Financial Report: Analysis of Ding Dong Plc for Investment Purposes

VerifiedAdded on 2022/12/22

|13

|3731

|1

Report

AI Summary

This report provides a comprehensive analysis of financial statements and ratios to evaluate investment opportunities, focusing on Ding Dong Plc and comparing Lockup Ltd and Secure Ltd. The analysis includes profitability, liquidity, solvency, and efficiency ratios, offering insights into each company's financial health. The report recommends investment strategies based on the ratio analysis, highlighting the importance of factors like dividend yield and capital structure. Furthermore, the report delves into International Accounting Standard (IAS) 38, discussing its significance in accounting for intangible assets, particularly in the context of Research and Development (R&D) expenditures. The report provides a detailed understanding of the application of IAS 38 and its implications for financial reporting and decision-making, providing a financial analyst's perspective on the investment potential of Ding Dong Plc.

INTERNATIONAL FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1 Recommending suitable firm top Ding Dong Plc for the investment purpose

through using ratio analysis.........................................................................................................1

Question 2 Critically evaluating the main contents of International Accounting Standards

which covers R&D......................................................................................................................5

Question 3....................................................................................................................................7

a. Income statement.....................................................................................................................7

b. Notes to income statement.......................................................................................................8

c. Statement of financial position................................................................................................9

d. Notes for Statement of Financial Position.............................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Question 1 Recommending suitable firm top Ding Dong Plc for the investment purpose

through using ratio analysis.........................................................................................................1

Question 2 Critically evaluating the main contents of International Accounting Standards

which covers R&D......................................................................................................................5

Question 3....................................................................................................................................7

a. Income statement.....................................................................................................................7

b. Notes to income statement.......................................................................................................8

c. Statement of financial position................................................................................................9

d. Notes for Statement of Financial Position.............................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

International financial reporting may be defined as framework which lays focus on drafting

financial statements which contains characteristics of consistency, transparency and

comparability. In the current times, business units make focus on presenting highly reliable

information to the stakeholders with the motive to influence their decision making. The present

report is based on different case scenario which will provide deeper insight about firm which

prove to beneficial from investment purpose. It will depict how ratio analysis tool can be used

for assessing the extent to which one organization is better than other referring ratio analysis

tool. Further, it will also develop understanding about IAS 38 and its importance in relation to

recording transactions pertaining to R&D.

Question 1 Recommending suitable firm top Ding Dong Plc for the investment purpose through

using ratio analysis

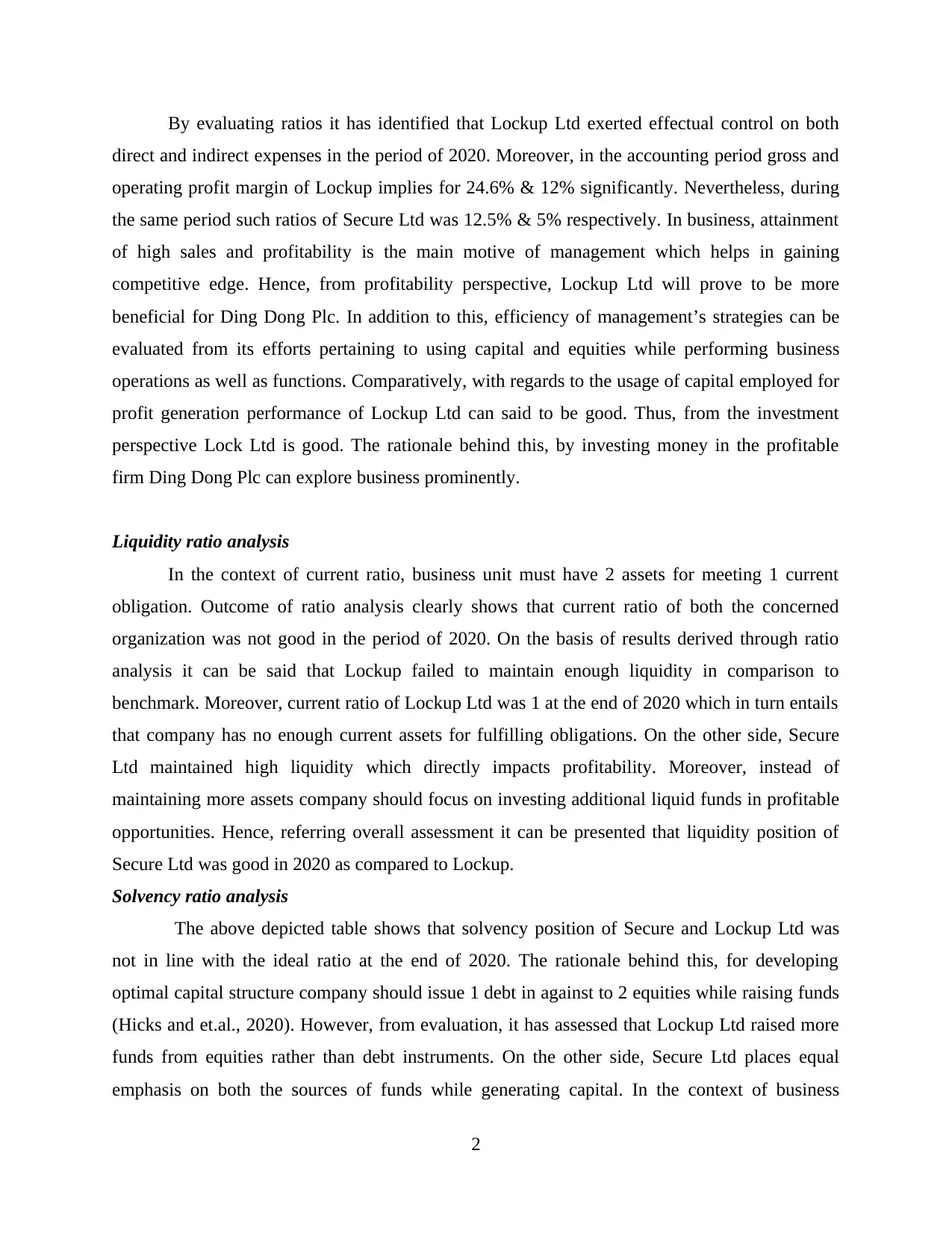

On the basis of cited case scenario, Ding Dong Plc is planning to expand business

operations. In this regard, business unit have two options for investment such as Lockup and

Secure Ltd. Hence, for assessing the attractiveness of investment opportunities ratio analysis tool

has been applied. Ratio analysis may be presented as a quantitative tool which enables investor

to evaluate business performance from several perspectives such as profitability, liquidity,

solvency and efficiency (Hamilton and et.al., 2021).

