International Finance Report: Derivative Instruments and Hedging

VerifiedAdded on 2022/10/17

|11

|2671

|235

Report

AI Summary

This report provides an overview of key concepts in international finance, focusing on derivative instruments and hedging strategies. It begins by defining and explaining the Theory of Purchasing Power Parity (PPPT) and the International Fisher's Effect (IFE), crucial for understanding exchange rate dynamics. The report then delves into various derivative instruments, including forward contracts, futures contracts, options, and swaps, detailing their functionalities and applications in risk management. It further explores interest rate derivatives, particularly Forward Rate Agreements (FRAs), and concludes with an explanation of the money market hedge, providing a practical example. The report references relevant literature to support the presented theories and concepts, offering a comprehensive understanding of international financial management and derivative applications. This report is designed to help students grasp the essentials of international finance and its practical applications.

International Finance

0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Purchasing Power Parity Theory (PPPT)........................................................................................2

International Fisher’s Effect (IFE) (Fisher-open)............................................................................2

Forward contract (derivative instrument)........................................................................................4

Futures contract (derivative instrument)..........................................................................................4

Options.............................................................................................................................................5

Swap (derivative instrument)...........................................................................................................6

Interest Rate Derivatives (derivative instrument)............................................................................6

Forward rate agreement (FRA) (derivative agreement)..................................................................6

Money Market Hedge......................................................................................................................6

References........................................................................................................................................8

1

Purchasing Power Parity Theory (PPPT)........................................................................................2

International Fisher’s Effect (IFE) (Fisher-open)............................................................................2

Forward contract (derivative instrument)........................................................................................4

Futures contract (derivative instrument)..........................................................................................4

Options.............................................................................................................................................5

Swap (derivative instrument)...........................................................................................................6

Interest Rate Derivatives (derivative instrument)............................................................................6

Forward rate agreement (FRA) (derivative agreement)..................................................................6

Money Market Hedge......................................................................................................................6

References........................................................................................................................................8

