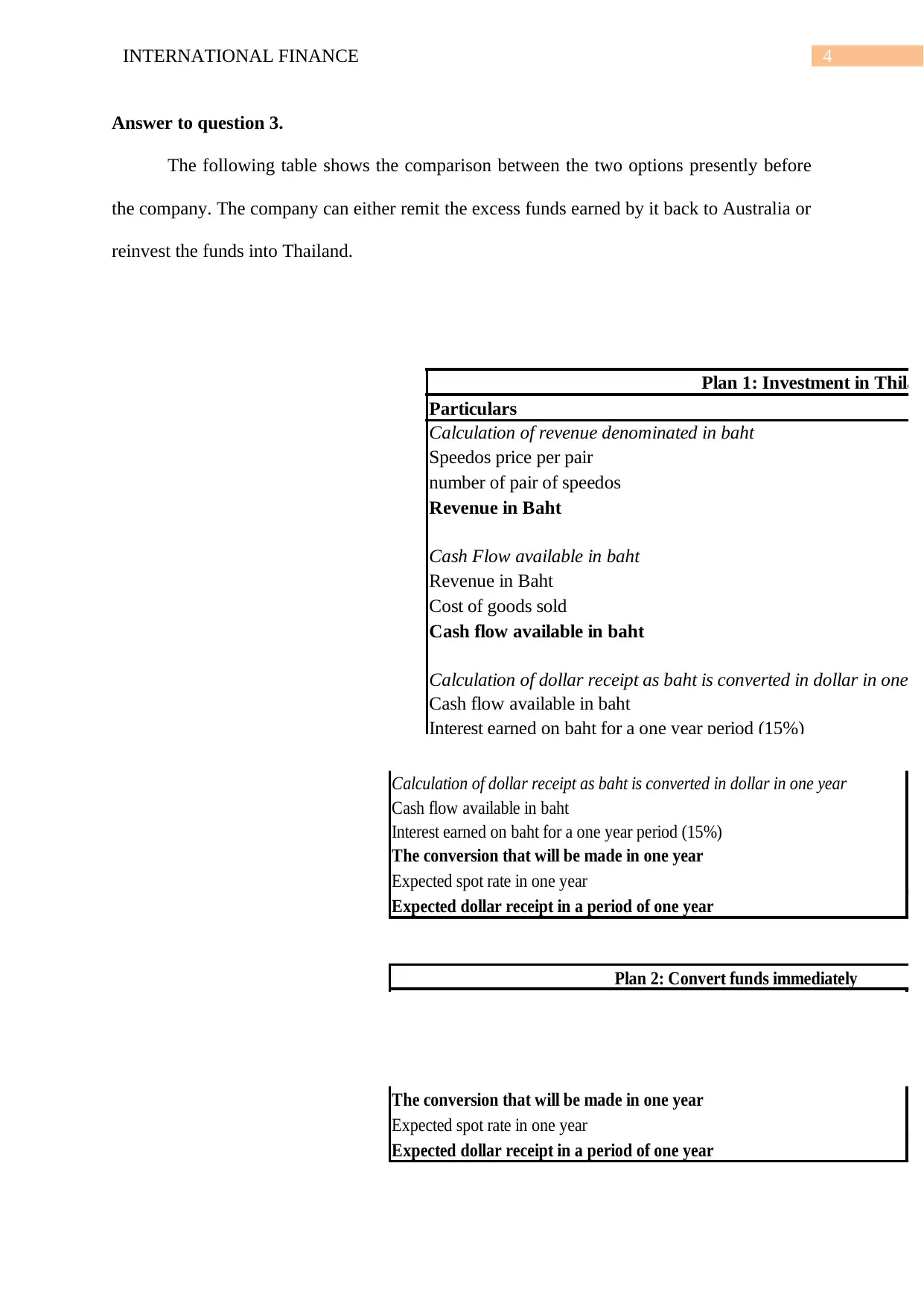

Answer to question 3.

The following table shows the comparison between the two options presently before

the company. The company can either remit the excess funds earned by it back to Australia or

reinvest the funds into Thailand.

Plan 1: Investment in Thilan

Particulars

Calculation of revenue denominated in baht

Speedos price per pair

number of pair of speedos

Revenue in Baht

Cash Flow available in baht

Revenue in Baht

Cost of goods sold

Cash flow available in baht

Calculation of dollar receipt as baht is converted in dollar in one ye

Cash flow available in baht

Interest earned on baht for a one year period (15%)

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht

Interest earned on baht for a one year period (15%)

The conversion that will be made in one year

Expected spot rate in one year

Expected dollar receipt in a period of one year

Plan 2: Convert funds immediately

The conversion that will be made in one year

Expected spot rate in one year

Expected dollar receipt in a period of one year

Answer to question 3.

The following table shows the comparison between the two options presently before

the company. The company can either remit the excess funds earned by it back to Australia or

reinvest the funds into Thailand.