Ratio Lockup Ltd Secure Ltd

Current ratio 1.0 5.0

Acid-test ratio 0.75 1.0

Accounts receivable days 40 30

Inventory turnover (times) 6.0 12.80

Accounts payable days 70 30

Percent of total debt to total assets 40% 80%

Gross profit percentage 24.6% 12.5%

Operating profit percentage 12% 5%

Return on capital employed 16% 4%

Return on equity 11% 11%

Gearing 20% 90%

Interest cover (times) 2 5

Dividends in pence 7.20 1.20

Profitability ratio analysis

1

International financial reporting may be defined as framework which lays focus on drafting

financial statements which contains characteristics of consistency, transparency and

comparability. In the current times, business units make focus on presenting highly reliable

information to the stakeholders with the motive to influence their decision making. The present

report is based on different case scenario which will provide deeper insight about firm which

prove to beneficial from investment purpose. It will depict how ratio analysis tool can be used

for assessing the extent to which one organization is better than other referring ratio analysis

tool. Further, it will also develop understanding about IAS 38 and its importance in relation to

recording transactions pertaining to R&D.

Question 1 Recommending suitable firm top Ding Dong Plc for the investment purpose through

using ratio analysis

On the basis of cited case scenario, Ding Dong Plc is planning to expand business

operations. In this regard, business unit have two options for investment such as Lockup and

Secure Ltd. Hence, for assessing the attractiveness of investment opportunities ratio analysis tool

has been applied. Ratio analysis may be presented as a quantitative tool which enables investor

to evaluate business performance from several perspectives such as profitability, liquidity,

solvency and efficiency (Hamilton and et.al., 2021).

Ratio Lockup Ltd Secure Ltd

Current ratio 1.0 5.0

Acid-test ratio 0.75 1.0

Accounts receivable days 40 30

Inventory turnover (times) 6.0 12.80

Accounts payable days 70 30

Percent of total debt to total assets 40% 80%

Gross profit percentage 24.6% 12.5%

Operating profit percentage 12% 5%

Return on capital employed 16% 4%

Return on equity 11% 11%

Gearing 20% 90%

Interest cover (times) 2 5

Dividends in pence 7.20 1.20

Profitability ratio analysis

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By evaluating ratios it has identified that Lockup Ltd exerted effectual control on both

direct and indirect expenses in the period of 2020. Moreover, in the accounting period gross and

operating profit margin of Lockup implies for 24.6% & 12% significantly. Nevertheless, during

the same period such ratios of Secure Ltd was 12.5% & 5% respectively. In business, attainment

of high sales and profitability is the main motive of management which helps in gaining

competitive edge. Hence, from profitability perspective, Lockup Ltd will prove to be more

beneficial for Ding Dong Plc. In addition to this, efficiency of management’s strategies can be

evaluated from its efforts pertaining to using capital and equities while performing business

operations as well as functions. Comparatively, with regards to the usage of capital employed for

profit generation performance of Lockup Ltd can said to be good. Thus, from the investment

perspective Lock Ltd is good. The rationale behind this, by investing money in the profitable

firm Ding Dong Plc can explore business prominently.

Liquidity ratio analysis

In the context of current ratio, business unit must have 2 assets for meeting 1 current

obligation. Outcome of ratio analysis clearly shows that current ratio of both the concerned

organization was not good in the period of 2020. On the basis of results derived through ratio

analysis it can be said that Lockup failed to maintain enough liquidity in comparison to

benchmark. Moreover, current ratio of Lockup Ltd was 1 at the end of 2020 which in turn entails

that company has no enough current assets for fulfilling obligations. On the other side, Secure

Ltd maintained high liquidity which directly impacts profitability. Moreover, instead of

maintaining more assets company should focus on investing additional liquid funds in profitable

opportunities. Hence, referring overall assessment it can be presented that liquidity position of

Secure Ltd was good in 2020 as compared to Lockup.

Solvency ratio analysis

The above depicted table shows that solvency position of Secure and Lockup Ltd was

not in line with the ideal ratio at the end of 2020. The rationale behind this, for developing

optimal capital structure company should issue 1 debt in against to 2 equities while raising funds

(Hicks and et.al., 2020). However, from evaluation, it has assessed that Lockup Ltd raised more

funds from equities rather than debt instruments. On the other side, Secure Ltd places equal

emphasis on both the sources of funds while generating capital. In the context of business

2

direct and indirect expenses in the period of 2020. Moreover, in the accounting period gross and

operating profit margin of Lockup implies for 24.6% & 12% significantly. Nevertheless, during

the same period such ratios of Secure Ltd was 12.5% & 5% respectively. In business, attainment

of high sales and profitability is the main motive of management which helps in gaining

competitive edge. Hence, from profitability perspective, Lockup Ltd will prove to be more

beneficial for Ding Dong Plc. In addition to this, efficiency of management’s strategies can be

evaluated from its efforts pertaining to using capital and equities while performing business

operations as well as functions. Comparatively, with regards to the usage of capital employed for

profit generation performance of Lockup Ltd can said to be good. Thus, from the investment

perspective Lock Ltd is good. The rationale behind this, by investing money in the profitable

firm Ding Dong Plc can explore business prominently.

Liquidity ratio analysis

In the context of current ratio, business unit must have 2 assets for meeting 1 current

obligation. Outcome of ratio analysis clearly shows that current ratio of both the concerned

organization was not good in the period of 2020. On the basis of results derived through ratio

analysis it can be said that Lockup failed to maintain enough liquidity in comparison to

benchmark. Moreover, current ratio of Lockup Ltd was 1 at the end of 2020 which in turn entails

that company has no enough current assets for fulfilling obligations. On the other side, Secure

Ltd maintained high liquidity which directly impacts profitability. Moreover, instead of

maintaining more assets company should focus on investing additional liquid funds in profitable

opportunities. Hence, referring overall assessment it can be presented that liquidity position of

Secure Ltd was good in 2020 as compared to Lockup.

Solvency ratio analysis

The above depicted table shows that solvency position of Secure and Lockup Ltd was

not in line with the ideal ratio at the end of 2020. The rationale behind this, for developing

optimal capital structure company should issue 1 debt in against to 2 equities while raising funds

(Hicks and et.al., 2020). However, from evaluation, it has assessed that Lockup Ltd raised more

funds from equities rather than debt instruments. On the other side, Secure Ltd places equal

emphasis on both the sources of funds while generating capital. In the context of business

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization, inclusion of more debt within capital structure places direct impact on profitability

aspect. Moreover, in debt, firm has accountability to make interest payment irrespective of aspect

whether profit generated during the concerned period or not. Further, high level of equities also

impose issue in relation to shareholders interruption in decision making. By keeping in mind all

such aspects it can be entailed that solvency Lockup maintained suitable capital structure over

others.