1

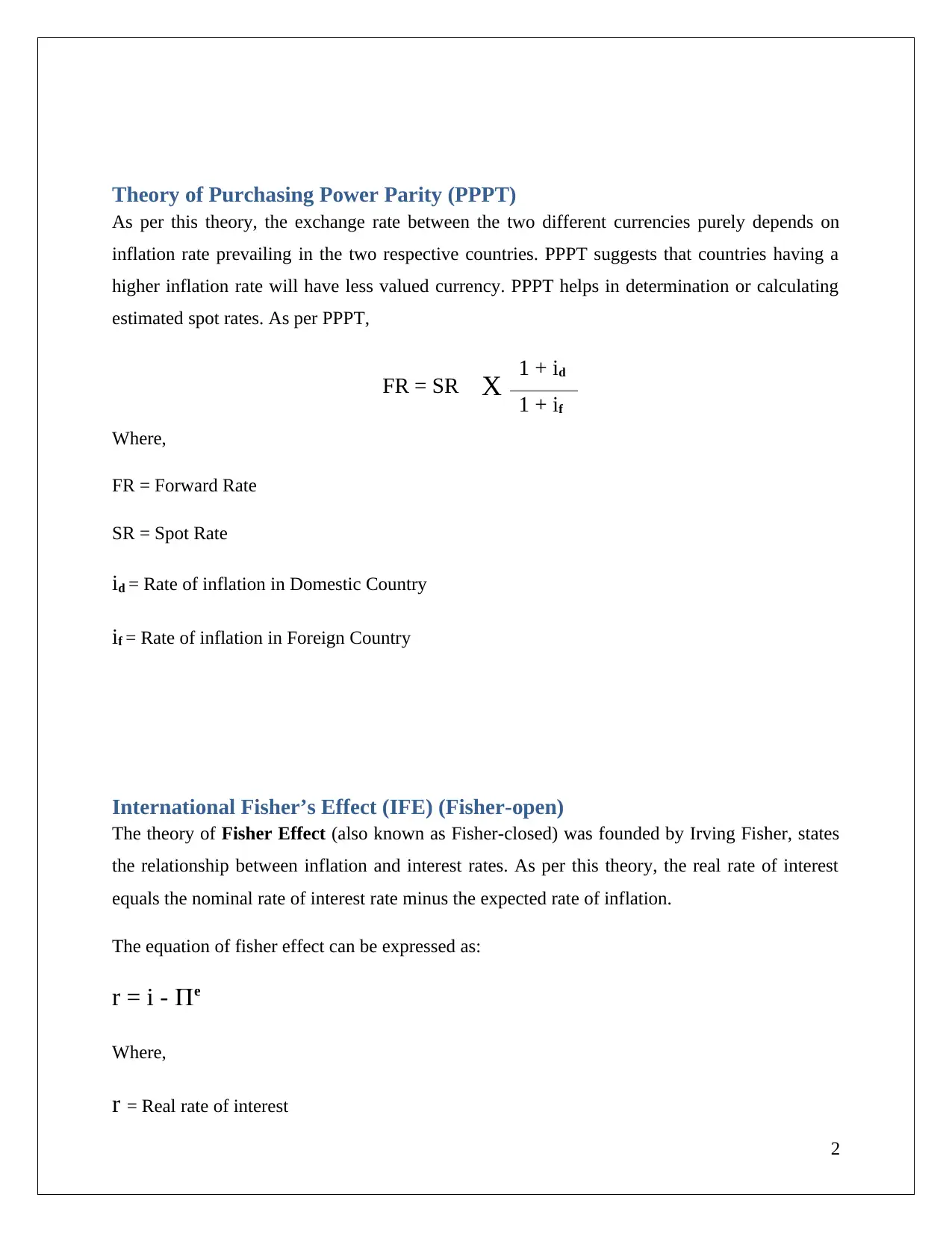

Theory of Purchasing Power Parity (PPPT)

As per this theory, the exchange rate between the two different currencies purely depends on

inflation rate prevailing in the two respective countries. PPPT suggests that countries having a

higher inflation rate will have less valued currency. PPPT helps in determination or calculating

estimated spot rates. As per PPPT,

FR = SR X 1 + id

1 + if

Where,

FR = Forward Rate

SR = Spot Rate

id = Rate of inflation in Domestic Country

if = Rate of inflation in Foreign Country

International Fisher’s Effect (IFE) (Fisher-open)

The theory of Fisher Effect (also known as Fisher-closed) was founded by Irving Fisher, states

the relationship between inflation and interest rates. As per this theory, the real rate of interest

equals the nominal rate of interest rate minus the expected rate of inflation.

The equation of fisher effect can be expressed as:

r = i - e

Where,

r = Real rate of interest

2

As per this theory, the exchange rate between the two different currencies purely depends on

inflation rate prevailing in the two respective countries. PPPT suggests that countries having a

higher inflation rate will have less valued currency. PPPT helps in determination or calculating

estimated spot rates. As per PPPT,

FR = SR X 1 + id

1 + if

Where,

FR = Forward Rate

SR = Spot Rate

id = Rate of inflation in Domestic Country

if = Rate of inflation in Foreign Country

International Fisher’s Effect (IFE) (Fisher-open)

The theory of Fisher Effect (also known as Fisher-closed) was founded by Irving Fisher, states

the relationship between inflation and interest rates. As per this theory, the real rate of interest

equals the nominal rate of interest rate minus the expected rate of inflation.

The equation of fisher effect can be expressed as:

r = i - e

Where,

r = Real rate of interest

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

i = Nominal rate of interest

e = Rate of inflation

This equation of fisher theory can be expressed using continuous compounding:

(1+i) = (1+r) (1+e)

The international Fisher effect is an improvement over the standard fisher effect theory and is

especially used in trading of foreign exchange and also to analyze the exchange rate model. This

theory considers present and risk-free rate of interest and does not consider the rate of inflation.

It uses rate of interest rather than rate of inflation to explain how the rate of exchange changes.