Plan 1: Investment in Thilan

Particulars

Calculation of revenue denominated in baht

Speedos price per pair

number of pair of speedos

Revenue in Baht

Cash Flow available in baht

Revenue in Baht

Cost of goods sold

Cash flow available in baht

Calculation of dollar receipt as baht is converted in dollar in one ye

Cash flow available in baht

Interest earned on baht for a one year period (15%)

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht

Interest earned on baht for a one year period (15%)

The conversion that will be made in one year

Expected spot rate in one year

Expected dollar receipt in a period of one year

Plan 2: Convert funds immediately

The conversion that will be made in one year

Expected spot rate in one year

Expected dollar receipt in a period of one year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5INTERNATIONAL FINANCE

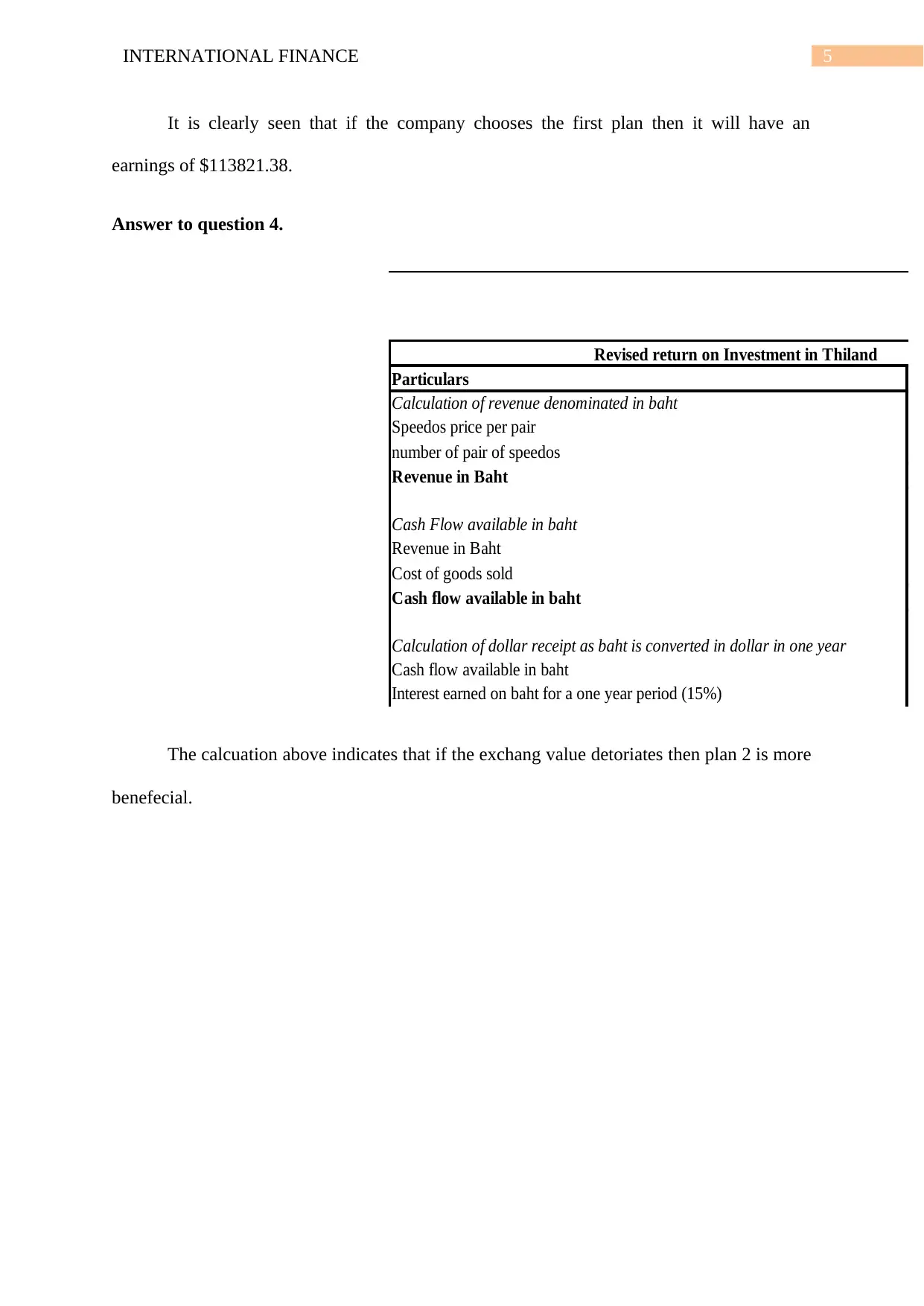

It is clearly seen that if the company chooses the first plan then it will have an

earnings of $113821.38.

Answer to question 4.

Revised return on Investment in Thiland

Particulars

Calculation of revenue denominated in baht

Speedos price per pair

number of pair of speedos

Revenue in Baht

Cash Flow available in baht

Revenue in Baht

Cost of goods sold

Cash flow available in baht

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht

Interest earned on baht for a one year period (15%)

The calcuation above indicates that if the exchang value detoriates then plan 2 is more

benefecial.

It is clearly seen that if the company chooses the first plan then it will have an

earnings of $113821.38.

Answer to question 4.