Efficiency ratio analysis

In this, with regards to accounts receivable ratio, Lockup Ltd getting funds from debtors

within 40 days. On the contrary to this, debtor’s turnover ratio of Secure Ltd was 30 days at the

end of 2020. It shows that Lockup Ltd is receiving payments from debtors later in comparison to

Secure. This in turn places direct impact on working capital aspects and thereby day to day

operations as well. However, in order to deal with and maintain effectual working capital Lockup

emphasized on getting credit extension from suppliers. As per accounts payable period, Lockup

Ltd made payment to creditors in 70 days. Whereas, Secure Ltd failed to get more credit period

from supplier’s side. In the case of having high payable days company have opportunity to invest

funds in other opportunities and thereby attain profit. On the basis of overall evaluation, it can be

said that working capital management of Lockup Ltd was prominent.

Inventory turnover ratio exhibits company’s ability in relation to selling and replacing its

inventory level. In 2020, stock turnover ratio of Lockup Ltd was 6 times, whereas 12.80 times of

Secure Ltd. Hence, outcome presents that Secure Ltd managed its inventory more efficiently

within the concerned year. Nevertheless, Lockup Ltd failed to sell its stock within the pre-

determined time period. In other words, during 2020, Lockup Ltd hold its stock for longer period

which in turn directly affects cash aspect. Lower inventory turnover ratio shows company’s

inability in relation to converting finished goods into cash. However, by taking into account

competent measures and strategic framework Lockup Ltd can improve its stock management,

sales & profitability as well.

Along with this, interest coverage ratio reflects that, in accounting period 2020, Secure

Ltd was highly capable for meeting current interest payments from available earnings. In

comparison to Secure ltd, Lockup can meet its interest payment only 2 times from the profit

generated during 2020. However, as per the standards, company’s position can said to be good

when it has minimum 2times interest coverage ratio. Accordingly, both the companies are in

3

aspect. Moreover, in debt, firm has accountability to make interest payment irrespective of aspect

whether profit generated during the concerned period or not. Further, high level of equities also

impose issue in relation to shareholders interruption in decision making. By keeping in mind all

such aspects it can be entailed that solvency Lockup maintained suitable capital structure over

others.

Efficiency ratio analysis

In this, with regards to accounts receivable ratio, Lockup Ltd getting funds from debtors

within 40 days. On the contrary to this, debtor’s turnover ratio of Secure Ltd was 30 days at the

end of 2020. It shows that Lockup Ltd is receiving payments from debtors later in comparison to

Secure. This in turn places direct impact on working capital aspects and thereby day to day

operations as well. However, in order to deal with and maintain effectual working capital Lockup

emphasized on getting credit extension from suppliers. As per accounts payable period, Lockup

Ltd made payment to creditors in 70 days. Whereas, Secure Ltd failed to get more credit period

from supplier’s side. In the case of having high payable days company have opportunity to invest

funds in other opportunities and thereby attain profit. On the basis of overall evaluation, it can be

said that working capital management of Lockup Ltd was prominent.

Inventory turnover ratio exhibits company’s ability in relation to selling and replacing its

inventory level. In 2020, stock turnover ratio of Lockup Ltd was 6 times, whereas 12.80 times of

Secure Ltd. Hence, outcome presents that Secure Ltd managed its inventory more efficiently

within the concerned year. Nevertheless, Lockup Ltd failed to sell its stock within the pre-

determined time period. In other words, during 2020, Lockup Ltd hold its stock for longer period

which in turn directly affects cash aspect. Lower inventory turnover ratio shows company’s

inability in relation to converting finished goods into cash. However, by taking into account

competent measures and strategic framework Lockup Ltd can improve its stock management,

sales & profitability as well.

Along with this, interest coverage ratio reflects that, in accounting period 2020, Secure

Ltd was highly capable for meeting current interest payments from available earnings. In

comparison to Secure ltd, Lockup can meet its interest payment only 2 times from the profit

generated during 2020. However, as per the standards, company’s position can said to be good

when it has minimum 2times interest coverage ratio. Accordingly, both the companies are in

3

good position to fulfil their obligations.

Investment ratios

Dividend is recognized as one of the main factors which helps in attracting and

maintaining the faith of shareholders in business operations. Nevertheless, dividend decision is

highly affected from the profit generated by the firm within financial year. In 2020, dividend

offered by Lockup and Secure accounts for 7.20 & 1.20 pence significantly. Thus, from

shareholders perspective, financial performance of Lockup was good.

To,

Ding Dong Plc

Date: 28th March 2020

From analysis it is reported to the higher management team that financial position and

performance of Lockup Ltd recognized as good. Through assessment, it has found that Lockup

Ltd generated higher profit margin, in 2020, over expenses incurred. Along with this, ability of

Lockup in relation to meeting current obligations from assets is good. As, company is able to

covert its assets into cash for fulfilling liabilities. Further, in comparison to Secure Ltd, capital

structure made by Lockup was good. Along with this, efficiency of Lockup Ltd in relation to

making use of both current and non-current assets can said to be better over Secure Ltd.

Considering overall assessment management of Ding Dong Plc is advised to invest in Lockup

Ltd. Moreover, financial performance of Lockup Ltd was sound in the category of profitability,

liquidity, solvency etc. As per the current performance, Ding Dong Plc can raise funds through

equity in the near future by investing in Lockup Ltd. Moreover, current company is offering high

and suitable dividend to the shareholders. Thus, this aspect will help investors in attracting more

investors. From overall perspective, investment in Lockup Ltd will contribute in the attainment

of Ding Dong Plc’s goals and objectives. Hence, higher management team of Ding Dong Plc is

advised to make focus on employing social media marketing tool. By this, firm can enhance its

reach at global level and entice decision making of customers. Meanwhile, it results into the

maximization of both sales and profitability. In addition to this, after investment, management

team of Ding Dong Plc should make focus on maintaining enough current assets so that liquidity

position can be improved. Besides this, before investment, Ding Dong Plc should also lay focus

on evaluating company’s culture, employee base and other external factors that impacts

4

Investment ratios

Dividend is recognized as one of the main factors which helps in attracting and

maintaining the faith of shareholders in business operations. Nevertheless, dividend decision is

highly affected from the profit generated by the firm within financial year. In 2020, dividend

offered by Lockup and Secure accounts for 7.20 & 1.20 pence significantly. Thus, from

shareholders perspective, financial performance of Lockup was good.