According to Puc and Mansaku (2016, p.249), nominal risk-free rate of interest contains a return

in real rate and anticipated inflation. IFE theory indicates that whose interest rate will be high

will have less valued currency because the high-interest rates (nominal) reflect estimated

inflation.

The equation of IFE can be denoted as:

E = variation in the rate of exchange

i1 = rate of interest of country 1

i2 = rate of interest of country 2

3

e = Rate of inflation

This equation of fisher theory can be expressed using continuous compounding:

(1+i) = (1+r) (1+e)

The international Fisher effect is an improvement over the standard fisher effect theory and is

especially used in trading of foreign exchange and also to analyze the exchange rate model. This

theory considers present and risk-free rate of interest and does not consider the rate of inflation.

It uses rate of interest rather than rate of inflation to explain how the rate of exchange changes.

According to Puc and Mansaku (2016, p.249), nominal risk-free rate of interest contains a return

in real rate and anticipated inflation. IFE theory indicates that whose interest rate will be high

will have less valued currency because the high-interest rates (nominal) reflect estimated

inflation.

The equation of IFE can be denoted as:

E = variation in the rate of exchange

i1 = rate of interest of country 1

i2 = rate of interest of country 2

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The theory of purchasing power and the international fisher’s effect provide the theoretical

exchange rates and this might be different from the actual different rate in which the contract can

be settled in future. These are the reasons which make the financial derivatives nullified or

unnecessary. Hedging is a method or technique by which we can nullify or neutralize the chances

of risk or loss which may occur due to changes/variations in rates of exchange.

To protect or hedge the financial derivatives contract different derivative instruments have been

discussed below:

Forward contract (derivative instrument)

This is a derivative instrument that is agreed between two parties such as between a seller and a

purchaser to purchase or sell the goods at a later date. According to Zha and Moser (2017, p.23),

when the contract is made the price of the goods is fixed by the parties so that the contract will

be settled at that price at a later date. The settlement date is also fixed by the parties at the time of

entering into a contract. The forward contract is especially used by those traders who want to

reduce the risk which arises due to change in the market price of the goods or securities. The

buyers hedge the contract with the sellers by paying a certain amount of commission. So the

sellers have to sell the goods or securities at a price fixed at the time of entering into a contract

with the buyers. The details of the contract are confidential and are not known to the general

public. For instance: a seller wants to sell 1000 refrigerator after six months and has fixed the

price with the bank now. The price of the 1000 refrigerator fixed by the seller and bank is $5

million. Both the parties’ seller and bank now enters into a forward contract that if the price of

refrigerator increases or decreases the seller will sell his refrigerator at $5 million after six

months. After six months the market price of 1000 refrigerator was reduced to $3 million and the

banks have to pay to the seller $2 million. So, in this case, it can be seen that the seller has

gained from the forward contract and the bank was in a loss. This type of contract is mostly used

by the buyer or seller so that they will not have to suffer for the losses due to an increase or

decrease in market price.

Futures contract (derivative instrument)

This is an agreement that is made between the sellers and the buyers of the securities or goods to

purchase or the securities at fixed price in future. This price and date are fixed by the sellers and

buyers at the time of entering into the contract. This contract is handed over to the clearing

houses so that they can settle the transaction. The futures contract is a derivative instrument and

can be made on goods such as gas and oil, corn, and wheat. Future contract market is a highly

liquid market and the parties to the contract are provided with the facility to exit the contract

whenever they want. As opined by Chang et al. (2016, p.584), future contract is one type of

speculation contract and the speculators use this type of contract for speculations so that they can

bet on the movement of prices of securities or goods in the market. The settlement of this type of

contract is settled on cash by the parties. Only commodity futures can be delivered physically

4

exchange rates and this might be different from the actual different rate in which the contract can

be settled in future. These are the reasons which make the financial derivatives nullified or

unnecessary. Hedging is a method or technique by which we can nullify or neutralize the chances

of risk or loss which may occur due to changes/variations in rates of exchange.