Revised return on Investment in Thiland

Particulars

Calculation of revenue denominated in baht

Speedos price per pair

number of pair of speedos

Revenue in Baht

Cash Flow available in baht

Revenue in Baht

Cost of goods sold

Cash flow available in baht

Calculation of dollar receipt as baht is converted in dollar in one year

Cash flow available in baht

Interest earned on baht for a one year period (15%)

The calcuation above indicates that if the exchang value detoriates then plan 2 is more

benefecial.

6INTERNATIONAL FINANCE

PART B:

Answer to question 1.

a) RioTinto:

The company is engaged in the metals and mining operations. It is one of the largest

metal and mining corporations across the globe. The company was established in 1873 which

was the result of collective investment from multinational investors to acquire a mining

complex in Rio Tinto in Huelva in Spain (Schoenmaker 2017). The company thereafter went

for many mergers and acquisitions to become a leader I production of many commodities like

aluminium, uranium, iron ore, copper, coals and diamonds. Though the company is mainly

concerned with extraction of minerals the company is also part of many refining activities

especially refining of Bauxite and iron ore.

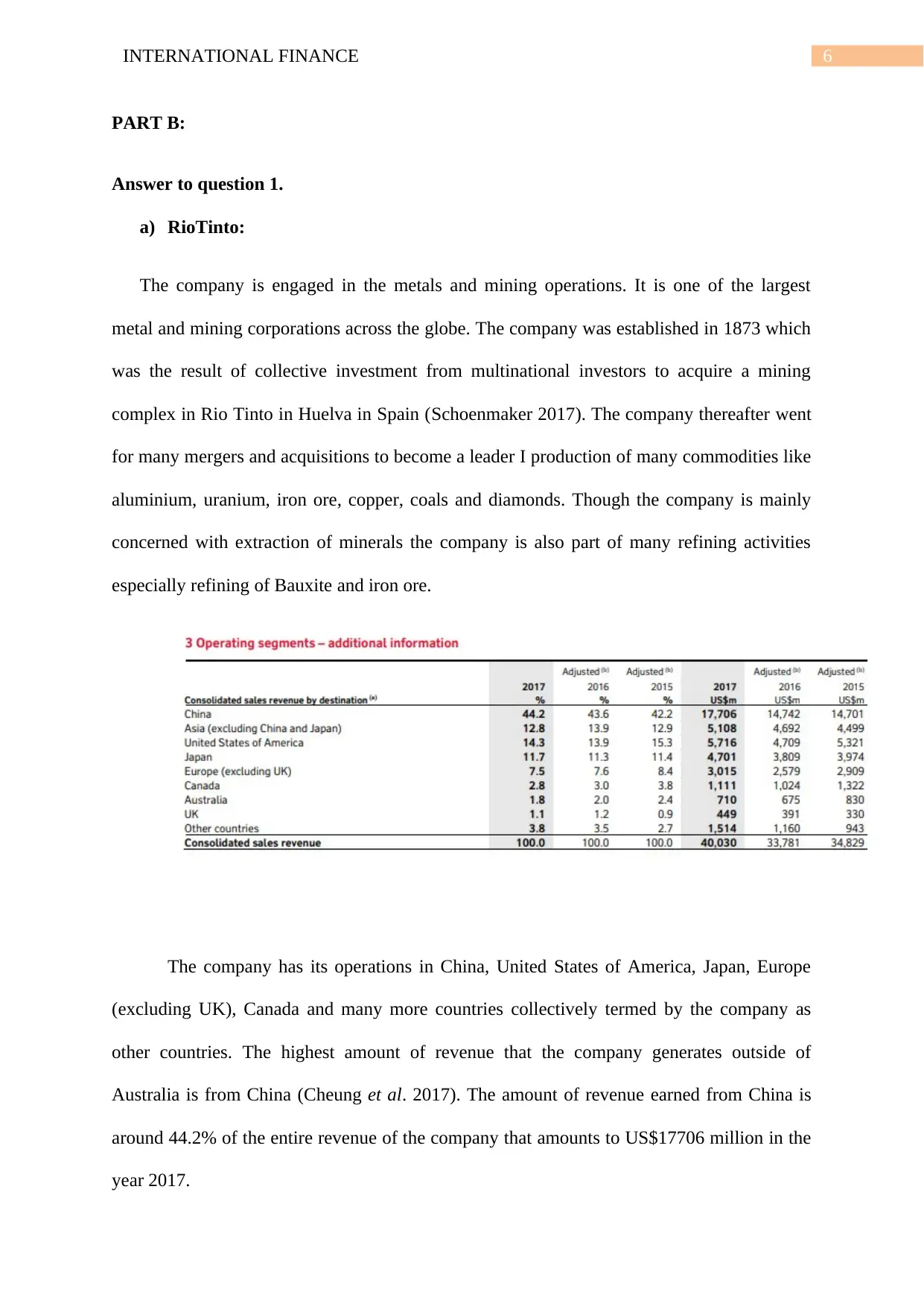

The company has its operations in China, United States of America, Japan, Europe

(excluding UK), Canada and many more countries collectively termed by the company as

other countries. The highest amount of revenue that the company generates outside of

Australia is from China (Cheung et al. 2017). The amount of revenue earned from China is

around 44.2% of the entire revenue of the company that amounts to US$17706 million in the

year 2017.