To,

Ding Dong Plc

Date: 28th March 2020

From analysis it is reported to the higher management team that financial position and

performance of Lockup Ltd recognized as good. Through assessment, it has found that Lockup

Ltd generated higher profit margin, in 2020, over expenses incurred. Along with this, ability of

Lockup in relation to meeting current obligations from assets is good. As, company is able to

covert its assets into cash for fulfilling liabilities. Further, in comparison to Secure Ltd, capital

structure made by Lockup was good. Along with this, efficiency of Lockup Ltd in relation to

making use of both current and non-current assets can said to be better over Secure Ltd.

Considering overall assessment management of Ding Dong Plc is advised to invest in Lockup

Ltd. Moreover, financial performance of Lockup Ltd was sound in the category of profitability,

liquidity, solvency etc. As per the current performance, Ding Dong Plc can raise funds through

equity in the near future by investing in Lockup Ltd. Moreover, current company is offering high

and suitable dividend to the shareholders. Thus, this aspect will help investors in attracting more

investors. From overall perspective, investment in Lockup Ltd will contribute in the attainment

of Ding Dong Plc’s goals and objectives. Hence, higher management team of Ding Dong Plc is

advised to make focus on employing social media marketing tool. By this, firm can enhance its

reach at global level and entice decision making of customers. Meanwhile, it results into the

maximization of both sales and profitability. In addition to this, after investment, management

team of Ding Dong Plc should make focus on maintaining enough current assets so that liquidity

position can be improved. Besides this, before investment, Ding Dong Plc should also lay focus

on evaluating company’s culture, employee base and other external factors that impacts

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations. Hence, by developing sound strategic and policy framework Ding Dong Plc can get

success through making investment in Lockup Ltd.

Sincerely

Financial analyst

Question 2 Critically evaluating the main contents of International Accounting Standards which

covers R&D

The pandemic has impacted businesses adversely in many ways. There are various

organization that has been shut down due to these crises. With respect to this, firms has requested

government to innovate such vaccines and equipment that can save them from not being wind up

and gain sustainability for longer duration.

IAS-38 highlights the accounting requirements for intangible assets. The Research and

development is an essential part of IAS which plays critical part in obtaining success regarding

its operations related to R & D (Agyei-Mensah, 2019). Its main objective is to identify

requirements that are measuring carrying amount of intangible assets of organizations. The

standard also aims to identify the characteristics of non-physical assets. In this crisis R&D

worked would be identified that can be sold, leased, etc. for utilization of world.

It is applied to all types of Intangible assets (IA) but excludes some special cases. It

excludes financial & insurance company non-physical assets, development, extraction &

evaluation of minerals, tools held for rent, sales, etc. The type of transactions that company can

acquire for receiving assets are exchange of assets, government grand, distinct purchase and

many more. In prior time it was difficult for business to distinct cost and other elements related

with IA (IAS 38 Intangible Assets, 2017). With respect to this, international accounting standard

has formulated the concept of intangible assets for acquiring clarity and understanding regarding

recording norms and conditions related with it. In business combination quality is improved &

international coverage can be given on this aspect.

IAS-38 has mentioned 6 conditions for this particular intangible assets. It comprises

technical feasibility for use, intention to complete, ability to sell, availability of resources for

completion, optimization of future benefits related to economy and reliable measurement of

5

success through making investment in Lockup Ltd.

Sincerely

Financial analyst

Question 2 Critically evaluating the main contents of International Accounting Standards which

covers R&D

The pandemic has impacted businesses adversely in many ways. There are various

organization that has been shut down due to these crises. With respect to this, firms has requested

government to innovate such vaccines and equipment that can save them from not being wind up

and gain sustainability for longer duration.

IAS-38 highlights the accounting requirements for intangible assets. The Research and

development is an essential part of IAS which plays critical part in obtaining success regarding

its operations related to R & D (Agyei-Mensah, 2019). Its main objective is to identify

requirements that are measuring carrying amount of intangible assets of organizations. The

standard also aims to identify the characteristics of non-physical assets. In this crisis R&D

worked would be identified that can be sold, leased, etc. for utilization of world.

It is applied to all types of Intangible assets (IA) but excludes some special cases. It

excludes financial & insurance company non-physical assets, development, extraction &

evaluation of minerals, tools held for rent, sales, etc. The type of transactions that company can

acquire for receiving assets are exchange of assets, government grand, distinct purchase and

many more. In prior time it was difficult for business to distinct cost and other elements related

with IA (IAS 38 Intangible Assets, 2017). With respect to this, international accounting standard

has formulated the concept of intangible assets for acquiring clarity and understanding regarding

recording norms and conditions related with it. In business combination quality is improved &

international coverage can be given on this aspect.

IAS-38 has mentioned 6 conditions for this particular intangible assets. It comprises

technical feasibility for use, intention to complete, ability to sell, availability of resources for

completion, optimization of future benefits related to economy and reliable measurement of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditures. In addition to this, reporting entry should be recognizable from the view point of

this 6 factors (Elsten and Hill, 2017). Expenditures that are related with development are not

coordinated expensed off. It does not allow to capitalize those items that are not matched with

conditions. It as well has two approaches such as revaluation model & the cost method. It has

stated that revaluation approach can be used only in case of licence that are non-passively

transacted. In addition to this, the basic objective of it is to recognise & measure non-physical

assets and getting information regarding disclosure.

Earlier, emphasis was placed on recognizing R&D as asset which separated from

goodwill. However, treatment pertaining to R&D as per IAS 38 was unclear and lacks

standardization in process. Hence, in order to improve reporting aspects and for making the

treatment of R&D more responsive several new aspects were introduced. Accordingly, R&D

must be recognized as expense when it is a kind of expenses (IAS 38 Intangible Assets, 2021).

Unlike this, cost incurred pertaining to development is recorded as an assets as per IAS 38. In

aspect to this, IAS-38 has expected organization to disclose all expenditures that are connected

with research and development which was expensed off priorly neglected. It has also been

mentioned in act to render valuable data disconnected balance sheet assets. Further, it supports

the non-disclosure for gaining competitive advantages.