To protect or hedge the financial derivatives contract different derivative instruments have been

discussed below:

Forward contract (derivative instrument)

This is a derivative instrument that is agreed between two parties such as between a seller and a

purchaser to purchase or sell the goods at a later date. According to Zha and Moser (2017, p.23),

when the contract is made the price of the goods is fixed by the parties so that the contract will

be settled at that price at a later date. The settlement date is also fixed by the parties at the time of

entering into a contract. The forward contract is especially used by those traders who want to

reduce the risk which arises due to change in the market price of the goods or securities. The

buyers hedge the contract with the sellers by paying a certain amount of commission. So the

sellers have to sell the goods or securities at a price fixed at the time of entering into a contract

with the buyers. The details of the contract are confidential and are not known to the general

public. For instance: a seller wants to sell 1000 refrigerator after six months and has fixed the

price with the bank now. The price of the 1000 refrigerator fixed by the seller and bank is $5

million. Both the parties’ seller and bank now enters into a forward contract that if the price of

refrigerator increases or decreases the seller will sell his refrigerator at $5 million after six

months. After six months the market price of 1000 refrigerator was reduced to $3 million and the

banks have to pay to the seller $2 million. So, in this case, it can be seen that the seller has

gained from the forward contract and the bank was in a loss. This type of contract is mostly used

by the buyer or seller so that they will not have to suffer for the losses due to an increase or

decrease in market price.

Futures contract (derivative instrument)

This is an agreement that is made between the sellers and the buyers of the securities or goods to

purchase or the securities at fixed price in future. This price and date are fixed by the sellers and

buyers at the time of entering into the contract. This contract is handed over to the clearing

houses so that they can settle the transaction. The futures contract is a derivative instrument and

can be made on goods such as gas and oil, corn, and wheat. Future contract market is a highly

liquid market and the parties to the contract are provided with the facility to exit the contract

whenever they want. As opined by Chang et al. (2016, p.584), future contract is one type of

speculation contract and the speculators use this type of contract for speculations so that they can

bet on the movement of prices of securities or goods in the market. The settlement of this type of

contract is settled on cash by the parties. Only commodity futures can be delivered physically

4

and the other futures are settled in cash. This instrument is mostly preferred by the institutional

investors.

Options

Options contracts are derivative financial contracts in which there are two different parties such

as option holders and option writers. Option contracts give right to the party to the option to sell

or purchase contracted securities or assets at the fixed price which is agreed today. Such an

agreed price is known as exercise price or strike price. There is no compulsion for the option

holder to settle the option contract. The action to be taken in this regard is solely at the choice of

the option holder. He will exercise such right only when it is beneficial for him.

Call Option: it means the right to purchase. A call option is exercised by the holder only when

the prevailing price in market is higher than the strike price.

Put Option: conveys the right to sell. A put option is exercised by the holder only when the

prevailing price in market is less than the exercise price. The seller, in this case, expect that

market price will get reduced

European Options: This option can be exercised at a specified future date. The seller or the buyer

to the contract can only exercise the European option at date of the maturity period.

American Options: This type of derivative instrument gives option to the holder to exercise the

option at any point of time on a later specified date. The holder of the American options can

exercise American options when it is favorable for the holder that when there is a situation to

gain from the options.

Exchange-traded option: it is an option which gives the party to the contract a right to purchase

the securities or goods at a fixed price which was agreed at the time of contract. This option does

not provide the obligation to the party to purchase the securities or goods at a price fixed by the

market.

The following models can be helpful to calculate the call option value

1. Portfolio Replication Model

2. Risk Neutral Model

3. Binomial Model

4. Black and Scholes Model

For calculating put option value, compute the value of call option and use ‘Put-Call Parity

Theory’.

5

investors.

Options

Options contracts are derivative financial contracts in which there are two different parties such

as option holders and option writers. Option contracts give right to the party to the option to sell

or purchase contracted securities or assets at the fixed price which is agreed today. Such an

agreed price is known as exercise price or strike price. There is no compulsion for the option

holder to settle the option contract. The action to be taken in this regard is solely at the choice of

the option holder. He will exercise such right only when it is beneficial for him.