PART B:

Answer to question 1.

a) RioTinto:

The company is engaged in the metals and mining operations. It is one of the largest

metal and mining corporations across the globe. The company was established in 1873 which

was the result of collective investment from multinational investors to acquire a mining

complex in Rio Tinto in Huelva in Spain (Schoenmaker 2017). The company thereafter went

for many mergers and acquisitions to become a leader I production of many commodities like

aluminium, uranium, iron ore, copper, coals and diamonds. Though the company is mainly

concerned with extraction of minerals the company is also part of many refining activities

especially refining of Bauxite and iron ore.

The company has its operations in China, United States of America, Japan, Europe

(excluding UK), Canada and many more countries collectively termed by the company as

other countries. The highest amount of revenue that the company generates outside of

Australia is from China (Cheung et al. 2017). The amount of revenue earned from China is

around 44.2% of the entire revenue of the company that amounts to US$17706 million in the

year 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7INTERNATIONAL FINANCE

The main foreign exchange risk faced by the company is that the effects of many

different currencies of the countries in which it operates influence all its shareholders equity,

cash flows and earnings. The Canadian and Australian dollars are two most important

currencies influencing the costs of the company. In a given year the foreign exchange

fluctuations can have significant influence over the Rio Tinto’s financial results. The

strengthening of US Dollars against the currencies in which the group’s costs are partly

denominated is healthy for the group whereas the strengthening of the US Dollars reduces the

value of non US Dollars denominated currencies in which the group’s net assets are

denominated thereby reducing the total equity (Frisari and Stadelmann 2015).

In order to mitigate these risks the group reflects its financial performance in terms of US

Dollars as it is the most appropriate way to present the data of the company in a comparable

way. Borrowings and cash balances of the group are denominated in US Dollars while the

company holds the majority of debt and other financial assets and liabilities including

intragroup balances in the functional currency of its subsidiaries (Frieden and Lake 2015).

b) Brambles Limited:

The company is engaged in the operations of supply chain management and logistics. The

company specialises in accumulation of unit load equipment and ancillary services. The

company has concentrated its operations mainly in the field of outsourcing of pallets, crates

and containers (Kalaitzake 2017). The company is currently employing more than 14000

employees via 850 service centres across the globe.

The main foreign exchange risk faced by the company is that the effects of many

different currencies of the countries in which it operates influence all its shareholders equity,

cash flows and earnings. The Canadian and Australian dollars are two most important

currencies influencing the costs of the company. In a given year the foreign exchange

fluctuations can have significant influence over the Rio Tinto’s financial results. The

strengthening of US Dollars against the currencies in which the group’s costs are partly

denominated is healthy for the group whereas the strengthening of the US Dollars reduces the

value of non US Dollars denominated currencies in which the group’s net assets are

denominated thereby reducing the total equity (Frisari and Stadelmann 2015).

In order to mitigate these risks the group reflects its financial performance in terms of US

Dollars as it is the most appropriate way to present the data of the company in a comparable

way. Borrowings and cash balances of the group are denominated in US Dollars while the

company holds the majority of debt and other financial assets and liabilities including

intragroup balances in the functional currency of its subsidiaries (Frieden and Lake 2015).

b) Brambles Limited:

The company is engaged in the operations of supply chain management and logistics. The

company specialises in accumulation of unit load equipment and ancillary services. The

company has concentrated its operations mainly in the field of outsourcing of pallets, crates

and containers (Kalaitzake 2017). The company is currently employing more than 14000

employees via 850 service centres across the globe.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8INTERNATIONAL FINANCE

