International Finance: Analyzing Currency Risk for Xinjiang Company

VerifiedAdded on 2020/05/11

|11

|2216

|90

Homework Assignment

AI Summary

This assignment analyzes the currency exchange risk faced by Xinjiang, a company making payments in USD while based in China. It evaluates different hedging strategies, including forward rates, interest rates, and put options, to mitigate the risk of currency fluctuations. The analysis includes detailed calculations of potential gains and losses associated with each strategy, considering factors like spot rates, premiums, and interest received. The assignment recommends the use of option trading to generate higher revenue, and argues that managing foreign exchange risk is crucial for companies like Xinjiang to reduce losses and maintain profitability. The analysis also depicts the unrealized gains/losses faced by Xinjiang and whether the company should remain unhedged or not.

Running head: INTERNATIONAL FINANCE

International Finance

Name of the Student:

Name of the University:

Authors Note:

International Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

1

Table of Contents

a) Analysing the different alternatives:......................................................................................2

b) Justifying the recommendations:...........................................................................................4

c.i) Depicting the unrealised gain/loss faced by Xinjiang through the recommendations:........6

c.ii) Depicting the how the overall unrealised gain or loss happed in each period of

settlement:..................................................................................................................................7

d.i) Depicting whether managing the overall foreign exchange risk is worth the amount of

effort required:...........................................................................................................................8

d.ii) Depicting whether a company like Xinjiang should choose to remain unhedged:............8

Reference and Bibliography:....................................................................................................10

1

Table of Contents

a) Analysing the different alternatives:......................................................................................2

b) Justifying the recommendations:...........................................................................................4

c.i) Depicting the unrealised gain/loss faced by Xinjiang through the recommendations:........6

c.ii) Depicting the how the overall unrealised gain or loss happed in each period of

settlement:..................................................................................................................................7

d.i) Depicting whether managing the overall foreign exchange risk is worth the amount of

effort required:...........................................................................................................................8

d.ii) Depicting whether a company like Xinjiang should choose to remain unhedged:............8

Reference and Bibliography:....................................................................................................10