It has been revised for due to some lacking area. One of the biggest modifications require

for the improvement is related with its ability of working. With respect to this, it was prior used

to recognize the IA but identified aspects were not mentioned. The fair value of IA is assessed

through sufficient reliability to be recognized separately from goodwill. This standard uses the

judgements for determining that which element is more significant for considering tangible and

intangible assets under sections. For example- IAS- 38 mainly includes computer software,

patents, customer & supplier relations, market share with rights, mortgage servicing rights,

franchises, fishing licence, import quotas, etc. There are several future economic benefits which

allows business combination to attain in order to comply with rules and regulations formulated.

It provides legal rights that give advantages while dealing with IA. It encourages firm to derive

this benefits by adhering norms and conditioned mentioned under the act.

The current rules are inappropriate for better accounting of cost. It is not clear and

specific of what to include and which elements that can be excluded. This makes balance sheet

6

this 6 factors (Elsten and Hill, 2017). Expenditures that are related with development are not

coordinated expensed off. It does not allow to capitalize those items that are not matched with

conditions. It as well has two approaches such as revaluation model & the cost method. It has

stated that revaluation approach can be used only in case of licence that are non-passively

transacted. In addition to this, the basic objective of it is to recognise & measure non-physical

assets and getting information regarding disclosure.

Earlier, emphasis was placed on recognizing R&D as asset which separated from

goodwill. However, treatment pertaining to R&D as per IAS 38 was unclear and lacks

standardization in process. Hence, in order to improve reporting aspects and for making the

treatment of R&D more responsive several new aspects were introduced. Accordingly, R&D

must be recognized as expense when it is a kind of expenses (IAS 38 Intangible Assets, 2021).

Unlike this, cost incurred pertaining to development is recorded as an assets as per IAS 38. In

aspect to this, IAS-38 has expected organization to disclose all expenditures that are connected

with research and development which was expensed off priorly neglected. It has also been

mentioned in act to render valuable data disconnected balance sheet assets. Further, it supports

the non-disclosure for gaining competitive advantages.

It has been revised for due to some lacking area. One of the biggest modifications require

for the improvement is related with its ability of working. With respect to this, it was prior used

to recognize the IA but identified aspects were not mentioned. The fair value of IA is assessed

through sufficient reliability to be recognized separately from goodwill. This standard uses the

judgements for determining that which element is more significant for considering tangible and

intangible assets under sections. For example- IAS- 38 mainly includes computer software,

patents, customer & supplier relations, market share with rights, mortgage servicing rights,

franchises, fishing licence, import quotas, etc. There are several future economic benefits which

allows business combination to attain in order to comply with rules and regulations formulated.

It provides legal rights that give advantages while dealing with IA. It encourages firm to derive

this benefits by adhering norms and conditioned mentioned under the act.

The current rules are inappropriate for better accounting of cost. It is not clear and

specific of what to include and which elements that can be excluded. This makes balance sheet

6

improper from international standards covering research and development (Dinh, Schultze, List

and Zbiegly, 2020). It requires three approaches that involves expensing research and

development values, selective capitalization, etc. in addition to this, it does not focuses on

important factor of institutions in turn they get risk of losing part of their net worth because of

not getting rid of assets from financial statements (Ertuğrul, 2020). The most advisable

recommendation can be allowing organization to utilize their usable approach from the

beginning. Tendencies to make balance in appropriate by involving intangible assets that

company is performing good so that shareholders can be attracted for investing. Defining these

assets differently under methods so hybrid system is suggested for effective functioning. Another

advice is permitting organization to achieve competitive advantage of uniqueness internally that

is distinct from external that is currently got mixtures with other organization (de Aguiar and

Bebbington, 2021). The proper valuation of cost of particular assets before it can be included in

present balance sheet. Further, making clear for companies that what constitute an non-physical

asset.