Call Option: it means the right to purchase. A call option is exercised by the holder only when

the prevailing price in market is higher than the strike price.

Put Option: conveys the right to sell. A put option is exercised by the holder only when the

prevailing price in market is less than the exercise price. The seller, in this case, expect that

market price will get reduced

European Options: This option can be exercised at a specified future date. The seller or the buyer

to the contract can only exercise the European option at date of the maturity period.

American Options: This type of derivative instrument gives option to the holder to exercise the

option at any point of time on a later specified date. The holder of the American options can

exercise American options when it is favorable for the holder that when there is a situation to

gain from the options.

Exchange-traded option: it is an option which gives the party to the contract a right to purchase

the securities or goods at a fixed price which was agreed at the time of contract. This option does

not provide the obligation to the party to purchase the securities or goods at a price fixed by the

market.

The following models can be helpful to calculate the call option value

1. Portfolio Replication Model

2. Risk Neutral Model

3. Binomial Model

4. Black and Scholes Model

For calculating put option value, compute the value of call option and use ‘Put-Call Parity

Theory’.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Put-Call Parity Theory: Put-call parity theory is a theory which establishes relationship between

price of put option, price of call option, exercise price, and current market price.

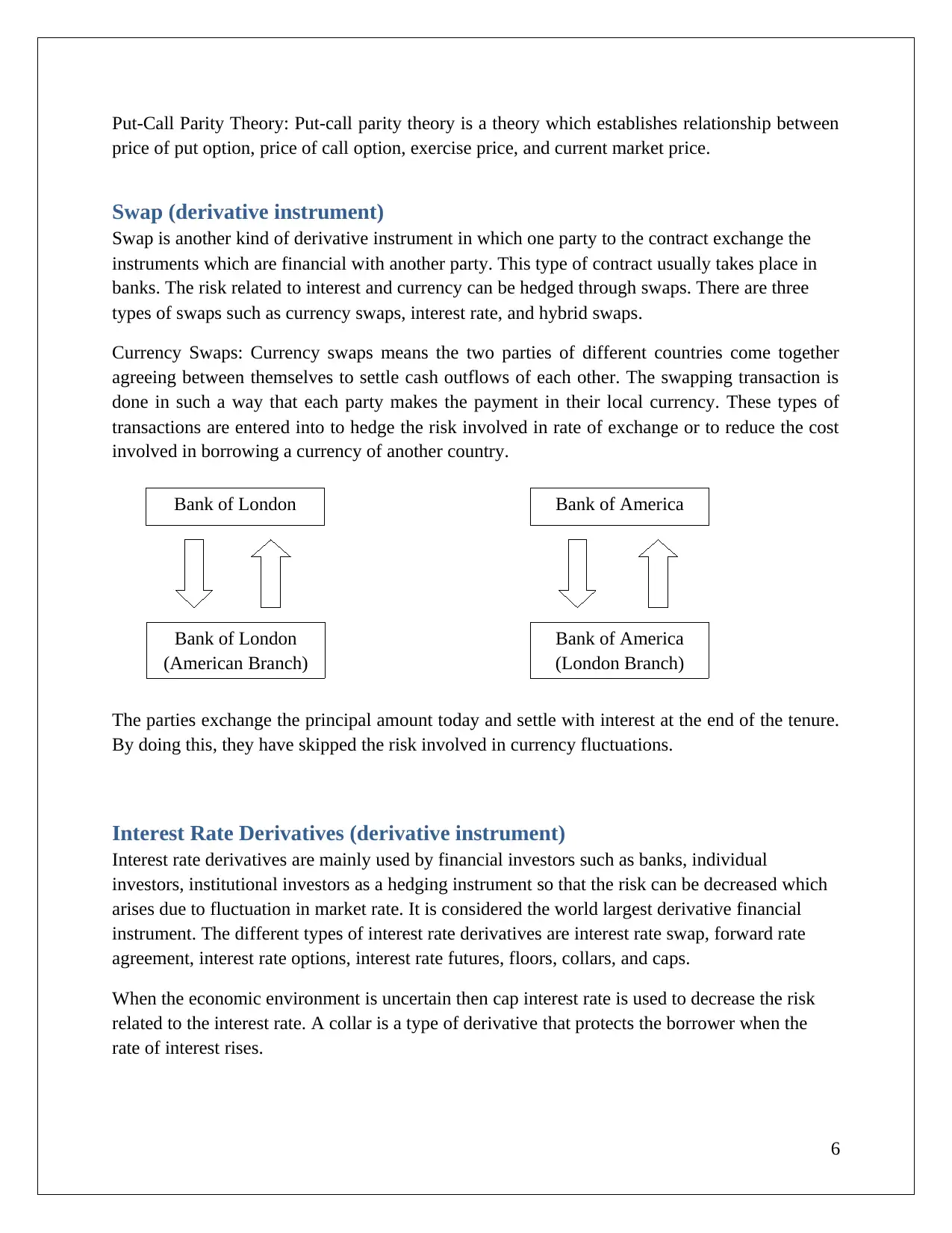

Swap (derivative instrument)

Swap is another kind of derivative instrument in which one party to the contract exchange the

instruments which are financial with another party. This type of contract usually takes place in

banks. The risk related to interest and currency can be hedged through swaps. There are three

types of swaps such as currency swaps, interest rate, and hybrid swaps.

Currency Swaps: Currency swaps means the two parties of different countries come together

agreeing between themselves to settle cash outflows of each other. The swapping transaction is

done in such a way that each party makes the payment in their local currency. These types of

transactions are entered into to hedge the risk involved in rate of exchange or to reduce the cost

involved in borrowing a currency of another country.

The parties exchange the principal amount today and settle with interest at the end of the tenure.

By doing this, they have skipped the risk involved in currency fluctuations.