INTERNATIONAL FINANCE

2

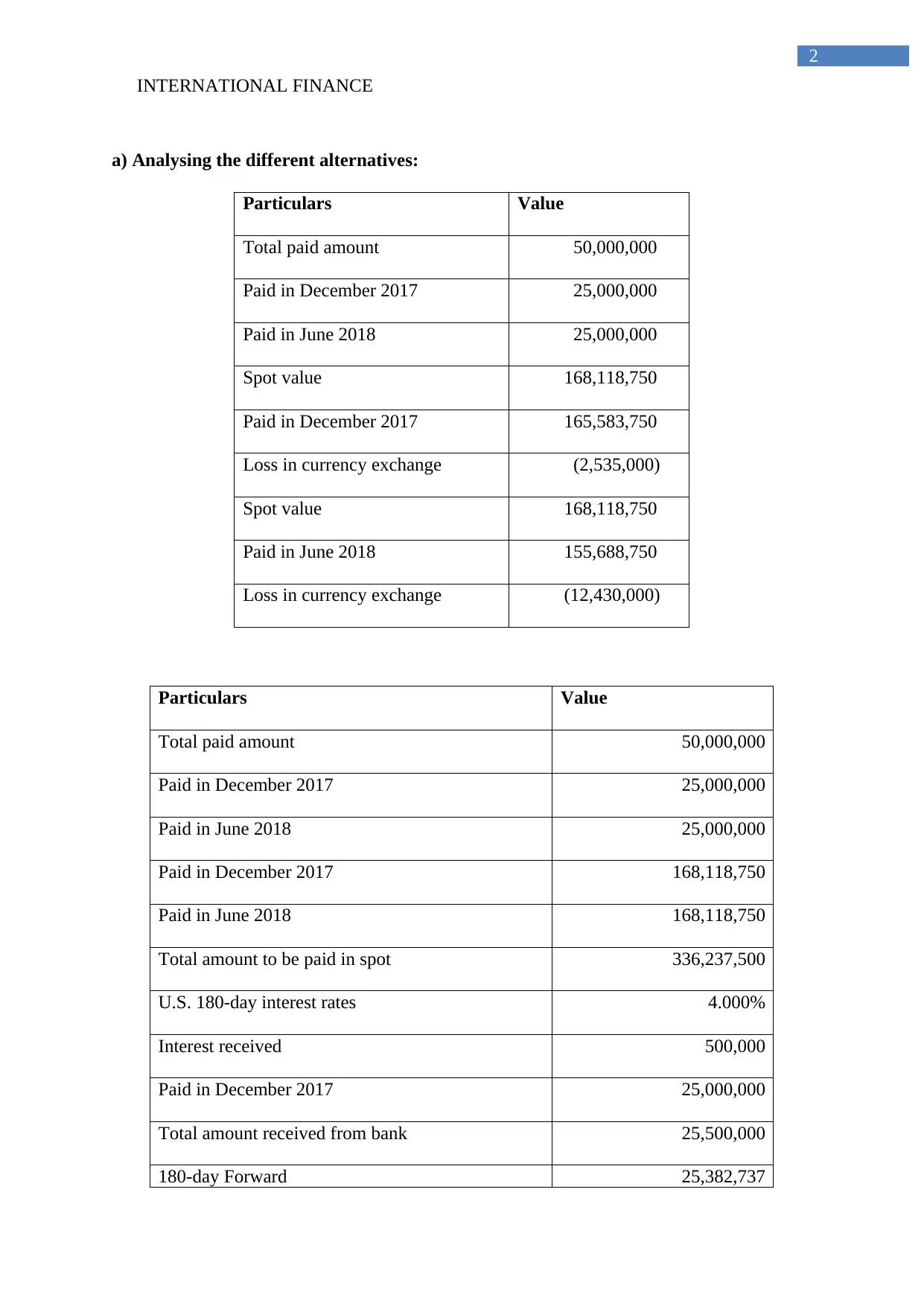

a) Analysing the different alternatives:

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Spot value 168,118,750

Paid in December 2017 165,583,750

Loss in currency exchange (2,535,000)

Spot value 168,118,750

Paid in June 2018 155,688,750

Loss in currency exchange (12,430,000)

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Paid in December 2017 168,118,750

Paid in June 2018 168,118,750

Total amount to be paid in spot 336,237,500

U.S. 180-day interest rates 4.000%

Interest received 500,000

Paid in December 2017 25,000,000

Total amount received from bank 25,500,000

180-day Forward 25,382,737

2

a) Analysing the different alternatives:

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Spot value 168,118,750

Paid in December 2017 165,583,750

Loss in currency exchange (2,535,000)

Spot value 168,118,750

Paid in June 2018 155,688,750

Loss in currency exchange (12,430,000)

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Paid in December 2017 168,118,750

Paid in June 2018 168,118,750

Total amount to be paid in spot 336,237,500

U.S. 180-day interest rates 4.000%

Interest received 500,000

Paid in December 2017 25,000,000

Total amount received from bank 25,500,000

180-day Forward 25,382,737

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

3

Profit from exchange of December 117,263

U.S. One year interest rates 4.255%

Interest received 1,063,750

Paid in June 2018 25,000,000

Total amount received from bank 26,063,750

360-day Forward 26,995,970

Loss from exchange of December (932,220)

Total loss from currency exchange (814,956)

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Spot Exchange rate 6.72475

180-day Put Option 6.650

premium 0.05

180-day Forward 6.623

Profit from risk exchange 0.05

Profit from risk exchange 1,285,000

Paid in December 2017 25,000,000

Payment 25,382,737

Profit from exchange 902,263

Spot Exchange rate 6.72475

3

Profit from exchange of December 117,263

U.S. One year interest rates 4.255%

Interest received 1,063,750

Paid in June 2018 25,000,000

Total amount received from bank 26,063,750

360-day Forward 26,995,970

Loss from exchange of December (932,220)

Total loss from currency exchange (814,956)