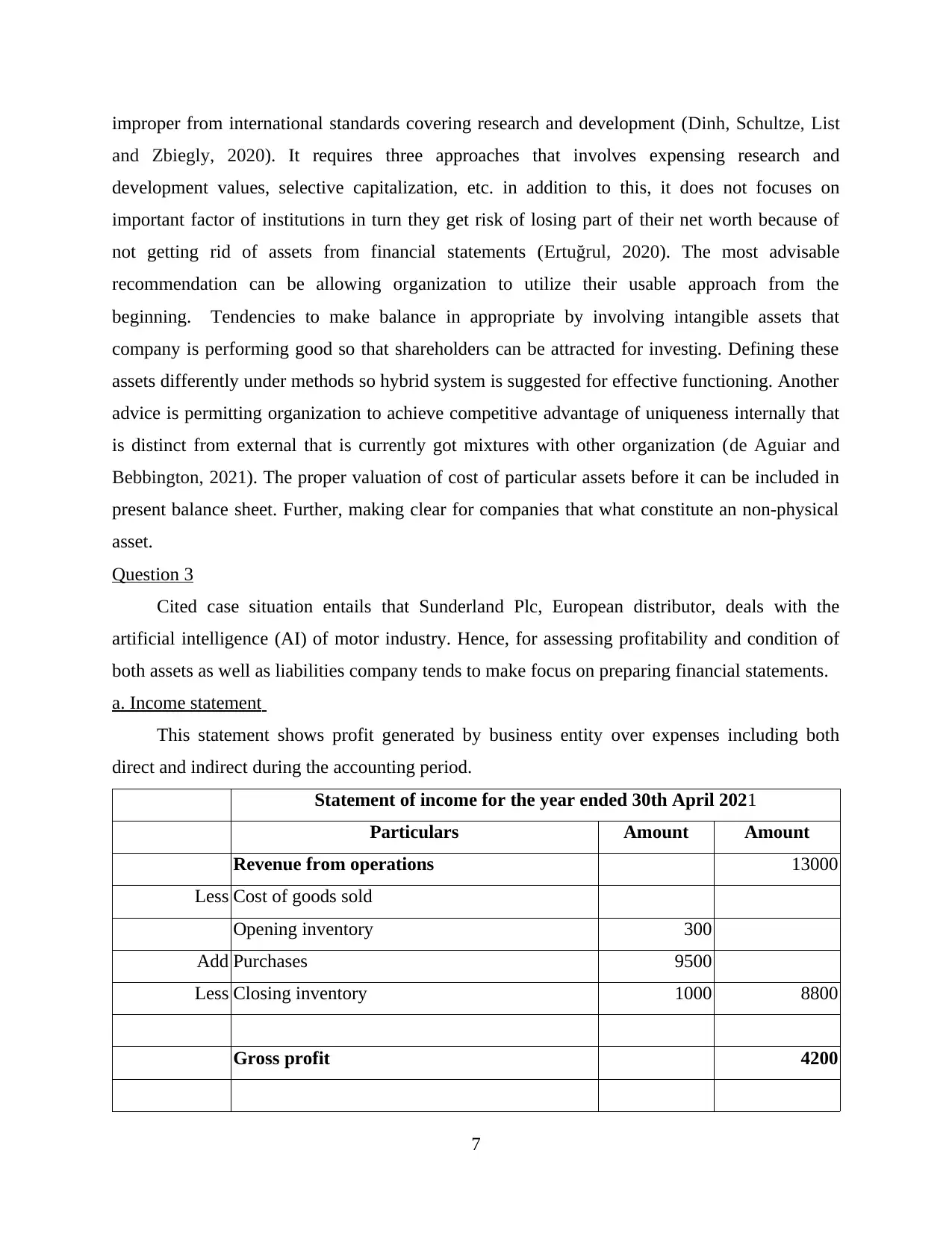

Question 3

Cited case situation entails that Sunderland Plc, European distributor, deals with the

artificial intelligence (AI) of motor industry. Hence, for assessing profitability and condition of

both assets as well as liabilities company tends to make focus on preparing financial statements.

a. Income statement

This statement shows profit generated by business entity over expenses including both

direct and indirect during the accounting period.

Statement of income for the year ended 30th April 2021

Particulars Amount Amount

Revenue from operations 13000

Less Cost of goods sold

Opening inventory 300

Add Purchases 9500

Less Closing inventory 1000 8800

Gross profit 4200

7

and Zbiegly, 2020). It requires three approaches that involves expensing research and

development values, selective capitalization, etc. in addition to this, it does not focuses on

important factor of institutions in turn they get risk of losing part of their net worth because of

not getting rid of assets from financial statements (Ertuğrul, 2020). The most advisable

recommendation can be allowing organization to utilize their usable approach from the

beginning. Tendencies to make balance in appropriate by involving intangible assets that

company is performing good so that shareholders can be attracted for investing. Defining these

assets differently under methods so hybrid system is suggested for effective functioning. Another

advice is permitting organization to achieve competitive advantage of uniqueness internally that

is distinct from external that is currently got mixtures with other organization (de Aguiar and

Bebbington, 2021). The proper valuation of cost of particular assets before it can be included in

present balance sheet. Further, making clear for companies that what constitute an non-physical

asset.

Question 3

Cited case situation entails that Sunderland Plc, European distributor, deals with the

artificial intelligence (AI) of motor industry. Hence, for assessing profitability and condition of

both assets as well as liabilities company tends to make focus on preparing financial statements.

a. Income statement

This statement shows profit generated by business entity over expenses including both

direct and indirect during the accounting period.

Statement of income for the year ended 30th April 2021

Particulars Amount Amount

Revenue from operations 13000

Less Cost of goods sold

Opening inventory 300

Add Purchases 9500

Less Closing inventory 1000 8800

Gross profit 4200

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

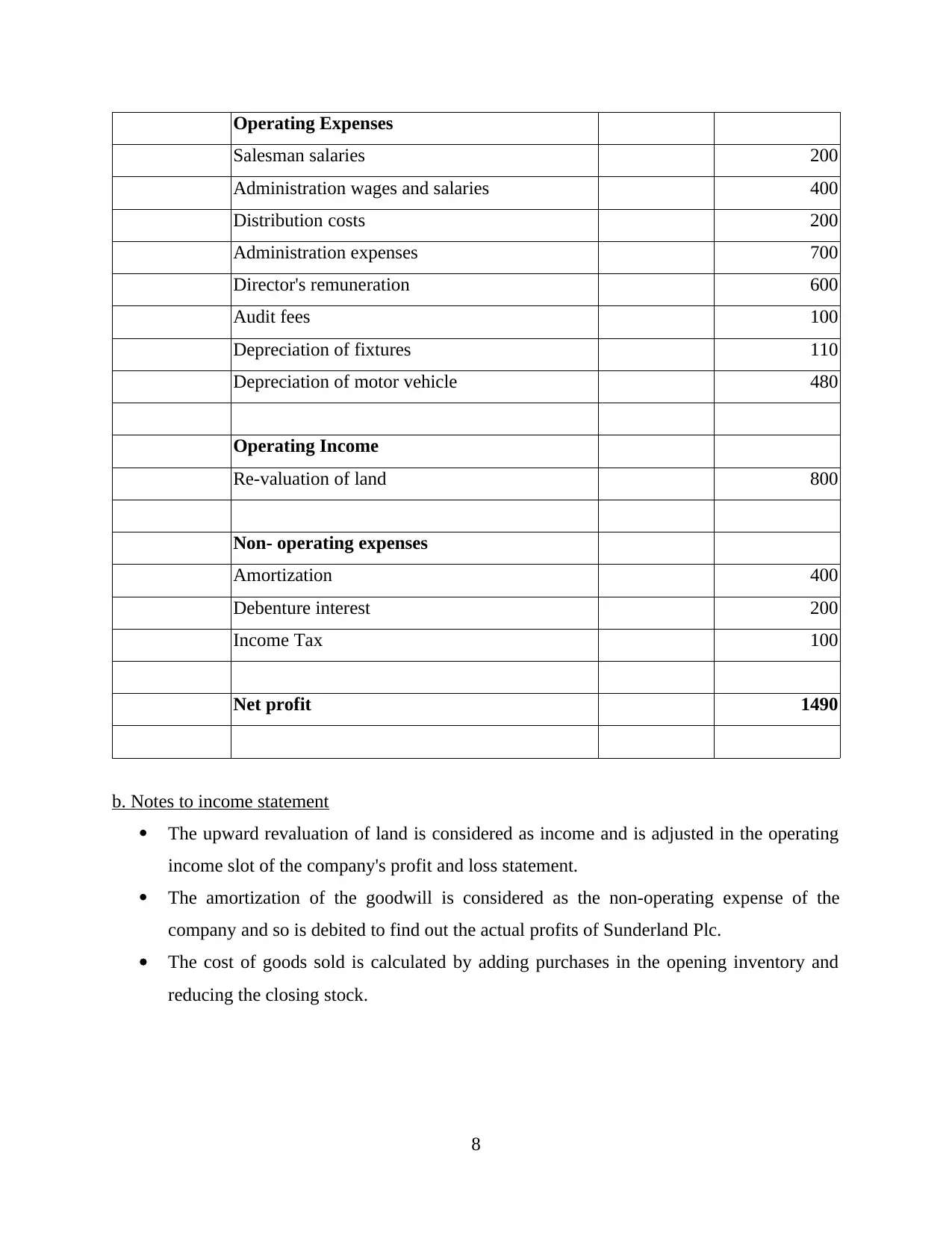

Operating Expenses

Salesman salaries 200

Administration wages and salaries 400

Distribution costs 200

Administration expenses 700

Director's remuneration 600

Audit fees 100

Depreciation of fixtures 110

Depreciation of motor vehicle 480

Operating Income

Re-valuation of land 800

Non- operating expenses

Amortization 400

Debenture interest 200

Income Tax 100

Net profit 1490

b. Notes to income statement

The upward revaluation of land is considered as income and is adjusted in the operating

income slot of the company's profit and loss statement.