Interest Rate Derivatives (derivative instrument)

Interest rate derivatives are mainly used by financial investors such as banks, individual

investors, institutional investors as a hedging instrument so that the risk can be decreased which

arises due to fluctuation in market rate. It is considered the world largest derivative financial

instrument. The different types of interest rate derivatives are interest rate swap, forward rate

agreement, interest rate options, interest rate futures, floors, collars, and caps.

When the economic environment is uncertain then cap interest rate is used to decrease the risk

related to the interest rate. A collar is a type of derivative that protects the borrower when the

rate of interest rises.

6

Bank of London Bank of America

Bank of America

(London Branch)

Bank of London

(American Branch)

price of put option, price of call option, exercise price, and current market price.

Swap (derivative instrument)

Swap is another kind of derivative instrument in which one party to the contract exchange the

instruments which are financial with another party. This type of contract usually takes place in

banks. The risk related to interest and currency can be hedged through swaps. There are three

types of swaps such as currency swaps, interest rate, and hybrid swaps.

Currency Swaps: Currency swaps means the two parties of different countries come together

agreeing between themselves to settle cash outflows of each other. The swapping transaction is

done in such a way that each party makes the payment in their local currency. These types of

transactions are entered into to hedge the risk involved in rate of exchange or to reduce the cost

involved in borrowing a currency of another country.

The parties exchange the principal amount today and settle with interest at the end of the tenure.

By doing this, they have skipped the risk involved in currency fluctuations.

Interest Rate Derivatives (derivative instrument)

Interest rate derivatives are mainly used by financial investors such as banks, individual

investors, institutional investors as a hedging instrument so that the risk can be decreased which

arises due to fluctuation in market rate. It is considered the world largest derivative financial

instrument. The different types of interest rate derivatives are interest rate swap, forward rate

agreement, interest rate options, interest rate futures, floors, collars, and caps.

When the economic environment is uncertain then cap interest rate is used to decrease the risk

related to the interest rate. A collar is a type of derivative that protects the borrower when the

rate of interest rises.