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Spot Exchange rate 6.72475

180-day Put Option 6.650

premium 0.05

180-day Forward 6.623

Profit from risk exchange 0.05

Profit from risk exchange 1,285,000

Paid in December 2017 25,000,000

Payment 25,382,737

Profit from exchange 902,263

Spot Exchange rate 6.72475

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

4

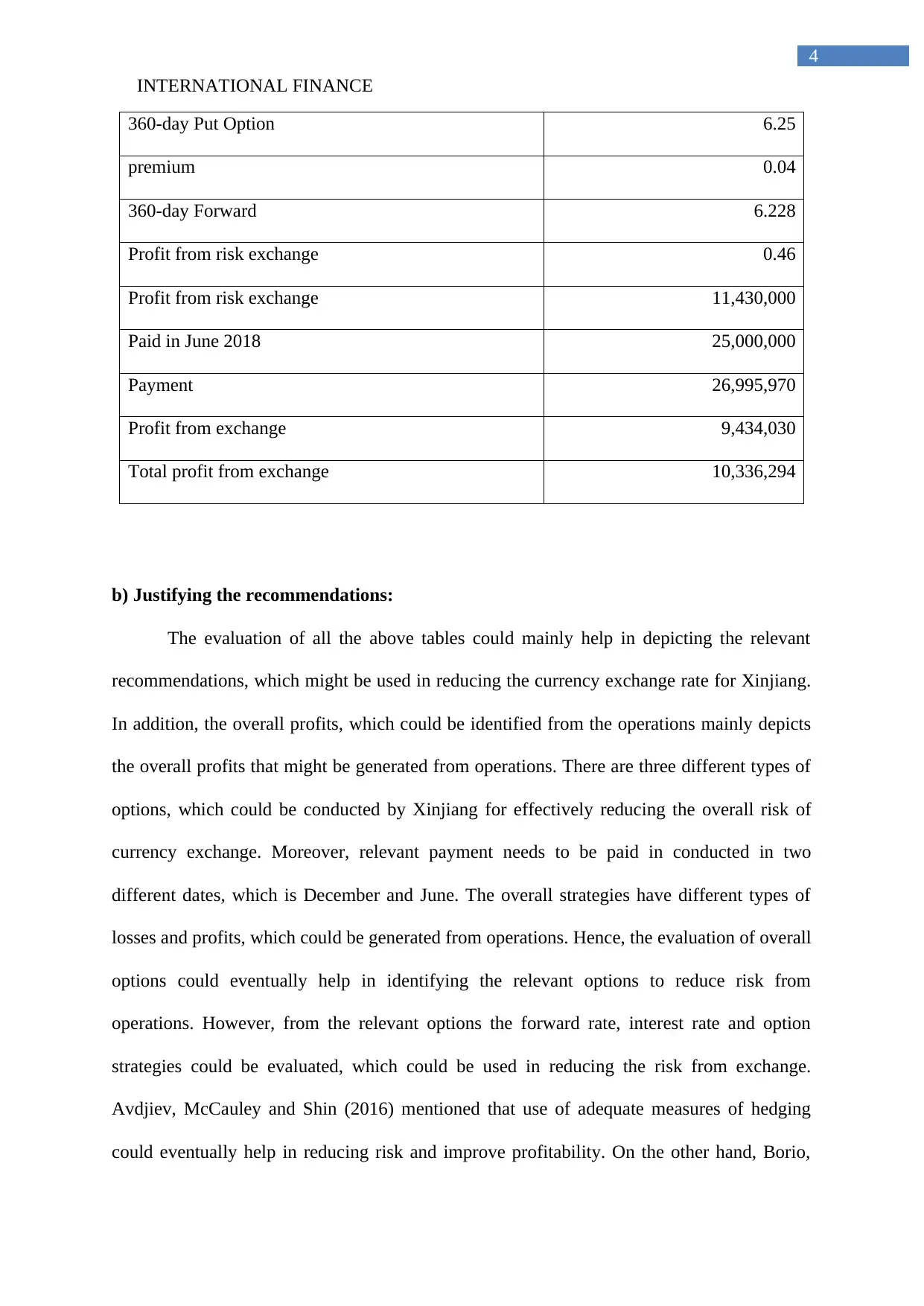

360-day Put Option 6.25

premium 0.04

360-day Forward 6.228

Profit from risk exchange 0.46

Profit from risk exchange 11,430,000

Paid in June 2018 25,000,000

Payment 26,995,970

Profit from exchange 9,434,030

Total profit from exchange 10,336,294

b) Justifying the recommendations:

The evaluation of all the above tables could mainly help in depicting the relevant

recommendations, which might be used in reducing the currency exchange rate for Xinjiang.

