International Finance Report: Portfolio Diversification and Governance

VerifiedAdded on 2022/11/18

|10

|2441

|496

Report

AI Summary

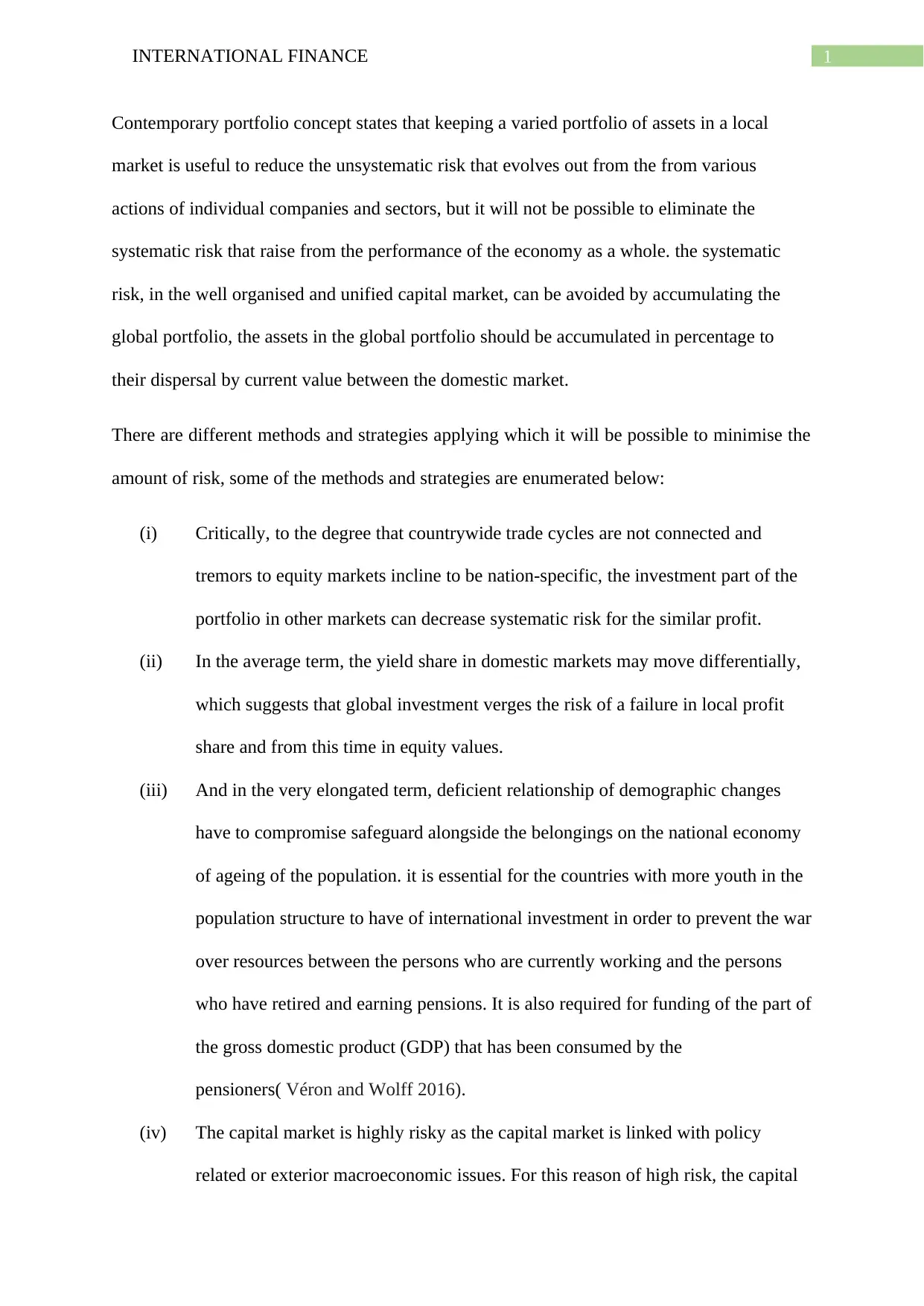

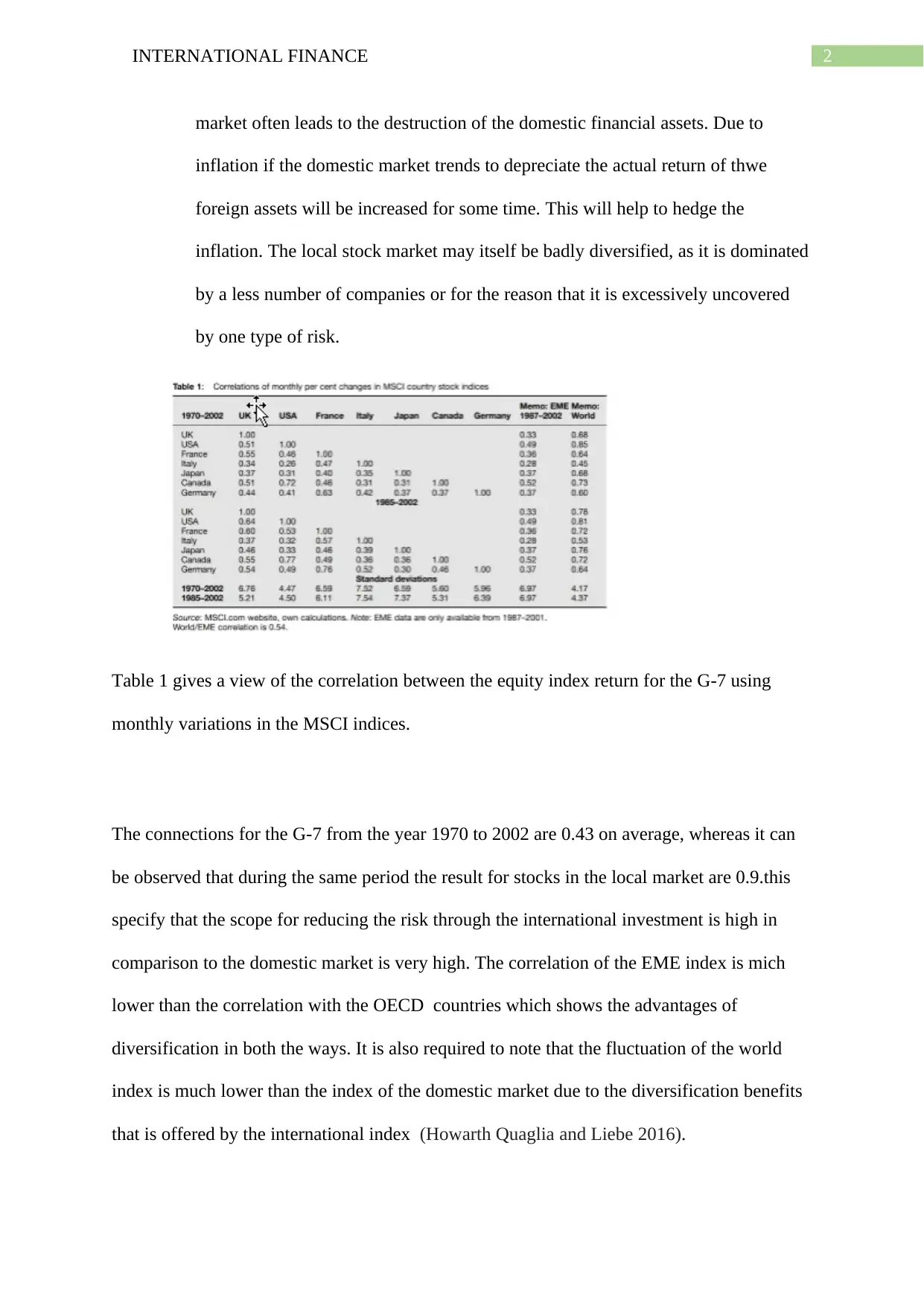

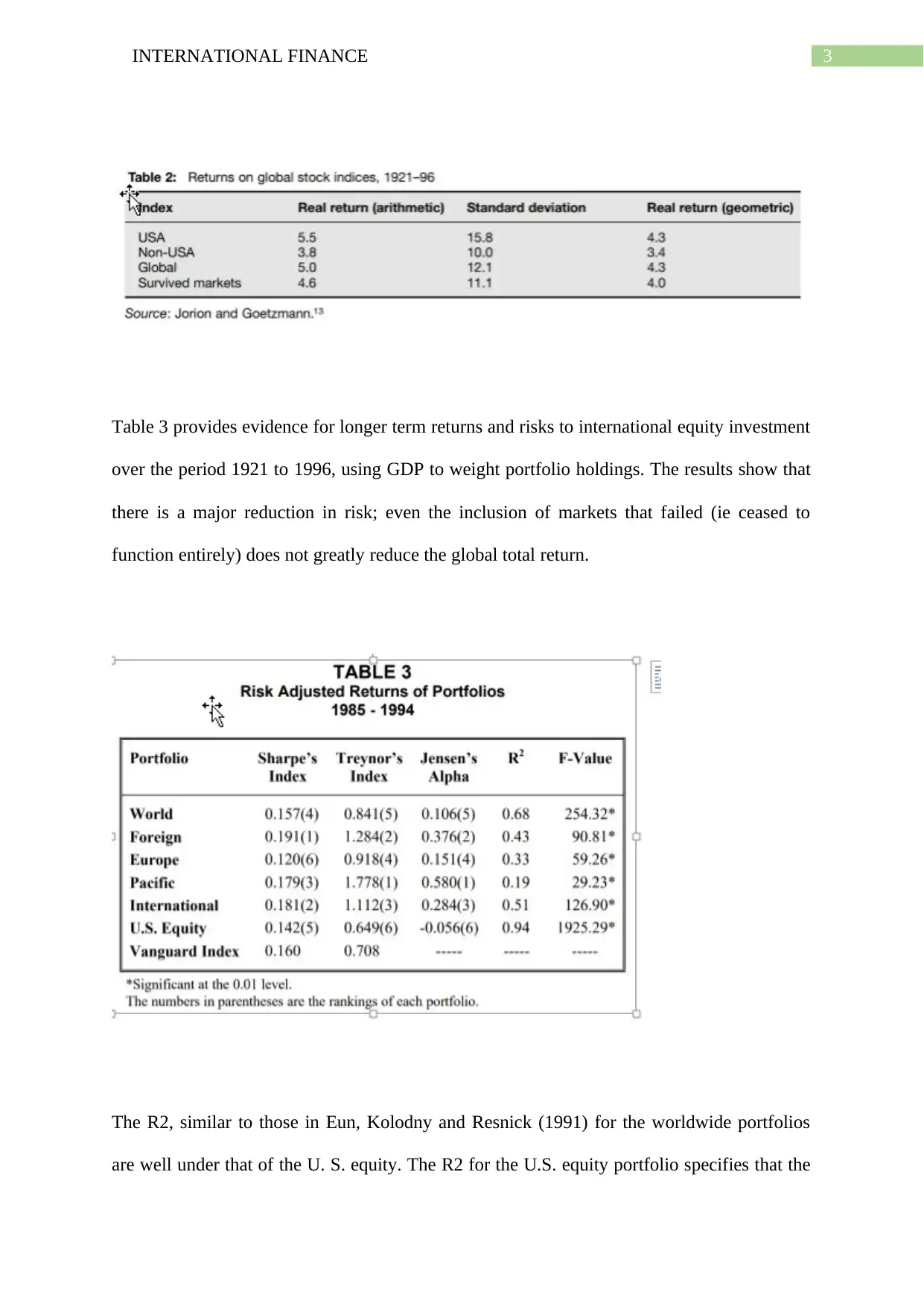

This report delves into the realm of international finance, examining the benefits of portfolio diversification in mitigating systematic risk and enhancing returns. It explores how global portfolios, structured in proportion to market distribution, can reduce risk, especially when national trade cycles are uncorrelated. The report also addresses the importance of corporate governance, defining its role in overseeing corporations and ensuring ethical practices. It highlights the shareholder and stakeholder methods, emphasizing the significance of considering various stakeholder interests. Furthermore, it discusses the impact of corporate governance on mutual funds, particularly concerning board composition, director compensation, and potential conflicts of interest, such as investment banks prioritizing their underwriting and advisory services over fund performance. The analysis includes empirical evidence from various studies, providing insights into fund performance, the influence of investment banking relationships, and the benefits of international diversification. The report concludes by underscoring the advantages of global portfolios in terms of risk-adjusted returns and the need for robust governance to protect investor interests.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.