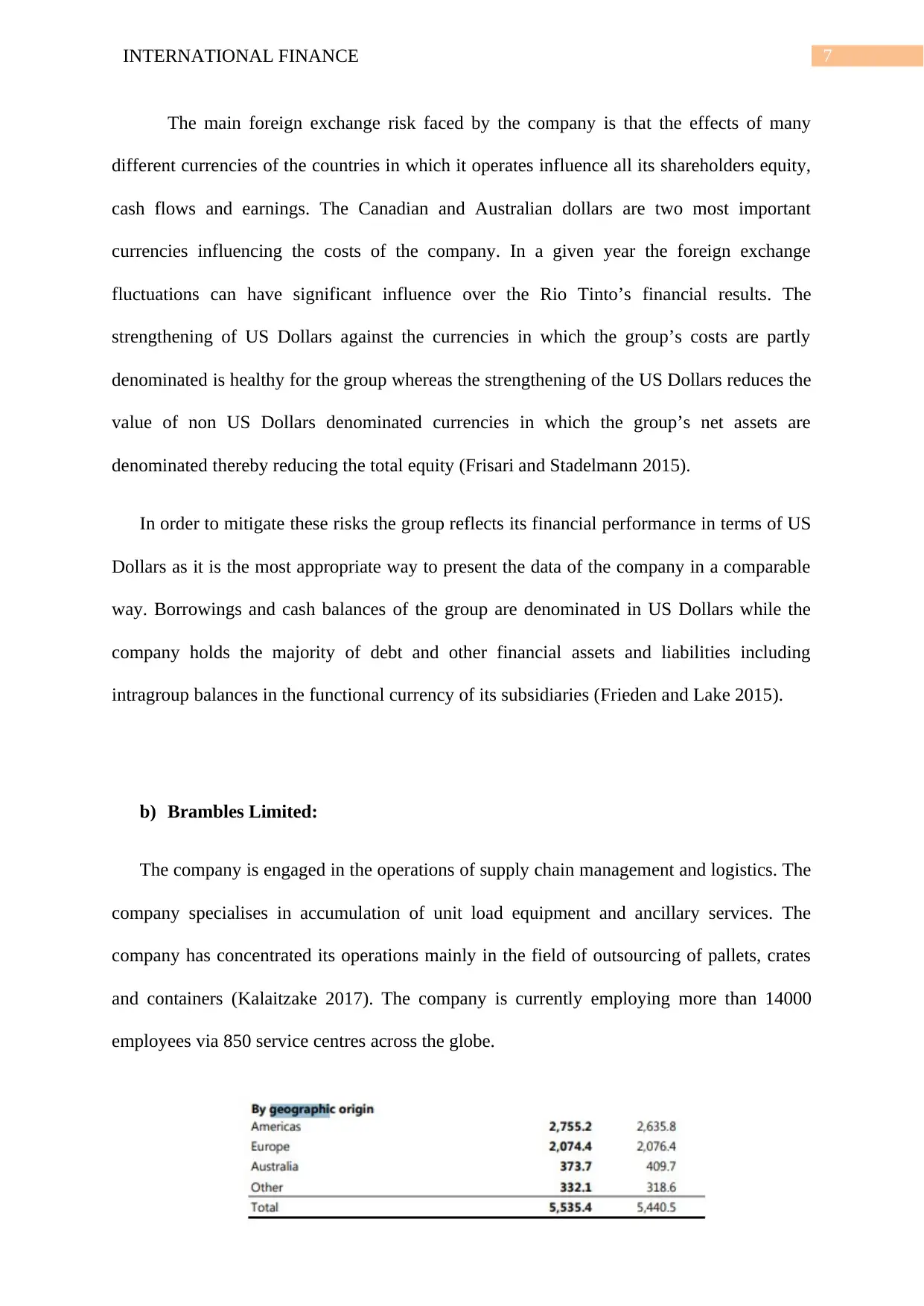

The operational arena of the company is wide ranging. It operates in America,

Europe, Australia and many other countries referred to by the company as others. The highest

revenue that is generated for the company except from Australia is from America. The

revenue from America amounts to US$2755 million in the year 2017. This suggest the

significance of America in respect of the revenue generated for the company as the revenue

generated from America is even more than that generated from Australia (McCauley and

Schenk 2015).

The foreign exchange risk of the company is constituted by the fluctuations or risk

involved in the translation of the transactions into the functional currencies of the various

subsidiaries of the company or translation of the value of the assets and liabilities of overseas

subsidiaries denominated in their respective currency into the functional currency of the

entire group. For the purposes of eradicating the risks foreign exchange hedging is used by

the company when the risks crosses certain thresholds. In addition to this forward foreign

exchange are entered into by the company to manage the exposures (Clarida 2015). The

company also incurs the expenses and incomes in the local currencies in order to contain the

exposures within certain limits. Further the translation risk exposure is eradicated by raising

debt in currencies where there is the presence of matching assets.

Answer to question 2.