In addition, the overall profits, which could be identified from the operations mainly depicts

the overall profits that might be generated from operations. There are three different types of

options, which could be conducted by Xinjiang for effectively reducing the overall risk of

currency exchange. Moreover, relevant payment needs to be paid in conducted in two

different dates, which is December and June. The overall strategies have different types of

losses and profits, which could be generated from operations. Hence, the evaluation of overall

options could eventually help in identifying the relevant options to reduce risk from

operations. However, from the relevant options the forward rate, interest rate and option

strategies could be evaluated, which could be used in reducing the risk from exchange.

Avdjiev, McCauley and Shin (2016) mentioned that use of adequate measures of hedging

could eventually help in reducing risk and improve profitability. On the other hand, Borio,

4

360-day Put Option 6.25

premium 0.04

360-day Forward 6.228

Profit from risk exchange 0.46

Profit from risk exchange 11,430,000

Paid in June 2018 25,000,000

Payment 26,995,970

Profit from exchange 9,434,030

Total profit from exchange 10,336,294

b) Justifying the recommendations:

The evaluation of all the above tables could mainly help in depicting the relevant

recommendations, which might be used in reducing the currency exchange rate for Xinjiang.

In addition, the overall profits, which could be identified from the operations mainly depicts

the overall profits that might be generated from operations. There are three different types of

options, which could be conducted by Xinjiang for effectively reducing the overall risk of

currency exchange. Moreover, relevant payment needs to be paid in conducted in two

different dates, which is December and June. The overall strategies have different types of

losses and profits, which could be generated from operations. Hence, the evaluation of overall

options could eventually help in identifying the relevant options to reduce risk from

operations. However, from the relevant options the forward rate, interest rate and option

strategies could be evaluated, which could be used in reducing the risk from exchange.

Avdjiev, McCauley and Shin (2016) mentioned that use of adequate measures of hedging

could eventually help in reducing risk and improve profitability. On the other hand, Borio,

INTERNATIONAL FINANCE

5

Gambacorta and Hofmann (2017) criticises that hedging could increase risk, when investors

are not able to comprehend risk affecting operations.

In addition, the overall valuation and calculation mainly help in identifying the most

viable investment options, which could be adopted by Xinjiang for reducing the risk of

payments. Hence, the use of forward rate hedging process has mainly portrayed a relevant

loss for Xinjiang, as it might not be able to reduce the risk from currency expense if payment

is conducted on December and June. This relevant forward rate exchange methods could fix

currency value for Xinjiang. Moreover, use of forward rate might increase ht overall loss

from operations, as Xinjiang will need to pay $2,378,706 extra for purchases that is

conducted for rail cars. This relevant use of forward rate could eventually fix the overall

payments that will be conducted for the contract. Borst and Lardy (2015) mentioned that

forward rate mainly focus the overall payments, where any benefits or loss opted from the

currency exchange will mainly be avoided.

Moreover, the use of exchange currency by utilising the swap method could mainly

provide relevant loss due to increased risk from operations. The total increased USD value

that will be paid by implementing the swap strategy is $814,956. This hedging strategy will

not able to provide relevant coverage and only reduce the profits generated from currency

exchange. Chinn and Kucko (2015) stated that, the use of swap strategy could only help in

reducing risk and compensating for the loss until it comes under the interest that is provided

by the bank any increment in loss excess of the overall interest paid by the banks will directly

increase risk of the currency exchange. This could mainly been seen on 180 day interest rate

and 360 day interest rate, where the 180 day interest payment directly compensate the

calculation in currency value. However, the 360 day interests were not able to compensate

with the relevant change in currency calculations where relevant loss from operations could

be identified.

5

Gambacorta and Hofmann (2017) criticises that hedging could increase risk, when investors

are not able to comprehend risk affecting operations.