The amortization of the goodwill is considered as the non-operating expense of the

company and so is debited to find out the actual profits of Sunderland Plc.

The cost of goods sold is calculated by adding purchases in the opening inventory and

reducing the closing stock.

8

Salesman salaries 200

Administration wages and salaries 400

Distribution costs 200

Administration expenses 700

Director's remuneration 600

Audit fees 100

Depreciation of fixtures 110

Depreciation of motor vehicle 480

Operating Income

Re-valuation of land 800

Non- operating expenses

Amortization 400

Debenture interest 200

Income Tax 100

Net profit 1490

b. Notes to income statement

The upward revaluation of land is considered as income and is adjusted in the operating

income slot of the company's profit and loss statement.

The amortization of the goodwill is considered as the non-operating expense of the

company and so is debited to find out the actual profits of Sunderland Plc.

The cost of goods sold is calculated by adding purchases in the opening inventory and

reducing the closing stock.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

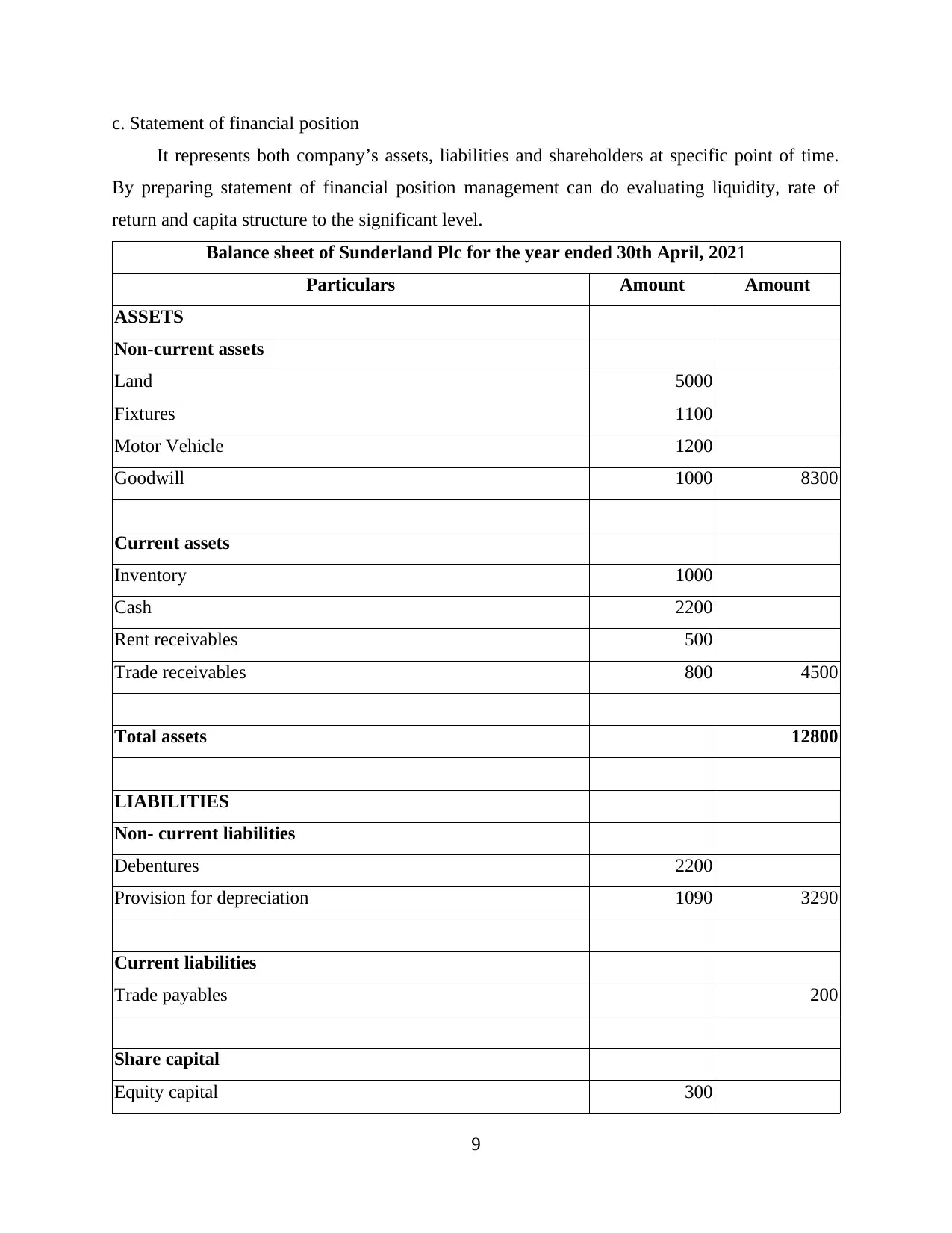

c. Statement of financial position

It represents both company’s assets, liabilities and shareholders at specific point of time.

By preparing statement of financial position management can do evaluating liquidity, rate of

return and capita structure to the significant level.

Balance sheet of Sunderland Plc for the year ended 30th April, 2021

Particulars Amount Amount

ASSETS

Non-current assets

Land 5000

Fixtures 1100

Motor Vehicle 1200

Goodwill 1000 8300

Current assets

Inventory 1000

Cash 2200

Rent receivables 500

Trade receivables 800 4500

Total assets 12800

LIABILITIES

Non- current liabilities

Debentures 2200

Provision for depreciation 1090 3290

Current liabilities

Trade payables 200

Share capital

Equity capital 300

9

It represents both company’s assets, liabilities and shareholders at specific point of time.

By preparing statement of financial position management can do evaluating liquidity, rate of

return and capita structure to the significant level.