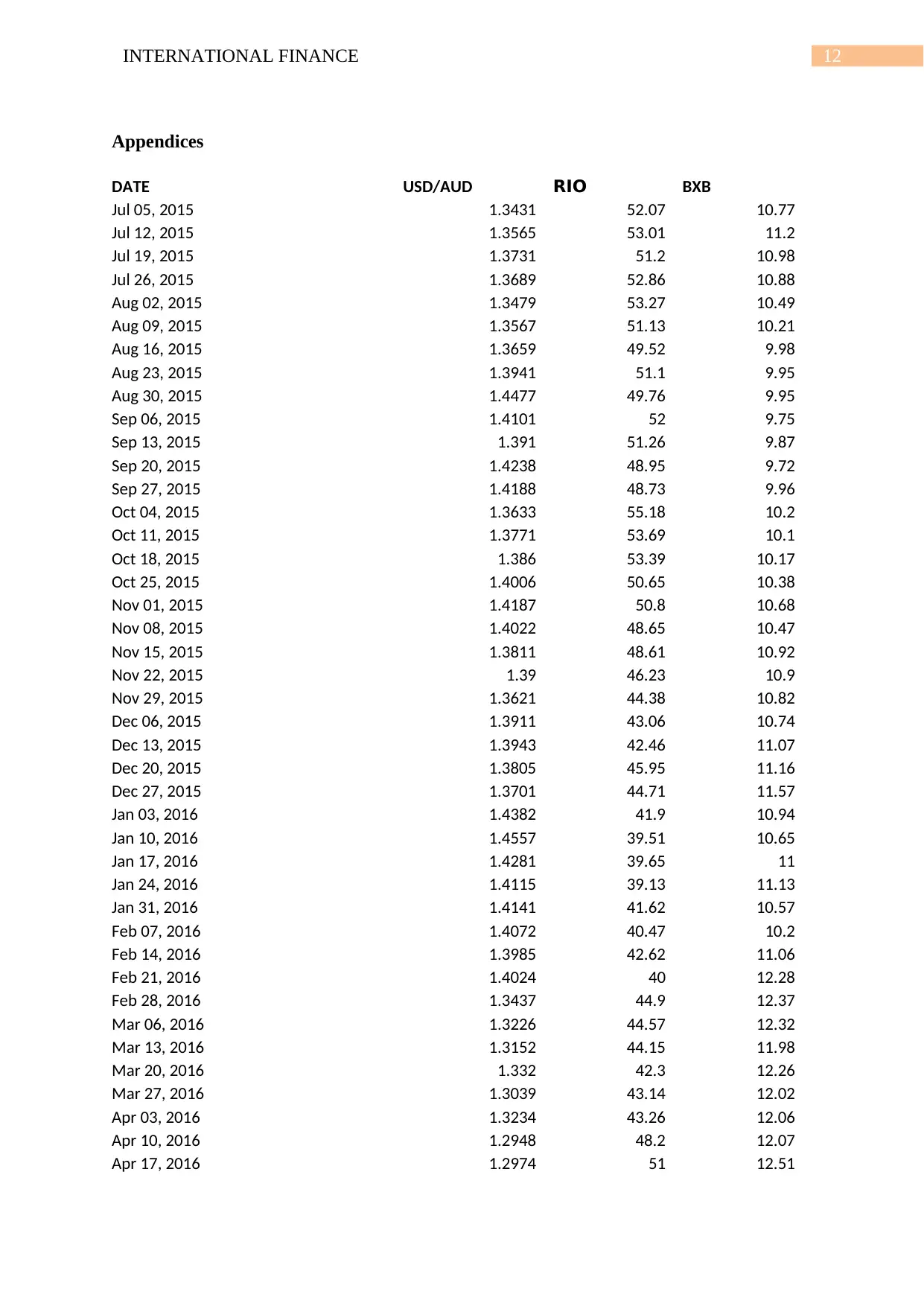

The correlation between the exchange rate of the USD/AUD, and the weekly share

prices of both the companies are provided in Appendices for last two years. On analysis, it

was found that both the company had a negative correlation with respect to the share price of

the companies and the exchange rates (Frankel 2015). This implies that if the exchange rates

go up the share prices of both the companies will go down and vice versa. Among the two

The operational arena of the company is wide ranging. It operates in America,

Europe, Australia and many other countries referred to by the company as others. The highest

revenue that is generated for the company except from Australia is from America. The

revenue from America amounts to US$2755 million in the year 2017. This suggest the

significance of America in respect of the revenue generated for the company as the revenue

generated from America is even more than that generated from Australia (McCauley and

Schenk 2015).

The foreign exchange risk of the company is constituted by the fluctuations or risk

involved in the translation of the transactions into the functional currencies of the various

subsidiaries of the company or translation of the value of the assets and liabilities of overseas

subsidiaries denominated in their respective currency into the functional currency of the

entire group. For the purposes of eradicating the risks foreign exchange hedging is used by

the company when the risks crosses certain thresholds. In addition to this forward foreign

exchange are entered into by the company to manage the exposures (Clarida 2015). The

company also incurs the expenses and incomes in the local currencies in order to contain the

exposures within certain limits. Further the translation risk exposure is eradicated by raising

debt in currencies where there is the presence of matching assets.

Answer to question 2.

The correlation between the exchange rate of the USD/AUD, and the weekly share

prices of both the companies are provided in Appendices for last two years. On analysis, it

was found that both the company had a negative correlation with respect to the share price of

the companies and the exchange rates (Frankel 2015). This implies that if the exchange rates

go up the share prices of both the companies will go down and vice versa. Among the two

9INTERNATIONAL FINANCE

companies RioTinto is more responsive to the changes in the exchange rates as compared to

Brambles Limited as the amount of correlation is greater in case of Rio Tinto.

Answer to question 3.

On analysis and comparison of the two companies, it can be seen that Brambles,

limited has no secondary listing on any stock exchange except Australian Stock Exchange

whereas Rio Tinto is listed on Australian Stock Exchange, New York Stock Exchange and

London Stock Exchange. Hence, the later has three listing that provides it with far more

liquidity than that of Bramble Limited in respect of arranging for funds (Medel et al. 2016).