In addition, the overall valuation and calculation mainly help in identifying the most

viable investment options, which could be adopted by Xinjiang for reducing the risk of

payments. Hence, the use of forward rate hedging process has mainly portrayed a relevant

loss for Xinjiang, as it might not be able to reduce the risk from currency expense if payment

is conducted on December and June. This relevant forward rate exchange methods could fix

currency value for Xinjiang. Moreover, use of forward rate might increase ht overall loss

from operations, as Xinjiang will need to pay $2,378,706 extra for purchases that is

conducted for rail cars. This relevant use of forward rate could eventually fix the overall

payments that will be conducted for the contract. Borst and Lardy (2015) mentioned that

forward rate mainly focus the overall payments, where any benefits or loss opted from the

currency exchange will mainly be avoided.

Moreover, the use of exchange currency by utilising the swap method could mainly

provide relevant loss due to increased risk from operations. The total increased USD value

that will be paid by implementing the swap strategy is $814,956. This hedging strategy will

not able to provide relevant coverage and only reduce the profits generated from currency

exchange. Chinn and Kucko (2015) stated that, the use of swap strategy could only help in

reducing risk and compensating for the loss until it comes under the interest that is provided

by the bank any increment in loss excess of the overall interest paid by the banks will directly

increase risk of the currency exchange. This could mainly been seen on 180 day interest rate

and 360 day interest rate, where the 180 day interest payment directly compensate the

calculation in currency value. However, the 360 day interests were not able to compensate

with the relevant change in currency calculations where relevant loss from operations could