6

Bank of London Bank of America

Bank of America

(London Branch)

Bank of London

(American Branch)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Forward rate agreement (FRA) (derivative agreement)

FRA is an agreement made between two parties on interest rate to be settled at a future date. The

settlement is made on cash between the parties. The party has to pay to the other party the

nominal difference in the rate which was fixed on agreement and the current market rate.

According to Nyhoff et al. (2015, p.714), the borrower is usually the one who pays the fixed rate

of interest and. The borrower will enter into the contract only when he believes that the rate of

interest will increase at a later date. The agreement is entered into the exchange rate of London

interbank exchange rate (LIBOR).

Money Market Hedge

Money market hedge means transactions of parallel borrowing or lending in two different

countries to seal the value or rate of home currency in a future transaction involving foreign

exchange.

For example:

An importer needs to make a payment of US$ 100,000 after 12 months.

Spot Rate US$1 = 60₹

12 months Forward Rate US$1 = 64.50₹

Rates in money market

India ( )₹ US ($)

Deposit rate 4%

Borrowing rate 10%

Step 1: Invest in US$ such amount so that US$ investment along with interest @4% p.a. on it

becomes equal to US$100,000.

Let amount invested = Z

Therefore, Z+Z*4%= US$ 100,000

Z = US$ 96,154

7

FRA is an agreement made between two parties on interest rate to be settled at a future date. The

settlement is made on cash between the parties. The party has to pay to the other party the

nominal difference in the rate which was fixed on agreement and the current market rate.

According to Nyhoff et al. (2015, p.714), the borrower is usually the one who pays the fixed rate

of interest and. The borrower will enter into the contract only when he believes that the rate of

interest will increase at a later date. The agreement is entered into the exchange rate of London

interbank exchange rate (LIBOR).

Money Market Hedge

Money market hedge means transactions of parallel borrowing or lending in two different

countries to seal the value or rate of home currency in a future transaction involving foreign

exchange.

For example:

An importer needs to make a payment of US$ 100,000 after 12 months.

Spot Rate US$1 = 60₹

12 months Forward Rate US$1 = 64.50₹

Rates in money market

India ( )₹ US ($)

Deposit rate 4%

Borrowing rate 10%

Step 1: Invest in US$ such amount so that US$ investment along with interest @4% p.a. on it

becomes equal to US$100,000.

Let amount invested = Z

Therefore, Z+Z*4%= US$ 100,000

Z = US$ 96,154

7

Step 2: Buy US$ 96,154 by taking loan at spot rate₹

Therefore, Loan amount = 96,154 x 60

= 57, 69,240₹

Step 3: After 12 months, realize US$ investment along with interest and pay US$ 100,000 to the

exporter.

Step 4: Repay loan along with interest₹

Therefore, amount to be repaid after 12 months = 57, 69,240 * 110%

= 63, 46,164₹

Equivalent outflow in case of forward cover = 100,000*64.50₹

= 64, 50,000₹

Therefore, money market hedge will be a better option as it leads to lesser outflow.₹

8

Therefore, Loan amount = 96,154 x 60

= 57, 69,240₹

Step 3: After 12 months, realize US$ investment along with interest and pay US$ 100,000 to the

exporter.

Step 4: Repay loan along with interest₹

Therefore, amount to be repaid after 12 months = 57, 69,240 * 110%

= 63, 46,164₹

Equivalent outflow in case of forward cover = 100,000*64.50₹

= 64, 50,000₹

Therefore, money market hedge will be a better option as it leads to lesser outflow.₹

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Adler, G., Lisack, N. and Mano, R., (2019). Unveiling the effects of foreign exchange

intervention: A panel approach. Emerging Markets Review, p.100620.

Aktan, B., Turen, S., Tvaronavičienė, M., Celik, S. and Alsadeh, H.A., (2018). Corporate

governance and performance of the financial firms in Bahrain. Polish Journal of Management

Studies, p.17.

Briggs, S. and Musa, M., (2017). THE EFFECT OF EXCHANGE RATES ON NIGERIA

ECONOMIC GROWTH (2006-2016). MACROECONOMIC IMPLICATIONS OF LOW LIFE

EXPECTANCY IN SUB-SAHARAN AFRICA NATIONS, p.5.