In respect of Bramble Limited it is advised to get itself listed on another stock exchange like

the New York Stock Exchange as the company is earning heavy revenue from that country

which substantiates the strong presence of the company in the country. Getting listed on the

stock exchange will help the company to expand its operations in America by using the funds

from the shareholders belonging to the country. The customers will have more faith in the

operations of the company as it will be required to give many disclosures relevant to the

directions of the statute of the country. Increased amount of compliances and satisfaction of

those by the company will help the company to build up its goodwill even more (Clarke and

Boersma 2016). The listing will also help the company to diversify its risk with respect to the

various fluctuations experienced in the stock market. In case of instability in one of the

exchanges the other one can perform the hedging function for the company. But, along with

the advantages the company should also consider the costs that are involved like registration

cost, compliance cost, reports and disclosure costs.

companies RioTinto is more responsive to the changes in the exchange rates as compared to

Brambles Limited as the amount of correlation is greater in case of Rio Tinto.

Answer to question 3.

On analysis and comparison of the two companies, it can be seen that Brambles,

limited has no secondary listing on any stock exchange except Australian Stock Exchange

whereas Rio Tinto is listed on Australian Stock Exchange, New York Stock Exchange and

London Stock Exchange. Hence, the later has three listing that provides it with far more

liquidity than that of Bramble Limited in respect of arranging for funds (Medel et al. 2016).

In respect of Bramble Limited it is advised to get itself listed on another stock exchange like

the New York Stock Exchange as the company is earning heavy revenue from that country

which substantiates the strong presence of the company in the country. Getting listed on the

stock exchange will help the company to expand its operations in America by using the funds

from the shareholders belonging to the country. The customers will have more faith in the

operations of the company as it will be required to give many disclosures relevant to the

directions of the statute of the country. Increased amount of compliances and satisfaction of

those by the company will help the company to build up its goodwill even more (Clarke and

Boersma 2016). The listing will also help the company to diversify its risk with respect to the

various fluctuations experienced in the stock market. In case of instability in one of the

exchanges the other one can perform the hedging function for the company. But, along with

the advantages the company should also consider the costs that are involved like registration

cost, compliance cost, reports and disclosure costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10INTERNATIONAL FINANCE

Reference

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), pp.409-451.

Borio, C., Gambacorta, L. and Hofmann, B., 2017. The influence of monetary policy on bank

profitability. International Finance, 20(1), pp.48-63.

Cheung, Y.W., Chinn, M. and Nong, X., 2017. Estimating currency misalignment using the

Penn effect: It is not as simple as it looks. International Finance, 20(3), pp.222-242.

Clarida, R., 2015. The Fed is Ready to Raise Rates: Will Past be Prologue?. International

Finance, 18(1), pp.93-108.

Clarke, T. and Boersma, M., 2016. Sustainable finance? A critical analysis of the regulation,

policies, strategies, implementation and reporting on sustainability in international

finance. UNEP-Inquiry: Design of a Sustainable Financial System.

Frankel, J.A., 2015. International finance and macroeconomics. NBER Reporter, (2), pp.1-9.

Frieden, J.A. and Lake, D.A., 2015. World Politics: Interests, Interactions, Institutions: Third

International Student Edition. WW Norton & Company.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82, pp.12-

22.

Kalaitzake, M., 2017. The Political Power of Finance: The Institute of International Finance

in the Greek Debt Crisis. Politics & Society, 45(3), pp.389-413.

Reference

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), pp.409-451.

Borio, C., Gambacorta, L. and Hofmann, B., 2017. The influence of monetary policy on bank

profitability. International Finance, 20(1), pp.48-63.

Cheung, Y.W., Chinn, M. and Nong, X., 2017. Estimating currency misalignment using the

Penn effect: It is not as simple as it looks. International Finance, 20(3), pp.222-242.

Clarida, R., 2015. The Fed is Ready to Raise Rates: Will Past be Prologue?. International

Finance, 18(1), pp.93-108.

Clarke, T. and Boersma, M., 2016. Sustainable finance? A critical analysis of the regulation,

policies, strategies, implementation and reporting on sustainability in international

finance. UNEP-Inquiry: Design of a Sustainable Financial System.

Frankel, J.A., 2015. International finance and macroeconomics. NBER Reporter, (2), pp.1-9.

Frieden, J.A. and Lake, D.A., 2015. World Politics: Interests, Interactions, Institutions: Third

International Student Edition. WW Norton & Company.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82, pp.12-

22.

Kalaitzake, M., 2017. The Political Power of Finance: The Institute of International Finance

in the Greek Debt Crisis. Politics & Society, 45(3), pp.389-413.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11INTERNATIONAL FINANCE

McCauley, R.N. and Schenk, C.R., 2015. Reforming the International Monetary System in

the 1970s and 2000s: Would a Special Drawing Right Substitution Account Have

Worked?. International Finance, 18(2), pp.187-206.

Medel, C.A., Pedersen, M. and Pincheira, P.M., 2016. The elusive predictive ability of global

inflation. International Finance, 19(2), pp.120-146.

Schoenmaker, D., 2017. Resolution of international banks: Can smaller countries

cope?. International Finance.

McCauley, R.N. and Schenk, C.R., 2015. Reforming the International Monetary System in

the 1970s and 2000s: Would a Special Drawing Right Substitution Account Have

Worked?. International Finance, 18(2), pp.187-206.

Medel, C.A., Pedersen, M. and Pincheira, P.M., 2016. The elusive predictive ability of global

inflation. International Finance, 19(2), pp.120-146.