be identified.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

6

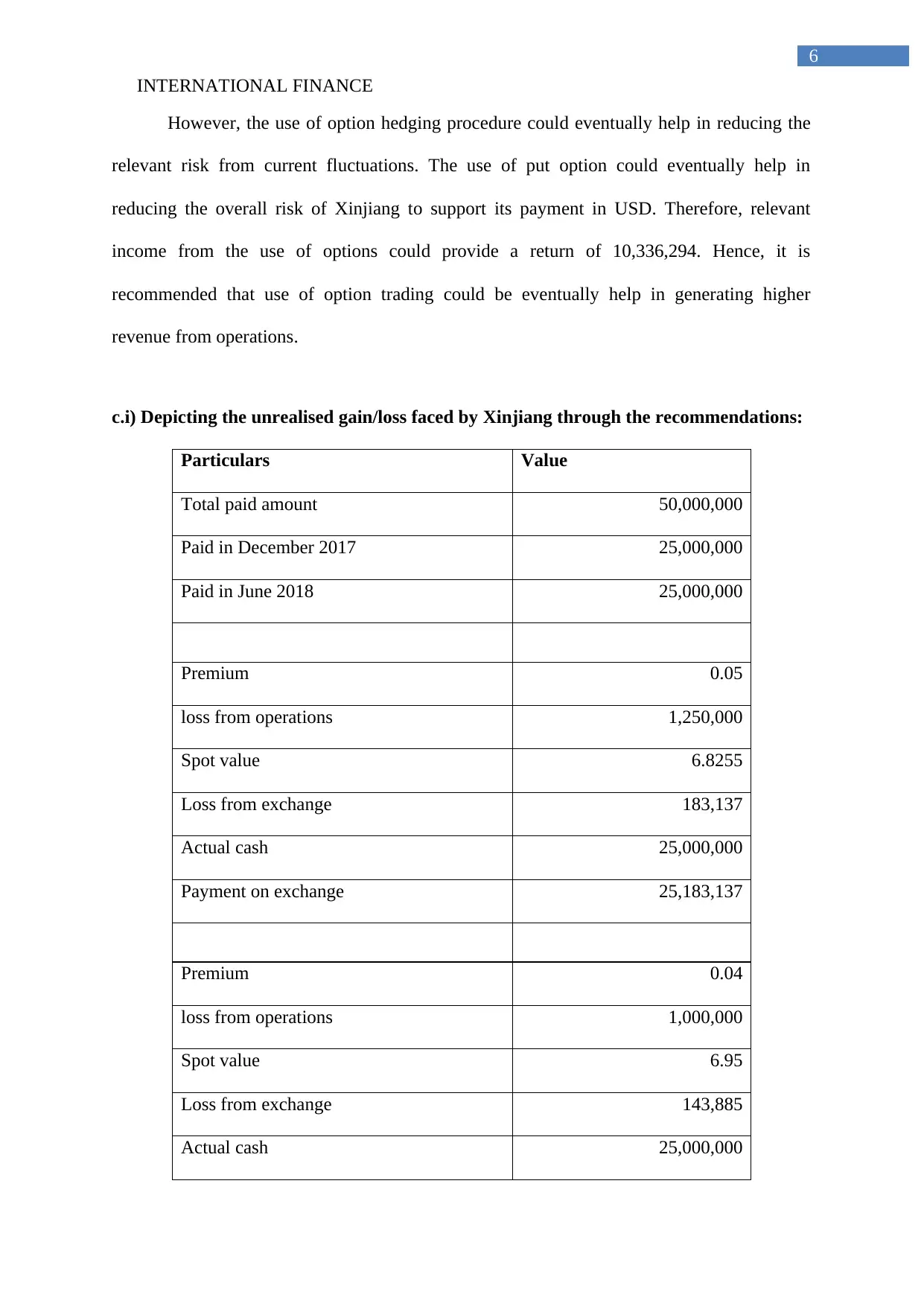

However, the use of option hedging procedure could eventually help in reducing the

relevant risk from current fluctuations. The use of put option could eventually help in

reducing the overall risk of Xinjiang to support its payment in USD. Therefore, relevant

income from the use of options could provide a return of 10,336,294. Hence, it is

recommended that use of option trading could be eventually help in generating higher

revenue from operations.

c.i) Depicting the unrealised gain/loss faced by Xinjiang through the recommendations:

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Premium 0.05

loss from operations 1,250,000

Spot value 6.8255

Loss from exchange 183,137

Actual cash 25,000,000

Payment on exchange 25,183,137

Premium 0.04

loss from operations 1,000,000

Spot value 6.95

Loss from exchange 143,885

Actual cash 25,000,000

6

However, the use of option hedging procedure could eventually help in reducing the

relevant risk from current fluctuations. The use of put option could eventually help in

reducing the overall risk of Xinjiang to support its payment in USD. Therefore, relevant

income from the use of options could provide a return of 10,336,294. Hence, it is

recommended that use of option trading could be eventually help in generating higher

revenue from operations.

c.i) Depicting the unrealised gain/loss faced by Xinjiang through the recommendations:

Particulars Value

Total paid amount 50,000,000

Paid in December 2017 25,000,000

Paid in June 2018 25,000,000

Premium 0.05

loss from operations 1,250,000

Spot value 6.8255

Loss from exchange 183,137

Actual cash 25,000,000

Payment on exchange 25,183,137

Premium 0.04

loss from operations 1,000,000

Spot value 6.95

Loss from exchange 143,885

Actual cash 25,000,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

7

Payment on exchange 25,143,885

Total payment 50,327,022

Actual intended payment 50,000,000

Extra premium payment (loss in USD) 327,022

c.ii) Depicting the how the overall unrealised gain or loss happed in each period of

settlement:

The relevant unrealised loss was mainly due to the increment in value of USD, which

relevant nullified the overall profit generated from put option. This put option was mainly

conducted due to the relevant payment system that was needed by Xinjiang. The overall

increment in value of USD was mainly the reasons where the company was fully hedged in

its payment. However, the only increment in loss was due to the premium, which was needed

to be paid by Xinjiang. Nevertheless, the unrealised loss was mainly due to the premium

payment that needs to be paid by Xinjiang, as it helps in reducing the overall risk from

investment.

The overall USD payment is mainly conducted for the rail products, which mainly

amount of 50 million. However, the overall payment needs to be hedged, as the payment is

conducted on USD, where the exchange rate could change with time. Moreover, the overall

premium payment is mainly conducted to hedge the currency exposure of Xinjiang. Frieden

(2015) stated that with the use of option pricing companies are mainly able to hedge their

currency exposure, while investing the least amount of money from their operations.

7

Payment on exchange 25,143,885

Total payment 50,327,022

Actual intended payment 50,000,000

Extra premium payment (loss in USD) 327,022

c.ii) Depicting the how the overall unrealised gain or loss happed in each period of

settlement:

The relevant unrealised loss was mainly due to the increment in value of USD, which

relevant nullified the overall profit generated from put option. This put option was mainly

conducted due to the relevant payment system that was needed by Xinjiang. The overall

increment in value of USD was mainly the reasons where the company was fully hedged in

its payment. However, the only increment in loss was due to the premium, which was needed

to be paid by Xinjiang. Nevertheless, the unrealised loss was mainly due to the premium

payment that needs to be paid by Xinjiang, as it helps in reducing the overall risk from

investment.