Balance sheet of Sunderland Plc for the year ended 30th April, 2021

Particulars Amount Amount

ASSETS

Non-current assets

Land 5000

Fixtures 1100

Motor Vehicle 1200

Goodwill 1000 8300

Current assets

Inventory 1000

Cash 2200

Rent receivables 500

Trade receivables 800 4500

Total assets 12800

LIABILITIES

Non- current liabilities

Debentures 2200

Provision for depreciation 1090 3290

Current liabilities

Trade payables 200

Share capital

Equity capital 300

9

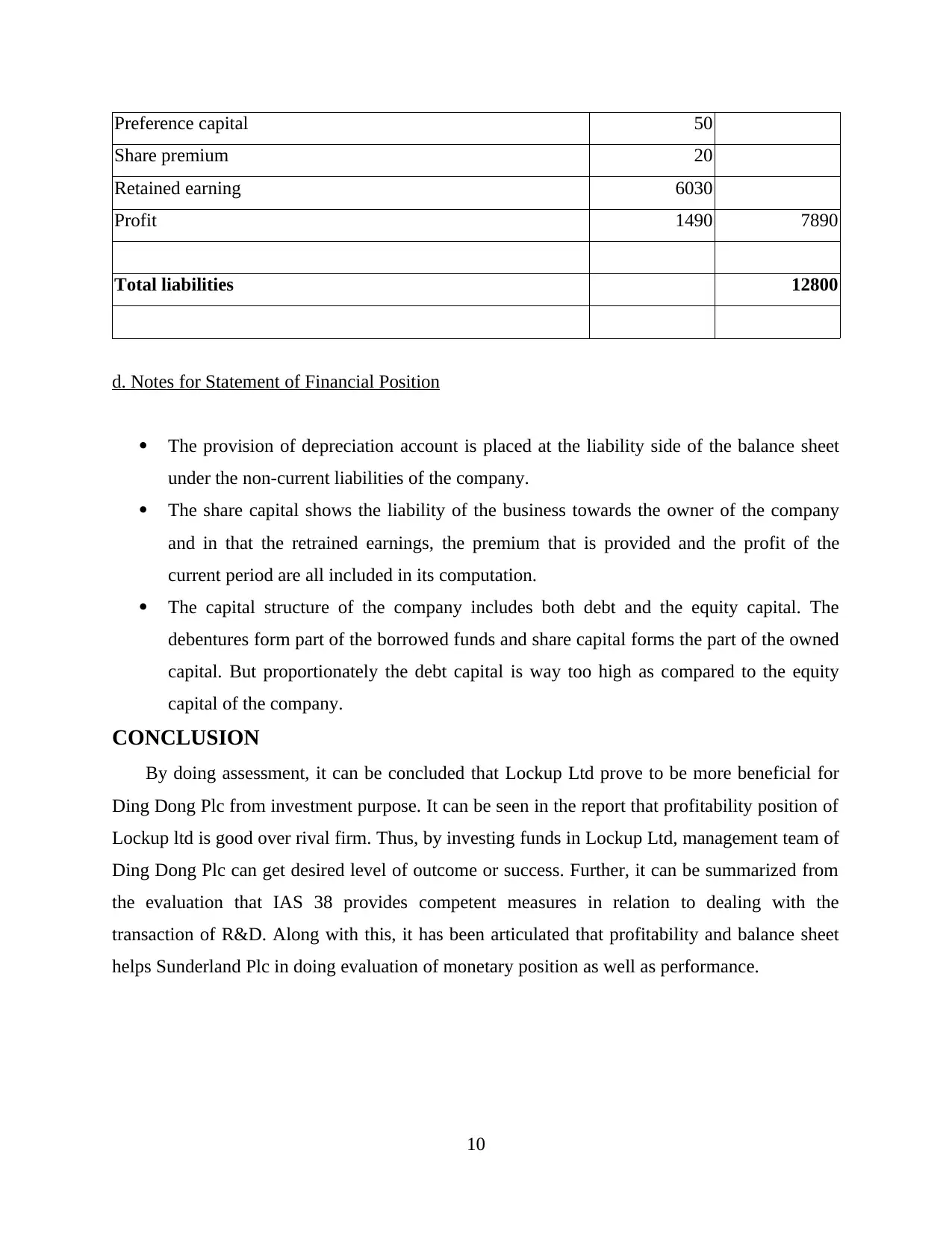

Preference capital 50

Share premium 20

Retained earning 6030

Profit 1490 7890

Total liabilities 12800

d. Notes for Statement of Financial Position

The provision of depreciation account is placed at the liability side of the balance sheet

under the non-current liabilities of the company.

The share capital shows the liability of the business towards the owner of the company

and in that the retrained earnings, the premium that is provided and the profit of the

current period are all included in its computation.

The capital structure of the company includes both debt and the equity capital. The

debentures form part of the borrowed funds and share capital forms the part of the owned

capital. But proportionately the debt capital is way too high as compared to the equity

capital of the company.

CONCLUSION

By doing assessment, it can be concluded that Lockup Ltd prove to be more beneficial for

Ding Dong Plc from investment purpose. It can be seen in the report that profitability position of

Lockup ltd is good over rival firm. Thus, by investing funds in Lockup Ltd, management team of

Ding Dong Plc can get desired level of outcome or success. Further, it can be summarized from

the evaluation that IAS 38 provides competent measures in relation to dealing with the

transaction of R&D. Along with this, it has been articulated that profitability and balance sheet

helps Sunderland Plc in doing evaluation of monetary position as well as performance.

10

Share premium 20

Retained earning 6030

Profit 1490 7890

Total liabilities 12800

d. Notes for Statement of Financial Position

The provision of depreciation account is placed at the liability side of the balance sheet

under the non-current liabilities of the company.

The share capital shows the liability of the business towards the owner of the company

and in that the retrained earnings, the premium that is provided and the profit of the

current period are all included in its computation.

The capital structure of the company includes both debt and the equity capital. The

debentures form part of the borrowed funds and share capital forms the part of the owned

capital. But proportionately the debt capital is way too high as compared to the equity

capital of the company.

CONCLUSION

By doing assessment, it can be concluded that Lockup Ltd prove to be more beneficial for

Ding Dong Plc from investment purpose. It can be seen in the report that profitability position of

Lockup ltd is good over rival firm. Thus, by investing funds in Lockup Ltd, management team of

Ding Dong Plc can get desired level of outcome or success. Further, it can be summarized from

the evaluation that IAS 38 provides competent measures in relation to dealing with the

transaction of R&D. Along with this, it has been articulated that profitability and balance sheet

helps Sunderland Plc in doing evaluation of monetary position as well as performance.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.