Schoenmaker, D., 2017. Resolution of international banks: Can smaller countries

cope?. International Finance.

12INTERNATIONAL FINANCE

Appendices

DATE USD/AUD RIO BXB

Jul 05, 2015 1.3431 52.07 10.77

Jul 12, 2015 1.3565 53.01 11.2

Jul 19, 2015 1.3731 51.2 10.98

Jul 26, 2015 1.3689 52.86 10.88

Aug 02, 2015 1.3479 53.27 10.49

Aug 09, 2015 1.3567 51.13 10.21

Aug 16, 2015 1.3659 49.52 9.98

Aug 23, 2015 1.3941 51.1 9.95

Aug 30, 2015 1.4477 49.76 9.95

Sep 06, 2015 1.4101 52 9.75

Sep 13, 2015 1.391 51.26 9.87

Sep 20, 2015 1.4238 48.95 9.72

Sep 27, 2015 1.4188 48.73 9.96

Oct 04, 2015 1.3633 55.18 10.2

Oct 11, 2015 1.3771 53.69 10.1

Oct 18, 2015 1.386 53.39 10.17

Oct 25, 2015 1.4006 50.65 10.38

Nov 01, 2015 1.4187 50.8 10.68

Nov 08, 2015 1.4022 48.65 10.47

Nov 15, 2015 1.3811 48.61 10.92

Nov 22, 2015 1.39 46.23 10.9

Nov 29, 2015 1.3621 44.38 10.82

Dec 06, 2015 1.3911 43.06 10.74

Dec 13, 2015 1.3943 42.46 11.07

Dec 20, 2015 1.3805 45.95 11.16

Dec 27, 2015 1.3701 44.71 11.57

Jan 03, 2016 1.4382 41.9 10.94

Jan 10, 2016 1.4557 39.51 10.65

Jan 17, 2016 1.4281 39.65 11

Jan 24, 2016 1.4115 39.13 11.13

Jan 31, 2016 1.4141 41.62 10.57

Feb 07, 2016 1.4072 40.47 10.2

Feb 14, 2016 1.3985 42.62 11.06

Feb 21, 2016 1.4024 40 12.28

Feb 28, 2016 1.3437 44.9 12.37

Mar 06, 2016 1.3226 44.57 12.32

Mar 13, 2016 1.3152 44.15 11.98

Mar 20, 2016 1.332 42.3 12.26

Mar 27, 2016 1.3039 43.14 12.02

Apr 03, 2016 1.3234 43.26 12.06

Apr 10, 2016 1.2948 48.2 12.07

Apr 17, 2016 1.2974 51 12.51

Appendices

DATE USD/AUD RIO BXB

Jul 05, 2015 1.3431 52.07 10.77

Jul 12, 2015 1.3565 53.01 11.2

Jul 19, 2015 1.3731 51.2 10.98

Jul 26, 2015 1.3689 52.86 10.88

Aug 02, 2015 1.3479 53.27 10.49

Aug 09, 2015 1.3567 51.13 10.21

Aug 16, 2015 1.3659 49.52 9.98

Aug 23, 2015 1.3941 51.1 9.95

Aug 30, 2015 1.4477 49.76 9.95

Sep 06, 2015 1.4101 52 9.75

Sep 13, 2015 1.391 51.26 9.87

Sep 20, 2015 1.4238 48.95 9.72

Sep 27, 2015 1.4188 48.73 9.96

Oct 04, 2015 1.3633 55.18 10.2

Oct 11, 2015 1.3771 53.69 10.1

Oct 18, 2015 1.386 53.39 10.17

Oct 25, 2015 1.4006 50.65 10.38

Nov 01, 2015 1.4187 50.8 10.68

Nov 08, 2015 1.4022 48.65 10.47

Nov 15, 2015 1.3811 48.61 10.92

Nov 22, 2015 1.39 46.23 10.9

Nov 29, 2015 1.3621 44.38 10.82

Dec 06, 2015 1.3911 43.06 10.74

Dec 13, 2015 1.3943 42.46 11.07

Dec 20, 2015 1.3805 45.95 11.16

Dec 27, 2015 1.3701 44.71 11.57

Jan 03, 2016 1.4382 41.9 10.94

Jan 10, 2016 1.4557 39.51 10.65

Jan 17, 2016 1.4281 39.65 11

Jan 24, 2016 1.4115 39.13 11.13

Jan 31, 2016 1.4141 41.62 10.57

Feb 07, 2016 1.4072 40.47 10.2

Feb 14, 2016 1.3985 42.62 11.06

Feb 21, 2016 1.4024 40 12.28

Feb 28, 2016 1.3437 44.9 12.37

Mar 06, 2016 1.3226 44.57 12.32

Mar 13, 2016 1.3152 44.15 11.98

Mar 20, 2016 1.332 42.3 12.26

Mar 27, 2016 1.3039 43.14 12.02

Apr 03, 2016 1.3234 43.26 12.06

Apr 10, 2016 1.2948 48.2 12.07

Apr 17, 2016 1.2974 51 12.51

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.