The overall USD payment is mainly conducted for the rail products, which mainly

amount of 50 million. However, the overall payment needs to be hedged, as the payment is

conducted on USD, where the exchange rate could change with time. Moreover, the overall

premium payment is mainly conducted to hedge the currency exposure of Xinjiang. Frieden

(2015) stated that with the use of option pricing companies are mainly able to hedge their

currency exposure, while investing the least amount of money from their operations.

INTERNATIONAL FINANCE

8

d.i) Depicting whether managing the overall foreign exchange risk is worth the amount

of effort required:

The relevant statement, whether management of overall exchange risk is worth the

effort is relevantly true, as with the hedging process loss generated by the company could be

reduced. The overall foreign currency hedging mainly allows the organisation to adequately

reduce the loss from transaction, if pricing of the currency fluctuates to undesirable levels.

The relevant hedging of the foreign exchange currency could mainly reduce the overall

excess damage, which might be conducted by the fluctuation on the exchange currency. The

overall foreign exchange risk could mainly be reduced with the help of hedging process, as

companies make decision on specific day, where currency rate is determined. This overall

hedging process mainly reduces the overall estimated of loss, which might be conducted due

the fluctuations in currency deviation from the actual estimated price. The companies while

making relevant decisions on the currency exchange could mainly help in reducing losses

from operations (Frisari and Stadelmann 2015).

The overall transaction that needs to be conducted by the company could mainly be

reduced with the help of hedging strategy, as it might fix the currency exchange value,

whereas fixing the overall cost of the product. Without the hedging procedure the companies

are not able to reduce risk from currency exchange, as the cost of the project might increase,

while invalidating the project. The relevant hedging method could eventually allow the

company to fix the actual cost of expenses conducted for the operations (Giordano, Pericoli

and Tommasino 2013).

d.ii) Depicting whether a company like Xinjiang should choose to remain unhedged:

From the overall valuation of the current position of Xinjiang it could be identified

that the company directly conducts purchases in USD, which might increase currency

8

d.i) Depicting whether managing the overall foreign exchange risk is worth the amount

of effort required:

The relevant statement, whether management of overall exchange risk is worth the

effort is relevantly true, as with the hedging process loss generated by the company could be

reduced. The overall foreign currency hedging mainly allows the organisation to adequately

reduce the loss from transaction, if pricing of the currency fluctuates to undesirable levels.

The relevant hedging of the foreign exchange currency could mainly reduce the overall

excess damage, which might be conducted by the fluctuation on the exchange currency. The

overall foreign exchange risk could mainly be reduced with the help of hedging process, as

companies make decision on specific day, where currency rate is determined. This overall

hedging process mainly reduces the overall estimated of loss, which might be conducted due

the fluctuations in currency deviation from the actual estimated price. The companies while

making relevant decisions on the currency exchange could mainly help in reducing losses

from operations (Frisari and Stadelmann 2015).

The overall transaction that needs to be conducted by the company could mainly be

reduced with the help of hedging strategy, as it might fix the currency exchange value,

whereas fixing the overall cost of the product. Without the hedging procedure the companies

are not able to reduce risk from currency exchange, as the cost of the project might increase,

while invalidating the project. The relevant hedging method could eventually allow the

company to fix the actual cost of expenses conducted for the operations (Giordano, Pericoli

and Tommasino 2013).

d.ii) Depicting whether a company like Xinjiang should choose to remain unhedged:

From the overall valuation of the current position of Xinjiang it could be identified

that the company directly conducts purchases in USD, which might increase currency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE

9

conversion risk. In addition, the overall conversion risk could mainly help in reducing the

overall profitability that might be generated from operations. The company directly purchase

equipment of higher value like 50 million in a particular year. This payments is mainly

conducted in USD, while the company is situated in China. Therefore, the conversion of the