Chang, H.S., Donohoe, M. and Sougiannis, T., (2016). Do analysts understand the economic and

reporting complexities of derivatives?. Journal of Accounting and Economics, 61(2-3), pp.584-604.

Engel, C., (2016). Exchange rates, interest rates, and the risk premium. American Economic

Review, 106(2), pp.436-74.

Ismailov, A. and Rossi, B., (2018). Uncertainty and deviations from uncovered interest rate

parity. Journal of International Money and Finance, 88, pp.242-259.

Kock, A., Heising, W. and Gemünden, H.G., (2016). A contingency approach on the impact of

front-end success on project portfolio success. Project Management Journal, 47(2), pp.115-129.

Lothian, J.R., (2017). Equilibrium relationships between money and other economic

variables. Essays in International Money and Finance: Interest Rates, Exchange Rates, Prices

and the Supply of Money Within and Across Countries, p.31.

9

Adler, G., Lisack, N. and Mano, R., (2019). Unveiling the effects of foreign exchange

intervention: A panel approach. Emerging Markets Review, p.100620.

Aktan, B., Turen, S., Tvaronavičienė, M., Celik, S. and Alsadeh, H.A., (2018). Corporate

governance and performance of the financial firms in Bahrain. Polish Journal of Management

Studies, p.17.

Briggs, S. and Musa, M., (2017). THE EFFECT OF EXCHANGE RATES ON NIGERIA

ECONOMIC GROWTH (2006-2016). MACROECONOMIC IMPLICATIONS OF LOW LIFE

EXPECTANCY IN SUB-SAHARAN AFRICA NATIONS, p.5.

Chang, H.S., Donohoe, M. and Sougiannis, T., (2016). Do analysts understand the economic and

reporting complexities of derivatives?. Journal of Accounting and Economics, 61(2-3), pp.584-604.

Engel, C., (2016). Exchange rates, interest rates, and the risk premium. American Economic

Review, 106(2), pp.436-74.

Ismailov, A. and Rossi, B., (2018). Uncertainty and deviations from uncovered interest rate

parity. Journal of International Money and Finance, 88, pp.242-259.

Kock, A., Heising, W. and Gemünden, H.G., (2016). A contingency approach on the impact of

front-end success on project portfolio success. Project Management Journal, 47(2), pp.115-129.

Lothian, J.R., (2017). Equilibrium relationships between money and other economic

variables. Essays in International Money and Finance: Interest Rates, Exchange Rates, Prices

and the Supply of Money Within and Across Countries, p.31.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nyhoff, J., Sturm, F. and Labuszewski, J., Chicago Mercantile Exchange Inc, (2015). Pricing a

Forward Rate Agreement Financial Product Using a Non-Par Value. U.S. Patent Application

14/714,872.

Puci, J. and Mansaku, S., (2016). An Empirical Evidence of the International Fisher Effect on

the USD to CNY Exchange Rate. Academic Journal of Interdisciplinary Studies, 5(1), p.249.

Schimmelfennig, F., (2018). European integration (theory) in times of crisis. A comparison of

the euro and Schengen crises. Journal of European Public Policy, 25(7), pp.969-989.

Zhao, F. and Moser, J., (2017). Bank lending and interest-rate derivatives. International Journal

of Financial Research, 8(4), pp.23-37.

10

Forward Rate Agreement Financial Product Using a Non-Par Value. U.S. Patent Application

14/714,872.

Puci, J. and Mansaku, S., (2016). An Empirical Evidence of the International Fisher Effect on

the USD to CNY Exchange Rate. Academic Journal of Interdisciplinary Studies, 5(1), p.249.

Schimmelfennig, F., (2018). European integration (theory) in times of crisis. A comparison of

the euro and Schengen crises. Journal of European Public Policy, 25(7), pp.969-989.

Zhao, F. and Moser, J., (2017). Bank lending and interest-rate derivatives. International Journal

of Financial Research, 8(4), pp.23-37.

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.