Chinese currency into USD is the main operation, which might increase losses for the

organisation. Hence, the use of hedging process could eventually help in reducing the overall

conversion risk that is haunting operations of the company. The no hedging policy might

directly hamper operational capability of the organisation. In addition, from the overall

evaluation of the case study weakness in USD can be identified, which is hampering the

conversion rate of Xinjian. Therefore, if the company does not hedge its foreign currency

exposure then the company will face higher cost for its products, which could be seen in the

above calculations. However, the change in value of USD was relatively declines in

comparison to the Chinese currency, which directly reflects the use of hedging procedure that

needs to be conducted by Xinjian. Moffett, Stonehill and Eiteman (2017) mentioned that use

of adequate hedging process allows the organisation to reduce loses, which might be

conducted from currency conversion.

9

conversion risk. In addition, the overall conversion risk could mainly help in reducing the

overall profitability that might be generated from operations. The company directly purchase

equipment of higher value like 50 million in a particular year. This payments is mainly

conducted in USD, while the company is situated in China. Therefore, the conversion of the

Chinese currency into USD is the main operation, which might increase losses for the

organisation. Hence, the use of hedging process could eventually help in reducing the overall

conversion risk that is haunting operations of the company. The no hedging policy might

directly hamper operational capability of the organisation. In addition, from the overall

evaluation of the case study weakness in USD can be identified, which is hampering the

conversion rate of Xinjian. Therefore, if the company does not hedge its foreign currency

exposure then the company will face higher cost for its products, which could be seen in the

above calculations. However, the change in value of USD was relatively declines in

comparison to the Chinese currency, which directly reflects the use of hedging procedure that

needs to be conducted by Xinjian. Moffett, Stonehill and Eiteman (2017) mentioned that use

of adequate hedging process allows the organisation to reduce loses, which might be

conducted from currency conversion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE

10

Reference and Bibliography:

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), pp.409-451.

Borio, C., Gambacorta, L. and Hofmann, B., 2017. The influence of monetary policy on bank

profitability. International Finance, 20(1), pp.48-63.

Borst, N. and Lardy, N., 2015. Maintaining Financial Stability in the People’s Republic of

China during Financial Liberalization. Peterson Institute of International Finance. WP 15-4

March 2015.

Chinn, M. and Kucko, K., 2015. The predictive power of the yield curve across countries and

time. International Finance, 18(2), pp.129-156.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Frieden, J., 2016. The governance of international finance. Annual Review of Political

Science, 19.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82, pp.12-

22.

Giordano, R., Pericoli, M. and Tommasino, P., 2013. Pure or Wake‐up‐Call Contagion?

Another Look at the EMU Sovereign Debt Crisis. International Finance, 16(2), pp.131-160.

Gomes, S., Jacquinot, P., Mohr, M. and Pisani, M., 2013. Structural reforms and

macroeconomic performance in the Euro Area countries: a model‐based

assessment. International Finance, 16(1), pp.23-44.

10

Reference and Bibliography:

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple coincidence in

international finance. Economic Policy, 31(87), pp.409-451.

Borio, C., Gambacorta, L. and Hofmann, B., 2017. The influence of monetary policy on bank

profitability. International Finance, 20(1), pp.48-63.

Borst, N. and Lardy, N., 2015. Maintaining Financial Stability in the People’s Republic of

China during Financial Liberalization. Peterson Institute of International Finance. WP 15-4

March 2015.

Chinn, M. and Kucko, K., 2015. The predictive power of the yield curve across countries and

time. International Finance, 18(2), pp.129-156.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Frieden, J., 2016. The governance of international finance. Annual Review of Political

Science, 19.

Frisari, G. and Stadelmann, M., 2015. De-risking concentrated solar power in emerging

markets: The role of policies and international finance institutions. Energy Policy, 82, pp.12-

22.

Giordano, R., Pericoli, M. and Tommasino, P., 2013. Pure or Wake‐up‐Call Contagion?

Another Look at the EMU Sovereign Debt Crisis. International Finance, 16(2), pp.131-160.

Gomes, S., Jacquinot, P., Mohr, M. and Pisani, M., 2013. Structural reforms and

macroeconomic performance in the Euro Area countries: a model‐based

assessment. International Finance, 16(1), pp.23-44.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.